Pet Probiotics Supplements Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2025) | USD 1.45 Billion |

| Market Size (2031) | USD 2.61 Billion |

| Growth Rate (2026 - 2031) | 11.40% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

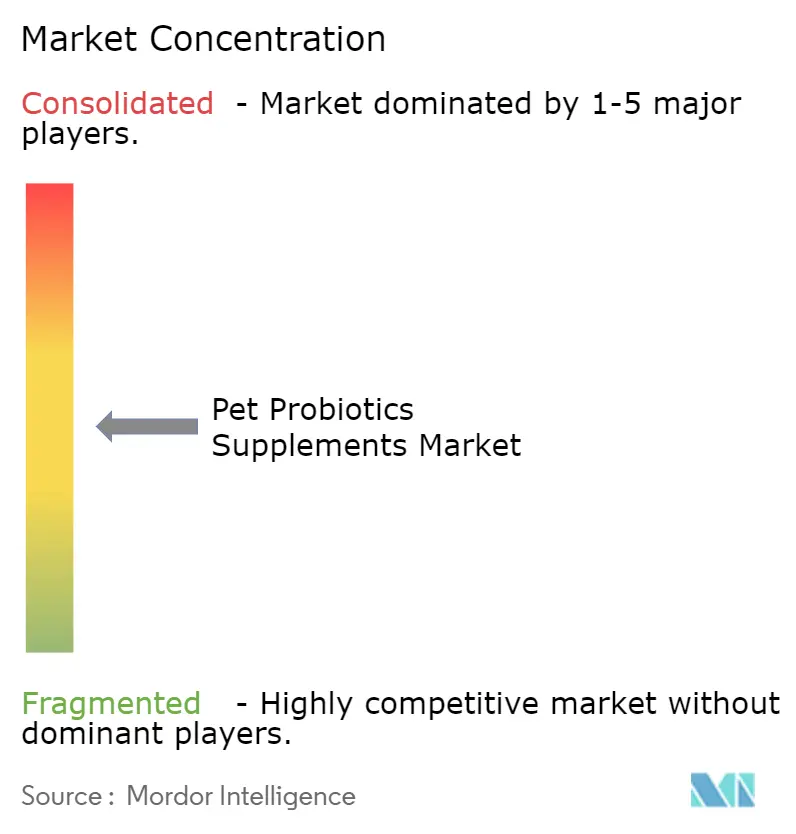

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Pet Probiotics Supplements Market Analysis by Mordor Intelligence

The pet probiotics supplements market was valued at USD 1.32 billion in 2025 and is projected to grow from USD 1.45 billion in 2026 to USD 2.61 billion by 2031, registering a CAGR of 11.4% between 2026 and 2031. Factors driving this growth include increasing disposable income allocated to preventive pet wellness, advancements in microbiome research, and a preference among pet owners for strain-specific, shelf-stable formulations. While dogs account for the majority of purchases, there is growing interest in probiotics for exotic pets, supported by the expansion of antibiotic-free aquaculture. Additionally, digital retail platforms are fostering recurring sales through subscription models that combine probiotics with joint and anxiety supplements. Veterinary endorsements further enhance consumer confidence in the efficacy of these products.

Key Report Takeaways

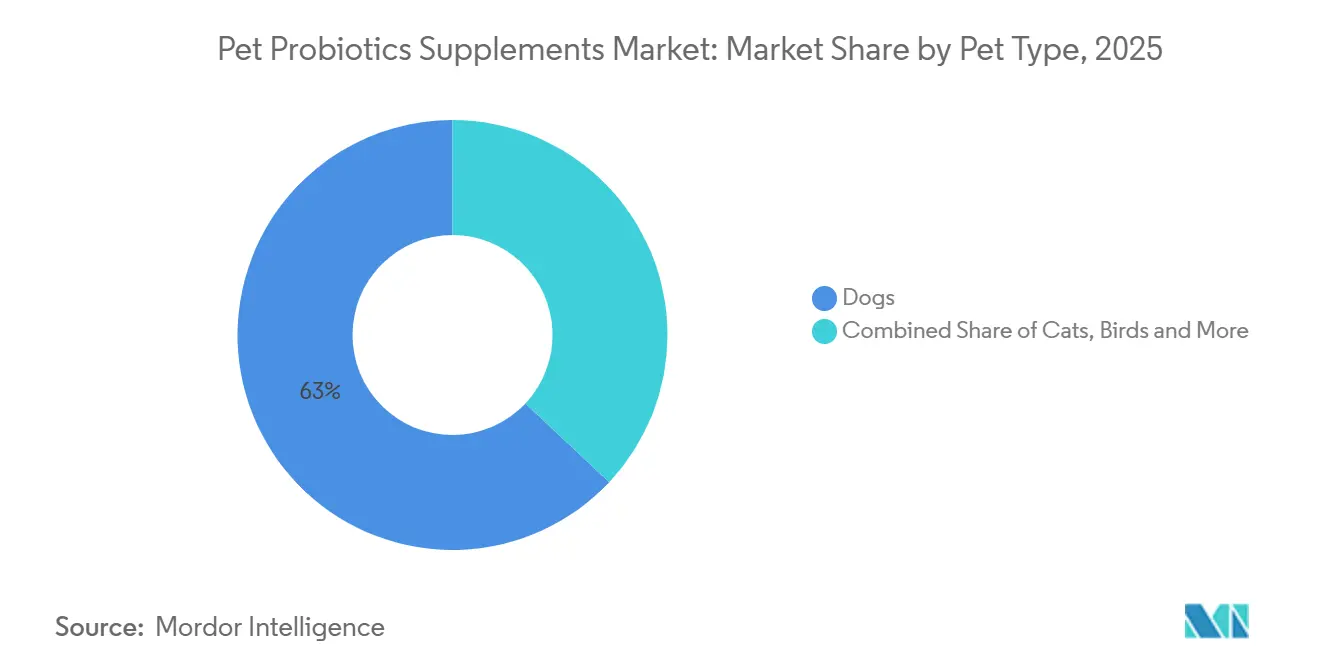

- By pet type, dogs accounted for the largest 63% of the market share in 2025, while the pet probiotics supplements market size for small mammals is projected to grow at the fastest CAGR of 15.4% from 2026 to 2031.

- By form, chewables held the largest 37.4% market share, whereas the market size for liquid pet probiotics supplements is projected to grow at the fastest CAGR of 12.8% from 2026 to 2031.

- By distribution channel, online retail captured the largest 46.2% of the market share in 2025 and is forecast to grow at the fastest CAGR of 14.6% from 2026 to 2031.

- By function, digestive health accounted for the largest 41.8% of the market share, while formulas targeting the anxiety and stress market size are advancing at the fastest CAGR of 13.9% from 2026 to 2031.

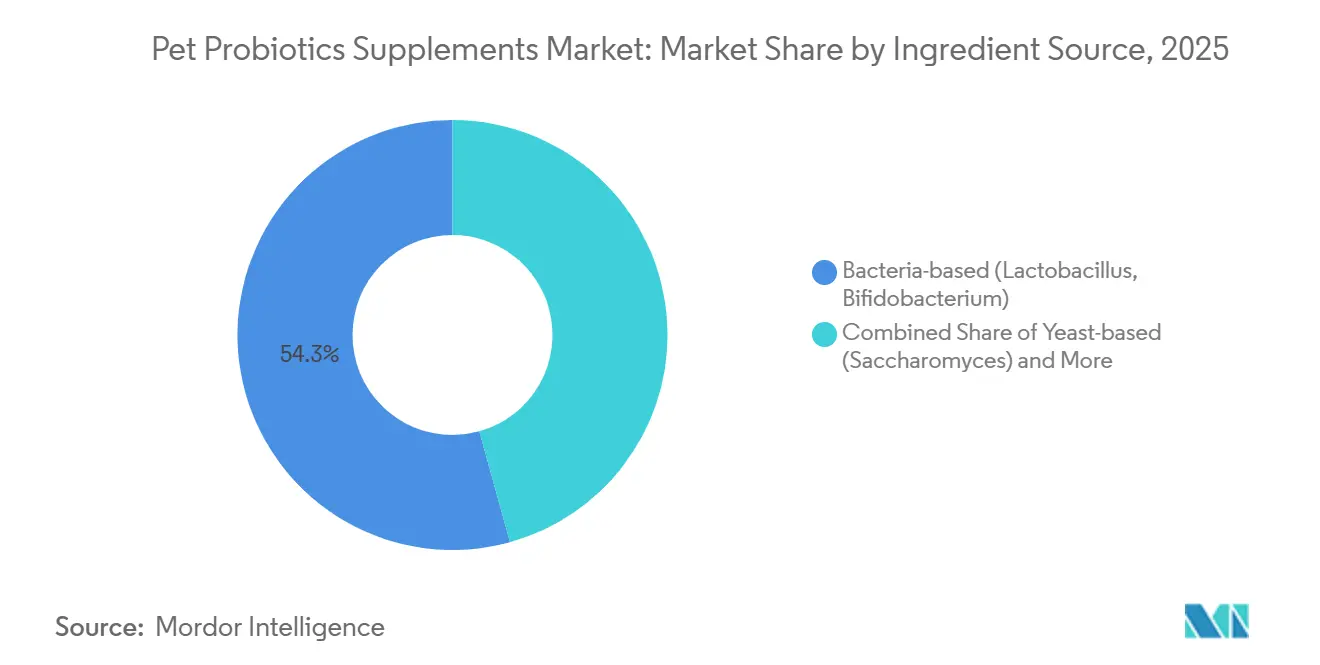

- By ingredient, bacteria-based blends held the largest 54.3% of the market share, whereas the spore-forming strains market size is registering a fastest CAGR of 18.3% from 2026 to 2031.

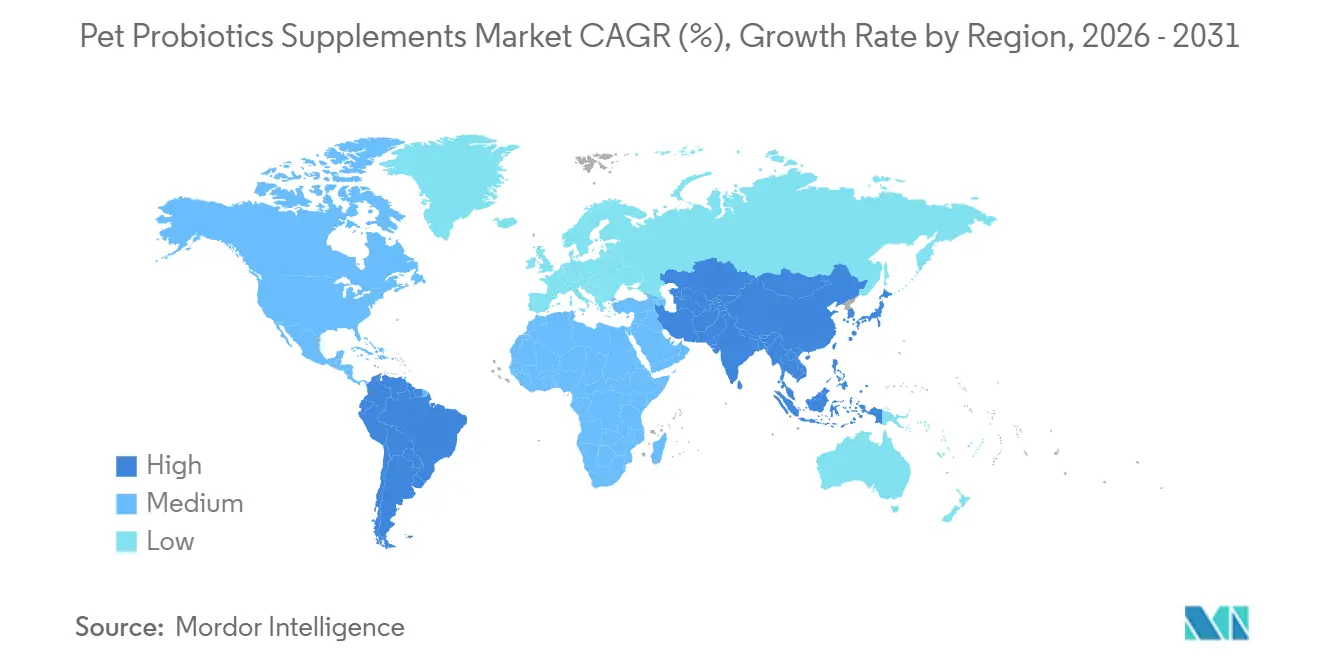

- By geography, North America accounted for the largest 43% of the market share, while the Asia-Pacific market size is poised for the fastest CAGR of 12.1% from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Pet Probiotics Supplements Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising pet humanization and premiumization driving demand | +2.8% | North America, Western Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Increasing veterinary endorsements for gut-health probiotics | +1.9% | North America, Europe, and Australia | Short term (≤ 2 years) |

| Rapid e-commerce penetration widening access to supplements | +2.3% | Global, led by North America and China | Short term (≤ 2 years) |

| DNA-based microbiome testing enabling personalized blends | +1.2% | North America, early adoption in United Kingdom and Australia | Medium term (2-4 years) |

| Aquaculture antibiotic stewardship boosting other pets demand | +0.9% | China, Vietnam, Thailand, Brazil, and Chile | Long term (≥ 4 years) |

| Next-gen postbiotic formulations improving shelf life | +1.5% | Europe and North America research hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Pet Humanization and Premiumization Driving Demand

According to the American Pet Products Association (APPA) 2025, the United States pet industry expenditures reached USD 152 billion in 2024. Additionally, pet owners maintained their spending levels despite economic fluctuations, highlighting the emphasis on advanced pet wellness through specialized distribution channels. Growing awareness of the benefits of probiotics in supporting pet health, including improved digestion, enhanced immunity, and overall well-being. Bundled products that combine probiotics with joint or calming supplements are increasing basket value, offering a more comprehensive approach to pet care.

Increasing Veterinary Endorsements for Gut-Health Probiotics

Veterinary clinical studies indicate that probiotics are effective in managing canine acute diarrhea, demonstrating benefits such as a shorter duration of symptoms and improved gut health outcomes [1]Source: Effect of a Probiotic on Clinical Outcome in Dogs with Acute Diarrhea, Journal of Veterinary Internal Medicine, onlinelibrary.wiley.com . Veterinary clinics now stock probiotic chewables at checkout counters, where point-of-care recommendations have proven effective in driving sales. Partnerships with big-box pharmacies are extending the reach of probiotics beyond traditional veterinary offices. Professional endorsements are also raising documentation standards, compelling brands to publish strain-specific data, which helps distinguish probiotics from general wellness products.

Rapid E-Commerce Penetration Widening Access to Supplements

Online retail platforms provide convenient access to various products, including chewables, liquids, and synbiotic powders designed for digestive health and anxiety relief. Reflecting this digital trend. According to the United States Agriculture Department's Foreign Agricultural Service 2025 Pet Food Market Update, in China a significant 66% increase in sales of prescription-based pet products, such as those for digestive and urinary health, through online channels in 2024. This growth is driven by pet owners prioritizing the convenience of doorstep delivery and subscription-based services. However, the risk of counterfeit products persists, prompting investments in QR-code authentication. Direct-to-consumer websites are reinvesting wholesale margins into social media education, which helps drive repeat purchases.

DNA-Based Microbiome Testing Enabling Personalized Blends

Fecal 16S rRNA testing kits are being used to match dysbiosis profiles with customized Lactobacillus and Bifidobacterium blends, offered through subscription models. Purina’s Petivity platform integrates urinary biomarkers to provide multi-parameter guidance. Quarterly retesting generates recurring revenue as factors like diet, age, and medication alter microbiota composition. While clinical evidence remains largely correlational, it may face increased regulatory scrutiny in the future. Early adopters are willing to pay premium prices when reports demonstrate specific bacterial changes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory ambiguity around strain-specific health claims | -1.2% | Global, strictest in Europe and North America | Medium term (2-4 years) |

| Limited longitudinal clinical evidence affecting confidence | -0.9% | Global, dampens premium adoption | Long term (≥ 4 years) |

| Fermentation-capacity bottlenecks for spore-forming probiotics | -0.6% | Global, highest in Asia-Pacific hubs | Short term (≤ 2 years) |

| Raw-diet movement reducing perceived supplement need | -0.4% | North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Ambiguity Around Strain-Specific Claims

The Food and Drug Administration (FDA) Center for Veterinary Medicine classifies most probiotics as feed ingredients, making pre-market efficacy trials voluntary. Product labels are permitted to claim general benefits such as “supports digestive health,” but they are prohibited from asserting disease treatment, which can lead to confusion among consumers. Currently, some of the probiotic brands display the National Animal Supplement Council (NASC) seal, leaving the majority of products without NASC oversight or auditing. In Europe, the European Pet Food Industry Federation (FEDIAF) requires strain identification but does not mandate outcome data, creating inconsistencies in global regulatory standards.

Limited Longitudinal Clinical Evidence Affecting Confidence

Fewer randomized trials in dogs and cats have tracked outcomes beyond six months, and none have evaluated overall survival rates. Veterinarians trained in evidence-based practices are often hesitant to recommend probiotics due to the lack of long-term data. Conducting multi-year studies to address these gaps can cost higher, which poses significant financial challenges for smaller brands. In the absence of robust, blinded research data, pet owners frequently rely on anecdotal reviews to guide their purchasing decisions. This knowledge gap in the market hinders the adoption of premium probiotic products, particularly among risk-averse consumer demographics who prioritize evidence-based solutions for their pets' health.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Pet Type: Dogs Lead, Small Mammals Surge

Dogs accounted for the largest 63% of the pet probiotics supplements market share in 2025, driven by established veterinary protocols recommending Enterococcus-based blends for managing acute diarrhea and chronic inflammatory enteropathy. Cats trailed behind due to challenges in ensuring daily compliance. However, a 2025 study utilizing Saccharomyces cerevisiae DSM 34246 demonstrated measurable improvements in fecal immunoglobulin A levels, indicating potential strain-specific adoption among cat owners. The pet probiotics supplements market size for small mammals is projected to grow at the fastest CAGR of 15.4% from 2026 to 2031, supported by increased exotic-pet adoption and advancements in research on cecal microbiome modulation.

Birds and fish, categorized under "other pets," are benefiting from antibiotic-free aquaculture mandates, which have highlighted Bacillus subtilis and Lactobacillus plantarum as immune enhancers and water-quality modulators. Ornamental birds, such as parrots and cockatiels, often experience stress-induced enteritis, which has been shown to respond to Lactobacillus reuteri supplementation. This represents a niche that mainstream brands have yet to address fully. This category also encompasses reptiles and amphibians, where probiotic applications are still in the experimental stage. Early trials indicate that Bacillus strains may help address dysbiosis in captive-bred iguanas and tree frogs.

By Form: Chewables Anchor, Liquids Gain Ground

Chewables accounted for the largest 37.4% of the pet probiotics supplements market share in 2025, as chicken-liver and cheese flavor systems effectively mask the bitterness of probiotics, ensuring daily compliance by pet owners, a critical factor for sustained gut colonization. Powders remain a cost-effective option for multi-pet households. However, exposure to humidity can result in clumping and CFU (colony-forming unit) loss, which may reduce repeat-purchase intent. Capsules are commonly used in veterinary channels due to their tamper-evident packaging and clearly labeled CFU counts, although cats and toy breeds often resist pill intake.

The market size for liquid pet probiotic supplements is projected to achieve a fastest 12.8% CAGR from 2026 to 2031, particularly favored for use in birds, fish, and felines, where syringe or dropper dosing minimizes stress. Emerging gels and pastes combine the dosing precision of liquids with the shelf stability of powders, making them suitable for post-surgical applications. Bake-stable spore-forming strains enable soft treats to function as both supplements and snacks, although high oven temperatures still require microencapsulation. Ongoing format innovations ensure that the pet probiotic supplements market remains adaptable to evolving owner preferences for convenience and palatability.

By Distribution Channel: Online Retail Commands Growth

Online retail accounted for the largest 46.2% of the market share in the pet probiotics supplements market in 2025. Market size for this segment is projected to grow at the fastest CAGR of 14.6% from 2026-2031, driven by platforms like Amazon and Chewy together controlling over 80% of e-commerce volume, leveraging subscription models and algorithm-driven cross-sell that traditional brick-and-mortar cannot replicate [2]Source: Pet Specialty Retail Under Pressure." Alvarez and Marsal Consumer Products and Retail Group, 2025, alvarezandmarsal.com. This model also enhances customer lifetime value, even with discounts offered through auto-ship programs. The convenience and personalization offered by online platforms continue to attract consumers, making this channel a key driver of growth in the pet probiotics supplements market.

Brick-and-mortar veterinary clinics report higher conversion rates when clinicians recommend products during checkout. However, clinic footfall decreased, driven by the increasing adoption of telemedicine, which provides greater convenience and accessibility for pet owners. Pet specialty stores are placing greater emphasis on experiential services, such as grooming, to address pricing competition from online retailers. Meanwhile, mass retailers are expanding their private label product lines, which are priced lower than established brands.

By Function: Digestive Core, Anxiety Rising

Digestive formulas held the largest 41.8% of the market share in the pet probiotics supplements market in 2025, supported by data indicating that Enterococcus faecium reduces acute diarrhea episodes in dogs. This segment benefits from growing awareness among pet owners about the importance of gut health in overall well-being. Immune support blends combining probiotics with beta-glucans are gaining interest among senior pet owners, driven by their potential to enhance immunity, although definitive causal evidence remains unestablished. Oral health products utilizing Streptococcus salivarius K12 target plaque and halitosis, addressing common dental issues in pets, but require stronger veterinary endorsements to achieve broader adoption and market penetration.

The anxiety and stress market size is projected to grow at the fastest CAGR of 13.9% from 2026 to 2031, driven by findings that Bifidobacterium longum BL999 modulates cortisol levels in separation-anxious dogs. This growth reflects increasing demand for natural solutions to behavioral issues in pets. Skin and coat formulations leverage the gut-skin axis, with Lactobacillus sakei probio65 reducing atopic dermatitis scores by 38% over eight weeks in 2026 trials [3]Source: Effects of Bacillus subtilis on Growth Performance and Disease Resistance in Aquaculture, MDPI Animals, mdpi.com . Joint-support synbiotics remain speculative but command 20–30% price premiums, reflecting their perceived value. Ongoing diversification ensures the pet probiotics supplements market remains adaptable to shifting wellness trends.

By Ingredient Source: Bacteria Prevail, Spores Disrupt

Bacteria-based blends accounted for the largest 54.3% of the market share in the pet probiotics supplements market in 2025, supported by the long-standing Generally Recognized As Safe (GRAS) designations from the Food and Drug Administration for Lactobacillus and Bifidobacterium strains. These strains are widely recognized for their safety and efficacy in promoting gut health, making them a preferred choice in the pet probiotics market. Yeast-based options, such as Saccharomyces boulardii, are primarily used to address antibiotic-associated diarrhea.

The spore-forming probiotics market size is set to grow at the fastest 18.3% CAGR from 2026 to 2031, driven by their ability to remain stable under ambient storage conditions for over 24 months. Their resilience to gastric acid enhances viable delivery, making them a reliable option for improving gut health in pets. Synbiotic blends, which combine probiotics with prebiotics like inulin or fructooligosaccharides, offer potential benefits, though evidence of their synergistic effects remains mixed. Postbiotics, consisting of heat-killed cells and metabolites, bypass the need for CFU labeling, simplifying compliance with the Association of American Feed Control Officials' regulations.

Geography Analysis

North America is projected to hold the largest market share of 43% in the pet probiotics supplement market in 2025. This dominance is driven by high companion animal ownership, a well-established network of veterinary clinics, and the adoption of data-driven direct-to-consumer platforms such as Purina Petivity and AnimalBiome. These platforms leverage fecal sequencing to provide strain-specific recommendations. The United States leads the region in terms of volume, with online sales accounting for a significant portion of pet supplement spending. Subscription-based purchases represent a growing segment of the market.

The Asia-Pacific market size is projected to grow at the fastest 12.1% CAGR from 2026 to 2031, driven by increased companion animal spending in urban Chinese households. In Japan, regulatory changes now permit health claims for Lactobacillus and Bifidobacterium under its feed-additive framework, enabling the development of functional snacks that bypass drug registration requirements. Australia combines high pet ownership with strong veterinary influence, though its small population limits overall market volume. India and Southeast Asian economies rely heavily on e-commerce due to limited veterinary clinic density.

Europe, the Middle East, Africa, South America, and Russia exhibit fragmented adoption patterns. Germany, France, and the United Kingdom lead under the Federation of European Companion Animal Veterinary Associations guidelines, which mandate strain identification but do not require efficacy proof. This allows for quick product cycles but results in variable clinical backing. In the Middle East, the United Arab Emirates and Saudi Arabia are experiencing growth due to expatriate pet ownership and premium retail expansion, though cultural norms limit penetration into mainstream households. In Africa, South Africa and Egypt remain niche markets as counterfeit risks and affordability challenges deter branded importers.

Competitive Landscape

In 2025, the market is moderately concentrated, with five major companies covering Nestle Purina PetCare Company, Mars, Incorporated, Nutramax Laboratories, Inc., Swedencare AB, and Zesty Paws, LLC. Despite this, opportunities exist for smaller competitors utilizing specialty strains or direct-to-consumer models. In 2026, Mars enhanced its fermentation capabilities at the Birstall research hub to advance the development of pet formulations optimized for palatability. Additionally, Nestle Purina PetCare Company's Petivity smart litter technology facilitates the collection of microbiome and biomarker data to support personalized dosing algorithms and proprietary data insights.

Emerging players are targeting niche segments such as stress management, skin and coat health, and care for exotic species, aiming to address specific and underserved needs within the market. In 2025, Native Microbials partnered with Zesty Paws, LLC to commercialize probiotic strains specifically developed for dogs, derived from healthy canine microbiomes, showcasing a focus on innovative and science-backed solutions. Furthermore, in 2026, Zesty Paws, LLC introduced its Professional line through Epiq Animal Health, achieving higher-margin conversions in veterinary clinics compared to e-commerce platforms.

Intellectual property activity in the pet probiotics market remained robust in 2024, with several new probiotic-related patents filed, and Enterococcus faecium frequently included in commercial formulations. In 2024, BIO-CAT collaborated with Caldic to distribute OptiFeed Bacillus blends, highlighting the growing integration between ingredient suppliers and finished-product manufacturers. In 2023, Lallemand made progress in both probiotic and postbiotic product development by introducing heat-stable Saccharomyces boulardii derivatives, which address formulation stability challenges and remove the need for cold-chain logistics.

Pet Probiotics Supplements Industry Leaders

-

Nestle Purina PetCare Company

-

Mars, Incorporated

-

Nutramax Laboratories, Inc.

-

Swedencare AB

-

Zesty Paws, LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Mars, Incorporated invested approximately £1.2 million (USD 1.5 million) in its Birstall, United Kingdom R and D hub to strengthen its pet care innovation capabilities. This investment aims to enhance research activities, including probiotic development and product testing, to address evolving pet health requirements.

- November 2025: Native Microbials and Zesty Paws, LLC have formed a strategic partnership to develop and commercialize probiotic strains specifically designed for canine health. This collaboration aims to utilize microbiome science to create targeted probiotic formulations for dogs.

- January 2024: Novozymes and Chr. Hansen have merged to form Novonesis Group A/S, a global leader in biosolutions with expertise in microbial and probiotic technologies. This merger enhances R&D, production, and innovation, advancing probiotic solutions for animal health, including pet supplements.

Global Pet Probiotics Supplements Market Report Scope

Pet probiotic supplements are dietary products that contain live microorganisms beneficial for maintaining and restoring the balance of gut microbiota in animals. These supplements support digestive health, strengthen immune function, and enhance overall well-being in pets by improving nutrient absorption and reducing gastrointestinal problems. The pet probiotics supplements market report is segmented by pet type (dogs, cats, birds, fish, and small mammals), by form (chewables, powder, capsules and tablets, liquids, gels and pastes), by distribution channel (online retail, veterinary clinics, pet specialty stores, mass-market retailers, and other distribution channels), by function-health benefit (digestive health, immune support, oral health, skin and coat, joint health, anxiety and stress, and other function), by ingredient source (bacteria-based (lactobacillus, bifidobacterium), yeast-based (saccharomyces), synbiotic blends, and spore-forming probiotics), and by geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The market sizes and forecasts are provided in terms of value (USD).

| Dogs |

| Cats |

| Others Pet Types |

| Chewables |

| Powder |

| Capsules and Tablets |

| Liquids |

| Other Forms |

| Online Retail |

| Veterinary Clinics |

| Pet Specialty Stores |

| Mass-Market Retailers |

| Other Distribution Channels |

| Digestive Health |

| Immune Support |

| Oral Health |

| Skin and Coat |

| Joint Health |

| Anxiety and Stress |

| Other Functions |

| Bacteria-based Probiotics (Lactobacillus, Bifidobacterium) |

| Yeast-based Probiotics (Saccharomyces) |

| Synbiotic Blends |

| Spore-forming Probiotics |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Pet Type | Dogs | |

| Cats | ||

| Others Pet Types | ||

| By Form | Chewables | |

| Powder | ||

| Capsules and Tablets | ||

| Liquids | ||

| Other Forms | ||

| By Distribution Channel | Online Retail | |

| Veterinary Clinics | ||

| Pet Specialty Stores | ||

| Mass-Market Retailers | ||

| Other Distribution Channels | ||

| By Function (Health Benefit) | Digestive Health | |

| Immune Support | ||

| Oral Health | ||

| Skin and Coat | ||

| Joint Health | ||

| Anxiety and Stress | ||

| Other Functions | ||

| By Ingredient Source | Bacteria-based Probiotics (Lactobacillus, Bifidobacterium) | |

| Yeast-based Probiotics (Saccharomyces) | ||

| Synbiotic Blends | ||

| Spore-forming Probiotics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large will global sales of pet probiotics supplements be by 2031?

The market is forecast to reach USD 2.61 billion by 2031, reflecting an 11.4% CAGR from 2026 to 2031.

Which pet type generates the most demand for probiotics?

Dogs dominate with 63% of 2025 revenue owing to strong veterinary protocols and owner familiarity with digestive products.

Which functional claim is expanding fastest?

Anxiety and stress formulations are projected to grow fastest at 13.9% CAGR from 2026-2031 as Bifidobacterium longum BL999 shows cortisol-modulation benefits.

Why are spore-forming strains gaining popularity?

Bacillus subtilis and Bacillus coagulans tolerate heat and gastric acid, enabling 24-month ambient storage and driving an 18.3% CAGR from 2026 to 2031 for spore products.

What channel offers the highest growth opportunity?

Online retail, led by Amazon and Chewy, already controls 46.2% of sales and is projected to rise fastest at 14.6% CAGR from 2026-2031.

Which region will outpace the global average?

Asia-Pacific is set for the fastest 12.1% CAGR, fueled by China's urban pet ownership surge and new Japanese feed-additive regulations.

Page last updated on: