Pipette Tips Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

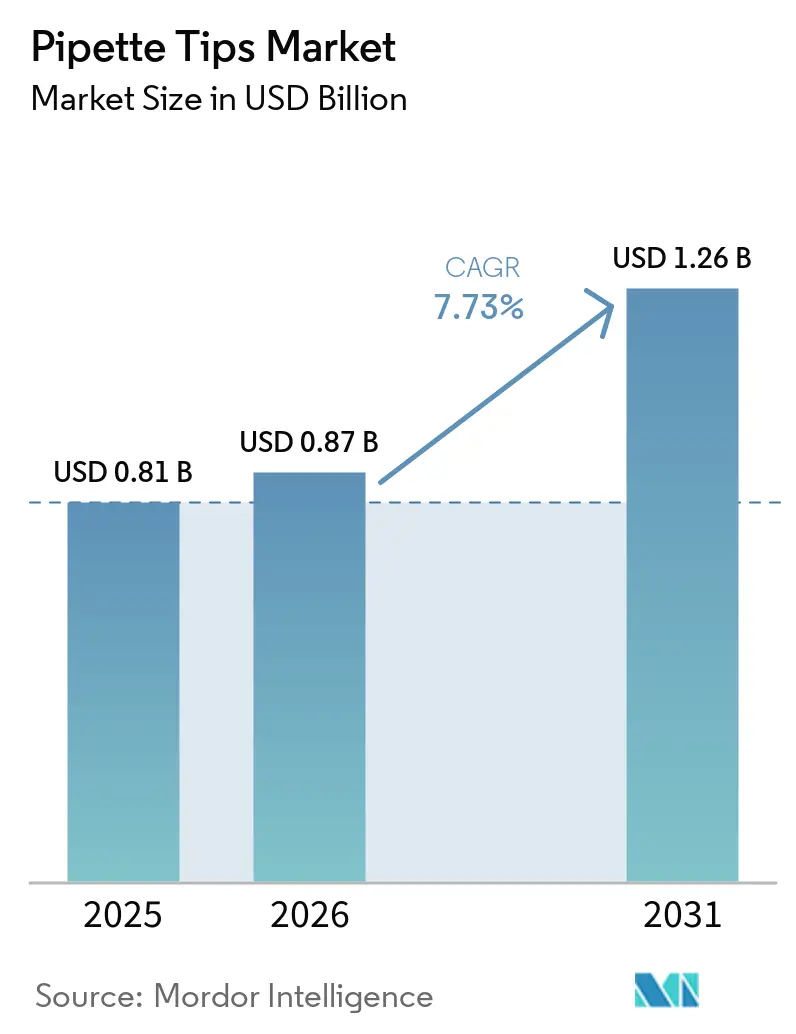

| Market Size (2026) | USD 0.87 Billion |

| Market Size (2031) | USD 1.26 Billion |

| Growth Rate (2026 - 2031) | 7.73% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pipette Tips Market Analysis by Mordor Intelligence

The Pipette Tips Market size is expected to increase from USD 0.81 billion in 2025 to USD 0.87 billion in 2026 and reach USD 1.26 billion by 2031, growing at a CAGR of 7.73% over 2026-2031.

The pipette tips market is driven by the growing adoption of high-throughput research workflows, rising demand for molecular diagnostics, and the increasing shift toward automated liquid handling in pharmaceutical R&D and clinical testing. Purchasing decisions now emphasize contamination control, robotic compatibility, and audited quality systems, giving validated consumables a competitive edge over basic low-cost products. Sustainability is also influencing buying behavior, with institutions focusing on product carbon disclosures and bio-based materials when selecting suppliers for routine laboratory consumables.

Key Report Takeaways

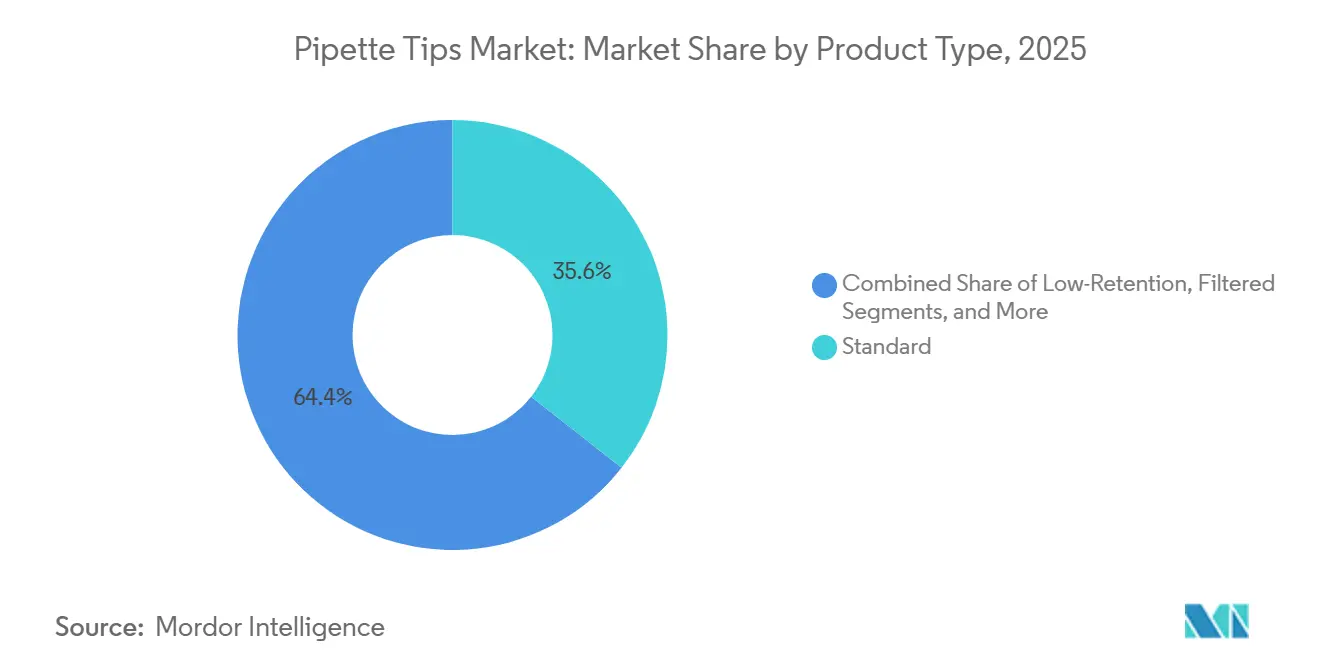

- By product type, standard tips held 35.64% of the pipette tips market share in 2025, while filtered tips are projected to expand at 8.76% CAGR through 2031.

- By technology type, robotic tips accounted for 58.47% share of the pipette tips market size in 2025 and also recorded the highest projected CAGR at 9.12% through 2031.

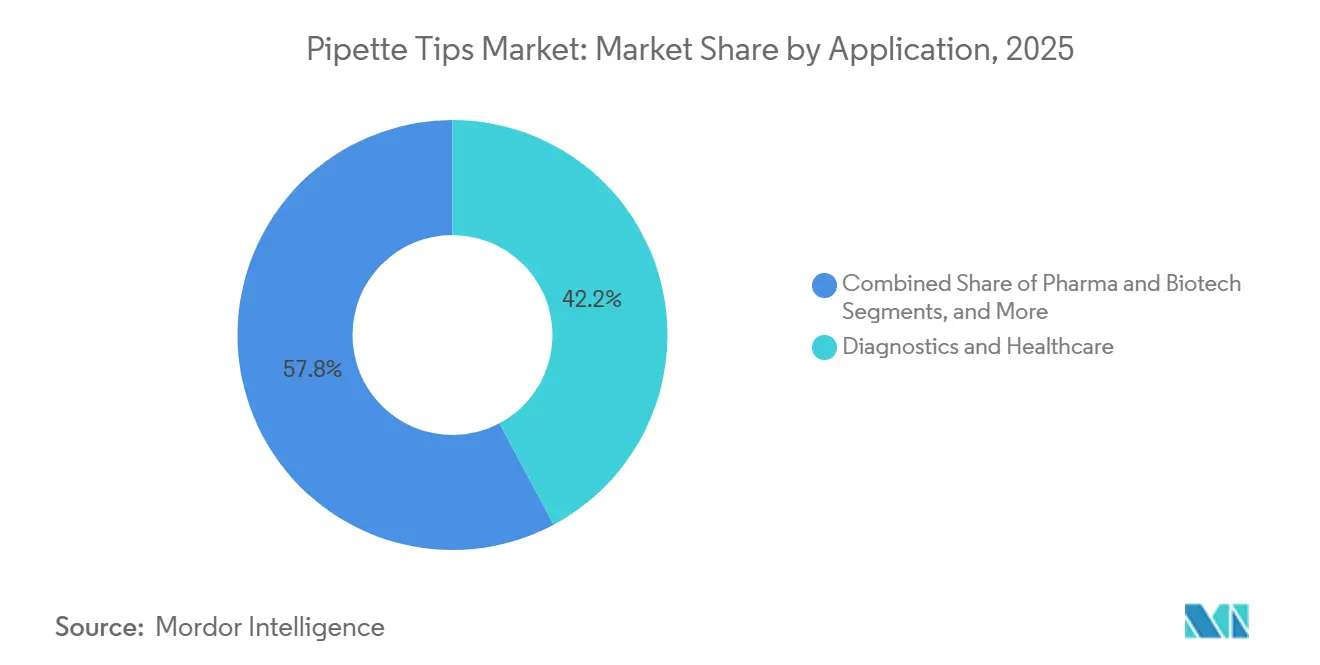

- By application, Diagnostics and Healthcare accounted for 42.23% share of the pipette tips market size in 2025, while Pharma and Biotech is expected to grow at 8.25% CAGR through 2031.

- By end user, diagnostics and healthcare held 51.78% share in 2025, while Pharmaceutical and biotechnology companies are projected to expand at 9.88% CAGR through 2031.

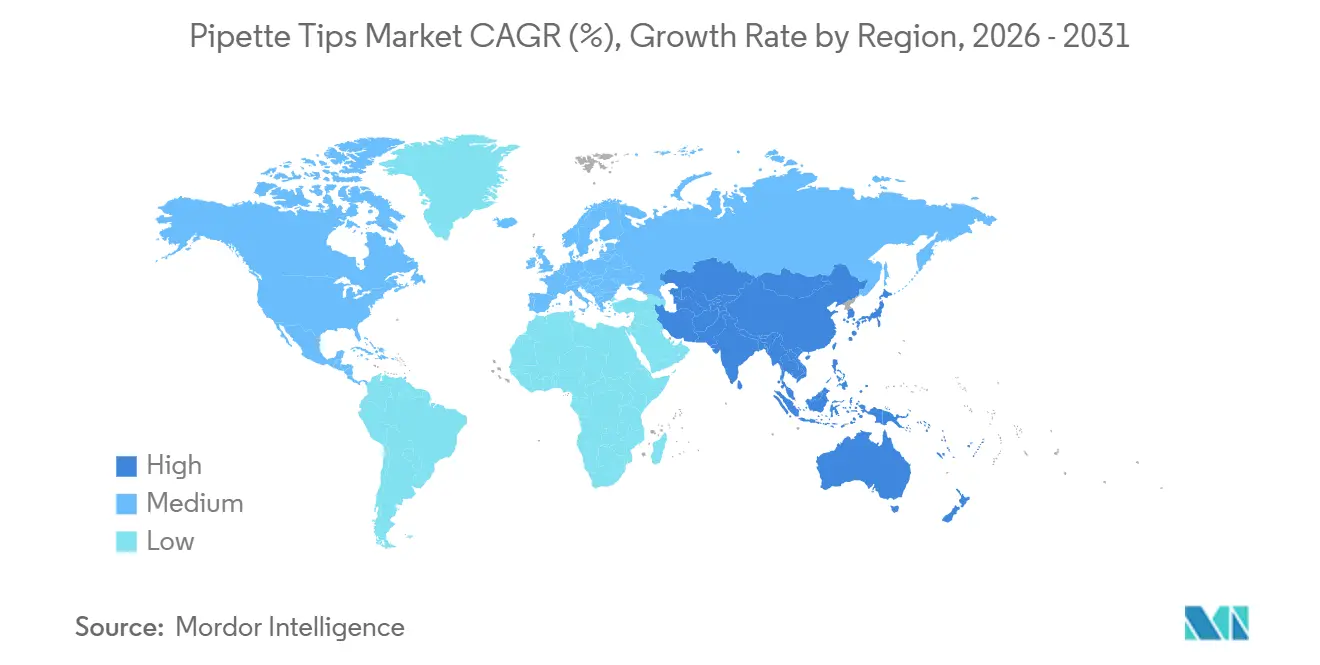

- By geography, North America commanded 38.86% share in 2025, while Asia-Pacific is projected to grow at 7.95% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Pipette Tips Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising high-throughput diagnostic and research workflows | +1.9% | Global, with concentration in North America and Western Europe | Short term (≤ 2 years) |

| Automation compatibility becomes a procurement standard | +1.7% | North America, Europe, APAC core including China, Japan, and South Korea | Medium term (2-4 years) |

| Single-use contamination control increases in molecular biology | +1.4% | Global, with spillover from APAC into Middle East and Africa | Short term (≤ 2 years) |

| Growth in sterile, Rnase-free, and DNase-free consumables | +1.1% | North America and Europe, with rising demand in APAC | Medium term (2-4 years) |

| Sustainability procurement shifts toward recyclable and bio-based materials | +0.6% | Europe first, followed by North America and APAC | Long term (≥ 4 years) |

| Localized Manufacturing And Dual-Sourcing Reduce Supply Chain Risk | +0.5% | North America, with a smaller but visible role in Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising High-Throughput Diagnostic and Research Workflows Drive Volume Consumption

High-throughput laboratories consume pipette tips at a significantly higher rate than traditional single-sample methods. For example, a single 96-well protocol can use 96 to 192 tips in one run, driving demand in plate-based testing, genomics, and drug discovery. In August 2025, Thermo Fisher Scientific opened a 375,000 sq ft carbon-neutral facility in Mebane, North Carolina, partially funded by a USD 192.5 million U.S. government contract.[1]NC Governor Press Release, “Governor Stein Underscores North Carolina's Leadership in Biotech Industry at Thermo Fisher Scientific Ribbon-Cutting Ceremony,” NC Governor, governor.nc.gov The facility is designed to produce 40 million pipette tips weekly, emphasizing the critical role of pipette tips in national health preparedness and laboratory operations. Advanced automation enables the production of 96 tips every 12 seconds, aligning manufacturing efficiency with rising laboratory demands. This increased capacity may lead to price pressures on imported standard formats in North America, requiring suppliers to focus on performance differentiation to maintain margins.

Automation Compatibility Becomes a Procurement Standard

Robotic liquid handling has redefined compatibility, requiring consumables to integrate seamlessly with automated systems. Research in 2025 demonstrated that an AI-driven computer vision model on the Opentrons OT-2 achieved 98% accuracy in detecting missing or incorrectly loaded pipette tips. Dimensional consistency is now critical, as inconsistent tip geometry can disrupt automated workflows and liquid handling.[2]U. Egle et al., “Real-Time AI-Driven Quality Control for Laboratory Automation: A Novel Computer Vision Solution for the Opentrons OT-2 Liquid Handling Robot,” Applied Intelligence, link.springer.com Suppliers unable to maintain tight tolerances may face challenges in automated procurement programs. Hamilton's GreenLine Tips, covering 85% of its catalog, combine quality assurance with sustainability, reflecting the market's shift toward precision-certified suppliers in automation-heavy accounts.

Single-Use Contamination Control Increases in Molecular Biology Workflows

Contamination control has become a fundamental requirement in molecular biology workflows. Eppendorf data revealed that aerosols generated during pipetting were effectively blocked by the ep Dualfilter T.I.P.S. design, enhancing reliability in PCR, NGS, and viral testing. As sequencing costs decline and sample volumes rise, laboratories are less tolerant of unfiltered tips due to the high cost of rework. ISO 15189:2022 has further emphasized sample integrity in clinical settings, driving the adoption of filtered tips even in budget-conscious environments. This shift positions contamination prevention as a compliance issue, favoring premium formats over standard products.

Growth in Sterile, RNase-Free, and DNase-Free Consumables Mirrors Biopharma Scale-Up

Biologic drug development increasingly relies on sterile, RNase-free, and DNase-free consumables due to their role in workflows involving proteins, nucleic acids, and cell-based systems. Sartorius reported strong growth in its consumables and services segment in fiscal 2025, with consumables driving 2-6% projected sales revenue growth in 2026. CDMOs and biopharma manufacturers now procure certified tips in bulk, as switching to cheaper alternatives can lead to documentation, validation costs, and process risks. This trend highlights the growing importance of repeat consumables in the pipette tips market, aligning with the needs of advanced biologics laboratories.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Plastic waste disposal pressure and recycling gaps | -0.9% | Europe under stronger regulation, followed by North America and APAC through institutional pressure | Medium term (2-4 years) |

| Price sensitivity in volume-based laboratory consumables | -1.2% | Global, with sharper pressure in APAC and South America | Short term (≤ 2 years) |

| Raw material and precision mold cost volatility | -0.8% | Global, with higher pressure on domestic manufacturers in North America | Short term (≤ 2 years) |

| Qualification burden for robotic and specialty tip compatibility | -0.5% | North America and Europe, where automation penetration is higher | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Plastic Waste Disposal Pressure and Recycling Gaps Create Procurement Risk

Laboratories generate significant volumes of plastic waste, with a 2025 study estimating 5.5 million tons of waste from around 20,500 research institutions globally. This waste has an environmental impact comparable to the CO2 emissions of over 1 million UK residents. Most recycling systems reject laboratory plastics due to contamination concerns, leaving incineration or landfill as the primary disposal methods. The EU's ESPR framework is driving stricter scrutiny on carbon disclosure, pushing buyers in Europe and North America to demand better end-of-life handling and lower embedded emissions.[3]Westburg Life Sciences, “Product Announcement: TripleA® PFAS-Free Pipette Tips,” Westburg Life Sciences, westburg.eu Suppliers without take-back programs, bio-based formulations, or recycling partnerships may face challenges in accessing the pipette tips market as sustainability becomes a key procurement factor. While demand for single-use tips persists, environmental performance will increasingly influence purchasing decisions.

Price Sensitivity in Volume-Based Laboratory Consumables Compresses Margins at Scale

Large academic systems, government labs, and hospital networks often prioritize unit price in tender contracts. Premium suppliers face challenges as attributes like certified purity, robotic precision, and bio-based materials do not always yield immediate volume advantages in tender-driven markets. To maintain price premiums, vendors must demonstrate lower costs per result, reduced contamination risks, or simplified automation validation. Pricing pressure is particularly strong in South and Southeast Asia, where local products are priced significantly lower than imported premium brands. While market expansion is possible in these regions, supplier margins will remain under pressure unless quality standards improve.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Filtered Formats Gaining at the Expense of Standard Tier Premium

In 2025, standard tips held a 35.64% share of the pipette tips market, leading in routine tasks like buffer preparation and gel loading. This dominance reflects the affordability and availability required for high-volume, low-sensitivity tasks. Filtered tips are projected to grow at an 8.76% CAGR through 2031, driven by increased adoption of contamination-sensitive methods like NGS and qPCR. Low-retention tips, though a smaller segment, are gaining relevance in cell culture and biologics handling, where loss impacts assay quality.

Specialty formats, such as extended-length and wide-bore tips, cater to niche yet demanding tasks in automated screening and liquid-level detection. The market is shifting as filtered tips transition from a premium niche to routine procurement, particularly among large accounts with strict quality controls. Suppliers with automated molding for filter integration hold a competitive edge due to the complexity of scaling this process. Eppendorf introduced its ept.i.p.s. bio-based pipette tip line in 2025, utilizing 90% renewable materials from recycled cooking oil. Westburg Life Sciences expanded this trend in 2026 with TripleA PFAS-free pipette tips, emphasizing material compliance as a key differentiator.

By Technology Type: Robotic Ecosystem Lock-In Defines the Competitive Moat

Robotic tips accounted for 58.47% of the pipette tips market in 2025 and are projected to grow at a 9.12% CAGR through 2031. This growth highlights the untapped potential for automation in laboratory workflows. Laboratories adopting automated liquid handlers often remain within validated tip ecosystems for performance and compliance. Programs from Tecan, Hamilton, and Eppendorf strengthen this lock-in by tying qualification to specific platform and consumable combinations. Non-robotic tips, while relevant in teaching labs and field diagnostics, face slower growth due to the absence of validated workflow stickiness.

The competitive edge lies in ecosystem compatibility rather than pricing or catalog variety. Procurement teams increasingly prefer suppliers offering dimensional data and cross-platform validation upfront, shifting qualification responsibility to manufacturers. Companies supporting multi-vendor automation environments with consistent batch geometry gain an advantage. ISO 9001 and ISO 13485 standards favor vendors with superior quality documentation and dimensional control in pharmaceutical automation.

By Application: Diagnostics Volume Dominates, Pharma Drives Margin

Diagnostics and healthcare held a 42.23% share of the pipette tips market in 2025, driven by routine testing in hospitals and point-of-care diagnostics. This segment leads due to steady testing volumes and strict single-use mandates. Pharma and biotech, forecasted to grow at an 8.25% CAGR through 2031, are expanding with advancements in mRNA therapeutics and gene therapy. Diagnostics rely on standard and filtered tips for repetitive tasks, while pharma opts for premium, automation-ready formats, reflecting distinct purchasing patterns.

Pharma procurement offers better margins and reduced price sensitivity, encouraging investment in higher-specification formats. Academia and education maintain stable demand and shape early standards influencing commercial practices. Other sectors, including environmental testing and food safety, contribute meaningful demand, emphasizing purity and sterility. As platforms like Opentrons Flex gain traction, academic buyers are shifting from bulk unfiltered options to racked, automation-compatible formats.

By End User: Pharmaceutical Companies Set the Quality Benchmark Others Follow

Diagnostics and healthcare end users dominated with a 51.78% share in 2025, reflecting the scale of clinical testing globally. This lead is volume-driven, as clinical labs consume significant quantities of pipette tips daily. Pharmaceutical and biotech companies, forecasted to grow at a 9.88% CAGR through 2031, are expanding due to biomanufacturing and demand for certified consumables. Buyers prioritize documentation, lot consistency, and integration with quality systems, driving demand in the pipette tips market.

Cell and gene therapy manufacturing is expected to grow rapidly, with automated workflows requiring frequent tip changes and adherence to approved consumables. CDMOs have become significant players, consuming tips at levels comparable to large clinical networks, reinforcing supplier loyalty. The "Others" category, including CDMOs, industrial labs, and environmental testing networks, continues to grow as standardized practices gain traction. Sartorius strengthened its position in advanced cell model workflows with its 2025 acquisition of MATTEK, aligning with premium demand in the pipette tips market.

Geography Analysis

In 2025, North America held a 38.86% share of the pipette tips market, maintaining its leading position. The region benefits from a strong biotechnology and pharmaceutical base, established clinical testing infrastructure, and a focus on supply continuity following earlier shortages. Thermo Fisher Scientific opened a facility in Mebane, North Carolina, in August 2025, with a weekly capacity of at least 40 million tips, supported by U.S. government funding. This development strengthens domestic supply, reducing reliance on cross-border sources. Europe remains a key market, driven by robust pharmaceutical research in Germany, the United Kingdom, France, and the Netherlands, alongside strict accreditation standards. The EU's ESPR framework is accelerating the adoption of low-carbon and bio-based consumables.

Asia-Pacific is projected to grow at a 7.95% CAGR through 2031, making it the fastest-growing region in the pipette tips market. China's demand is fueled by investments in biotech parks, clinical laboratory networks, and biologics manufacturing. India is expanding diagnostic capacity, driving demand for standard high-volume tips and certified products for quality-focused laboratories. Japan, while mature, is shifting toward higher-value automated formats, supported by domestic biomanufacturing priorities. South Korea and Australia contribute with advanced genomics and life science research infrastructure. The region's growth is driven by a mix of China's scale, India's diagnostics expansion, and automation demand in developed research hubs.

The Middle East and Africa benefit from healthcare infrastructure investments, particularly in the GCC and South Africa, though import dependence and customs complexities limit faster growth. South America, led by Brazil and Argentina, has a strong pharmaceutical research base and increasing clinical trial activity, but price sensitivity and currency volatility challenge premium tip adoption. Dual-sourcing has become a common procurement strategy, with buyers engaging one global supplier and one regional backup to mitigate disruption risks. This approach expands the supplier pool while intensifying competition as suppliers strive to retain market share.

Competitive Landscape

In the pipette tips market, Eppendorf SE, Thermo Fisher Scientific, Sartorius AG, Hamilton Company, and Tecan Trading AG dominate the premium tier, leveraging integrated instrument and consumable strategies. Competing with a focus on differentiation, a wider group including Biotix, Labcon North America, INTEGRA Biosciences, Sarstedt, Greiner Bio-One, and Starlab International emphasize universal-fit compatibility, sustainability, and regional targeting. Suppliers now gain a competitive edge by linking tip performance to broader workflows, rather than merely expanding catalog size. Proprietary innovations like Eppendorf's TwinLid reload system, Hamilton's GreenLine portfolio, and Sartorius's Safetyspace gap filter design elevate routine consumables to premium status. Such strategies increase switching costs, as labs prioritize fit consistency, validated performance, and thorough documentation once workflows are set.

The pipette tips market presents opportunities in sustainability and advanced automation. Mid-sized suppliers differentiate with bio-based, PFAS-free, and take-back products, even without the reach of industry giants. Material choices, such as Hamilton's GreenLine and Westburg's TripleA PFAS-free launch, are becoming central to competitive messaging. As tip verification integrates with workflows, software-linked confirmation tools are gaining importance in automated settings. Vendors excelling in both physical precision and digital workflow validation are likely to gain market traction.

Innovative systems like IonField Systems' PureTIP One, which automates tip cleaning for up to 70 racks hourly, challenge the single-use model. However, stringent standards like ISO 13485 and FDA 21 CFR Part 820 remain significant barriers for smaller entrants targeting regulated pharmaceutical and clinical markets. Investments such as Thermo Fisher's in North Carolina and Sartorius's planned September 2025 launch of the Cubis II Pipette Calibration System highlight how leading companies are expanding regional and service footprints. This strategy strengthens their market position and preserves pricing power as competition intensifies across regions, product tiers, and sustainability narratives.

Pipette Tips Industry Leaders

Thermo Fisher Scientific Inc.

Eppendorf SE

Corning Incorporated

Sartorius AG

Gilson Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Biotage, a global leader in drug discovery and analytical testing, acquired DPX Technologies to strengthen its sample preparation capabilities and expand in pipette tip technology.

- September 2025: Eppendorf introduced ept.i.p.s. bio-based pipette tips, made from over 90% renewable materials, reducing the carbon footprint by 28% compared to fossil-based alternatives.

- August 2025: Thermo Fisher Scientific opened a 375,000-sq-ft carbon-neutral manufacturing facility in Mebane, NC, with a weekly capacity of 40 million pipette tips, supported by advanced automation.

Global Pipette Tips Market Report Scope

As per the scope of the report, pipette tips are small, disposable, cone-shaped plastic attachments. They are placed on the end of a pipette, a handheld lab tool used to measure and transfer tiny amounts of liquid.

The pipette tips market is segmented by product type, technology type, application, end-user, and geography. By product type, the market includes standard, filtered, low-retention, and specialty & other product types. By technology type, the market is segmented into non-robotic and robotic. By application, the market is categorized into diagnostics and healthcare, pharma and biotech, academia and education, and other applications. By end-user, the market is segmented into diagnostics and healthcare, pharmaceutical and biotechnology companies, academic and research institutes, and others. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Standard |

| Filtered |

| Low-Retention |

| Specialty and Other Product Types |

| Non-Robotic |

| Robotic |

| Diagnostics and Healthcare |

| Pharma and Biotech |

| Academia and Education |

| Other Applications |

| Diagnostics and Healthcare |

| Pharmaceutical and Biotechnology Companies |

| Academic and Research Institutes |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Standard | |

| Filtered | ||

| Low-Retention | ||

| Specialty and Other Product Types | ||

| By Technology Type | Non-Robotic | |

| Robotic | ||

| By Application | Diagnostics and Healthcare | |

| Pharma and Biotech | ||

| Academia and Education | ||

| Other Applications | ||

| By End User | Diagnostics and Healthcare | |

| Pharmaceutical and Biotechnology Companies | ||

| Academic and Research Institutes | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the 2026 value and 2031 outlook for pipette tips?

The pipette tips market reaches USD 0.806 billion in 2026 and is forecast to reach USD 1.2 billion by 2031, growing at a 7.73% CAGR.

Which product type leads demand and which one grows the fastest?

Standard tips led with 35.64% share in 2025, while filtered tips are projected to grow fastest at 8.76% CAGR through 2031.

Why are robotic tips expanding so quickly?

Robotic tips held 58.47% share in 2025 and are forecast to grow at 9.12% CAGR because labs are moving toward automation, validated compatibility, and tighter dimensional control.

Which end users are creating the strongest future demand?

Diagnostics and Healthcare remains the largest end-user group at 51.78% share in 2025, while Pharmaceutical and Biotechnology Companies are growing fastest at 9.88% CAGR.

Which region is expected to grow the fastest through 2031?

Asia-Pacific is the fastest-growing region with a 7.95% CAGR, supported by life science expansion in China, diagnostics growth in India, and automation demand in developed research markets.

How is sustainability changing supplier selection?

Buyers are paying more attention to carbon footprint, bio-based materials, PFAS-free formulations, and recycling pathways, which is lifting the profile of differentiated premium tip suppliers.

Page last updated on: