Deflectable Catheters Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.16 Billion |

| Market Size (2031) | USD 2.81 Billion |

| Growth Rate (2026 - 2031) | 5.38% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

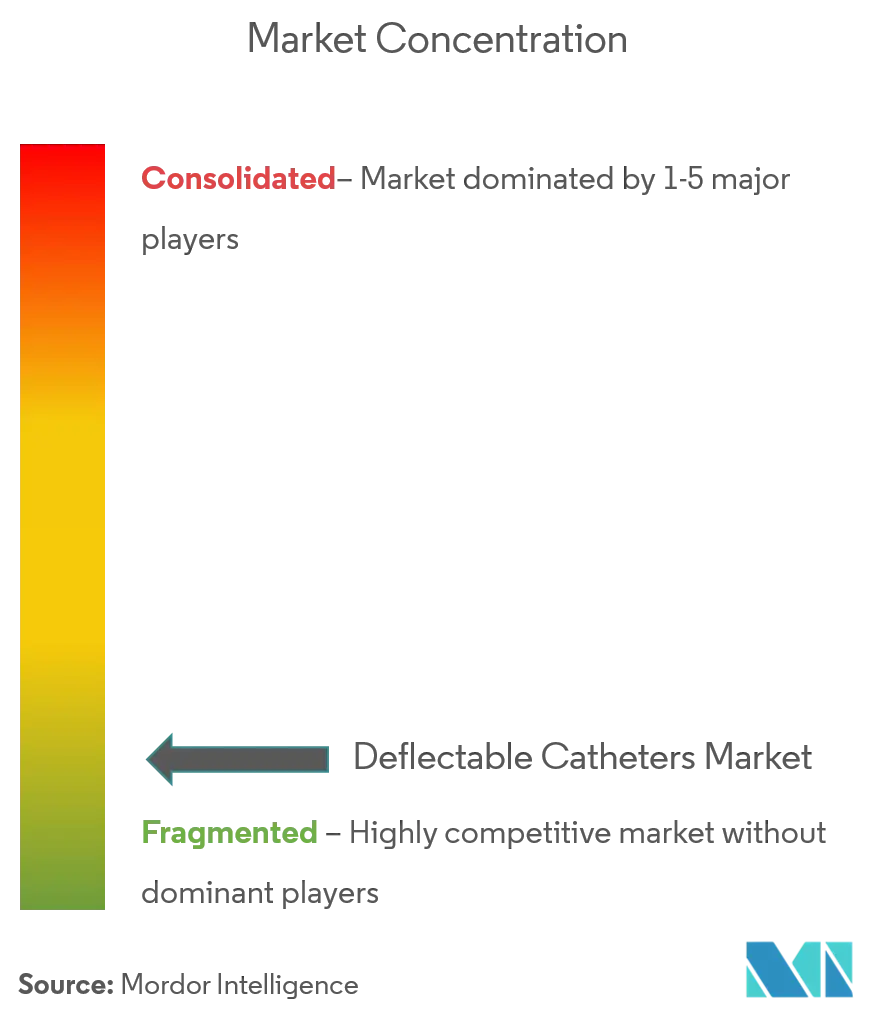

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Deflectable Catheters Market Analysis by Mordor Intelligence

Deflectable catheters market size in 2026 is estimated at USD 2.16 billion, growing from 2025 value of USD 2.05 billion with 2031 projections showing USD 2.81 billion, growing at 5.38% CAGR over 2026-2031. Demand remains rooted in electrophysiology (EP) procedures, yet growth shifts toward premium applications such as pulsed-field ablation that require superior steerability and variable stiffness profiles. Multi-directional shaft designs gain traction in complex left-atrium interventions, while Pebax-based polymers replace legacy PTFE amid supply constraints and rising biocompatibility needs. Regionally, North America leads today, but Asia-Pacific delivers the steepest volume expansion as training centers multiply and reimbursement frameworks liberalize. At the same time, nitinol wire shortages and tightening FDA/MDR evidence rules lift entry barriers, placing a premium on robust supply chains and well-resourced clinical affairs teams.

Key Report Takeaways

- By application, electrophysiology mapping and ablation accounted for 52.01% of the deflectable catheter market share in 2025, while structural heart and TAVI support is projected to expand at a 6.47% CAGR through 2031.

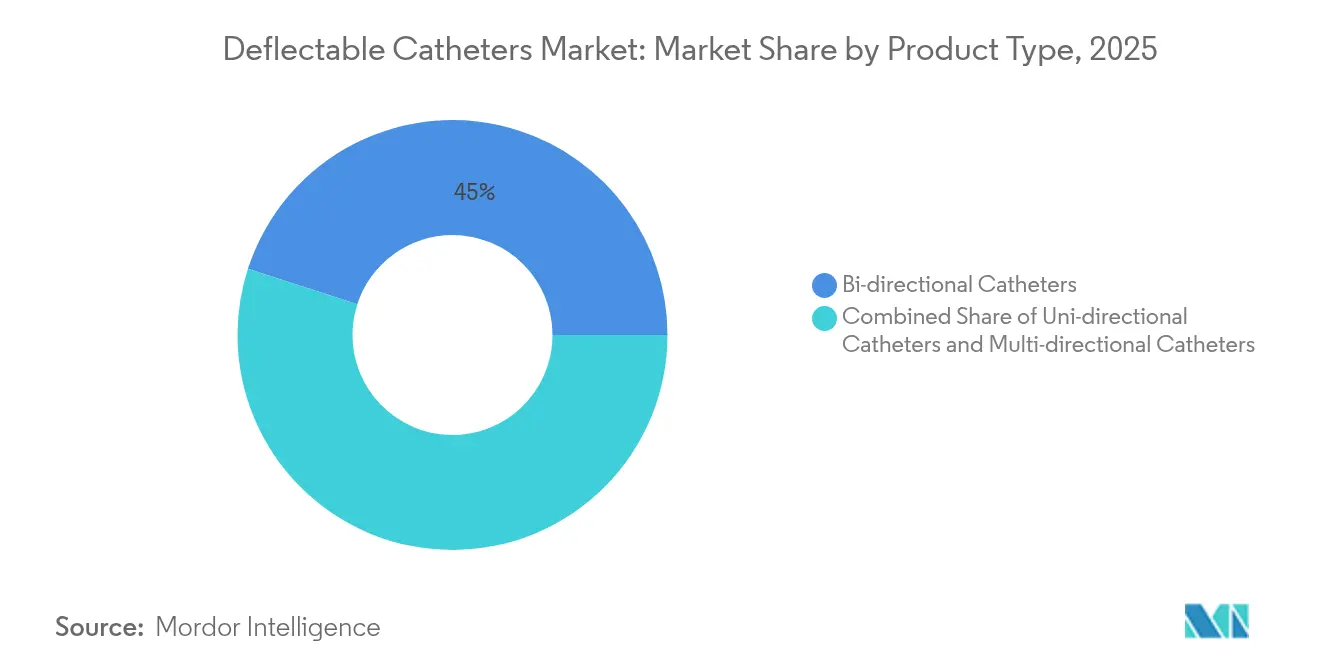

- By product type, bi-directional catheters led with 45.02% revenue share in 2025; multi-directional designs are forecast to grow at 6.08% CAGR to 2031.

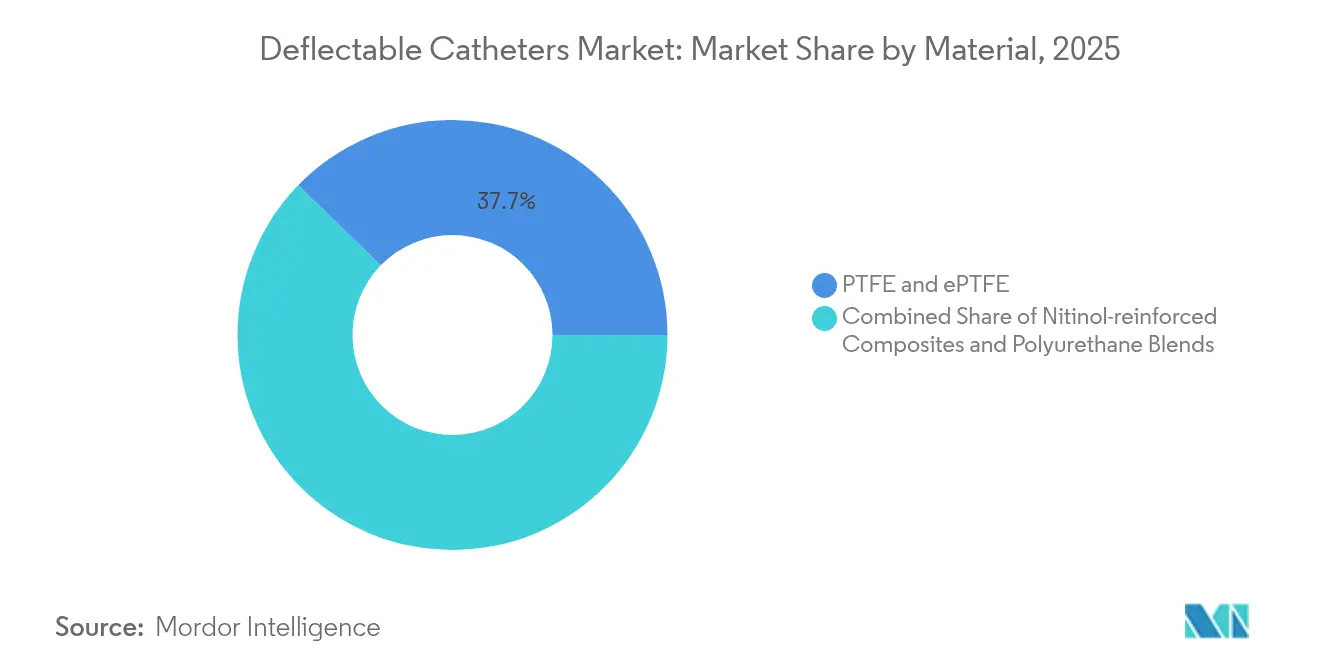

- By material, PTFE held 37.74% share of the deflectable catheter market size in 2025 and Pebax/polyurethane blends are advancing at a 6.93% CAGR through 2031.

- By end user, hospitals and cardiac centers controlled 64.68% of the deflectable catheter market size in 2025, whereas ambulatory surgery centers are set to rise at a 6.76% CAGR between 2026-2031.

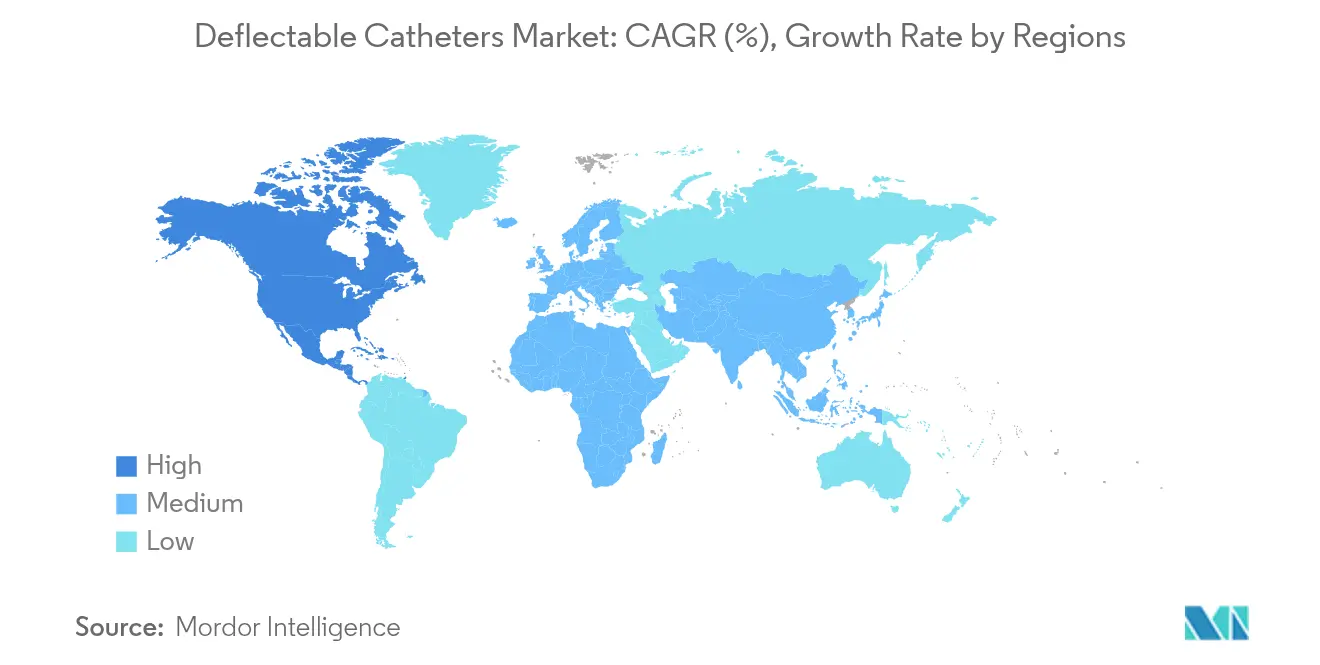

- By geography, North America captured 43.08% of the deflectable catheter market in 2025; Asia-Pacific remains the fastest-growing region at 7.26% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Deflectable Catheters Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CVD prevalence & aging population | +1.2% | Global, concentrated in North America & Europe | Long term (≥ 4 years) |

| Rising uptake of minimally-invasive EP ablation procedures | +1.8% | Global, led by North America, expanding in Asia-Pacific | Medium term (2-4 years) |

| Rapid material innovation (Pebax blends, low-profile nitinol braids) | +0.9% | Global, R&D concentrated in North America & Europe | Medium term (2-4 years) |

| Hospital cap-ex shift toward catheter-lab automation | +0.7% | North America & Europe, emerging in Asia-Pacific | Long term (≥ 4 years) |

| Pulsed-field ablation platforms require next-gen steerability | +1.1% | Global, early adoption in developed markets | Short term (≤ 2 years) |

| AI-assisted mapping catheters unlocking complex left-atrium cases | +0.6% | North America & Europe, selective Asia-Pacific centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High CVD Prevalence & Aging Population

The rising global cardiovascular burden keeps procedure volumes high, but aging anatomy introduces tortuous vasculature and calcified lesions that demand agile shaft response and refined tip control. Variable stiffness zones, segmented braid layers, and micro-marker feedback facilitate safe navigation in frail vessels, reducing fluoroscopy time and contrast use in elderly cohorts.

Rising Uptake of Minimally-Invasive EP Ablation Procedures

EP labs now perform higher case counts as single-shot technologies shorten workflow and enable day-case ablations. Ambulatory surgery centers executed 1.8% of percutaneous coronary interventions in 2024 with hospital-equivalent safety, prompting catheter makers to emphasize fast exchange transitions and durable lesion quality even in resource-light settings. Boston Scientific’s FARAPULSE platform illustrates demand for steerable delivery sheaths that align precisely and limit collateral damage [1]Boston Scientific, “Boston Scientific Reports First-Quarter 2025 Results,” bostonscientific.com.

Rapid Material Innovation (Pebax Blends, Low-Profile Nitinol Braids)

PTFE shortages in 2024 exposed the vulnerability of single-source resins, pushing OEMs toward Pebax, polyurethane, and nitinol-lined hybrids that retain pushability yet flex around sharp bends. Zeus expanded extrusion capacity by 127% to keep pace with OEM requests for thin-wall Pebax liners, signalling durable adoption of these alternative polymers.

Hospital Cap-ex Shift Toward Catheter-Lab Automation

Integrated imaging and robotic navigation suites encourage procurement teams to bundle hardware with catheter contracts, rewarding vendors that guarantee seamless interoperability. Covenant Health’s USD 1.2 million lab upgrade prioritised software-driven workflows and attracted premium steerable sheaths compatible with robotic drivers. Catheter designers now embed magnetic sensors and extend pull-wire life cycles to match automated deployment profiles.

Pulsed-Field Ablation Platforms Require Next-Gen Steerability

PFA systems demand tight tissue contact for uniform electroporation. Boston Scientific’s steerable catheters obtained regulatory approval in Japan and China, reflecting global pursuit of loop-based architectures with force sensing to reduce char formation. Device makers are reallocating R&D budgets from legacy radiofrequency shafts toward variable-loop mechanics and multi-sensor arrays.

AI-Assisted Mapping Catheters Unlocking Complex Left-Atrium Cases

The 88% arrhythmia-free survival reported in the TAILORED-AF trial validates AI-guided ablation, accelerating demand for catheters embedded with high-density electrodes and on-board processors for real-time electrogram parsing. Open-source robotic platforms such as CardioXplorer demonstrate enhanced path planning and lower wall collision forces, raising expectations for datacentric catheter designs [2]Journal of Clinical Medicine, “Catheter-Related Thrombosis in Cardiovascular Procedures,” mdpi.com.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Device-related infection & thrombus risks | -0.8% | Global, heightened scrutiny in developed markets | Short term (≤ 2 years) |

| Stringent FDA & MDR evidence requirements | -1.1% | Global, most restrictive in North America & Europe | Medium term (2-4 years) |

| Shortage of trained electrophysiologists | -0.6% | Asia-Pacific, Latin America, Middle East & Africa | Long term (≥ 4 years) |

| Tight global supply of micro-braided nitinol wire | -0.4% | Global, concentrated impact on premium segment | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Device-Related Infection & Thrombus Risks

Clinical vigilance around catheter-associated thrombosis prompts regulators to spotlight material coatings and intraprocedural anticoagulation. Direct oral agents lower systemic clot burden, yet bleeding events hike reintervention rates, nudging engineers toward heparin-bonded surfaces and smoother junction geometries. Multiple recalls in 2024 amplified hospital purchasing committees’ focus on proven safety records.

Stringent FDA & MDR Evidence Requirements Raise Time-to-Market

The FDA’s 2024 Quality System Regulation alignment with ISO 13485 and Europe’s MDR mandate full clinical investigation for even modest design tweaks, inflating R&D spend and delaying launch by 12-18 months on average. Market entrants must scale clinical affairs teams and deploy proactive surveillance to secure reimbursement and clinician trust.

Tight Global Supply of Micro-Braided Nitinol Wire

Aerospace demand and constrained melting capacity tightened supply of superelastic wire, delaying production of premium multi-directional shafts. OEMs responded by dual-sourcing and miniaturizing braid densities to preserve torque while trimming material usage, though near-term availability remains uncertain for high-complexity builds.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Multi-Directional Innovation Drives Growth

The multi-directional cohort grows at 6.08% CAGR to 2031 while bi-directional catheters preserve 45.02% leadership in the deflectable catheter market. High-angle articulation and twist-free torque transfer unlock access to posterior pulmonary veins and ventricular septal targets, boosting adoption in complex EP and TAVI support cases. Johnson & Johnson’s OMNYPULSE 12 mm tip with integrated contact-force telemetry exemplifies the pivot toward smart multi-vector navigation.

Complex ergonomics and premium sensor arrays elevate average selling prices, yet OEMs offset costs through modular platform designs that share handle assemblies across product lines. Meanwhile, uni-directional shafts cater to diagnostic flow mapping and remain viable in cost-sensitive geographies. The deflectable catheter market size for multi-directional designs is projected to expand 98 basis points in share by 2031, reflecting sustained substitution momentum.

By Application: Structural Heart Procedures Accelerate Market Evolution

Structural heart and TAVI support posts a 6.47% CAGR, dwarfing mature electrophysiology growth rates even though EP controls 52.01% of 2025 revenue. Valve‐delivery sheaths need consistent curve retention under dynamic aortic loading, motivating R&D into kink-resistant nitinol braids and low-friction liners. Clinical data confirm reduced paravalvular leak rates when steerable deflectors ensure coaxial alignment during deployment.

EP mapping and ablation retains scale thanks to expanding atrial fibrillation prevalence and guideline shifts endorsing early rhythm control. However, pricing pressure intensifies as commoditized bi-directional shafts face new entrants. Peripheral vascular and coronary support segments supply diversifying revenue, while imaging catheters sustain diagnostic throughput across all modalities.

By Material: Advanced Polymers Challenge Traditional Dominance

PTFE commanded 37.74% share in 2025 but faces substitution as Pebax and polyurethane blends grow 6.93% annually to 2031. Dual-durometer Pebax layers supply soft tip transition yet preserve push force, enabling safe septal crossings. Composite nitinol braids embedded in poly-ether block amides deliver torque fidelity at slimmer profiles, freeing space for lumen-based sensors. The deflectable catheter market share of Pebax is poised to climb by 225 basis points by 2031 amid persistent PTFE cost volatility.

Nitinol-reinforced thermoplastics anchor premium shafts in structural heart channels where radial strength and shape memory outperform stainless steel equivalents. Patent filings covering split slits and elastically deformable rails underscore continued material experimentation targeting steerability without sacrificing kink resistance.

By End User: ASC Adoption Reshapes Market Dynamics

Hospitals and cardiac centers still capture 64.68% of the deflectable catheter market size, yet ambulatory surgery centers record a brisk 6.76% CAGR through 2031. ASC administrators prioritize disposable-only inventory, streamlined kit packaging, and rapid room turnaround, prompting manufacturers to bundle pre-shaped sheaths with diagnostic mapping and ablation catheters. Clinical registries report non-inferior 30-day major adverse cardiac event rates between ASC and hospital settings, reinforcing the shift toward outpatient care.

For large academic centers, robotics and AI mapping drive incremental demand for high-value multi-sensor shafts, while community hospitals gravitate toward cost-controlled bi-directional models. Vendors tailor go-to-market strategies accordingly, offering tiered product families that share core handle ergonomics yet differ in articulation range and sensor density.

Geography Analysis

North America held 43.08% of 2025 revenue as mature reimbursement pathways and high EP penetration support steady replacement cycles for legacy shafts. Provider consolidation fosters bulk purchasing, favoring suppliers with integrated platforms covering mapping, ablation, and imaging.

Asia-Pacific delivers the fastest 7.26% CAGR as public-private partnerships build EP labs and governments expand insurance coverage for catheter-based procedures. Samsung Medical Center operates the region’s first ventricular arrhythmia training hub, performing more than 100 complex cases each year with 85% success, catalyzing regional skill transfer. China’s NMPA has streamlined device approvals, spurring joint ventures between multinationals and local OEMs to co-produce Pebax shafts close to demand centers. Europe demonstrates measured expansion fueled by guideline-driven adoption and MDR-driven quality upgrades. National health systems balance cost with outcome data, giving incremental advantage to products with strong real-world evidence. The European Heart Rhythm Association’s accredited sites anchor clinician training and promote uniform practice standards . In South America and the Middle East & Africa, deflectable catheter uptake trails infrastructure build-outs, though urban cardiac hubs increasingly solicit turnkey EP suites from global vendors.

Regulatory Landscape

In the United States, deflectable catheters used for cardiovascular applications are commonly regulated as Class II devices under FDA medical device rules and typically reach market via the 510(k) pathway (often under 21 CFR 870.1250, product code DQY). Review predictability is shaped by MDUFA V performance goals for FY 2023-2027, while the FDA Quality Management System Regulation (QMSR) took effect on February 2, 2026, aligning quality system expectations more closely with ISO 13485 and increasing the emphasis on design controls, risk management, and postmarket feedback loops for steerable catheter iterations.

In Europe, devices fall under the EU MDR (Regulation (EU) 2017/745), where clinical evaluation (Article 61), post-market surveillance, and constrained equivalence pathways tighten evidence requirements for design changes. In June 2026, Commission Delegated Regulation (EU) 2026/1359 and 2026/1451 were published, expanding exemptions for certain well-established technologies, including specific cannulas and catheters, from elements of notified body technical documentation assessment and mandatory clinical investigations. This provides a compliance lever for legacy catheter lines while keeping postmarket vigilance and surveillance obligations in place.

Value Chain Analysis

The value chain starts with specialized raw materials and subcomponents, including medical-grade polymers (PTFE/ePTFE and newer Pebax or polyurethane blends) and metallic reinforcements such as stainless steel and nitinol used in pull-wires and braid structures. Upstream constraints center on medical-grade nitinol melt and conversion capacity, which can tighten availability for premium multi-directional shafts. As a result, OEMs and contract manufacturers often dual-source or redesign braid densities to protect torque response while reducing material intensity.

Midstream manufacturing combines extrusion (often multilumen liners), braiding or coil winding, handle and deflection assembly, bonding and tip forming, and sterilization and packaging. A meaningful share of this activity is executed by specialized contract manufacturers and component suppliers. Platform-based development, such as Freudenberg Medicals Composer-style modular assemblies, supports shorter development cycles by reusing validated deflection and handle architectures across multiple catheter programs. Downstream, distribution runs through direct sales and hospital or cardiac-center purchasing groups, and it is increasingly tied to procedure ecosystems in electrophysiology and structural heart, where interoperability with mapping, ablation, and access toolkits supports pull-through and repeat purchasing.

Competitive Landscape

Competitive intensity remains moderate. Abbott, Medtronic, Boston Scientific, and Johnson & Johnson’s Biosense Webster division rely on end-to-end ecosystems that lock in catheter pull-through via proprietary mapping consoles and ablation generators. Boston Scientific’s acquisition pipeline continues to emphasize disruptive PFA and imaging assets to extend its platform reach.

Product-safety vigilance shapes perception after Johnson & Johnson initiated a Class 1 recall of 497 VARIPULSE catheters on neurovascular injury reports in 2024 FDA. Incidents highlight the need for robust post-market surveillance and have spurred customer audits of vendor quality systems. Meanwhile, material shortages forced OEMs to invest in dual-source nitinol annealing and Pebax compounding, insulating leaders from future supply shocks.

Patent filings climb in steerable handle mechanics, tri-segment shaft braids, and lumen-integrated micro-sensors, indicating intensifying R&D. Cross-industry collaborations emerge as AI start-ups license mapping algorithms to legacy catheter firms. Success will hinge on integrating data analytics, robotics, and material science into cohesive procedural toolkits that reduce operator variability and compress case duration.

Deflectable Catheters Industry Leaders

Abbott

Boston Scientific Corporation

Medtronic

Teleflex Incorporated

Johnson & Johnson

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Product differentiation is increasingly tied to next-generation steerability for electrophysiology workflows, especially as pulsed-field ablation adoption raises expectations for precise tissue contact, repeatable loop geometry, and variable stiffness profiles. The commercial signal is visible in dual-energy and PFA-adjacent catheter introductions and approvals by major platforms, and the shift away from single-material designs after the 2024 PTFE supply disruption has accelerated interest in Pebax or polyurethane blends and thin-wall liners.

White space is also extending beyond traditional EP into adjacent interventions that rely on active steering. This includes neurovascular and peripheral navigation, where acute vessel selection can be a limiting step for passive catheters. Peer-reviewed work published during 2025 to January 2026 reports performance gains for actively deflectable microcatheters and steerable guidewire systems in complex anatomy. It also describes research on microrobotic or magnetically controlled stiffness-tuning concepts, which suggests a pathway to retrofit-like capability upgrades using existing catheter form factors. Together, these trends point to opportunities for suppliers that can pair reliable pull-wire mechanics with lower-friction polymer systems and add sensing or software-defined control without materially increasing profile or compromising thrombosis and infection risk management.

Recent Industry Developments

- July 2026: Johnson & Johnson announced FDA approval of the Dual Energy THERMOCOOL SMARTTOUCH SF Platform, combining radiofrequency and pulsed field energy in a catheter ablation solution. The approval expands options for electrophysiology labs standardizing on platform-based workflows, and it increases competitive pressure for steerable catheter portfolios that can support dual-energy procedural strategies.

- April 2026: Johnson & Johnson entered a definitive agreement to acquire Atraverse Medical, a developer of RF guidewire systems for left-heart access used in atrial fibrillation procedures, and the acquisition was completed in Q2 2026. The deal strengthens the companys access and navigation toolkit around transseptal and left-heart workflows, supporting tighter integration between access, mapping, and ablation steps.

- June 2024: Abbott Medical received FDA 510(k) clearance (K241370) for the Agilis NxT Steerable Introducer Dual-Reach. The clearance supports continued lifecycle refresh of steerable access and introducer offerings used in complex cardiac procedures, helping vendors defend share where hospitals prioritize proven safety and familiar handling characteristics.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as revenues generated from steerable, deflectable medical catheters that can actively bend at the distal tip and are used to reach target anatomy during minimally invasive diagnostic or therapeutic procedures.

Scope exclusions: We exclude guide sheaths, non-steerable drainage catheters, and small disposable accessories such as introducers.

Segmentation Overview

- By Product Type

- Uni-directional Catheters

- Bi-directional Catheters

- Multi-directional Catheters

- By Application

- Coronary Interventions

- Electrophysiology (EP) Mapping & Ablation

- Diagnostic Imaging

- Peripheral Interventions

- Structural Heart & TAVI Support

- By Material

- Pebax / Polyurethane Blends

- PTFE & ePTFE

- Nitinol-reinforced Composites

- By End User

- Hospitals & Cardiac Centers

- Ambulatory Surgery Centers

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to map the demand pool and keep assumptions tied to real procedure activity and device adoption patterns. We typically refer to public health statistics and clinical activity sources such as the US CDC, OECD Health Statistics, the World Bank, and WHO indicators to understand disease burden, aging trends, and care access that drive procedure volumes.

On the supply and regulatory side, inputs were cross-checked using sources such as the US FDA device databases and safety communications, European Commission medical device framework pages, and peer-reviewed journals indexed on PubMed for usage trends across electrophysiology and other catheter-based interventions. We also reviewed company filings and investor presentations to confirm product positioning and revenue exposure, and we used a paid subscription for company financials and intelligence, plus a patent database, to validate product cycles and innovation intensity. These examples are not exhaustive, and other public sources were also consulted to collect data, validate numbers, and clarify open questions.

Primary Interviews and Surveys

Primary work focused on confirming how deflectable catheters are used in practice, the frequency of selection versus non-deflectable alternatives, and how pricing behaves across regions and care settings. We spoke with a mix of manufacturers, distributors, and clinical stakeholders such as lab managers and procurement teams, and feedback was balanced across APAC, EMEA, and the Americas to avoid over-weighting a single reimbursement or practice environment.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 17% | APAC: 44% |

| Mid tier: 54% | Functional/Unit leaders: 28% | EMEA: 36% |

| Smaller Players: 17% | Managers: 55% | Americas: 20% |

Market-Sizing & Forecasting

Sizing was built using a top-down demand reconstruction, where procedure volumes and treated patient pools are translated into catheter usage, and then converted into value using regional average selling prices. To keep the model practical, it relies on repeatable inputs such as electrophysiology procedure counts, the share of cases needing steerability, average catheters used per procedure, replacement and single-use patterns, and hospital versus ambulatory adoption splits.

After the top-down totals were built, selective bottom-up checks were run to pressure-test outcomes, including sampled supplier revenue ranges, channel discussions on unit throughput, and ASP banding by product capability (uni-directional versus multi-directional) where data was available. When direct unit signals were missing for smaller countries, gap handling was done through proxying from similar procedure intensity markets and adjusting for access, reimbursement maturity, and the pace of lab capacity additions.

For forecasting, we used scenario analysis supported by expert views on EP lab expansion, minimally invasive procedure growth, technology refresh cycles, and expected pricing movement. Assumptions were kept consistent year to year, and any change in a driver was applied deliberately so the trend remains explainable on a client call.

Data Validation & Update Cycle

Validation was done through multiple checks so the final totals do not rely on a single data stream. We compared model outputs against independent signals such as procedure growth trends, regulatory activity patterns, and the plausibility of implied unit demand versus installed lab capacity, and then reviewed outliers before sign-off.

When a variance looked material, respondents were re-contacted to confirm whether the gap was caused by scope, timing, or a real market shift. Reports are refreshed annually, and interim updates are made when major events can move demand or pricing. Before delivery, an analyst performs a fresh pass on key inputs so clients receive the most current view available at that time.

Mordor Intelligence's Deflectable Catheters Market Size Versus Other Published Estimates

Published market sizes for deflectable catheters often do not match because each publisher makes different calls on what products count, how pricing is treated, and which year is used as the starting point. Even when the same currency is used, the spread can widen due to differences in procedure assumptions and how quickly adoption is expected to move.

Some estimates group in adjacent products and procedure accessories, which tends to lift the total market value. In Mordor Intelligence, the value is limited to factory-gate revenue for steerable deflectable catheters (including those sold loose or bundled), and it leaves out guide sheaths and small disposable accessories such as introducers, which keeps the estimate closer to catheter-only demand signals.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.16 B (2026) | |

| Global Consultancy A | USD 2.18 B (2026) | Uses a different forecast window and growth profile, which can shift the implied 2026 value through back-calculation, and scope language does not clearly state whether accessory items or non-deflectable catheter families are excluded. |

| Industry Research Group B | USD 2.01 B (2024) | Anchors the size two years earlier and may apply conservative adoption and pricing assumptions across regions, and the segmentation includes materials and broader intervention categories that can change what gets counted as a deflectable catheter. |

Looking across the three figures, the gap is mainly explained by timing and what is included around the catheter itself, not by a disagreement that the core demand is growing. By keeping inputs traceable to procedure volumes, utilization, and realistic ASP bands, we can explain each step and adjust assumptions without rewriting the whole model.

Key Questions Answered in the Report

What is the current Deflectable Catheters Market size?

The deflectable catheter market reached USD 2.16 billion in 2026 and is forecast to grow to USD 2.81 billion by 2031 at a 5.38% CAGR.

Who are the key players in Deflectable Catheters Market?

Abbott, Boston Scientific Corporation, Medtronic, Teleflex Incorporated and Johnson & Johnson are the major companies operating in the Deflectable Catheters Market.

Which application segment is expanding the fastest?

Structural heart and TAVI support is the fastest-growing application, projected to register a 6.47% CAGR through 2031 as indications widen to lower-risk patient groups.

Which region has the biggest share in Deflectable Catheters Market?

In 2025, the North America accounts for the largest market share in Deflectable Catheters Market.

Why are Pebax and polyurethane materials gaining share?

Pebax blends combine flexibility and pushability while avoiding the PTFE supply bottlenecks that disrupted production in 2024, driving their 6.93% CAGR to 2031.

Page last updated on: