Home Infusion Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

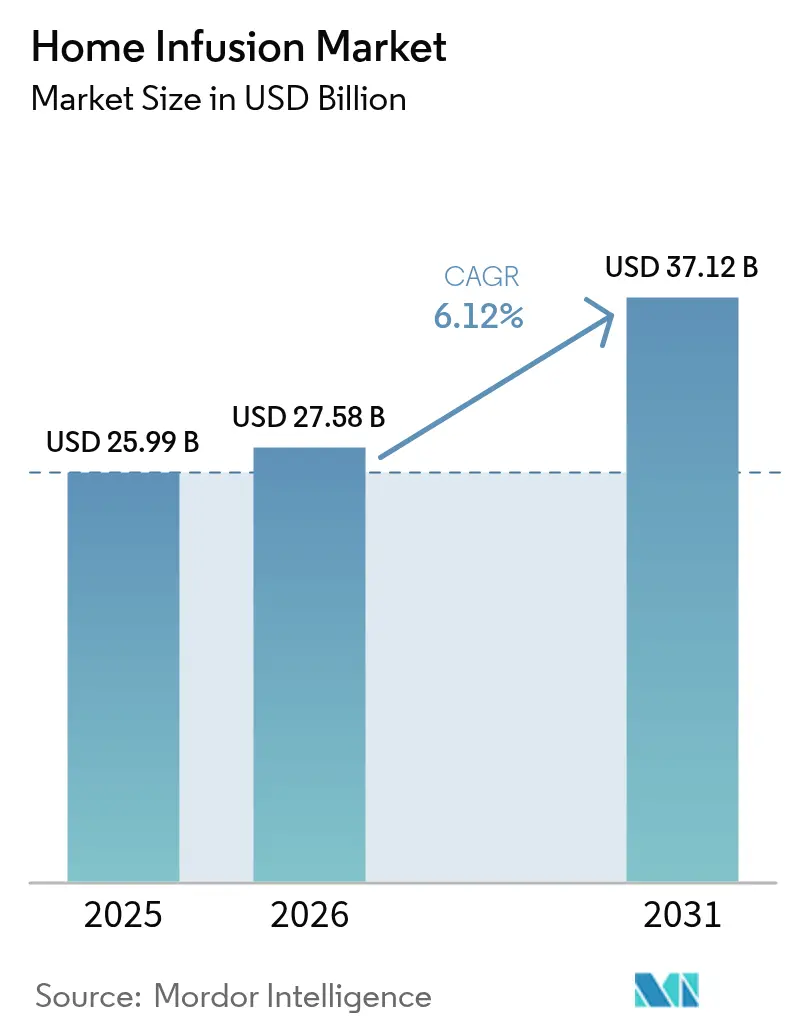

| Market Size (2026) | USD 27.58 Billion |

| Market Size (2031) | USD 37.12 Billion |

| Growth Rate (2026 - 2031) | 6.12% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Home Infusion Market Analysis by Mordor Intelligence

The home infusion market size in 2026 is estimated at USD 27.58 billion, growing from 2025 value of USD 25.99 billion with 2031 projections showing USD 37.12 billion, growing at 6.12% CAGR over 2026-2031. Demand growth is rooted in the migration of complex care from hospitals to residences, a shift encouraged by the Medicare home-infusion benefit and similar payer reforms that now reimburse professional services, equipment, and supplies delivered at home. Portable pump innovations, artificial‐intelligence monitoring, and expanding biologics pipelines further widen clinical indications that can be managed outside institutional settings. North America remains the revenue anchor on the strength of mature reimbursement structures and national provider networks; Asia-Pacific, however, outpaces every other region as healthcare infrastructure investments and rapid population aging converge. Market fragmentation persists, with more than 800 independent operators creating consolidation opportunities that private equity firms pursue to secure scale advantages in nursing coverage, supply purchase, and technology deployment. Nevertheless, recurring revenue profiles and strong clinical outcomes sustain aggressive capital allocation by large strategics and financial sponsors alike.

Key Report Takeaways

- By product, infusion pumps held 49.60% of the home infusion market share in 2025, while portable pumps are projected to expand at an 10.7% CAGR through 2031.

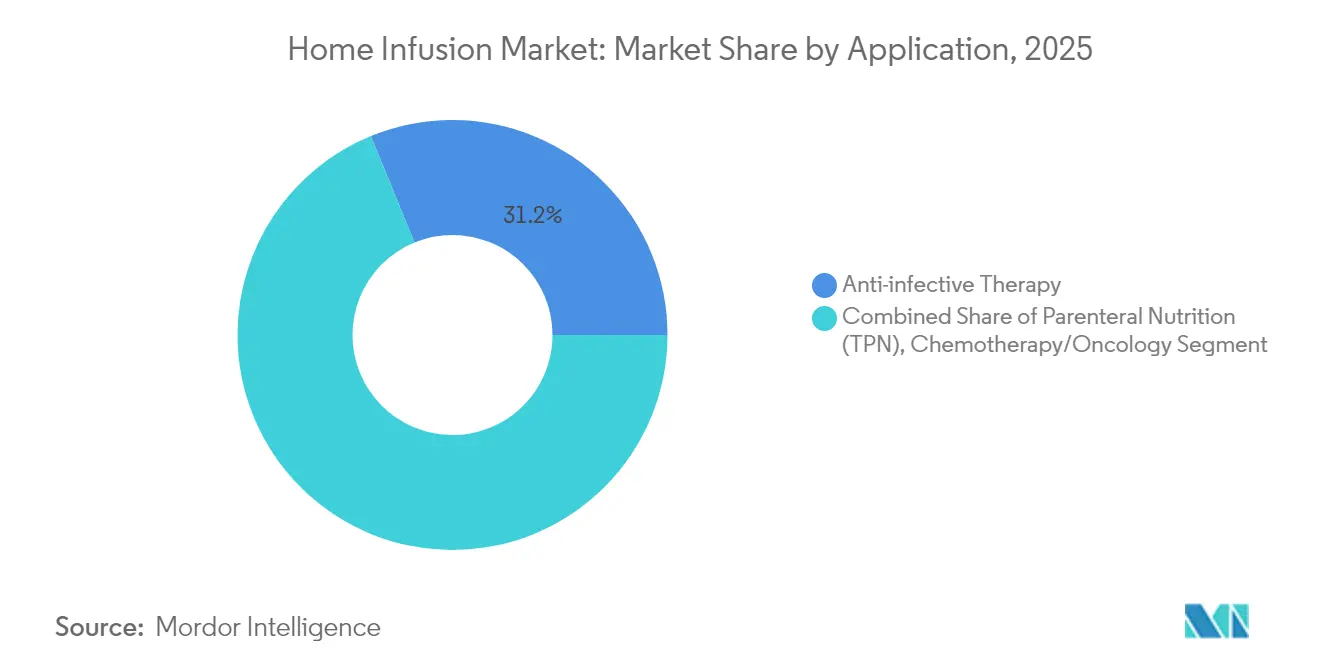

- By application, anti-infective therapy led with 31.20% revenue share in 2025; chemotherapy infusion is poised to grow at a 10.12% CAGR to 2031.

- By end user, home-care settings commanded 61.80% of the home infusion market size in 2025, whereas ambulatory infusion centers are forecast to rise at a 9.41% CAGR over the same period.

- By geography, North America accounted for 51.85% of the home infusion market size in 2025, and Asia-Pacific is set to post the highest regional CAGR at 8.74% between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Home Infusion Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging population and chronic-disease burden | +1.80% | Global; highest in Asia-Pacific and North America | Long term (≥ 4 years) |

| Uptake of home care to cut hospital costs | +1.50% | North America & Europe; spreading to Asia-Pacific | Medium term (2-4 years) |

| Expansion of Medicare home-infusion benefit | +1.20% | United States; spillover to Canada | Short term (≤ 2 years) |

| Growth of subcutaneous biologics suited for ambulatory pumps | +0.90% | Global; strongest in developed markets | Medium term (2-4 years) |

| AI-driven remote pump monitoring and predictive maintenance | +0.60% | North America & Europe first, Asia-Pacific next | Long term (≥ 4 years) |

| Private-equity funding surge for ambulatory infusion centers | +0.40% | North America; selective EU markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Aging Population and Chronic-Disease Burden Population

Aging reshapes care-delivery priorities, with the United Nations projecting the global 65-plus cohort to reach 1.6 billion by 2050. Two-thirds of these seniors will live in Asia, intensifying demand for chronic-disease therapies that can be administered outside hospitals. In Europe, new cancer cases climbed to 3.2 million in 2022, while treatment spending doubled to EUR 146 billion in 2023. The clinical load drives sustained uptake of portable and elastomeric pumps that support immunotherapy, parenteral nutrition, and long-term antibiotic regimens. Stakeholders view precise home delivery as a counterbalance to hospital bed shortages and budget pressures, solidifying the growth outlook for the home infusion market.

Uptake of Home Care to Cut Hospital Costs

Payers increasingly reward home-based delivery because it trims facility overhead, shortens inpatient stays, and improves patient satisfaction. The 2025 home health update raised Medicare reimbursement for home health agencies by 2.7%, reinforcing the economics of shifting infusion services away from hospitals. COVID-19 accelerated this migration, and specialty infusion expenditures grew 38% in 2023, a trend projected to continue as high-cost cell and gene therapies enter commercial rollout[1]Centers for Medicare & Medicaid Services, “CY 2025 Home Health Prospective Payment System Final Rule,” cms.gov. Private-equity investment mirrors these incentives; Court Square Capital Partners’ stake in Soleo Health underlines financial confidence in scalable home infusion platforms. As health systems rationalize site-of-care mix, infusion providers that demonstrate outcomes equivalence at lower total cost gain preferred-network status.

Expansion Of Medicare Home-Infusion Benefit

Since January 2021, Medicare has reimbursed professional services, equipment, and supplies for qualifying drugs delivered at home. Policy refinements in 2025 set an IVIG rate of USD 431.83, establishing predictable economics for specialty immunology therapies. The benefit’s structure obliges suppliers to meet quality metrics, prompting investment in trained nursing staff, smart pumps, and electronic documentation. Commercial payers and state Medicaid programs typically align with Medicare precedent, producing a multiplier effect that broadens addressable volumes for accredited providers. Consequently, the home infusion market gains a powerful reimbursement backbone that supports scale expansion.

Private-Equity Funding Surge for Ambulatory Infusion Centers

Financial sponsors view infusion centers as infrastructure-light assets with predictable cash flows. Growth equity fuels greenfield builds and tuck-in acquisitions that broaden payer contracts and therapy portfolios. The strategy is most visible in the United States, where roll-up platforms assemble regional networks to capture specialty biologic volumes. Select European markets show similar traction as payer reforms reward nonhospital settings. Capital inflows shorten technology adoption cycles and raise competitive stakes, propelling the home infusion market toward modernization.

Restraints Impact Table*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High acquisition and maintenance cost of infusion pumps | -0.80% | Global; acute in price-sensitive emerging markets | Medium term (2-4 years) |

| Device-related adverse events and recalls | -0.60% | Global; regulatory focus in North America, Europe | Short term (≤ 2 years) |

| Home-care nursing shortages constraining capacity | -1.10% | North America & Europe; visible in Asia-Pacific | Long term (≥ 4 years) |

| Fragmented payer rules delaying reimbursement | -0.70% | United States; variable in EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Acquisition and Maintenance Cost of Infusion Pumps

Advanced pumps blend mechanical precision with complex software, raising up-front capital needs and ongoing service fees. Smaller operators struggle to fund the latest smart models, encouraging partnership with third-party engineering firms such as Prescott’s, which Morgan Stanley Capital Partners acquired to improve device uptime across provider sites. Regulatory demands for cybersecurity patches and firmware validation add recurring expense that only scaled enterprises can absorb readily. Consequently, cost hurdles slow technology, refresh rates in emerging markets and intensify consolidation pressure in mature geographies.

Device-related Adverse Events and Recalls

Product recalls jeopardize clinician confidence and impose logistics costs. In April 2025 the FDA warned ICU Medical for software modifications made without proper 510(k) clearance, signaling strict oversight of post-market changes that might affect pump performance. Providers must allocate resources to track serial numbers, retrain staff, and swap devices to comply with corrective actions, all of which eat into operating margins. Negative publicity can also disrupt payer relationships, temporarily dampen equipment demand, and restrain the home infusion market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Pumps Drive Adoption Across Delivery Modes

Infusion pumps captured 49.60% of 2025 revenue, cementing their role as the backbone of home dosing accuracy. Portable models, favored for their compact designs and intuitive interfaces, are projected to log an 10.7% CAGR to 2031. The home infusion market size for portable pumps is therefore set to expand far faster than legacy large-volume models, which still serve patients discharged with high-flow hydration or nutrition needs. Elastomeric pumps, which operate without external power, earn physician support in outpatient antimicrobial therapy thanks to proven cost savings of EUR 4,031 per episode when refill programs are deployed. Smart connectivity functions further differentiate premium units by enabling clinicians to adjust parameters remotely and create audit trails that satisfy payer audits. Consumables such as IV sets and antimicrobial filters ride the installed-base wave, yielding recurring revenue streams that buttress manufacturers' financial models.

Growth momentum ripples across adjunct categories as well. Patient-controlled analgesia units improve post-operative recovery at home by aligning opioid dosing with real-time pain scores, thereby reducing hospital readmissions. Insulin patch pumps combine continuous glucose sensing with closed-loop algorithms; early data show improved glycemic control yet adoption lags due to device cost and patient-training requirements. Software updates remain a regulatory flashpoint: the April 2025 FDA warning to ICU Medical exemplifies the compliance expectations that manufacturers must meet when enhancing user interfaces or wireless protocols. Overall, product innovation anchors revenue growth, reinforcing the competitive weight of firms that can integrate electromechanical reliability with cloud analytics.

By Application: Anti-Infective Leads, Oncology Accelerates

Anti-infective therapy continues to hold 31.20% of total revenue as outpatient parenteral antimicrobial therapy programs become standard in tertiary-care discharge pathways. The home infusion market share for anti-infectives reflects stable demand for long-tail regimens treating osteomyelitis, endocarditis, and resistant urinary tract infections. Adoption is most pronounced in North America and Europe, where antibiotic stewardship protocols support in-home monitoring via telehealth consultations. Concurrently, chemotherapy infusion stands out as the fastest-expanding indication, projected to grow 10.12% annually through 2031. Subcutaneous monoclonal antibodies and targeted therapies that require monthly or quarterly dosing align perfectly with patient desires to avoid hospital settings; Eisai’s LEQEMBI illustrates this paradigm shift.

Parenteral nutrition remains essential for short-bowel syndrome and cancer cachexia, while hydration therapy is gaining ground for chronic heart-failure and geriatric dehydration management. Pain and analgesia segments profit from on-demand dosing pumps that reduce systemic opioid exposure. Endocrinology applications such as continuous insulin infusion are pinpointed as an under-penetrated frontier: only a fraction of eligible diabetics use pumps despite documented HbA1c improvements. Specialty biologics for primary immunodeficiencies and rare diseases augment the long-tail revenue profile, commanding premium pricing that offsets their low patient numbers. Because each indication imposes unique stability, sterility, and monitoring parameters, providers specializing in complex therapies often secure durable network partnerships.

By End User: Home Dominance, Center Momentum

Home settings contributed 61.80% of 2025 revenue, underscoring enduring patient preference for familiar surroundings and caregiver support. The home infusion market size linked to home environments draws power from reimbursement parity with hospital outpatient departments and from positive patient outcomes tracked through electronic symptom diaries. Ambulatory infusion centers, though still smaller in absolute terms, are on course for a 9.41% CAGR. They appeal to oncologists and rheumatologists who seek controlled clinical environments without the overhead of inpatient facilities. FDA approvals for over 30 cell and gene therapies amplify demand for centers equipped with negative-pressure rooms and advanced handling protocols, stimulating facility upgrades across metropolitan corridors.

Hospital outpatient departments retain relevance for high-acuity patients needing immediate crash-cart backup or radiologic surveillance. Specialty pharmacies continue integrating infusion bays to capture vertical value in dispensing high-cost biologics. Option Care Health, which operates 177 US locations, demonstrates how geographic breadth underpins service-level guarantees and results in 16.3% revenue growth during Q1 2025. Private equity consolidation of mid-sized centers accelerates network density, raising payer negotiating leverage and fostering standardized clinical protocols. Providers collectively advance toward hybrid care models, assigning each therapy to the most cost-effective, patient-appropriate venue.

Geography Analysis

North America commands 51.85% of global revenue, powered by Medicare’s robust home infusion benefit and a dense web of accredited suppliers. The United States alone could redirect up to USD 265 billion of facility spend to home settings by 2025, according to policy analysts, giving the home infusion market size unparalleled expansion leeway. Canada’s provincial systems adopt similar care-migration strategies, while Mexico’s private insurers introduce bundled home-infusion packages to court its growing middle class. Device manufacturers prioritize UL-listed products and cybersecurity features to align with stringent FDA and Health Canada requirements, which in turn nurture clinician confidence.

Asia-Pacific exhibits the fastest regional CAGR at 8.74% through 2031. Rapid population aging, rising chronic-disease prevalence, and infrastructure investments under the Asian Infrastructure Investment Bank's health strategy form a potent triad of growth drivers. China’s Healthy China 2030 policy elevates home-based chronic-care modalities, creating an addressable market that attracts both local pump makers and multinationals. Japan, already a super-aged society, expands its long-term insurance program to subsidize infusion equipment rentals, while South Korea pioneers AI-enabled pump oversight through nationwide 5G networks. In South and Southeast Asia, pharmaceutical production clusters in India and Singapore localize supply chains, trimming import duties and shortening lead times.

Europe presents heterogeneity in reimbursement but benefits from the European Medicines Agency’s centralized drug approvals. Germany and France implement national home-infusion formularies under social-insurance umbrellas; the United Kingdom’s National Health Service pilots “out-of-hospital chemotherapy” that leverages local nursing agencies. Southern and Eastern European countries lag due to budget constraints, though EU regional funds occasionally subsidize digital-health adoption.

The Middle East and Africa remain nascent yet promising. Gulf Cooperation Council nations, led by Saudi Arabia and the United Arab Emirates, invest in smart-hospital and home-care ecosystems powered by high broadband penetration. Sub-Saharan Africa sees sporadic pilot programs for HIV and tuberculosis home therapy, but infrastructure deficits and reimbursement gaps limit scale. In South America, Brazil and Argentina spearhead adoption, driven by demographic shifts and expanding private insurance. Currency volatility, however, raises equipment prices, necessitating creative financing solutions such as vendor leasing and outcome-based contracts.

Competitive Landscape

The home infusion market features more than 800 independent companies, reflecting a historically low barrier to entry for licensed pharmacies and nursing agencies. Market leaders leverage vertical integration, owning compounding pharmacies, logistics fleets, and nursing pools to protect margins against reimbursement compression. Technology differentiation also secures competitive moats; BrightSpring Health Services lifted infusion and specialty prescriptions by 22% between December 2023 and December 2024 by integrating e-prescribing, telepharmacy, and AI-based therapy monitoring[3]BrightSpring Health Services, “2024 Year-End Operational Update,” brightspringhealth.com .

Private equity sponsors accelerate consolidation, executing roll-up strategies that aggregate regional players into national or multi-state platforms. These investors inject capital for pump fleet upgrades, cybersecurity hardening, and payer-contract analytics, thereby raising operational sophistication. Device manufacturers such as Becton Dickinson, which announced a corporate separation to sharpen its focus on medication delivery and advanced monitoring, hedge against pump commoditization by bundling software services and analytics dashboards.

Emerging disruptors include specialty pharmacies integrating infusion suites to capture high-margin orphan-drug revenues and med-tech startups offering predictive maintenance for pumps. Competitive intensity remains high but tilts toward scaled entities that can weather regulatory scrutiny, nursing shortages, and cybersecurity demands.

Home Infusion Industry Leaders

Option Care Health

Coram CVS Health

Baxter International

Fresenius Kabi

ICU Medical

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Medicare Payment Advisory Commission recommended 2026 payment updates that maintain support for home health services fundamental to infusion therapy delivery

- February 2025: Court Square Capital Partners completed a strategic investment in Soleo Health, a national specialty pharmacy and infusion provider serving 22,000+ patients annually.

- February 2025: Becton Dickinson unveiled plans to spin off its Biosciences and Diagnostic Solutions units, creating a pure-play med-tech company centered on medication delivery platforms and patient monitoring

- January 2025: The U.S. Department of Health and Human Services published its AI Strategic Plan, promoting responsible use of artificial intelligence in medical device oversight and patient-care optimization.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the home infusion therapy market as all value generated when prescription drugs or biologics are delivered intravenously or sub-cutaneously at a patient's residence, together with the rental or sale of infusion pumps, tubing sets, catheters, and related disposables. We also track support service fees that accompany each at-home episode of care.

Scope exclusion: parenteral therapies administered in hospitals, physician-office suites, and ambulatory infusion centers are not counted.

Segmentation Overview

- By Product

- Infusion Pumps

- Large-volume pumps

- Syringe pumps

- Elastomeric pumps

- Insulin pumps

- Patient-controlled analgesia (PCA) pumps

- IV Administration Sets

- Accessories & Disposables

- Infusion Pumps

- By Application

- Anti-infective Therapy

- Parenteral Nutrition (TPN)

- Chemotherapy/Oncology

- Hydration Therapy

- Pain & Analgesia Management

- Endocrinology

- Other Applications

- By End User

- Home-care Settings

- Ambulatory Infusion Centers

- Hospital Out-patient Departments

- Specialty Pharmacies

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Our team interviewed infusion pharmacists, visiting nurses, payor case managers, and pump distributors across North America, Europe, and Asia-Pacific. These discussions clarified patient adherence patterns, real-world average selling prices, and uptake of portable pumps, letting us reconcile desk findings and refine regional weightings before final sign-off.

Desk Research

We first mapped demand drivers through publicly available datasets such as Centers for Medicare & Medicaid Services home-care claims, National Home Infusion Association utilization briefs, WHO Global Health Expenditure dashboards, and OECD chronic-disease prevalence tables. Regulatory filings on the US FDA 510(k) portal and European CE databases helped our analysts benchmark installed pump bases and average replacement cycles. Company 10-Ks, investor decks, and reputable trade press supplied price-movement clues and pipeline volumes, while D&B Hoovers provided cross-checks on leading service providers' revenue mix. This list is illustrative; dozens of additional open and paid feeds supported fact gathering and validation.

A second sweep focused on hard-to-source regional indicators, import duty schedules for elastomeric sets, home-health reimbursement bulletins, and customs shipment records processed through Volza, which grounded our starting values.

Market-Sizing & Forecasting

We begin with a top-down construct that rebuilds the eligible patient pool from chronic infection, oncology, and parenteral nutrition cohorts, applies therapy-specific penetration rates, and layers verified ASPs to reach 2025 revenue. Supplier roll-ups and sample pharmacy invoice checks serve as a bottom-up reasonableness screen. Key variables like Medicare Part B payment updates, shift in hospital-to-home discharge ratios, biologic share of oncology drugs, pump average life, and regional nurse visit frequency feed a multivariate regression that extends the series to 2030. Data gaps, such as unreported private-pay episodes, are bridged with conservative uplift factors endorsed during expert calls.

Data Validation & Update Cycle

We run variance scans against independent NHIA metrics, flag outliers, and circulate the model for peer review. Before every annual refresh, an analyst re-contacts three domain experts and updates exchange rates, ensuring clients receive the latest calibrated view.

Why Our Home Infusion Therapy Baseline Commands Reliability

Published estimates often diverge because firms select different service scopes, pricing ladders, and refresh cadences.

Key gap drivers include whether drug reimbursement outside North America is counted, if ambulatory center revenue is blended with home care, static versus dynamic ASP progressions, and the frequency with which chronic-disease incidence tables are re-benchmarked.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 25.99 B (2025) | Mordor Intelligence | - |

| USD 38.66 B (2024) | Global Consultancy A | Combines ambulatory and hospital-at-home services; relies on discharge data without pump price checks |

| USD 24.51 B (2024) | Research Publisher B | Excludes drug component in Asia; linear growth assumption; biennial refresh |

These contrasts show that Mordor's disciplined scope definition, dual-track patient and price modeling, and yearly update cadence deliver a balanced, transparent baseline that decision-makers can trace back to clearly documented variables and repeatable steps.

Key Questions Answered in the Report

What is the current value of the home infusion market?

The home infusion market is valued at USD 27.58 billion in 2026 and is projected to reach USD 37.12 billion by 2031.

Which product category generates the highest revenue?

Infusion pumps hold the largest share at 49.60% of 2025 revenue, with portable pumps expected to post the fastest 10.7% CAGR through 2031.

Which clinical application is growing the quickest?

Chemotherapy infusion is the fastest-expanding application, advancing at a 10.12% CAGR from 2026 to 2031 as oncology care shifts to outpatient and home settings.

How significant is home-care as an end-user segment?

Home-care settings account for 61.80% of 2025 revenue, reflecting both patient preference and payer incentives that reward care delivered outside hospitals.

Which region is forecast to grow the most rapidly?

Asia-Pacific is set to register the highest regional growth, increasing at a 8.74% CAGR between 2026 and 2031 due to rapid population aging and infrastructure investment.

Page last updated on: