Cell Therapy Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

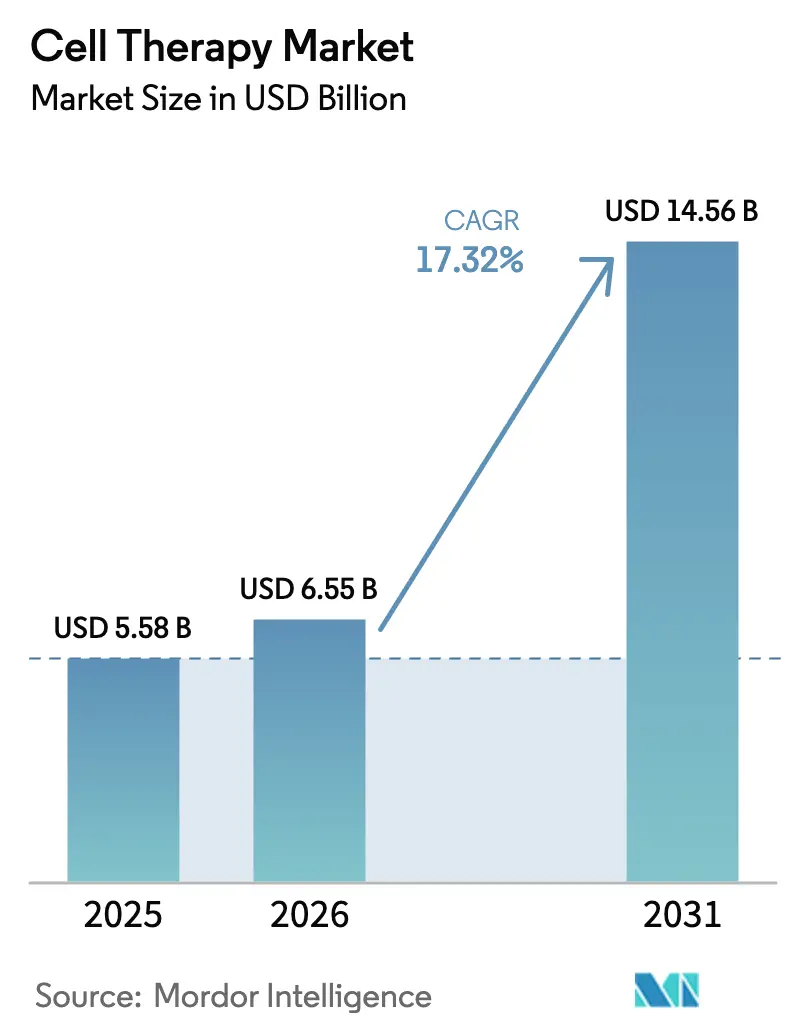

| Market Size (2026) | USD 6.55 Billion |

| Market Size (2031) | USD 14.56 Billion |

| Growth Rate (2026 - 2031) | 17.32% CAGR |

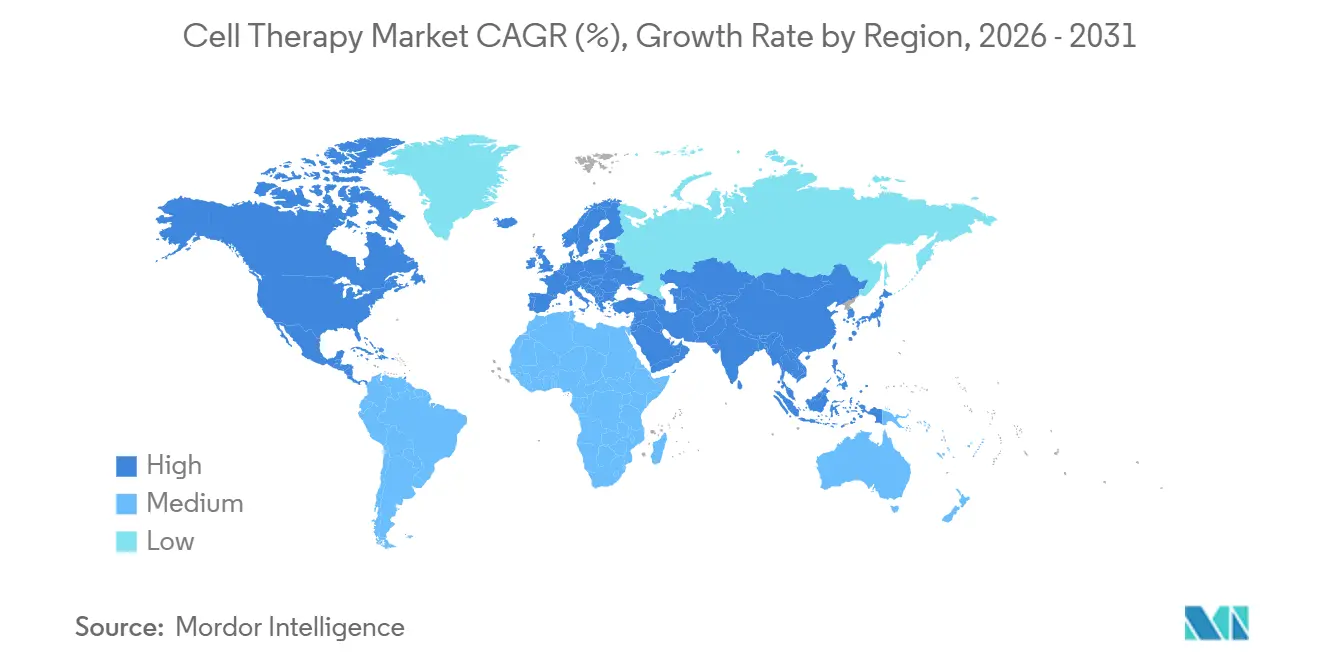

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cell Therapy Market Analysis by Mordor Intelligence

The Cell Therapy Market size is expected to increase from USD 5.58 billion in 2025 to USD 6.55 billion in 2026 and reach USD 14.56 billion by 2031, growing at a CAGR of 17.32% over 2026-2031.

Rising approvals for autologous chimeric antigen receptor T-cell (CAR-T) products, the pivot toward allogeneic platforms, and new reimbursement pathways in the United States, Europe, and Asia-Pacific are widening patient access and shortening time-to-revenue cycles. Contract development and manufacturing organizations (CDMOs) added 180,000 liters of allogeneic capacity between 2024 and 2025, cutting clinical-grade lead times from 8 weeks to 3 weeks and lowering production costs significantly. Medicare’s New Technology Add-on Payment (NTAP) program in the United States has reduced hospital exposure by covering up to 65% of costs above the diagnosis-related group rate for 11 cell therapies, encouraging provider adoption.

Key Report Takeaways

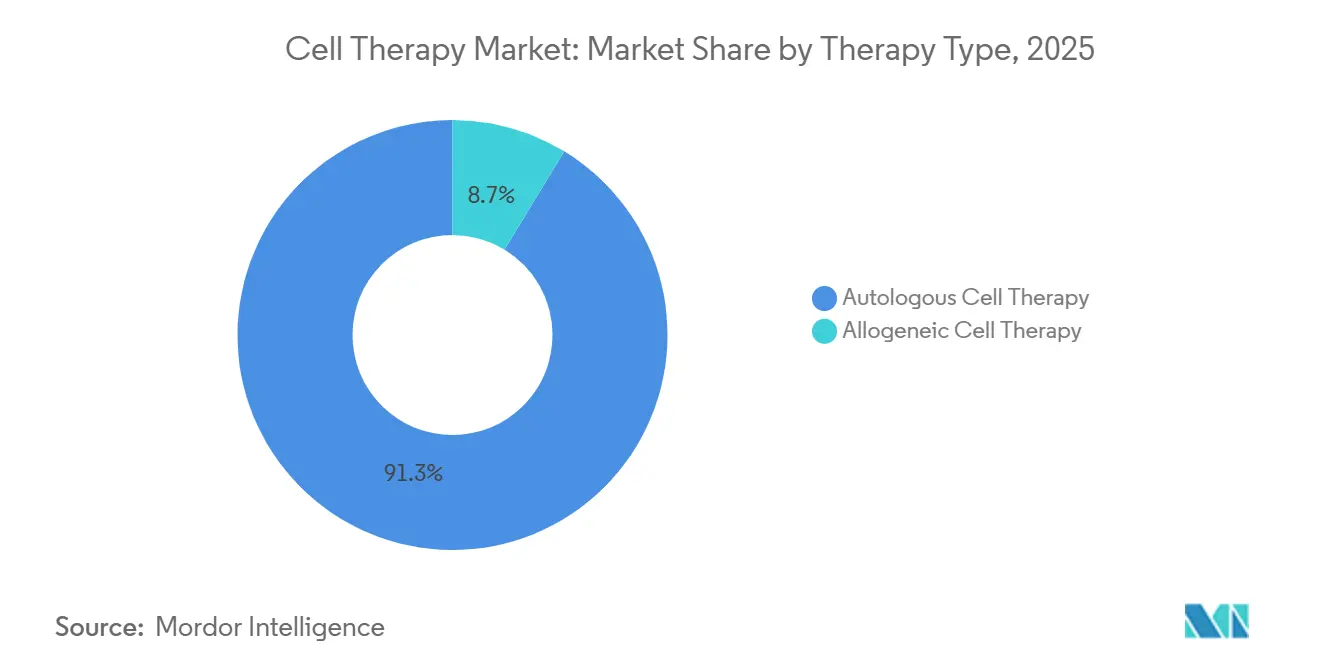

- By therapy type, autologous CAR-T maintained 91.3% of the cell therapy market share in 2025, but allogeneic therapies posted the highest growth at a 17.34% CAGR through 2031.

- By cell type, immune-cell platforms led with 56.1% revenue in 2025; stem-cell products recorded the fastest 18.32% CAGR to 2031.

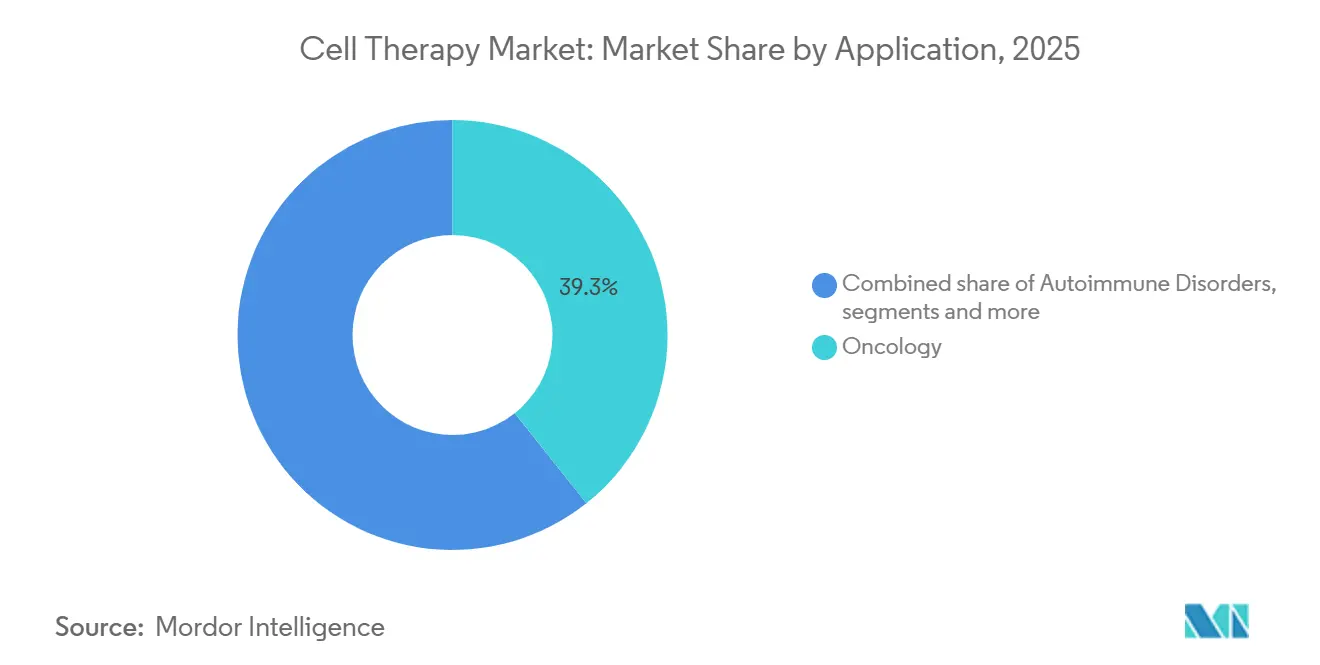

- By application, oncology captured 39.3% revenue in 2025, while neurological disorders expanded at a 17.47% CAGR on the back of late-stage Parkinson’s disease programs.

- By end user, hospitals and clinics accounted for 65.2% spending in 2025; specialized cell-and-gene centers scaled at an 18.08% CAGR as payers favored dedicated infrastructure.

- By geography, North America held 54.2% of the cell therapy market size in 2025; Asia-Pacific registered the fastest 17.89% CAGR, driven by four domestic CAR-T approvals in China during 2024.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cell Therapy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising approvals and commercial launches of autologous CAR-T therapies | +4.2% | North America, Europe | Short term (≤ 2 years) |

| Build-out of global CDMO capacity for allogeneic pipelines | +3.8% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Expansion of national reimbursement pathways | +3.1% | Germany, United States, Japan, South Korea | Medium term (2-4 years) |

| Indication expansion beyond oncology into autoimmune and cardiovascular diseases | +2.9% | Global | Long term (≥ 4 years) |

| AI-optimized closed bioreactor systems cutting costs ≥40% | +2.2% | Major manufacturing hubs | Medium term (2-4 years) |

| Integration of 3D-bioprinted scaffolds enabling combination implants | +1.0% | United States, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Approvals and Commercial Launches of Autologous CAR-T Therapies

The United States Food and Drug Administration (FDA) and the European Medicines Agency (EMA) approved nine new CAR-T indications between 2024 and 2025, reducing median review time from 14 months to 9 months [1]U.S. Food and Drug Administration, “Approved Cellular and Gene Therapy Products,” fda.gov. Novartis reported USD 680 million in 2025 revenue for Kymriah, reflecting 28% growth following label expansion to follicular lymphoma. European conditional approvals for three autologous T-cell receptor therapies in 2025 were the first for solid tumors, unlocking a USD 2.1 billion addressable segment by 2028. United States commercial payers linked 30–50% of reimbursement to six-month complete response rates across five CAR-T products in 2024, lowering upfront risk for hospitals. Japan’s regenerative-medicine fast-track designation halved review times for candidates with Phase 2 data showing ≥40% objective responses.

Build-Out of Global CDMO Capacity for Allogeneic Pipelines

CDMOs installed 180,000 liters of allogeneic capacity from 2024 to 2025, including Lonza’s 50,000-liter Portsmouth facility and Charles River’s 40,000-liter Leiden site. Off-the-shelf platforms now generate a therapy batch within 48 hours, down from 4-6 weeks for autologous processes, and the cost-of-goods dropped from USD 350,000 to USD 75,000 per dose. Allogene Therapeutics’ ALPHA2 candidate delivered 67% complete remission in large B-cell lymphoma and targets a U.S. biologics license filing by mid-2026. Vertex and CRISPR Therapeutics committed USD 420 million to a Swiss base-edited T-cell plant, aiming for 100,000 annual doses by 2028. Samsung Biologics’ USD 300 million Incheon facility secured four regional contracts, signaling Asia-Pacific supply-chain localization.

Expansion of National Reimbursement Pathways

Germany’s NUB pathway allowed hospitals to bill three allogeneic candidates ahead of full health-technology assessment, accelerating revenue capture by up to 24 months. Medicare’s NTAP program added 11 cell therapies in 2025, with USD 80,000–200,000 per-case top-ups that eased provider economics. Japan’s conditional reimbursement pathway enabled formulary entry with Phase 2 data in 2024 on the condition of seven-year post-market surveillance. South Korea priced two locally manufactured CAR-Ts at 40% below U.S. list levels, opening access to 1,200 patients annually. The United Kingdom’s final National Institute for Health and Care Excellence (NICE) guidance unlocked GBP 120 million in National Health Service funding for second-line large B-cell lymphoma in 2025.

AI-Optimized Closed Bioreactor Systems Cutting COGs Greater Than 40%

Lonza’s Cocoon platform delivered a 42% per-dose cost reduction for autologous CAR-T production compared with open systems by automating glucose feeds and oxygen control [2]Lonza Group, “Q2 2025 Earnings Transcript,” lonza.com. Machine-learning algorithms trained on 18,000 runs predicted cell viability with 94% accuracy, lowering batch-failure rates to 2%. Kite Pharma trimmed vein-to-vein time for Yescarta from 27 days to 16 days after four U.S. sites adopted automated lines in 2024. Fate Therapeutics hit USD 50,000 cost-of-goods per dose for iPSC-derived NK cells via 21-day continuous perfusion. The FDA recognized AI-controlled bioreactors as compliant process-analytical technology in 2025, allowing post-approval algorithm updates without fresh filings.

Restraints Impact Analysis*

| Restraint | (~) (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost-of-goods for personalized autologous batches | -2.8% | Global | Short term (≤ 2 years) |

| Viral-vector and plasmid supply-chain bottlenecks | -1.9% | North America, Europe | Medium term (2-4 years) |

| Long-term genomic-integrity data gaps post-editing | -1.2% | Global | Long term (≥ 4 years) |

| ESG scrutiny of donor tissue and cryogenic logistics | -0.7% | Europe, North America, Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost-of-Goods for Personalized Autologous Batches

Autologous CAR-T production averaged USD 350,000 per dose in 2025, driven by patient-specific apheresis, viral-vector transduction, and two-week expansion cycles. Yescarta’s average selling price fell 18% between 2023 and 2025 under outcomes-based contracts, trimming gross margin from 82% to 71%. German and French payers introduced EUR 100,000 per QALY thresholds in 2024, forcing 35% confidential discounts and squeezing profitability. High fixed costs of USD 12 million annually per GMP suite undermine scale for therapies addressing fewer than 500 patients per year. Limited affordability in middle-income countries, where per-capita health spending is below USD 2,000, restricts diffusion and caps revenue growth potential.

Viral-Vector and Plasmid Supply-Chain Bottlenecks

Lentiviral-vector shortages delayed 11 Phase 2 cell-therapy trials in 2024, stretching lead times from 16 weeks in 2022 to 32 weeks in 2024. Thermo Fisher reported a USD 1.8 billion services backlog in Q1 2025 and added 20,000 liters of extra capacity slated for Q4 2026 to ease constraints. Plasmid DNA lead times exceeded 24 weeks in 2024, with 40% price inflation year-over-year. FDA guidance in July 2024 supported non-viral electroporation and lipid-nanoparticle methods for early-phase trials, and six sponsors adopted these approaches by year-end FDA.GOV. Lonza and Catalent committed USD 1.1 billion to viral-vector expansion in 2024, but analysts project a 30% supply deficit through 2028.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

Therapy Type: Allogeneic Platforms Reshape Manufacturing Economics

Autologous products held 91.3% of the cell therapy market share in 2025, supported by mature CAR-T franchises and established reimbursement pathways. However, the allogeneic segment is advancing at a 17.34% CAGR through 2031 as off-the-shelf availability removes the 4-6 week manufacturing wait, lowers cost-of-goods to USD 75,000, and streamlines logistics.

Investor confidence intensified in 2025 when Vertex and CRISPR Therapeutics backed a Swiss plant designed for 100,000 doses annually, underscoring the scalability edge of allogeneic platforms. Regulatory flexibility, such as FDA acceptance of non-viral transfection, has shortened timelines, while outcomes-based contracting is tightening margins for autologous players. Allogeneic candidates, therefore, position the cell therapy market for cost-efficient penetration into less-affluent geographies without sacrificing margin integrity.

By Cell Type: Stem Cells Gain on Immune Platforms

Immune-cell therapies dominated 56.1% revenue in 2025, largely from CAR-T and tumor-infiltrating lymphocyte programs endorsed by strong oncology data. Stem-cell platforms are expanding at an 18.32% CAGR as mesenchymal and induced pluripotent stem-cell (iPSC) candidates demonstrate efficacy in cardiovascular and neurological disorders.

Mesoblast’s Phase 3 heart-failure trial cut major adverse events by 34%, while Takeda’s iPSC cardiomyocytes are enrolling ischemic patients with the first readout expected in 2026. Breakthroughs in scaffold and 3D-printing technologies are further elevating stem-cell momentum, positioning them as the cell therapy market’s diversification engine beyond hematologic malignancies.

By Application: Neurological Disorders Outpace Oncology Growth

Oncology delivered 39.3% revenue in 2025, yet neurological disorders are the fastest-growing application, posting a 17.47% CAGR through 2031, thanks to iPSC-derived dopaminergic neuron programs that achieved 32% Unified Parkinson’s Disease Rating Scale motor improvement at 12 months. Autoimmune indications also gained traction as systemic lupus erythematosus entered late-stage evaluation with 73% remission.

Cardiovascular, orthopedic, and ophthalmology segments are emerging as next-wave opportunities on the strength of mesenchymal, chondrocyte, and retinal-cell trials. These trends diversify the cell therapy market size base, lowering reliance on oncology and smoothing revenue volatility linked to competitive saturation in B-cell malignancies.

By End User: Specialized Centers Scale Faster Than Hospitals

Hospitals and clinics accounted for 65.2% of 2025 outlays, but specialized cell-and-gene centers are scaling at an 18.08% CAGR by standardizing apheresis, cryopreservation, and post-infusion care. Mayo Clinic’s 12-bed unit treated 180 patients in its first year and reduced cytokine-release-syndrome admissions to 4%, versus a 12% national benchmark.

Academic institutes drive Phase 1-2 innovation, while CDMOs provide industrialized capacity that underpins the cell therapy market size for allogeneic pipelines. High hospital utilization rates of 85% in top U.S. centers create bottlenecks, amplifying the strategic value of purpose-built facilities.

Geography Analysis

North America recorded a 54.2% share in 2025, with NTAP covering USD 80,000-200,000 per case and five commercial insurers shifting 30-50% payment to outcome-based models. Approvals rose to nine indications for CAR-T therapy between 2024-2025, and Yescarta revenue grew 22% to USD 2.1 billion. High apheresis-suite utilization at 85% created 6-8-week waits, underscoring capacity constraints.

Europe held a 28% share as Germany’s NUB pathway accelerated billing for three allogeneic therapies, while NICE guidance released GBP 120 million in U.K. funding. Conditional approvals for T-cell receptors targeting solid tumors opened a USD 2.1 billion European opportunity. However, QALY thresholds introduced in 2024 require an average of 35% discounts, tempering revenue expansion.

Asia-Pacific registered the fastest 17.89% CAGR; China’s first domestic CAR-T approval, Carvykti, addressed 2,500 multiple-myeloma patients in year one. Japan’s conditional reimbursement route accepted Phase 2 data with a mandatory seven-year follow-up. South Korea reimbursed two local CAR-Ts at 40% lower prices, serving 1,200 patients in 2025. Supply-chain localization via Samsung Biologics and growing CDMO capacity are consolidating the region as the cell therapy market’s next growth engine.

Competitive Landscape

The cell therapy market exhibits moderate concentration: the top five companies, Novartis, Gilead Sciences, Bristol Myers Squibb, Johnson & Johnson, and Legend Biotech captured a significant share of 2025 autologous CAR-T revenue [3]Novartis AG, “Annual Report 2025,” novartis.com. Label expansions and earlier-line oncology approvals underpin incumbents’ defenses, but allogeneic entrants and CDMOs are redistributing share. Vertex and CRISPR’s USD 420 million Swiss facility signals manufacturing scale as a strategic moat, while Allogene Therapeutics posted 67% complete remission in pivotal trials.

Emerging disruptors such as Fate Therapeutics achieved a USD 50,000 per-dose cost, and Samsung Biologics has secured four Asia-Pacific contracts, underscoring how technology and localized capacity shift competitive dynamics. Patent-filing velocity is high. CRISPR Therapeutics registered 14 base-editing patents across 2024-2025 while regulators mandate 15-year follow-up for gene-edited products, favoring well-capitalized firms. Cost-reduction technologies like AI-optimized bioreactors and 3D-printed scaffolds are lowering entry barriers, intensifying rivalry across oncology, autoimmune, and neurologic segments.

Strategic moves in 2025 included Sanofi’s USD 1.2 billion Amunix acquisition, Lonza’s 50,000-liter Portsmouth facility, and Charles River’s 40,000-liter Leiden expansion, each aiming to secure capacity ahead of anticipated demand spikes. As reimbursement models pivot to outcomes and supply scales, competitive advantage is defined increasingly by manufacturing agility, indication breadth, and post-market surveillance infrastructure.

Cell Therapy Industry Leaders

Corestem Inc.

Chiesi Farmaceutici S.p.A.

Tego Science

Allogene Therapeutics Inc.

Takeda Pharmaceuticals

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: FDA approved Waskyra (etuvetidigene autotemcel), a gene therapy for patients with Wiskott-Aldrich syndrome (WAS), marking the first approved treatment of its kind for this rare and life-threatening immunodeficiency.

- November 2025: Bharat Biotech International Ltd entered the cell and gene therapy sector by launching Nucelion Therapeutics Pvt Ltd, a wholly owned CRDMO dedicated to research, development, and manufacturing in the cell therapy industry.

- January 2025: Gameto’s Fertilo gets FDA clearance for a phase 3 trial, pioneering iPSC-based fertility treatment to shorten IVF cycles and improve reproductive care.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the cell therapy market as all investigational and commercial products in which viable human cells, stem, immune, or tissue-specific, are introduced into a patient to repair, replace, or modulate biological functions. This spans autologous and allogeneic modalities, with oncology, cardiovascular, neurological, orthopedic, autoimmune, and wound-healing applications included.

Scope Exclusion: Gene-only vectors and acellular regenerative scaffolds lie outside our remit.

Segmentation Overview

- By Therapy Type

- Autologous Cell Therapy

- Allogeneic Cell Therapy

- By Cell Type

- Stem Cell Therapy

- Hematopoietic Stem Cells

- Mesenchymal Stem Cells

- Induced Pluripotent Stem Cells

- Immune Cell Therapy

- T-Cell Therapy (incl. CAR-T, TCR-T)

- NK-Cell Therapy

- Dendritic Cell Therapy

- Fibroblast & Chondrocyte-based Therapies

- Stem Cell Therapy

- By Application

- Oncology

- Autoimmune Disorders

- Cardiovascular Diseases

- Orthopedic & Musculoskeletal

- Neurological Disorders

- Wound Healing & Dermatology

- Ophthalmology

- By End User

- Hospitals & Clinics

- Specialized Cell- & Gene-Therapy Centers

- Academic & Research Institutes

- Contract Manufacturing & CRO Facilities

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of APAC

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Multiple conversations with cell-therapy manufacturers, transplant centers, payers, and principal investigators across North America, Europe, and Asia help validate addressable patient pools, average treatment costs, batch yields, and rollout bottlenecks. Insights from these stakeholders let us adjust model variables where desk sources are silent or dated.

Desk Research

Mordor analysts first map the evidence base through open sources such as FDA CBER approval archives, EMA PRIME listings, ClinicalTrials.gov, WHO Global Observatory for Cell and Gene Therapies, and trade association digests from ARM or ISCT. Company 10-Ks, investor decks, and hospital reimbursement schedules provide real-world pricing and uptake clues. Paid databases, D&B Hoovers for revenue splits and Dow Jones Factiva for deal flow, supply financial alignment and news velocity. Many additional references underpin each data point, the above list being illustrative rather than exhaustive.

Market-Sizing and Forecasting

A blended top-down build starts with treated patient volumes drawn from registry data, prevalence-to-eligibility filters, and recorded CAR-T, MSC, or iPSC dose releases, which are then multiplied by median therapy price bands. Supplier roll-ups and sampled ASP times dose counts provide a selective bottom-up check that reconciles gaps. Key drivers in the model include clinical trial success ratios, regulatory approval cadence, manufacturing capacity, liters of bioreactor output, reimbursement penetration, and allogeneic share gains. Five-year outlooks employ multivariate regression layered over ARIMA time series to reflect lagged relationships between trial readouts, capacity expansion, and price compression.

Data Validation and Update Cycle

Outputs pass three-stage peer review, variance thresholds trigger re-checks against external indices, and material events such as landmark approvals prompt mid-cycle refreshes. The dashboard is reopened just before publication so clients always receive the latest consensus.

Credibility Anchor: Why Mordor's Cell Therapy Baseline Commands Confidence

Published market estimates often diverge because firms pick different product mixes, price points, and update schedules.

Key gap drivers include some studies that track only stem-cell products or technology inputs; others extrapolate early-stage pipeline counts into revenue too aggressively; many convert currencies once a year, whereas Mordor updates exchange rates quarterly; finally, our annual refresh incorporates every new FDA, EMA, or NMPA approval before rolling forecasts forward.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 17.13 B (2025) | Mordor Intelligence | - |

| USD 5.89 B (2024) | Global Consultancy A | Excludes immune-cell therapies and uses static 2023 ASPs |

| USD 6.04 B (2024) | Trade Journal B | Counts only commercial sales, omits hospital-administered compassionate doses |

The comparison shows that when the same therapy classes, compassionate-use volumes, and current prices are aligned, Mordor's figure emerges as a balanced, transparent baseline that stakeholders can replicate with publicly traceable variables.

Key Questions Answered in the Report

How large is the cell therapy market in 2026?

The cell therapy market size reached USD 6.55 billion in 2026 and is projected to climb to USD 14.56 billion by 2031.

Which type of therapy is growing fastest?

Allogeneic, off-the-shelf therapies are the fastest, advancing at a 17.34% CAGR through 2031 due to lower cost-of-goods and shorter manufacturing lead times.

What region will post the highest growth?

Asia-Pacific is expected to deliver the highest regional CAGR of 17.89% as China, Japan, and South Korea streamline approvals and expand reimbursement.

What is the main cost challenge for autologous CAR-T?

Personalized production averages USD 350,000 per dose and involves high fixed GMP costs, pressuring margins and affordability.

How are manufacturers reducing costs?

AI-optimized closed bioreactors, capacity expansion at CDMOs, and non-viral gene-delivery methods are cutting per-dose costs significantly.

Which application segment is expanding fastest?

Neurological disorders lead with a 17.47% CAGR, fueled by late-stage trials in Parkinson’s disease using iPSC-derived neurons.

Page last updated on: