Veterinary Reference Laboratory Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

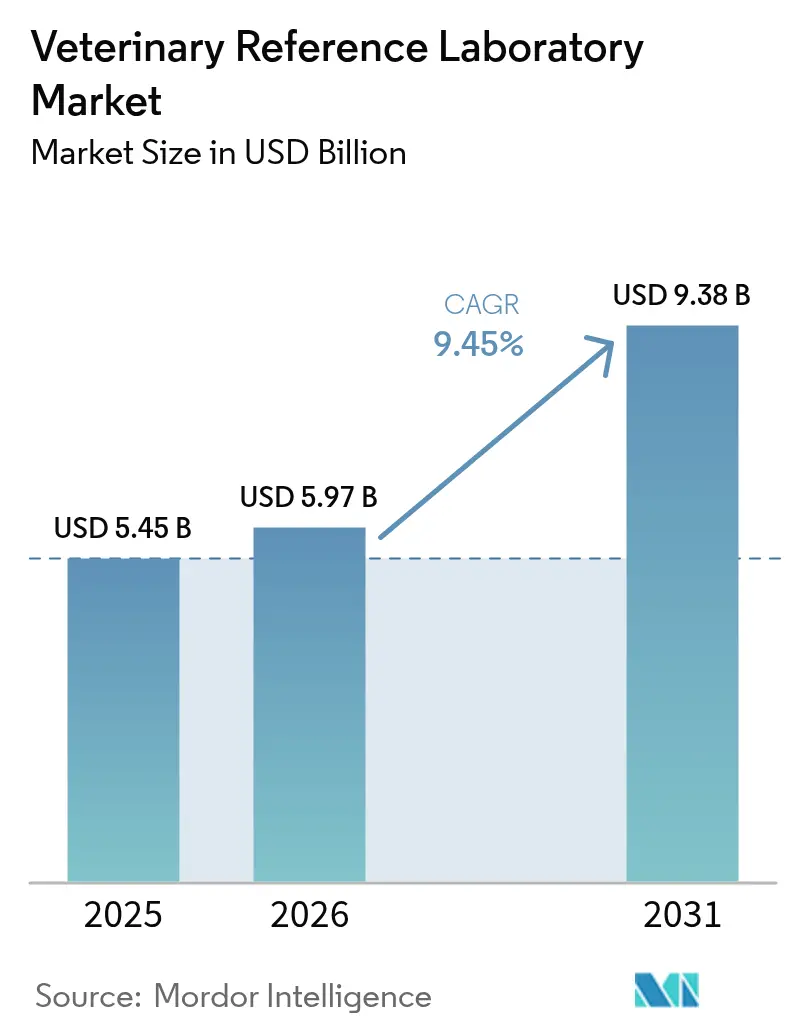

| Market Size (2026) | USD 5.97 Billion |

| Market Size (2031) | USD 9.38 Billion |

| Growth Rate (2026 - 2031) | 9.45% CAGR |

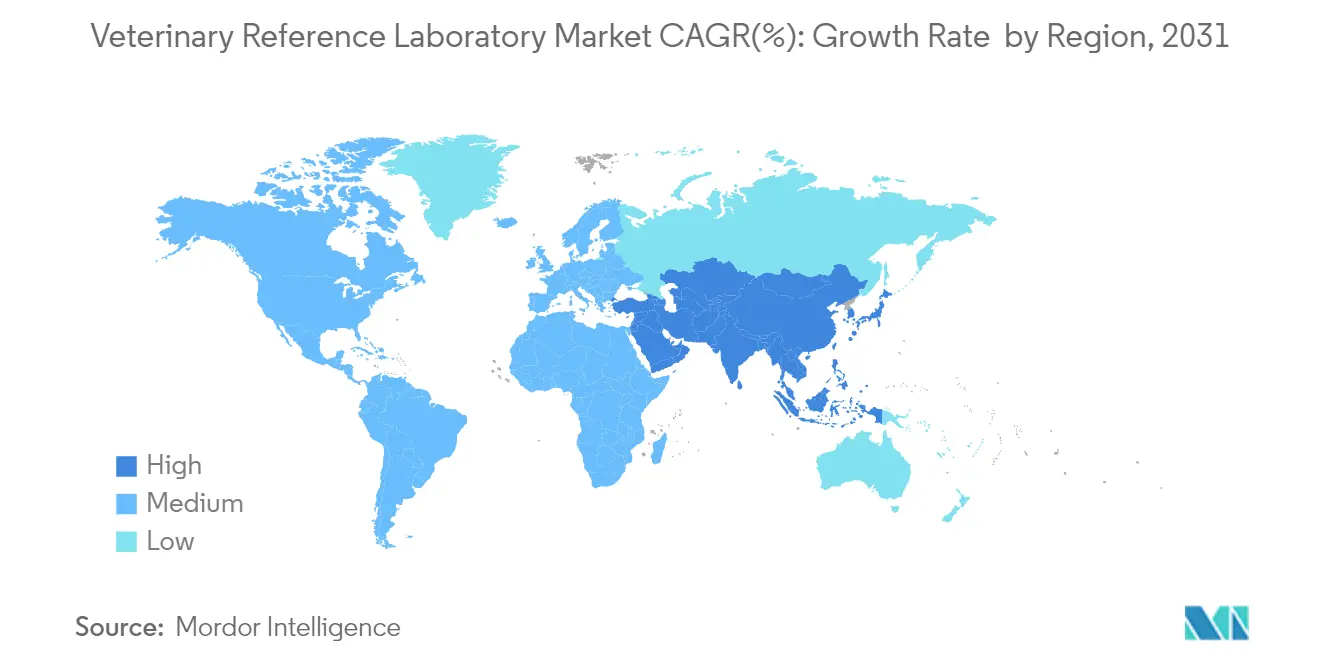

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

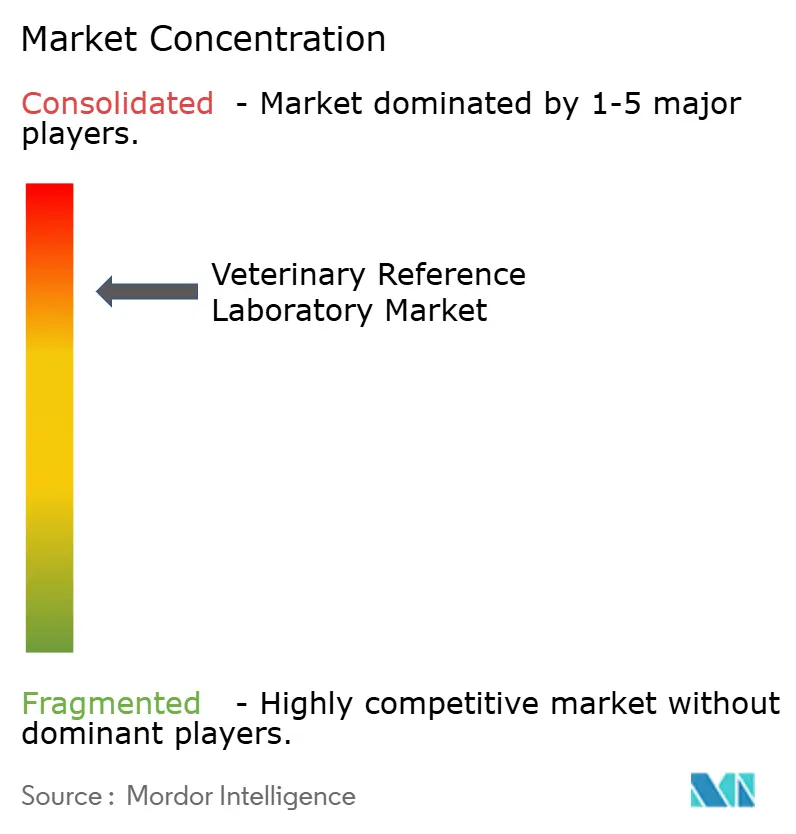

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Veterinary Reference Laboratory Market Analysis by Mordor Intelligence

Veterinary Reference Laboratory market size in 2026 is estimated at USD 5.97 billion, growing from 2025 value of USD 5.45 billion with 2031 projections showing USD 9.38 billion, growing at 9.45% CAGR over 2026-2031.

The veterinary reference laboratory market is valued at USD 5.45 billion in 2025 and is projected to reach USD 8.60 billion by 2030, registering a 9.58% CAGR. Strong pet humanization trends, growing pet insurance coverage, and steady technology breakthroughs in immuno- and molecular diagnostics underpin this expansion. The convergence of artificial intelligence, next-generation sequencing, and point-of-care testing enlarges clinical possibilities while compressing diagnostic turnaround times. Infectious disease surveillance mandates following H5N1 outbreaks and antimicrobial stewardship rules sustain recurring testing volumes. Industry participants respond by integrating reference laboratories, imaging, software, and tele-health assets into unified platforms that simplify the clinician workflow and lock in recurring revenue.

Key Report Takeaways

- By animal type, companion animals accounted for 65.05% of the veterinary reference laboratory market share in 2025; livestock applications are projected to grow at a 10.02% CAGR through 2031.

- By service type, immunodiagnostics led with 42.98% revenue share in 2025, while molecular diagnostics is forecast to expand at a 10.48% CAGR to 2031.

- By application, clinical pathology accounted for a 38.22% share of the veterinary reference laboratory market in 2025, and virology is projected to grow at an 11.05% CAGR through 2031.

- By end user, veterinary clinics held 48.05% of the veterinary reference laboratory share in 2025; point-of-care and in-house laboratories are set to grow at a 12.03% CAGR through 2031.

- By geography, North America retained a 38.90% revenue share in 2025, whereas the Asia-Pacific region is expected to post the fastest growth, with a 12.04% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Veterinary Reference Laboratory Market*

| Driver | (˜) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising companion animal population and pet-humanization trend | +2.10% | Global, strongest in North America and Asia-Pacific | Long term (≥ 4 years) |

| Growing uptake of pet insurance and higher veterinary spend | +1.80% | North America and Europe core, expanding to Asia-Pacific | Medium term (2-4 years) |

| Increasing prevalence of zoonotic and chronic animal diseases | +1.40% | Global, intensified in agricultural regions | Short term (≤ 2 years) |

| Technology advances in immuno- and molecular diagnostics | +1.60% | North America and Europe leading, Asia-Pacific following | Medium term (2-4 years) |

| Tele-veterinary logistics platforms boosting sample volumes | +0.90% | Global, pronounced in underserved areas | Short term (≤ 2 years) |

| Antimicrobial-stewardship rules elevating lab testing in food animals | +1.20% | North America and Europe, expanding globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing uptake of pet insurance and higher veterinary spend

Premiums reached USD 4.5 billion in 2024, more than doubling since 2019. Concentrated underwriting among the top ten insurers heightens reimbursement standardization, which in turn lifts acceptance of advanced diagnostics. Veterinary cost inflation of 8.24% reinforces the value proposition of insurance and encourages owners to authorize comprehensive testing without cost anxiety..

Technology advances in immuno- and molecular diagnostics

AI-enabled platforms such as Zoetis Vetscan Imagyst now deliver cytology, hematology, and urine-sediment readings inside the clinic. Next-generation sequencing cancer panels achieve 92.7% detection accuracy and reveal actionable genomic variants for therapeutic planning frontiersin.org. Multiplex PCR assays detect pathogens at 10 copies/µL while matching national reference standards.

Rising companion animal population and pet-humanization trend

U.S. households owned 87.9 million dogs and 73.8 million cats in 2024, and canine patients generated 81% of practice revenue. Owners increasingly demand human-grade diagnostics, evidenced by an 80% accuracy rate of liquid-biopsy cancer monitoring compared with 41% for conventional imaging.

Increasing prevalence of zoonotic and chronic animal diseases

More than 800 U.S. dairy herds experienced H5N1 infection during 2024, and 38 human cases were reported in California, spurring mandatory surveillance across species[1]Source: Centers for Disease Control and Prevention, “Human Cases of Highly Pathogenic Avian Influenza A(H5N1) — California,” cdc.gov. Expanded pathogen range in horses and cattle underscores the One Health imperative.

Restraints Impact Analysis of Veterinary Reference Laboratory Market*

| Restraint | (˜) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of advanced tests & lab automation | -1.30% | Global, with greater impact in emerging markets | Medium term (2-4 years) |

| Shortage of board-certified veterinary pathologists | -0.80% | North America & Europe primarily, expanding globally | Long term (≥ 4 years) |

| Clinic-level PoC diagnostics cannibalising send-out volumes | -0.70% | North America & Europe core, spreading to Asia-Pacific | Short term (≤ 2 years) |

| Data-privacy hurdles for cloud-based LIMS integration | -0.50% | Global, with varying regulatory intensity by region | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High cost of advanced tests and lab automation

Fully automated systems carry steep capital requirements that many small clinics cannot absorb. Over 80% of China’s pet hospitals earn under 2.4 million yuan annually, constraining equipment upgrades. Mobile laboratories and cartridge-based analyzers mitigate barriers but still require upfront hardware investment.

Shortage of board-certified veterinary pathologists

Aging specialist cohorts in North America and Europe lengthen turnaround for histopathology and cytology. AI triage solutions and virtual consult platforms extend expertise but cannot fully replace human judgment

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Veterinary Reference Laboratory Market Segment Analysis

By Service Type:

Molecular diagnostics erodes immunodiagnostics leadershipImmunodiagnostics held 42.98% of the veterinary reference laboratory market in 2025 based on entrenched use in routine screening. Molecular diagnostics, however, is forecast to compound at 10.48% through 2031 on the back of superior pathogen specificity, precision medicine, and shrinking run times. Multiplex PCR panels and next-generation sequencing propel this growth trajectory, supported by falling reagent costs and software automation. Immunodiagnostics’ installed base and clinician familiarity sustain its revenue, but competitive pressure steadily diverts high-value oncology and infectious disease testing toward molecular formats.

AI-enhanced cartridge analyzers bring molecular throughput into clinics, shortening result cycles from days to under an hour. Reference laboratories differentiate themselves with whole-genome and liquid biopsy services that inform targeted therapy selection. As test menus broaden, bundled subscription pricing models emerge, anchoring client loyalty and stabilizing cash flows. With these shifts, molecular platforms continue to capture incremental revenue while immunoassay providers add multiplex capability to defend share. Both segments fuel aggregate expansion of the veterinary reference laboratory market.

By Application:

Virology acceleration challenges clinical pathology dominanceClinical pathology accounted for 38.22% of 2025 revenues and remains indispensable for wellness exams and chronic-disease monitoring. Virology’s 11.05% CAGR outpaces every other application due to heightened H5N1 surveillance and mandatory influenza testing in livestock. Rapid antigen and RT-PCR panels, validated against national standards, dominate high-volume screening protocols and facilitate trade compliance. Regulatory emphasis on early detection prompts governments to subsidize virology capacity expansion in dairy, poultry, and equine sectors.

Meanwhile, antimicrobial-stewardship programs elevate bacteriology demand, and AI fecal-analysis systems accelerate parasitology adoption. Toxicology testing grows steadier, driven by rising pet exposure to household chemicals. Other niche applications appear as emerging pathogens and novel therapies require specialized assays. Collectively, diverse testing needs reinforce the growth prospects of the veterinary reference laboratory.

By Animal Type:

Companion animals continue to headline growthCompanion animals represented 65.05% revenue in 2025 and are on track for a 10.74% CAGR through 2031 as owners seek human-equivalent care. Dogs contribute the bulk of samples, although feline-specific innovations, such as bulk-acoustic-wave thyroid assays, gain traction. Enhanced insurance reimbursement and willingness to fund oncology panels solidify companion animals as the mainstay of the veterinary reference laboratory market. In contrast, livestock testing, although smaller, benefits from stringent biosecurity and food safety rules. Cattle surveillance intensifies following dairy-related H5N1 incidents, and multiplex assays targeting porcine respiratory pathogens sustain demand in swine operations. These programs, together, reinforce the veterinary reference laboratory market’s resilience across various animal categories.

Continued growth in companion care cascades into specialized equine sports-medicine panels and exotic-pet diagnostics, diversifying laboratory revenue streams. Livestock providers invest in on-farm sampling logistics and pooled testing to manage cost. Technology transfer between companion and livestock domains accelerates assay innovation and platform scalability.

By End User:

Point-of-care revolution reshapes service deliveryVeterinary clinics retained 48.05% share in 2025 but face stiff competition from fast-growing in-house and mobile laboratories, which post a 12.03% CAGR. Cartridge-based analyzers and cloud-linked microscopes empower clinicians to perform advanced assays without external referrals. Reference laboratories respond by offering specialized panels, guaranteed turnaround times, and integrated teleconsults. Veterinary hospitals leverage scale to deploy high-throughput analyzers, while start-ups design AI-driven interfaces that simplify the interpretation of complex assays.

Universities and research institutes maintain leadership in validation studies and novel assay development, providing a pipeline of technologies that are later commercialized by private laboratories. Telemedicine platforms blur the boundary between clinician and lab, funneling digital images and biometric data into cloud models for instant analytics. This multi-channel ecosystem enhances access, speed, and diagnostic depth, sustaining the broader veterinary reference laboratory market.

Geography Analysis

APAC Veterinary Reference Laboratory Market

Asia-Pacific is the fastest-advancing region at a 12.04% CAGR to 2031. China’s pet economy reached 300 billion yuan (USD 41 billion) in 2024 with veterinary care at 28% of spend, though profitability constraints in smaller clinics spur demand for cost-efficient diagnostics. Japanese innovators deploy AI-powered fecal analysis and after-hours tele-health, improving accessibility in an aging-society. Australia attracts multinational investment, as Zoetis expanded vaccine production capacity through a new Melbourne site. Varied regulatory frameworks and uneven infrastructure create a patchwork of opportunities across the region, yet rising household incomes and changing pet-owner behavior support sustained uptake of laboratory services.

North America Veterinary Reference Laboratory Market

North America maintained 38.90% market share in 2025 courtesy of mature practice infrastructure and high pet-care expenditure. FDA Guidance #263, effective June 2024, mandates prescription oversight for antimicrobials, indirectly boosting diagnostic volumes in food animals avma.org. Workforce shortages and declining clinic visits temper momentum, nudging providers toward automation to preserve productivity.

EMEA Veterinary Reference Laboratory Market

Europe demonstrates steady mid-single-digit expansion supported by regulatory harmonization and recent consolidation. Mars Incorporated completed acquisitions of SYNLAB Vet and Cerba Vet, enhancing test menu breadth and geographic reach . Antimicrobial-stewardship campaigns encourage diagnostics-guided therapy, and established veterinary training programs sustain demand for specialized assays. Emerging markets in the Middle East and Africa remain nascent yet promising, evidenced by the Philippines’ PHP 20 million investment in a new veterinary-diagnostic facility pna.gov.ph. Point-of-care platforms offer scalable options for regions lacking extensive laboratory networks, underlining a global convergence toward accessible diagnostics.

Competitive Landscape

Consolidation marks the competitive tone. Mars Incorporated folded Heska, SYNLAB Vet, and Cerba Vet into its Science & Diagnostics division within twelve months, crafting an end-to-end ecosystem spanning reference labs, imaging, rapid tests, and tele-health. IDEXX sustains innovation leadership, preparing to commercialize the inVue Dx cellular analyzer and multi-cancer screening panel, underpinned by an estimated USD 45 billion total addressable market. Zoetis differentiates itself through AI integration, adding cytology and hematology modules to Vetscan Imagyst, constructing a 32,000-square-foot reference lab in Louisville[2]Source: Zoetis Inc., “Zoetis Opens Largest Diagnostics Reference Laboratory in Louisville,” zoetis.com , and expanding manufacturing capacity in Australia.

Thermo Fisher’s intent to divest parts of its diagnostics unit for USD 4 billion signals potential reshaping of supply dynamics, possibly triggering new partnerships or acquisitions. Regional innovators, such as Japan’s Coo & RIKU, introduce AI-based fecal diagnostics, while U.S. start-ups like Moichor leverage cloud AI to reduce test costs, highlighting the white-space potential in affordable solutions. The strategic focus is shifting toward integrated hardware-software-data bundles that reinforce customer retention through subscription and consumable revenue streams. Competitive pressure, together with pathologist scarcity, accelerates AI adoption and automation, raising the innovation bar across the veterinary reference laboratory market.

Veterinary Reference Laboratory Industry Leaders

IDEXX Laboratories, Inc.

Greencross Vets

Heska Corporation

Zoetis Inc.

Mars Inc.

- *Disclaimer: Major Players sorted in no particular order

Veterinary Reference Laboratory Market Companies Covered in this Report

- IDEXX

- VCA Animal Diagnostic Services (Mars)

- Zoetis Reference Laboratories

- GD Animal Health (Royal GD)

- Heska

- Antech Diagnostics

- SYNLAB Vet

- Veterinary Pathology Group (VPG)

- Laboklin GmbH

- NationWide Laboratories

- Asia Veterinary Diagnostics

- CVS Group plc

- Pathovet (Latin America)

- IDEXX BioAnalytics

- Inovie Vet

- ProtaTek International

- Thermo Fisher Scientific (Vet diagnostic services)

- Neogen

- Virbac Diagnostics

- Boehringer Ingelheim Vetmedica Labs

- Phibro Animal Health Diagnostics

Recent Industry Developments in Veterinary Reference Laboratory Market

- June 2025: Zoetis launched AI Masses for rapid cytology on the Vetscan Imagyst analyzer expanding in-clinic capabilities.

- May 2025: Zoetis opened a 32,000 sq ft diagnostics reference lab in Louisville to improve turnaround times.

- June 2024: IDEXX added quantitative pancreatic lipase testing to the Catalyst platform, delivering results in under 10 minutes.

Veterinary Reference Laboratory Market Report Scope and Research Methodology

Market Definition and Coverage

According to Mordor Intelligence, the veterinary reference laboratory market captures only fee-based diagnostic services performed in independent or corporate laboratories that accept external animal samples, run tests such as immunoassays, clinical chemistry, hematology, and molecular diagnostics, and issue interpretive reports to veterinarians around the world. The valuation counts service revenue alone and excludes reagent retail, analyzer sales, and in-clinic point-of-care cartridges.

Scope exclusion: Tests executed inside primary veterinary clinics, farm-gate rapid kits, and purely academic teaching labs are excluded to avoid double counting.

Segments Covered in This Report

- By Service Type

- Clinical Chemistry

- Hematology

- Immunodiagnostics

- Molecular Diagnostics

- Urinalysis

- Others

- By Application

- Clinical Pathology

- Bacteriology

- Virology

- Parasitology

- Toxicology

- Others

- By Animal Type

- Companion Animals

- Dogs

- Cats

- Horses

- Others

- Livestock Animals

- Cattle

- Swine

- Poultry

- Others

- Companion Animals

- By End User

- Veterinary Hospitals

- Veterinary Clinics

- Research Institutes & Universities

- Point-of-Care / In-house Labs

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Primary Research

We followed desk work with interviews and surveys involving reference-lab executives, practicing veterinarians across North America, Europe, and Asia-Pacific, and procurement leads at corporate clinic chains. These conversations confirmed regional price dispersion, momentum toward molecular tests, and realistic turnaround time expectations, closing the key information gaps flagged earlier.

Desk Research

Our team first compiled publicly available animal health statistics and trade records from sources such as USDA-APHIS, Eurostat, the World Organisation for Animal Health, and national pet insurance associations. We then layered in customs datasets that quantify cross-border reagent flows. Company filings, IPO prospectuses, and recent 10-K statements from listed diagnostic providers offered revenue anchors and average selling price clues.

Next, we reviewed peer-reviewed journals on canine vector-borne disease prevalence, Questel patent abstracts covering multiplex PCR panels, and tender notices aggregated by Tenders Info that signal government surveillance demand. D&B Hoovers supplied firm-level growth rates that helped verify historical trends. The sources named are illustrative; many additional publications, conference proceedings, and industry portals informed data collection and validation.

Market-Sizing & Forecasting

A top-down reconstruction starts with companion and livestock animal populations, disease screening rates, and average tests per case to create an addressable test pool that is multiplied by validated service prices to reach the 2025 revenue baseline. Results are then cross-checked through selective bottom-up supplier roll-ups and sampled invoice audits gathered during primary calls.

Key variables inside the model include pet population growth, pet insurance enrollment ratios, incidence of zoonotic outbreaks, laboratory network consolidation rates, reagent price trajectories, and regional currency moves. Five-year projections rely on multivariate regression blended with ARIMA to capture cyclical livestock swings, while scenario analysis tests upside from rapid PCR uptake. Where bottom-up data were missing, comparable geography adjustment factors filled the void before final convergence.

Data Validation & Update Cycle

Each model run is stress tested by senior reviewers who compare outputs with independent metrics such as IDEXX segment disclosures, Volza shipment data, and reagent price indices. Variances beyond preset thresholds trigger re-contacts with field sources. Reports refresh annually, with interim updates issued when disease outbreaks or material M&A reshape market structure. Before delivery, an analyst makes a fresh pass so clients receive the latest view.

How Mordor Intelligence's Veterinary Reference Laboratory Market Size Compares to Other Published Estimates

Published estimates often diverge because firms bundle different service baskets, apply distinct price grids, and refresh figures at varying times. Our disciplined scope selection and continual primary network help narrow these uncertainties.

Gaps arise when other studies add in-clinic testing revenue, treat reagent sales as service income, or extrapolate using static price escalators. Some forecasts assume every new assay is adopted at double-digit rates, whereas Mordor aligns uptake to validated disease prevalence data and uses IMF average exchange rates, giving decision makers a defensible middle path.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 5.45 B (2025) | Mordor Intelligence | - |

| USD 4.90 B (2024) | Global Consultancy A | Includes clinic-run tests and applies uniform 12 % ASP uplift across regions |

| USD 4.60 B (2024) | Industry Association B | Uses mixed 2022 volumes without adjusting for inflation |

| USD 4.83 B (2025) | Trade Journal C | Forecast built solely on historical CAGR without primary validation |

The comparison shows external values cluster below ours, yet each shortfall links to broader or outdated assumptions. By triangulating validated volumes with current price intelligence, Mordor Intelligence delivers a balanced, transparent baseline that clients can trace and replicate with confidence.

Key Questions Answered in the Report

What is the current size of the veterinary reference laboratory market?

The market stands at USD 5.97 billion in 2026 and is forecast to reach USD 9.38 billion by 2031.

Which segment will grow fastest through 2031?

Molecular diagnostics leads with a 10.48% CAGR owing to precision medicine adoption and rapid PCR innovations.

Why is Asia-Pacific the key growth region?

Rising pet ownership, expanding middle-class spending, and rapid technology uptake propel a 12.04% CAGR in Asia-Pacific.

How are point-of-care platforms changing diagnostic delivery?

Cartridge analyzers and AI microscopes provide lab-grade results in clinics, driving a 12.03% CAGR for in-house testing.

What impact do zoonotic outbreaks have on the market?

Events like the H5N1 dairy-herd infections boost virology testing demand, elevating the segment to an 11.05% CAGR.

Page last updated on: