Compound Semiconductor Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

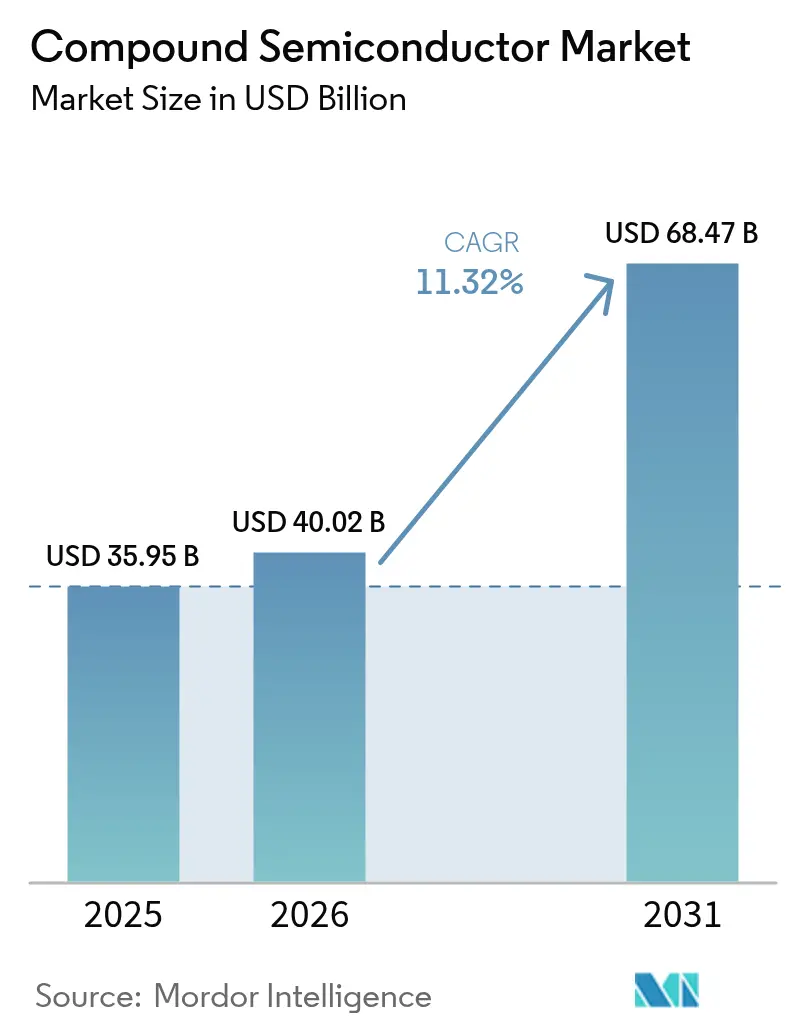

| Market Size (2026) | USD 40.02 Billion |

| Market Size (2031) | USD 68.47 Billion |

| Growth Rate (2026 - 2031) | 11.32% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Compound Semiconductor Market Analysis by Mordor Intelligence

The compound semiconductor market size in 2026 is estimated at USD 40.02 billion, growing from 2025 value of USD 35.95 billion with 2031 projections showing USD 68.47 billion, growing at 11.32% CAGR over 2026-2031. Momentum came from the widening use of wide-bandgap materials that boosted efficiency in power electronics, RF communications, and optoelectronics. Rising electric vehicle charging infrastructure, accelerating 5G standalone deployments, and premium display demand collectively lifted unit shipments and average selling prices. Foundry capacity hikes in Asia-Pacific, domestic-manufacturing incentives in the United States and Europe, and sustained capital spending by automotive OEMs sustained the investment cycle. At the same time, geopolitical export controls on gallium, germanium, and indium, coupled with weather-related raw-material disruptions, highlighted supply-chain fragility and underscored the strategic value of diversified sourcing.

Key Report Takeaways

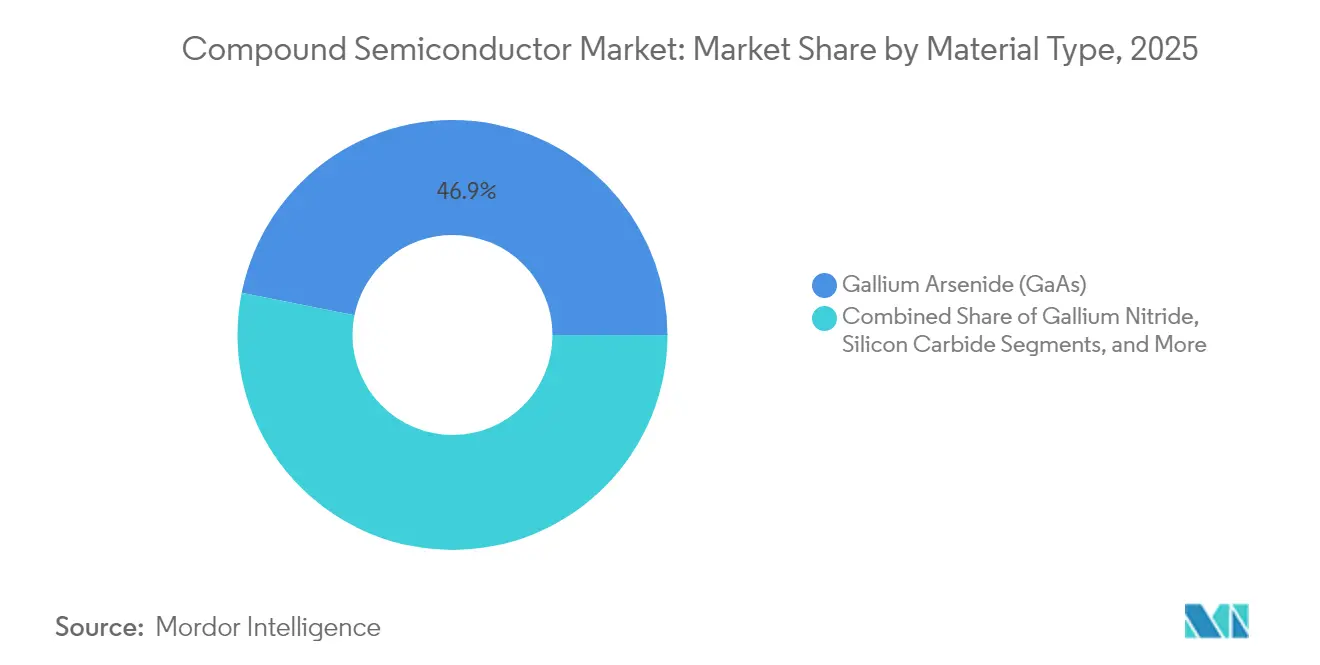

- By material type, gallium arsenide led with 46.85% revenue share in 2025, while silicon carbide is projected to expand at an 18.1% CAGR through 2031.

- By wafer size, the 150 mm category accounted for 48.02% of the compound semiconductor market share in 2025; 200 mm wafers are expected to grow at a 14.95% CAGR to 2031.

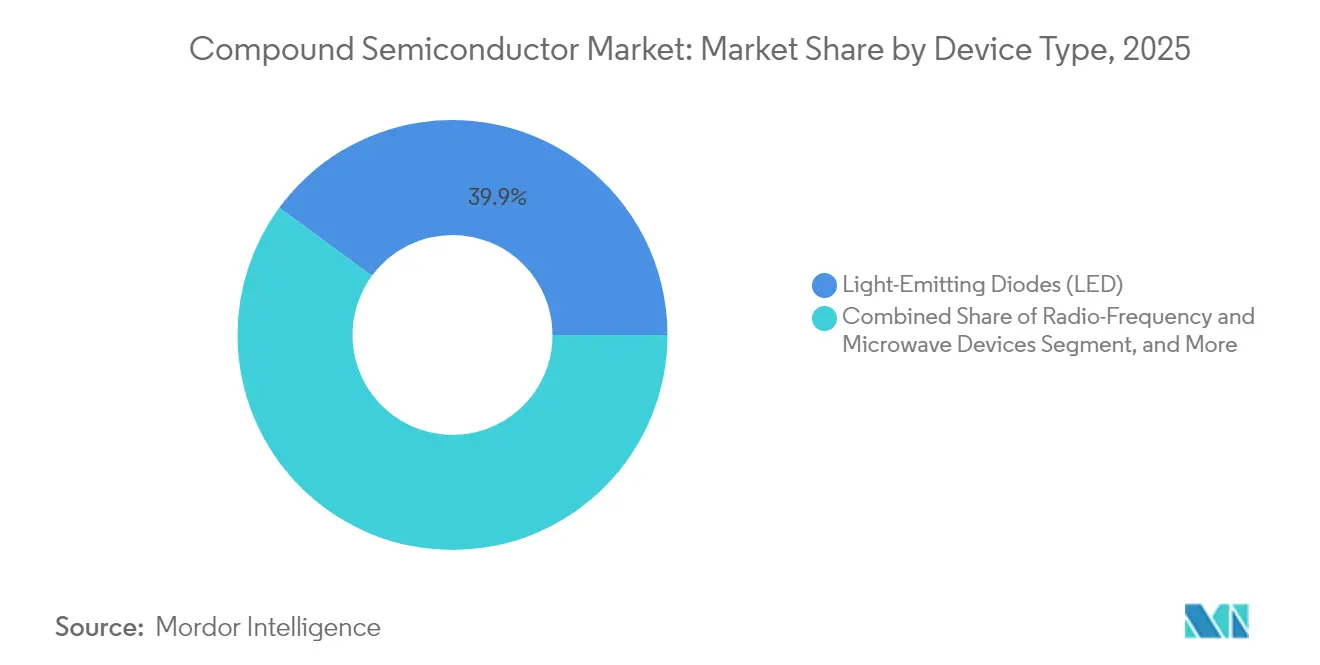

- By device type, LEDs captured 39.92% revenue in 2025, whereas power electronics are advancing at a 16.75% CAGR through 2031.

- By end-user industry, telecom and datacom infrastructure held 27.85% of the compound semiconductor market size in 2025, and automotive and transportation are forecast to grow at a 18.9% CAGR between 2026 and 2031.

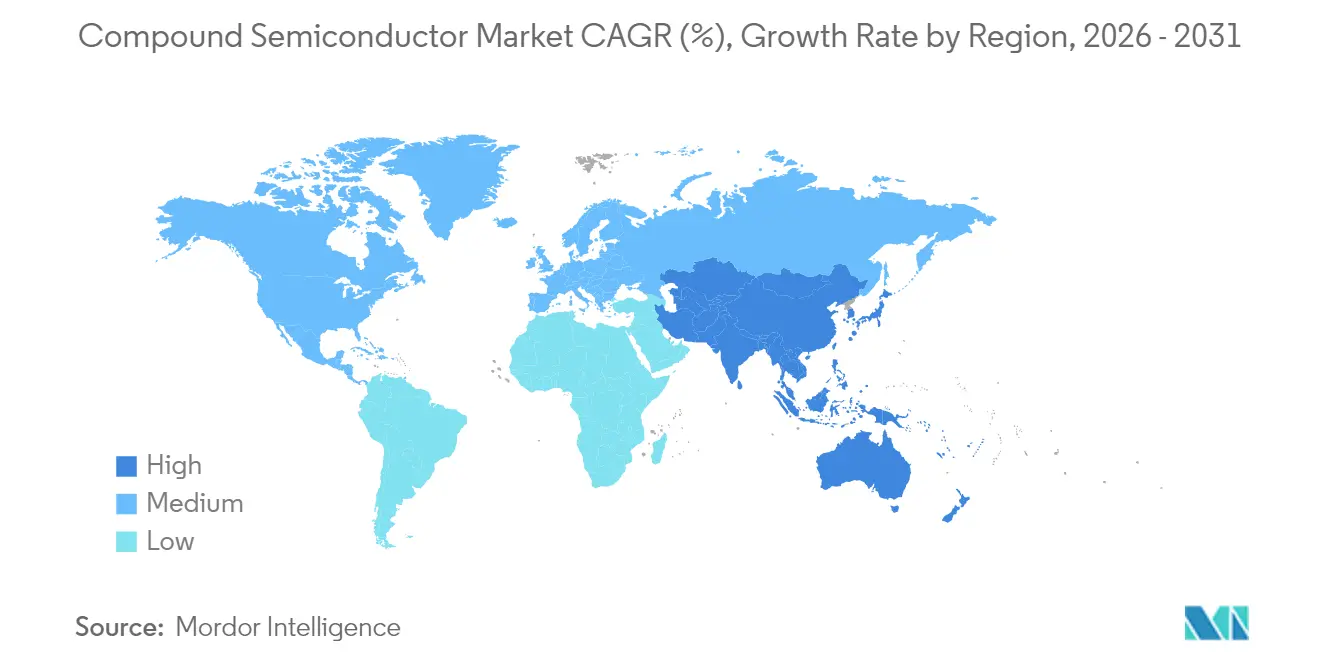

- By geography, Asia-Pacific commanded 58.25% revenue in 2025; the region is on track for a 13.95% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Compound Semiconductor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| GaN-on-Si power devices in EU and China EV chargers | +2.1% | Europe and China, spill-over to North America | Medium term (2-4 years) |

| 5G massive-MIMO RF front-ends in US and APAC | +1.8% | North America and APAC core, spill-over to Europe | Short term (≤ 2 years) |

| Micro/Mini-LED adoption in TVs and AR wearables | +1.4% | Global, early gains in APAC manufacturing hubs | Medium term (2-4 years) |

| SiC traction inverters for European commercial EVs | +1.9% | Europe's core, expanding to North America and China | Medium term (2-4 years) |

| III-V fab incentives under US/EU CHIPS Acts | +1.3% | North America and Europe, a competitive response in APAC | Long term (≥ 4 years) |

| InP-based LiDAR PICs for autonomous vehicles | +0.9% | Global, early deployment in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

GaN-on-Si power devices in EU and China EV chargers

European emissions rules and China’s highway electrification drove GaN-on-Si adoption in 350 kW and higher fast chargers that achieved 95% power-conversion efficiency and cut installation costs by up to 40% compared with silicon alternatives.[1]HAL Science, “Vertical GaN Devices: Reliability Challenges,” hal.science EU Green Deal funding of EUR 2 billion (USD 2.26 billion) for wide-bandgap fabs reinforced the transition, while China’s gallium export curbs spurred local sourcing strategies.

5G massive-MIMO RF front-ends in US and APAC

The migration toward standalone 5G and 64T64R or larger antenna arrays required GaAs and GaN power amplifiers that reduced base-station energy use by 40% and enabled millimeter-wave coverage. Initial deployments in South Korea reached 95% population coverage, and CHIPS Act grants prepared US fabs for domestic GaAs expansion.

Micro/Mini-LED adoption in TVs and AR wearables

Panel makers migrated from OLED to micro-LED for premium displays. Apple prototype smartphones integrated GaN-on-sapphire micro-LEDs that delivered 6,800 PPI and 50% lower power draw than OLED, while automotive cockpits adopted the tech for sunlight-readable dashboards.

SiC traction inverters for European commercial EVs

Mercedes-Benz eTruck platforms used SiC MOSFETs in 800 V inverters that reached 98% efficiency and reduced cooling complexity by 25%. Infineon’s EUR 7 billion (USD 7.91 billion) Malaysia fab targeted 30% of global SiC power capacity by 2030.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of 200 mm SiC substrates | -1.7% | Global, acute impact in automotive chains | Short term (≤ 2 years) |

| High Cap-Ex of MOCVD reactors | -1.2% | Global, particularly for new entrants | Medium term (2-4 years) |

| Reliability concerns in >650 V GaN devices | -0.8% | Global, regulatory scrutiny in automotive | Medium term (2-4 years) |

| US export controls on epi tools to China | -0.9% | China's core, spillover globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shortage of 200 mm SiC substrates

Manufacturers reported a 40% supply gap for 200 mm SiC wafers because boule growth cycles took up to 14 days, and furnace capacity was limited. Automotive OEMs, therefore, locked multi-year deals at premium prices, and substrate makers such as II-VI gained pricing power.

High Cap-Ex of MOCVD reactors

A single metal-organic chemical-vapor-deposition reactor costs USD 3-8 million, and a 200 mm GaN line demands as many as 15 units, raising entry barriers above USD 40 million. The dominance of two tool vendors constrained scaling and encouraged consolidation among smaller fabs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: SiC Accelerates as GaAs Holds the Lead

The compound semiconductor market size for materials saw gallium arsenide retain a 46.85% share in 2025. Silicon carbide recorded an 18.1% CAGR outlook, underpinned by traction inverters and fast-charging power modules. Gallium nitride took incremental share through 650 V bidirectional IC launches that widened adoption in energy-storage bidirectional chargers. Indium phosphide remained essential in LiDAR photonic integrated circuits and sub-THz 6G prototypes, although absolute volumes were low.

Segment growth hinged on wide-bandgap attributes, high electron mobility and high breakdown voltage, that silicon could not match. Research breakthroughs in RF GaN-on-Si promised to extend GaN usage into 6G base-station PAs. Cost pressures lingered because gallium and indium feedstock remained under export-control scrutiny, raising interest in recycled sources and material alternatives such as AlYN.

By Wafer Size: 200 mm Drives Cost Optimisation

In 2025, 150 mm substrates captured 48.02% revenue, yet 200 mm platforms projected the fastest 14.95% CAGR. Automotive power modules, which depend on high die counts, favoured 200 mm to secure a projected 30% die-per-wafer cost saving over 150 mm lines. Infineon’s Malaysia megafab validated the scale economics with 200 mm SiC lines designed for 30% of global supply by 2030.

Smaller (≤ 100 mm) formats preserved positions in low-volume, performance-critical sectors such as satellite communications. While 300 mm opportunities emerged in GaN-on-Si prototypes, technical hurdles—film stress, bow control, and defect density—kept commercial adoption beyond the forecast period. Equipment suppliers prioritised 200 mm reactor platforms to maximise utilisation, targeting 85-90% loading to amortise capital costs.

By Device Type: Power Electronics Overtakes Traditional LEDs

LEDs accounted for 39.92% revenue in 2025, but power-electronics devices are forecast to post a 16.75% CAGR, pushing the compound semiconductor market toward electrification. Tesla’s SiC-based traction inverters set a benchmark, delivering a 5% range gain, which subsequently drove similar adoptions across commercial trucks and buses. RF and microwave devices expanded steadily as 5G and satellite backhaul demanded linear high-efficiency PAs.

Optoelectronics such as vertical-cavity surface-emitting lasers entered automotive LiDAR and high-speed optical interconnects, whereas photovoltaic cells stayed limited to space applications where gallium arsenide triple-junction architectures justified premium pricing. The rising power-device mix improved overall ASPs and margins for integrated device makers, thereby underpinning cap-ex allocation toward wide-bandgap fab expansions.

By End-User Industry: Automotive Transformation Shapes Demand

Telecom and datacom held 27.85% of the compound semiconductor market share in 2025, yet automotive is projected to expand at a 18.9% CAGR on the back of electrified drivetrains and advanced driver-assistance systems. BYD’s full-platform SiC integration yielded a 10% drivetrain-efficiency gain, validating value creation in even mid-range passenger models. Consumer electronics remained a stable, albeit slower-growing, contributor as flagship smartphones integrated GaAs/GaN RF front-ends and next-generation micro-LED displays.

Industrial and energy sectors leveraged SiC and GaN in solar inverters and utility-scale battery energy-storage systems to reduce conversion losses. Aerospace and defense continued to command high ASPs for radar and satellite payloads. Healthcare represented an emerging niche, with compound semiconductors powering wireless implants and precision diagnostic lasers.

Geography Analysis

Asia-Pacific held 58.25% revenue in 2025 and posted a 13.95% CAGR outlook to 2031. The compound semiconductor market size for the region benefited from China’s planned 8.6 million-wafer-per-month capacity and Taiwan’s foundry dominance. Export controls on gallium, germanium, and indium introduced in 2024 highlighted concentration risks, prompting local governments to channel subsidies toward upstream materials.

North America advanced domestic supply-chain agendas under the USD 39 billion CHIPS incentive. Skyworks and Qorvo lined up GaAs expansion projects, and TSMC’s USD 165 billion Arizona cluster accelerated to include compound-semiconductor advanced-packaging capability. Defense requirements for assured access to III-V devices added impetus.

Europe positioned wide-bandgap semiconductors as a pillar of its Green Deal and European Chips Act. Germany allocated EUR 2 billion (USD 2.26 billion) to local production, while Nexperia committed USD 200 million for a Hamburg SiC line. Supply-chain localisation aims to mitigate Asia-centric shocks such as the quartz-mine disruption in North Carolina that threatened 70-90% of global high-purity quartz.

Regulatory Landscape

Export controls and licensing requirements increasingly shape compliance for compound semiconductor materials, devices, and manufacturing tools. In January 2026, the US Department of Commerce, Bureau of Industry and Security (BIS) revised its license review policy for certain semiconductor exports to China and Macau, adding diligence and licensing friction across fab, OSAT, and design supply chains that use controlled semiconductor manufacturing items. In April 2026, BIS published a final rule extending the application deadline for companies to become Approved Integrated Circuit (IC) Designers from April 13, 2026, to December 31, 2026, which affects how eligible designers maintain access and continuity under the updated control framework.

In Europe, industrial policy is widening from capacity support toward targeted technology sovereignty in areas relevant to compound semiconductors. In June 2026, the European Commission advanced a Chips Act 2.0 proposal that explicitly highlights strategic dependencies, including photonic integrated circuit technologies, and outlines mechanisms such as pilot lines, competence centers, and a Chips Fund to accelerate industrial deployment. These policy moves are influencing where companies plan epitaxy, wafering, and advanced packaging capacity, and they are increasing the premium on traceability for sensitive materials such as gallium, germanium, indium, and related upstream inputs.

Value Chain Analysis

The compound semiconductor value chain covers upstream raw materials and refining (gallium, germanium, indium, tungsten, tellurium, and related metals), crystal growth and substrate manufacturing (SiC, GaAs, InP, GaN templates), epitaxy (MOCVD/MBE), device fabrication, and packaging and test (including high-reliability power modules and RF front ends), with end-market integration across automotive, industrial and energy, telecom/datacom, and defense. Upstream concentration and permitting remain a central risk, reinforced by China extending licensing requirements in February 2025 to include additional strategic inputs such as tungsten, tellurium, bismuth, indium, and molybdenum, which can tighten lead times and raise qualification burdens for global supply chains.

Midstream and downstream players are responding through tighter partnerships, qualification programs, and moves to larger wafers where feasible. In March 2025, STMicroelectronics and Innoscience signed a GaN technology development and manufacturing agreement aimed at expanding front-end capacity and improving supply resilience. For advanced optoelectronics and interconnects, Quintessent and IQE set up a quantum dot epitaxial wafer supply chain in January 2025 with production deliveries scheduled through 2025. On the materials frontier, June 2026 commercialization of a 6-inch and 8-inch homoepitaxial gallium oxide wafer mass-production line by Hangzhou Garen Semiconductor shows how newer ultra-wide-bandgap substrates are entering the supply base, creating an alternative pathway for ultra-high-voltage device roadmaps while also introducing new qualification and toolchain requirements.

Competitive Landscape

Industry concentration evolved toward moderate levels. Five vendors held more than 90% of the SiC power niche, yet diversified portfolios in RF and optoelectronics diluted overall dominance. STMicroelectronics led SiC power at 32.6% share, underpinned by a EUR 5 billion (USD 5.65 billion) Italian expansion. Infineon acquired GaN Systems and launched a USD 7.91 billion Malaysia fab. Onsemi purchased Qorvo’s SiC JFET line for USD 115 million, accelerating vertical integration.

Substrate technology and epitaxial process control remained key differentiators. Patent-portfolio races centred on vertical GaN structures and AlYN compounds.[4]Total Telecom, “Nexperia to Invest USD 200 Million in Hamburg,” totaltele.com Fabless challengers such as Transphorm targeted niche automotive power modules, leveraging outsourcing to lift asset efficiency. Government incentives shaped location decisions, with US and EU grants favouring domestic fabs for strategic autonomy.

Second-tier players focused on specialty markets—InP photonics, micro-LED epi wafers, and high-efficiency space solar cells—where performance outweighed scale. Strategic alliances between tool vendors and materials suppliers shortened process-qual cycles, enabling quicker customer qualifications and reinforcing incumbent positions.

Compound Semiconductor Industry Leaders

Skyworks Solutions Inc.

Wolfspeed Inc.

Qorvo Inc.

Analog Devices Inc.

OSRAM GmbH (ams-OSRAM AG)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Opportunities are taking shape where policy-backed capacity buildouts align with high-value compound semiconductor demand in power and photonics. In the United States, CHIPS-linked funding is anchoring SiC manufacturing investments tied to electrification and grid efficiency. In July 2026, Bosch reached a funding agreement with the US Department of Commerce for up to USD 225 million in direct funding to support a USD 2 billion investment at its Roseville, California facility for SiC power semiconductor production, with commercial output beginning in 2026. This supports whitespace for domestic substrate-to-module ecosystems, supplier qualification services, and advanced packaging capabilities that can shorten design-in cycles for automotive and energy customers.

In photonics and high-speed connectivity, InP substrates and manufacturing capacity are increasingly relevant for scaling datacenter infrastructure and optical interconnects. In July 2026, Sumitomo Electric Industries committed JPY 18 billion (about USD 120 million) to expand InP substrate capacity at its Itami Works, targeting 3.1 times fiscal 2024 capacity by fiscal 2028, and Coherent signed a letter of intent for up to USD 50 million in CHIPS and Science Act funding to expand its 6-inch InP manufacturing facility in Sherman, Texas. Outside the US and EU, India announced India Semiconductor Mission (ISM) 2.0 in May 2026 to deepen the ecosystem and scale compound semiconductor production and advanced packaging, while Japan is drawing large-scale foundry investments such as Tower Semiconductor's July 2026 USD 3 billion dual-track expansion plan (including Silicon Photonics, SiGe, and advanced packaging with government grants). Together, these developments point to near-term demand for equipment, epitaxy, metrology, and advanced packaging providers that can support qualification at scale across SiC, GaN, and InP value chains.

Recent Industry Developments

- June 2026: Wolfspeed launched a dedicated data center solutions team and opened a regional office in Santa Clara, California, to focus on power architectures for AI infrastructure. The initiative aligns SiC device roadmaps and application engineering with hyperscale power-density constraints, accelerating design-in activity beyond traditional automotive-heavy demand profiles.

- May 2026: Wolfspeed introduced new 3.3 kV SiC power module families in two industry-standard footprints, including baseplate and baseplate-less options for energy and high-power conversion use cases. The release expands the addressable range for SiC modules into higher-voltage systems and strengthens platform standardization for OEM and integrator qualification.

- June 2025: TSMC advanced the schedule of its USD 165 billion Arizona project, which includes plans to add compound-semiconductor advanced-packaging capability. Earlier availability of localized packaging capacity supports North American supply-chain assurance goals for compound semiconductor devices used in telecom, datacom, and defense systems.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenues from compound semiconductor materials and devices made using two or more elements, sold into electronics where performance needs go beyond silicon for speed, power handling, or optical functions.

Scope exclusions: The sizing excludes silicon-only semiconductors and general electronics assembly value that does not belong to the compound semiconductor device or material itself.

Segmentation Overview

- By Material Type

- Gallium Arsenide (GaAs)

- Gallium Nitride (GaN)

- Silicon Carbide (SiC)

- Indium Phosphide (InP)

- Gallium Phosphide (GaP)

- Other III-V and II-VI Compounds

- By Wafer Size

- ≤100 mm

- 150 mm

- 200 mm

- 300 mm and Above

- By Device Type

- Light-Emitting Diodes (LED)

- Radio-Frequency and Microwave Devices

- Optoelectronics (Laser, Photodetector)

- Power Electronics

- Photovoltaic Cells

- By End-User Industry

- Telecom and Datacom Infrastructure

- Consumer Electronics

- Automotive and Transportation

- Industrial and Energy

- Aerospace and Defense

- Healthcare and Life Sciences

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Nordics (Sweden, Finland, Norway, Denmark)

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- India

- Taiwan

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Mexico

- Rest of South America

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with public statistics and technical references that explain the demand pool and the pace of adoption. We typically review sources such as the US International Trade Commission and UN Comtrade for trade signals, the US Energy Information Administration for electrification indicators, and the International Telecommunication Union for network rollout context. For technology grounding, publications from organizations such as IEEE and other peer-reviewed journals help confirm device use cases and performance-driven substitution away from silicon.

We also cross-check public company filings, investor decks, product announcements, and reputable industry press to understand mix changes across RF, optoelectronics, LEDs, and power electronics. Where needed, paid subscriptions are used for company financials and intelligence, patent databases, and shipment-level import and export checks to reduce guesswork on volumes and pricing direction. These examples are not exhaustive, and many additional public sources were reviewed to collect, verify, and clarify inputs.

Primary Interviews and Surveys

Primary work focused on speaking with stakeholders across the value chain, including material suppliers, wafer and device manufacturers, and downstream buyers in telecom, automotive, industrial, and consumer electronics. Interviews and structured surveys were used to confirm adoption timelines, typical ASP movement, and how supply constraints and qualification cycles affect realized demand across APAC, EMEA, and the Americas.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 13% | APAC: 43% |

| Mid tier: 52% | Functional/Unit leaders: 32% | EMEA: 30% |

| Smaller Players: 18% | Managers: 55% | Americas: 27% |

Market-Sizing & Forecasting

The model is built using top-down logic where end-market demand signals are translated into compound semiconductor device consumption, and then converted into value using practical price and mix assumptions. For compound semiconductors, adoption rates in EV powertrains and charging, 5G and RF front-end content, LED and optoelectronics unit trends, and wafer supply additions are the main anchors that shape the demand curve.

Those totals are then checked using selective bottom-up approximations, such as sampled supplier revenue roll-ups, channel feedback on typical device pricing bands, and volume estimates inferred from capacity additions and utilization talk tracks. When a bottom-up view has gaps, such as private companies or mixed revenue reporting, we adjust using peer ratios and application shares confirmed during interviews, and then keep the assumptions visible for review.

Forecasting uses scenario analysis supported by simple multivariate relationships between the market value and drivers such as EV production, 5G deployments, industrial power demand, and reported wafer capacity. Assumptions on ASP progression are refreshed by tracking mix shifts between GaN, SiC, GaAs, and optoelectronics products, then stress-tested against buyer feedback.

Data Validation & Update Cycle

Outputs are validated through multiple checks so the final number stays consistent with real market signals. We compare results against independent indicators like device shipment commentary, capacity and utilization updates, trade flows for key materials and wafers, and patenting or qualification activity that can indicate upcoming ramps.

Variance checks are run at the regional and application level, and unusual jumps are investigated before sign-off, followed by a second analyst review for logic and math consistency. Reports are refreshed annually, and interim updates are triggered when material events occur, such as major capacity expansions, export controls, or step changes in EV and telecom demand. Before delivery, a final review pass is completed so clients receive the most current view available at that time.

Mordor Intelligence's Compound Semiconductor Market Size Versus Other Published Estimates

It is normal to see different market sizes for compound semiconductors because publishers do not always count the same device boundaries, years, and pricing basis. Differences also come from whether the estimate emphasizes materials, wafers, devices, or a mix, and how fast adoption is assumed in EV power, RF, and optoelectronics.

Key gap drivers usually sit in three places: scope choices (for example, counting only device revenue versus adding adjacent modules), how ASPs are carried forward (flat prices versus mix-led declines), and how the base year is anchored to capacity, utilization, and end-market units. By tracking wafer capacity additions, utilization swings, and application-level adoption curves, Mordor Intelligence keeps the 2026 total aligned to a device-focused revenue pool rather than mixing in broader electronics value.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 40.02 B (2026) | |

| Industry Publisher A | USD 45.42 B (2026) | The estimate appears to use a broader product scope that can include more downstream value in certain applications, and it may apply a different base-year reset that lifts the starting ASP and mix assumptions. |

| Industry Publisher B | USD 43.70 B (2025) | The number is anchored to a different year and is paired with a slower growth path, which can reflect more conservative adoption timing in EV and telecom, plus a different approach to currency timing and regional weighting. |

The spread in values is mainly explained by year alignment and what is counted around the device boundary, followed by how ASPs and mix are carried through the forecast. Keeping the steps tied to visible demand indicators and clearly stated scope rules helps us provide a number that can be replicated and updated when new capacity or adoption data becomes available.

Key Questions Answered in the Report

What is the current value of the compound semiconductor market?

The compound semiconductor market was valued at USD 40.02 billion in 2026.

How fast is the compound semiconductor market expected to grow?

The market is projected to grow at a 11.32% CAGR, reaching USD 68.47 billion by 2031.

Which region leads the compound semiconductor market?

Asia-Pacific held 58.25% revenue in 2025, driven by large-scale manufacturing capacity.

Why are 200 mm SiC wafers important?

They lower die cost by roughly 30% versus 150 mm wafers, which supports automotive electrification.

Who dominates the SiC power-device segment?

STMicroelectronics led with 32.6% share, and the top five companies controlled more than 90% of the niche.

What is the main growth driver for compound semiconductor demand in automotive?

SiC traction inverters and GaN fast chargers improve efficiency and support higher-voltage EV architectures.

Page last updated on: