Pericardiocentesis Procedures Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.14 Billion |

| Market Size (2031) | USD 1.5 Billion |

| Growth Rate (2026 - 2031) | 5.63% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pericardiocentesis Procedures Market Analysis by Mordor Intelligence

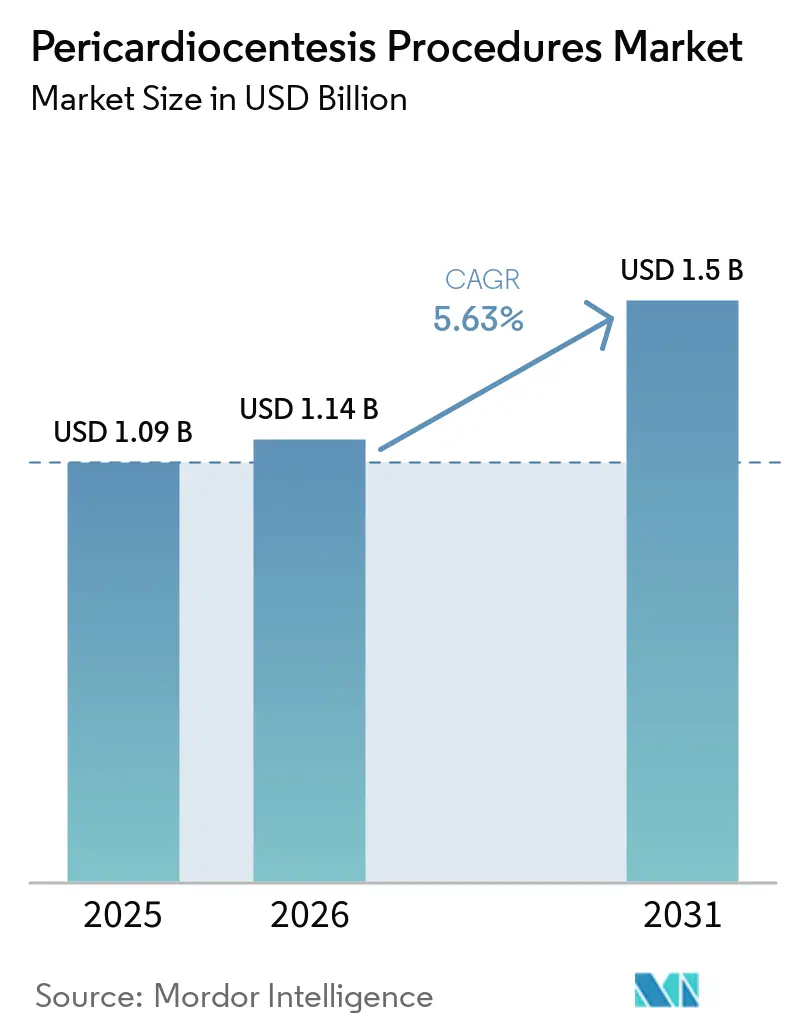

The Pericardiocentesis Procedures Market size was valued at USD 1.09 billion in 2025 and is estimated to grow from USD 1.14 billion in 2026 to reach USD 1.5 billion by 2031, at a CAGR of 5.63% during the forecast period (2026-2031).

The pericardiocentesis procedures market is expanding because older populations are living longer with cardiovascular disease, renal failure, autoimmune disorders, and cancer, all of which raise the likelihood of clinically significant pericardial effusion that needs drainage. Real-time echocardiographic guidance has become deeply embedded in clinical practice, which has improved procedural safety, reduced dependence on blind access, and widened the pool of patients who can be treated with more confidence across hospitals and critical care settings. The pericardiocentesis procedures market is also benefiting from broader use cases, because drainage is now being used not only for life-threatening tamponade but also for recurrent, malignancy-associated, and elective effusion management in cardio-oncology and inflammatory care pathways. The market still operates through two distinct economic layers, with kits and catheters behaving like standardized consumables while imaging systems remain more differentiated and more closely tied to workflow control. Competitive direction in the pericardiocentesis procedures market therefore depends on reimbursement rules, operator training, short-stay migration, and hospital procurement choices just as much as on underlying disease burden.

Key Report Takeaways

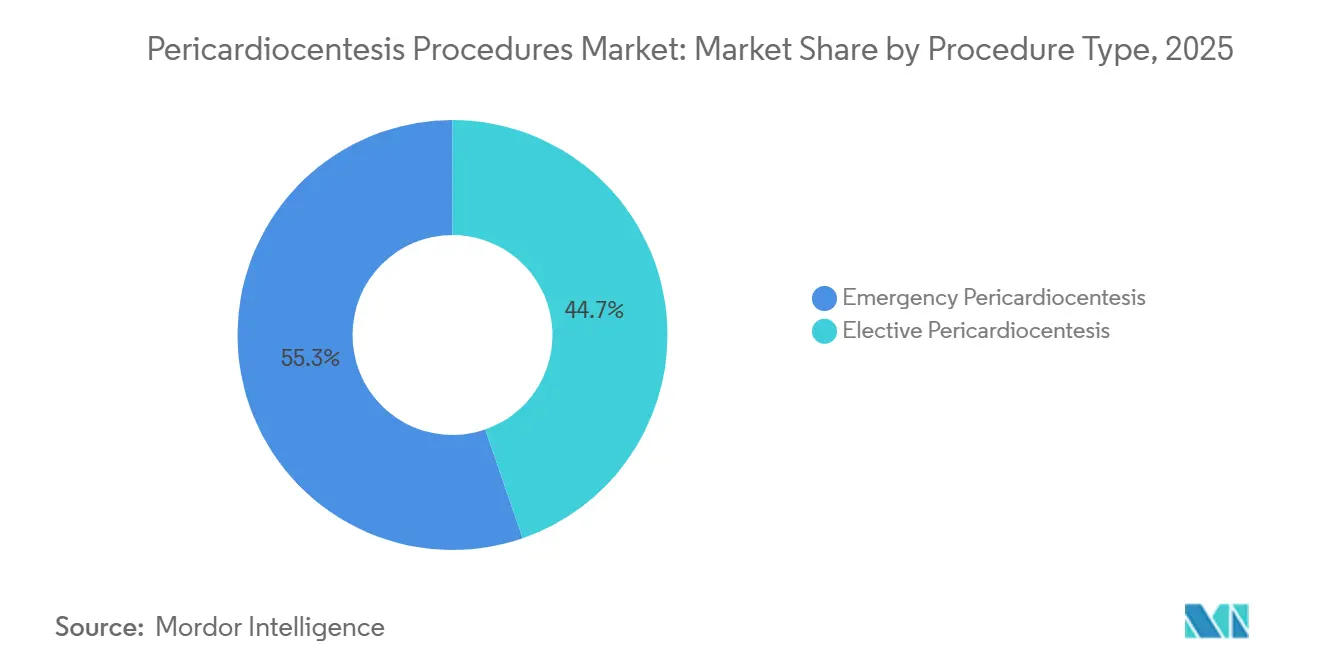

- By procedure type, emergency pericardiocentesis held 55.32% of the pericardiocentesis procedures market share in 2025, while elective pericardiocentesis is forecast to expand at a 7.14% CAGR through 2031.

- By application, cardiac tamponade accounted for 46.82% share of the pericardiocentesis procedures market size in 2025, while pericardial effusion is advancing at a 6.32% CAGR through 2031.

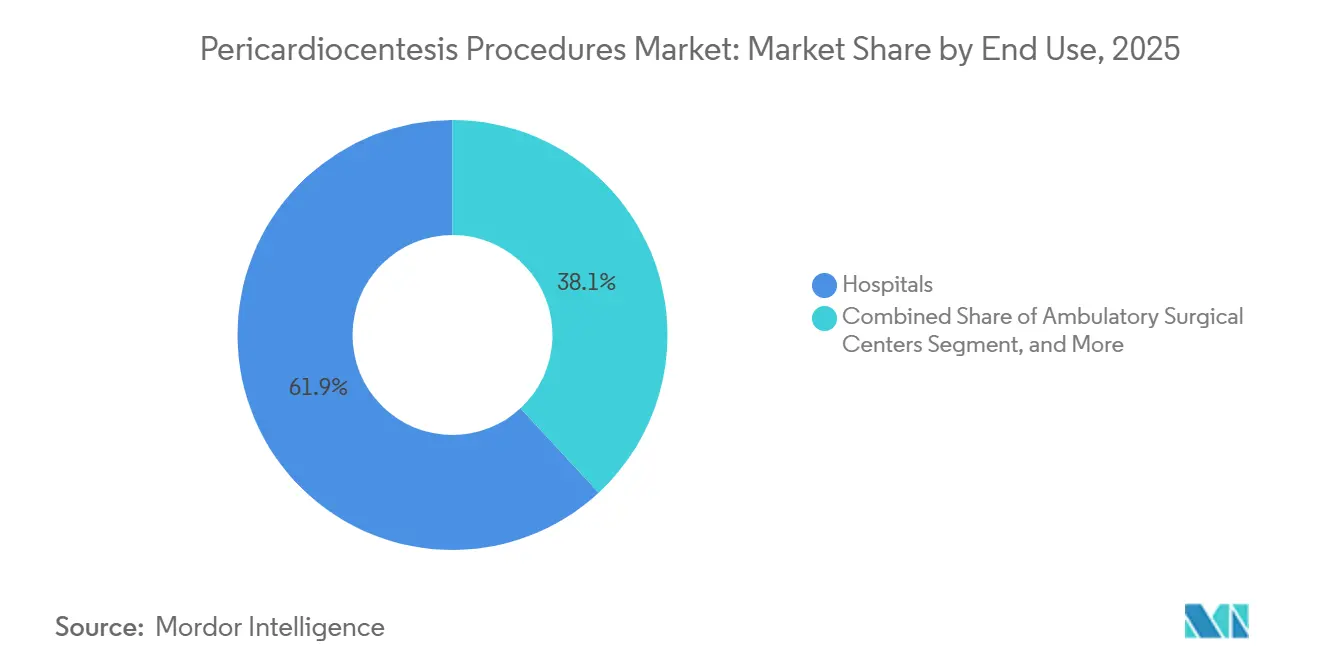

- By end use, hospitals accounted for 61.87% of share of the pericardiocentesis procedures market size in 2025, while ambulatory surgical centers recorded the highest projected CAGR at 7.68% through 2031.

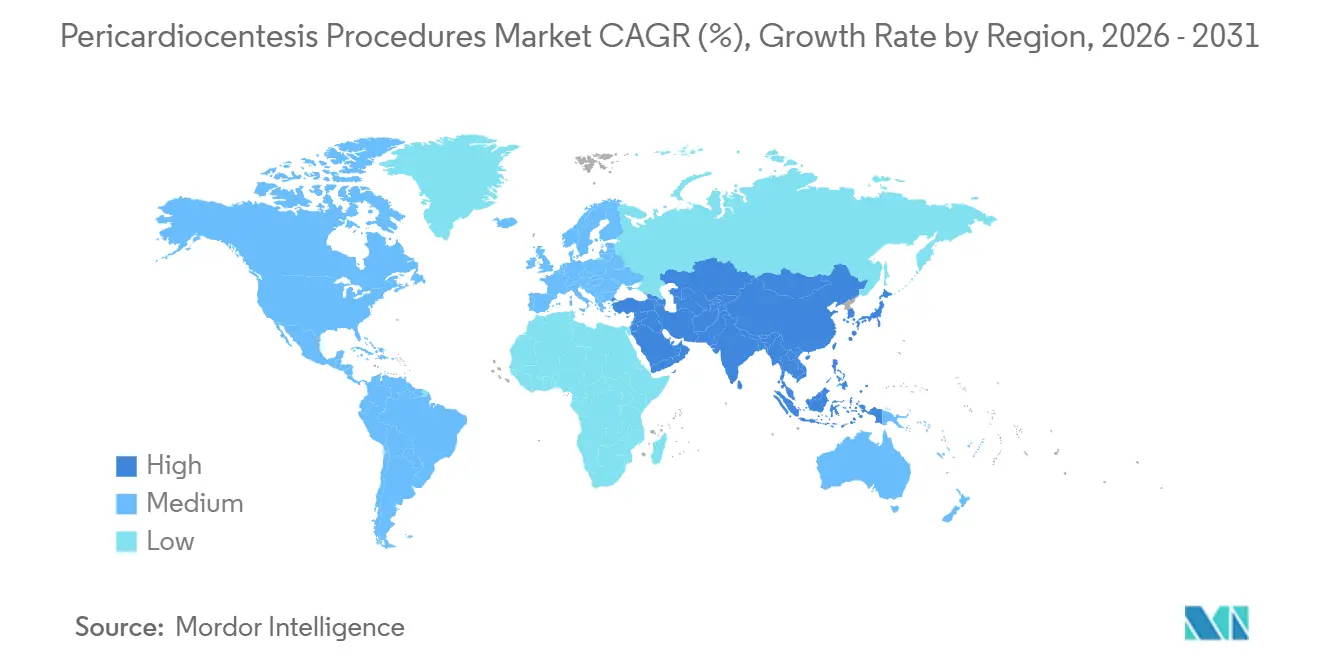

- By geography, North America held 37.23% share in 2025, while Asia-Pacific recorded the fastest projected CAGR at 6.03% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Pericardiocentesis Procedures Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Pericardial Effusion And Cardiac Tamponade Burden | +2.0% | Global, strongest in North America, Europe, and Asia-Pacific | Long term (≥ 4 years) |

| Broader Use Of Echocardiography-Guided Bedside Drainage | +1.2% | North America and Europe as early adopters, Asia-Pacific expanding rapidly | Medium term (2-4 years) |

| Oncology-Linked Procedural Demand From Malignant Effusions | +0.8% | Global, especially the United States, the European Union, Japan, and South Korea | Medium term (2-4 years) |

| Day-Case And Short-Stay Workflow Shift In Cardiac Centers | +0.6% | North America leading, early gains in Europe and Australia | Medium term (2-4 years) |

| Expansion Of Point-Of-Care Ultrasound In Emergency Pathways | +0.7% | Global, especially high-volume emergency departments in Asia-Pacific and the Middle East and Africa | Short term (≤ 2 years) |

| Standardization Of Pericardiocentesis Kits And Protocols | +0.5% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Pericardial Effusion and Cardiac Tamponade Burden

The pericardiocentesis procedures market is absorbing more case volume as older patients live longer with renal failure, autoimmune disease, systemic sclerosis, malignancy, and other conditions that can lead to clinically significant pericardial effusion. A 2024 retrospective study at a Japanese cardiovascular hospital found pericardial effusion in 0.4% of patients undergoing echocardiography, and malignancy plus idiopathic causes each represented close to one-third of drainage-requiring cases. The same study reported elevated all-cause mortality and cardiovascular event rates during follow-up, which supports closer monitoring and timely drainage in higher-risk patients. Under-treatment is also visible in pulmonary hypertension, where patients underwent pericardiocentesis less often than patients without pulmonary hypertension, despite a mortality benefit, leaving a meaningful pool of delayed or unrealized procedures inside the pericardiocentesis procedures market. A 4-year Middle Eastern retrospective also showed that tuberculosis, malignancy, and post-interventional causes all contribute to regional demand, which means procedure growth is being driven through different clinical pathways rather than a single disease pattern.[1]Heart Views Editorial Team, “Characteristics of Significant Pericardial Effusion and Outcomes of Pericardiocentesis, A 4-Year Retrospective Data Review,” Heart Views, journals.lww.com

Oncology-Linked Procedural Demand From Malignant Effusions

The pericardiocentesis procedures market is being reshaped by the growing overlap between oncology and cardiology, where malignant effusions and immune-related complications are creating recurring procedural demand. A 2024 systematic review in Cardio-Oncology found that 68% of patients with immune checkpoint inhibitor associated pericardial disease required pericardiocentesis and 41% experienced cardiac tamponade, with nivolumab and pembrolizumab most often involved and lung cancer the leading underlying malignancy.[2]Marta Palaskas et al., “Immune Checkpoint Inhibitors and Pericardial Disease, A Systematic Review,” Cardio-Oncology, link.springer.com A 2025 disproportionality analysis of the FAERS database showed a sustained rise in reports of drug-induced pericardial effusion from 2012 onward, with immune checkpoint inhibitor signals taking a growing share of total reports. Recurrence is a major reason this driver matters so much because a 2025 review noted that close to 50% of patients who discontinued immune checkpoint inhibitor therapy and underwent initial pericardiocentesis later developed recurrent effusion, turning one episode into a multi-procedure care path. A 2025 Turkish retrospective further reinforced this pattern by identifying malignancy as the most common cause of drainage-requiring effusions at 34.6%, while also linking malignant etiology, tamponade, and low serum albumin to worse outcomes that now influence triage at oncology-cardiac centers.[3]Advances in Interventional Cardiology Editorial Team, “Etiologies, Fluid Characteristics, and Outcomes of Pericardiocentesis, A Five-Year Retrospective Study From a Single Center,” Advances in Interventional Cardiology, termedia.pl

Broader Use of Echocardiography-Guided Bedside Drainage

The pericardiocentesis procedures market has moved decisively toward echocardiography-guided drainage, and this shift is widening access beyond catheterization suites into intensive care units and emergency departments. A 199-procedure retrospective analysis published in 2025 reported that imaging guidance was used in 89.6% of cases, with echo-guided or echo-assisted methods accounting for 77.4% of all procedures, while overall success reached 98.5%, and the major complication rate was just 0.5%. A 2025 cohort study in post-cardiac surgery patients found that only 5.56% of cases managed with bedside pericardiocentesis by cardiothoracic ICU physicians later required operative drainage, which supports broader use outside specialist lab settings. As echo-guided bedside drainage becomes more routine, the pericardiocentesis procedures market is seeing procedure volume spread across more care sites, while demand for portable imaging and training support becomes more important. This same decentralization also reduces the hold of traditional referral pathways, because critical care teams can intervene earlier in patients who previously would have waited for transfer or formal laboratory scheduling.

Day-Case and Short-Stay Workflow Shift in Cardiac Centers

The pericardiocentesis procedures market is also being influenced by the steady migration of selected cardiac procedures into shorter-stay and outpatient settings. CMS stated in the 2025 OPPS and ASC final rule that 234 Medicare-certified ambulatory surgical centers offered cardiovascular services, and CMS projected that 33% of cardiology procedures would shift to ASC settings by the end of 2025 as covered procedure pathways continue to expand. A 2025 Medicare analysis of electrophysiology device implants found that ASC-based procedures carried significantly lower costs than hospital outpatient departments, which helps explain why payers and providers continue to examine elective drainage in similar settings. Capital equipment needs, staffing requirements, and certificate-of-need rules still slow the transition, especially where on-site echo and surgical backup remain limited. Even so, the shift toward day-case cardiology care is structurally intact, and it is gradually opening a larger scheduling window for elective effusion drainage inside the pericardiocentesis procedures market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Procedural Complication Risk And Low-Volume Operator Variability | -0.8% | Global, more pronounced in emerging markets with fewer specialist centers | Long term (≥ 4 years) |

| Reimbursement Friction Across Emergency And Inpatient Settings | -0.6% | North America and Europe | Medium term (2-4 years) |

| Dependence On Skilled Imaging And Drainage Support Teams | -0.5% | Core Asia-Pacific markets, with spillover into the Middle East and Africa | Medium term (2-4 years) |

| Sterile Consumable Supply Volatility And Kit Availability Constraints | -0.4% | Global, especially high-dependency markets in South America and the Middle East and Africa | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Procedural Complication Risk and Low-Volume Operator Variability

The pericardiocentesis procedures market still faces a clear limit from operator experience, because safety and confidence remain closely tied to case volume and training quality. The 2025 IRCCS San Gerardo study showed that nearly one-quarter of historical subxiphoid procedures were performed blindly and recommended discontinuing routine blind access because guided techniques performed better. A 2026 multidimensional CUSUM analysis found that a novice operator reached procedural competency only after close to 14 cases, with the first 14 cases taking a median 12.7 minutes compared with 7.9 minutes after that threshold. That learning curve concentrates early risk in low-volume hospitals and helps explain why complex effusion management keeps consolidating into larger referral centers across the pericardiocentesis procedures market. Simulation-based mitigation is advancing, but it remains a support measure rather than a full replacement for repeated live procedural exposure.

Reimbursement Friction Across Emergency and Inpatient Settings

The pericardiocentesis procedures market also faces uneven reimbursement because emergency and elective drainage can fall into different coding and payment environments depending on the site of care. The American College of Cardiology noted that the 2025 OPPS final rule raised outpatient department payment by only 2.9%, which remains below the cost pressure many catheter-enabled drainage programs face in higher-acuity settings. Emergency procedures performed during inpatient care are commonly absorbed into MS-DRG weighted payments, while outpatient and ASC cases depend more directly on CPT and APC assignment, which are reviewed annually and can change planning assumptions. This difference makes hospitals more selective when they consider building dedicated elective drainage pathways, especially when case volumes are still emerging. Across Europe, the same issue appears in another form, because some systems support more itemized coding for diagnostic and therapeutic drainage, while others keep broader reimbursement structures that provide less direct procedural visibility.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Procedure Type: Emergency Volume Dominates, Elective Pipeline Accelerates

Emergency pericardiocentesis represented 55.32% of procedure volume in 2025, which kept the largest share of the pericardiocentesis procedures market inside urgent drainage pathways. That position reflects the clinical reality that tamponade can deteriorate quickly into shock and arrhythmia when drainage is delayed. A 13-year single-center registry covering 66,812 invasive cardiac procedures reported an overall tamponade incidence of 0.176%, with rates reaching 1.42% in left atrial appendage closure, which supports a steady baseline of unplanned drainage demand. Elective pericardiocentesis is projected to grow at a 7.14% CAGR through 2031 as clinicians intervene earlier in moderate malignant and inflammatory effusions for diagnosis, symptom relief, and prevention of tamponade progression.

Guidance choice is becoming just as important as timing inside the Pericardiocentesis procedures industry, because imaging has changed who can perform the procedure and where it can be performed. Echo-guided or echo-assisted methods accounted for 77.4% of procedures in the 199-case Italian cohort, which confirms that echocardiography has become the practical standard for most routine cases. This guidance model supports portability, real-time visualization, and freedom from radiation exposure, which gives it a clear advantage in critical care and bedside settings. Fluoroscopy-guided drainage still matters in catheterization laboratories and in anterior or loculated effusions where echocardiographic windows are weak, and a 2025 Turkish retrospective documented fluoroscopy-guided subxiphoid procedures across 127 cases with mostly malignant and idiopathic etiologies. CT-guided access remains a smaller niche for post-surgical or anatomically difficult effusions, which means the pericardiocentesis procedures market continues to support a layered guidance mix rather than a single universal approach.

By Application: Tamponade Anchors Demand While Effusion Management Broadens Scope

Cardiac tamponade accounted for 46.82% of the pericardiocentesis procedures market size in 2025, which kept it as the largest application because hemodynamic compromise still demands immediate drainage. At the same time, pericardial effusion is the fastest-growing application and is expected to advance at a 6.32% CAGR through 2031 as more moderate cases are identified earlier on echocardiography. A 2025 study in the Journal of the American Heart Association found that pericardial effusion carries independent prognostic value in the general population even below tamponade thresholds, which supports earlier intervention in selected patients. The pericardiocentesis procedures market is therefore broadening beyond rescue care and moving further into planned symptom management and diagnostic drainage.

The oncology effect cuts across all three application groups, because immune checkpoint inhibitor-associated disease can appear as pericarditis, progressive effusion, or acute tamponade. A 2026 JAHA analysis using the TriNetX database found that immune checkpoint inhibitor-associated pericarditis had materially higher tamponade and recurrence rates than non-immune checkpoint inhibitor cohorts at both 90-day and 1-year follow-up. That pattern raises repeat procedure demand and makes follow-up planning more important in cancer centers. Pericarditis remains a smaller segment, but it stays clinically meaningful because it can progress, recur, or sit alongside malignant effusion in higher-risk patients. National treatment rules also matter, and French oncology guidance limits pericardiocentesis in lung cancer to tamponade-presenting patients, which preserves high-acuity use but restricts elective drainage growth in that setting.

By End Use: Hospitals Lead While ASCs Define the Growth Frontier

Hospitals held 61.87% of procedure volume in 2025, which kept the largest share of the pericardiocentesis procedures market within inpatient and hospital-based cardiac care. Their lead remains strong because acute tamponade management still depends on hemodynamic monitoring, advanced imaging access, and cardiothoracic surgical backup that most outpatient sites cannot fully replicate. Ambulatory surgical centers are the fastest-growing end-use segment and are projected to expand at a 7.68% CAGR through 2031 as short-stay cardiology care becomes more accepted. CMS stated that 234 Medicare-certified ASCs offered cardiovascular services in early 2025, which shows that the setting base for elective pericardiocentesis is already meaningful and still expanding.

Cost pressure supports this migration because a 2025 Medicare analysis found lower costs for ASC-based cardiac procedures than for hospital outpatient departments. Specialty clinics occupy a narrower role and tend to focus on recurrent malignant effusions within integrated cardio-oncology programs. Reimbursement still slows the shift, because the approval path for more complex cardiovascular procedures in ASCs moves more slowly than provider interest does. The pericardiocentesis procedures industry, therefore, remains hospital-centered even as outpatient capacity grows. Over time, the pericardiocentesis procedures market is likely to widen by setting rather than replacing hospitals, with acute care and elective care continuing to sit in different operational lanes.

Geography Analysis

North America held 37.23% of the pericardiocentesis procedures market size in 2025, supported by dense cardiac center infrastructure, advanced echocardiography use, and established reimbursement channels. The United States remains the regional anchor, where CMS implemented a 2.9% outpatient payment update for 2025 and continued to support both hospital outpatient and ASC procedural pathways. Those payment structures help sustain procedure availability across multiple care settings, even though providers still face pressure to control costs in higher-volume programs. The region also benefits from high immune checkpoint inhibitor treatment volumes and better cardio-oncology coordination, which creates a more recurring referral flow for malignant and immune-related effusions.

Europe remains the second-largest regional block in the pericardiocentesis procedures market, with Germany standing out for a stronger coding structure and more formalized procedural pathways. That framework supports better documentation, benchmarking, and quality reporting, which helps larger centers manage both emergency and planned drainage more consistently. France takes a more restrictive stance in oncology, where national guidance limits pericardiocentesis in lung cancer to tamponade-presenting cases and therefore contains elective expansion. The United Kingdom, Italy, Spain, and other European markets are steadily widening multi-modal imaging adoption as cardiac center capacity improves and guidance tools reach more secondary hospitals.

Asia-Pacific is forecast to grow at a 6.03% CAGR through 2031, making it the fastest-growing region in the pericardiocentesis procedures market. Japan already shows measurable clinical density, with a 2024 hospital study finding pericardial effusion in 0.4% of echocardiography patients and continued follow-up risk after presentation. Japan also showed rising academic attention in 2025 through dedicated coverage of tamponade management and pericardial drainage protocols. India remains underpenetrated relative to disease burden because imaging access and specialist capacity are still uneven outside major centers. The Middle East and Africa are expanding more gradually, but a 4-year retrospective from the region showed meaningful etiologic diversity, which underlines the need for flexible procedural protocols and adaptable kit selection. South America is growing from a smaller base as cancer treatment adoption and hospital investment raise demand for both emergency drainage and malignant-effusion related elective procedures.

Competitive Landscape

The pericardiocentesis procedures market has a moderately consolidated structure, with one set of companies focused on kits and catheters and another set focused on imaging guidance. Merit Medical Systems and Cook Medical anchor the consumable layer, while Becton, Dickinson, B. Braun Melsungen, Teleflex, and Terumo compete across adjacent access and drainage categories. In consumables, competitive separation depends more on tray configuration, catheter design, procurement fit, and supply reliability than on major clinical differentiation. In imaging, GE HealthCare, Koninklijke Philips, and Siemens Healthineers shape workflow through portable and higher-end ultrasound platforms that support emergency departments, intensive care units, and catheterization laboratories. This split gives the pericardiocentesis procedures market a two-layer competitive pattern, with recurring consumable demand on one side and higher-value guidance control on the other.

Teleflex made one of the clearest portfolio moves in 2025 when it announced a definitive agreement to acquire BIOTRONIK’s Vascular Intervention business for EUR 760 million, or USD 826 million, which signaled a broader push across adjacent cardiovascular access categories. Cook Medical and Siemens Healthineers then introduced an integrated Interventional MRI Suite at SIR 2026, and Cook launched a dedicated iMRI division, which points to a tighter linkage between devices and guidance infrastructure in tertiary settings. Teleflex also received FDA 510(k) clearance in April 2025 for the AC3 Range intra-aortic balloon pump, which strengthens its position in high-acuity cardiovascular care that can sit close to post-procedure stabilization workflows. The pericardiocentesis procedures market is also watching newer access concepts closely because more controlled entry tools could reduce hesitation in anatomically complex cases. Regulatory entry requirements under FDA 510(k) and ISO 13485 continue to favor companies that already have quality systems, hospital relationships, and established sales channels.

White space remains strongest in AI-supported ultrasound interpretation, advanced training systems for lower-volume operators, and products designed for loculated or post-surgical effusions. Training has become a competitive lever because hospitals need safer ways to shorten the learning curve for clinicians who perform the procedure less often. The pericardiocentesis procedures market, therefore, rewards vendors that can link access tools, imaging support, training value, and dependable supply in a single hospital-ready offer. Competitive intensity is moderate to high, but the field still leaves room for workflow innovation where safety, portability, and reimbursement all matter.

Pericardiocentesis Procedures Industry Leaders

3M

B. Braun Melsungen AG

Cardinal Health, Inc.

GE HealthCare Technologies Inc.

Teleflex Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Cook Medical and Siemens Healthineers debuted an integrated Interventional MRI Suite at SIR 2026, enabling radiation-free, real-time image-guided minimally invasive procedures. Cook Medical simultaneously launched its dedicated iMRI division, signaling strategic intent to develop guidance-integrated procedure capabilities with direct implications for complex effusion drainage workflows in tertiary cardiac centers.

- April 2025: Teleflex received FDA 510(k) clearance for the AC3 Range Intra-Aortic Balloon Pump, designed for IABP support across patient transport modes including ambulances and air transport, a product that directly complements post-pericardiocentesis hemodynamic stabilization pathways in high-acuity emergency settings.

- February 2025: Teleflex announced a definitive agreement to acquire BIOTRONIK's Vascular Intervention business for EUR 760 million, marking the largest announced medtech transaction in the interventional cardiovascular access space in early 2025 and reshaping competitive positioning in procedural access.

Global Pericardiocentesis Procedures Market Report Scope

Pericardiocentesis is a minimally invasive medical procedure used to remove excess fluid from the pericardial sac (the membrane surrounding the heart). It is performed therapeutically to relieve life-threatening pressure on the heart (cardiac tamponade) and diagnostically to analyze the fluid for conditions like cancer or infection.

The pericardiocentesis procedures market is segmented by procedure type, guidance method, application, and end use. By procedure type, it includes emergency pericardiocentesis and elective pericardiocentesis. By guidance method, procedures are performed using echocardiography guidance, fluoroscopy guidance, or CT guidance. By application, pericardiocentesis is primarily used in cases of cardiac tamponade, pericardial effusion, and pericarditis. By end use, adoption is driven by hospitals, ambulatory surgical centers, and specialty clinics.

| Emergency Pericardiocentesis |

| Elective Pericardiocentesis |

| Echocardiography-Guided Pericardiocentesis |

| Fluoroscopy-Guided Pericardiocentesis |

| CT-Guided Pericardiocentesis |

| Cardiac Tamponade |

| Pericardial Effusion |

| Pericarditis |

| Hospitals |

| Ambulatory Surgical Centers |

| Specialty Clinics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Procedure Type | Emergency Pericardiocentesis | |

| Elective Pericardiocentesis | ||

| By Guidance Method | Echocardiography-Guided Pericardiocentesis | |

| Fluoroscopy-Guided Pericardiocentesis | ||

| CT-Guided Pericardiocentesis | ||

| By Application | Cardiac Tamponade | |

| Pericardial Effusion | ||

| Pericarditis | ||

| By End Use | Hospitals | |

| Ambulatory Surgical Centers | ||

| Specialty Clinics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the expected value of pericardiocentesis procedures by 2031?

The pericardiocentesis procedures market is forecast to reach USD 1.50 billion by 2031, rising from USD 1.14 billion in 2026 at a 5.63% CAGR.

Which region leads current demand for pericardiocentesis procedures?

North America led with a 37.23% share in 2025, supported by strong cardiac center infrastructure, reimbursement pathways, and wide echocardiography use.

Which region is growing the fastest through 2031?

Asia-Pacific is projected to grow the fastest at a 6.03% CAGR through 2031 as hospital investment and oncology-related demand continue to rise.

Why is elective pericardiocentesis gaining traction?

Elective procedures are growing at a 7.14% CAGR because clinicians are draining moderate malignant and inflammatory effusions earlier for diagnosis, symptom relief, and prevention of progression.

Which end-use setting will expand the most quickly?

Ambulatory surgical centers are expected to post the fastest growth at a 7.68% CAGR, although hospitals still held 61.87% of volume in 2025.

Page last updated on: