Paediatric Cardiology Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.89 Billion |

| Market Size (2031) | USD 6.02 Billion |

| Growth Rate (2026 - 2031) | 4.26% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

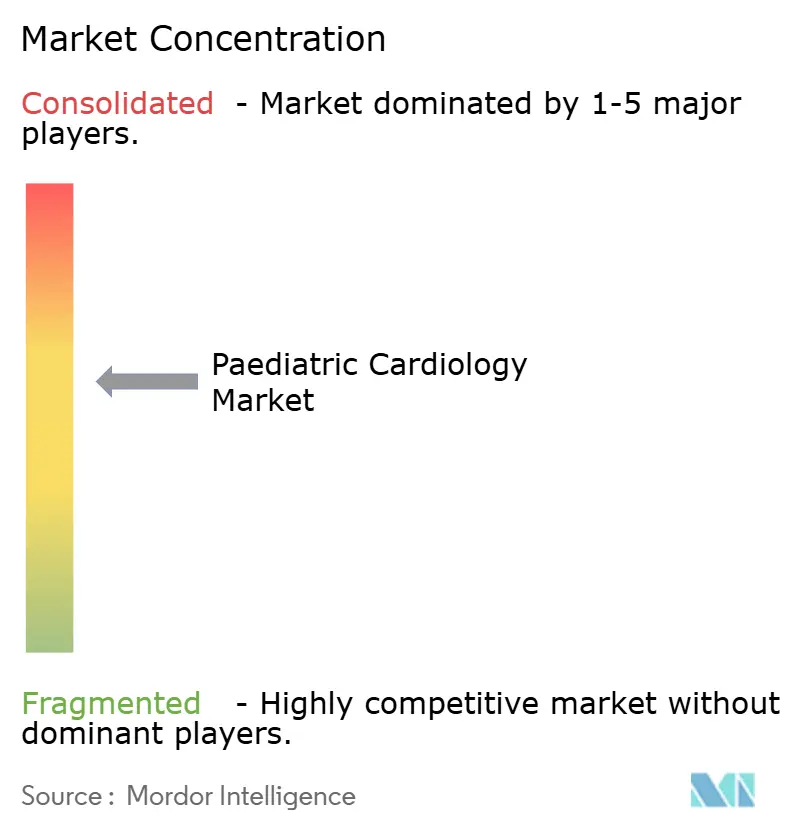

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Paediatric Cardiology Market Analysis by Mordor Intelligence

The paediatric cardiology market size is expected to grow from USD 4.69 billion in 2025 to USD 4.89 billion in 2026 and is forecast to reach USD 6.02 billion by 2031 at 4.26% CAGR over 2026-2031. This measured trajectory hides structural changes such as the need for devices that grow with the child, the rise of transcatheter therapies that sidestep open surgery, and the growing reliance on centres of excellence that pool scarce specialist skills. North America dominates revenue owing to mature reimbursement systems and high‐volume paediatric heart centres, while Asia-Pacific is expanding fastest as health systems add paediatric catheterisation labs and build specialist capacity. Regulatory shifts, typified by the FDA’s 2024 decision to widen Impella heart-pump use in children weighing ≥30 kg, accelerate market access for miniaturised devices. In parallel, rapid miniaturisation—illustrated by the world’s smallest pacemaker implantation at NYU Langone in February 2025—shows how engineering advances are redrawing clinical possibilities.

Key Report Takeaways

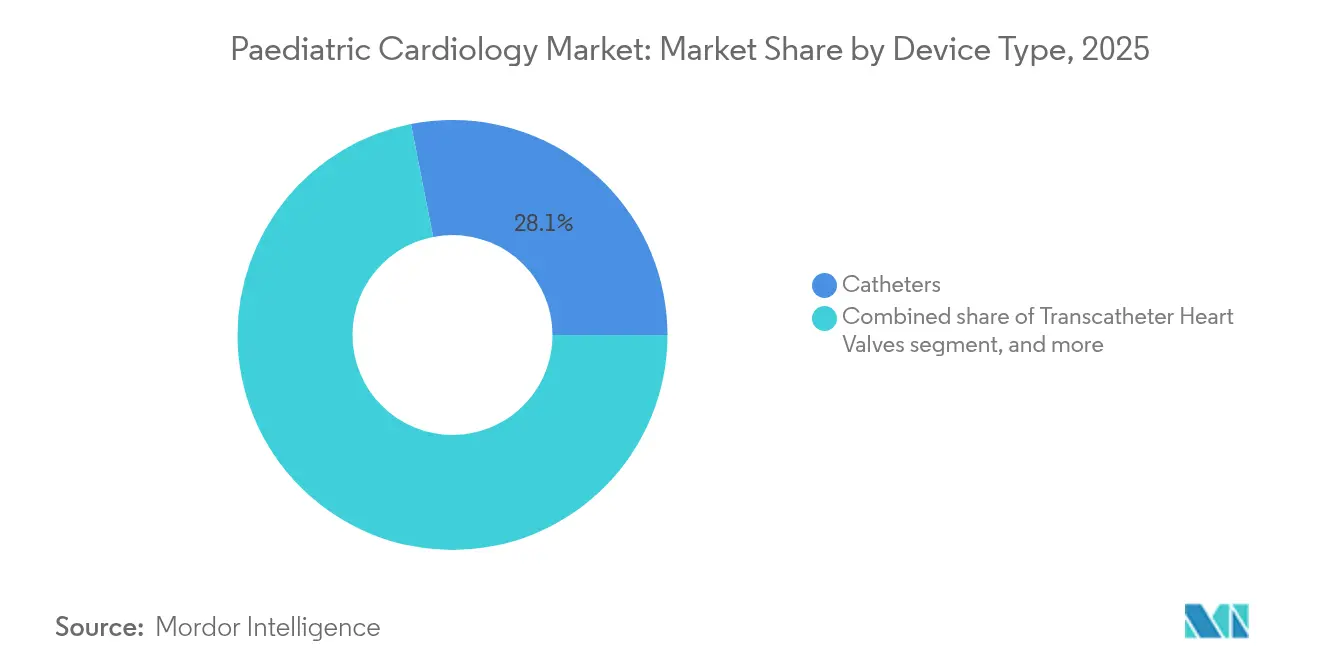

- By device type, catheters accounted for 28.10% of paediatric cardiology market share in 2025, while transcatheter heart valves are set to log the fastest 6.47% CAGR through 2031.

- By surgical procedures, interventional procedures held 45.80% of 2025 revenue, whereas heart rhythm management procedures are forecast to grow at 6.88% CAGR during 2026-2031.

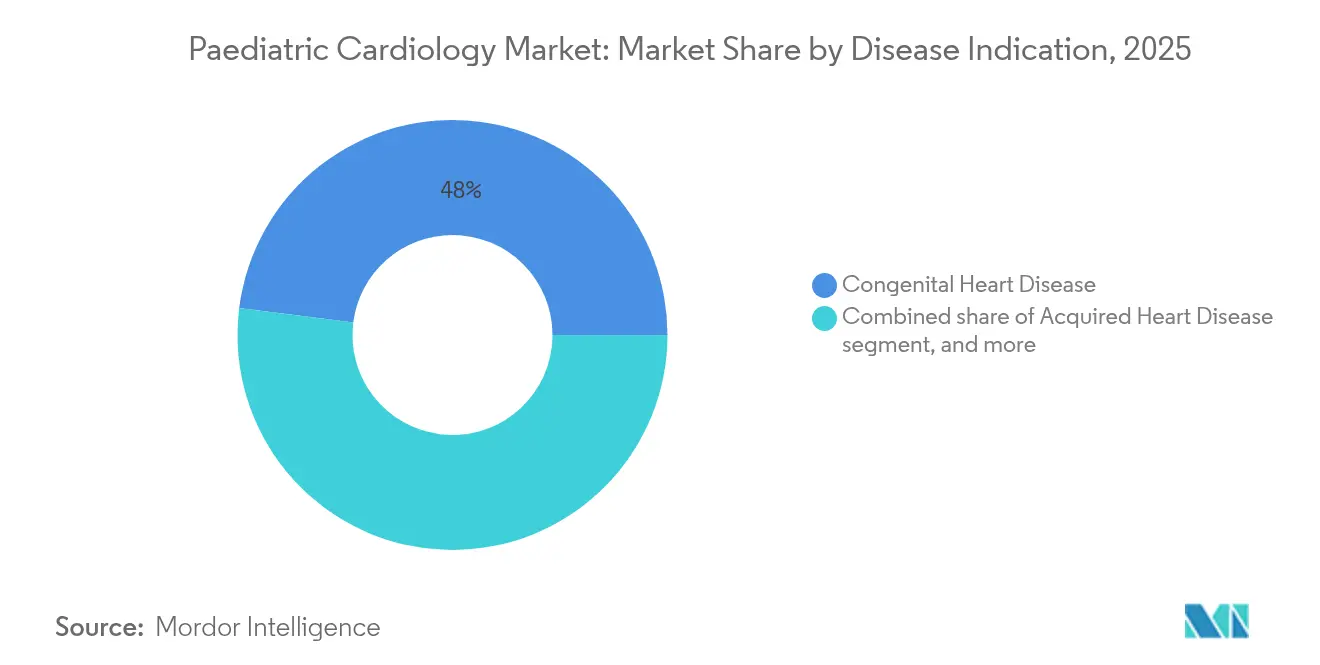

- By disease indication, congenital heart disease represented 48.00% of paediatric cardiology market share in 2025, yet cardiomyopathies are expected to expand at 7.74% CAGR to 2031.

- By end user, hospitals captured 71.00% of 2025 spending; specialty clinics are on course for a 7.54% CAGR over the next five years.

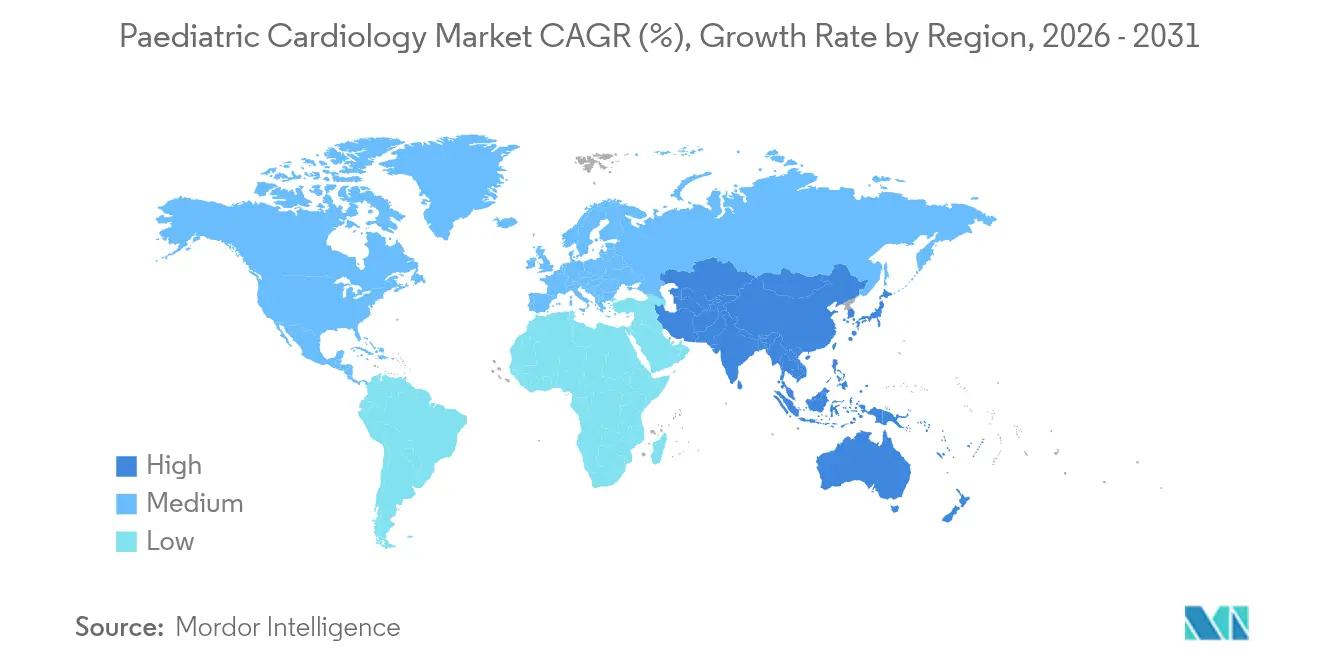

- By geography, North America generated 41.90% of global sales in 2025, but Asia-Pacific leads growth at 5.35% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Paediatric Cardiology Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Burden Of Congenital Heart Diseases Worldwide | +1.2% | Global, with higher impact in APAC and MEA | Long term (≥ 4 years) |

| Rapid Technological Advancements In Pediatric Cardiology Devices | +0.8% | North America & EU core, spill-over to APAC | Medium term (2-4 years) |

| Government Funding And Favorable Reimbursement Policies | +0.6% | North America & EU primarily | Medium term (2-4 years) |

| Expansion Of Specialized Pediatric Cardiology Centers | +0.5% | APAC core, emerging in MEA | Long term (≥ 4 years) |

| Increasing Adoption Of Minimally Invasive Transcatheter Procedures | +0.7% | Global, led by North America | Short term (≤ 2 years) |

| Growing Strategic Collaborations And Industry Investments | +0.4% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Burden of Congenital Heart Diseases Worldwide

Roughly 40,000 babies are born each year in the United States with congenital heart defects, and 2.4 million Americans live with these conditions[1]American Heart Association, “Congenital heart defects statistics,” heart.org. Globally, hypertrophic cardiomyopathy affects 1 in 200-500 persons, underscoring the need for lifelong surveillance. Rising survival rates mean children transition into adulthood requiring device replacements that fit growing bodies. In April 2025, Chinese surgeons implanted a 45 g magnetically levitated artificial heart in a 7-year-old, demonstrating how innovation is targeting paediatric size constraints. Sub-Saharan African nations such as Sudan and Zimbabwe lack paediatric cardiac surgery capacity entirely, creating long-range demand for mobile teams and public–private projects that feed future paediatric cardiology market growth.

Rapid Technological Advancements in Paediatric Cardiology Devices

Miniaturisation is advancing from stents that expand with the child’s artery to leadless pacemakers small enough for infants. Westchester Medical Center reported success with growth-accommodating aortic stents that minimise repeat interventions. At Toronto’s Hospital for Sick Children, a robotic micro-injector can test multiple therapies on beating heart tissue, accelerating drug discovery for inherited arrhythmias. In November 2024, BrightHeart’s AI software gained FDA clearance for prenatal detection of congenital defects, standardising expertise across centres. Collectively, these breakthroughs sharpen competitive edges and set higher performance baselines across the paediatric cardiology market.

Government Funding and Favourable Reimbursement Policies

The NIH and Children’s Heart Foundation award up to USD 150,000 per project for paediatric cardiac research, underwriting early-stage device ideas. Medicaid reform and private-payer parity laws in selected US states now recognise the higher resource use inherent in paediatric interventions, improving provider revenue stability[2]Healthcare Financial Management Association, “Medicaid reimbursement for paediatric cardiac care,” hfma.org. In 2024 the FDA approved an expandable paediatric stent line that can be dilated as children grow, cutting the need for serial surgeries. Such policy signals give manufacturers clearer reimbursement pathways, fuelling R&D investment in the paediatric cardiology industry.

Expansion of Specialised Paediatric Cardiology Centres

Cleveland Clinic and Johns Hopkins boosted fellowship positions for paediatric cardiologists in 2025 to counter specialist shortages. In January 2025, Rady Children’s Hospital joined forces with Children’s HealthCare of California, pooling resources under the new Rady Children’s Health system to improve surgical throughput. China’s focus on magnetic-levitation ventricular assist devices for children underlines how emerging markets leapfrog to state-of-the-art solutions. Concentrated centres accrue learning curves that lift procedural success and stimulate device demand, strengthening the paediatric cardiology market’s long-term resilience.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost Of Pediatric Cardiology Procedures And Devices | -0.9% | Global, more pronounced in emerging markets | Long term (≥ 4 years) |

| Stringent Regulatory Approval Processes | -0.6% | Global, particularly North America & EU | Medium term (2-4 years) |

| Limited Access To Skilled Pediatric Cardiologists In Developing Regions | -0.5% | APAC, MEA, Latin America | Long term (≥ 4 years) |

| Supply Chain Disruptions And Reimbursement Constraints | -0.4% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cost of Paediatric Cardiology Procedures and Devices

Hospital charges can vary by more than 300% for identical paediatric cardiac interventions, limiting access for uninsured families. Devices must be produced in multiple sizes and undergo small-cohort trials, pushing unit costs higher than adult equivalents. Coverage gaps affect outcomes; Medicaid-insured children often face treatment delays compared with those on private plans. Financial strain extends over a lifetime of follow-up and replacement, shaping demand patterns across the paediatric cardiology market.

Stringent Regulatory Approval Processes

Manufacturers must extrapolate adult trial data while staging paediatric studies that are hard to enrol, prolonging FDA timelines. Europe’s CE marking route differs materially, forcing duplicated dossiers and adding cost. Devices such as the SAPIEN 3 valve or AMPLATZER occluder each needed multi-region evidence packages before paediatric use[3]European Medicines Agency, “Pediatric investigation plans for cardiac devices,” ema.europa.eu. Smaller innovators often lack the capital for this regulatory gauntlet, consolidating share with large incumbents and tempering overall paediatric cardiology market growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Transcatheter Innovation Drives Growth

Catheters secured 28.10% of 2025 revenue and remain indispensable across diagnostic and therapeutic workflows, underpinning the paediatric cardiology market size for baseline consumables. Transcatheter heart valves, however, are charting a 6.47% CAGR to 2031, underscoring a pivot toward minimally invasive solutions that shorten recovery and cut hospital stay. The 2024 Edwards–JenaValve deal extended transcatheter options tailored for high-risk children, signalling intensified competition in growth-accommodating valve technology.

Expandable stents capable of enlarging with arterial growth illustrate engineering designed for paediatric physiology, and W.L. Gore’s CARDIOFORM device hit 100% closure rates for atrial-septal defects in recent trials. Occlusion devices retain stable niches for septal anomalies, while introducer sheaths are shrinking in French size to cut vascular trauma. As AI-guided imaging improves placement accuracy, transcatheter platforms are set to reshape the paediatric cardiology market.

By Surgical Procedures: Interventional Dominance Accelerates

Interventional approaches claimed 45.80% of 2025 value, positioning them as the economic backbone of the paediatric cardiology market share. Heart rhythm management, though smaller, is progressing fastest at a 6.88% CAGR thanks to leadless pacemakers demonstrated in infants at NYU Langone. UC Davis added proof in teenagers with the dual-chamber leadless system effective at 13 years old.

Open-heart surgery still anchors care for complex reconstructions, yet the discovery that newborns possess heightened regenerative capacity is nudging clinicians toward earlier, less invasive correction where feasible. Bioabsorbable scaffolds that remodel as the heart heals are in early trials, pointing to hybrid paths that merge surgical principles with catheter-based deployment.

By Disease Indication: Cardiomyopathies Lead Growth

Congenital heart disease controlled 48.00% of 2025 sales, anchoring the paediatric cardiology market size in core volume therapies. Cardiomyopathies, propelled by AI-assisted diagnostics such as Johns Hopkins’ MAARS model with 89% predictive accuracy, are climbing at a 7.74% CAGR. Earlier diagnosis multiplies the pool eligible for implantable mini-devices and gene-targeted drugs.

Pulmonary hypertension management is evolving with sensor-based monitoring systems inherited by Edwards through the Endotronix purchase, allowing earlier intervention. Rare disorders remain niche but lucrative given high device ASPs and compassionate-use programs, bolstering the high-value tail of the paediatric cardiology market.

By End User: Specialty Clinics Gain Momentum

Hospitals generated 71.00% of turnover in 2025 owing to comprehensive ICU and surgical suites. Yet specialty clinics are advancing fastest at 7.54% CAGR, mirroring a trend toward focused centres that concentrate experience and lower per-procedure complications. The new Rady Children’s Health network pools two California systems to capture referral flows and streamline procurement.

Tele-echocardiography and remote rhythm monitoring broaden clinic reach into rural zones, channelling additional patients for elective catheterisation. Ambulatory surgery centres now outfit mini cath-labs for same-day septal defect closures in carefully selected cases, further diversifying the paediatric cardiology market.

Geography Analysis

North America retained a 41.90% revenue share in 2025, reflecting deep procedural experience, early device roll-outs, and payer models that reimburse complex paediatric cases FDA.gov. The FDA’s pediatric-first policy initiatives, including breakthrough-device designations for growth-oriented valves, preserve the region’s edge. Insurance cost pressures and workforce shortages temper absolute growth but spur operational efficiencies that ripple across the paediatric cardiology market.

Asia-Pacific is accelerating at 5.35% CAGR to 2031 as governments channel funds into tertiary children’s hospitals and catheterisation training. Milestones such as China’s 45 g artificial heart in a 7-year-old and Japan’s trials of AI prenatal scanners highlight the region’s leap-frog mentality. Capacity gaps persist—several ASEAN states average fewer than one paediatric cardiac surgeon per million children—but joint ventures with US and EU centres are closing skills deficits.

Europe shows steady uptake aided by universal coverage and cross-border research consortia. The European Society of Cardiology’s standardised training modules harmonise competencies, smoothing device adoption rates. Meanwhile, Middle East & Africa and South America register early-stage growth constrained by limited cath-lab density. Philanthropic missions and outbound medical travel partly offset local deficits, yet long logistics chains extend device delivery times, moderating paediatric cardiology market penetration until domestic infrastructure scales.

Competitive Landscape

Market leadership clusters around Abbott Laboratories, Medtronic, Edwards Lifesciences, and Boston Scientific, each leveraging adult technology platforms refashioned for paediatric anatomy. Abbott’s TriClip adaptation for congenital tricuspid leaks shows pipeline breadth. Edwards’ USD 1.2 billion dual buy of JenaValve and Endotronix in July 2024 stitched together valve and sensor technologies to widen its high-risk paediatric umbrella.

Mid-tier challengers focus on niche innovations. BrightHeart’s FDA-cleared AI imaging suite slots into prenatal workflows, a gateway to downstream interventional device sales. W.L. Gore exploits fluoropolymer expertise for growth-accommodating occluders, while startups in Israel and Singapore pursue absorbable stent polymers. Collaboration between NewYork-Presbyterian and device makers to trial heart-regeneration therapies marks a third vector—biologics that may one day reduce implant reliance.

Competitive intensity rests on intellectual property around miniaturisation and adaptive sizing. Firms proficient in navigating paediatric study protocols enjoy first-mover safety as follow-on entrants wrestle with small study populations. As reimbursement frameworks catch up with paediatric complexity, the paediatric cardiology market increasingly rewards companies with targeted regulatory units and long-run servicing programs for devices implanted at infancy yet monitored into adulthood.

Paediatric Cardiology Industry Leaders

Abbott Laboratories

Medtronic Plc

Edwards Lifesciences

Boston Scientific Corp.

Terumo Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Union Hospital Wuhan surgeons implanted a 45 g magnetically levitated artificial heart in a 7-year-old boy, the smallest such device yet used in paediatrics.

- March 2025: Baylor College of Medicine and QIMR Berghofer researchers discovered calcium-channel manipulation that triggers cardiomyocyte proliferation, a potential therapy for paediatric heart failure.

- February 2025: Northwestern Medicine found newborn macrophages secrete thromboxane A2 enabling post-injury heart regeneration, informing timing of paediatric interventions.

- January 2025: Rady Children’s Hospital merged with Children’s HealthCare of California creating Rady Children’s Health.

- December 2024: Johnson & Johnson secured FDA clearance expanding Impella heart pump use to children ≥30 kg.

- November 2024: BrightHeart’s AI software received FDA clearance for prenatal detection of congenital heart defects.

Global Paediatric Cardiology Market Report Scope

As per the research scope, pediatric cardiology involves pediatric cardiologists collaborating with infant specialists to deliver holistic care to infants and children grappling with intricate heart conditions. These cardiologists devise comprehensive treatment plans, predominantly leveraging diagnostic and surgical methods.

The pediatric cardiology market is categorized by product type, surgical procedures, disease indication, end-user, and geography. Product types include transcatheter heart valves, occlusion devices, atherectomy devices, catheters, stents, introducer sheaths, and others. Surgical procedures encompass interventional procedures, heart rhythm management, and others. Disease indications cover congenital heart disease, acquired heart disease, arrhythmias, cardiomyopathies, patent foramen ovale (PFO), pulmonary hypertension, and others. End-users span hospitals, specialty clinics, and other end users. Geographically, the market spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. The Report Offers the Value (in USD) for the Above Segments.

| Transcatheter Heart Valves |

| Occlusion Devices |

| Atherectomy Devices |

| Catheters |

| Stents |

| Introducer Sheaths |

| Other Device Type |

| Interventional Procedures |

| Heart Rhythm Management Procedures |

| Other Surgical Procedures |

| Congenital Heart Disease |

| Acquired Heart Disease |

| Arrhythmias |

| Cardiomyopathies |

| Patent Foramen Ovale (PFO) |

| Pulmonary Hypertension |

| Other Disease Indications |

| Hospitals |

| Specialty Clinics |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Device Type | Transcatheter Heart Valves | |

| Occlusion Devices | ||

| Atherectomy Devices | ||

| Catheters | ||

| Stents | ||

| Introducer Sheaths | ||

| Other Device Type | ||

| By Surgical Procedures | Interventional Procedures | |

| Heart Rhythm Management Procedures | ||

| Other Surgical Procedures | ||

| By Disease Indication | Congenital Heart Disease | |

| Acquired Heart Disease | ||

| Arrhythmias | ||

| Cardiomyopathies | ||

| Patent Foramen Ovale (PFO) | ||

| Pulmonary Hypertension | ||

| Other Disease Indications | ||

| By End User | Hospitals | |

| Specialty Clinics | ||

| Other End Users | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the paediatric cardiology market in 2026?

The paediatric cardiology market size stands at USD 4.89 billion in 2026.

What annual growth is expected through 2031?

The sector is forecast to register a 4.26% CAGR to reach USD 6.02 billion by 2031.

Which region is expanding fastest in paediatric cardiac care?

Asia-Pacific leads growth with a projected 5.35% CAGR owing to rising infrastructure investment and specialist training.

Which device segment is growing most quickly?

Transcatheter heart valves are posting the highest device CAGR at 6.47% as minimally invasive procedures gain traction.

What is the main clinical driver of demand?

The persistent burden of congenital heart diseaseÑaffecting 40,000 newborns annually in the United States aloneÑanchors long-term device demand.

Why are specialty clinics gaining share?

Concentrated expertise and tele-monitoring technologies let specialty clinics perform complex procedures efficiently, driving a 7.54% CAGR in their revenue.

Page last updated on: