Companion Animal Diagnostic Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

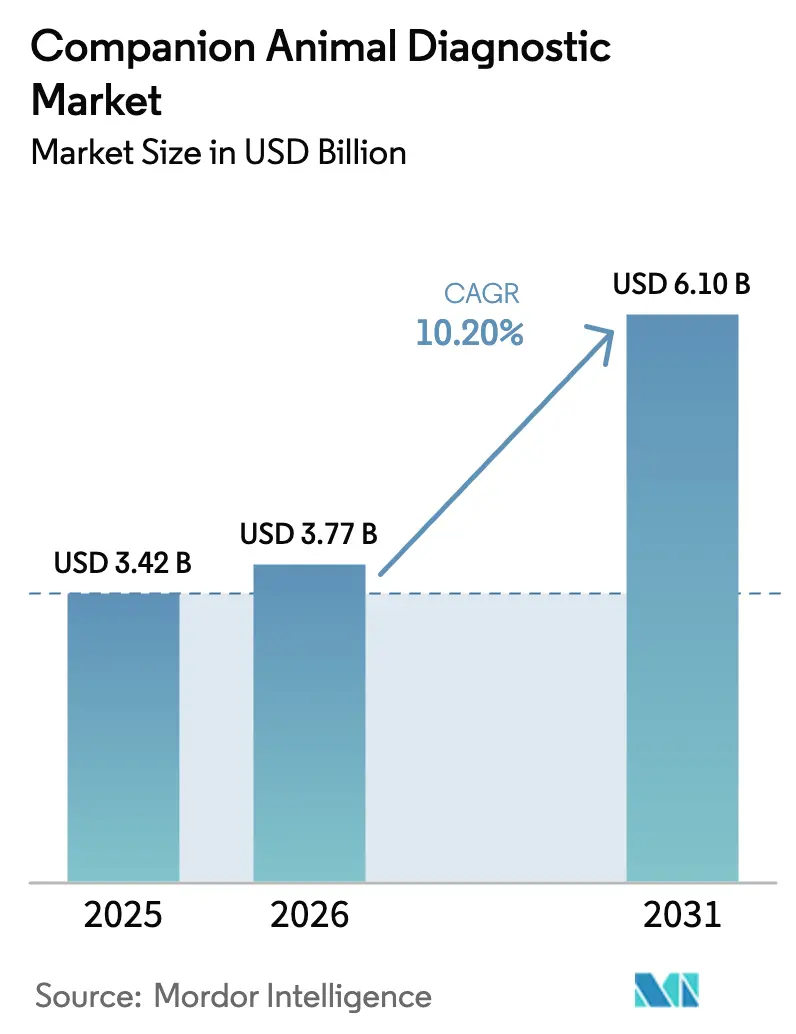

| Market Size (2026) | USD 3.77 Billion |

| Market Size (2031) | USD 6.10 Billion |

| Growth Rate (2026 - 2031) | 10.20% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Companion Animal Diagnostic Market Analysis by Mordor Intelligence

The companion animal diagnostic market size is projected to expand from USD 3.42 billion in 2025 and USD 3.77 billion in 2026 to USD 6.10 billion by 2031, registering a CAGR of 10.20% between 2026 to 2031. Substantial pet insurance uptake in North America, mandatory pathogen identification rules in the European Union, and rapid urban pet ownership in the Asia-Pacific region jointly underpin this expansion. Clinics are upgrading to AI-enabled point-of-care analyzers that shave diagnostic turnaround from two days to under fifteen minutes, strengthening in-house revenue streams. Regulatory mandates such as EU Regulation 2024/1973 have converted bacteriology from elective to compulsory testing, guaranteeing sustained volume growth and accelerating the shift from conventional culture to multiplex molecular panels. Meanwhile, the delayed but steep adoption curve in China, Japan, and India signals fresh white-space for suppliers that can balance advanced capability with lower selling prices. Competitive dynamics favor three vertically integrated leaders that already control instrument placements and reagent ecosystems, yet emerging microfluidic biosensors suggest disruptive potential over the next three years.

Key Report Takeaways

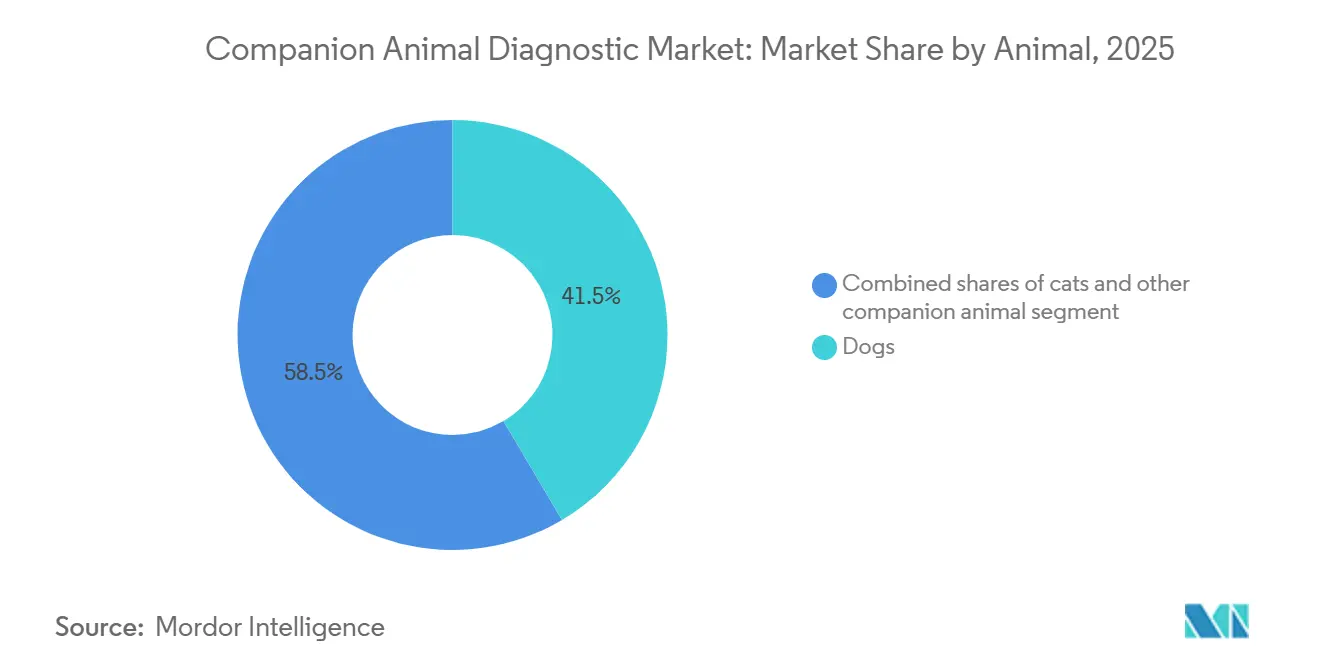

- By animal, dogs led with 41.5% of the companion animal diagnostic market share in 2025, while other companion animals are forecast to expand at an 11.23% CAGR to 2031.

- By application, clinical pathology held 33.4% revenue share in 2025, while parasitology is advancing at an 11.78% CAGR through 2031.

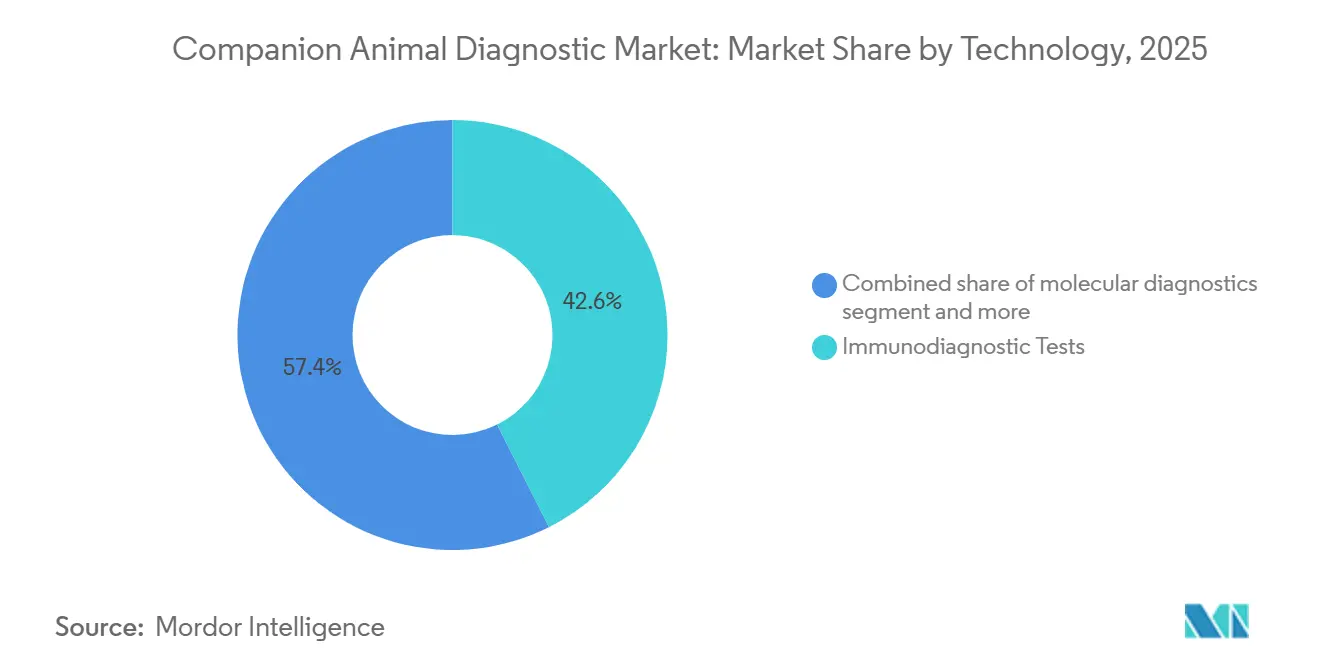

- By technology, immunodiagnostic tests accounted for 42.6% of spending in 2025; molecular diagnostics are projected to rise at an 11.98% CAGR to 2031.

- By end user, diagnostic laboratories commanded 46.5% revenue share in 2025; point-of-care and research settings are growing at a 12.21% CAGR through 2031.

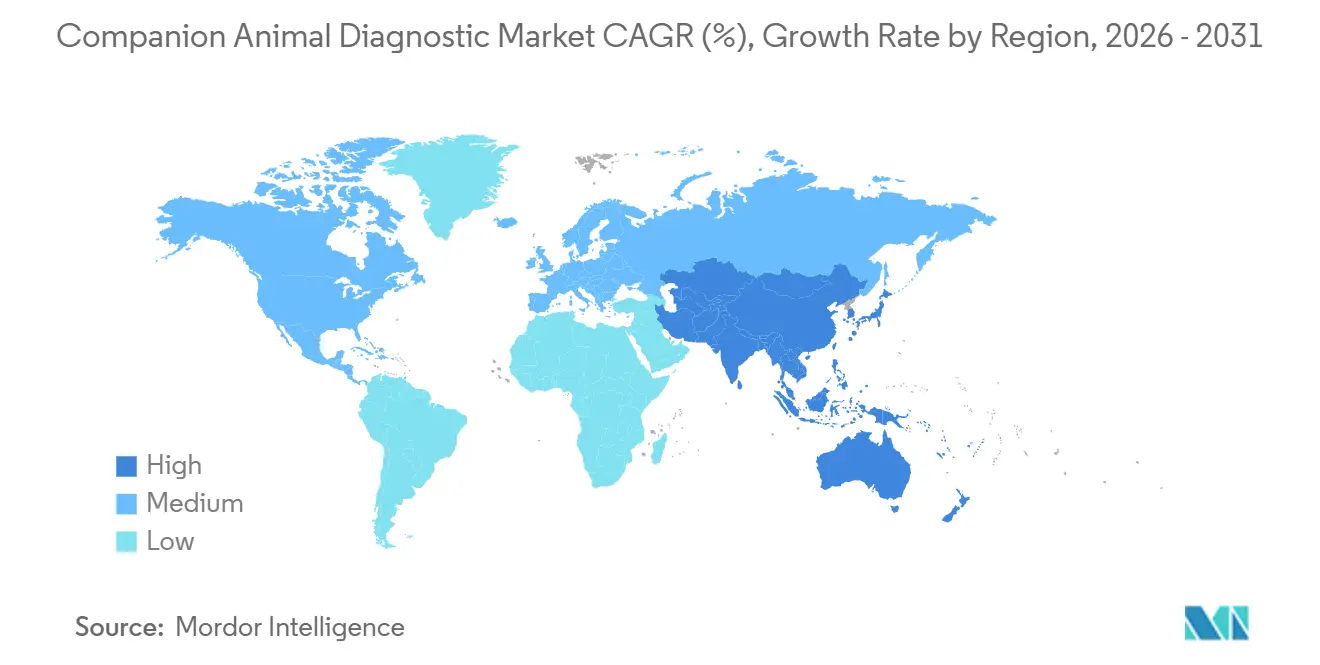

- By Geography, North America held 47.1% revenue share in 2025, and Asia-Pacific is expected to register a CAGR of 11.41% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Companion Animal Diagnostic Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for pet insurance | +1.8% | North America and EU core markets, with Australia penetration doubling from 10% (2020) to 21% (2024) | Medium term (2-4 years) |

| Growth in companion animal population | +2.1% | Global, with highest gains in Asia-Pacific urban centers (China 120M+ pets, Japan 18.4M pets, India 30M dogs) | Long term (≥ 4 years) |

| Increasing number of veterinary practitioners in developed economies | +1.2% | North America (127,536 US vets, 4.6% growth), Western Europe (33,000+ UK vets), Australia | Medium term (2-4 years) |

| AI-enabled point-of-care analytics lowering diagnostic turnaround | +2.3% | North America and EU lead adoption, spill-over to APAC metropolitan areas (Tokyo, Shanghai, Seoul) | Short term (≤ 2 years) |

| Growing adoption of multiplex panels for exotic pets | +0.9% | Global, concentrated in North America and EU specialty clinics with board-certified avian/exotic practitioners | Medium term (2-4 years) |

| Tele-veterinary platforms integrating at-home sample collection | +1.5% | North America pioneering (Labrador, FetchDx), expanding to EU and urban APAC markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Pet Insurance

North America closed 2023 with 5.36 million insured pets, a 6.8% year-on-year rise that still covered just 5.7% of the eligible population [1]North American Pet Health Insurance Association, “State of the Industry Report 2023,” naphia.org. Each percentage-point gain unlocks roughly USD 150 million in incremental test spending because insured owners are more than three times as likely to authorize advanced imaging and molecular panels. Mature European markets continue to expand more slowly, yet Australia doubled penetration to 21% by 2024, illustrating room for late-stage acceleration. Insurers increasingly bundle annual blood and urine panels into wellness policies, smoothing demand across economic cycles. Manufacturers that secure formulary inclusion can ride these prepaid volumes and protect pricing integrity.

Growth in Companion Animal Population

Urban Asia-Pacific now drives household pet acquisition: Japan’s dog-and-cat population reached 18.4 million in 2024, while China surpassed 120 million across tier-1 and tier-2 cities. Demography alone, however, does not ensure revenue; India’s ratio of one veterinarian for every 10,000 pets suppresses clinical test uptake despite a 30 million-dog population. The inflection occurs once middle-class households consistently allocate USD 300–500 per year to preventive care, a threshold now visible in Beijing, Shanghai, and Bengaluru. Global suppliers that pair lower-cost panels with remote-reading apps are best positioned to convert latent demand into billable volume.

Increasing Number of Veterinary Practitioners in Developed Economies

The United States workforce expanded to 127,536 veterinarians in 2024, enabling longer consultation windows and routine annual diagnostics [2]American Veterinary Medical Association, “Veterinary Workforce Statistics 2024,” avma.org. The United Kingdom logged 33,000 registered veterinarians the same year, while Germany, France, and Spain added 2,800 practitioners. Each additional clinician boosts laboratory utilization by USD 18,000 annually via wellness blood chemistry and fecal antigen screening. Geographic imbalances persist, so mobile diagnostic trucks and telemedicine platforms are emerging to serve rural undersupply, creating secondary equipment markets for compact analyzers.

AI-Enabled Point-of-Care Analytics Lowering Diagnostic Turnaround

Zoetis Vetscan Imagyst now interprets fecal floats, blood smears, urine sediment, and dermatology slides in under five minutes, with anomaly detection rates up to 15% over manual review. IDEXX Vetscan OptiCell automates hematology differentiation at USD 35,000 per unit, a price feasible for mid-size clinics. AI cuts turnaround from 24–48 hours to chair-side decisions, prompting broad in-clinic adoption. Reference laboratories respond by expanding esoteric menus such as next-generation sequencing panels that remain impractical on benchtop platforms.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating overall pet-care costs | -1.4% | Global, most acute in North America and EU where veterinary labor inflation exceeds 7% annually | Short term (≤ 2 years) |

| Limited reimbursement outside North America & Europe | -1.1% | Latin America, MEA, Southeast Asia, with penetration below 2% in Brazil, Argentina, Thailand, Vietnam | Long term (≥ 4 years) |

| Shortage of cold-chain logistics for advanced reagents in emerging markets | -0.7% | APAC emerging economies (India, Indonesia, Philippines), MEA, Latin America tropical regions | Medium term (2-4 years) |

| Rising antimicrobial-resistance regulations slowing bacteriology test approvals | -0.6% | EU core (Germany, France, Netherlands) under Regulation 2024/1973, expanding to North America and APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Reimbursement Outside North America & Europe

Latin America has fewer than 400,000 insured pets despite an 80 million-animal base, while Southeast Asia has fewer than 250,000 insured pets, leaving molecular assays priced at USD 80-150 beyond reach for most clinics. Cash-pay markets gravitate toward USD 25-40 chemistry panels, limiting diagnostic depth. Vendors must choose between discounted emerging-market SKUs or delayed entry until insurance platforms mature.

Escalating Overall Pet-Care Costs

Average U.S. veterinary spending per dog exceeded USD 1,200 in 2024, pushing uninsured owners to decline optional panels that collectively account for 22% of in-clinic diagnostic revenue. Practices now tier protocols into budget and comprehensive packages, risking under-diagnosis among price-sensitive clients. Suppliers that roll out subscription reagent pricing or lower-cost antigen tests can recapture volume without eroding margins.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Animal: Diagnostic Spending Dominated by Dogs, Surging Growth in Exotics

Dogs generated 41.5% of the companion animal diagnostic market revenue in 2025, supported by 65.1 million dog households in the United States and higher per-animal spend on breed-specific screening. Exotic pets, including birds and rabbits, will outpace all categories at an 11.23% CAGR, fueled by new multiplex PCR panels able to detect twelve psittacine pathogens from a single swab.

The segment’s momentum reflects a 14% rise in board-certified avian and exotic practitioners in 2024, creating professional demand for specialized assays. Economies of scope allow one USD 15 multiplex test to replace three separate USD 60 single-pathogen assays, expanding routine screening. This tailwind positions the exotic category as a pivotal contributor to companion animal diagnostic market growth between 2026 and 2031.

By Application: Parasitology Ascends via Tele-Veterinary Channels

Clinical pathology held 33.4% of application revenue in 2025, anchoring wellness exams and pre-anesthetic workups. Parasitology is projected to lead growth at an 11.78% CAGR, driven by at-home fecal kits mailed to reference labs, a workflow pioneered by Labrador’s USD 79 subscription.

Mail-in convenience appeals to time-constrained pet owners and removes clinic visit barriers, a model that processed 12,000 samples in Q3 2024 alone. Clinics counter by bundling parasite screens into puppy and kitten packages, preserving some in-house volume. Nevertheless, remote fecal testing will inject new recurring revenue into the companion animal diagnostic market while challenging clinic-centric sales channels.

By Technology: Molecular Assays Deliver Fastest Upside

Immunodiagnostics remained the largest spend bucket at 42.6% in 2025, but molecular diagnostics will drive an 11.98% CAGR to 2031, the fastest among all technologies. RealPCR panels now identify up to eight respiratory pathogens from one swab in six hours, enabling same-day therapy.

Sequencing-based oncology tests from Antech provide actionable mutation data for canine lymphoma at USD 450 per panel. These capabilities shorten empirical treatment and support antimicrobial stewardship mandates, propelling revenue expansion and reinforcing the premium tier of the companion animal diagnostic market.

By End User: Point-of-Care Capacity Expands Fastest

Diagnostic laboratories captured 46.5% revenue in 2025, leveraging broad menus and logistics scale. Point-of-care environments will post a 12.21% CAGR to 2031, aided by Heska’s Element POC system that unifies chemistry, hematology, immunoassay, and coagulation for about USD 45,000 per clinic.

Clinics favor real-time answers that influence care plans during client visits, relegating esoteric tests to reference labs. This in-house migration tilts consumable demand toward rapid cartridges, reinforcing recurring revenue streams and intensifying instrument placement battles among incumbent suppliers inside the companion animal diagnostic market.

Geography Analysis

North America represented 47.1% of 2025 revenue, buoyed by 5.36 million insured pets and a veterinary workforce exceeding 127,000 practitioners. Average annual spend per dog topped USD 1,200 in 2024, a level that supports early adoption of AI-driven analyzers and multiplex PCR panels. Canada contributes incremental growth, whereas Mexico remains under-penetrated, creating white-space for mid-tier reagent bundles. IDEXX booked 9% organic growth in Q3 2024, largely from North American clinics adding reference instruments.

Europe ranked second by value, propelled by pet insurance penetration above 25% in the United Kingdom and mandatory bacteriology testing under Regulation 2024/1973, a directive expected to lift culture volume by up to 30% within two years [3]European Medicines Agency, “Regulation 2024/1973,” ema.europa.eu. Scandinavia’s 40% penetration sustains premium diagnostics, while Southern and Eastern Europe lag due to lower discretionary income. Reference labs in Germany and France are adopting automated microbiology systems that shrink time-to-result to 24 hours, aligning with stewardship timelines.

Asia-Pacific is forecast to deliver an 11.41% CAGR through 2031, led by China’s 120 million-plus pet population and Japan’s mature clinic infrastructure. Insurance coverage remains below 1% in China, so suppliers courting the region emphasize lower-cost antigen tests and bundled wellness plans. Australia stands out with penetration doubling to 21% by 2024, enabling rapid analyzer installations. India’s undersupply of veterinarians caps near-term revenue, yet telemedicine platforms are starting to bridge access gaps in tier-one cities.

Competitive Landscape

IDEXX, Zoetis, and Neogen Corporation jointly command a majority of companion animal diagnostic market revenue through hardware, consumables, and cloud analytics ecosystems. IDEXX’s razor-and-blade model places subsidized instruments that lock clinics into proprietary reagent purchases; placements grew 11% in 2024. Zoetis leverages pharmaceutical distribution to cross-sell its Vetscan line, producing USD 198 million in Q3 2024 diagnostics revenue. Heska differentiates with its single-footprint Element POC analyzer that trims capital spend for small clinics.

Specialists fill niche gaps. Zoologix addresses exotic species with 12-pathogen PCR panels that lower per-pathogen costs by 75%. Tele-veterinary startups Labrador and QSM Diagnostics enable at-home fecal testing, capturing low-acuity volume that once flowed through brick-and-mortar clinics. BioMérieux and Thermo Fisher supply automated culture and reagent systems to reference labs but lack direct clinic channels, limiting visibility at the point of care.

Patent filings for saliva-based microfluidic chips targeting parvovirus and feline leukemia rose sharply in 2024, highlighting a potential platform shift toward non-invasive diagnostics. Incumbents may need to acquire these innovators or risk ceding share when commercial launches occur within three years.

Companion Animal Diagnostic Industry Leaders

Neogen Corporation

Zoetis Inc.

IDEXX Laboratories Inc.

INDICAL BIOSCIENCE GmbH

Randox Laboratories Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Zoetis acquired Veterinary Pathology Group in the UK and Ireland to broaden its diagnostics network.

- June 2025: IDEXX launched the Catalyst Cortisol Test, extending its point-of-care menu.

- January 2025: IDEXX rolled out Cancer Dx, a USD 15 blood panel for early canine lymphoma detection.

Global Companion Animal Diagnostic Market Report Scope

Companion animal diagnostics encompass a broad range of medical tools and tests used by veterinarians to detect, monitor, and manage the health of companion animals such as dogs, cats, and more.

The companion animal diagnostic market is segmented by animal, application, technology, end user, and geography. By animal, the market is categorized into dogs, cats, and other companion animals. By application, it is segmented into bacteriology, parasitology, clinical pathology, and other applications. By technology, the segmentation includes immunodiagnostic tests, molecular diagnostics, diagnostic imaging, and other diagnostics. By end user, the segmentation includes veterinary hospitals & clinics, diagnostic laboratories, and others. Geographically, the market is segmented across North America, Europe, the Asia-Pacific region, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Cats |

| Dogs |

| Other Companion Animals (birds, rabbits, etc.) |

| Bacteriology |

| Parasitology |

| Clinical Pathology |

| Other Applications |

| Immunodiagnostic Tests |

| Molecular Diagnostics |

| Diagnostic Imaging |

| Other Diagnostics (biosensors, microfluidics) |

| Veterinary Hospitals & Clinics |

| Diagnostic Laboratories |

| Others (Point-of-Care/In-house Testing and Research & Academic Institutes) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of APAC | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Animal | Cats | |

| Dogs | ||

| Other Companion Animals (birds, rabbits, etc.) | ||

| By Application | Bacteriology | |

| Parasitology | ||

| Clinical Pathology | ||

| Other Applications | ||

| By Technology | Immunodiagnostic Tests | |

| Molecular Diagnostics | ||

| Diagnostic Imaging | ||

| Other Diagnostics (biosensors, microfluidics) | ||

| By End-User | Veterinary Hospitals & Clinics | |

| Diagnostic Laboratories | ||

| Others (Point-of-Care/In-house Testing and Research & Academic Institutes) | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of APAC | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the companion animal diagnostics market?

The market is estimated to reach USD 3.77 billion in 2026 and is projected to hit USD 6.10 billion by 2031.

Which region holds the largest share of spending on companion animal tests?

North America led with 47.1% of global revenue in 2025 thanks to high insurance coverage and advanced clinic infrastructure.

Which application segment is growing fastest in diagnostics for pets?

Parasitology is advancing at an 11.78% CAGR through 2031, driven by at-home fecal testing kits and tele-veterinary adoption.

How is AI influencing diagnostic workflows in veterinary practice?

AI-enabled analyzers like Vetscan Imagyst and Vetscan OptiCell cut interpretation times to minutes and allow clinics to shift many tests in-house, boosting point-of-care revenue.

Page last updated on: