Malaysia Integrated Facility Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

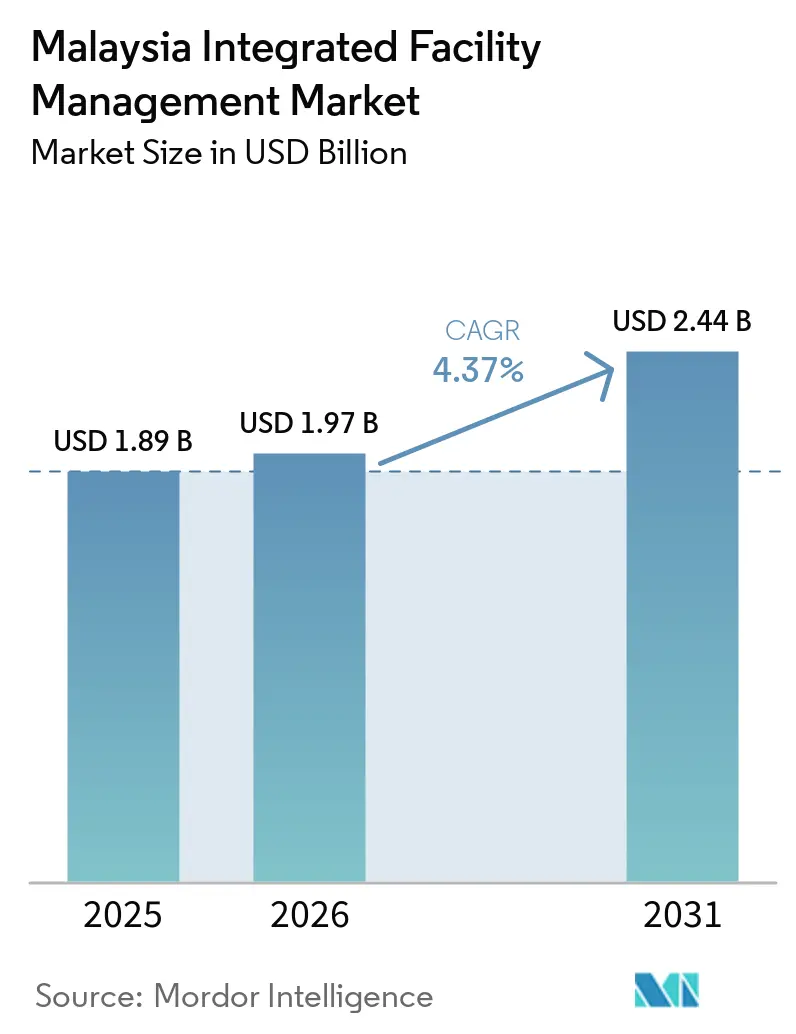

| Base Year Market Size (2025) | USD 1.89 Billion |

| Market Size (2026) | USD 1.97 Billion |

| Market Size (2031) | USD 2.44 Billion |

| Growth Rate (2026 - 2031) | 4.37% CAGR |

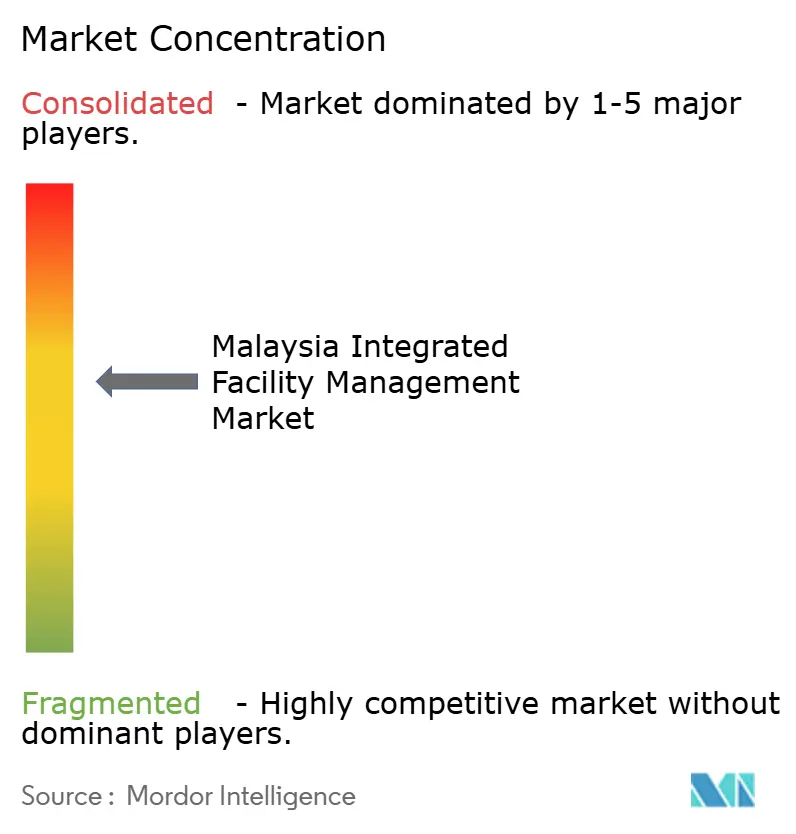

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Malaysia Integrated Facility Management Market Analysis by Mordor Intelligence

The Malaysia Integrated Facility Management Market size is expected to grow from USD 1.89 billion in 2025 to USD 1.97 billion in 2026 and is forecast to reach USD 2.44 billion by 2031 at 4.37% CAGR over 2026-2031.

Demand remained tied to Malaysia’s urban expansion, with the National Property Information Centre reporting a 12.5% year-on-year rise in total property transaction value to MYR 64.4 billion (USD 14.47 billion), in Q3 2025. This supports a larger base of managed buildings that require outsourced services over time. The 13th Malaysia Plan placed digital asset management and infrastructure resilience on the national development agenda, which strengthens the role of integrated providers across both public and private building portfolios. Malaysia’s stock of government complexes, industrial estates, data centers, healthcare facilities, and mixed-use assets is rising faster than internal maintenance teams can scale, which keeps outsourced service demand durable across the forecast period. Competition reflects a clear split between global operators with stronger technology stacks and domestic concessionaires with deeper local relationships, while contract decisions are moving steadily toward service continuity, compliance discipline, and digital maintenance capability. Cost pressure from skill shortages, dependence on foreign labour, digital investment needs, the February 2025 minimum wage increase to MYR 1,700 (USD 428.45) per month, and the July 2025 electricity tariff increase is tightening margins for smaller firms and may push the market toward gradual consolidation.

Key Report Takeaways

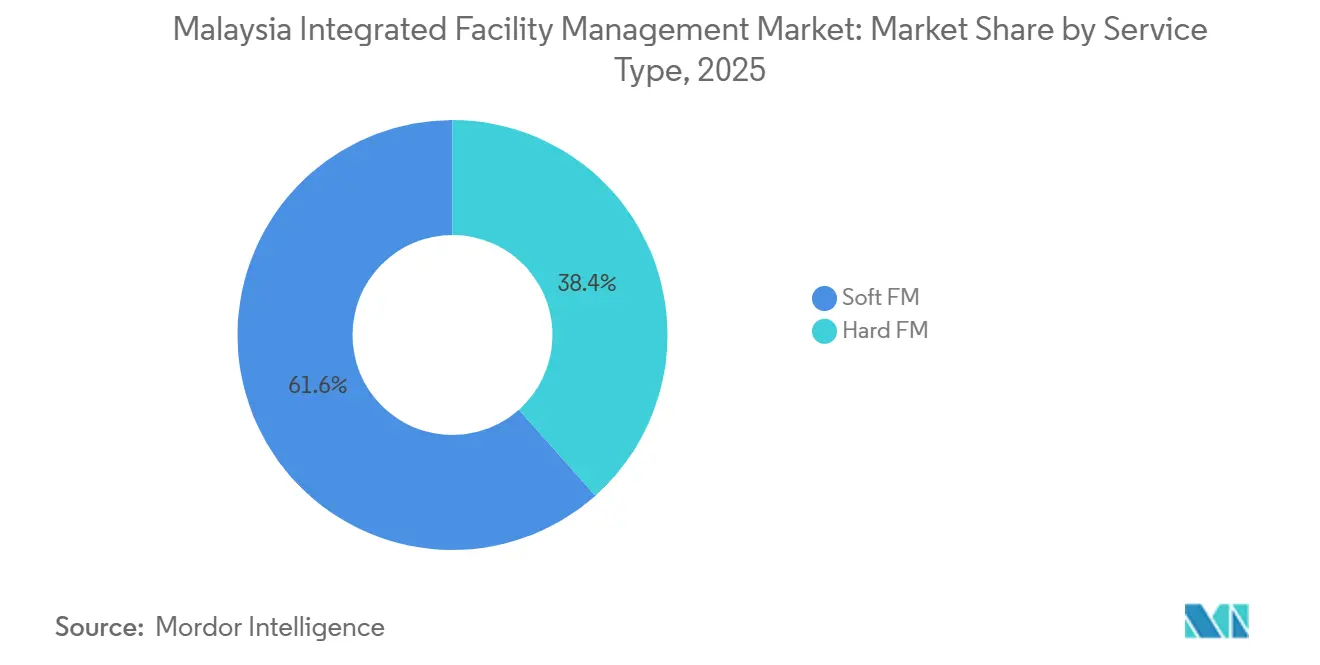

- By service type, soft facility management held 61.6% of the Malaysia integrated facility management market share in 2025, while hard facility management recorded the highest projected CAGR at 5.1% through 2031.

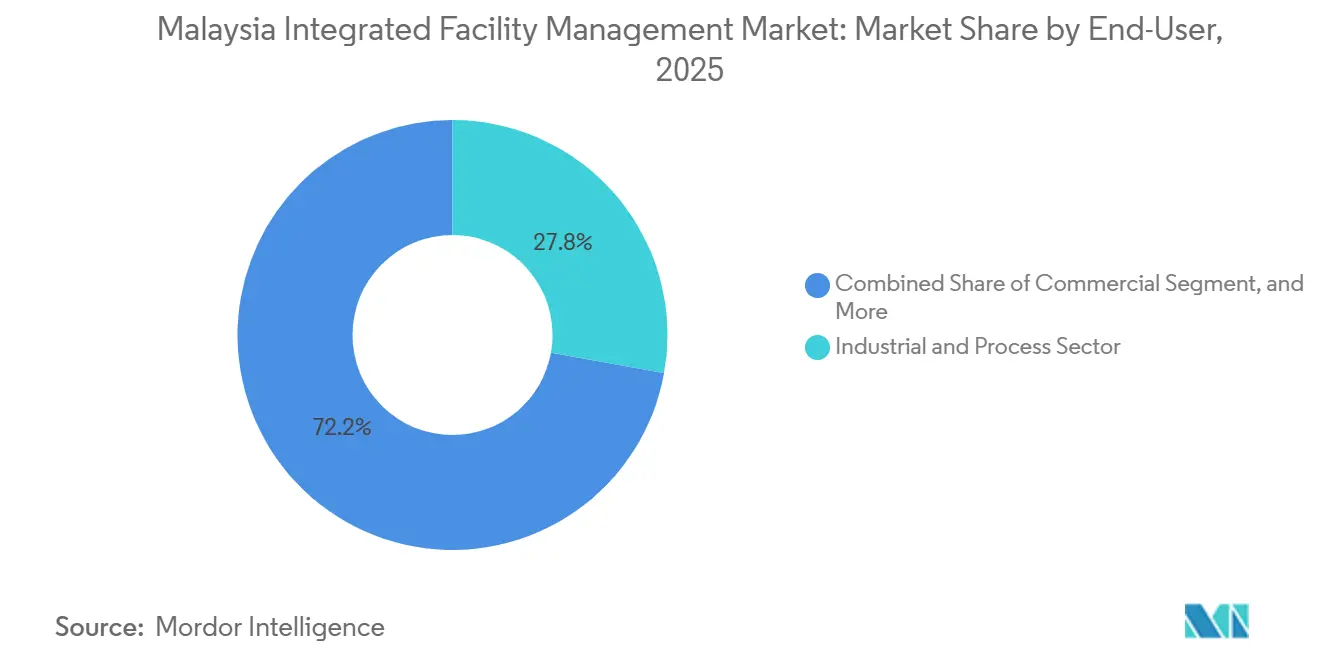

- By end-user, the industrial and process sector accounted for 27.8% of the Malaysia integrated facility management market size in 2025, while the commercial sector is forecast to expand at a 4.9% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Malaysia Integrated Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Adoption of Smart Technologies In Facility Management | +1.2% | Global, concentrated in Klang Valley and the Johor data center corridor | Medium term (2-4 years) |

| Rapid Expansion of Commercial Real Estate And Industrial Assets In Urban Centers | +0.9% | Johor-Singapore SEZ, Greater Kuala Lumpur, Penang E&E corridor | Short term (≤2 years) |

| Government Green Building Incentives And ESG Mandates | +0.6% | National, with early gains in Klang Valley and Johor | Medium term (2-4 years) |

| Rise of Public-Private Partnerships for Government Building Management | +0.4% | National, concentrated in Putrajaya, Sabah, and Sarawak | Short term (≤2 years) |

| Mandatory BIM Integration and Digital Twin Adoption in FM | +0.3% | National mandate, with deepest early impact in Klang Valley and Johor | Medium term (2-4 years) |

| Increasing Corporate Focus on Workplace Health, Wellness, and Indoor Environmental Quality | +0.2% | Global, concentrated in Klang Valley Grade A commercial stock | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of Smart Technologies in Facility Management

The Malaysia integrated facility management market is moving toward a more digital operating model as building owners expect better asset visibility, faster response times, and tighter control of maintenance spending. The July 1, 2025, BIM mandate for public and private construction projects valued at MYR 10 million (USD 2.25 million), or more raised the baseline for digital handover and made structured asset data more important when new buildings enter service.[1]Ministry of Finance Malaysia, “Treasury Circular PK 1.15,” MOF Malaysia, treasury.gov.my Asset information aligned with PeDATA and SKATA standards improves 3D visualization, scheduled maintenance, and lifecycle planning, which gives the Malaysia integrated facility management market a stronger link between project completion and ongoing service delivery.[2]Construction Industry Development Board Malaysia, “CIDB Standards And Certification Information,” CIDB, cidb.gov.my This matters because providers with BIM-linked CMMS platforms can carry forward asset histories and maintenance rules in ways that disconnected operators cannot easily match. Research cited in the draft also showed that GBI-certified buildings had a 28% adoption rate for digital twin and HVAC-BMS integration, compared with 7% in non-certified stock, which shows how premium buildings are advancing FM practices faster than the wider building base. As a result, the Malaysia integrated facility management market is rewarding operators that can combine software, building controls, and field execution into one service model rather than treating technology as a stand-alone add-on.

Rapid Expansion of Commercial Real Estate and Industrial Assets In Urban Centers

The Malaysia integrated facility management market is expanding with the country’s rising stock of commercial, industrial, logistics, and mixed-use assets, especially in Johor and the Klang Valley. Approved investments reached MYR 285.2 billion (USD 64.12 billion), in the first nine months of 2025, and Johor alone drew MYR 91.1 billion (USD 20.47 billion), which increased the long-term need for structured services across new buildings and industrial sites. CapitaLand Investment’s partnership with Coronade Properties on the 1.25 million sq ft Coronation Square Mall in Johor Bahru added another visible example of a large-format commercial asset that will require bundled maintenance, cleaning, security, landscaping, and energy management throughout its operating life. The same pattern is visible in industrial property, where portfolio expansion in logistics and manufacturing assets is creating more recurring service demand across high-use facilities with stricter uptime and compliance requirements. The Malaysia integrated facility management market is also seeing a quality shift because data centers require 24-hour uptime management, precision cooling, power continuity, and advanced fire suppression, which makes those contracts more complex than conventional office or retail work. That difference supports a stronger growth profile for providers that can manage critical environments rather than only general building operations.

Government Green Building Incentives and ESG Mandates

The Malaysia integrated facility management market is benefiting from a policy environment that gives owners clearer financial reasons to install and maintain greener building systems. The Green Investment Tax Allowance offered a 100% capital allowance under Tier 1 or 60% under Tier 2 for qualifying green technology assets, with the current incentive window running from January 1, 2024, through December 31, 2026.[3]Malaysian Green Technology and Climate Change Corporation, “Green Investment Tax Allowance,” MGTC, mgtc.gov.my The Green Technology Financing Scheme 5.0 also reopened up to MYR 1.0 billion (USD 224.7 million) in financing through December 2026 for eligible green projects, including green building construction and management, backed by a 60% to 80% government guarantee on the green component. These programs matter for the Malaysia integrated facility management market because owners who claim tax or financing support are more likely to adopt systems such as HVAC-BMS, battery energy storage, and rainwater harvesting that require regular specialist servicing after installation. The Green Building Index also requires reassessment every three years, which creates repeated compliance cycles rather than one-time certification activity. Research referenced in the draft found that model predictive control systems in Malaysian green buildings reduced energy use by 23% to 30%, which supports wider demand for energy-focused maintenance and performance monitoring services under integrated contracts.

Rise Of Public-Private Partnerships for Government Building Management

The Malaysia integrated facility management market continues to rely on government contracts as one of its most stable revenue anchors, and public-private models are widening the route through which those contracts are awarded. A 2024 pre-qualification tender issued by the Prime Minister’s Office covered federal shared buildings in the Central Zone under a public-private partnership structure and required CIDB Grade G7 certification under Category F, which keeps government work concentrated among operators with the right compliance depth. That certification threshold acts as both a quality filter and a market-access barrier, which is why the Malaysia integrated facility management market still shows a clear advantage for domestic concessionaires in public building portfolios. The healthcare side of the same model is also important, because PwC’s 2024 analysis in the draft found that 55.6% of Malaysia’s historical healthcare PPP projects focused on hospital support services, biomedical engineering maintenance, and laundry. The CIDB FM PRO Apprentice 2026 program also points to stronger institutional support for this channel, since it trains G1 to G4 contractors in integrated facility management and gives the top five participants sponsored UAE placements for hands-on exposure. Over time, this makes the Malaysia integrated facility management market more capable of supporting broader PPP use without relying only on the current pool of large incumbents.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Market Structure with Compliance and Certification Challenges | -0.8% | National, most acute for mid-market and SME operators | Medium term (2-4 years) |

| High Initial Capital Requirements for Technology Adoption and System Integration | -0.5% | National, deepest constraint for operators outside Klang Valley | Long term (≥4 years) |

| Shortage of Technically Skilled FM Professionals and High Workforce Turnover | -0.4% | National, intensified in Johor and Klang Valley due to labour competition | Short term (≤2 years) |

| Regulatory and Competitive Barriers For International Operators | -0.3% | National, concentrated in government procurement and listed concessions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented Market Structure with Compliance and Certification Challenges

The Malaysian integrated facility management market has a healthy demand base, but service quality remains uneven because a large share of providers still operate at a small scale across local tender markets. A 2024 literature review cited in the draft found that the sector’s main challenge was the lack of standardized maintenance processes across operators, which leads to inconsistent delivery quality and weaker contract renewal potential. Providers also need to manage overlapping registration and approval requirements across CIDB, the Ministry of Finance, JKR-linked public works structures, and healthcare-specific rules, which can be difficult for mid-sized firms with limited compliance staff. This keeps a meaningful share of government-linked work within a relatively small certified pool, even when the broader Malaysia integrated facility management market remains crowded. The same fragmentation also makes it harder for clients to compare providers on a standard basis because performance measures are not yet uniform across contracts. As long as certification depth and operating discipline remain uneven, the Malaysia integrated facility management market will continue to show a split between well-qualified concessionaires and a more price-led middle tier.

High Initial Capital Requirements for Technology Adoption and System Integration

The Malaysia integrated facility management market is also constrained by the cost of digital transformation, especially for firms that do not have large concession contracts or strong balance sheets. The draft highlighted that BIM deployment requires spending on hardware, cloud infrastructure, LOD 500-compliant asset modelling, PeDATA and SKATA licensing, and workforce training, which raises the entry cost for smaller operators. A study of Malaysian FM professionals also identified high upfront investment, difficulty proving return on investment, and a shortage of BIM-capable staff as the three most-cited barriers to digital twin adoption in FM. The July 2025 electricity tariff increase added pressure at the same time because operators are now paying more to run buildings while also being pushed to install efficiency systems that demand new capital outlays. The draft noted that digital twin and smart HVAC-BMS payback periods averaged 2.2 to 3.1 years in Malaysia, which is a long period for firms working on tight payment cycles and modest cash reserves. This creates a two-speed pattern in the Malaysia integrated facility management market, in which larger firms can keep upgrading their operating model while smaller firms delay investment and risk falling behind on service quality.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Soft FM Leads While Hard FM Gains Technical Momentum

Soft Facility Management (FM) accounted for 61.6% of the Malaysia integrated facility management (IFM) market size in 2025, which shows how strongly the market still depends on recurring labour-based services across public, commercial, and institutional buildings. Cleaning, security, pest control, landscaping, waste management, catering, and reception services stayed dominant because they are needed frequently and across a broad building base, unlike mechanical maintenance, which follows a more periodic schedule. In the Malaysia IFM industry, those soft service categories also face the most intense price competition because switching costs remain low in cleaning and guarding contracts. Providers therefore rely heavily on workforce control, route planning, attendance tracking, and tighter scheduling to protect margins in contracts that are large by volume but thinner in profitability. The February 2025 minimum wage increase to MYR 1,700 (USD 382) per month placed extra pressure on this segment because labour cost is still the largest cost item in most soft service contracts.

Hard FM is forecast to grow at a 5.1% CAGR through 2031, making it the fastest-growing service category within the Malaysia IFM market. This part of the market is being lifted by more technically demanding buildings that need specialized work across electromechanical systems, HVAC, fire safety, and mission-critical infrastructure. The Malaysia IFM market share is still led by Soft FM, but Hard FM is closing the gap in value terms because each contract now carries more technical scope and tighter uptime requirements. Data center development in Johor is an important reason, since facilities operating at low PUE levels and under 24-hour service expectations need precision cooling, power continuity, and constant optimization that go beyond conventional commercial maintenance. Johnson Controls’ work across multiple Sunway Group properties also shows how one building technology deployment can spread across a developer’s wider portfolio, which strengthens repeat hard-service revenue once performance is proven. In the Malaysia IFM industry, the July 2025 BIM requirement also supports Hard FM because digital handover makes it easier to structure asset maintenance from the first day a building enters operation.

By End-User: Industrial And Process Holds the Largest Base While Commercial Expands Fastest

Industrial and process captured 27.8% of the Malaysia IFM market share in 2025, which made it the largest end-user group by revenue. The segment’s weight reflects the scale and operating complexity of Malaysia’s manufacturing, utilities, and process facilities, where maintenance standards are linked closely to uptime, worker safety, and environmental control. The Johor-Singapore SEZ has strengthened that position further because advanced manufacturing and clean energy were identified as priority areas, which raises the need for higher-specification support services around industrial assets. Industrial contracts also tend to run longer and cover more technical scope than routine commercial work, which helps explain why the segment leads the Malaysia integrated facility management market despite a smaller site count than the total commercial property base. This part of the market also benefits from the fact that factory operators usually prefer planned preventive maintenance and compliance-led service routines rather than ad hoc repair work.

Commercial is projected to expand at a 4.9% CAGR through 2031, making it the fastest-growing end-user category in the Malaysia IFM market. Growth is coming from several sources at the same time, including hyperscale data centers, newer Grade A offices, retail developments, warehousing assets, and fintech-led office demand. The commercial segment therefore sits at the point where Soft FM volume and Hard FM complexity increasingly meet, especially in buildings that must satisfy ESG, occupant comfort, and uptime expectations together. Retail and office properties add recurring demand for cleaning, security, and tenant services, while data centers and digital infrastructure raise the need for specialized technical maintenance that carries higher contract value. Hospital and public infrastructure projects in Melaka, Penang, and Sarawak also show how healthcare and institutional demand remain steady in the wider Malaysia IFM market, even if commercial is expanding faster at present. The other end-user group, which includes multi-house residential estates and mixed-use communities, is still smaller, but township development and build-to-rent activity in the Klang Valley and Johor are creating a larger future pipeline for integrated operators.

Geography Analysis

The Malaysia integrated facility management market remained anchored in the Klang Valley because this corridor has the country’s deepest concentration of Grade A offices, government facilities, healthcare sites, and regional headquarters. The area also has the most mature client base, which means occupiers and owners are more likely to seek integrated contracts that combine maintenance, compliance, energy management, and tenant-facing services. Modern premium offices in the Klang Valley continued to attract demand because energy efficiency and indoor environmental quality increasingly affect tenant choice and rental resilience, thereby raising the value of providers that can manage certified buildings effectively. Putrajaya gives this corridor another layer of stability, since public-sector procurement remains a consistent source of recurring work for firms with the right concession and certification credentials. Perbadanan Putrajaya awarded more than MYR 100 million (USD 22.47 million), in facilities management and maintenance contracts during 2025 across residential quarters, convention facilities, and neighborhood complexes, which shows the depth and regularity of public demand in this part of the Malaysia integrated facility management market.

Johor is the most dynamic growth geography in the Malaysia integrated facility management market because investment inflows are changing both the scale and the quality of demand. The Johor-Singapore SEZ, the RTS Link due by the end of 2026, and the state’s data center construction pipeline are creating more large, technical, and long-duration contracts than the state handled a few years ago. Data center operations are especially important because they require redundant power systems, strict humidity and temperature control, uninterrupted operations, and advanced fire suppression, which gives Johor a higher-value service mix than a standard office-led growth story. CapitaLand Investment’s planned Coronation Square Mall in Johor Bahru also points to a longer stream of retail-related contracts that will extend well beyond initial construction and into daily operations. The advanced manufacturing and medtech focus within the Johor-Singapore SEZ adds another layer of diversification, so the Malaysia integrated facility management market in Johor is not dependent on one asset class alone.

Penang’s role in the Malaysia integrated facility management market is tied to its electronics manufacturing base and rising healthcare infrastructure. The state combines industrial demand with medical services and medical tourism, which creates a balanced mix of technical maintenance, compliance-driven building operations, and occupant support services. Hospital development in Bertam, under a build-and-lease arrangement signed in March 2025, is a good example because the asset will generate facilities management needs over a long operating horizon once it comes into service. East Malaysia, especially Sabah and Sarawak, still leans more heavily on concession-based public contracts, which means growth is steadier and more institution-led than in Penang or Johor. AWC’s concession extension in Sarawak and Weida’s 20-year Sarawak General Hospital structure show that the Malaysia integrated facility management market in East Malaysia is gradually shifting toward larger, longer-duration frameworks that can justify sustained capacity deployment by specialized operators.

Competitive Landscape

The Malaysia integrated facility management market has a moderately consolidated, so competitive conditions depend heavily on the contract type and client group. Domestic concessionaires keep an advantage in government work because long-standing JKR relationships, CIDB Grade G7 capability, and experience in public procurement remain difficult for new entrants to replicate quickly. International firms are more visible in premium commercial portfolios, where clients value standardized reporting, multi-site delivery, global procurement support, and stronger technology platforms. This means the Malaysia integrated facility management market is no longer being shaped only by price competition, especially in contracts tied to data centers, healthcare, or certified green buildings. Instead, differentiation is moving toward bundled service delivery, stronger compliance systems, and the ability to turn building data into better uptime and lower lifecycle cost.

Leading operators in the Malaysia integrated facility management market are also widening the scope of what they sell under one contract. Hard FM and Soft FM are increasingly being combined under integrated agreements, while predictive maintenance, connected sensors, and energy management are being added as value layers rather than offered separately. Honeywell’s Advance Control for Buildings reflects that shift because the solution is positioned for settings such as data centers and healthcare facilities, where cybersecurity, machine-learning-enabled automation, and faster network performance improve the case for smart building operations. Johnson Controls’ wider engagement across Sunway Group assets also shows how performance in one property can lead to portfolio-level adoption when owners see measurable savings and operating consistency. In the Malaysia integrated facility management market, that kind of portfolio expansion is becoming one of the clearest ways for firms to deepen client relationships and extend contract life without relying only on fresh tender wins.

The main white space in the Malaysia integrated facility management market lies in data center operations, healthcare support under PPP structures, and small to medium commercial assets in secondary cities where systematic coverage is still limited. Technology-led challengers are entering through CMMS, building automation, and analytics-based service models, which means some new competitors are winning contracts because they can prove performance instead of relying only on relationship-led selling. ISS reported 4.3% organic growth and a 94% client retention rate globally in 2025, which supports the broader view that data-backed retention and cross-selling are becoming more important in integrated service markets. As this logic spreads, the Malaysia integrated facility management market is likely to see a wider gap between digitally capable incumbents and smaller firms that still depend on manual processes and price-led tendering.

Malaysia Integrated Facility Management Industry Leaders

UEM Edgenta Berhad

GFM Services Berhad

ISS A/S

CBRE Group, Inc.

JLL Property Services (Malaysia) Sdn. Bhd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: AWC Berhad Clinches MYR 99.12 million (USD 22.29 Million), IFM Contract from Telekom Malaysia. AWC's subsidiary Ambang Wira Sdn Bhd secured a 5-year integrated facilities management contract from TM Technology Services Sdn Bhd, covering data centers and buildings at TM Central 1. The deal runs from November 1, 2025, to October 31, 2030, and elevates the company's positioning in the fast-growing data center FM sub-market.

- February 2026: GFM Services Bags MYR 367.2 million (USD 82.52 Million), FM Contract for Istana Negara. GFM Services Bhd secured a 5-year FM contract from JKR for Istana Negara, Kuala Lumpur, lifting its order book to MYR 1.41 billion (USD 316.9 million). The win demonstrates the scale achievable through government landmark concessions and reinforces GFM's position as a public-sector FM specialist.

- February 2026: Weida Secures MYR 351 million (USD 78.88 Million), 20-Year Government Concession for Sarawak General Hospital. Weida (M) Bhd's associate signed a 20-year build-lease-maintain-transfer concession with the Ministry of Health for Sarawak General Hospital, expanding the use of long-horizon PPP structures for healthcare FM in East Malaysia.

- January 2026: AWC Berhad Wins MYR 82.5 million (USD 18.54 Million), JKR Contract for Putrajaya Government Buildings. AWC's subsidiary secured a 5-year FM and maintenance contract for Kompleks E buildings in Presint 1, Putrajaya, from January 1, 2026, to December 31, 2030, housing the Ministry of Education and the Department of National Unity.

Malaysia Integrated Facility Management Market Report Scope

The Malaysia Integrated Facility Management Market Report is Segmented by Service Type (Hard Facility Management [Asset Management, MEP and HVAC Services, Fire Systems and Safety, and Other Hard Facility Management Services], and Soft Facility Management [Office Support and Security, Cleaning Services, Catering Services, and Other Soft Facility Management Services]), End User (Commercial (includes BFSI, IT and Telecom, Retail and Warehouses, etc.), Hospitality (includes Eateries, Restaurants and Large-Scale Hotels), Institutional and Public Infrastructure (includes Government Establishments, Educatioand other Soft Facility Management Services, Transportation such as Airports and Railways, etc.), Healthcare (includes Public and Private Healthcare Facilities), Industrial and Process Sector (includes Manufacturing, Energy including Oil and Gas Exploration, Mining, etc.), and Other End-User Industries (Multi-House Residential, Entertainment, Sports and Leisure)). The Market Forecasts are Provided in Terms of Value (USD).

| Hard Facility Management | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard Facility Management Services | |

| Soft Facility Management | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft Facility Management Services |

| Commercial |

| Hospitality |

| Institutional and Public Infrastructure |

| Healthcare |

| Industrial and Process Sector |

| Other End-User Industries |

| By Service Type | Hard Facility Management | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard Facility Management Services | ||

| Soft Facility Management | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft Facility Management Services | ||

| By End User Industry | Commercial | |

| Hospitality | ||

| Institutional and Public Infrastructure | ||

| Healthcare | ||

| Industrial and Process Sector | ||

| Other End-User Industries | ||

Key Questions Answered in the Report

What is the 2031 outlook for integrated facility management in Malaysia?

The Malaysia integrated facility management market was valued at USD 1.89 billion in 2025 and is forecast to reach USD 2.44 billion by 2031, growing at a 4.4% CAGR over 2026-2031.

Which service category leads revenue in Malaysia?

Soft FM led in 2025 with 61.6% share, supported by recurring demand for cleaning, security, landscaping, catering, and other labour-based services across public and commercial buildings.

Which service category is growing the fastest through 2031?

Hard FM is forecast to grow the fastest at a 5.1% CAGR, driven by data centers, healthcare facilities, and more complex commercial and industrial buildings.

Which end-user group holds the largest base today?

Industrial and process was the largest end-user segment in 2025 with 27.8% share, reflecting the technical needs of manufacturing, utilities, and process facilities.

Why is Johor becoming more important for facility management providers?

Johor is benefiting from the Johor-Singapore SEZ, the RTS Link, major commercial projects, and a strong data center pipeline, all of which are creating larger and more technical service contracts.

What is the main challenge holding smaller operators back?

Smaller firms face a mix of certification burdens, skill shortages, wage pressure, and high digital investment costs, especially for BIM, IoT, CMMS, and smart building integration.

Page last updated on: