Breast Shells Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

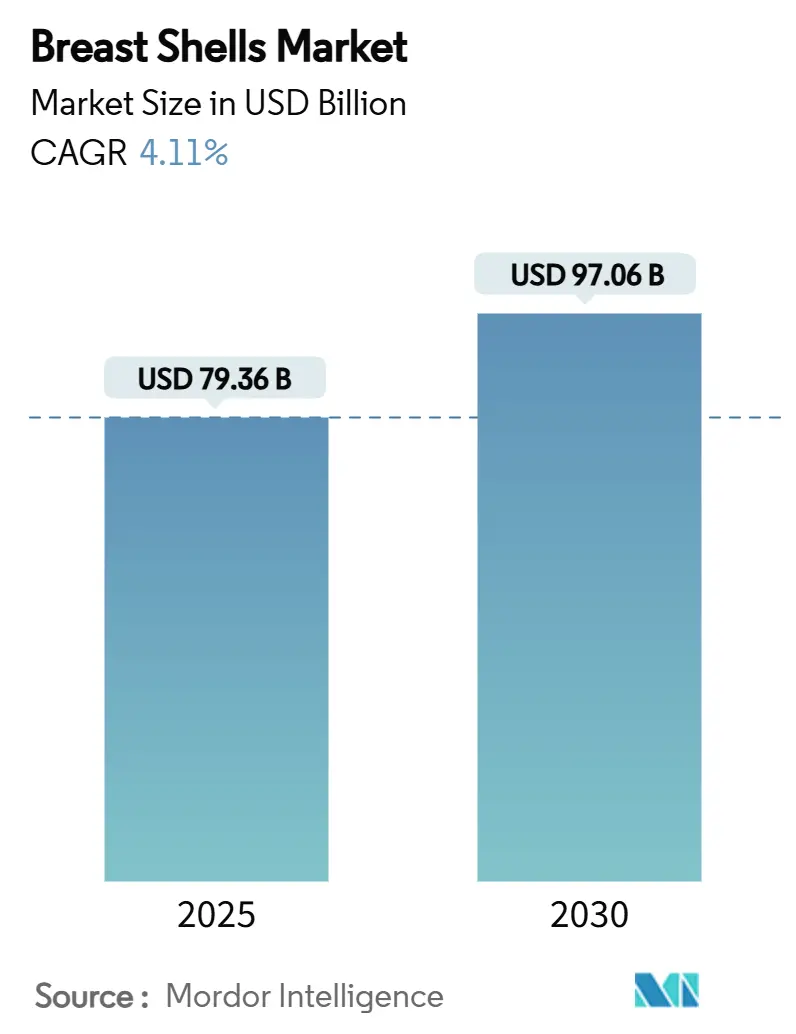

| Market Size (2025) | USD 79.36 Billion |

| Market Size (2030) | USD 97.06 Billion |

| Growth Rate (2025 - 2030) | 4.11% CAGR |

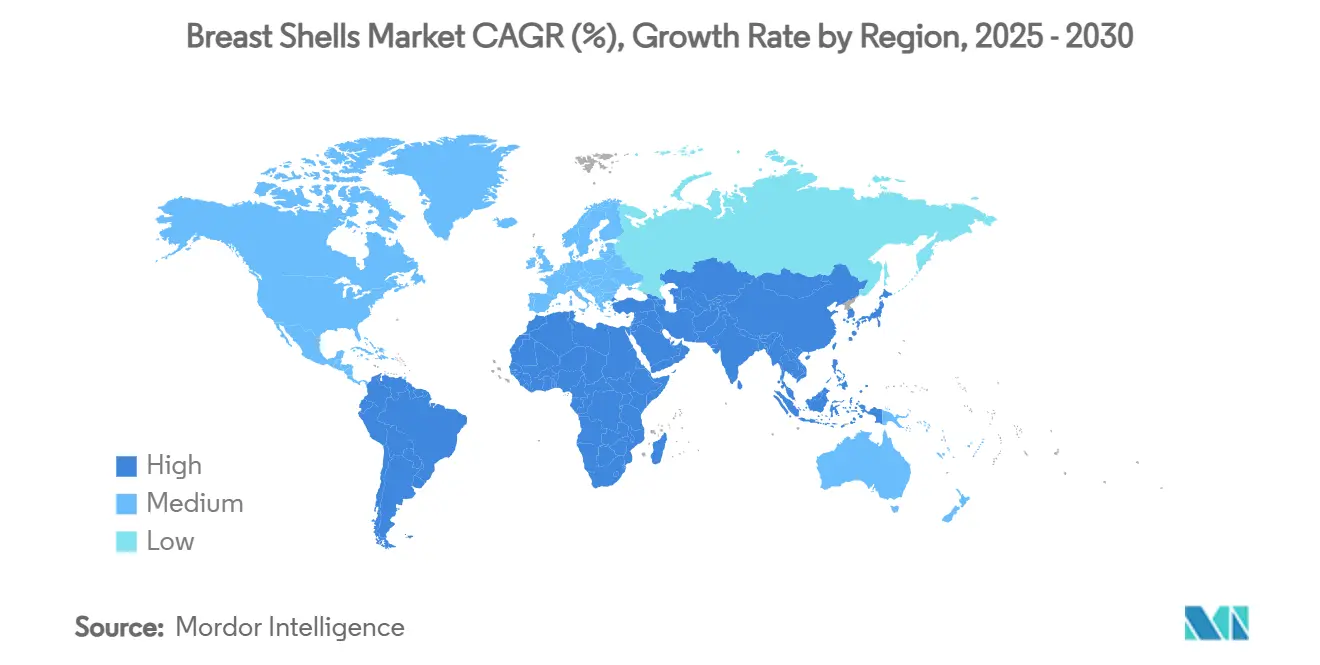

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

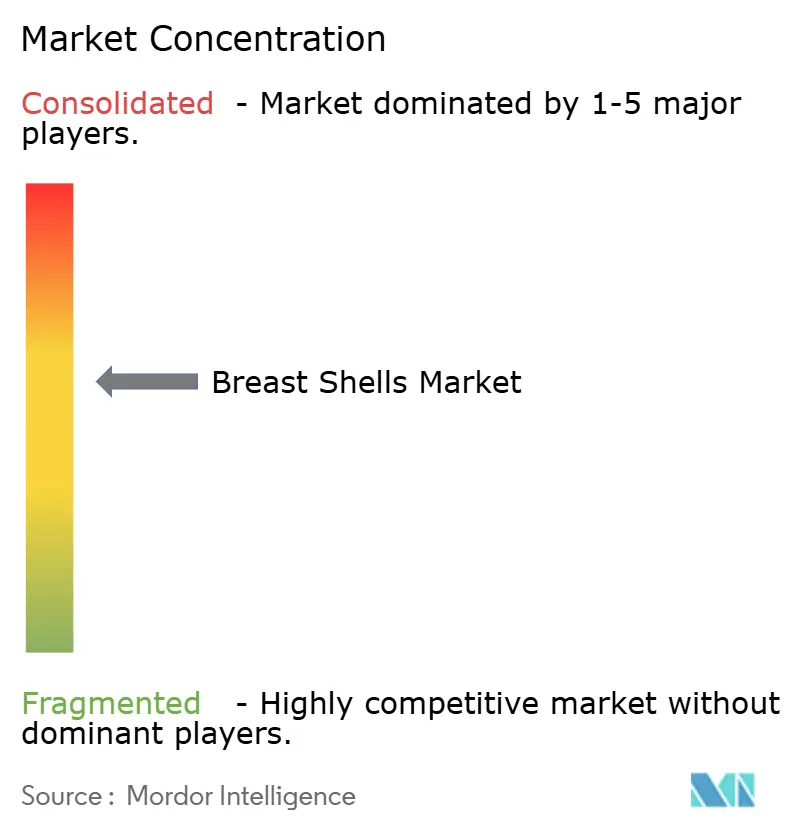

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Breast Shells Market Analysis by Mordor Intelligence

The breast shells market size reached USD 79.36 billion in 2025 and is expected to rise to USD 97.061 billion by 2030, reflecting a 4.11% CAGR and underscoring steady uptake of technologically refined lactation accessories across major economies. Robust advocacy for breastfeeding, the roll-out of reimbursement mandates in the United States and parts of Europe, and rapid digital commerce adoption create a supportive demand climate. Manufacturers are differentiating through vented designs with airflow lattice patterns, medical-grade silicone construction, and Internet-of-Things (IoT) features that track leakage or milk volume, thereby commanding premium pricing in hospital and consumer channels. Growth opportunities are concentrated in Asia-Pacific where urban middle-income households and government breastfeeding campaigns converge, while North America anchors value through insurance coverage and high brand loyalty. Competitive pressure now centres on sustainability; firms are substituting bio-based silicones and recycled resins to comply with tightening polymer regulations in Europe and North America.

Key Report Takeaways

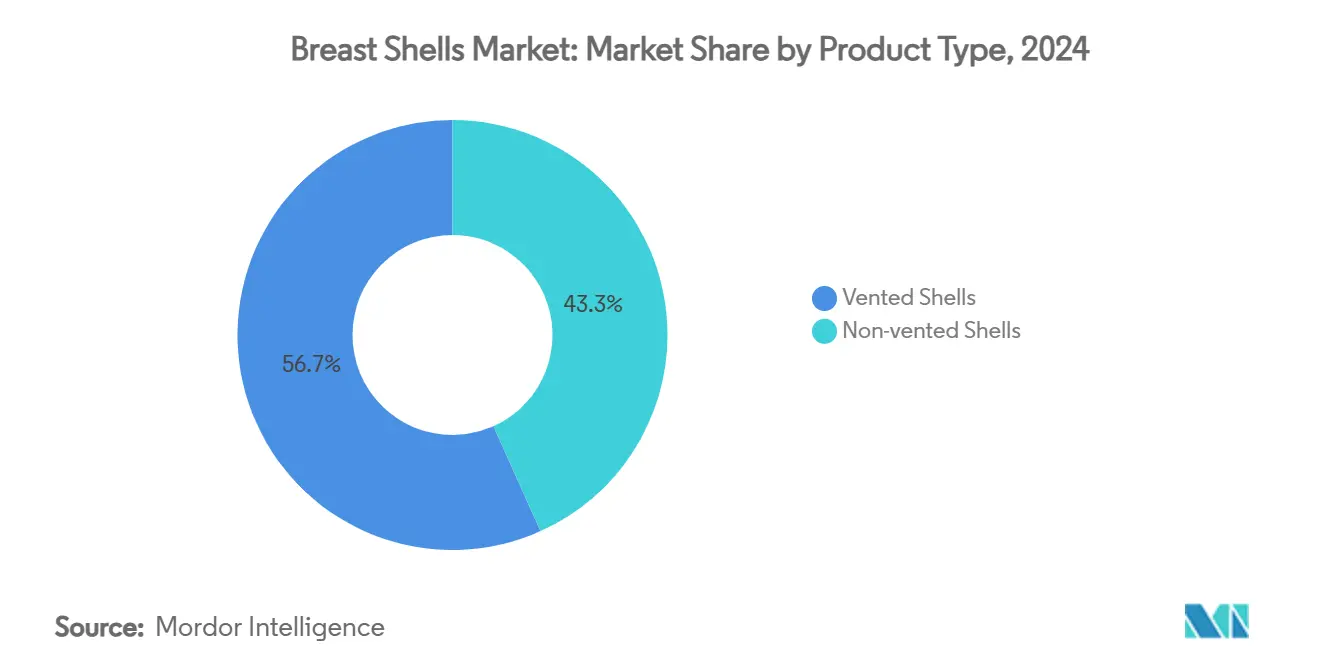

- By product type, vented shells captured 56.72% revenue share in 2024 and are projected to post a 7.34% CAGR through 2030.

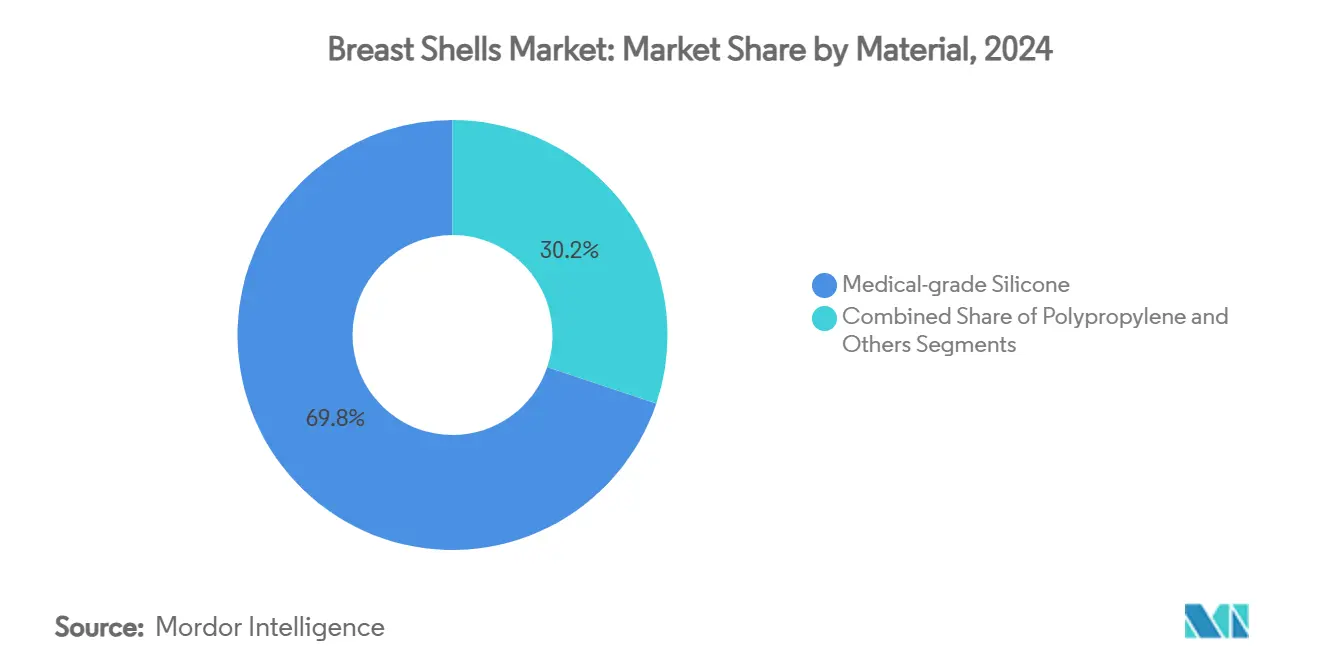

- By material, medical-grade silicone held 69.83% share in 2024, while bio-based silicone is forecast to expand at a 6.83% CAGR to 2030.

- By distribution channel, online retail accounted for 41.44% of revenue in 2024 and is set to rise at an 8.67% CAGR through 2030.

- By geography, North America led with 37.48% market value in 2024, whereas Asia-Pacific is expected to record a 6.59% CAGR between 2025 and 2030.

Global Breast Shells Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Global Breastfeeding-Support Initiatives | +0.8% | Global, with stronger impact in APAC and Europe | Medium term (2-4 years) |

| Reimbursement For Lactation Accessories In Key Markets | +0.6% | North America & EU primarily | Short term (≤ 2 years) |

| E-Commerce Proliferation In Maternal-Care Products | +1.2% | Global, with highest impact in Asia-Pacific | Short term (≤ 2 years) |

| Product Upgrades (Vented, Ergonomic Silicone Designs) | +0.9% | Global, led by North America and Europe | Medium term (2-4 years) |

| Demand From NICU & Premature-Birth Management | +0.5% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Integration Of Wearable IoT Sensors For Leakage Detection | +0.7% | North America & EU early adoption, APAC following | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Global Breastfeeding-Support Initiatives

World Health Organization scorecards show exclusive breastfeeding rates climbing to 48% in 2023, a 10-point gain over 12 years.[1]World Health Organization, “Implementation of the Baby-Friendly Hospital Initiative,” who.int Governments respond by embedding lactation guidance and accessory reimbursement into public-health protocols, prompting hospitals to purchase breast shells as part of discharge kits. The Baby-Friendly Hospital Initiative now spans 152 countries and requires 75% exclusive breastfeeding at discharge, reinforcing institutional demand. China’s policy package that extends maternity leave and mandates public nursing spaces amplifies retail pull for premium accessories.[2]Li Junying et al., “Investigation of Maternal Breastfeeding Guarantee Policy Needs,” frontiersin.orgCollectively, these measures lock in predictable volume offtake and encourage manufacturers to align capacity planning with public-sector tenders.

Reimbursement for Lactation Accessories in Key Markets

The Affordable Care Act obliges private insurers in the United States to cover breast pumps and related accessories, a policy mirrored in parts of the European Union. Reimbursement removes price barriers for mothers, lifts unit sales in hospital channels, and encourages the purchase of higher-margin, clinically validated shells. Insurers increasingly require proof of efficacy, motivating firms to conduct trials that bolster product claims. Faster reimbursement approvals in Germany and France widened the hospital procurement pipeline in 2025, helping premium shells outpace entry-level substitutes in these markets.

E-Commerce Proliferation in Maternal-Care Products

Online retail captured 41.44% share in 2024 and is rising at an 8.67% CAGR as privacy, next-day delivery, and peer reviews sway consumer journeys. Brands exploit direct-to-consumer storefronts to bypass retailer mark-ups while offering size-guidance videos and live lactation chat support. Pandemic-era digital habits persisted through 2025, with Asia-Pacific displaying the steepest acceleration as smartphone penetration exceeds 80% in urban China and India. Integrated tele-lactation consults enhance platform stickiness, driving repeat purchases of replacement shell inserts and ancillary creams.

Product Upgrades in Vented Ergonomic Silicone Designs

Vented shells with 105° flange angles, exemplified by Medela’s PersonalFit Flex, lift expressed milk volume by 11% and drainage efficiency by 4% in clinical settings.[3]Medela, “Flex Technology – A Whole New Pumping Experience,” medela.com Airflow lattice structures reduce moisture build-up, cutting dermatitis incidence among nursing mothers and extending daily wear time. These performance gains justify price premiums of 18-22% versus non-vented counterparts in hospital tenders. Bio-based silicone grades growing at 6.83% CAGR support sustainability targets without compromising sterilisability.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Clinical Evidence On Long-Term Efficacy | -0.3% | Global, particularly in evidence-based healthcare systems | Medium term (2-4 years) |

| Counterfeits & Low-Cost Substitutes In Emerging Asia | -0.5% | Asia-Pacific primarily, with spillover effects | Short term (≤ 2 years) |

| Regulatory Ambiguity Around "Medical-Device" Labeling | -0.4% | Global, with varying regional interpretations | Long term (≥ 4 years) |

| Sustainability Backlash Versus Single-Use Polymer Shells | -0.6% | Europe & North America leading, global following | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Clinical Evidence on Long-Term Efficacy

Randomised trials attest to short-term comfort benefits, yet few longitudinal studies track outcomes beyond six months. Evidence gaps make some paediatric clinicians reluctant to prescribe premium shells and dampen insurance coverage in markets such as the United Kingdom. The United States Food and Drug Administration is ratcheting up scrutiny of efficacy claims, obliging manufacturers to fund multi-year studies that may delay new launches. This evidence deficit trims addressable demand in cautious healthcare systems that tie procurement to peer-reviewed data.

Counterfeits and Low-Cost Substitutes in Emerging Asia

U.S. Customs reports that 31% of seized counterfeit personal-care items in 2023 originated from Asia, eroding brand equity and posing hygiene risks. E-commerce giants struggle to police third-party sellers, allowing look-alike shells to undercut genuine products by up to 60% in Indonesia and Vietnam. Brand owners now spend an estimated 4% of revenue on anti-counterfeiting measures, squeezing margins and diverting funds from R&D.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Vented Shells Drive Innovation

The segment commanded 56.72% of the breast shells market share in 2024 and is projected to grow at 7.34% CAGR to 2030. Vented architecture with airflow lattices mitigates skin maceration and improves milk drainage, enabling longer daily wear and reinforcing nursing confidence. Clinical testing by Medela confirmed 11% higher expressed volume when mothers used a 105° flange angle, reinforcing performance-based differentiation. Non-vented designs still appeal in cost-sensitive contexts and emergency kits where simplicity outweighs technology. Future growth pivots on embedding IoT sensors; early adopter pilots in California maternity wards show a 15% uptick in refill purchases when leak-alert features are enabled. Manufacturers explore 3D-printing for personalised fit, signalling a shift toward mass customisation.

Second-generation vented shells integrate soft-touch bio-silicone, achieving comparable durability while lowering carbon footprints by 25% according to internal life-cycle assessments. Hospital procurement managers in France have begun adding sustainability points to tender scoring, favouring suppliers that document cradle-to-grave impacts. The convergence of clinical validation, comfort gains, and eco-design underpins a multi-year replacement wave that expands the breast shells market.

By Material: Medical-Grade Silicone Dominance

Medical-grade silicone held 69.83% share of the breast shells market size in 2024, reflecting superior biocompatibility and sterilisability. Its hypoallergenic profile safeguards mothers with postoperative sensitivity, and resistance to bacterial colonisation suits prolonged use in humid climates. Artsana’s 2024 sustainability report shows recycled silicone adoption without compromising ISO 10993 biocompatibility thresholds, supporting circular economy objectives. Polypropylene retains footholds in low-income settings and public tenders where acquisition cost trumps longevity.

Bio-based silicone is the fastest-growing sub-segment at 6.83% CAGR through 2030. Breakthrough polymer chains derived from sugarcane feedstocks reduce fossil-based inputs by 45% and satisfy European EcoDesign directives. Medela piloted such materials in its Contact Nipple Shield, recording no adverse reactions during a 12-week post-launch surveillance window. Momentum is likely to accelerate once mass-balance certification lowers unit cost premiums, expanding uptake across upper-mid-price shells.

By Distribution Channel: Online Retail Transformation

Online retail accounted for 41.44% of market revenue in 2024 and is advancing at an 8.67% CAGR as millennial and Gen-Z parents embrace digital convenience. Leading brands deploy AI chatbots that provide fitting tips, while subscription models automate replenishment of replacement valves and storage bags, increasing lifetime customer value. Hospital and pharmacy retail maintains relevance for first-use education but faces declining margins as insurers reimburse direct-to-consumer purchases through Health Savings Accounts in the United States.

Specialty baby stores differentiate through lactation consultants and immediate product trials, sustaining mid-single-digit growth. Supermarkets and hypermarkets remain outlets for entry-level shells, yet premium offerings increasingly appear as click-and-collect SKUs linked to e-commerce platforms. Willow’s acquisition of Elvie illustrates a playbook that aligns connected hardware, mobile apps, and proprietary storefronts to orchestrate end-to-end maternal-care ecosystems.

Geography Analysis

North America led the breast shells market with 37.48% value share in 2024 on the back of Affordable Care Act provisions that mandate breast pump coverage and indirectly boost accessory demand. Reimbursement removes cost sensitivity, letting hospitals specify premium, clinically validated shells. Paid family-leave policies correlate with 5.36% higher exclusive breastfeeding rates, extending average shell usage duration. Canada’s single-payer system added breast shells to postpartum care kits in several provinces during 2025, further reinforcing regional dominance.

Asia-Pacific is the fastest-growing geography at a 6.59% CAGR to 2030. China’s breastfeeding guarantee framework, combined with rapid e-commerce expansion, fuels premium shell uptake among urban middle-class mothers. Japan’s ageing society surprisingly lifts per-capita expenditure as older mothers invest in high-end accessories to support later-life pregnancies. India’s urban hospitals increasingly bundle shells with pumps to comply with updated accreditation standards, catalysing demand in tier-one cities.

Europe remains a mature yet innovative market where sustainability expectations steer purchasing patterns. The European Commission’s plastics strategy pushes hospitals to adopt reusable or bio-based shells, spurring material innovation. Meanwhile, Middle East and Africa and South America present emerging opportunities; rising urbanisation and private healthcare investment in the Gulf Cooperation Council states and Brazil create pockets of premium demand, although overall uptake is limited by uneven insurance coverage and lower disposable incomes.

Competitive Landscape

The breast shells market shows moderate fragmentation with a tier of global leaders—Medela, Philips, and Lansinoh. Companies differentiate via clinical validation, ergonomic design, and integration into broader maternal-health ecosystems rather than price competition. Medela retained the #1 most trusted breast-pump brand ranking in the United States, Canada, and the United Kingdom in 2025, reinforcing premium positioning. Philips leverages cross-portfolio synergies with its Avent range and hospital relationships, while Lansinoh protects market space through a growing patent estate on electric pump and vibratory waveform technologies.

Strategic consolidation is underway. Willow’s April 2025 acquisition of Elvie created a vertically integrated platform spanning wearable pumps, mobile apps, and telemetry-enabled shells. Material science collaborations also intensify; Solvay’s alliance with Hegen delivered the first recycled-content baby bottle, indicating potential spill-over to shell components. Emerging entrants focus on IoT analytics and customised fit via 3D-printing, yet face barriers posed by regulatory clearance and reimbursement evidence.

Sustainability and regulatory compliance represent shared challenges. European market access now requires lifecycle transparency, prompting investments in bio-based silicone and recyclable packaging. At the same time, U.S. and Japanese regulators expand post-market surveillance for device-embedded sensors, requiring cybersecurity safeguards that raise development costs but offer differentiation to compliant innovators.

Breast Shells Industry Leaders

Medela AG

Koninklijke Philips N.V.

Lansinoh Laboratories

Ameda Inc.

Pigeon Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Medela launched the Magic InBra wearable pump featuring FluidFeel Technology that merges hospital-grade suction with discreet portability.

- March 2025: Munchkin introduced Flow Nipple Shield +, the first shield allowing visual confirmation of milk flow during nursing, signalling the firm’s expansion into infant nutrition accessories.

Global Breast Shells Market Report Scope

| Vented Shells |

| Non-vented Shells |

| Medical-grade Silicone |

| Polypropylene |

| Others (TPE, Bio-plastics) |

| Hospital & Pharmacy Retail |

| Baby Specialty Stores |

| Supermarkets/Hypermarkets |

| Online Retail |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Vented Shells | |

| Non-vented Shells | ||

| By Material | Medical-grade Silicone | |

| Polypropylene | ||

| Others (TPE, Bio-plastics) | ||

| By Distribution Channel | Hospital & Pharmacy Retail | |

| Baby Specialty Stores | ||

| Supermarkets/Hypermarkets | ||

| Online Retail | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

1. What is the current breast shells market size?

The breast shells market size reached USD 79.36 billion in 2025 and is projected at USD 97.061 billion by 2030.

2. Which product type leads the market?

Vented shells with airflow lattice technology dominated with 56.72% market share in 2024 and offer the fastest growth trajectory.

3. Why is online retail growing so fast?

Privacy, detailed product education, and insurer acceptance of direct-to-consumer purchases propel online retail, which is expanding at an 8.67% CAGR.

4. Which region is expected to post the highest growth?

Asia-Pacific is forecast to grow at a 6.59% CAGR through 2030 as breastfeeding promotion policies and rising urban incomes converge.

5. How are sustainability concerns influencing product development?

Manufacturers are shifting toward bio-based silicone and recycled resins to meet European and North American mandates aimed at reducing single-use plastics.

Page last updated on: