Physiological Saline Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

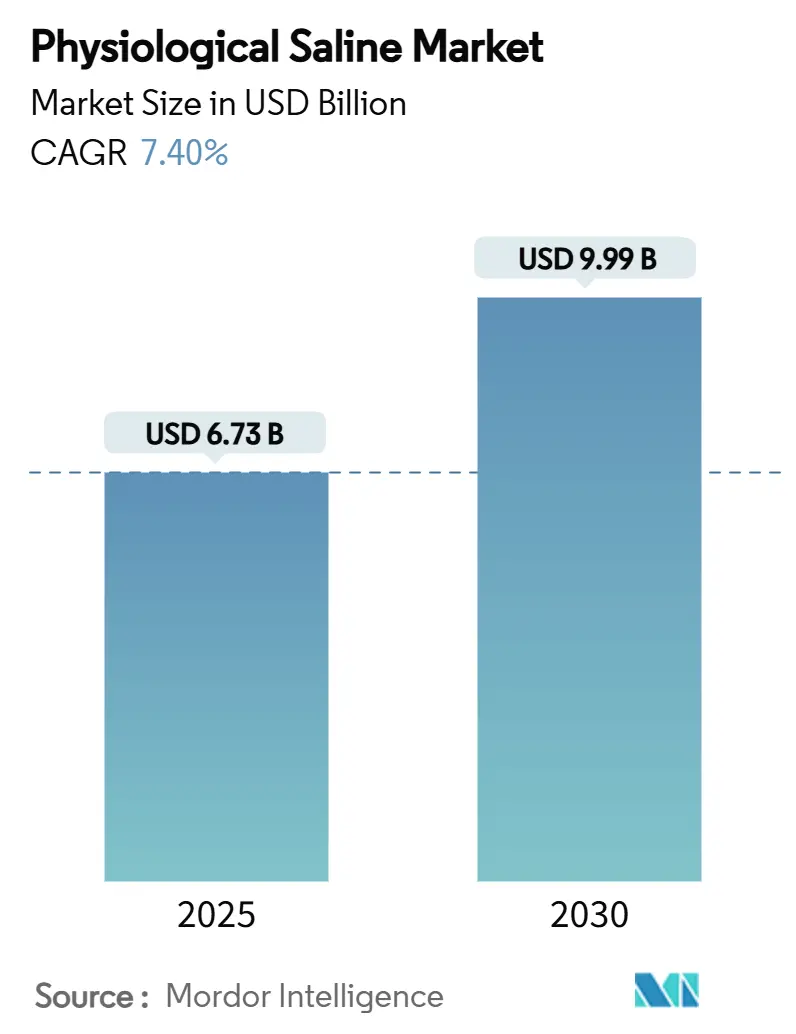

| Market Size (2025) | USD 6.73 Billion |

| Market Size (2030) | USD 9.99 Billion |

| Growth Rate (2025 - 2030) | 7.40% CAGR |

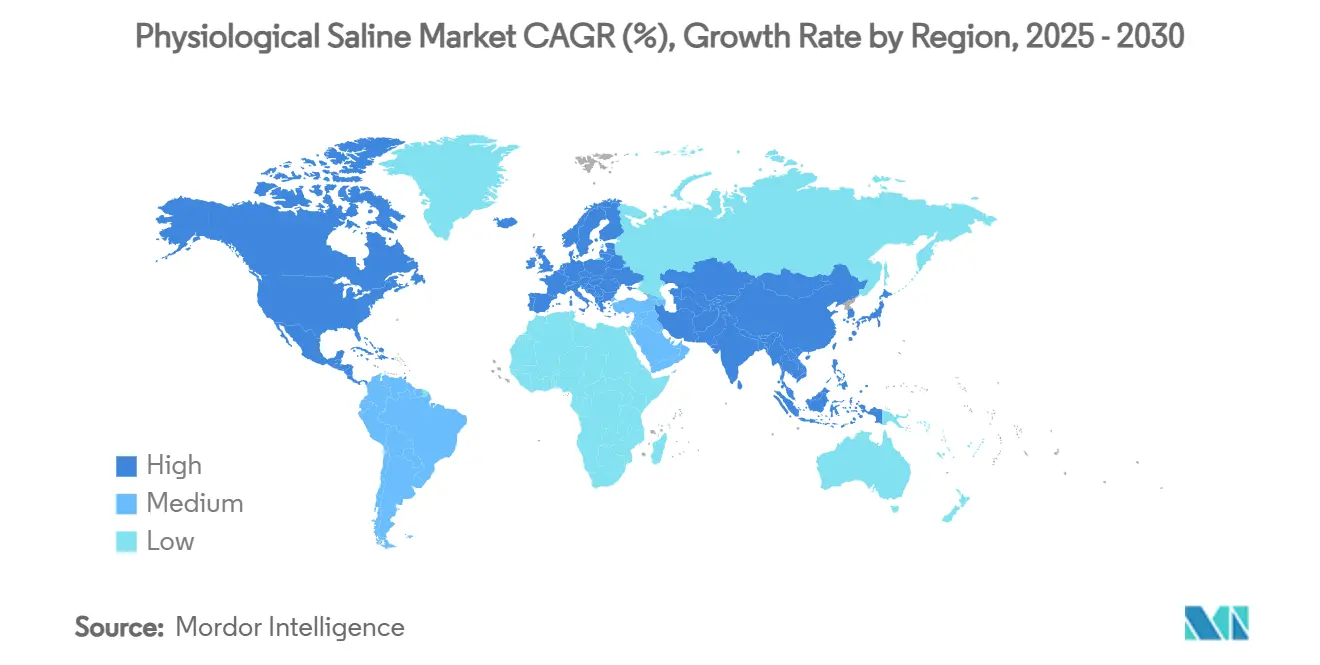

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Physiological Saline Market Analysis by Mordor Intelligence

The physiological saline market size stands at USD 6.73 billion in 2025 and is projected to climb to USD 9.99 billion by 2030, reflecting a 7.40% CAGR during the forecast window. Growing dependence on intravenous (IV) therapy across emergency medicine, surgery, dialysis, oncology infusions, and rapidly expanding home-care programs fuels this trajectory. Hospitals still consume the largest volumes, yet new demand originates from ambulatory surgical centers and in-home infusion providers that value supply-chain resilience and ready-to-use formats. Rising chronic kidney disease (CKD) prevalence, shifting reimbursement toward value-based care, and clinical preference for balanced crystalloids over traditional 0.9% saline reinforce the expansion. Competitive strategies revolve around geographic manufacturing redundancy, advanced packaging, and technology-enabled distribution, most significantly as drone logistics for remote deliveries, while demographic pressures from aging populations further enlarge the physiological saline market.

Key Report Takeaways

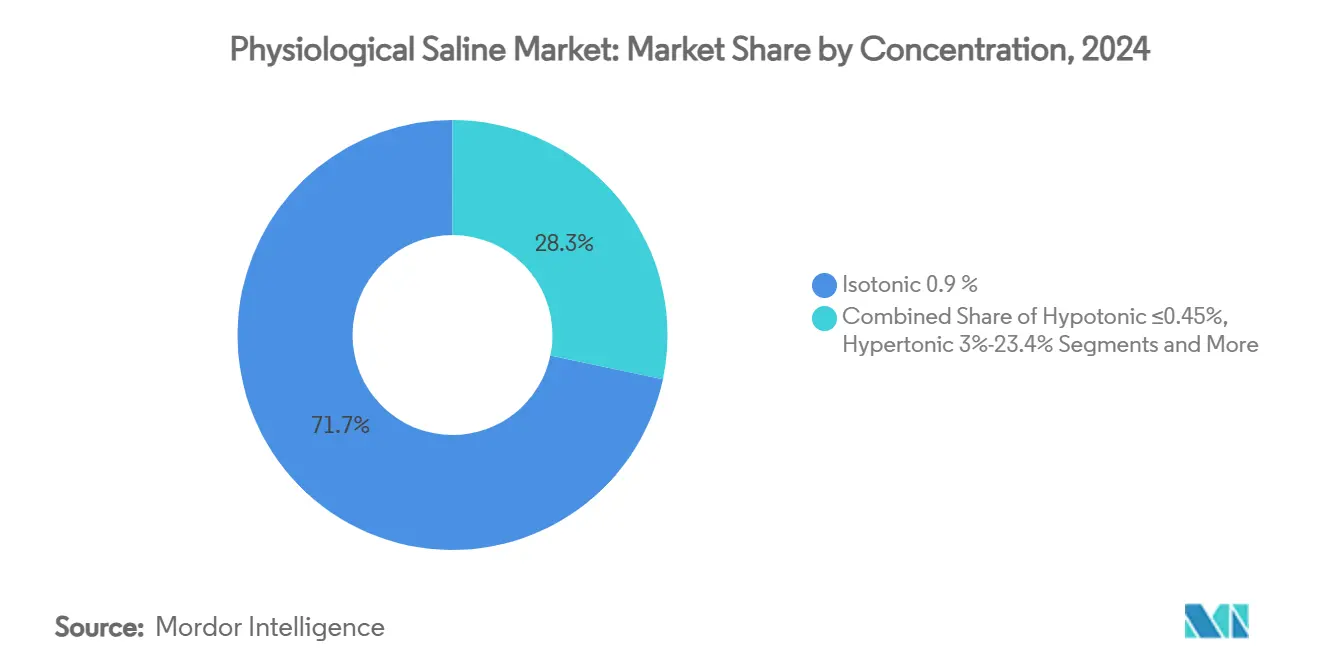

- By concentration, isotonic 0.9% saline led with 71.7% physiological saline market share in 2024; balanced solutions are advancing at a 9.4% CAGR through 2030.

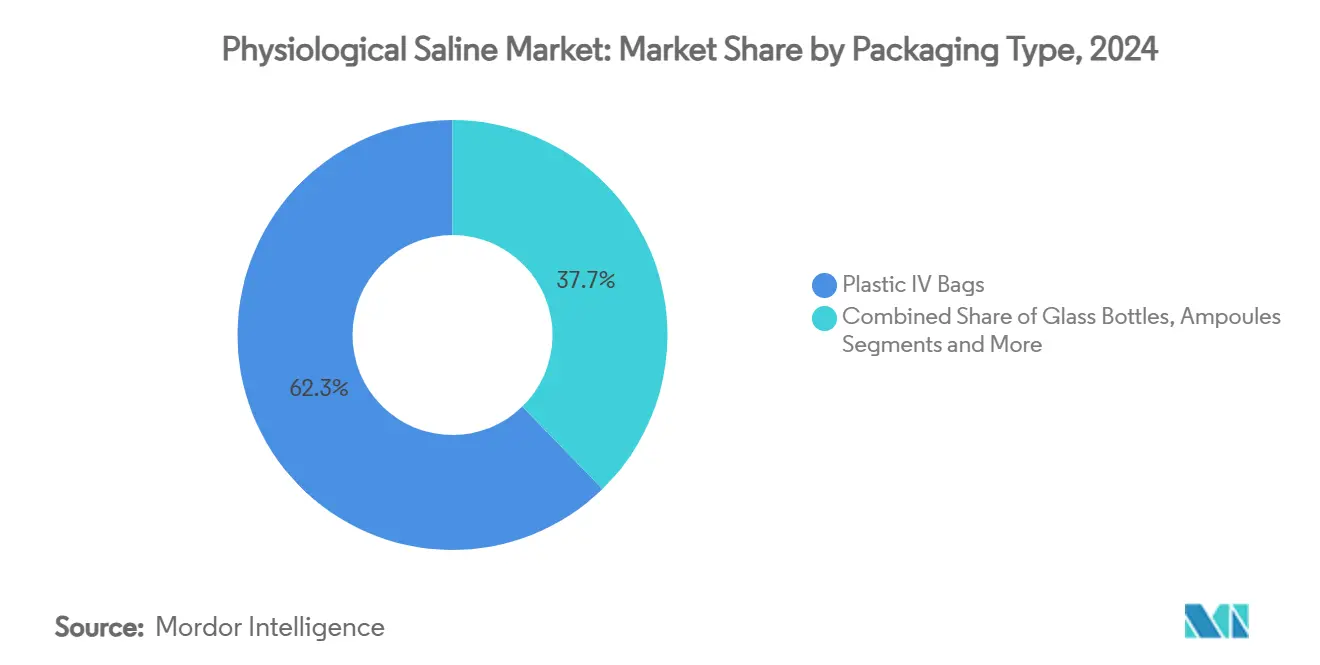

- By packaging, plastic IV bags held 62.3% share of the physiological saline market size in 2024, while pre-filled syringes posted the fastest 8.8% CAGR to 2030.

- By end user, hospitals accounted for a 48.4% slice of the physiological saline market size in 2024 and home-healthcare plus emergency medical services are expanding at a 9.8% CAGR through 2030.

- By geography, North America maintained 34.90% physiological saline market share in 2024; Asia Pacific is set to outpace all regions at a 7.8% CAGR to 2030.

Global Physiological Saline Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global surgical & trauma procedure volumes | +1.80% | North America & Europe | Medium term (2-4 years) |

| Increasing prevalence of CKD driving dialysis saline demand | +1.20% | North America & APAC | Long term (≥ 4 years) |

| Expansion of IV therapy in home-care & ambulatory settings | +1.50% | North America & Europe expanding to APAC | Medium term (2-4 years) |

| Widening geriatric population with fluid-replacement needs | +1.00% | Developed markets worldwide | Long term (≥ 4 years) |

| Saline as carrier for large-volume biologic infusions | +0.80% | North America & Europe | Medium term (2-4 years) |

| Drone-enabled emergency logistics for saline bag delivery | +0.30% | Remote regions worldwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Global Surgical & Trauma Procedure Volumes

Growing elective and trauma surgery volumes keep isotonic crystalloid solutions as first-line resuscitation therapy, with trauma guidelines endorsing warmed 0.9% saline and lactated Ringer’s for permissive hypotension scenarios. Hospital chains in India alone plan USD 2.2 billion bed expansions, enlarging baseline IV fluid demand. Evidence-based protocols increasingly mandate fluid warmers to curb hypothermia and integrate balanced crystalloids for acidosis mitigation, broadening the physiological saline market beyond conventional formulations. Military medicine reinforces this driver by retaining crystalloids as foundational resuscitation tools in combat casualty care.[1]Springer, “Advancements in Damage Control Care,” springer.comCollectively, capacity expansions and protocol refinements underpin steady demand across the physiological saline market.

Increasing Prevalence of CKD Driving Dialysis Saline Demand

CKD incidence continues rising, with integrated kidney-care platforms such as DaVita managing 58,000 risk-based patients dependent on dialysis-grade saline. Fresenius Medical Care’s FDA-cleared 5008X system enables high-volume hemodiafiltration that reduces mortality by 23% compared with traditional dialysis, amplifying saline consumption per treatment session. Hemodialysis units consume 1.7 million L of water annually, emphasizing the fluid-intensive nature of renal therapy. U.S. payment adjustments introduced in 2025 reshape procurement, steering providers toward value-optimized yet high-purity physiological saline market products. The convergence of regulatory policy, mortality-lowering technology, and growing patient pools consolidates dialysis as a durable growth pillar for the physiological saline market.

Expansion of IV Therapy in Homecare & Ambulatory Settings

Pre-filled syringes such as BD PosiFlush attain 34% compliance with hub-scrubbing protocols, double that of manual methods, reducing infection risk in the physiological saline market. Proposed U.S. legislation to expand Medicare reimbursement would further bolster at-home infusion volumes, stimulating demand for tamper-evident, small-volume saline formats. Connectivity solutions facilitate inventory management and remote monitoring, minimizing wastage and ensuring therapy continuity. Rising outpatient procedures and patient preference for comfort intensify pressure on suppliers to deliver versatile physiological saline market packaging engineered for portability.

Widening Geriatric Population with Fluid-Replacement Needs

Older populations experience higher dehydration and electrolyte imbalance risks, driving continuous fluid replacement therapy in acute and long-term settings. Structured hydration protocols lifted intake compliance from 15% to 60% among hospitalized seniors, showcasing unmet demand for reliable IV fluids. Supply disruptions led health systems to slash fluid usage by 70% via stewardship while safeguarding outcomes, underscoring the resiliency and adaptability of the physiological saline market. Geriatric infusion care emphasizes balanced crystalloids to avoid hyperchloremic acidosis, expanding sales of buffered solutions. Nursing guidelines increasingly recommend catheter technologies suited for fragile veins, necessitating compatible low-particulate physiological saline market formulations.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift toward balanced crystalloids over 0.9% saline | −0.8% | North America & Europe | Medium term (2-4 years) |

| Supply-chain bottlenecks in medical-grade PVC & resins | −1.2% | North America | Short term (≤ 2 years) |

| Regulatory push to phase-out single-use plastic IV bags | −0.6% | Europe & North America | Long term (≥ 4 years) |

| Emerging on-site compounding / 3-D printed IV fluids | −0.4% | North America & Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shift Toward Balanced Crystalloids Over 0.9% Saline

A meta-analysis covering 34,685 critical-care case reports found an 89.5% likelihood that balanced crystalloids cut mortality relative to normal saline.[2]The Lancet Respiratory Medicine, “Balanced crystalloids versus saline,” sciencedirect.com Pediatric ICU studies echo the benefits, displaying superior acid-base profiles within 12 hours. Hospitals trialing lactated Ringer’s hospital-wide recorded non-inferior safety and operational feasibility against saline in randomized crossovers. As formularies switch, traditional saline volumes face contraction, pressuring manufacturers whose revenues lean heavily on 0.9% offerings within the physiological saline market.

Supply-Chain Bottlenecks in Medical-Grade PVC & Resins

Hurricane Helene disabled Baxter’s North Carolina facility, formerly supplying 60% of U.S. IV fluids, exposing deep supply-chain fragility.[3]CDC, “Disruptions in IV solutions,” cdc.gov The FDA responded with expiration-date extensions and emergency imports, yet localized shortages persisted into 2025. Australia mirrored the crisis as its regulator flagged surgery cancellations due to unprecedented fluid shortfalls. Resin scarcity forces OEMs to diversify toward cyclic olefin polymers and multilayer films, raising capital outlays and moderating near-term output in the physiological saline market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Concentration: Clinical Familiarity Versus Evidence-Based Shift

Isotonic 0.9% saline commands a 71.7% physiological saline market share thanks to decades of protocol-entrenched use across global hospitals. Balanced formulations, however, post the highest 9.4% CAGR as sepsis, DKA, and pediatric guidelines highlight electrolyte equilibrium benefits. Hypotonic variants remain confined to maintenance therapy and pediatric diuresis, whereas hypertonic saline serves neurosurgical and hyponatremia emergencies. Evidence that buffered solutions mitigate hyperchloremic acidosis nudges purchasing committees to reevaluate formularies, suggesting gradual share redistribution in the physiological saline market.

Manufacturers hedge risk by scaling balanced crystalloids while sustaining isotonic lines to satisfy existing tenders. Education initiatives targeting prescribers accelerate conversion, yet procurement inertia and price differentials temper the pace of transition. Over the forecast horizon, balanced solutions are positioned to capture a wider proportion of the physiological saline market, particularly in tertiary centers across North America and Europe, where evidence uptake is swift.

By Packaging Type: Efficiency and Sustainability Drive Format Selection

Plastic IV bags retain a 62.3% share due to cost-efficiency, lightweight transport, and established supply chains. Pre-filled syringes, though smaller in volume, record an 8.8% CAGR, propelled by infection control, labor savings, and compatibility with in-home infusion pumps. Glass containers remain niche for photostable solutions. At the same time, ampoules and vials satisfy critical care micro-dosing.

Packaging innovation focuses on multilayer recyclable films and tamper-evident syringes, driven by single-use plastic regulations. Baxter’s pilot diverted over 6 tons of IV bag plastic from landfills, indicating market appetite for greener options. Suppliers integrating smart RFID tags enable real-time inventory tracking, reducing expiries and ensuring continuous physiological saline market supply in decentralized care settings.

Geography Analysis

North America’s 34.90% physiological saline market share rests on sophisticated infrastructure, premium reimbursement, and rapid evidence assimilation. Hurricane-induced shortage fallout propelled ICU Medical and Otsuka’s USD 200 million joint venture to harden capacity, illustrating strategic re-shoring. Regulatory flexibility, evidenced by expedited emergency imports, supports supply continuity while maintaining safety thresholds.

Asia Pacific, expanding at a 7.8% CAGR, benefits from hospital build-outs, liberalized foreign investment, and rising chronic disease prevalence. India’s 17,800 planned beds and China’s relaxed medical-device approval pathways invite capital, yet intense local competition prompted Baxter’s withdrawal from China, showcasing entry barriers for multinationals. Domestic champions like Kelun capitalize on cost leadership and government procurement favor.

Europe presents a mature, regulation-driven terrain emphasizing sustainability and balanced crystalloids. EMA’s device framework harmonizes safety expectations, allowing innovators such as Grifols to scale immunoglobulin manufacturing for EU and U.S. markets. Environmental policy shapes purchasing, giving an edge to suppliers offering recyclable containers and lower-chloride solutions.

Competitive Landscape

Leading manufacturers such as Baxter, Fresenius Kabi, and B. Braun leverage global plants, regulatory acumen, and integrated distribution. Baxter’s post-Helene recovery restored pre-storm production, yet underscored vulnerability in concentrated footprints. ICU Medical and Otsuka’s mega-facility targets 1.4 billion-unit capacity, fostering competitive parity and buffering regional shortages.

Technology investment differentiates suppliers: BD banks on smart, pre-fillable syringe lines, while ICU Medical’s FDA-cleared Plum Solo and Duo pumps integrate EMR connectivity for dosage accuracy. Fresenius Kabi’s Premier supply-chain award spotlights resilience groundwork via U.S. plant expansion. Start-ups explore 3-D printing of sterile fluids and drone-optimized distribution, signaling potential disruptors to the physiological saline market.

Price sensitivity endures, but providers increasingly weigh sustainability credentials and continuity guarantees when awarding multi-year tenders. Manufacturers that pair volume scale with novel packaging and digital traceability stand best poised to capture incremental physiological saline market share.

Physiological Saline Industry Leaders

Baxter International Inc.

Fresenius Kabi AG

B. Braun Melsungen AG

ICU Medical Inc.

Otsuka Pharmaceutical Co.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: ICU Medical and Otsuka Pharmaceutical Factory announced the creation of a USD 200 million joint venture to strengthen IV solutions manufacturing in North America.

- October 2024: Hurricane Helene disrupted Baxter International's North Carolina facility producing 60% of U.S. IV fluid supply, prompting industry-wide supply chain resilience initiatives.

- October 2024: B. Braun announced a 20% increase in IV fluid production capacity to address market shortages, demonstrating industry responsiveness to supply disruptions.

Global Physiological Saline Market Report Scope

| Isotonic (0.9 %) |

| Hypotonic (?0.45 %) |

| Hypertonic (3 %, 5 %, 7.5 %, 23.4 %) |

| Balanced/Buffered Saline (e.g., Plasma-Lyte) |

| Plastic IV Bags |

| Glass Bottles |

| Ampoules & Vials |

| Pre-filled Syringes |

| Hospitals |

| Ambulatory Surgery Centres |

| Dialysis Centres |

| Home-Healthcare & EMS |

| Clinics & Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Concentration | Isotonic (0.9 %) | |

| Hypotonic (?0.45 %) | ||

| Hypertonic (3 %, 5 %, 7.5 %, 23.4 %) | ||

| Balanced/Buffered Saline (e.g., Plasma-Lyte) | ||

| By Packaging Type | Plastic IV Bags | |

| Glass Bottles | ||

| Ampoules & Vials | ||

| Pre-filled Syringes | ||

| By End User | Hospitals | |

| Ambulatory Surgery Centres | ||

| Dialysis Centres | ||

| Home-Healthcare & EMS | ||

| Clinics & Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the physiological saline market in 2025 and how fast is it growing?

The physiological saline market size is USD 6.73 billion in 2025 and is forecast to expand at a 7.40% CAGR to reach USD 9.99 billion in 2030.

Which saline concentration dominates hospital procurement in 2025?

Isotonic 0.9% saline still leads with 71.7% physiological saline market share in hospital formularies, though balanced solutions are gaining traction.

What packaging format is expanding fastest?

Pre-filled saline syringes record the highest 8.8% CAGR as infection-control and efficiency needs rise in home-care and ambulatory settings.

Why is Asia Pacific the most attractive growth region?

Infrastructure build-outs, liberalized investment rules, and rising CKD incidence push Asia Pacific physiological saline demand at a 7.8% CAGR through 2030.

How are manufacturers addressing supply-chain risk?

Leading firms diversify manufacturing across regions, adopt recyclable materials, and explore drone logistics to mitigate raw-material shortages and single-facility disruptions.

What clinical trend could reduce traditional 0.9% saline volumes?

Growing evidence favoring balanced crystalloids for critical-care resuscitation is shifting protocols and could gradually curb conventional saline consumption.

Page last updated on: