Phosphoramidite Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.28 Billion |

| Market Size (2031) | USD 1.74 Billion |

| Growth Rate (2026 - 2031) | 6.34% CAGR |

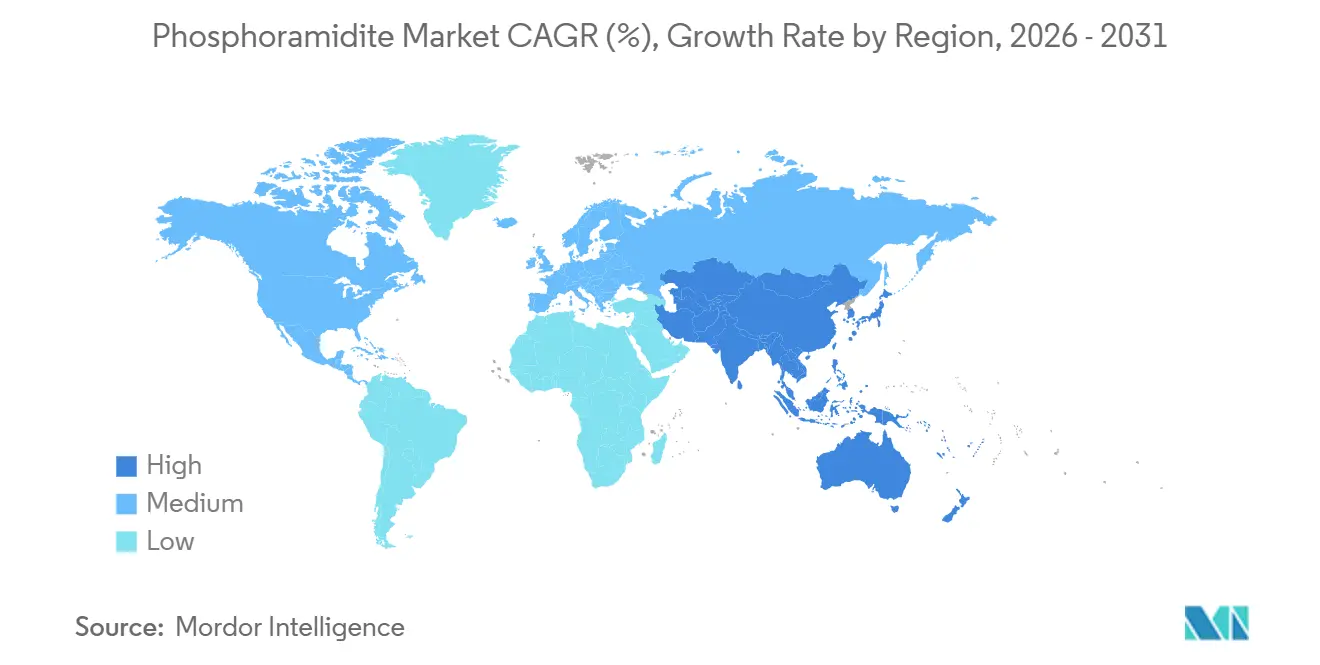

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Phosphoramidite Market Analysis by Mordor Intelligence

The Phosphoramidite Market size is expected to increase from USD 1.20 billion in 2025 to USD 1.28 billion in 2026 and reach USD 1.74 billion by 2031, growing at a CAGR of 6.34% over 2026-2031.

Driven by a sustained appetite for nucleic-acid therapeutics and a growing reliance on contract development and manufacturing organizations, the momentum is further fueled by the inaugural commercial deployments of enzymatic DNA (Deoxyribonucleic Acid)/RNA (Ribonucleic Acid) synthesis platforms. Regulatory clarity surrounding antisense oligonucleotides and small-interfering RNAs is not only shortening clinical timelines but also elevating the annual GMP (Good Manufacturing Practice)-grade amidite consumption per late-stage program to a range of 50-200 kg, thereby intensifying the demand for upstream reagents. Concerns over supply security are channeling additional capacity towards North America. At the same time, scale-ups in China and India, bolstered by subsidies, are heightening regional cost competition. In Europe, mandates on solvent recycling are steering manufacturers towards greener chemistries, effectively curbing hazardous waste and reducing input costs.

Key Report Takeaways

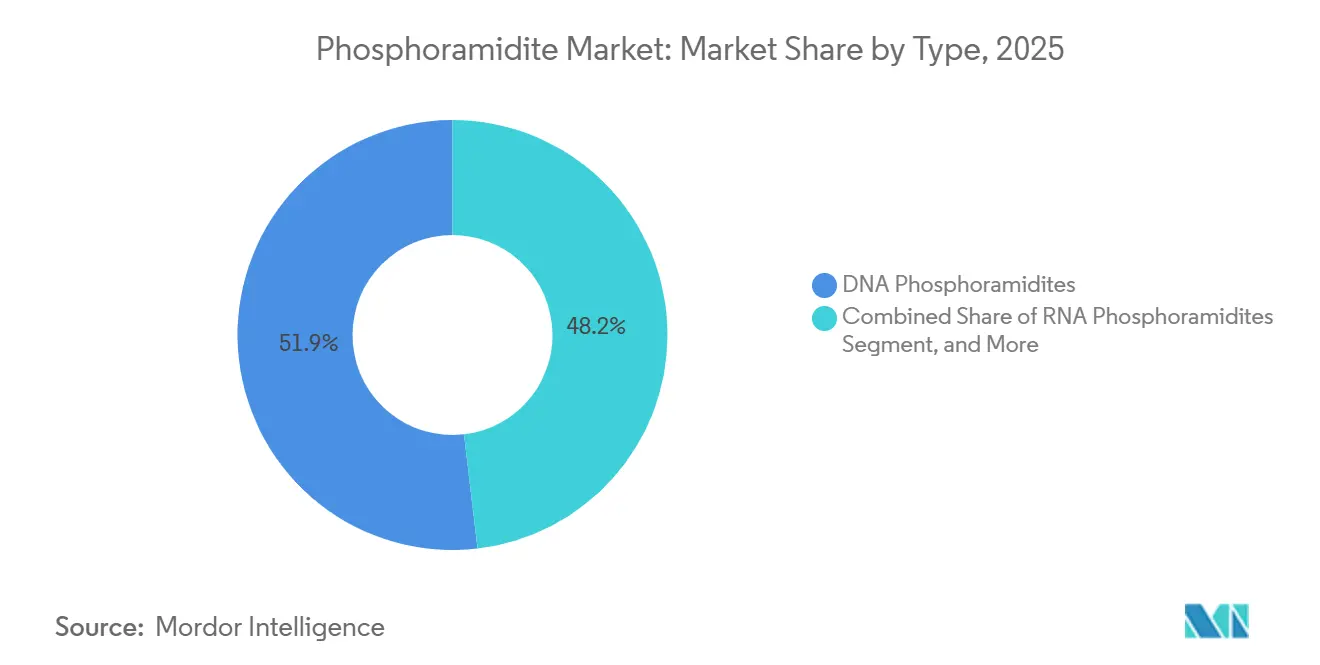

- By type, DNA phosphoramidites led with 51.85% share in 2025, while LNA phosphoramidites are poised to register an 8.21% CAGR through 2031.

- By end-user, pharmaceutical and biotechnology companies captured 56.74% of 2025 revenue, whereas CDMOs and CROs are set to expand at a 9.18% CAGR during 2026-2031.

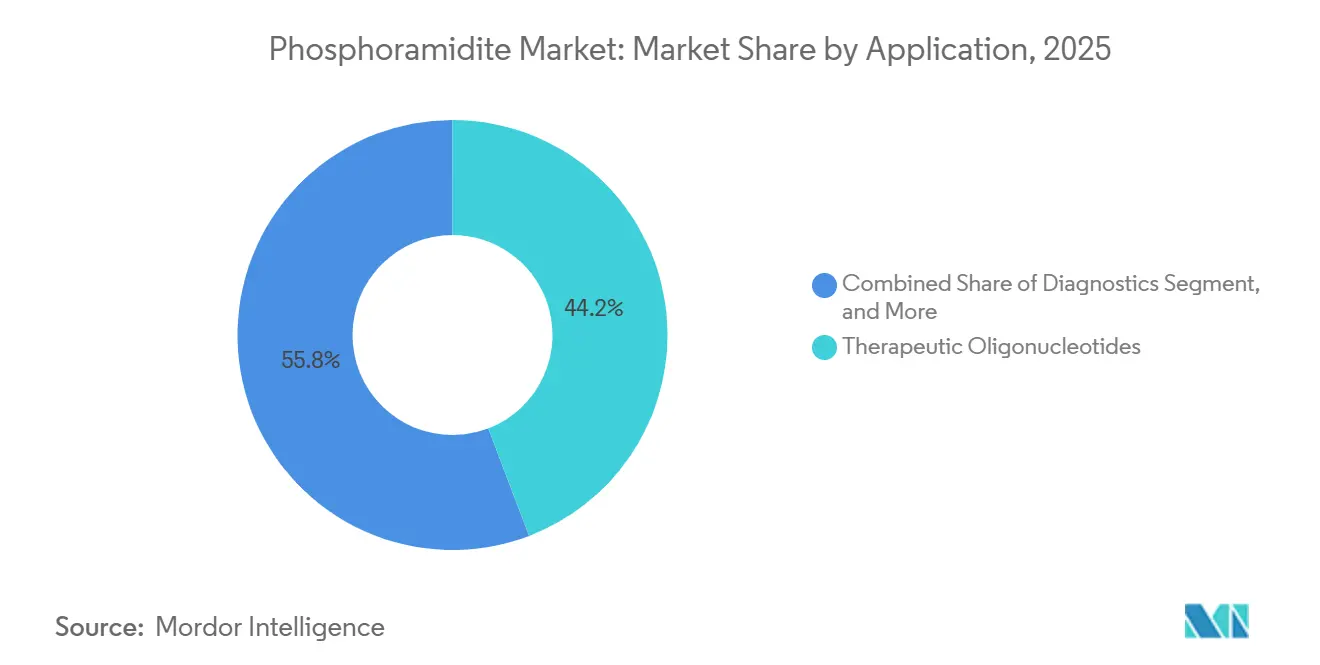

- By application, therapeutic oligonucleotides accounted for 44.20% of sales in 2025, while gene and cell therapy are projected to grow at a 9.31% CAGR over the forecast period.

- By purity grade, standard research grade accounted for 48.10% of 2025 demand, and GMP grade is forecast to grow at an 8.05% CAGR through 2031.

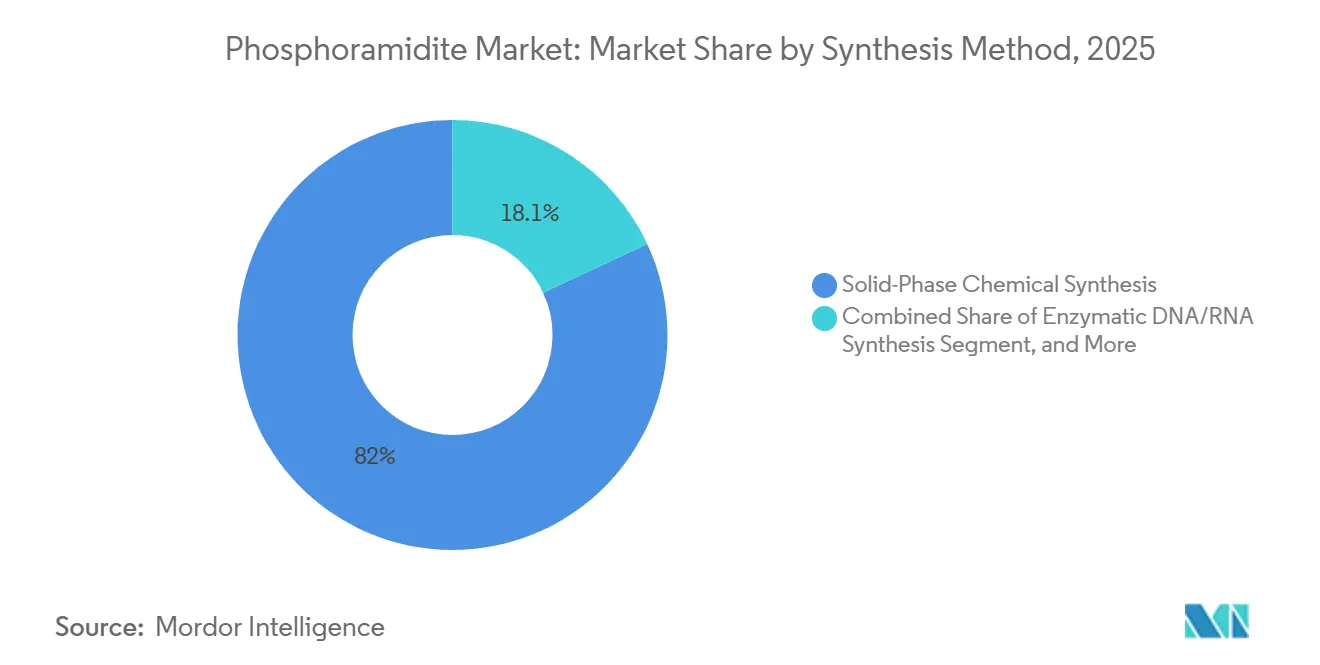

- By synthesis method, solid-phase chemical synthesis accounted for 81.95% in 2025, with enzymatic DNA/RNA synthesis expected to grow at a 7.86% CAGR through 2031.

- By production scale, research and discovery batches (<1 mmol) accounted for 63.75% of 2025 volume, while commercial-scale GMP manufacturing (>100 mmol) is projected to grow at an 8.72% CAGR.

- By geography, North America maintained a 39.78% share in 2025, and Asia-Pacific is anticipated to record a 7.29% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Phosphoramidite Market Trends and Insights

Driver Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rapid expansion of nucleic-acid therapeutics pipeline | +1.8% | Global, led by North America and Europe | Medium term (2–4 years) |

| Technological advances in high-throughput oligo synthesis | +1.2% | North America, Europe, Asia-Pacific hubs | Short term (≤ 2 years) |

| Government funding for genomic research | +0.9% | North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Growing personalized medicine & diagnostics demand | +1.1% | Global early adoption in North America, Western Europe | Medium term (2–4 years) |

| Hybrid enzymatic–chemical amidites enable new workflows | +0.7% | North America and Europe; Asia-Pacific scaling | Long term (≥ 4 years) |

| Green-chemistry solvent recycling incentives | +0.4% | Europe, North America, Asia-Pacific | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rapid Expansion of Nucleic-Acid Therapeutics Pipeline

In Q4 2024, the clinical development pipeline included 1,261 RNA-based therapies, a 23% increase from 2023. Notably, 87 candidates advanced to Phase 2 or 3 in 2024, each demanding multi-kilogram Good Manufacturing Practice (GMP) amidite volumes.[1]Advanced Research Projects Agency for Health, “FY 2025 Budget Allocation,” ARPA-H, arpa-h.gov The FDA's March 2024 approval of olezarsen, which leveraged locked nucleic acid (LNA) chemistry, sparked 18 new LNA initiatives within just 9 months. Updated insights on oligonucleotide clinical pharmacology, trimmed by about 4 months from Phase 1 durations, boosting reagent demand. Roche's expansive alliance with Ionis and Novartis' takeover of Chinook highlight big pharma's dedication to oligo modalities. Together, these late-stage initiatives are projected to drive an additional USD 40-60 million in phosphoramidite purchases through 2026.

Technological Advances in High-Throughput Oligo Synthesis

In December 2024, scientists at Michigan Technological University synthesized 1,728-mer oligonucleotides, breaking the previous ~200-mer barrier.[2]Hongene Biotech, “exNA Technology Licensing,” Hongene, hongene.com This advancement paves the way for direct assembly of messenger RNA (mRNA) strands, potentially reducing the cost of self-amplifying RNA vaccines by around 40%. Current high-density platforms have increased efficiency, processing 384-well plates in just six hours, three times faster than older columns. This acceleration is crucial for Clustered Regularly Interspaced Short Palindromic Repeats (CRISPR) screens, which often require up to 100,000 guides per run. The quicker cycles not only enhance cash conversion for Contract Development and Manufacturing Organizations (CDMOs) but also allow for minimum orders of 5-10 grams, making it easier for academic labs to access. With this expanded capability, the phosphoramidite market is poised to grow as longer, more intricate constructs become a staple in routine production runs.

Government Funding for Genomic Research

In FY 2025, the Advanced Research Projects Agency for Health (ARPA-H) allocated a substantial USD 1.5 billion for bolstering RNA-therapy infrastructure.[3]Advanced Research Projects Agency for Health, “FY 2025 Budget Allocation,” ARPA-H, arpa-h.gov Of this, a significant USD 320 million was directed towards strengthening the domestic amidite supply chain. Meanwhile, Australia's Genomics Health Futures Mission committed USD 335 million over a decade. In a parallel move, Horizon Europe dedicated USD 195 million specifically for oligonucleotides targeting rare diseases. On another front, China's 14th Five-Year Plan rolled out hefty subsidies of USD 390 million, aiming to boost local Active Pharmaceutical Ingredient (API) production and reduce reliance on imports by 2028. These strategic financial moves not only ease the path for new capacity expansions but also broaden the geographic sourcing landscape.

Growing Personalized Medicine & Diagnostics Demand

As of 2023, there are approximately 170 Food and Drug Administration (FDA) cleared or approved companion diagnostics (CDx), each utilizing 5-15 custom probe sets. Meanwhile, in January 2025, Medicare started reimbursing circulating tumor DNA tests. This move could elevate annual test volumes to an impressive 1.8 million by 2027. While therapeutic oligonucleotides (oligos) command a price of USD 800-1,200 per gram, diagnostic probes, priced between USD 150-250 per gram, necessitate a wider stock-keeping unit (SKU) range. This pricing strategy leads suppliers to maintain a stock of 120-150 amidite variants. Such a dual-track demand compels suppliers to adopt distinct supply-chain strategies, ensuring both high-margin, low-volume and moderate-margin, high-volume channels are well catered to.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High capital required for gmp-grade plants | -0.8% | Global; most acute in North America, Europe | Medium term (2–4 years) |

| Stringent raw-material purity regulations | -0.5% | North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Pfas-related solvent restrictions escalate compliance cost | -0.6% | North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Loss of exclusivity on key backbone-protection patents | -0.4% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Required for GMP-Grade Plants

A single greenfield plant expansion can exceed USD 725 million, as confirmed by Agilent’s 2025 announcement to double oligonucleotide output with operations commencing in 2026.[4]American Society of Gene & Cell Therapy, “RNA Therapy Pipeline Report Q4 2024,” ASGCT, asgct.org Build-out complexity spans reactor suites, solvent recovery systems, and Class C cleanrooms, while validation timelines stretch to multiple years. Smaller entrants often struggle to marshal comparable funding, which concentrates capacity among financially robust incumbents. Extended payback periods and the prospect of technology obsolescence amplify investment risk, thereby tempering market entry despite rising demand.

Stringent Raw-Material Purity Regulations

FDA guidance finalized in 2024 tightened limits on reactive and mutagenic impurities and introduced enhanced analytical-method validation for phosphoramidite suppliers. Meeting these specifications requires high-resolution mass spectrometry, dedicated segregated lines, and expanded documentation archives. Thermo Fisher’s multi-tier impurity classification exemplifies the level of detail now expected. Compliance investments raise operational costs and extend release timelines, especially for enterprises operating across jurisdictions still lacking harmonized standards.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: LNA Modifications Command Therapeutic Premium

DNA phosphoramidites held 51.85% of the phosphoramidite market share in 2025 and continue anchoring the phosphoramidite market thanks to their central role in antisense and diagnostic probe synthesis. LNA subtypes, while representing a smaller base, are forecast to outpace other chemistries at an 8.21% CAGR amid rising in vivo stability needs. The phosphoramidite market size for DNA-based variants is projected to expand steadily as multi-kilogram oncology and cardiology drug campaigns enter late-stage trials. Continued academic demand plus new CRISPR guide-RNA workflows sustain RNA amidite volume, whereas specialty modifications such as 2'-O-methyl and thiophosphate command premium pricing niches.

Advances in multi-modification strategies, exemplified by the 1,3-dithian-2-yl-methoxycarbonyl method for acylated bases, are broadening design possibilities for combination therapies. Enzymatic ligation-based construction methods trialed by several biotech firms complement, rather than compete with, chemical DNA amidites, particularly for highly modified backbones.

By End-User: CDMOs Capture Outsourcing Wave

Pharmaceutical and biotechnology enterprises consumed 56.74% of the phosphoramidite market in 2025, driven by expanding therapeutic pipelines and vertically integrated manufacturing ambitions. Outsourcing trends nonetheless propel CDMOs and CROs, whose 9.18% CAGR marks the fastest uptake in the forecast horizon. WuXi STA’s 27 operational oligonucleotide lines and TriLink’s CleanCap licensing model attest to brisk service demand. Academic institutions preserve a meaningful baseline volume, while diagnostic labs increasingly order high-purity lots for regulated test kits.

By Application: Gene Therapy Drives Specification Complexity

Therapeutic oligonucleotides generated 44.20% of phosphoramidite market revenue in 2025, and pipeline momentum suggests continued leadership. Companion diagnostics and sequencing workflows in the diagnostics arena secure steady consumption rates, whereas gene and cell therapy, boosted by CRISPR-enabled ex vivo editing, record the fastest 9.31% CAGR. The phosphoramidite market size tied to viral-vector guide RNAs is set to expand sharply once larger patient pools enter pivotal trials.

By Purity Grade: Research Grade Leads Volume

Research grade accounted for 48.10% of 2025 shipments and remains the highest-volume tier because exploratory projects consume numerous sequences at modest purity thresholds. GMP-grade demand grows faster at an 8.05% CAGR as commercial launches and later-stage trials increase. Thermo Fisher’s TheraPure catalog, offering sub-0.20% reactive impurity levels, exemplifies the premium positioning that secures pricing power.

By Synthesis Method: Chemical Synthesis Maintains Dominance

In 2025, solid-phase chemistry dominated the market, capturing an 81.95% share, supported by coupling efficiencies of 99% or higher and integrated production assets. Resonant acoustic mixing reduced solvent usage by 90% while maintaining yields between 63% and 92%. Enzymatic constructs are growing at a compound annual growth rate (CAGR) of 7.86%, but their limited scale and product-purity challenges keep them in a supplementary role. Hybrid protocols are expected to provide a balanced approach, combining the specificity of chemical methods with the sustainability benefits of enzymatic processes.

By Production Scale: Research Scale Dominates Volume

Batches below 1 mmol made up 63.75% of 2025 shipments, mirroring the fragmented nature of early discovery. Commercial-scale lots above 100 mmol surge at 8.72% CAGR as approved drugs ramp volumes. Agilent’s and BioSpring’s large-scale projects underscore a maturing landscape in which few certified suppliers manage clinical-to-commercial transitions.

Geography Analysis

North America posted 39.78% revenue share in 2025, underpinned by established regulatory clarity, large developer presence, and significant venture-capital flows. Merck KGaA’s USD 76 million upgrade of its Missouri bioconjugation site illustrates sustained capital deepening within the region. The United States also leads in CleanCap-enabled mRNA technologies through TriLink’s licensing ecosystem, reinforcing domestic innovation clusters.

Asia-Pacific is forecast to grow at 7.29% CAGR through 2031, propelled by lower production costs and rising internal demand for advanced therapies. WuXi STA’s 169-acre Taixing facility, operational since early 2024, exemplifies the scale domestic CDMOs are reaching. Policy shifts encouraging “China-plus-many” sourcing, combined with updated anti-espionage regulations, are prompting multinational firms to diversify across India, Vietnam, and Thailand, reshaping supply-chain geography.

Europe maintains a strategic foothold through advanced manufacturing and rigorous quality norms. BioSpring’s Offenbach RNA megafacility, on track for completion in 2027, will be among the world’s largest dedicated nucleic-acid plants, underscoring regional commitment to high-value biologics. Coupled with the European Pharma Oligonucleotide Consortium’s harmonization work, the continent remains a reference point for manufacturing excellence and green-chemistry adoption.

Competitive Landscape

The phosphoramidite industry shows moderate concentration. Thermo Fisher Scientific, Danaher’s Integrated DNA Technologies, and Merck KGaA leverage vertical integration from raw materials to final oligonucleotide services. Their scale affords cost advantages, global logistics reach, and robust compliance infrastructures. Niche specialists such as Glen Research and Biosynth differentiate on customized modifications and rapid small-batch fulfillment.

Strategic licensing, notably TriLink’s CleanCap accord with Lonza, expands addressable markets for mRNA capping while embedding proprietary technology within broader drug-substance services. Sustainability initiatives, including solvent-recycling loops and energy-efficient reactor systems, are emerging competitive levers as clients seek lower environmental footprints. While enzymatic synthesis poses a long-term competitive variable, current throughput and impurity limitations preserve chemical incumbents’ advantages.

Phosphoramidite Industry Leaders

TriLink BioTechnologies

Bioneer Corporation

Thermo Fisher Scientific Inc.

Biosynth Ltd

Hongene Biotech Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Luxna Biotech Co., Ltd. and Inabata & Co., Ltd. have entered into a licensing agreement, granting Inabata the rights to manufacture and commercialize the modified nucleic acid GuNA amidite. This agreement establishes a strategic partnership, leveraging Inabata's robust global sales network and expertise in developing new market opportunities, alongside Luxna's innovative modified nucleic acid technology.

- November 2025: Kolon Life Science unveiled a structurally modified phosphoramidite for RNA therapeutics during TIDES Europe 2025, expanding its RNA polymer drug portfolio in Korea.

- August 2025: Hongene licensed exNA technology from UMass Chan Medical School, enabling backbone-modified oligonucleotides that rely on advanced phosphoramidite chemistry.

- February 2025: Agilent Technologies began shipments from its USD 725 million Frederick, Colorado expansion, signing five-year GMP supply deals with three pharma sponsors.

Global Phosphoramidite Market Report Scope

Phosphoramidites are modified nucleosides and are a standard chemical utilized in modern DNA synthesis. Phosphoramidites permit the sequential addition of new bases to the DNA chain in an exquisitely simple and exceptionally efficient cyclic reaction.

The phosphoramidite market is segmented by type, end-user, and geography. By type, the market is segmented into DNA phosphoramidites, RNA phosphoramidites, and other phosphoramidites. By end-user, the market is segmented into pharmaceutical and biotechnology companies, academic and research institutes, and other end users. The report also covers the market sizes and forecasts for the phosphoramidite market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| DNA Phosphoramidites |

| RNA Phosphoramidites |

| LNA Phosphoramidites |

| 2'-O-Methyl RNA Phosphoramidites |

| Specialty / Modified Phosphoramidites |

| Pharmaceutical & Biotechnology Companies |

| Academic & Research Institutes |

| CDMOs & CROs |

| Diagnostic Laboratories |

| Other End-Users |

| Therapeutic Oligonucleotides |

| Diagnostics |

| Gene & Cell Therapy |

| Synthetic Biology & Gene Editing |

| Research Tools |

| Standard Research Grade |

| HPLC Grade |

| GMP Grade |

| Ultra-High Purity Grade |

| Solid-Phase Chemical Synthesis |

| Enzymatic DNA/RNA Synthesis |

| Hybrid Chemical-Enzymatic |

| Research/Discovery Scale (<1 mmol) |

| Pilot/Clinical Scale (1-100 mmol) |

| Commercial / GMP Manufacturing Scale (>100 mmol) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Type | DNA Phosphoramidites | |

| RNA Phosphoramidites | ||

| LNA Phosphoramidites | ||

| 2'-O-Methyl RNA Phosphoramidites | ||

| Specialty / Modified Phosphoramidites | ||

| By End-User | Pharmaceutical & Biotechnology Companies | |

| Academic & Research Institutes | ||

| CDMOs & CROs | ||

| Diagnostic Laboratories | ||

| Other End-Users | ||

| By Application | Therapeutic Oligonucleotides | |

| Diagnostics | ||

| Gene & Cell Therapy | ||

| Synthetic Biology & Gene Editing | ||

| Research Tools | ||

| By Purity Grade | Standard Research Grade | |

| HPLC Grade | ||

| GMP Grade | ||

| Ultra-High Purity Grade | ||

| By Synthesis Method | Solid-Phase Chemical Synthesis | |

| Enzymatic DNA/RNA Synthesis | ||

| Hybrid Chemical-Enzymatic | ||

| By Production Scale | Research/Discovery Scale (<1 mmol) | |

| Pilot/Clinical Scale (1-100 mmol) | ||

| Commercial / GMP Manufacturing Scale (>100 mmol) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the phosphoramidite market in 2026?

The phosphoramidite market size is USD 1.28 billion in 2026.

What is the expected growth rate through 2031?

Forecast CAGR is 6.34% through 2031.

Which application consumes the most phosphoramidites?

Therapeutic oligonucleotides account for 44.20% of 2025 revenue.

Which region is expanding fastest?

Asia-Pacific is projected to grow at 7.29% CAGR to 2031.

What is driving demand from CDMOs?

Outsourcing of complex oligonucleotide manufacturing is pushing CDMO/CRO demand at 9.18% CAGR.

How are suppliers addressing environmental concerns?

Firms are adopting solvent-reduction technologies such as resonant acoustic mixing, cutting solvent volumes by 90%.

Page last updated on: