Veterinary Molecular Diagnostics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

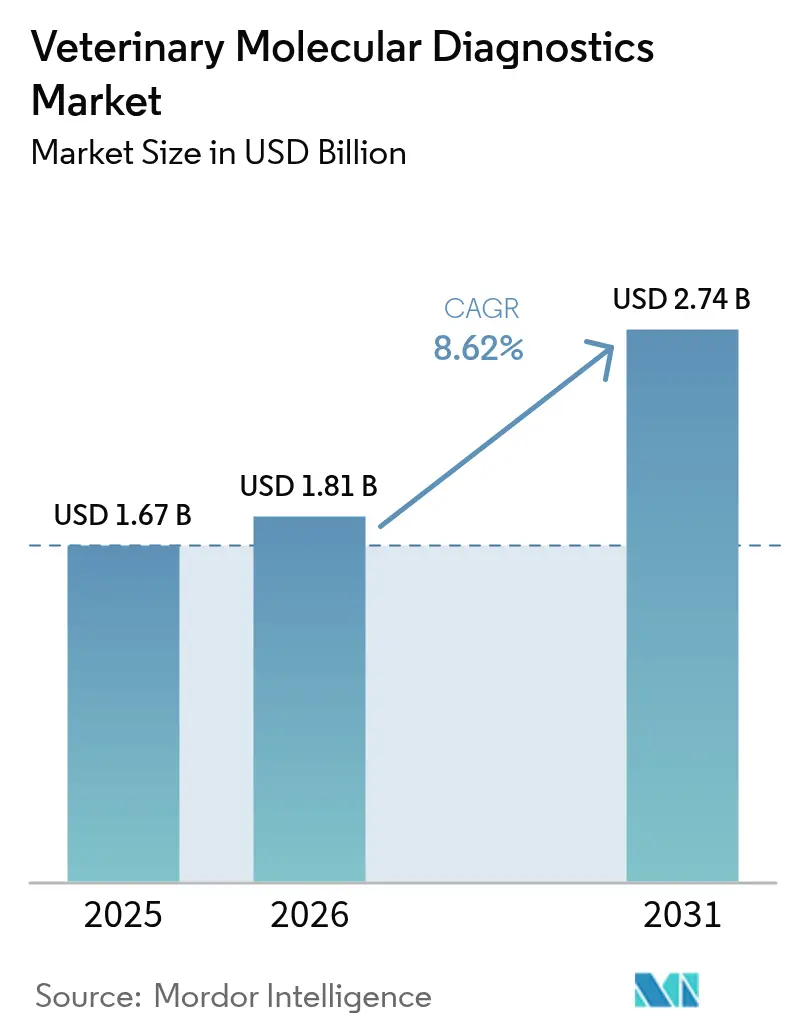

| Market Size (2026) | USD 1.81 Billion |

| Market Size (2031) | USD 2.74 Billion |

| Growth Rate (2026 - 2031) | 8.62% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Veterinary Molecular Diagnostics Market Analysis by Mordor Intelligence

The veterinary molecular diagnostics market size is expected to grow from USD 1.67 billion in 2025 to USD 1.81 billion in 2026 and is forecast to reach USD 2.74 billion by 2031 at 8.62% CAGR over 2026-2031. Adoption accelerates as veterinarians confront larger and more frequent outbreaks of high‐consequence diseases, embrace precision medicine, and integrate artificial-intelligence tools into daily workflows. Portable nanopore sequencing, syndromic multiplex panels, and cloud-based analytics are shifting testing from reference laboratories toward point-of-care settings, widening access while shortening turnaround times. North American leadership continues, yet Asia Pacific records the fastest growth as companion-animal ownership and intensive livestock production expand. Competitive rivalry centers on technology breadth rather than price, with leading firms bundling instruments, consumables, software, and data services to lock in customers and capture recurring revenue.

Key Report Takeaways

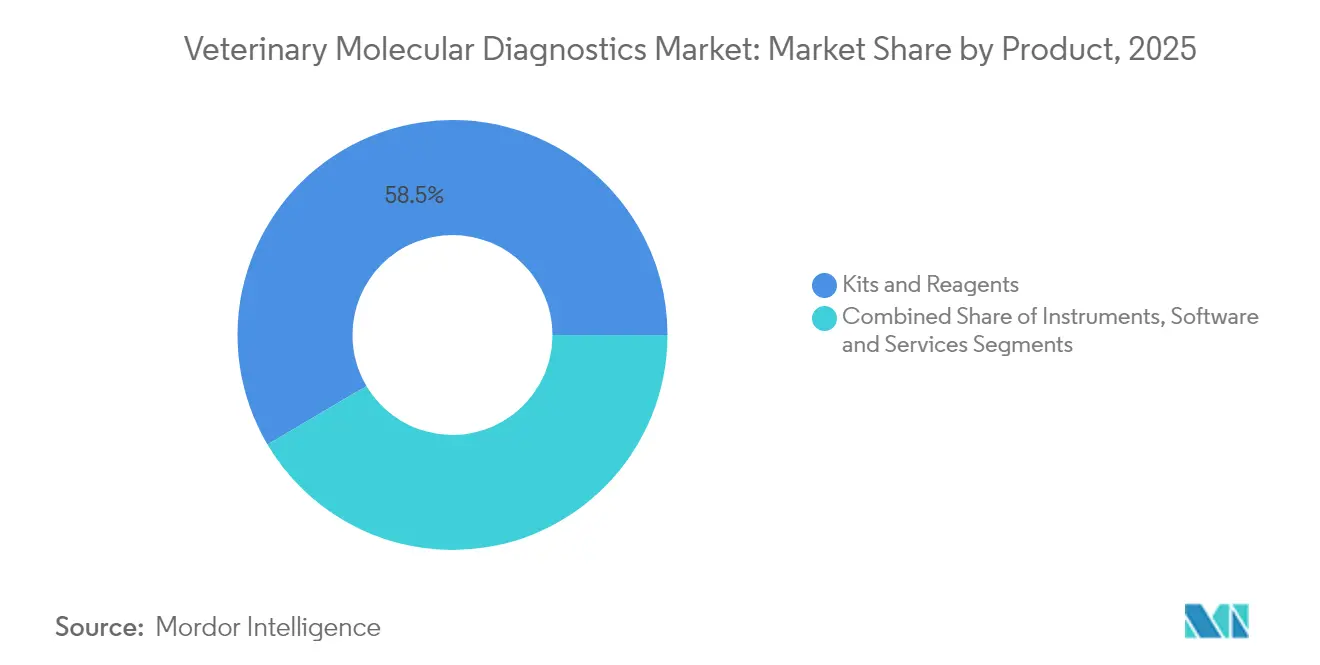

- By product type, kits and reagents held 58.50% of the veterinary molecular diagnostics market share in 2025, while software and services are set to grow at an 11.7% CAGR through 2031.

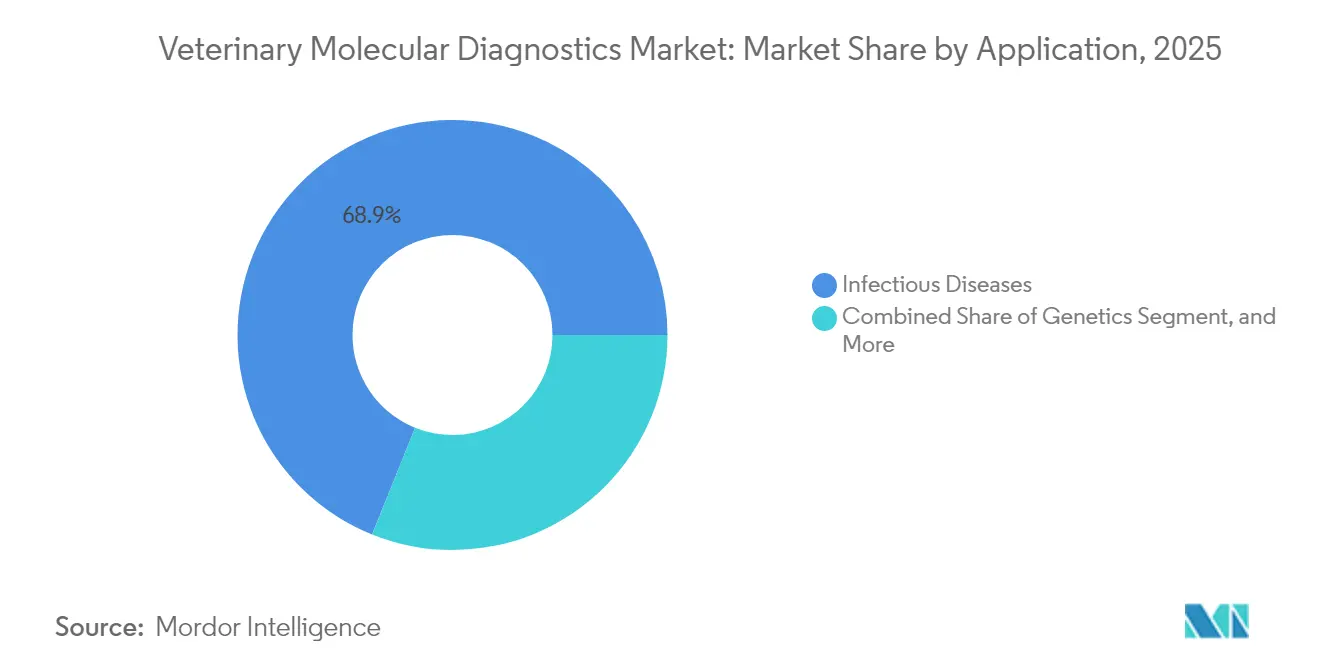

- By application, infectious disease testing accounted for 68.90% of the veterinary molecular diagnostics market size in 2025; genetics is expected to record a 10.24% CAGR to 2031.

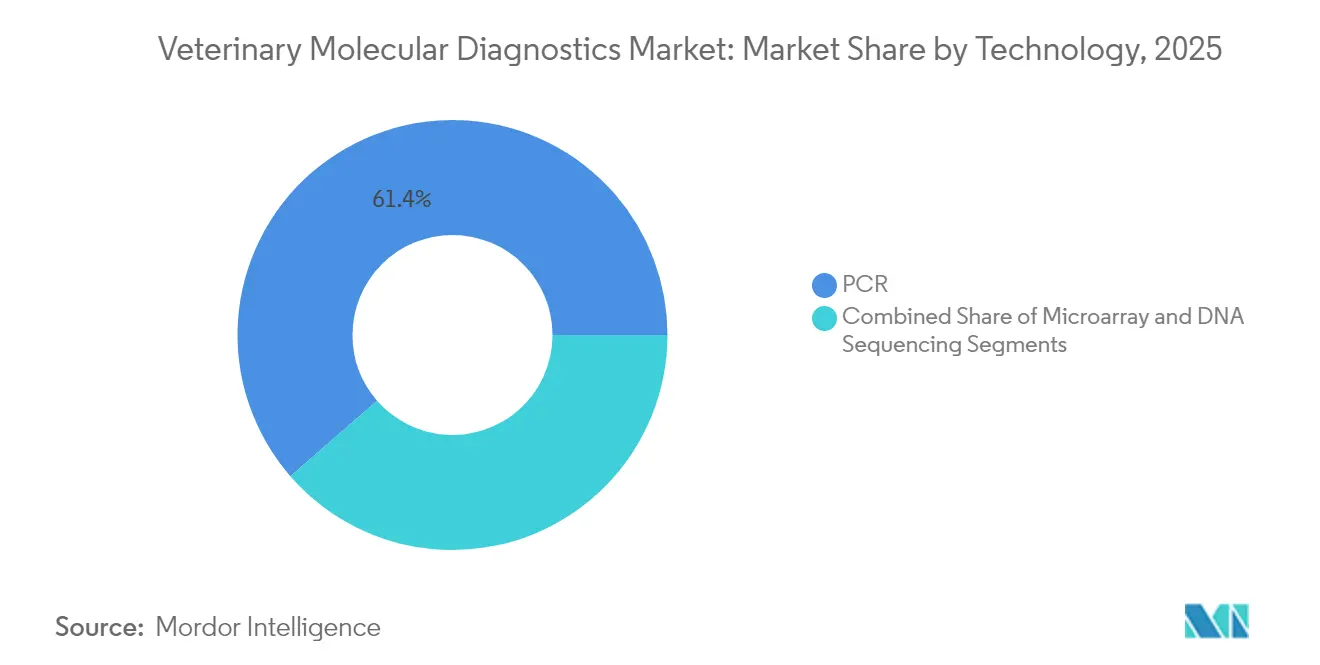

- By technology, PCR maintained 61.40% revenue share in 2025; DNA sequencing is projected to expand at a 13.6% CAGR over the same period.

- By animal type, companion animals dominated with a 64.45% 2025 revenue share, whereas livestock testing for poultry and cattle is forecast to grow the quickest at 11.12% CAGR over the same period.

- By end user, reference laboratories led the market with a 67.40% share in 2025; clinics are adopting point-of-care systems at the fastest pace, at 12.16% CAGR over the same period.

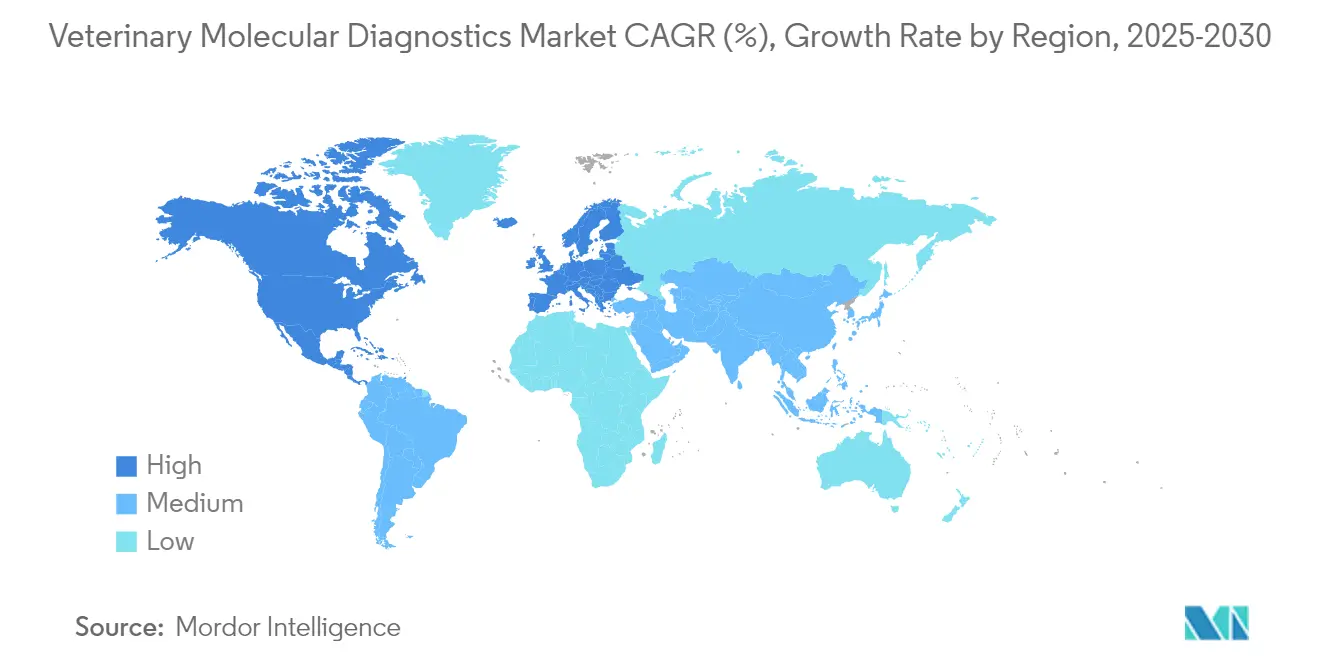

- By geography, North America captured 41.20% of the veterinary molecular diagnostics market share in 2025; Asia Pacific is projected to post an 10.96% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Veterinary Molecular Diagnostics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise in prevalence of animal infectious diseases | +2.10% | Global; acute in North America and Europe | Short term (≤ 2 years) |

| Growing demand for animal-derived proteins | +1.80% | Asia Pacific core; spill-over to MEA and South America | Medium term (2-4 years) |

| Increasing companion-animal ownership & spend | +1.60% | North America and EU; expanding to Asia Pacific cities | Medium term (2-4 years) |

| Adoption of syndromic multiplex panels | +1.40% | North America and Europe, early Asia Pacific uptake | Short term (≤ 2 years) |

| One-Health AMR surveillance funding surge | +1.20% | Global; concentrated in developed markets | Long term (≥ 4 years) |

| Portable nanopore sequencing enters field use | +0.60% | Global; early roll-out in resource-limited settings | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rise in Prevalence of Animal Infectious Diseases

High-pathogenicity avian influenza H5N1 infected U.S. dairy cattle in 2024, pushing laboratories such as the University of Minnesota to process more than 115,000 samples by May 2025. Such surges spur demand for high-throughput PCR platforms that deliver hundreds of results per day and drive adoption of whole-genome sequencing to track viral evolution. Confirmed human H5N1 cases linked to cattle reinforce the One-Health imperative, making molecular diagnostics essential infrastructure for joint animal–human outbreak response. Investments in sequencing capacity therefore shift the veterinary molecular diagnostics market toward integrated, rapid and scalable solutions.

Growing Demand for Animal-Derived Proteins

Rising meat and dairy consumption in Asia Pacific is pushing producers to intensify biosecurity and select disease-resistant genetics. Livestock operators now deploy high-resolution melting assays to distinguish pathogen strains and apply genetic markers for superior feed conversion, cutting antibiotic usage while protecting welfare. This production-oriented testing sustains long-term sales of multiplex platforms capable of combining pathogen detection with genetic profiling inside a single workflow.

Increasing Companion-Animal Ownership & Spend

Eighty percent of pet owners in the United States visit a veterinarian within six months, and willingness to pay for advanced diagnostics is rising. Liquid biopsies, hereditary disease panels, and AI-enabled interpretation tools such as Mars Petcare’s chronic-kidney-disease predictor broaden routine wellness portfolios. Portable analyzers delivering laboratory-quality PCR results during a single clinic visit enhance customer satisfaction and push the veterinary molecular diagnostics market deeper into first-opinion settings.

Adoption of Syndromic Multiplex Panels

Clinical signs often originate from multiple pathogens, making single-plex tests inefficient. Platforms like QIAGEN’s QIAstat-Dx detect up to 12 genomic targets and report within 30 minutes, while including resistance markers that guide antibiotic stewardship. Alveo Technologies’ poultry avian influenza cartridge reaches 99% specificity and uploads results in real time, showing how modular microfluidics reshape biosecurity programs.

One-Health AMR Surveillance Funding Surge

WHO’s antimicrobial-resistance research agenda highlights rapid point-of-care tests as a top priority. The European Union cut antimicrobial use in food animals by 28.3% from 2018-2022, creating a regulatory pull for fast resistance-gene assays. bioMérieux devotes 75% of R&D to AMR solutions, underscoring the commercial importance of integrated panels that detect pathogens and resistance determinants in a single run.

Portable Nanopore Sequencing Enters Field Use

Oxford Nanopore’s MinION delivers real-time genomic reads in barns and remote clinics, enabling on-site avian-influenza surveillance without costly sample transport. Direct RNA sequencing and ultra-long reads let veterinarians characterize complex viral genomes and monitor mutations immediately, widening access in developing regions with minimal laboratory infrastructure.

Restraints Impact Table*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of skilled veterinary molecular diagnosticians | -1.80% | Global; acute shortages in rural and developing areas | Medium term (2-4 years) |

| High cost of instruments & consumables | -1.40% | Developing markets and small practices worldwide | Short term (≤ 2 years) |

| Limited multi-species assay validation standards | -0.90% | Global; regulatory complexity highest in emerging markets | Long term (≥ 4 years) |

| Sample-logistics hurdles in decentralised networks | -0.60% | Rural areas and developing regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Lack of Skilled Veterinary Molecular Diagnosticians

Vacancy rates for laboratory technologists have reached 35%-40% in human health, with parallel gaps in veterinary practice. Rural veterinarians must often double as lab technicians, yet most veterinary curricula provide limited molecular-biology training. Staffing shortages slow installation of advanced platforms and limit the veterinary molecular diagnostics market in smaller clinics.

High Cost of Instruments & Consumables

Comprehensive PCR or sequencing systems frequently exceed USD 100,000, while per-test consumable costs run 3-5 times higher than conventional assays. Financial pressure is acute for stand-alone practices and rural clinics, causing a two-tier market where sophisticated testing concentrates in corporate chains and reference laboratories.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Kits Drive Revenue, Software Accelerates Growth

Kits and reagents produced 58.50% of 2025 revenues, anchoring a recurring business model that stabilizes cash flow for suppliers. Software and services, however, are expanding at an 11.7% CAGR as cloud analytics, AI interpretive modules, and subscription data portals become integral to laboratory operations. Leading vendors bundle consumables, instruments, and analytics, reinforcing switching barriers. The veterinary molecular diagnostics market size attributable to consumables is forecast to remain dominant through 2031, yet software will command increasing strategic importance for differentiation. Instrument margins tighten as miniaturization and open-platform designs lower entry barriers, illustrated by portable nanopore sequencers costing a fraction of legacy bench-top systems. As a result, manufacturers pivot toward integrated ecosystems that pair hardware with digital interpretation and lifetime kit revenue.

By Application: Infectious Diseases Dominate, Genetics Gains Momentum

Infectious disease surveillance generated 68.90% of 2025 sales and remains the core of the veterinary molecular diagnostics market as laboratories manage avian influenza, African swine fever, and canine parvovirus. Syndromic panels shorten differential diagnosis and reduce empirical antibiotic use. Genetics applications, advancing at a 10.24% CAGR, reflect pet owners’ desire for hereditary screening and breeders’ focus on genomic selection. Liquid biopsies for oncology further widen clinical adoption. The veterinary molecular diagnostics market size for genetics is projected to accelerate as sequencing costs fall, enabling routine screening for both disease predisposition and performance traits.

By Technology: PCR Leads, DNA Sequencing Shows Promise

PCR held 61.40% revenue share in 2025 due to robustness, speed, and cost-effectiveness. Innovations such as rapid-cycle chemistry permit sub-hour turnaround, bringing PCR into in-clinic use. DNA sequencing, projected to grow 13.6% annually, extends beyond confirmatory testing into frontline diagnostics, especially as nanopore formats make field deployment practical. The convergence of PCR amplification with on-chip sequencing workflows blurs traditional boundaries and could reshape the veterinary molecular diagnostics market by delivering both qualitative and quantitative insights in one platform.

By Animal Type: Companion Animals Drive Innovation

Companion animals dominated with a 64.45% 2025 revenue share, whereas livestock testing for poultry and cattle is forecast to grow the quickest at 11.12% CAGR over the same period. Companion animals generate the largest spending as owners seek human-level care, including AI-guided interpretation of molecular results. Predictive analytics for chronic kidney disease and oncology screening expand the service mix at veterinary hospitals. Livestock testing grows strongly in poultry and dairy cattle, where proactive surveillance underpins productivity and food safety. Precision selection based on molecular markers reduces antibiotic inputs and aligns with One-Health goals, reinforcing the veterinary molecular diagnostics industry’s relevance to public health.

By End User: Reference Labs Lead, Clinics Embrace Point-of-Care

Reference laboratories led the market with a 67.40% share in 2025; clinics are adopting point-of-care systems at the fastest pace, at 12.16% CAGR over the same period. Reference laboratories dominate high-complexity testing through economies of scale, supporting next-generation sequencing and bespoke pathogen panels. Yet, clinics are the fastest-growing users as cartridge-based PCR systems and portable sequencers deliver definitive results during appointments. This decentralisation increases testing volumes and feeds cloud databases that power AI benchmarking, deepening customer reliance on integrated vendor ecosystems.

Geography Analysis

North America captured 41.20% revenue in 2025, underpinned by extensive veterinary infrastructure, generous pet-care spending, and USDA funding of USD 64.429 million for animal-health diagnostics in 2025. Federal fast-track pathways for new assays accelerate innovation, though rural skills shortages remain a bottleneck.

Europe maintains a substantial share thanks to strict antimicrobial stewardship rules. Regulation (EU) 2019/6 modernizes veterinary medicinal oversight and boosts demand for rapid resistance testing. Between 2018 and 2022, the region cut antimicrobial use in food animals by 28.3%, prompting farms to adopt molecular surveillance as a compliance tool.

Asia Pacific is the fastest-growing territory at an 10.96% CAGR. Middle-class pet ownership, mega-dairy expansion, and supportive policies such as the ASEAN Medical Device Directive spur uptake. Latin America and the Middle East & Africa record steady adoption, although currency volatility and limited laboratory networks temper growth. Portable diagnostic kits tailored for diverse species and climates show promise for accelerating penetration in these regions.

Regulatory Landscape

Regulation in veterinary molecular diagnostics remains fragmented by jurisdiction, and official disease-control programs often determine the practical pathway for assay use. In the United States, USDA APHIS oversight is central for assays used in official testing, including expectations for licensed diagnostic test kits and APHIS-approved laboratories operating under prescribed methods and proficiency practices (with requirements referenced through APHIS guidance and 9 CFR provisions for approved testing). This structure supports standardized surveillance workflows for high-consequence diseases and tends to steer procurement toward validated, program-aligned PCR and sequencing solutions.

Across Europe, veterinary IVDs do not fall under the same harmonized device legislation used for human IVDs (Regulation (EU) 2017/746 is human-focused), so manufacturer compliance requirements remain more country-specific. Standardization efforts are advancing through formal standards: CEN published EN 18000-1:2026 and EN 18000-2:2026, which set requirements around application files and batch-to-batch quality controls for animal-health IVD reagents. In Australia, NATA made its Animal Health ISO/IEC 17025 appendix effective in February 2026, reinforcing laboratory controls such as physical separation of pre- and post-amplification areas for nucleic-acid testing, and raising quality-system expectations for accredited veterinary molecular laboratories.

Value Chain Analysis

The value chain runs from upstream suppliers of enzymes, primers/probes, plastics, and microfluidic components through assay design and validation, kit manufacturing, instrument production, and distribution to reference laboratories, veterinary hospitals and clinics, and on-farm users. A defining characteristic is dependence on specialized consumables and imported reagents in many regions, which increases exposure to lead times and single-source risk for critical inputs such as polymerases and fluorescent chemistries. Validation, quality control, and documentation are tightly coupled to downstream adoption because reference labs and official testing programs require standardized performance, pushing suppliers to provide complete workflows (sample prep, reagents, controls, software) rather than standalone components.

Downstream, sample logistics and workflow support are pivotal. Reference labs capture high-complexity volumes, while field-deployable isothermal PCR and portable sequencing expand access where transport and infrastructure constraints disrupt sample integrity and instrument uptime. Distribution partnerships increasingly bridge technology developers and animal-health channels, illustrated by Enalees announcing a strategic distribution agreement with Unisensor in March 2026 to broaden reach of its Rhéa rapid isothermal PCR tests across European and North American livestock markets. Regulatory and oversight touchpoints also shape the chain, including USDA APHIS laboratory approval requirements and the clarified USDA-FDA oversight framework for animal biologicals, which influence how companies structure labeling, validation packages, and go-to-market routes for diagnostics used in surveillance and control programs.

Competitive Landscape

The veterinary molecular diagnostics market exhibits moderate concentration. IDEXX Laboratories, Zoetis, and Thermo Fisher Scientific bundle instruments, reagents, cloud analytics, and AI modules, creating high switching costs while relying on a consumables-driven revenue stream. IDEXX’s VetLab platform now incorporates machine-learning algorithms that auto-interpret PCR traces and suggest clinical actions, reinforcing user loyalty. Zoetis leverages its Vetscan Imagyst AI engine to automate image analysis across hematology and cytology, complementing molecular assays.

Emerging players pursue portability and rapid turnaround. Alveo Technologies, in partnership with Royal GD, released a 45-minute avian-influenza PCR cartridge achieving 99% specificity, ideal for on-farm screening. bioMérieux’s acquisition of SpinChip Diagnostics gives it microfluidic technology that produces lab-quality immunoassays from whole blood in 10 minutes, positioning the firm for hybrid molecular-immuno platforms.

Investment flows increasingly target platforms that merge pathogen detection with resistance-gene analysis, cloud reporting, and epidemiological dashboards. Vendors able to deliver interoperable data across human, animal, and environmental health domains align with government One-Health strategies and may gain procurement preference.

Veterinary Molecular Diagnostics Industry Leaders

Idexx Laboratories Inc.

Thermo Fischer Scientific Inc.

Biomerieux SA

QIAGEN N.V.

Zoetis Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

White space is expanding for molecular platforms that shorten time-to-action during outbreaks while also fitting routine precision-medicine workflows for companion animals. Capacity pressure from high-consequence disease testing has already been demonstrated, such as the University of Minnesota processing more than 115,000 H5N1-related samples by May 2025, which reinforces demand for scalable PCR and sequencing that can be deployed across networks. One route to absorb these volumes is centralized, logistics-optimized reference testing, highlighted by Zoetis opening a 32,000-square-foot reference laboratory at the UPS Healthcare Labport in Louisville, Kentucky (May 2025), linking high-throughput molecular work with overnight specimen movement and faster reporting.

A second opportunity area is newer modalities and automation that broaden what can be tested and where. In 2025, Oxford Nanopore Technologies introduced the ElysION workstation to automate end-to-end sequencing workflows, reducing manual steps that often constrain adoption in veterinary labs with staffing constraints. On the assay-expansion side, NGS and novel assay chemistries are moving into focused veterinary use cases: MiDOG Animal Diagnostics launched MiDOG Parasite-Only Testing in July 2026 as a dedicated NGS-based parasite detection offering. Published research also continues to validate CRISPR-based and hybrid approaches for rapid pathogen detection in livestock syndromes, including diarrhea panels. Together, these developments point to opportunities for vendors that pair assays with curated genomic databases, cloud reporting, and training to address multi-species validation gaps and operational bottlenecks in decentralized testing.

Recent Industry Developments

- July 2026: MiDOG Animal Diagnostics launched MiDOG Parasite-Only Testing, positioned as a dedicated next-generation sequencing-based parasite detection test for veterinary medicine. The launch broadens molecular testing beyond bacteria and viruses into parasite and worm identification where microscopy and antigen tests can be limiting. It also reinforces the role of curated genomic databases and bioinformatics as competitive assets in veterinary diagnostics workflows.

- May 2025: Zoetis opened a 32,000-square-foot reference laboratory at the UPS Healthcare Labport in Louisville, Kentucky, expanding its diagnostics network and anchoring high-throughput services at a logistics hub. Co-location with a major healthcare logistics provider supports overnight specimen movement and faster turnaround for advanced testing, including molecular diagnostics. The build-out strengthens centralized capacity while raising the bar for network scale and service speed among large diagnostic providers.

- July 2024: Mars completed the purchase of Cerba HealthCare stakes in Cerba Vet and ANTAGENE, expanding its European reference-laboratory footprint. The acquisition consolidates testing capabilities and increases access to specialized diagnostics across the region, supporting higher sample throughput and broader test menus. Integration of reference-lab assets also supports recurring consumables and service revenue tied to molecular testing volumes.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the veterinary molecular diagnostics market covers molecular methods and related products used to detect, identify, or genotype animal pathogens and genetic conditions. Revenue is counted for test kits, reagents, instruments, and enabling software used in veterinary testing workflows.

Scope exclusions: Routine immunoassays, clinical chemistry and biochemistry analyzers, and imaging systems are excluded from this market sizing.

Segmentation Overview

- By Product

- Instruments

- Kits & Reagents

- Software & Services

- By Application

- Infectious Diseases

- Genetics

- Other Applications

- By Technology

- PCR

- Microarray

- DNA Sequencing

- By Animal Type

- Companion Animals

- Livestock

- By End User

- Veterinary Hospitals & Clinics

- Reference Laboratories

- Research Institutes

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the factual base for the model, so the market estimate is not built from assumptions alone. We reviewed public health and animal-disease reporting, then tied those signals to diagnostics adoption patterns across clinics, reference labs, and livestock settings.

Sources used include, such as the World Organisation for Animal Health (WOAH) disease updates, USDA and related animal health statistics, the European Commission and ECDC One Health and zoonoses material, and peer-reviewed journals indexed in PubMed that cover PCR and sequencing use in veterinary diagnostics. We also relied on company annual reports, investor presentations, product catalogs, and reputable press coverage for pricing direction and product mix. Where gaps existed, paid subscriptions for company financials and intelligence, news and financials, patent databases, and shipment-level trade data were used to cross-check activity and timing. These examples are not exhaustive, and many other public sources were reviewed for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary work focused on checking what desk research could not fully answer, mainly test volumes, typical pricing by assay type, and where molecular methods are actually being used (reference labs versus in-clinic workflows). We spoke with a mix of diagnostic laboratories, veterinary clinic decision-makers, distributors, and technical specialists across APAC, EMEA, and the Americas, so the final model could be tuned to real purchasing and utilization patterns.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 13% | APAC: 37% |

| Mid tier: 48% | Functional/Unit leaders: 35% | EMEA: 36% |

| Smaller Players: 21% | Managers: 52% | Americas: 27% |

Market-Sizing & Forecasting

Sizing starts from a top-down build where reported animal disease incidence, testing guidelines, and lab throughput signals are used to reconstruct the addressable diagnostics demand pool by major regions, and then the molecular share is applied. To keep the totals realistic, the output is corroborated with selective bottom-up approximations, such as sampled test volume checks from reference labs, channel feedback on reagent pull-through, and indicative ASP times volume for common PCR panels.

Key inputs used in the model include companion animal and livestock population trends, reportable disease outbreaks and surveillance intensity, typical test menu mix between PCR, isothermal methods, sequencing, and microarray, instrument placement and utilization ranges, and pricing progression for consumables versus instruments. Where a country level data series was thin, we filled gaps using regional proxies that were validated in interviews, then adjusted using trade and patent activity as supporting signals.

For forecasting, we used scenario analysis supported by near-term expert consensus on demand drivers like outbreak cycles, clinic-to-lab referral behavior, and point-of-care molecular adoption. Growth rates were then applied with checks so they align with practical constraints, including lab capacity expansion speed and consumables availability.

Data Validation & Update Cycle

Validation is done through multiple checks so the estimate is not driven by one data source. We compare the model outputs against independent signals, such as instrument installation momentum, reported testing intensity during outbreaks, and the expected split of revenue between consumables and capital equipment, and then outliers are reviewed before sign-off.

When large variances show up by region or by technology, analysts revisit assumptions, re-check calculations, and re-contact relevant experts to confirm what changed. Reports are refreshed annually, with interim updates when material events occur, such as major regulatory shifts or sudden disease waves. Before delivery, a final pass is completed so clients receive the latest updated view based on the newest public data and interview feedback.

Mordor Intelligence's Veterinary Molecular Diagnostics Market Size Compared With Other Published Estimates

Published market sizes for veterinary molecular diagnostics often differ because the counted product set, the year used for the starting point, and the way pricing and volumes are combined are not consistent across studies. Differences also come from whether results are built from disease-driven demand signals or from broader diagnostics spending pools.

Routine immunoassays and clinical chemistry analyzers sit outside Mordor Intelligence's scope, which is one reason the 2026 value can look higher or lower than figures that mix molecular methods with wider veterinary diagnostics tools or services. Another common driver is timing, since some sources cite 2023 or 2024 values and then apply faster or slower ASP progression without clearly tying it to reagent pull-through, instrument utilization, and outbreak-driven testing cycles.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.81 B (2026) | |

| Global Consultancy A | USD 1.12 B (2023) | Uses an earlier base year and a broader segment structure, and the write-up does not clearly separate molecular-only revenues from adjacent diagnostic categories across end users. |

| Industry Publisher B | USD 1.04 B (2024) | Starts from a 2024 base with a lower growth path and provides limited transparency on how test volumes, instrument placements, and consumables pricing were combined across regions. |

The spread is mainly explained by what gets included as molecular diagnostics, which year is quoted, and how pricing and utilization are validated. By keeping the scope limited to molecular kits, reagents, instruments, and enabling software, and then checking the totals against real-world testing and capacity signals, the estimate stays traceable to clear variables and repeatable steps.

Key Questions Answered in the Report

What is the current size of the veterinary molecular diagnostics market?

The market stands at USD 1.81 billion in 2026 and is projected to reach USD 2.74 billion by 2031.

Which application segment holds the largest share?

Infectious disease testing leads with 68.90% share in 2025 due to intensified surveillance for pathogens such as avian influenza H5N1.

Which region is growing the fastest?

Asia Pacific is forecast to grow at an 10.96% CAGR through 2031, driven by rising pet ownership and livestock intensification.

Which is the fastest growing region in Veterinary Molecular Diagnostics Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

How are portable diagnostics influencing the market?

Portable nanopore sequencing and rapid PCR cartridges are shifting testing from reference labs to farms and clinics, improving turnaround times and expanding access.

What role does antimicrobial-resistance surveillance play?

One-Health initiatives and regulatory targets for reduced antibiotic use are funding rapid resistance-gene panels, boosting demand for integrated molecular platforms.

Who are the key market leaders?

IDEXX Laboratories, Zoetis, Thermo Fisher Scientific, bioMérieux, and QIAGEN leverage bundled consumables, instruments, and AI-powered software to maintain competitive advantages.

Page last updated on: