High Pressure Balloon Catheter Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

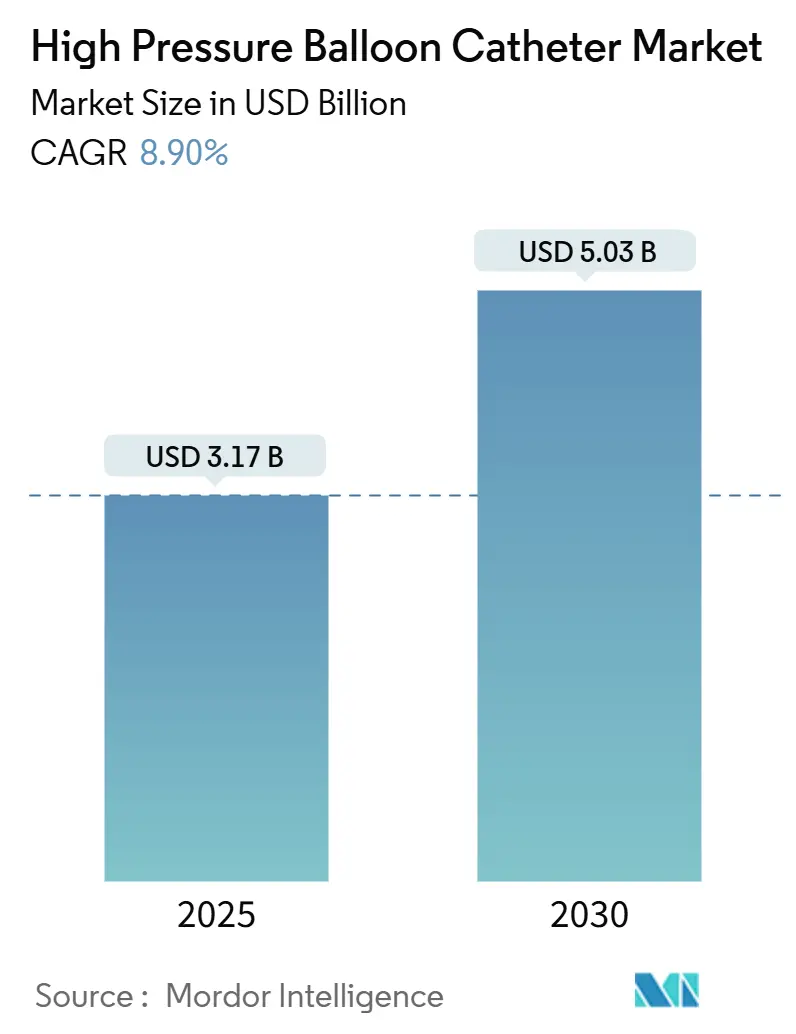

| Market Size (2025) | USD 3.17 Billion |

| Market Size (2030) | USD 5.03 Billion |

| Growth Rate (2025 - 2030) | 8.90% CAGR |

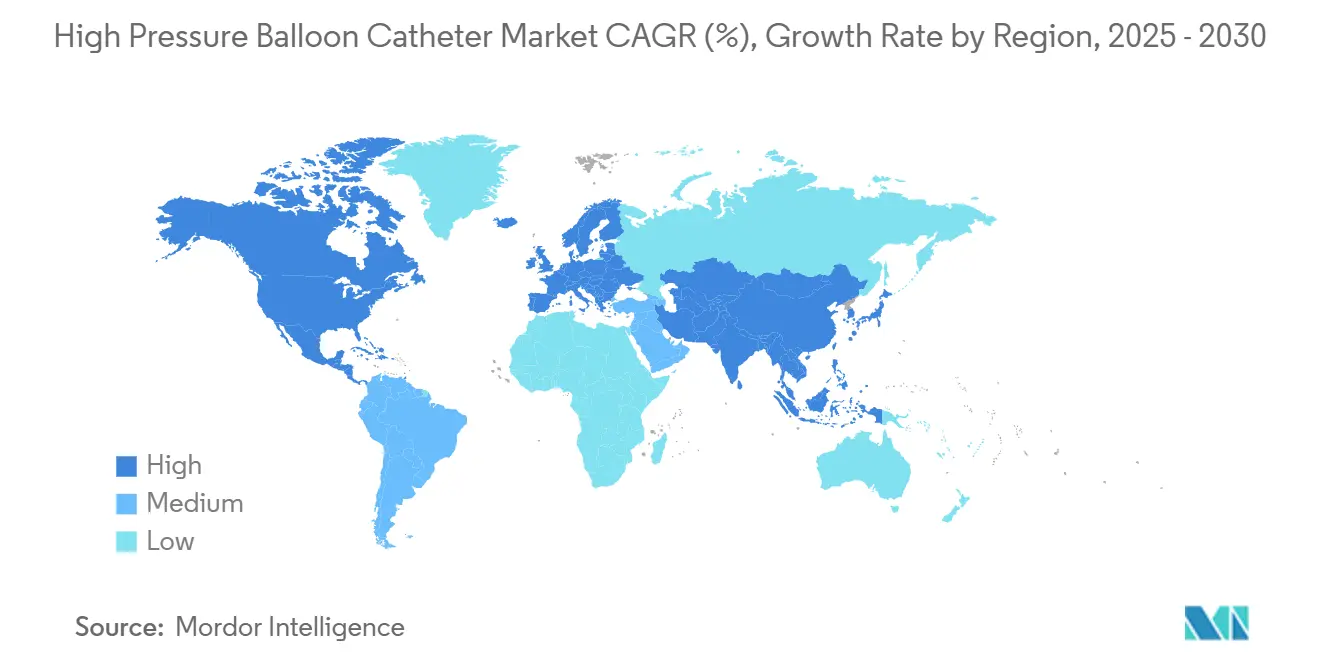

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

High Pressure Balloon Catheter Market Analysis by Mordor Intelligence

The high-pressure balloon catheter market size reached USD 3.17 billion in 2025 and is forecast to reach USD 5.03 billion by 2030, translating to an 8.9% CAGR over the period. The expansion reflects rising procedure volumes for complex coronary and peripheral lesions, escalating cardiovascular disease prevalence, and sustained innovation aimed at ultra-high-pressure performance. Nylon and polyethylene terephthalate (PET) remain the core balloon materials because they balance burst strength and deliverability, while composite designs are extending rated burst pressures toward 40 ATM. Device makers are also capitalizing on procedure migration to outpatient settings, which improves patient access and lowers total cost of care. Regionally, North America leads adoption, yet Asia Pacific shows the fastest uptake as health-care infrastructure strengthens and reimbursement frameworks broaden. Competitive intensity is moderate because a handful of diversified firms hold long-standing cardiology franchises, but specialist entrants are gaining share in structural heart and drug-coated balloon niches.

Key Report Takeaways

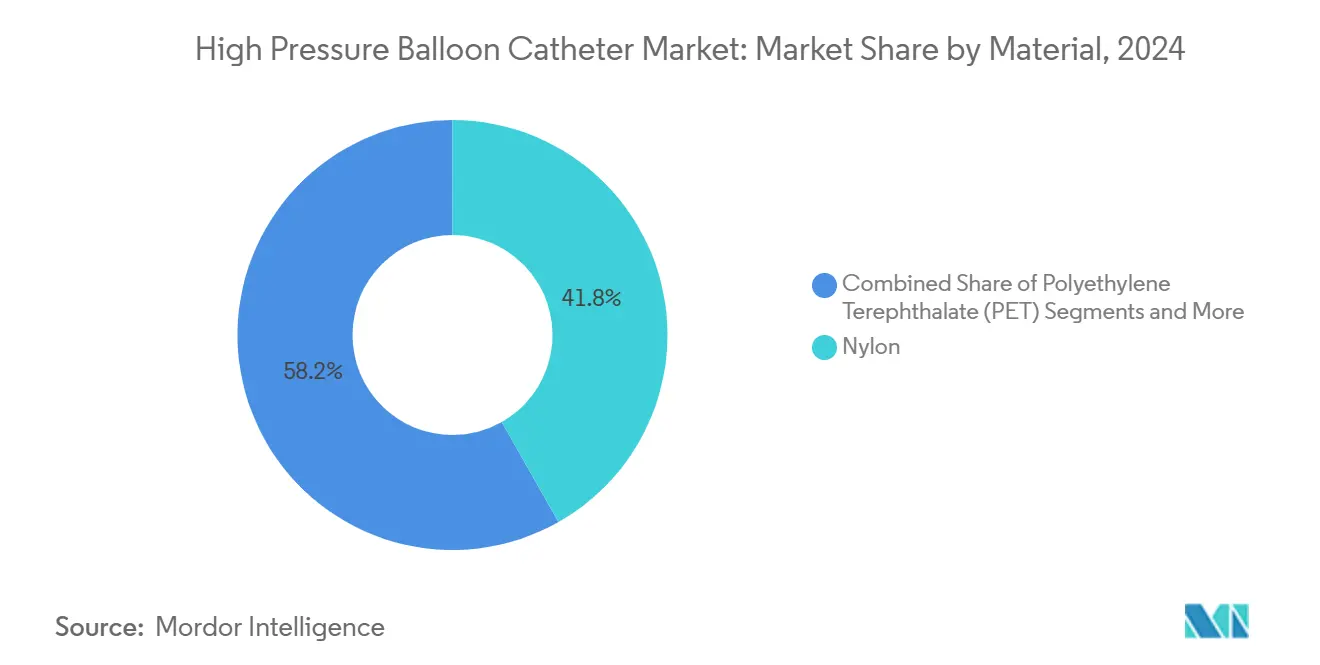

- By material, nylon led with 41.8% of 2024 sales, while PET is projected to advance at a 9.5% CAGR from 2025 to 2030.

- By application, coronary angioplasty commanded 62.3% of 2024 revenue, whereas peripheral angioplasty is forecast to grow the fastest at a 10.8% CAGR through 2030.

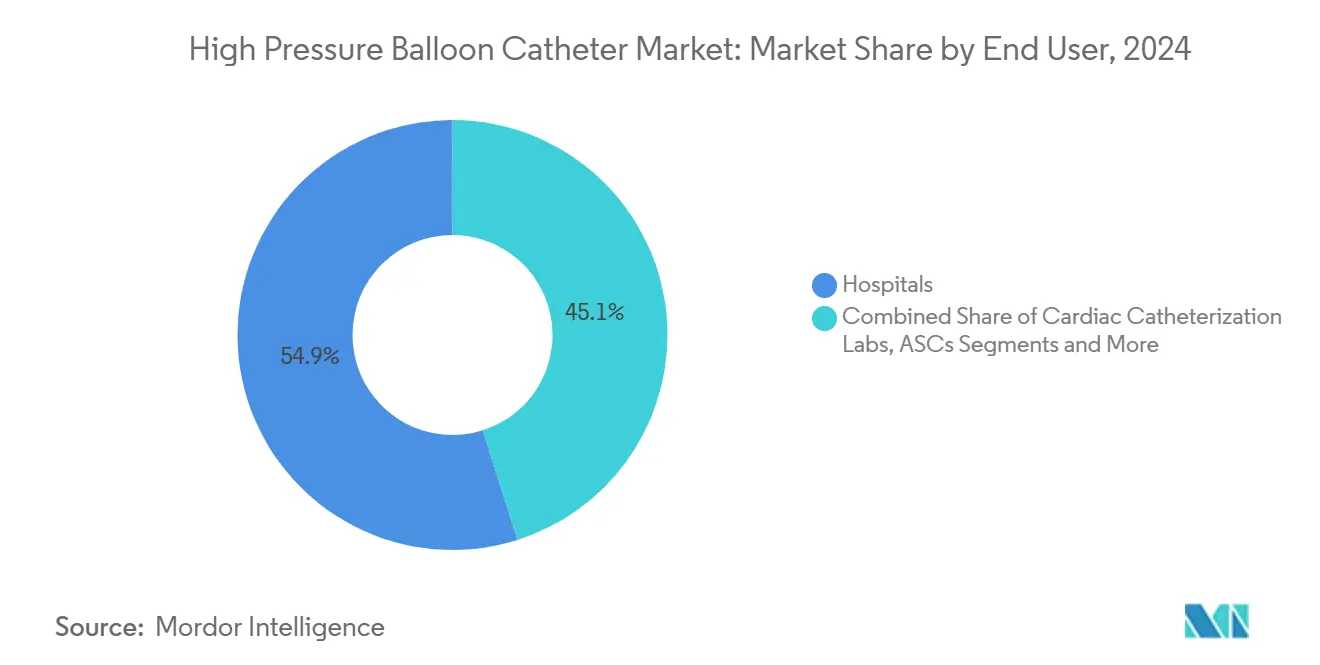

- By end user, hospitals accounted for 54.9% of demand in 2024, but ambulatory surgical centers are expected to post the highest growth at an 11.6% CAGR over the forecast period.

- By pressure range, balloons rated 20–25 atm held 38.6% of 2024 volume, while devices operating above 30 atm are set to expand at a 12.1% CAGR to 2030.

- By geography, North America generated 41.2% of 2024 revenue, yet Asia Pacific is anticipated to record the fastest regional growth at a 10.9% CAGR during 2025–2030.

Global High Pressure Balloon Catheter Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge In Complex Coronary & Peripheral Lesions Requiring Higher Burst-Pressure Balloons | +2.10% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Growing Prevalence Of Cardiovascular Disease & Obesity | +1.80% | Global, highest in middle SDI regions | Long term (≥ 4 years) |

| Rapid Adoption Of Minimally Invasive PCI & PTA Procedures | +1.50% | APAC core, spill-over to MEA | Short term (≤ 2 years) |

| Advances In Non-Compliant PET/Nylon Composites Enabling 40-Atm Balloons | +1.30% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Increased Use Of HP Balloons For Lesion Preparation Prior To Drug-Coated Balloon Therapy | +1.00% | Global | Short term (≤ 2 years) |

| Emerging Use In Structural Heart Interventions (E.G., TAVR Balloon Valvuloplasty) | +0.80% | North America & EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Complex Coronary & Peripheral Lesions Requiring Higher Burst-Pressure Balloons

Heavily calcified lesions now represent up to 38% of percutaneous coronary interventions, a rise that pushes clinicians toward plaque-modification strategies supported by balloons capable of 40 ATM inflation.[1]Proment, “Plaque Modification Techniques to Treat Calcified Coronary Lesions,” recintervcardiol.org Source: Clinical studies show that ultra-high-pressure dilation improves stent expansion and trims target-lesion revascularization by 15% compared with standard balloons, reinforcing protocol updates that prioritize adequate lesion preparation. Aging populations add complexity as older patients present multi-vessel disease patterns, increasing demand for devices delivering greater radial force. Physician training programs now incorporate ultra-high-pressure techniques, accelerating adoption curves globally. As reimbursement codes have evolved to recognize specialized balloons, hospitals report faster capital-budget approvals, tightening the link between clinical evidence and purchasing decisions.

Growing Prevalence of Cardiovascular Disease & Obesity

Ischemic heart disease caused 20.5 million deaths in 2021, and projections show more than 184 million U.S. adults will live with cardiovascular disease or stroke by 2050.[2]American Heart Association, “Forecasting the Burden of Cardiovascular Disease and Stroke in the United States Through 2050,” ahajournals.org High body mass index contributed to 1.9 million of those deaths, while hypertension grew alongside obesity, generating patient pools that often exhibit diffuse calcification requiring high-pressure dilation. Middle-income countries face the fastest rise as rapid urbanization spurs sedentary lifestyles, adding procedure volumes in settings where interventional cardiology capacity is still scaling. Clinical guidelines increasingly recommend percutaneous treatment earlier in disease progression, which encourages device utilization per encounter. Consequently, manufacturers that combine training with value-based packaging gain traction in cardiometabolic hotspots.

Rapid Adoption of Minimally Invasive PCI & PTA Procedures

Ambulatory surgery centers (ASCs) posted 11.6% annual growth in percutaneous coronary interventions and now deliver comparable safety outcomes to hospital settings. These centers favor devices that shorten procedure time, pushing demand for rapid-exchange, non-compliant balloons with predictable diameter control. Asia Pacific health investment—set to lift medtech spending to USD 140 billion in 2025—accelerates catheter sales as governments endorse local manufacturing for supply resilience. Coupled with AI-driven pre-procedure planning, operators report efficiency gains that translate into more cases per day. Pay-for-performance reimbursement further incentivizes devices that limit complications and readmissions, cementing the value proposition for high-pressure balloons that reduce restenosis rates.

Advances in Non-Compliant PET/Nylon Composites Enabling 40-ATM Balloons

Dual-layer and braided constructions deliver burst pressures exceeding 40 ATM while preserving 0.019-inch profiles for tortuous anatomy. Process refinements in extrusion and blow molding cut wall thickness without compromising strength, which helps reach distal lesions and supports post-dilation in valve replacement cases. Regulatory testing against ISO 25539 and FDA biocompatibility standards encourages material selection that balances compliance with fatigue resistance. Suppliers mitigate polymer volatility by dual-sourcing PET and Pebax grades, insulating production from price spikes. Collectively, these engineering advances widen therapeutic windows for percutaneous solutions that formerly required surgery.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter EU MDR & FDA Requirements Prolonging Approval Timelines | -1.20% | North America & EU | Medium term (2-4 years) |

| Risk Of Vessel Dissection Or Perforation At Very High Pressures | -0.80% | Global | Short term (≤ 2 years) |

| Rising Preference For Atherectomy & Lithotripsy Devices In Calcified Lesions | -1.50% | North America & EU, expanding globally | Long term (≥ 4 years) |

| Volatile Prices & Shortages Of Medical-Grade Polymers (PET, Pebax) | -0.90% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stricter EU MDR & FDA Requirements Prolonging Approval Timelines

Revised EU MDR documentation extends legacy device deadlines to 2028, adding post-market monitoring and clinical‐performance follow-up demands that lengthen time-to-market.[3]Medical Device Coordination Group, “MDCG 2021-25 Rev.1,” health.europa.eu Parallel FDA quality-system updates effective February 2026 align with ISO 13485, obliging manufacturers to upgrade validation test plans and traceability, which elevates compliance costs. Smaller firms risk pipeline delays because additional biocompatibility and durability data now run 12-18 months beyond historical norms. Early engagement with notified bodies mitigates risk but still absorbs management bandwidth that could flow to product development.

Risk of Vessel Dissection or Perforation at Very High Pressures

Inflation beyond 30 ATM boosts force but heightens injury potential, especially in small-diameter vessels. Real-world registries note dissection in 4% of ultra-high-pressure cases compared with 1.2% at standard pressures. Operators rely on intravascular imaging to size balloons conservatively, offsetting hazard but adding cost and workflow complexity. Training remains uneven, and liability concerns prompt conservative adoption in low-volume centers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Performance Gains from Advanced Polymers

The nylon segment contributed 41.8% of the high-pressure balloon catheter market share in 2024. Its puncture resistance and predictable compliance kept it the benchmark for complex coronary work. The segment will expand steadily as new cross-linking chemistries lift rated burst pressure without sacrificing trackability. PET reached USD 0.92 billion and is advancing at a 9.5% CAGR, making it the fastest-growing contributor to the high-pressure balloon catheter market size because its tensile strength permits thinner walls, which reduces crossing profiles during peripheral interventions. Composite structures that blend PET with Pebax target lesions demanding over 30 ATM, and early clinical feedback supports wider use once cost parity is achieved.

Manufacturers emphasize extrusion control, maintaining concentricity within ±0.001 inch to improve uniform expansion at high pressure. Supply chain security is central; therefore, several firms are vertically integrating polymer compounding to guard against resin shocks. Regulatory clearing processes favor well-characterized materials, giving incumbents an edge, yet start-ups focusing on nanocomposite coatings promise incremental gains in lubricity that could shorten procedure time. Sustainability agendas drive interest in recycling production scrap, lowering the total cost of ownership while aligning with hospital environmental goals.

By Application: Peripheral Procedures Accelerate

Coronary angioplasty generated 62.3% of the high-pressure balloon catheter market size in 2024, supported by dominant stent-placement workflows. Physicians value non-compliant balloons for post-dilation to ensure optimal stent expansion in heavily calcified segments. Peripheral angioplasty posted USD 0.71 billion and will grow at 10.8% CAGR through 2030, buoyed by reimbursement expansion for below-the-knee interventions that reduce amputation risk. Drug-coated balloon use in femoropopliteal arteries requires aggressive lesion prep, further bolstering ultra-high-pressure balloon volumes.

Gastroenterology and urological uses remain niche but demonstrate strong clinical success rates that encourage cross-disciplinary technology transfer. Structural heart therapies, including balloon valvuloplasty before transcatheter aortic valves, open new procedure categories and extend lifecycle revenue for cardiac portfolios. In all indications, imaging guidance such as IVUS and OCT is driving precise balloon sizing, reinforcing the value for devices with tight rated compliance ranges.

By End User: Outpatient Settings Reshape Demand

Hospitals commanded 54.9% of the high-pressure balloon catheter market revenue in 2024 because they house integrated heart programs, complex imaging, and surgical backup. Capital purchase committees typically renew balloon contracts every two years, favoring vendors that bundle pumps, wires, and support catheters. Ambulatory surgery centers handled 1.8% of PCI volume in 2024 but will post the fastest growth at 11.6% CAGR to 2030, fueled by payer pressure to migrate cases to lower-cost sites. ASCs prize balloons packaged with rapid-inflation devices to minimize turnaround times.

Cardiac catheterization laboratories inside tertiary hospitals maintain stable procedure volumes even as some elective work shifts to the outpatient setting. Academic and research centers, though smaller by volume, remain key to technology validation; they enroll patients in randomized trials that often become evidence cornerstones for guideline changes. Specialized clinics are emerging in emerging markets, filling service gaps and boosting device uptake among newly insured populations.

By Pressure Range: Ultra-High Pressure Leads Innovation

Balloons rated 20-25 ATM delivered USD 1.22 billion and held 38.6% of global revenue in 2024. The segment balances efficacy and safety for most coronary cases. Devices exceeding 30 ATM accounted for USD 0.64 billion and will grow at 12.1% CAGR because lesion complexity is rising and physician confidence in new dual-layer designs is increasing. Operators often begin with a lower-pressure balloon for predilatation before switching to an ultra-high-pressure model, which drives multi-device use per case.

The 25-30 ATM range remains a workhorse for moderately calcified lesions and drug-coated balloon prep. Lower-pressure balloons, commonly 12-18 ATM, retain importance in selecting pediatric and gastrointestinal indications where vessel fragility mandates caution. The portfolio breadth across pressure tiers enables manufacturers to take into account loyalty by meeting evolving clinical scenarios without additional vendor qualification.

Geography Analysis

North America generated USD 1.31 billion and captured 41.2% of global revenue in 2024, powered by established reimbursement, widespread intravascular imaging, and continuous physician education programs. New Current Procedural Terminology codes for complex plaque-modification support the adoption of premium balloons. Hospitals favor vendors with proven field support because inventory turnover averages two weeks, demanding reliable logistics.

Europe contributed USD 0.97 billion and benefits from stringent quality standards that accelerate trust in higher-pressure designs. Drug-coated balloon use is well entrenched, driving complementary demand for lesion-prep balloons. Funding pressures, however, encourage group purchasing, pushing suppliers to compete on bundled value rather than unit price.

Asia Pacific posted USD 0.62 billion and is growing at 10.9% CAGR as China, Japan, and India expand cath-lab density. Local manufacturing initiatives under “Buy China” and “Make in India” policies shorten lead times and trim import duties, allowing faster product refresh cycles. Training hubs in Singapore and Seoul disseminate best practices across the region, reinforcing standardized protocols that favor predictable-compliance balloons.

Latin America, the Middle East, and Africa combined for USD 0.27 billion. Brazil and Argentina spearhead South American growth with public-private investments that add cath labs in secondary cities. Gulf Cooperation Council countries prioritize cardiovascular centers of excellence that import advanced devices, but broader regional adoption remains gated by payer coverage. Across emerging markets, telehealth and mobile diagnostics identify untreated vascular disease earlier, enlarging future procedural volumes.

Competitive Landscape

Market concentration is moderate, with the top five suppliers controlling an estimated 55% of shipments. Boston Scientific, Medtronic, and Abbott leverage integrated cardiology portfolios and regulatory prowess to safeguard their share. Boston Scientific’s Athletis balloon, operating at 40 ATM, highlights proprietary braided engineering that sets a benchmark for burst pressure. Medtronic complements its stent franchises by bundling high-pressure balloons in global contracts, enhancing procedural consistency.

Cordis re-entered the space after a private equity spin-out, positioning the RAIDEN platform at 22 ATM with a value-priced offer to regain accounts. Niche manufacturers focus on ultra-high-pressure or specialty balloons for structural heart and gastrointestinal use. Strategic acquisitions are common; Abbott’s CE-marked Volt PFA system underscores the trend of broadening technology scope through inorganic moves.

Competitive differentiation leans on stronger burst pressures, lower profiles, and enhanced push ability. Companies that add intravascular imaging or AI-based sizing tools fortify ecosystem control. Regulatory mastery also matters; firms that navigate EU MDR’s clinical-evidence mandates faster can launch next-generation balloons sooner, widening the performance gap. Sustainability credentials are emerging as a tender criterion, prompting pilot programs for single-material balloons that streamline recycling without compromising clinical utility.

High Pressure Balloon Catheter Industry Leaders

Abbott Laboratories

Boston Scientific Corporation

Medtronic Plc

B. Braun Group

Terumo Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2024: Boston Scientific received FDA clearance for the AGENT drug-coated balloon, the first coronary DCB approved in the United States, after showing superiority over uncoated balloons in reducing target-lesion failure rates.

- May 2024: New technology has enabled ultra-high-pressure balloon catheters to operate at 40 ATM, a breakthrough for treating calcified and non-dilatable lesions. Boston Scientific's Athletis Ultra-High-Pressure Balloon uses a braided design to maintain its diameter under tough conditions.

- October 2024: FDA approved the Sphere-9 Catheter and Affera Ablation System, integrating a balloon tip that achieved 73.8% arrhythmia-free survival at 12 months.

Global High Pressure Balloon Catheter Market Report Scope

| Nylon |

| Polyethylene Terephthalate (PET) |

| Polyurethane |

| Pebax & Other Copolymers |

| Composite / Hybrid Polymers |

| Coronary Angioplasty |

| Peripheral Angioplasty |

| Urologic Balloon Dilatation |

| Gastroenterology (e.g., EUS access) |

| Other Emerging Uses |

| Hospitals (In-patient) |

| Cardiac Catheterization Labs |

| Ambulatory Surgical Centers |

| Specialty Clinics |

| Research & Academic Centers |

| 10-20 atm |

| 20-25 atm |

| 25-30 atm |

| >30 atm |

| Ultra-high Pressure / Non-Compliant |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Material | Nylon | |

| Polyethylene Terephthalate (PET) | ||

| Polyurethane | ||

| Pebax & Other Copolymers | ||

| Composite / Hybrid Polymers | ||

| By Application | Coronary Angioplasty | |

| Peripheral Angioplasty | ||

| Urologic Balloon Dilatation | ||

| Gastroenterology (e.g., EUS access) | ||

| Other Emerging Uses | ||

| By End User | Hospitals (In-patient) | |

| Cardiac Catheterization Labs | ||

| Ambulatory Surgical Centers | ||

| Specialty Clinics | ||

| Research & Academic Centers | ||

| By Pressure Range | 10-20 atm | |

| 20-25 atm | ||

| 25-30 atm | ||

| >30 atm | ||

| Ultra-high Pressure / Non-Compliant | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the 3D printed brain models market in 2025?

The market is valued at USD 41.2 million in 2025 and is forecast to grow at a 9.5% CAGR to USD 64.8 million by 2030.

Which material type grows fastest in neurosurgical 3D printing?

Bioprinted hydrogels expand at a 27.5% CAGR because they support functional neural network formation for research and drug testing.

Why are hospitals investing in point-of-care 3D printing suites?

FDA-cleared integrated printer-software combos let hospitals produce patient-specific models within hours, trimming operative time and qualifying for reimbursement.

What limits wider adoption of these models today?

Labor-intensive DICOM segmentation and fragmented biocompatibility standards raise costs and slow throughput.

Which company innovations should executives watch?

3D Systems FDA-cleared POC platform and Medtronic's BrainSense DBS, both developed on 3D printed brain models, signal market-shaping advances.

Page last updated on: