India Feed Probiotics Market Size and Share

Market Overview

| Study Period | 2018 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

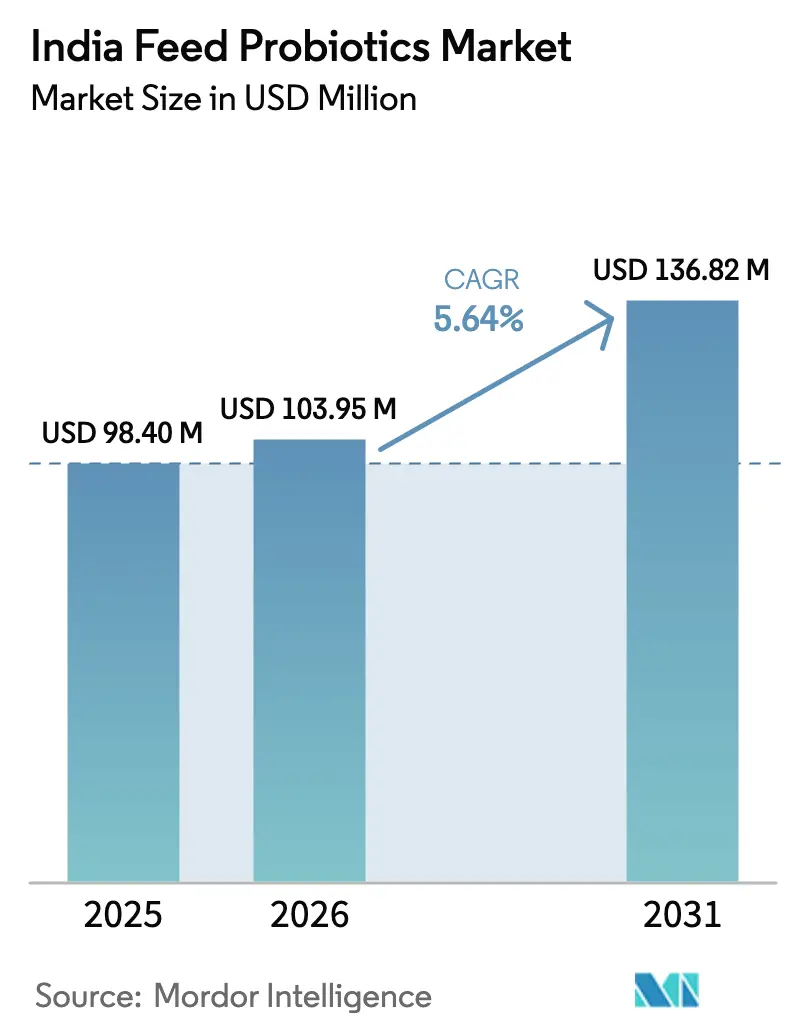

| Base Year Market Size (2025) | USD 98.4 Million |

| Market Size (2026) | USD 103.95 Million |

| Market Size (2031) | USD 136.82 Million |

| Growth Rate (2026 - 2031) | 5.64% CAGR |

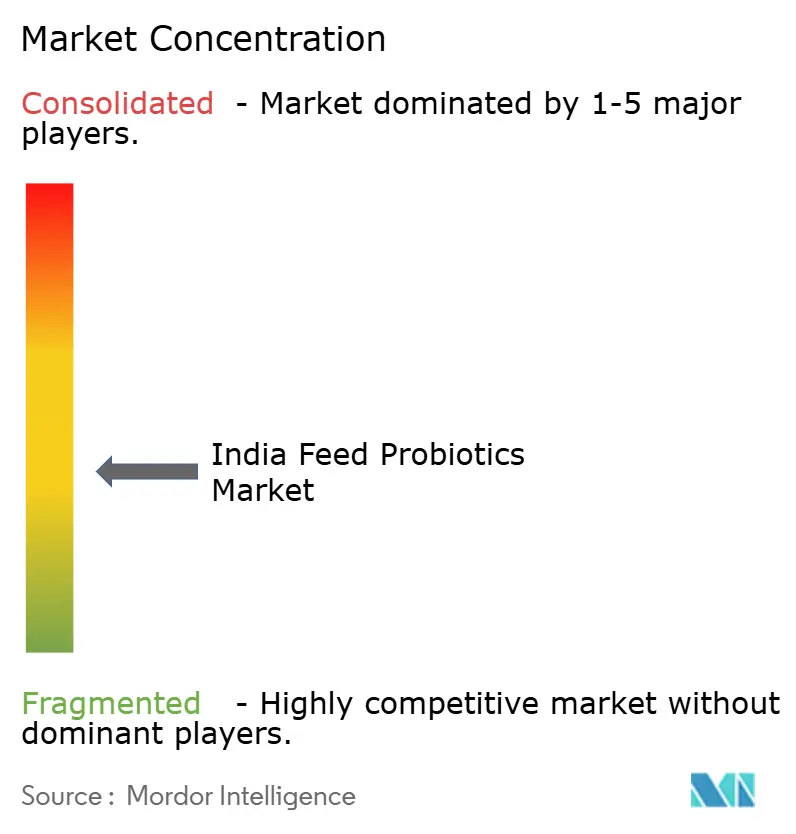

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Feed Probiotics Market Analysis by Mordor Intelligence

The India feed probiotics market size is expected to grow from USD 98.4 million in 2025 to USD 103.95 million in 2026 and is forecast to reach USD 136.82 million by 2031 at 5.64% CAGR over 2026-2031. Expansion follows the nationwide ban on antibiotic growth promoters, the wider adoption in intensive poultry and aquaculture systems, and government incentives that subsidize biological additives for small producers. Demand also aligns with India’s Blue Revolution target of 15 million metric tons of fish by 2030, positioning probiotics as critical for disease management and sustainable intensification.[1]Source: Department of Fisheries, “Blue Revolution: Integrated Development and Management of Fisheries,” dof.gov.in Rapid commercial broiler capacity additions, residue-free export requirements, and research-backed strain innovations further accelerate adoption across organized and semi-organized livestock operations. Still, price sensitivity among smallholders and state-level regulatory variations temper full-scale penetration, directing suppliers toward cost-optimized formulations and extension-led marketing.

Key Report Takeaways

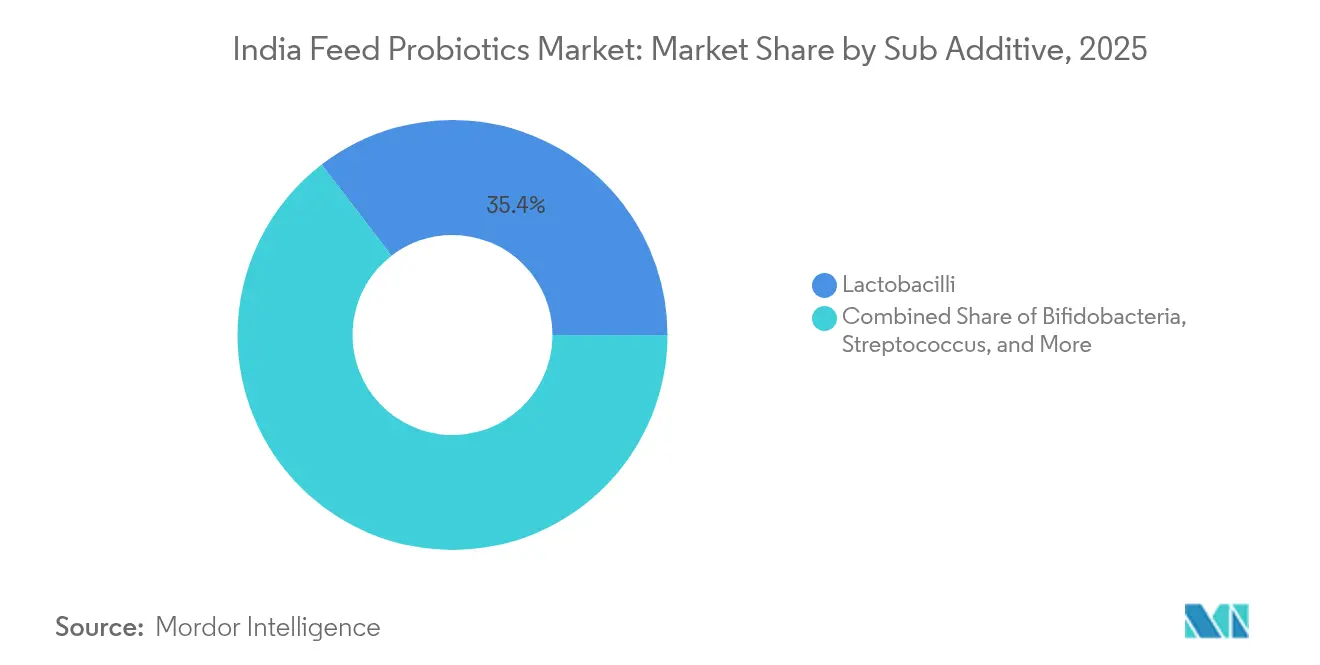

- By sub additive, Lactobacilli captured 35.42% of the India feed probiotics market share in 2025, while Bifidobacteria is forecast to post the fastest 5.77% CAGR through 2031.

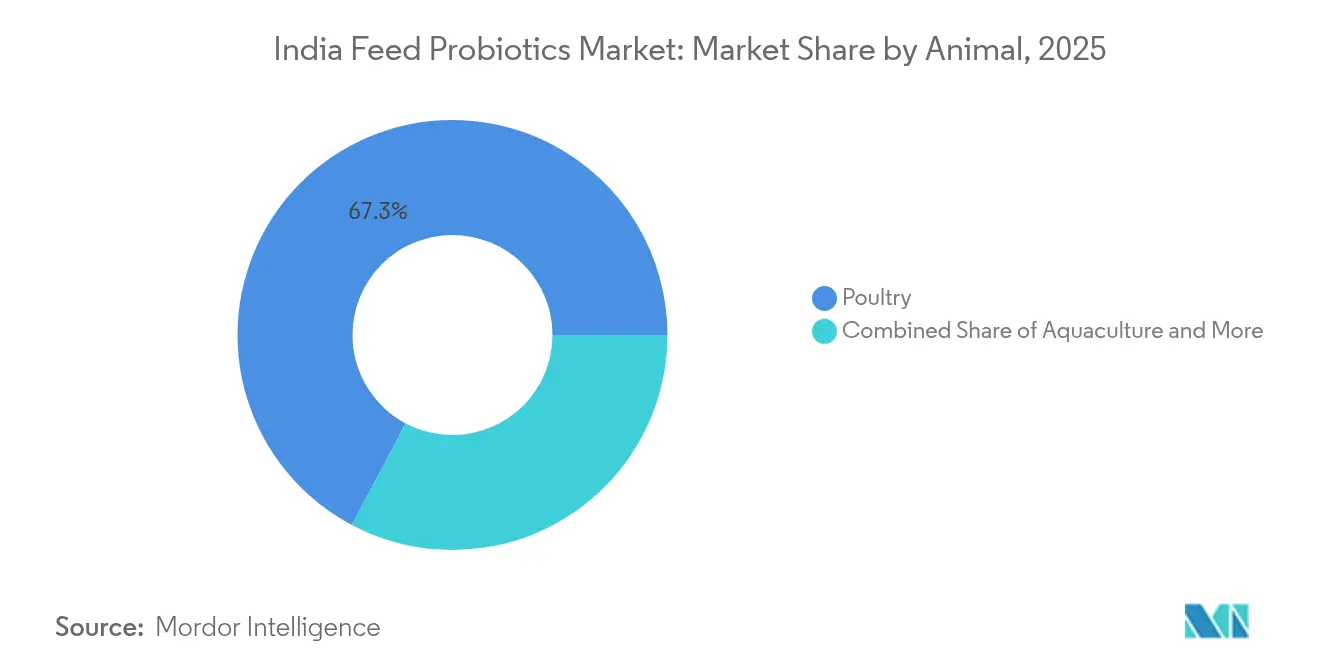

- By animal, poultry commanded 67.25% share of the India feed probiotics market size in 2025 and is advancing at a 5.69% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Feed Probiotics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ban on Antibiotic Growth Promoters | +1.2% | National, with immediate effects in commercial operations | Short term (≤ 2 years) |

| Rapid Commercial Poultry Capacity Expansion | +0.9% | Concentrated in Andhra Pradesh, Tamil Nadu, and Maharashtra | Medium term (2-4 years) |

| Government Aquaculture Programs | +0.8% | Coastal states and with spillover to freshwater regions | Long term (≥ 4 years) |

| Demand for Residue-Free Animal Products | +0.7% | Export-oriented regions and urban consumption centers | Medium term (2-4 years) |

| Chronic Fodder Protein Gap Boosting Feed-Efficiency Additives | +0.6% | Northern plains and drought-prone regions | Long term (≥ 4 years) |

| Blockchain-Enabled Provenance Premiums | +0.3% | Premium market segments and organized retail chains | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Ban on Antibiotic Growth Promoters

The FSSAI amendment, effective April 2025, removed colistin, tylosin, and other antibiotic growth promoters from 78% of commercial feed formulas, compelling an immediate switch to biological alternatives.[2]Source: Food Safety and Standards Authority of India, “Food Safety and Standards (Food Products Standards and Food Additives) Amendment Regulations, 2024,” fssai.gov.in Multi-strain probiotic blends now replicate feed conversion benefits while ensuring residue-free compliance demanded by Middle-East importers. Major premix makers have reformulated flagship lines within six months, and early field trials show broiler weight gains holding steady after substitution. Distributors report that the regulatory deadline compressed adoption cycles, pulling forward orders that otherwise would have been staggered through 2026. The policy signal has also redirected Research and Development budgets toward stability-enhanced spore-forming strains.

Rapid Commercial Poultry Capacity Expansion

Integrated broiler complexes are adding roughly 2.5 million birds monthly, driving feed output and creating a baseline pull for functional additives.[3]Source: Ministry of Agriculture and Farmers Welfare, “Livestock Production Statistics 2025,” agricoop.gov.in New facilities embed probiotics in starter diets from day one, sidestepping the retrofitting hurdles typical of legacy sheds. Rising per-capita chicken consumption from 3.5 kg in 2024 to 4.2 kg in 2025 reinforces volume growth, while zero-antibiotic certification opens premium channels in the Gulf Cooperation Council region. Feed formulators note a 9-12 month payback on probiotic inclusion through improved feed conversion ratios (FCR) and lower mortality, making the case compelling for investors financing greenfield farms.

Government Aquaculture Programs

Phase II of the Blue Revolution earmarks INR 20,050 crore (USD 2.4 billion) in grants and soft loans through 2030 to scale marine and freshwater production. A significant share of the budget subsidizes bio-security inputs, with probiotics receiving cost-sharing of up to 40% for smallholders. Biofloc systems, increasingly favored in inland shrimp clusters, require dense populations of beneficial bacteria to maintain water quality, making probiotics non-negotiable rather than optional. State fisheries departments have begun bulk procurement to reduce unit costs, creating dependable offtake streams for domestic manufacturers. Longer term, aquaculture growth diversifies demand beyond poultry, stabilizing overall sales.

Demand for Residue-Free Animal Products

UAE and Saudi Arabia mandate antibiotic-residue certificates for poultry imports, and Indian exporters receive price premiums of 8-10% for compliant consignments. Domestic urban consumers similarly pay 15-20% more for verified antibiotic-free labels in organized retail. Producers, therefore, position probiotics as a marketing asset that underpins clean-label claims. Retail chains utilize QR-code traceability, and pilots show that provenance verification can lift turnover in metropolitan supermarkets. As the organized retail share in meat sales grows from 8% in 2024 to a projected 15% in 2027, residue-free positioning will mainstream probiotic inclusion.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Inconsistent FSSAI Strain-Specific Approvals | -0.8% | National, affecting all commercial operations | Short term (≤ 2 years) |

| High Price Sensitivity Among Smallholders | -0.6% | Rural areas, traditional farming regions | Medium term (2-4 years) |

| Shrimp Feed Demand Contraction After 2023 Price Slump | -0.4% | Coastal aquaculture regions | Short term (≤ 2 years) |

| Cannibalization by Synbiotics and Post-biotics | -0.3% | Premium market segments, research-intensive applications | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Inconsistent FSSAI Strain-Specific Approvals

FSSAI's strain-specific approval process creates regulatory bottlenecks that delay product launches and increase compliance costs, with registration fees ranging from INR 1,000 to INR 5,000 (USD 12 to USD 60) per strain and processing times varying from 30 to 180 days based on documentation completeness. The regulatory framework requires extensive safety and efficacy data for each probiotic strain, creating barriers for smaller manufacturers who lack resources for comprehensive dossier preparation. This regulatory uncertainty particularly impacts innovative strain development, as companies hesitate to invest in research and development without clear approval pathways, limiting the introduction of next-generation probiotic solutions.

High Price Sensitivity Among Smallholders

India's fragmented livestock sector, dominated by smallholder farmers operating 1-5 animals per household, exhibits extreme price sensitivity that limits probiotic adoption despite demonstrated benefits. Probiotics typically add INR 0.50-1.50 (USD 0.006-0.018) per kg to feed costs, representing a 3-8% increase in total feed expenses that many smallholders cannot absorb given their subsistence-level operations. This cost sensitivity is exacerbated by limited access to credit and the absence of premium pricing for probiotic-enhanced products in local markets, creating a structural barrier to market penetration in rural areas where 86% of livestock operations are located.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sub Additive: Leadership of Lactobacilli with Bifidobacteria Closing the Gap

Lactobacilli retained 35.42% of India feed probiotics market share in 2025 on the back of a long safety record and approvals across poultry, aqua, and ruminant diets. Firms package multi-species Lactobacillus blends in coated granules to survive pelleting temperatures and acidic gut conditions. The India feed probiotics market continues to favor these strains because they align with FSSAI’s established monograph list, simplifying regulatory clearance and distribution. At the same time, the India feed probiotics market is pivoting toward next-gen species as performance trials validate emerging options.

Bifidobacteria are projected to clock a 5.77% CAGR through 2031, reflecting superior pelleting stability and immunomodulatory benefits demonstrated in controlled studies. Suppliers now promote Bifidobacterium-dominant blends for broilers under heat stress and for biofloc shrimp ponds due to their robust performance in high-density environments. Enterococcus and Pediococcus serve niche marine applications where salt tolerance matters, while Streptococcus shows promise in methane-reducing dairy feed concepts. Yeast-based and spore-forming probiotics populate the “other” category and allow longer shelf life, enabling penetration into remote distribution channels.

By Animal: Poultry Supremacy with Aquaculture Upside

Poultry formats generated 67.25% of the India feed probiotics market size in 2025, buoyed by integrated broiler complexes that favor feed-embedded performance enhancers, and are advancing at a 5.69% CAGR through 2031. Standard grower diets using 200 grams of probiotic premix per ton translate into measurable FCR improvements, allowing integrators to recoup additive costs within a single production cycle. Layers also benefit from better shell strength, which reduces breakage during transport to urban centers.

Aquaculture ranks as the second-largest consumer of freshwater, and marine systems adopt probiotics for disease suppression and water quality control, particularly in biofloc tanks. The India feed probiotics market gains additional momentum in ruminants as cooperatives distribute probiotic sachets alongside compound feed to improve microbial protein synthesis in the rumen. Swine and minor species contribute modest volumes, but regional pork demand in the Northeast holds localized growth opportunities.

Geography Analysis

Southern India accounted for a significant share of the India feed probiotics market in 2025, supported by Andhra Pradesh’s twin strengths in shrimp and broiler production, Tamil Nadu’s mixed livestock base, and Karnataka’s scaling dairy clusters. Proximity to ports simplifies the import of carrier materials and export of finished products, giving manufacturers logistics advantages and enabling sharper pricing.

Western and northern states, led by Maharashtra, Punjab, and Haryana, exhibit accelerating uptake driven by commercial dairies and expanding broiler integrations. Better extension networks and cold-chain infrastructure facilitate demonstration programs that communicate FCR gains to farmers. State-run milk federations increasingly co-market probiotics with mineral-vitamin blends, broadening exposure among smallholders.

Eastern and Northeastern regions remain under-penetrated yet promising. Fragmented farm structures and limited technical support slow animal rates, but government fishery clusters in West Bengal and Assam now pilot probiotic-fortified feeds to curb disease outbreaks. As infrastructure invests in cold chain and processing plants, these states are anticipated to contribute an expanding slice of the nationwide volume.

Competitive Landscape

The India feed probiotics industry is moderately fragmented, with the top five companies collectively controlling a significant revenue share of sales. Multinationals leverage proprietary strains and encapsulation technologies, whereas domestic suppliers compete on price and localized technical service. DSM-Firmenich and Cargill operate in-country production units, reducing lead times and foreign-exchange exposure, while Indian firms such as Abode Biotec focus on indigenous strains adapted to local feed matrices.

Product differentiation centers on thermo-tolerant spore formers and multi-strain consortia targeting specific species or production conditions. Intellectual-property filings have risen since 2024 as companies seek patents on formulation processes, encouraged by stronger legal protection for biologics. Marketing strategies increasingly bundle probiotics with enzymes or acidifiers, creating one-bag solutions that simplify dosage for feed mills.

Distribution remains a critical battleground. Large integrators purchase directly, locking in supply contracts that guarantee volume visibility for producers. The more fragmented smallholder segment relies on dealer networks and cooperatives, necessitating tailored pack sizes and aggressive credit terms. Digital platforms that provide traceability and performance benchmarking emerge as value-added service differentiators.

India Feed Probiotics Industry Leaders

DSM-Firmenich

Adisseo (Bluestar)

Novonesis

Evonik Industries AG

Kerry Group plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Phileo by Lesaffre formed a partnership with CanBiocin, a Canadian biotechnology company that develops species-specific probiotics for pets. The partnership aims to increase the availability of probiotic solutions for dogs, cats, and other companion animals in global markets, including the Asia-Pacific regions such as India.

- October 2023: ADM expanded its international distribution partnership with Nutramax Laboratories. This expansion provides wider access to Nutramax's companion animal health products across the Asia-Pacific region, including India. The product range includes probiotic supplements such as Proviable, Cosequin, and Denamarin.

India Feed Probiotics Market Report Scope

Bifidobacteria, Enterococcus, Lactobacilli, Pediococcus, Streptococcus are covered as segments by Sub Additive. Aquaculture, Poultry, Ruminants, Swine are covered as segments by Animal.| Bifidobacteria |

| Enterococcus |

| Lactobacilli |

| Pediococcus |

| Streptococcus |

| Other Probiotics |

| Aquaculture | By Sub Animal | Fish |

| Shrimp | ||

| Other Aquaculture Species | ||

| Poultry | By Sub Animal | Broiler |

| Layer | ||

| Other Poultry Birds | ||

| Ruminants | By Sub Animal | Beef Cattle |

| Dairy Cattle | ||

| Other Ruminants | ||

| Swine | ||

| Other Animals |

| Sub Additive | Bifidobacteria | ||

| Enterococcus | |||

| Lactobacilli | |||

| Pediococcus | |||

| Streptococcus | |||

| Other Probiotics | |||

| Animal | Aquaculture | By Sub Animal | Fish |

| Shrimp | |||

| Other Aquaculture Species | |||

| Poultry | By Sub Animal | Broiler | |

| Layer | |||

| Other Poultry Birds | |||

| Ruminants | By Sub Animal | Beef Cattle | |

| Dairy Cattle | |||

| Other Ruminants | |||

| Swine | |||

| Other Animals | |||

Market Definition

- FUNCTIONS - For the study, feed additives are considered to be commercially manufactured products that are used to enhance characteristics such as weight gain, feed conversion ratio, and feed intake when fed in appropriate proportions.

- RESELLERS - Companies engaged in reselling feed additives without value addition have been excluded from the market scope, to avoid double counting.

- END CONSUMERS - Compound feed manufacturers are considered to be end-consumers in the market studied. The scope excludes farmers buying feed additives to be used directly as supplements or premixes.

- INTERNAL COMPANY CONSUMPTION - Companies engaged in the production of compound feed as well as the manufacturing of feed additives are part of the study. However, while estimating the market sizes, the internal consumption of feed additives by such companies has been excluded.

| Keyword | Definition |

|---|---|

| Feed additives | Feed additives are products used in animal nutrition for purposes of improving the quality of feed and the quality of food from animal origin, or to improve the animals’ performance and health. |

| Probiotics | Probiotics are microorganisms introduced into the body for their beneficial qualities. (It maintains or restores beneficial bacteria to the gut). |

| Antibiotics | Antibiotic is a drug that is specifically used to inhibit the growth of bacteria. |

| Prebiotics | A non-digestible food ingredient that promotes the growth of beneficial microorganisms in the intestines. |

| Antioxidants | Antioxidants are compounds that inhibit oxidation, a chemical reaction that produces free radicals. |

| Phytogenics | Phytogenics are a group of natural and non-antibiotic growth promoters derived from herbs, spices, essential oils, and oleoresins. |

| Vitamins | Vitamins are organic compounds, which are required for normal growth and maintenance of the body. |

| Metabolism | A chemical process that occurs within a living organism in order to maintain life. |

| Amino acids | Amino acids are the building blocks of proteins and play an important role in metabolic pathways. |

| Enzymes | Enzyme is a substance that acts as a catalyst to bring about a specific biochemical reaction. |

| Anti-microbial resistance | The ability of a microorganism to resist the effects of an antimicrobial agent. |

| Anti-microbial | Destroying or inhibiting the growth of microorganisms. |

| Osmotic balance | It is a process of maintaining salt and water balance across membranes within the body's fluids. |

| Bacteriocin | Bacteriocins are the toxins produced by bacteria to inhibit the growth of similar or closely related bacterial strains. |

| Biohydrogenation | It is a process that occurs in the rumen of an animal in which bacteria convert unsaturated fatty acids (USFA) to saturated fatty acids (SFA). |

| Oxidative rancidity | It is a reaction of fatty acids with oxygen, which generally causes unpleasant odors in animals. To prevent these, antioxidants were added. |

| Mycotoxicosis | Any condition or disease caused by fungal toxins, mainly due to contamination of animal feed with mycotoxins. |

| Mycotoxins | Mycotoxins are toxin compounds that are naturally produced by certain types of molds (fungi). |

| Feed Probiotics | Microbial feed supplements positively affect gastrointestinal microbial balance. |

| Probiotic yeast | Feed yeast (single-cell fungi) and other fungi used as probiotics. |

| Feed enzymes | They are used to supplement digestive enzymes in an animal’s stomach to break down food. Enzymes also ensure that meat and egg production is improved. |

| Mycotoxin detoxifiers | They are used to prevent fungal growth and to stop any harmful mold from being absorbed in the gut and blood. |

| Feed antibiotics | They are used both for the prevention and treatment of diseases but also for rapid growth and development. |

| Feed antioxidants | They are used to protect the deterioration of other feed nutrients in the feed such as fats, vitamins, pigments, and flavoring agents, thus providing nutrient security to the animals. |

| Feed phytogenics | Phytogenics are natural substances, added to livestock feed to promote growth, aid in digestion, and act as anti-microbial agents. |

| Feed vitamins | They are used to maintain the normal physiological function and normal growth and development of animals. |

| Feed flavors and sweetners | These flavors and sweeteners help to mask tastes and odors during changes in additives or medications and make them ideal for animal diets undergoing transition. |

| Feed acidifiers | Animal feed acidifiers are organic acids incorporated into the feed for nutritional or preservative purposes. Acidifiers enhance congestion and microbiological balance in the alimentary and digestive tracts of livestock. |

| Feed minerals | Feed minerals play an important role in the regular dietary requirements of animal feed. |

| Feed binders | Feed binders are the binding agents used in the manufacture of safe animal feed products. It enhances the taste of food and prolongs the storage period of the feed. |

| Key Terms | Abbreviation |

| LSDV | Lumpy Skin Disease Virus |

| ASF | African Swine Fever |

| GPA | Growth Promoter Antibiotics |

| NSP | Non-Starch Polysaccharides |

| PUFA | Polyunsaturated Fatty Acid |

| Afs | Aflatoxins |

| AGP | Antibiotic Growth Promoters |

| FAO | The Food And Agriculture Organization of the United Nations |

| USDA | The United States Department of Agriculture |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms