Animal Pregnancy Test Kit Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

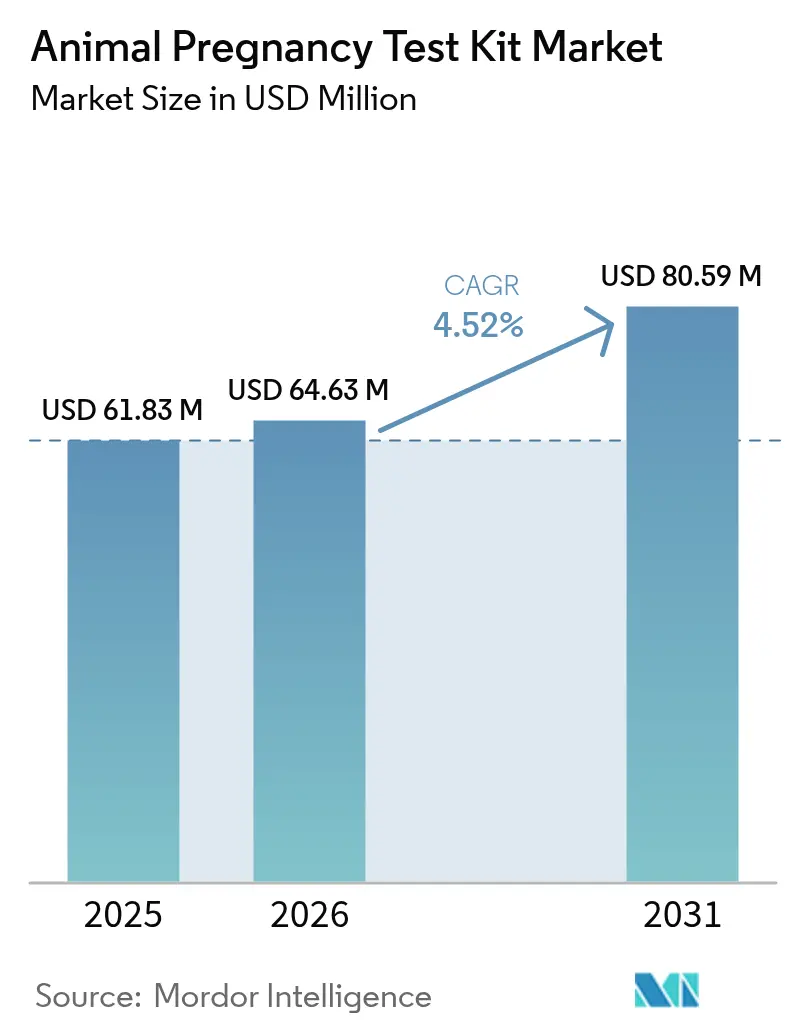

| Market Size (2026) | USD 64.63 Million |

| Market Size (2031) | USD 80.59 Million |

| Growth Rate (2026 - 2031) | 4.52% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Animal Pregnancy Test Kit Market Analysis by Mordor Intelligence

The Animal Pregnancy Test Kit market size is expected to grow from USD 61.83 million in 2025 to USD 64.63 million in 2026 and is forecast to reach USD 80.59 million by 2031 at 4.52% CAGR over 2026-2031. Steady expansion reflects mounting pet-humanisation, broader precision-livestock practices and technology that compresses result turnaround times. Growth remains resilient because producers view early pregnancy detection as a proven cost saver, while pet owners perceive rapid in-home testing as an extension of routine preventive care. Technological gains in lateral-flow and ELISA formats drive migration from lab-centric work-flows to point-of-care use, supporting clinical decision-making in minutes. Regulatory tightening, especially in the United States, raises entry barriers and nudges competitors toward differentiated sensor platforms that promise higher analytical sensitivity. Despite macro-economic caution, regional demand pockets emerge wherever veterinary insurance penetration improves and tele-health channels widen product access.

Key Report Takeaways

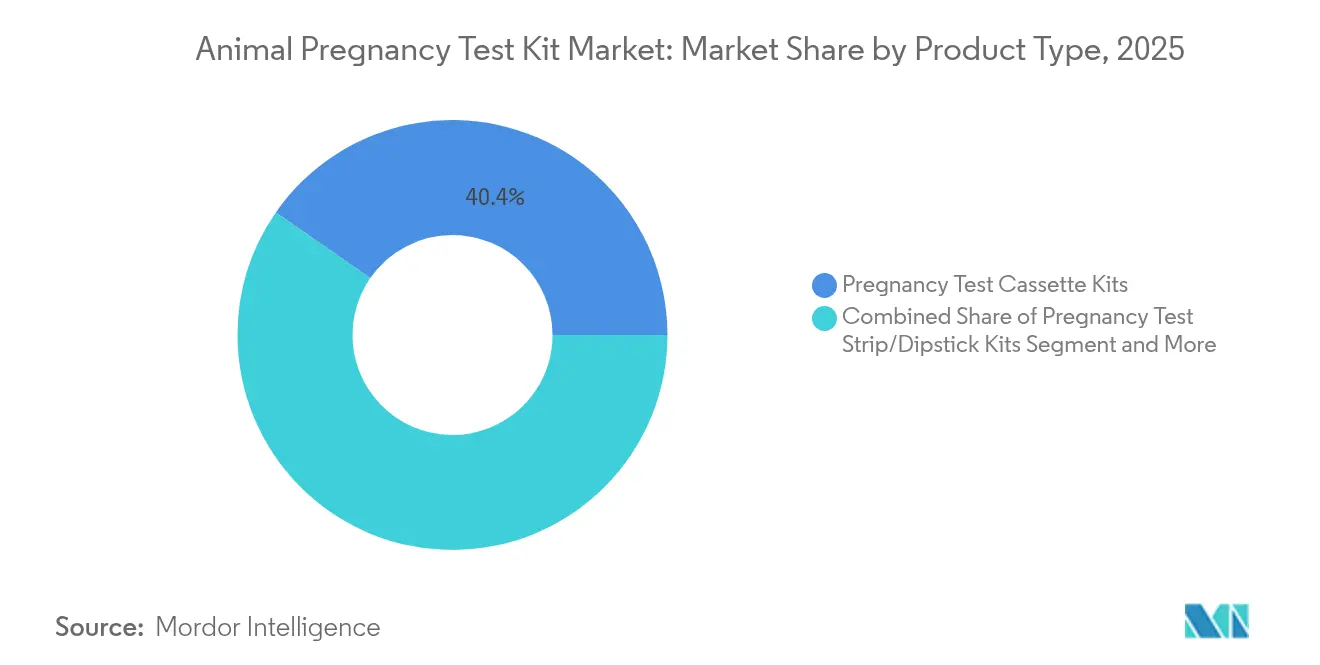

- By product type, pregnancy test cassette kits commanded 40.35% of animal pregnancy test kit market share in 2025, while ELISA-based kits are projected to compound at 6.28% CAGR through 2031.

- By animal type, livestock applications held 68.62% share of the animal pregnancy test kit market size in 2025 and companion animals are advancing at a 5.18% CAGR through 2031.

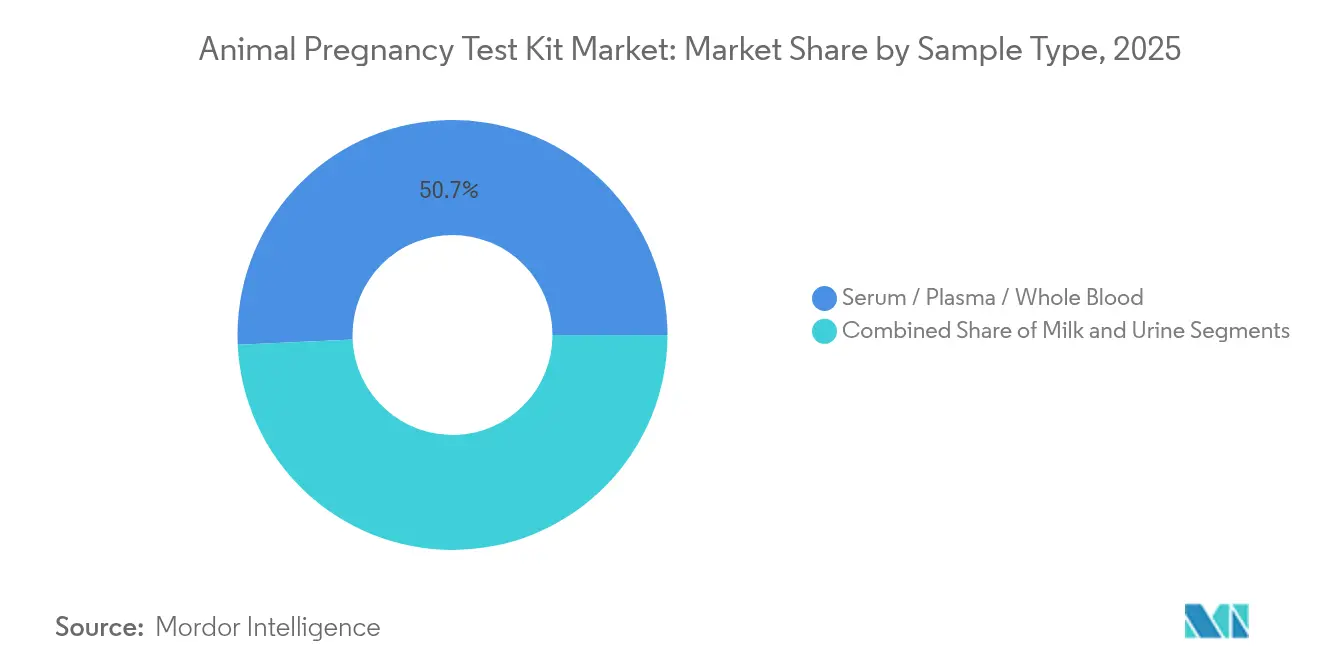

- By sample type, serum / plasma / whole-blood methods accounted for 50.72% share in 2025, whereas urine testing is on track for a 5.9% CAGR to 2031.

- By distribution channel, veterinary hospitals and clinics captured 44.71% revenue share in 2025, while e-commerce leads growth at 5.66% CAGR through 2031.

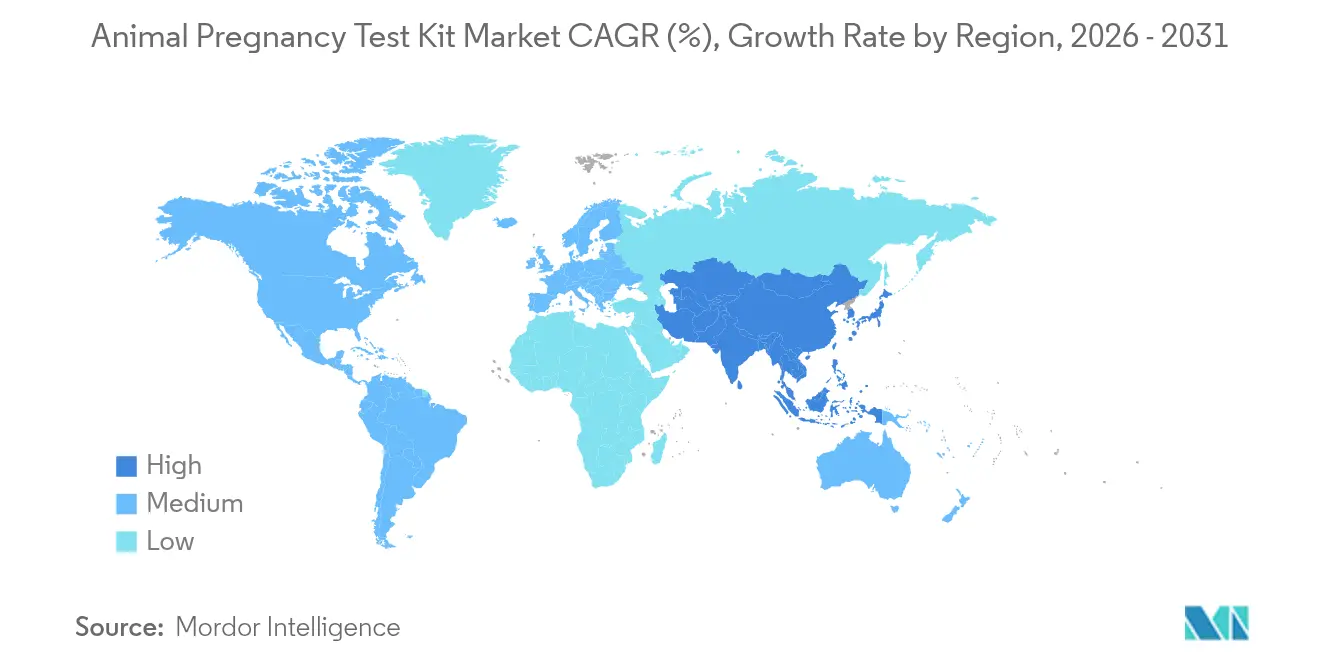

- By geography, North America led with 36.22% share in 2025; Asia-Pacific records the highest projected CAGR at 6.05% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Animal Pregnancy Test Kit Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Global Pet Ownership and "Humanisation" of Companion Animals | +0.8% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Increasing Herd-Fertility Economics for Dairy & Beef Producers | +0.7% | Global, strongest in North America, Europe, and Oceania | Long term (≥ 4 years) |

| Advances in Rapid Lateral-Flow & ELISA Diagnostic Formats | +0.6% | Global, with early adoption in developed markets | Short term (≤ 2 years) |

| Growing Veterinary Healthcare Spend & Insurance Penetration | +0.5% | North America & Europe core, expanding to APAC | Medium term (2-4 years) |

| Nanomaterial-Enabled Ultra-Early Biosensor Kits | +0.4% | North America & Europe, with spillover to APAC | Long term (≥ 4 years) |

| Tele-Veterinary Platforms Bundling At-Home Pregnancy Testing | +0.3% | Global, with fastest adoption in North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising global pet ownership and “humanisation” of companion animals

Companion animals shifted from utility roles to family status, prompting owners to request human-grade diagnostics, including at-home pregnancy tests. Post-pandemic pet adoptions boosted total dog and cat populations, creating sustained demand for preventive kits that slot seamlessly into routine wellness schedules.[1]Source: Rebecca Niemiec et al., “Addressing Access to Veterinary Care and Workforce Challenges,” Frontiers in Veterinary Science, frontiersin.org Direct-to-consumer brands such as Bellylabs report high reorder rates, suggesting strong repeat-usage behaviour. Younger owners, comfortable with digital retail, prefer instant results, encouraging manufacturers to integrate mobile read-outs for clearer interpretation. Insurance policies increasingly reimburse reproductive testing, further normalising purchase frequency. Early detection also cuts emergency caesarean costs, reinforcing the economic case for regular screening.

Increasing herd-fertility economics for dairy and beef producers

Producers face tight feed margins and milk-price volatility, turning pregnancy confirmation into a cost-avoidance imperative. Extension studies show early culling of open cows can save thousands of USD per herd annually.[2]Source: Maria Camila Lopez Duarte et al., “Pregnancy Diagnosis on Beef Cattle Today,” EDIS, edis.ifas.ufl.edu Yet only one-third of U.S. beef operations deploy structured testing protocols, highlighting latent demand. Adoption accelerates where herd-management software automatically imports test results and triggers breeding alerts. Sexed-semen programs rely on quick confirmation to recycle high-value embryos, multiplying kit utilisation. Livestock bankers increasingly look for evidence of reproductive efficiency when extending credit, indirectly reinforcing kit usage across commercial operations.

Advances in rapid lateral-flow and ELISA diagnostic formats

New membranes, improved antibody pairings and post-assay metal enhancement shave detection limits to femtomolar ranges, with some lateral-flow assays nearing 99% sensitivity and 96% specificity. ELISA methods employing fluorescent sandwich design detect biomarker concentrations well under 80 pg/mL, mirroring central-lab accuracy. Miniaturised microfluidic cassettes cut sample volumes to microlitre levels, allowing field use without cold-chain logistics. Veterinary practices value immediate answers that let them reschedule breeding cycles the same day. As manufacturing scale rises, unit costs have begun to fall, paving the way for hybrid platforms that marry lab precision with bedside convenience.

Growing veterinary healthcare spend and insurance penetration

Insurance coverage widens the affordability envelope for diagnostics. Policies in the United States now cover selected reproductive tests, driving higher utilisation in insured pets versus uninsured cohorts. Corporate clinic chains bundle pregnancy kits into annual wellness packages, creating subscription revenue while smoothing owner outlays. In livestock, co-operatives negotiate bulk procurement that lowers per-test cost for members, reinforcing periodic testing habits. The trend fosters a virtuous cycle where broader coverage increases test volumes, which in turn funds further R&D for even faster formats.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Price Point of Advanced Kits for Smallholders | -0.9% | Global, most acute in developing markets and rural areas | Medium term (2-4 years) |

| Sub-Optimal Sensitivity / Specificity Causing False Results | -0.7% | Global, with higher impact in resource-limited settings | Short term (≤ 2 years) |

| Low Practitioner Awareness in Emerging Markets | -0.6% | APAC, Latin America, and Africa | Long term (≥ 4 years) |

| Regulatory Grey-Zones for DTC Animal Diagnostics | -0.5% | Global, with particular complexity in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High price point of advanced kits for smallholders

ELISA kits can cost up to five times more than basic lateral-flow strips, ranging from USD 15-50 per test, a significant outlay for small farms where average daily milk margins remain thin.[3]Source: New Mexico Department of Agriculture, “Veterinary Diagnostic Services Fee Schedule,” nmdeptag.nmsu.edu The economics worsen when repeat testing is needed across long breeding seasons. Portable ultrasound systems present an even steeper hurdle, with initial investment exceeding USD 2,000 and further training costs. Without subsidised access, uptake among smallholders stays muted, limiting volume growth in emerging economies that house the bulk of global livestock.

Sub-optimal sensitivity / specificity causing false results

Although headline accuracy figures approach human diagnostics, real-world performance varies according to sampling technique, biomarker stability and operator skill. False positives can mislead cattle managers into delaying rebreeding open cows, translating into lost lactation days and feed sunk costs. Early gestation tests carry higher false-negative risk when biomarker titres remain low, eroding practitioner confidence. Manufacturers respond with clearer sample-handling instructions and smartphone applications that guide result interpretation, yet continuous field validation remains essential to overcome entrenched scepticism.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: ELISA technology drives premium segment growth

The animal pregnancy test kit market size allocated to product types shows pregnancy test cassette kits retained 40.35% revenue share in 2025, but ELISA kits are projected to advance fastest at 6.28% CAGR. Livestock operators often reach for cassette formats because they are rugged, cost-efficient and offer herd-level economies. Conversely, equine breeders and companion-animal clinics pay premiums for ELISA’s quantitative read-outs that support precise gestation staging, a capability lateral-flow strips lack. Hybrid microfluidic cartridges now blend rapid flow paths with ELISA capture chemistry, trimming assay time to under 15 minutes without sacrificing analytical power. As regulatory scrutiny strengthens, professional buyers favour formats that provide electronic audit trails, an emerging competitive differentiator.

While cassette kits remain ubiquitous on dairy farms, ELISA penetration rises wherever insurers reimburse test costs, tilting purchasing toward accuracy over price. The animal pregnancy test kit market sees manufacturers reposition strip-/dipstick products as mid-tier options that cater to mixed-practice clinics needing balanced cost and reliability. With nanomaterial-enhanced sensors entering late-stage validation, incumbent formats face future substitution risk, yet price elasticity in commodity-focused livestock segments suggests cassettes will defend baseline volumes through 2031.

By Animal Type: Companion animals outpace livestock growth

Livestock held 68.62% of animal pregnancy test kit market share in 2025, largely due to the sheer scale of global cattle inventories. Companion-animal testing, however, clocks a 5.18% CAGR, reflecting owners’ readiness to emulate human prenatal care protocols. Bovine testing enjoys entrenched protocols that tie pregnancy confirmation to feed rationing and genetic selection, making kits a predictable input expense. Swine producers now integrate whole-blood rapid assays into automated farrowing-management systems, enhancing litter planning accuracy.

In household pets, direct-to-consumer formats such as canine saliva and urine cassettes drive incremental volume with minimal veterinary intervention, mirroring human home pregnancy testing. Feline testing, historically limited to veterinary labs, benefits from newer progesterone chemistries that allow chair-side screening. These shifts anchor the animal pregnancy test kit industry’s move toward diversified portfolios that cater simultaneously to farm bio-economics and boutique pet-care preferences.

By Sample Type: Urine testing gains momentum

Serum, plasma and whole-blood samples controlled 50.72% revenue in 2025, a testament to veterinarians’ familiarity with venipuncture and established biomarker correlation ranges. Urine testing accelerates at 5.9% CAGR as owners value needle-free collection and reduced animal stress. Chemical stabilisers extend urine sample shelf life to 48 hours, permitting shipment from remote barns to reference labs without cold chains. Milk testing occupies a functional niche in dairy herds, where routine sampling dovetails with fat-protein analysis and mastitis surveillance.

For canine and feline owners, urine-based kits mean testing can occur at home, with smartphone apps that colour-match strip results for higher reliability. Livestock urine tests continue to improve accuracy through nano-structured electrodes that amplify hormonal signal strength. The animal pregnancy test kit market size generated from urine formats is expected to multiply as regulatory clearance for direct-to-consumer distribution widens.

By Distribution Channel: E-commerce disrupts traditional models

Veterinary hospitals and clinics retained 44.71% revenue share in 2025, anchored by trust, professional guidance and bundled reproductive-health services. Nevertheless, online platforms are expanding fastest at a 5.66% CAGR because they offer price transparency, doorstep delivery and educational content that demystifies usage. Retail farm stores maintain relevance for smallholders seeking immediate supply replenishment, yet they lack the depth of product selection found online.

In the companion segment, influencers and breeder networks promote specific e-commerce brands, triggering viral demand spikes and recurring subscription orders. For livestock operations, cloud-based dashboards now integrate with supplier APIs, auto-reordering kits when pregnancy testing events are scheduled, thus embedding e-commerce into herd-management routines. Regulatory oversight grows stricter for online sales, compelling platforms to verify product licences and ensure post-sale customer support.

Geography Analysis

North America generated 36.22% of 2025 revenue, propelled by advanced veterinary infrastructure, insurance uptake and strict reproductive management norms. The United States spearheads adoption of AI-supported reference labs that report pregnancy status within hours, allowing same-day rebreeding decisions. Canada benefits from dairy supply-management incentives that reimburse pregnancy testing, while Mexico’s export-oriented beef sector adopts kits to meet traceability mandates.

Asia-Pacific records a 6.05% CAGR, the fastest worldwide, as expanding commercial dairies in China and India turn to low-cost cassette kits to boost calving intervals. Urban pet ownership in Tokyo, Seoul and Shanghai fuels direct-to-consumer sales, especially urine-based formats. Veterinary associations in Thailand and Vietnam partner with manufacturers to subsidise training, narrowing the practitioner awareness gap. Price sensitivity remains pronounced in rural smallholder communities, yet cooperative bulk-buying schemes begin to dilute cost barriers.

Europe represents a mature but innovation-centric terrain. Dairy producers in France and Germany integrate milk pregnancy assays into robotic milking systems, securing consistent herd-level data streams. The European Food Safety Authority’s push for validated diagnostic performance standards benefits ELISA suppliers with established clinical dossiers. Eastern European markets witness rapid catch-up growth as EU rural-development funds back reproductive efficiency projects. Collectively, these patterns affirm the animal pregnancy test kit market’s regional mosaic, where domestic regulatory stance and economic structure dictate adoption velocity.

Competitive Landscape

The animal pregnancy test kit market balances moderate fragmentation with pockets of concentration. IDEXX Laboratories anchors its position through the Alertys suite that spans blood, milk and on-farm lateral-flow formats, providing an end-to-end ecosystem that discourages brand switching. Zoetis deepens service breadth via its 2025 Louisville reference lab, shortening turnaround times and offering integrated analytics that flag reproductive disorders before they erode productivity. Neogen leverages its sizable distribution footprint to place cassette kits in retail farm outlets, widening reach among smallholders.

Regulatory change operates as a competitive moat. The FDA’s Laboratory Developed Tests rule obliges new entrants to align with medical-device quality systems, elevating compliance costs and favouring incumbents with prior documentation. Simultaneously, breakthrough R&D in nanomaterial sensors tempts venture-backed disruptors who propose femtomolar detection at commodity prices, though few have yet met full regulatory readiness.

Strategic partnerships proliferate. Software vendors integrate kit data into breeding-management dashboards, and tele-health platforms co-brand pregnancy tests to drive consultation revenue. Mergers and acquisitions continue, exemplified by Mars Inc.’s talks to acquire Cerba Vet and ANTAGENE, hinting at cross-pollination between pet-food giants and diagnostic specialists. Market participants now view technology scalability—rather than raw manufacturing volume—as the decisive lever for sustainable share gains within the animal pregnancy test kit market.

Animal Pregnancy Test Kit Industry Leaders

IDEXX laboratories

Fassisi

Bio Tracking

BioNote Incorporation

J and G Biotech Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2023: A simple progesterone test kit for gilts developed at Chulalongkorn University entered multi-country pilot deployment, promising faster on-farm decisions.

- July 2023: Ring Biotechnology Co. Ltd. introduced a whole-blood rapid cow pregnancy test that targets pregnancy-associated glycoproteins for early detection.

Global Animal Pregnancy Test Kit Market Report Scope

As per the scope of the report, animal pregnancy test kits are rapid-response kits used to determine the pregnancy status of an animal. These are commonly used in animal husbandry units to determine whether induced or artificial insemination was successful. The animal pregnancy test market is segmented by Product Type (Pregnancy Test Kit Cassettes, Pregnancy Test Kit Strips, and Enzymes-Linked Immunoassay Test Kits), Distribution Channel (Veterinary Hospitals and Clinics, Retail Stores, and E-commerce), and Geography (North America, Europe, Asia-Pacific, and Rest of the World). The report offers the value (in USD million) for the above segments.

| Pregnancy Test Cassette Kits |

| Pregnancy Test Strip/Dipstick Kits |

| ELISA-based Kits |

| Companion Animals | Dogs |

| Cats | |

| Other Companion Animals | |

| Livestock | Bovine |

| Equine | |

| Swine | |

| Small Ruminants |

| Serum / Plasma / Whole Blood |

| Milk |

| Urine |

| Veterinary Hospitals and Clinics |

| Retail Stores |

| E-commerce |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Rest of the World |

| By Product Type | Pregnancy Test Cassette Kits | |

| Pregnancy Test Strip/Dipstick Kits | ||

| ELISA-based Kits | ||

| By Animal Type | Companion Animals | Dogs |

| Cats | ||

| Other Companion Animals | ||

| Livestock | Bovine | |

| Equine | ||

| Swine | ||

| Small Ruminants | ||

| By Sample Type | Serum / Plasma / Whole Blood | |

| Milk | ||

| Urine | ||

| By Distribution Channel | Veterinary Hospitals and Clinics | |

| Retail Stores | ||

| E-commerce | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Rest of the World | ||

Key Questions Answered in the Report

Which product category is growing fastest?

ELISA-based kits register the highest projected growth at 6.28% CAGR due to laboratory-grade sensitivity and quantitative results.

Why are companion-animal pregnancy tests gaining traction?

Pet humanisation and expanding insurance coverage drive owners to seek the same preventive diagnostics used in human healthcare, pushing a 5.18% CAGR in the companion segment.

How will new U.S. regulations affect market entry?

The FDA’s Laboratory Developed Tests rule mandates stringent device-quality systems, increasing compliance costs and raising entry barriers for start-ups.

Which region offers the fastest growth potential?

Asia-Pacific leads with a forecast 6.05% CAGR, supported by commercial dairy expansion and rising urban pet ownership.

Are urine-based tests reliable for early detection?

Recent nano-enhanced urine assays achieve accuracy rates that rival blood-based methods, making them a viable, needle-free option for home and farm use.

Page last updated on: