Global Biophotonics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

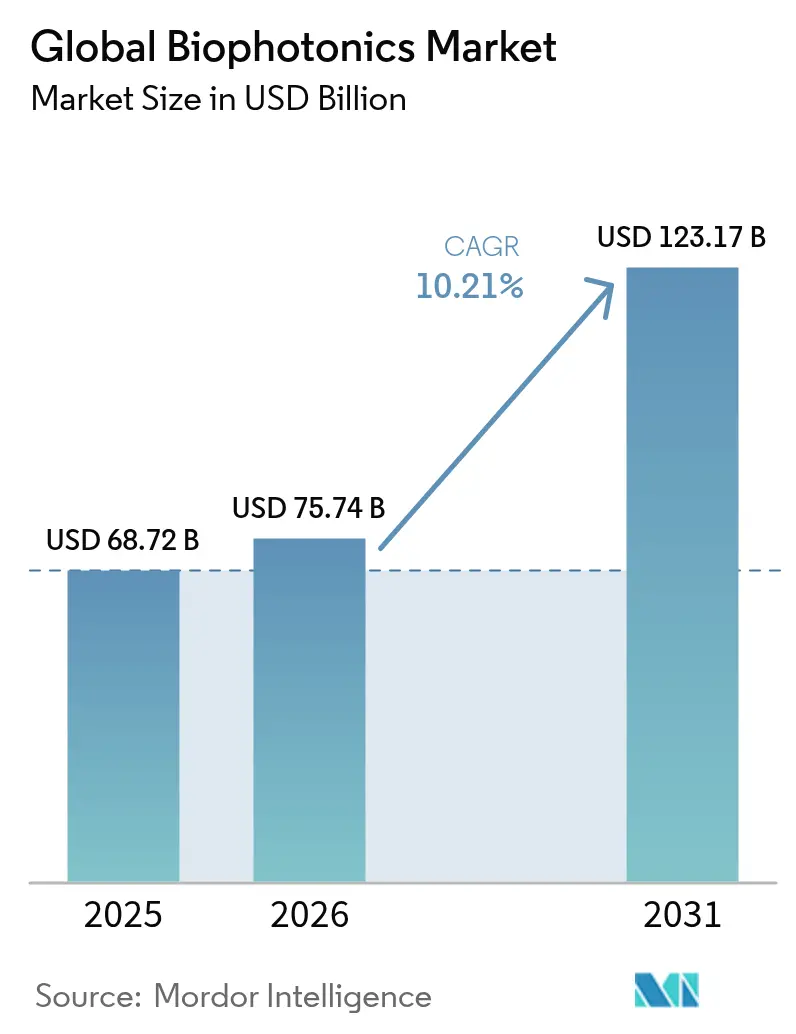

| Market Size (2026) | USD 75.74 Billion |

| Market Size (2031) | USD 123.17 Billion |

| Growth Rate (2026 - 2031) | 10.21% CAGR |

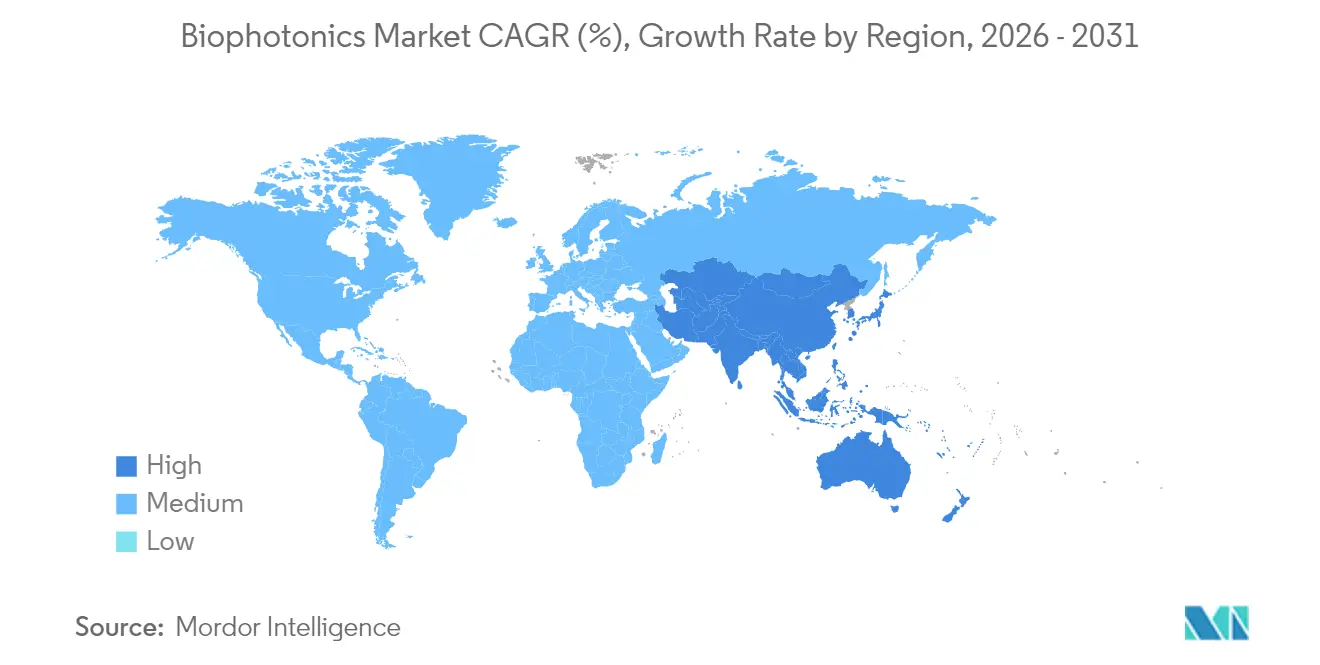

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

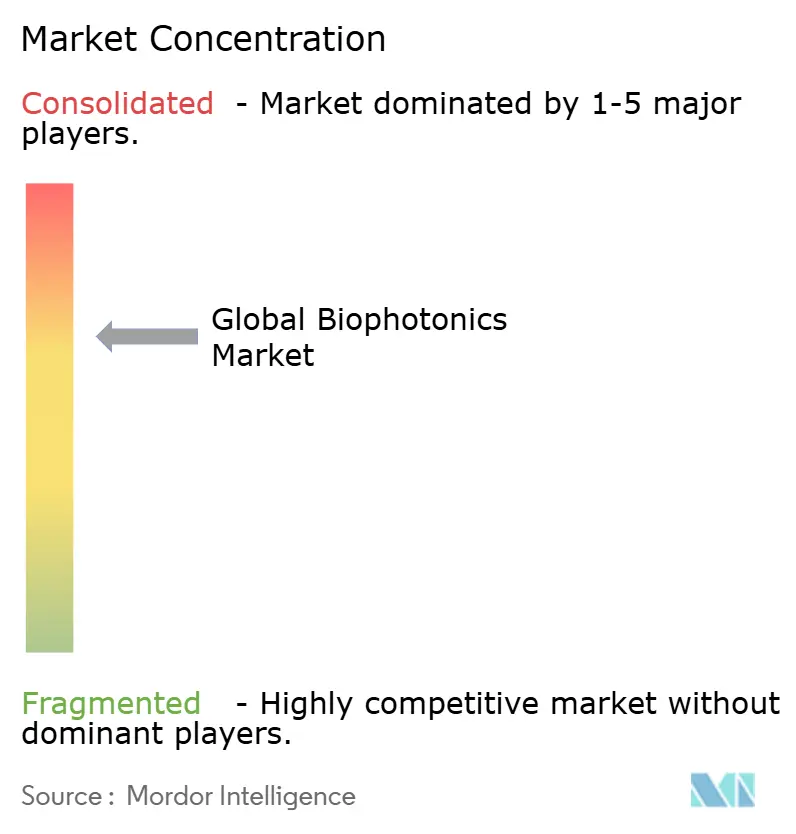

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Biophotonics Market Analysis by Mordor Intelligence

Biophotonics market size in 2026 is estimated at USD 75.74 billion, growing from 2025 value of USD 68.72 billion with 2031 projections showing USD 123.17 billion, growing at 10.21% CAGR over 2026-2031. Strong growth stems from the convergence of artificial intelligence with optical technologies, where AI-enabled spectroscopy delivers 98.8% accuracy in non-invasive glucose monitoring. Nanotechnology paired with photoacoustic tomography now supports real-time stroke assessment, signaling a shift beyond conventional imaging toward precision therapeutic guidance. Asia-Pacific records the fastest expansion as China’s USD 4.17 billion 2024 investment in biomanufacturing and Japan’s USD 307 million program in optical chips build regional momentum. Lasers hold the leading product position due to precision surgical adoption, while imaging systems outpace other product groups through 2030. Hospitals continue to anchor demand, yet academic institutes move quickly as governments prioritize R&D initiatives.

Key Report Takeaways

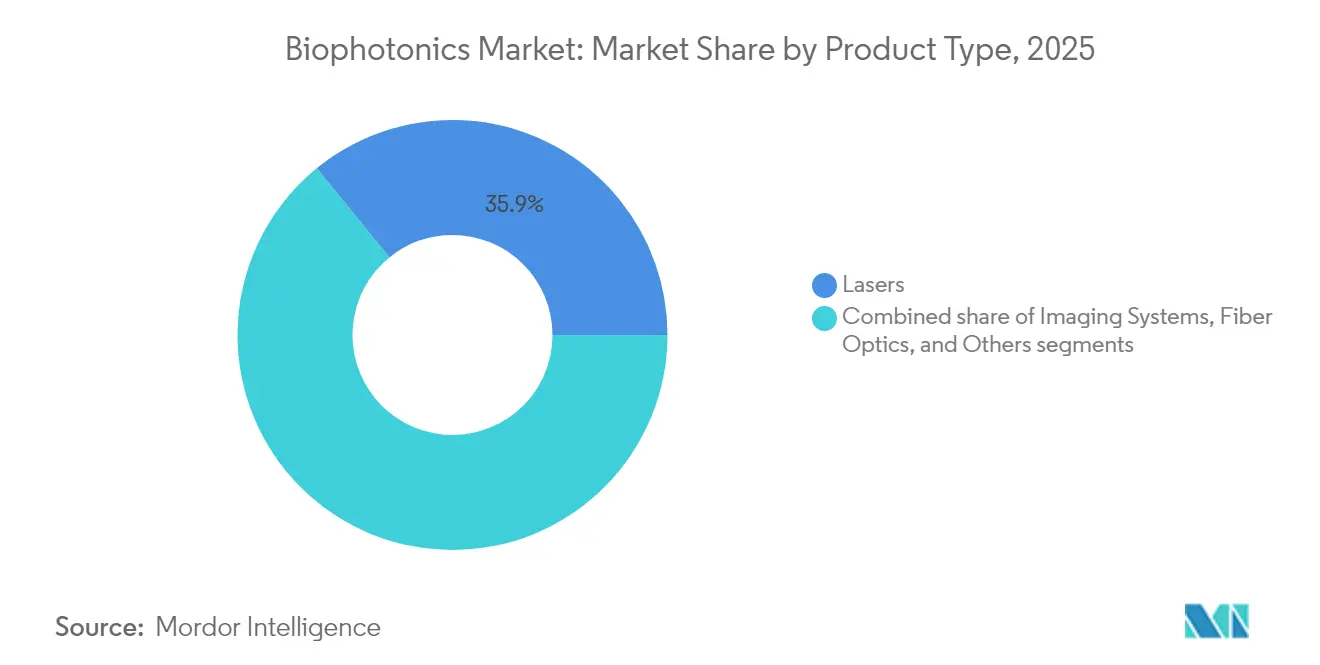

- By product type, lasers led with 35.88% of biophotonics market share in 2025, while imaging systems are projected to post an 11.23% CAGR through 2031.

- By technology, in-vitro platforms accounted for 60.92% of the biophotonics market size in 2025; in-vivo systems are forecast to advance at a 10.62% CAGR to 2031.

- By application, medical diagnostics retained 55.21% share of the biophotonics market size in 2025, whereas biosensors are on track for a 11.69% CAGR to 2031.

- By usage, hospitals and clinics commanded 51.74% share in 2025; academic and research institutes are set to expand at a 11.78% CAGR through 2031.

- By geography, North America led with 37.10% of biophotonics market share in 2025, while Asia-Pacific is projected to record the fastest 10.96% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Biophotonics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing use of biophotonics in diagnostics | +2.1% | Global, led by Asia-Pacific adoption | Medium term (2-4 years) |

| AI-enabled spectroscopy for rapid PoC testing | +1.9% | Global, accelerated in Asia-Pacific | Short term (≤ 2 years) |

| Growing geriatric population | +1.8% | Global, concentrated in North America & Europe | Long term (≥ 4 years) |

| Emergence of nanotechnology in biophotonics | +1.5% | North America & EU research hubs | Medium term (2-4 years) |

| Advancements in photo-acoustic tomography (PAT) | +1.2% | Global, clinical validation in developed markets | Short term (≤ 2 years) |

| Precision-agriculture demand for biophotonic sensors | +0.8% | Global, emerging markets focus | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Use of Biophotonics in Diagnostics

Surface-enhanced Raman spectroscopy improved with machine learning reaches 87% balanced accuracy[1]Ben Cox, “A Multibeam Fabry–Perot Scanner Enables High-Speed Clinical Photoacoustic Tomography,” Nature Biomedical Engineering, nature.com for head and neck cancer detection using ear wax samples. Photoacoustic tomography supplies real-time vascular monitoring during stroke treatment. Smartphone spectrometers delivering 1 nm resolution across 440–1,300 nm open field diagnostics. The FDA created Class II special controls for near-infrared hematoma detectors, validating optical approaches. Integration with 6G networks offers ultra-low latency transmission for instant clinical decisions.

Growing Geriatric Population

Individuals aged 65 plus require three to four times more diagnostic procedures than younger cohorts, elevating long-term demand. Near-infrared spectroscopy enables continuous glucose monitoring[2]Na Kyung Lee, “Status and Trends of the Digital Healthcare Industry,” Healthcare Informatics Research, e-hir.org, addressing 537 million diabetes cases. Autofluorescence imaging secures 97% tumor-free margins in oral cancer surgery. Photobiomodulation supports Alzheimer’s management. Aging trends align with precision medicine to sustain biophotonic platform adoption.

Emergence of Nanotechnology in Biophotonics

Persistent luminescence nanoparticles deliver simultaneous imaging and targeted therapy. Quantum dots improve near-infrared imaging through reduced scattering. Metasurface biosensors heighten viral detection sensitivity. Enzyme-responsive nanomedicines activate near-infrared-II photoacoustic imaging for cascade-enhanced radiotherapy. Atomic force microscopy paired with AI detects oral cancer at nanoscale resolution.

Advancements in Photo-acoustic Tomography (PAT)

All-optical 3D PAT scanners now create detailed vascular images within seconds. Transcranial imaging benefits from homogeneous skull modeling. Low-cost multichannel acquisitions achieve 46.10 dB signal-to-noise ratios. Temporal encoding merges PAT with fluorescence data. Implicit neural representation tackles sparse-view limitations in dynamic reconstruction.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of awareness & skilled personnel | -1.4% | Global, acute in emerging markets | Medium term (2-4 years) |

| High cost of biophotonic systems | -1.1% | Price-sensitive markets, developing regions | Short term (≤ 2 years) |

| Stringent reimbursement frameworks | -0.9% | North America & Europe | Long term (≥ 4 years) |

| Rare-earth supply risk for laser diodes | -0.7% | Global manufacturing, Asia-Pacific production | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Lack of Awareness & Skilled Personnel

Interdisciplinary expertise gaps slow adoption because staff must unite optics, biology, and data science skills. Clinicians unfamiliar with optical diagnostics hesitate to integrate new tools. Universities struggle to offer targeted curricula, limiting ready talent. Regulatory navigation adds complexity. Dedicated laboratories at the University of Central Florida reflect early institutional responses.

High Cost of Biophotonic Systems

Clinical photoacoustic units often exceed a USD 500,000 tag, restricting purchases to well-funded centers. Rare-earth supply risks inflate laser prices. Limited Medicare reimbursement narrows hospital budgets. Specialized maintenance pushes lifetime ownership costs higher. Portable spectrometers promise lower prices yet lack clinical-grade precision.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Imaging Systems Drive Innovation

Lasers contributed 35.88% to the biophotonics market share in 2025, reflecting their role in precise photodynamic therapy and surgical work. Imaging systems are forecast to register an 11.23% CAGR, the highest among products, as surgeons seek real-time tissue characterization during operations. Fiber optics benefit from miniaturization trends, powering wearable biosensors. Hybrid quantum sensing improves single-molecule detection. Carl Zeiss consolidated capabilities by forming photonics business units. Manufacturers invest in automated lines to curb costs and meet growing volume. Greater component standardization speeds device certification. Collaborative R&D between optics firms and AI start-ups accelerates platform convergences. Environmental monitoring devices reuse core imaging modules, widening the addressable demand across agriculture and water safety.

Market participants refine beam quality and pulse stability to support emerging photoimmunotherapy protocols. Component vendors expand gallium arsenide wafer capacity for higher-power diode lasers. Imaging system suppliers integrate cloud-based analytics to cut interpretation time. The combined effect sustains product leadership while anchoring the broader biophotonics market.

By Technology: In-Vivo Applications Accelerate

In-vitro platforms maintained 60.92% of the biophotonics market size in 2025, thanks to established lab workflows. In-vivo systems are predicted to rise at a 10.62% CAGR as clinicians favor minimally invasive surgical guidance systems that provide real-time tissue assessment without specimen removal. Photoacoustic tomography now visualizes cerebral vessels through intact skulls. Optical guidance achieves 100% diagnostic success in single-insertion brain biopsies. Regulatory agencies outline streamlined pathways for real-time devices, aiding commercialization. Wearable monitors connect to IoT networks for continuous data feeds. Energy-efficient light sources extend device operating times. Hospitals integrate in vivo outputs into electronic health records, enhancing longitudinal care. Start-ups target ambulatory surgery centers with compact consoles. Emerging transdermal probes enable metabolic tracking, reinforcing expansion prospects for the biophotonics market.

By Application: Biosensors Transform Diagnostics

Analytics sensing held 29.96% share in 2025, bolstered by spectroscopic chemistry analysis. Biosensors will grow at a 11.69% CAGR as AI improves single-cell detection. Surface-enhanced Raman spectroscopy identifies drug concentrations down to 10 pg/mL. Optical coherence tomography moves into dermatology and cardiology. Light therapy gains recognition for Alzheimer’s care. Microscopy surpasses diffraction limits in live-cell imaging. Short-wave infrared see-through imaging assists surgeons. New polymer substrates reduce sensor cost, encouraging point-of-care deployment. Agricultural biosensors monitor soil nitrates, underscoring non-medical potential within the biophotonics market.

By Usage: Medical Diagnostics Maintain Dominance

Medical diagnostics accounted for 55.21% of the biophotonics market size in 2025 and will progress at a 10.41% CAGR. AI-powered research data platforms integrate clinical datasets for personalized care. Photodynamic therapy provides targeted cancer management with fewer systemic effects. Portable spectrometers support disease screening in remote areas. Food quality testing uses spatially offset Raman to detect honey fraud with 99% accuracy. Industry-specific software reduces analysis time, supporting wider uptake. Hospitals adopt leasing models to offset up-front costs. Telemedicine programs deploy handheld devices, reinforcing global demand for the biophotonics market.

By End-User: Academic Institutes Drive Innovation

Hospitals and clinics dominated with 51.74% share in 2025, favored by structured procurement and evidence needs. Academic and research institutes will expand at a 11.78% CAGR as national funds target photonics. Biopharma companies channel USD 2.5 billion into AI-mediated discovery. Food laboratories broaden optical testing amid stricter safety rules. Environmental agencies add fiber-optic probes for water-quality assessments. The University of Central Florida launched a dedicated lab to improve fiber-optic epidural placement. Collaborative hubs couple laser designers with neuroscientists, expediting translational research. Venture capital flows toward campus spin-offs that leverage open-source algorithms. Academic discoveries continue feeding product pipelines across the biophotonics market.

Geography Analysis

North America commanded 37.10% of biophotonics market share in 2025, supported by a mature healthcare system and an FDA framework that now classifies radiological optimization systems under Class II for faster clearance. Thermo Fisher allocated USD 2 billion for domestic expansion, reinforcing analytical instrument supply. Medicare reimbursement gaps limit some diagnostic rollouts. Specialist centers gain coverage for optical cervical screening, sustaining demand. Research grants underpin AI-photonics convergence, while the region’s rare-earth policies aim to secure laser diode inputs. Competition intensifies as start-ups commercialize handheld imaging, adding depth to the biophotonics market.

Europe posts a steady 9.87% CAGR, driven by a EUR 124.6 billion photonics ecosystem. Carl Zeiss advances ophthalmic portfolios by absorbing DORC and investing 15% of revenue back into R&D. The Medical Device Regulation harmonizes standards yet raises compliance costs for small firms. Horizon Europe funding prioritizes precision agriculture, lifting uptake of optical sensors. Cross-border academic consortia enhance technology validation, aligning with regional sustainability goals. Semiconductor laboratories in Dresden accelerate industrial microscopy solutions, extending market depth.

Asia-Pacific is the fastest-growing region at 10.96% CAGR. China leads with a USD 4.17 billion biomanufacturing infusion in 2024. Pilot photonic chip lines in Shanghai Jiao Tong University boost AI and quantum applications. Japan’s USD 307 million optical chip program seeks semiconductor leadership. India invests in quantum photonics despite infrastructure gaps. Local firms emphasize low-cost laser sources to satisfy price-sensitive healthcare providers. Government incentives lower import taxes on diagnostic optics, while telehealth efforts spread mobile spectrometers to underserved zones. Rapid clinic construction across Southeast Asia accelerates demand, supporting expansion of the biophotonics market.

Regulatory Landscape

Biophotonic systems used for diagnosis and therapy are regulated as medical devices, with requirements focused on clinical performance evidence, risk management, and electrical safety for light-emitting equipment. In the United States, the FDA has maintained a stringent stance for certain optical device categories, keeping diagnostic endoscopic light source systems (Product Code OAY) in Class III as of March 2026. This reinforces the need for robust clinical evidence and well-defined special controls before any reclassification discussions.

In Europe, Regulation (EU) 2017/745 (MDR) continues to frame market access, linking conformity assessment to harmonised standards and technical documentation. The European Commission published Implementing Decision (EU) 2026/1231 in June 2026, updating harmonised standards supporting MDR, including medical electrical equipment standards such as EN 60601-1:2006/A13:2024. Standards activity also affects product design and verification, as BS EN IEC 60601-2-57:2026 adds specific safety and essential performance requirements for non-laser light source equipment (200 nm to 3000 nm) used across diagnostic and therapeutic use cases.

Value Chain Analysis

The biophotonics value chain begins with upstream materials and components such as laser diodes, detectors, filters, fibers, precision optics, and semiconductor-based photonic elements. These are then integrated into imaging systems, spectroscopy platforms, OCT, microscopy, and light-therapy systems. Midstream players combine optoelectronics with embedded software and increasingly AI-enabled analytics, and they validate performance through preclinical and clinical studies to meet medical-device requirements, before distributing via direct sales to hospitals and clinics, channel partners for laboratories, and system integrators serving academic and research institutes.

Downstream adoption depends on workflow completeness and service coverage, not only hardware delivery. That has supported more partnering and portfolio integration, including Bruker acquiring NanoString Technologies in May 2024 to add spatial biology and single-molecule fluorescence imaging capabilities to its instrument portfolio. It also includes Carl Zeiss Meditec partnering with the Singapore Eye Research Institute in November 2024 to advance OCT and ophthalmic imaging. Supply continuity and cost remain sensitive to specialized photonic components, including rare-earth-linked inputs used in certain laser systems, so multi-sourcing, localized manufacturing clusters, and tighter supplier relationships are central to execution for high-value clinical photoacoustic and imaging platforms.

Competitive Landscape

Market consolidation is moderate. Thermo Fisher pledged USD 50 billion for acquisitions and has already spent USD 4.1 billion on Solventum to deepen analytical capabilities. Carl Zeiss created dedicated photonics units and completed the DORC purchase to enhance ophthalmic integration. Becton Dickinson separated bioscience and diagnostic lines and acquired Edwards Lifesciences Critical Care for USD 4.2 billion. White-space growth appears in precision agriculture, where photonic sensors expand faster than clinical segments.

Patent activity in quantum sensing and metasurfaces signals a shift toward fundamental optical control. Vertical integration secures laser diode supply, countering rare-earth volatility. Smartphone-grade spectrometers achieve laboratory-equivalent performance, allowing new entrants without fabrication facilities.

Partnerships between optics giants and cloud AI providers accelerate algorithm deployment. The competitive narrative centers on integrated hardware-software ecosystems, reinforcing strategic depth across the biophotonics market.

Global Biophotonics Industry Leaders

Carl Zeiss AG

Danaher Corporation

Hamamatsu Photonics KK

Olympus Corporation

Thermo Fisher Scientific Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Opportunities center on use cases where biophotonic hardware, AI analytics, and workflow integration reduce time-to-result and support advanced imaging for point-of-care and intraoperative decision-making. Actions taken in 2026 reinforce this direction: ZEISS partnered with EDGE Biotechnologies in April 2026 to integrate AI-accelerated quantitative image analysis assays for biopharma R&D, and Hamamatsu Photonics expanded digital pathology workflow collaborations in May 2026 around deploying multiple whole slide imaging systems in an academic medical setting. These steps point to whitespace for end-to-end solutions that combine sample preparation, imaging, and analysis within a validated workflow, rather than standalone devices.

Therapeutics and oncology-linked biophotonics also show formal development pathways that can widen the addressable scope of light-based platforms. Immunophotonics received a China patent in June 2026 covering use of its IP-001 platform in combination with checkpoint inhibitors for solid tumors, while Guided Therapeutics submitted a PMA clinical report to the US FDA in June 2026 for its LuViva Advanced Cervical Scan. In parallel, miniaturized sensors for point-of-care testing and Raman-enabled surgical guidance remain commercialization targets, with scaling tied to clinical evidence generation, reimbursement fit, and component cost management for advanced clinical photoacoustic platforms that can exceed USD 500,000 in capital price points.

Recent Industry Developments

- May 2026: Carl Zeiss AG partnered with EDGE Biotechnologies to integrate AI-accelerated, end-to-end quantitative image analysis assays for biopharma R&D workflows. The collaboration supports tighter coupling of imaging hardware with analysis software, helping labs standardize and scale complex assay readouts across discovery and translational research pipelines.

- May 2026: Hamamatsu Photonics K.K. launched a digital pathology workflow collaboration with the Keck School of Medicine of USC that included installation of multiple NanoZoomer systems. The collaboration strengthens adoption of whole slide imaging in clinical-academic settings and expands demand for integrated scanning, data handling, and pathology workflow modernization.

- October 2024: Carl Zeiss opened a semiconductor applications laboratory in the Dresden Innovation Hub to automate microscopy workflows. The facility adds applied development and demonstration capacity that supports higher-throughput microscopy and inspection-like automation approaches that transfer into life-science imaging workflows.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the biophotonics market covers light-based tools and systems designed to interact with biological material for research, medical diagnosis, and therapy, including the supporting hardware and consumables used with these systems.

Scope exclusions: We exclude optical products mainly built for telecom or industrial inspection where there is no intended biological interface.

Segmentation Overview

- By Product Type

- Imaging Systems

- Lasers

- Fiber Optics

- Others

- By Technology

- In-Vitro

- In-Vivo

- By Application

- Surface Imaging

- Inside Imaging

- See-through Imaging

- Microscopy

- Biosensors

- Analytics Sensing

- Spectromolecular

- Light Therapy

- Optical Coherence Tomography

- By Usage

- Tests and Components

- Medical Therapeutics

- Medical Diagnostics

- Non-Medical Application

- By End-User

- Hospitals & Clinics

- Academic & Research Institutes

- Biotechnology & Pharma Companies

- Food-Quality Labs

- Other End-Users

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by building a clear picture of where biophotonics demand is coming from and how it is funded, before we size anything. We use public sources such as the US FDA device databases, National Institutes of Health (NIH) funding award data, the World Health Organization (WHO) health indicators, and OECD health statistics to understand adoption pace across diagnostics and therapy.

On the supply and innovation side, we refer to sources such as USPTO and WIPO patent databases, peer-reviewed optics and biomedical journals, and national statistics portals for trade and production indicators when relevant. Company filings, annual reports, and investor decks are used to understand product mix and regional exposure. A paid subscription for company financials and patent intelligence is used selectively to standardize disclosures and track technology families. This desk list is not exhaustive, and many other public sources were used to collect, cross-check, and clarify data points.

Primary Interviews and Surveys

Primary work is used to pressure-test the model assumptions that desk sources cannot fully explain, especially around typical system pricing, consumables attach rates, replacement cycles, and where demand is shifting across clinical and research settings. We spoke with a balanced set of respondents across manufacturers, distributors, hospital and lab procurement, and research users across APAC, EMEA, and the Americas, so regional adoption patterns and currency timing could be validated.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 18% | APAC: 45% |

| Mid tier: 48% | Functional/Unit leaders: 26% | EMEA: 31% |

| Smaller Players: 22% | Managers: 56% | Americas: 24% |

Market-Sizing & Forecasting

Market sizing is built using a top-down and bottom-up approach, where the main total is reconstructed from the addressable clinical and research demand pool and then checked against supplier-side reality. In practice, we start from healthcare and life-science activity indicators and narrow them down to the portion that typically uses light-based imaging, sensing, and therapy tools.

Inputs that help shape the totals include diagnostic procedure volumes where optical methods are used, research spending tied to imaging and photonics-enabled workflows, installed base growth for key instrument classes, average selling prices by system category, and consumables usage per installed system, since recurring spend can be meaningful. When data is sparse for a country or a niche modality, gaps are handled through peer-market analogs and ratio-based assumptions, then revalidated in calls. Forecasts are developed using scenario analysis supported by a short list of demand drivers, such as chronic disease load, hospital capital budgets, research funding direction, and regulatory clearance momentum for new optical devices. The outputs are sanity-checked with sampled ASP x volume calculations from interviews.

Data Validation & Update Cycle

Outputs are validated by comparing model results with independent signals, such as funding trends, regulatory activity, and the pace of instrument placements reported in public disclosures. When a number looks out of pattern, it is traced back to the assumption level and reviewed again, and follow-up outreach is triggered if the variance cannot be explained by a clear market event.

Before sign-off, the model and narrative go through multi-step internal reviews so the same logic is applied across regions and years. The dataset is refreshed on an annual cycle, and interim updates are done when material events occur, such as policy changes, major reimbursement shifts, or large technology launches. Right before delivery, we do a fresh pass to ensure the latest updates are reflected in the final view clients receive.

Mordor Intelligence's Biophotonics Market Estimate Compared With Other Published Estimates

It is normal to see different market sizes for biophotonics because publishers do not always count the same things, and they may also use different base years and pricing logic. The spread usually comes from what is treated as biophotonics, how hardware versus consumables are counted, and whether the numbers align to clinical demand, research demand, or a mix.

By tracking instrument placements, checking consumables attach assumptions, and refreshing currency timing inputs, Mordor Intelligence keeps the 2026 value aligned to biophotonics systems that are intentionally used with biological material, rather than adjacent optical categories that never touch life-science workflows. Some estimates appear to use a different year anchor or a broader interpretation of optical technologies, which can pull in neighboring areas like general photonics components or wider research instrumentation, and that tends to lift or shift the total. Differences also show up when ASP progression is applied as a flat uplift without matching it to product mix changes and replacement cycles.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 75.74 B (2026) | |

| Industry Research House A | USD 62.60 B (2024) | Uses an earlier base year and does not clearly state scope exclusions, which can change what is counted as biophotonics and how quickly hardware and consumables are ramped in the model. |

| Global Consultancy B | USD 67.81 B (2023) | Anchors the series to 2023 and describes a broad optical technology view, so the total can differ based on whether adjacent optical research areas are included and how pricing and mix shift are applied over time. |

Looking at the three values together, the main takeaway is that year selection and category boundaries can move the total by several billions even before growth is applied. Our approach is meant to stay traceable to practical demand signals, so a reader can see which clinical and research activities are driving the number and what assumptions would need to change for the estimate to move.

Key Questions Answered in the Report

How is artificial intelligence transforming biophotonics diagnostics?

AI-enhanced spectroscopy and imaging workflows are cutting analysis times and boosting accuracy, already reaching 98.8% precision in non-invasive glucose testing.

Which emerging technology is expanding the possibilities of in-vivo imaging?

Photoacoustic tomography combined with nanomaterials now visualizes cerebral vessels through intact skulls, offering real-time stroke monitoring in clinical environments .

Why are biosensors becoming pivotal in next-generation biophotonic applications?

Surface-enhanced Raman techniques paired with machine learning enable single-cell biomarker detection, advancing personalized medicine and rapid drug monitoring.

What supply-chain risk could affect biophotonic equipment pricing?

Reliance on rare-earth elements for high-power laser diodes exposes manufacturers to material shortages that can raise system costs.

How are healthcare organizations addressing the skills gap in biophotonics?

Hospitals are teaming with universities to establish interdisciplinary training labs—such as the dedicated biophotonics facility at the University of Central Florida—to blend optics, biology and data science expertise.

Which non-medical sector is emerging as a promising outlet for biophotonic sensors?

Precision agriculture is increasingly deploying optical probes to track crop health and soil nutrients, underscoring demand for sustainable farming solutions.

Page last updated on: