Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

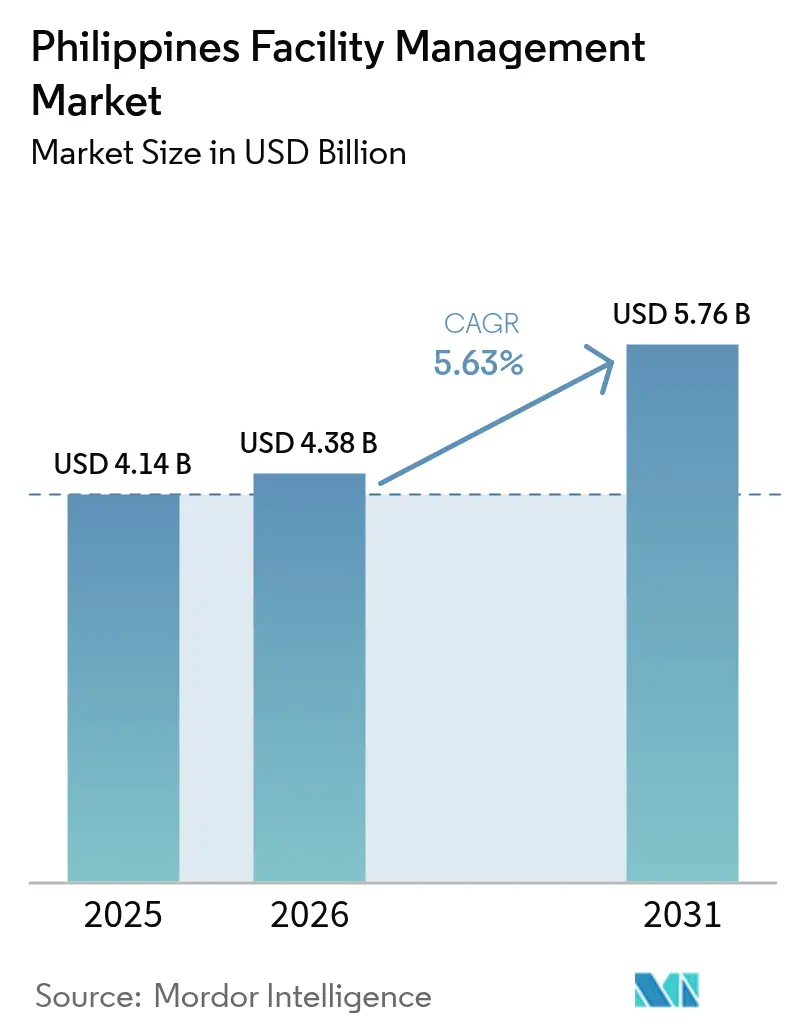

| Base Year Market Size (2025) | USD 4.14 Billion |

| Market Size (2026) | USD 4.38 Billion |

| Market Size (2031) | USD 5.76 Billion |

| Growth Rate (2026 - 2031) | 5.63% CAGR |

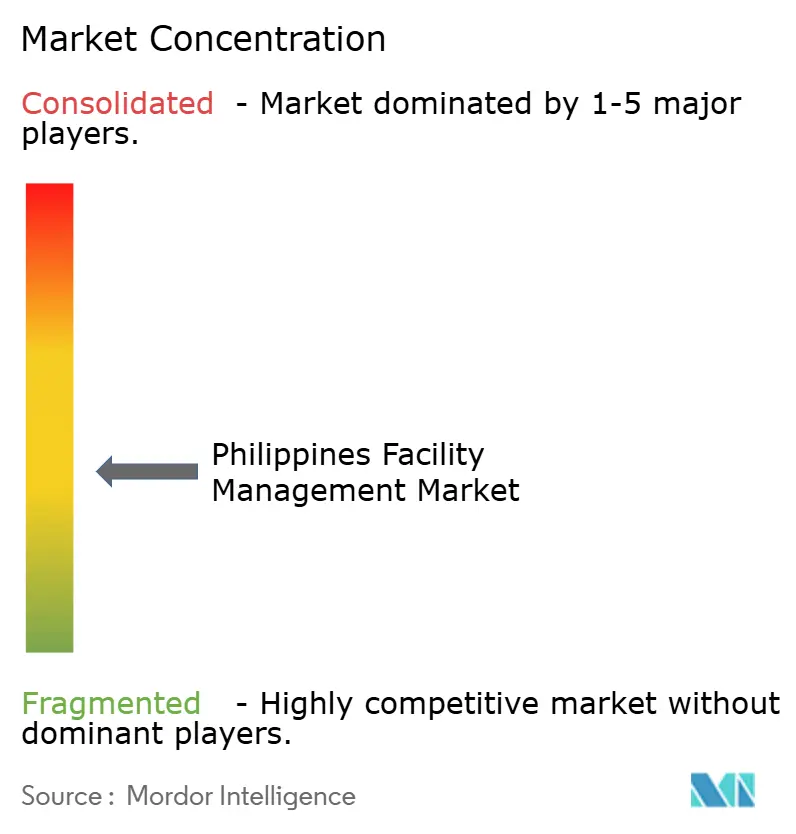

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Philippines Facility Management Market Analysis by Mordor Intelligence

The Philippines facility management market size is projected to expand from USD 4.14 billion in 2025 and USD 4.38 billion in 2026 to USD 5.76 billion by 2031, registering a 5.63% CAGR between 2026 to 2031. Expedited infrastructure spending, a visible shift toward outsourced contracts, and rapid technology adoption are underpinning steady headline growth, even though price-based competition continues to squeeze margins. Multinational occupiers are standardizing performance-based service-level agreements across Metro Manila, Cebu, and emerging provincial hubs, creating openings for certified operators that can document uptime and energy savings. At the same time, demand for hygiene-centric soft services is rising as landlords embed health-and-safety metrics into vendor scorecards, while hyperscale data-center development is spawning a specialist segment that commands premium fees for precision maintenance and continuous monitoring. The result is a two-speed landscape where technology-enabled integrators gain share while smaller single-service vendors face higher compliance costs and labor shortages.

Key Report Takeaways

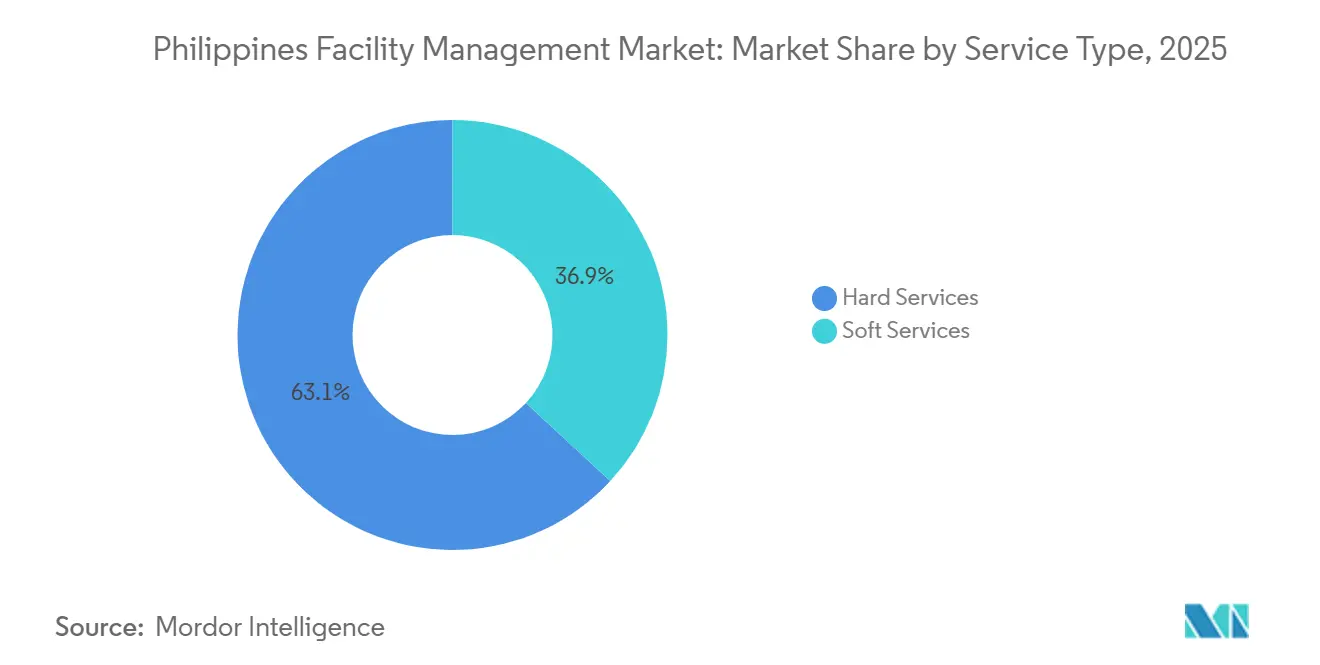

- By service type, hard services led with 63.12% revenue share in 2025, while soft services are projected to grow at a 6.02% CAGR through 2031.

- By offering type, in-house arrangements accounted for 58.91% in 2025, and outsourced models are expected to advance at a 6.13% CAGR to 2031.

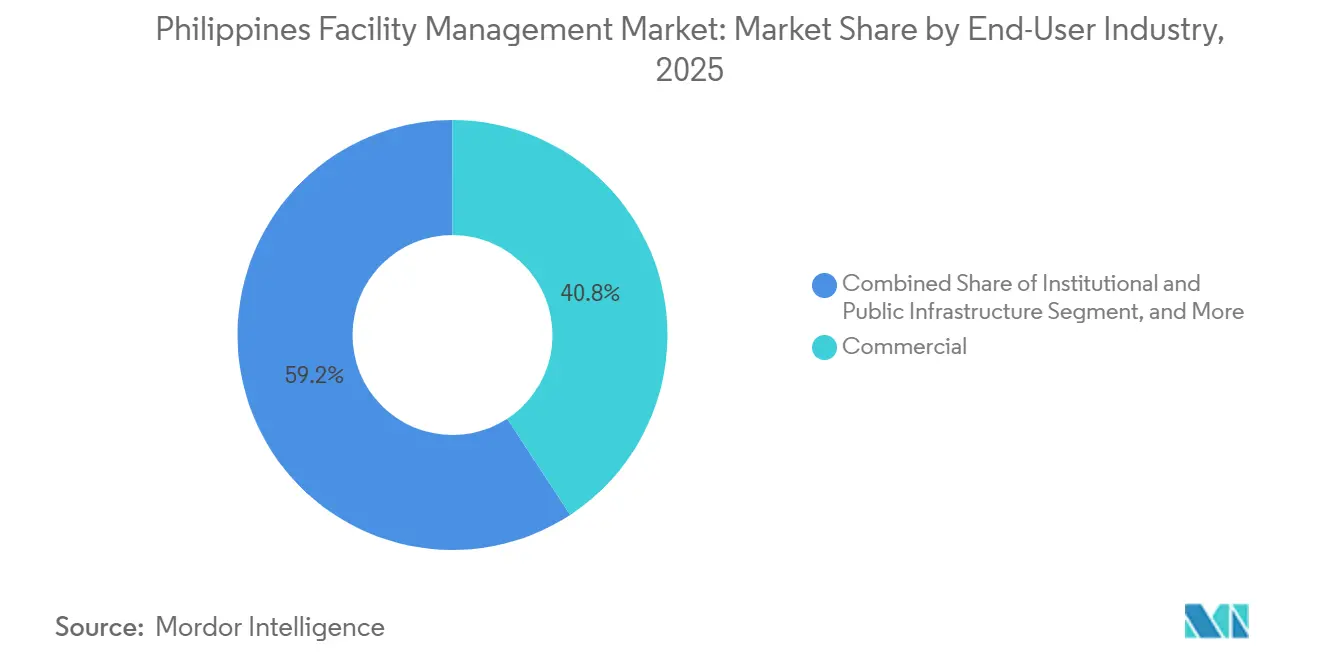

- By end-user industry, commercial real estate contributed 40.78% of 2025 revenue, whereas healthcare is forecast to post the fastest 7.08% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Philippines Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Infrastructure Development Fueling Demand | +1.4% | National, Metro Manila, Cebu, Davao | Medium term (2-4 years) |

| Technology Integration Transforming Service Delivery | +1.2% | Metro Manila, Clark Freeport Zone, PEZA economic zones | Long term (≥4 years) |

| Sustainable Facility Management Bolstering Competitive Advantage | +0.9% | Metro Manila, Makati CBD, Bonifacio Global City | Medium term (2-4 years) |

| Outsourcing Trend Gaining Momentum | +1.1% | National, BPO hubs in Metro Manila, Cebu, Iloilo | Short term (≤2 years) |

| Data-Center Build-out Creating Specialized FM Opportunities | +0.7% | Metro Manila, Cavite, Laguna | Medium term (2-4 years) |

| PPP Act 2023 Enabling Performance-Based O and M Contracts | +0.3% | National, early transport and hospital projects | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Infrastructure Development Fueling Demand

Build Better More earmarked PHP 9 trillion (USD 155.6 billion) for transport corridors, gateways, and mass-transit lines that will need decades of cleaning, security, and long-cycle equipment care. Early design-build packages already stipulate ISO 41001-aligned preventive-maintenance plans, drawing facility managers into blueprints before groundbreak. Twelve toll-road concessions awarded in 2024 included cleanliness benchmarks and incident-response protocols favoring firms with nationwide technician pools.[1]Department of Public Works and Highways, “Build Better More Project List,” dpwh.gov.ph Rapid urbanization added 2.3 million residents to Metro Manila, Cebu, and Davao between 2020 and 2025, amplifying demand for outsourcing in mixed-use towers and logistics hubs.[2]Philippine Statistics Authority, “Urban Population Update 2025,” psa.gov.ph Developers are consolidating eight to twelve vendors into single integrated contracts, reducing coordination friction and standardizing key performance indicators across portfolios. These dynamics anchor a predictable project funnel that supports long-term revenue visibility for scale players in the Philippines facility management market.

Technology Integration Transforming Service Delivery

Internet of Things sensors, cloud-based building-management systems, and machine-learning diagnostics are moving from pilot to portfolio scale in premium offices and data halls. A University of Cebu field study showed that predictive analytics cut chiller downtime by 31% and sliced energy use by 18% in a 50,000 square-meter tower.[3]University of Cebu, “AI-Driven Chiller Optimization Study,” uc.edu.ph The Philippine Green Building Council recorded 47 new BERDE-certified projects in 2024, most equipped with smart metering that feeds live data to service dashboards.[4]Philippine Green Building Council, “BERDE Certification Statistics 2025,” philgbc.org Compliance catalysts are materializing as the Energy Efficiency and Conservation Act mandates periodic energy audits for properties above 10,000 square meters.[5]Department of Energy, “Energy Efficiency and Conservation Act Guidelines,” doe.gov.ph Outcome-based contracts are emerging, where payment hinges on uptime or energy-reduction milestones, aligning incentives for both landlords and vendors. These developments expand addressable value pools and reinforce the technology premium inside the Philippines facility management market.

Sustainable Facility Management Bolstering Competitive Advantage

Multinational tenants now embed ESG metrics into bid weightings, lifting providers that carry ISO 14001 credentials and transparent carbon baselines. BERDE applications increased 22% year on year in 2025 as landlords anticipated stricter disclosure rules. Operators respond with biodegradable cleaning agents, waste-segregation audits aligned with Republic Act 9003, and staff upskilling in water-reduction techniques. Ayala Land and SM Prime published 2024 ESG reports that quantify Scope 3 emissions from outsourced workstreams, raising the bar for contractors seeking renewals. Electric vehicle fleets for mobile technicians and rooftop solar retrofits are no longer fringe initiatives but key differentiators in competitive tenders. The sustainability pull is therefore converting environmental stewardship from marketing narrative to contractual necessity within the Philippines facility management market.

Outsourcing Trend Gaining Momentum

Corporations are diverting capital toward core revenue activities, allowing non-core services to migrate to third-party specialists. The BPO industry, with 1.57 million employees in 2024, prefers turnkey integrated contracts that bundle janitorial, pantry, and security functions to ensure uniform hygiene across multi-site footprints. Republic Act 11966 streamlined 15-to-30-year O and M procurements, normalizing performance penalties and milestone-based payouts in public projects. Private landlords are mirroring the model in office towers, stipulating uptime deductions that reward predictive maintenance capabilities. Smaller Philippine vendors are forming joint ventures to secure bid scale, pooling MEP expertise with digital reporting tools to challenge global incumbents. This structural handoff from in-house teams to contractors will deepen the addressable base for the Philippines facility management market across the forecast horizon.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Labor Shortages Constraining Market Growth | -0.8% | National, Metro Manila, Cebu | Short term (≤2 years) |

| Regulatory Compliance Increasing Operational Complexity | -0.5% | National, Metro Manila | Medium term (2-4 years) |

| High Cost Sensitivity Leading to Price-Based Competition | -0.4% | National, provincial cities | Short term (≤2 years) |

| Energy Cost Volatility Inflating Operating Budgets | -0.6% | National, cooling-intensive assets | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Labor Shortages Constraining Market Growth

Overseas demand for Filipino electricians, HVAC engineers, and controls programmers siphoned 1.77 million workers abroad in 2024, thinning the domestic talent bench. Technical Education and Skills Development Authority data reveal that only 38% of TVET graduates land jobs within six months, spotlighting curriculum gaps in IoT integration and fire-system commissioning. Metro Manila wages for certified technicians rose 12% year on year to PHP 25,000-35,000 (USD 432-605) per month, eroding fixed-price contract margins. Global integrators lure scarce specialists with overseas rotations and structured learning paths, leaving small firms to backfill with apprentices and longer mobilization timelines. Consequently, labor scarcity caps near-term scaling capacity for the Philippines facility management market.

Energy Cost Volatility Inflating Operating Budgets

Meralco’s generation tariff reached PHP 11.63 (USD 0.20) per kWh in November 2024 amid LNG supply swings, pushing energy to as high as 55% of total spend in data-center and mall portfolios Meralco.com.ph. While the Energy Regulatory Commission introduced monthly rate recalibrations, many FM contracts signed in 2022-2023 locked pass-through ceilings that now sit below actual costs. Clients resist mid-cycle reopeners, citing budget freezes, which forces contractors to absorb spikes or risk service degradation. The strategic workaround is energy-performance contracting, where vendors finance LEDs, VFDs, and rooftop solar, sharing verified savings over multiyear horizons. Nonetheless, short-run volatility still undermines predictability in the Philippines facility management market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Hard Services Anchor Revenue, Soft Services Accelerate

Hard services captured 63.12% of 2025 revenue inside the Philippines facility management market share, reflecting the capital intensity of mechanical-electrical-plumbing upkeep, HVAC optimization, and fire-safety assurance. Cooling loads account for roughly 60% of commercial-building energy demand in the archipelago’s tropical climate, keeping HVAC tune-ups, chiller overhauls, and airflow balancing at the top of landlord priorities. Bureau of Fire Protection audits under Republic Act 9514 have tightened annual inspection regimes, expanding demand for certified suppression-system technicians. Asset-management platforms that map equipment life cycles and forecast capital expenditures are gaining favor with real-estate investment trusts eager to demonstrate fiduciary stewardship to institutional investors. As a result, sophisticated hard-service offerings command higher average selling prices than commodity soft services, even though volume growth is slower.

Soft services are projected to post a 6.02% CAGR through 2031, outpacing hard services as occupiers channel budgets toward hygiene, security, and workplace experience. Twice-daily high-touch disinfection, mandated by the Department of Health’s 2024 guidelines, entrenched recurring janitorial runs and electrostatic spray programs. Call-center landlords reinstated reception staffing, mail-room sorting, and access-control monitoring once hybrid attendance stabilized, underpinning volume in office support. Catering is rebounding on the back of talent retention agendas that use subsidized meals as an employee-engagement lever. In aggregate, soft-service momentum broadens the revenue base and diversifies risk within the Philippines facility management market.

By Offering Type: Outsourced Models Gain Share

In-house teams still accounted for 58.91% of market revenue in 2025, largely within government ministries, public universities, and heavy-industry plants that favor direct control or are bound by civil-service mandates. Yet the Public-Private Partnership Act added legal scaffolding for hybrid models where agencies outsource technical silos like biomedical asset care or hazardous-waste handling to certified contractors. Cost pressures and head-count freezes in private conglomerates also catalyze selective hand-offs of non-core functions.

Outsourced contracts across single-service, bundled, and integrated tiers are forecast to compound at 6.13% over 2026-2031. Single contracts persist among SMEs wanting price flexibility, while bundled packages dominate BPO campuses where janitorial, pantry, and pest control are grouped under one invoice. Integrated facility management, which fuses technical and soft workstreams with unified SLAs, is now the fastest-scaling tier, especially among multinationals and hyperscale data-center operators that value consolidated dashboards and Asia-Pacific benchmarking. CBRE Philippines noted double-digit growth in IFM inquiries during 2024, a clear data point confirming demand migration toward comprehensive outsourcing. ISO 41001 certification has effectively become a gate-pass for bids above USD 5 million, raising the professionalism bar inside the Philippines facility management market.

By End-User Industry: Healthcare Leads Growth

Commercial real estate delivered 40.78% of 2025 revenue, driven by Metro Manila office towers, retail malls, and mixed-use estates. Despite a 26% vacancy rate tied to the offshore gaming ban, developers in Makati, Bonifacio Global City, and Ortigas introduced premium FM packages that embed tenant-experience metrics to differentiate space. Retail landlords such as SM Prime and Ayala Malls contract deep-cleaning, security, and HVAC services to ensure uninterrupted shopper comfort during peak tourist-traffic weekends, reinforcing steady soft-service baseline volume.

Healthcare exhibits the fastest 7.08% CAGR through 2031 and is becoming a strategic specialty inside the Philippines facility management market size for clinical assets. Makati Medical Center’s PHP 2 billion upgrade added critical-care beds that require round-the-clock biomedical calibration, infection-control protocols, and strict hazardous-waste segregation. The Department of Health identified 23 district hospitals for PPP procurement in 2024, guaranteeing long-horizon contracts that cover housekeeping, laundry, sterilization, and MEP maintenance. Private chains such as St. Luke’s Medical Center outsource full service bundles under seven-year terms to focus internal capital on surgical robotics and specialized staffing, underscoring a value shift toward professional FM integrators. Outside healthcare, hospitality is rebounding with 5.4 million international arrivals in 2024, reinstating demand for laundry, pool, and landscape upkeep, while industrial parks in PEZA zones lean on specialized FM for cleanrooms and waste-water compliance.

Geography Analysis

Metro Manila accounts for roughly 55%-60% of the Philippines facility management market, anchored by more than 3 million m² of Grade-A office, 100 plus malls, and the densest hospital and data-center clusters in the country. Key landlords such as Ayala Land, Megaworld, and Robinsons Land outsource integrated packages to multinational operators, embedding uptime and energy-efficiency clauses to sharpen tenant value propositions. The region’s hyperscale pipeline, which includes STT GDC’s 60 MW Manila 2 campus, demands precision cooling, N+1 power redundancy, and 24-hour fire monitoring, stimulating premium technical-service fees and specialized workforce certification requirements.

Cebu is the secondary growth pole for the Philippines facility management market, powered by 180,000 BPO seats and an expanding resort inventory surrounding Mactan Island. Office parks in Cebu Business Park deploy outsourced janitorial, security, and pantry packages to maintain corporate hygiene standards, while beachfront hotels contract landscaping and pool-chemistry upkeep to comply with Department of Tourism quality audits. The city government’s green-building ordinance, enacted in 2024, is accelerating demand for energy-audit services and green-cleaning certifications, further professionalizing service scope.

Davao and emerging provincial cities such as Iloilo, Bacolod, and Cagayan de Oro display lower outsourcing penetration but rising opportunity as logistics hubs and agro-industrial parks scale. Cold-storage warehouses for banana and tuna exports need temperature-monitor controls, while new mixed-use developments leverage bundled security and waste-collection contracts to sidestep hiring overhead. However, fragmented local vendors still dominate single-service slots, and budget sensitivity slows adoption of integrated models. This spatial divergence maintains a dual-tier structure within the Philippines facility management market, where scale players focus on metro corridors and domestic specialists serve labor-cost-advantaged provinces.

Competitive Landscape

The top ten vendors command about 35%-40% of revenue, indicating moderate fragmentation across the Philippines facility management market. Global brands such as CBRE Philippines, Jones Lang LaSalle, Cushman and Wakefield, ISS Facility Services Philippines, and Sodexo On-Site Services leverage multinational capital, proprietary analytics, and cross-border benchmarking to secure long-cycle integrated contracts from REITs and hyperscale clients. ISS A/S disclosed deployment of IoT sensors across 12 million m² in Asia-Pacific properties during 2024, feeding predictive-maintenance engines that cut call-outs by 15%. These data-rich platforms afford real-time visibility, an advantage hard to replicate for asset-light local rivals.

Domestic specialists such as Servicio Filipino, Meralco Industrial Engineering Services Corporation, Santos Knight Frank, and Century Properties Management anchor their competitiveness in local labor networks, flexible pricing, and provincial client intimacy. Several have formed consortia to bid on hospital PPPs, pooling biomedical technicians with digital governance tools to meet outcome-based key performance indicators. PPP Act contractual structures, which deduct payouts for uptime lapses, favor providers with balance-sheet depth, nudging the industry toward gradual consolidation.

Regulatory overhead is another competitive filter. Department of Labor and Employment Order 198-18 compels providers to maintain certified safety officers and documented OSH training logs, while Bureau of Fire Protection audits require annual compliance files. Operators with ISO 41001 and ISO 9001 systems clear pre-qualification faster, reinforcing entry barriers. Energy-cost volatility is spurring partnerships between FM firms and solar-oriented ESCOs, with joint offerings bundling predictive maintenance and renewable retrofits, giving early movers another differentiation layer in the Philippines facility management market.

Philippines Facility Management Industry Leaders

Atalian Global Services Philippines Inc.

Servicio Filipino Inc.

Meralco Industrial Engineering Services Corporation

SGS Philippiness Inc.

Cushman & Wakefield Debenham Tie Leung Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: STT GDC commenced operations at its 60 MW Manila 2 hyperscale data center in Cavite, awarding a 10-year integrated FM contract that guarantees 99.99% uptime.

- December 2025: The Philippines Green Building Council confirmed 47 new BERDE certifications in 2025, accelerating demand for ISO 14001-qualified FM vendors.

- November 2025: Makati Medical Center finished a PHP 2 billion expansion and signed a seven-year contract covering housekeeping, biomedical maintenance, and hazardous-waste disposal.

- October 2025: The Department of Health issued PPP guidelines for 23 district hospitals, embedding outcome-based FM payment triggers.

Philippines Facility Management Market Report Scope

Facility management (FM) services involve managing building upkeep, utilities, maintenance operations, waste services, security, etc. These services are further segmented into hard and soft facility management services. The adoption of FM solutions and services is likely to be driven by several factors, including an increase in demand for cloud-based FM solutions and a rise in demand for FM systems linked to intelligent software.

The Philippines Facility Management Market Report is Segmented by Service Type (Hard Services including Asset Management, MEP and HVAC Services, Fire Systems and Safety, Other Hard Facility Management Services; Soft Services including Office Support and Security, Cleaning Services, Catering Services, Other Soft Facility Management Services), Offering Type (In-house, Outsourced including Single Facility Management, Bundled Facility Management, Integrated Facility Management), End-User Industry (Commercial, Hospitality, Institutional and Public Infrastructure, Healthcare, Industrial and Process, Other End-User Industries), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

By Service Type

| Hard Services | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard Facility Management Services | |

| Soft Services | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft Facility Management Services |

By Offering Type

| In-house | |

| Outsourced | Single Facility Management |

| Bundled Facility Management | |

| Integrated Facility Management |

By End-user Industry

| Commercial |

| Hospitality |

| Institutional and Public Infrastructure |

| Healthcare |

| Industrial and Process |

| Other End-User Industries |

| By Service Type | Hard Services | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard Facility Management Services | ||

| Soft Services | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft Facility Management Services | ||

| By Offering Type | In-house | |

| Outsourced | Single Facility Management | |

| Bundled Facility Management | ||

| Integrated Facility Management | ||

| By End-user Industry | Commercial | |

| Hospitality | ||

| Institutional and Public Infrastructure | ||

| Healthcare | ||

| Industrial and Process | ||

| Other End-User Industries | ||

Key Questions Answered in the Report

How large is the Philippines facility management market today and where is it heading by 2031 ?

The market is valued at USD 4.38 billion in 2026 and is on track to reach USD 5.76 billion by 2031, reflecting a 5.63% CAGR.

Which service type generates the most revenue in Philippines properties ?

Hard services, led by HVAC, MEP, and fire-safety maintenance, delivered 63.12% of market turnover in 2025.

What segment is expanding fastest inside healthcare facilities ?

Outsourced integrated contracts covering biomedical equipment calibration, infection control, and laundry are growing at a 7.08% CAGR through 2031.

Why are data centers critical to future FM growth in the country ?

A USD 1.09 billion hyperscale pipeline demands 24-hour precision cooling and redundancy care, creating premium-fee opportunities for certified integrators.

How is the PPP Act changing public-sector FM contracts ?

Republic Act 11966 lets agencies bundle up to 30 years of operations and maintenance into concessions with outcome-based payouts, widening the formal opportunity pool for large-scale providers.

What is the biggest operational risk FM contractors face in 2026 ?

Volatile energy tariffs can erase margins on fixed-rate agreements, pushing providers toward energy-performance contracts that hedge consumption risk.

Page last updated on: