Perfusion Radiology Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.20 Billion |

| Market Size (2031) | USD 4.24 Billion |

| Growth Rate (2026 - 2031) | 5.80% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

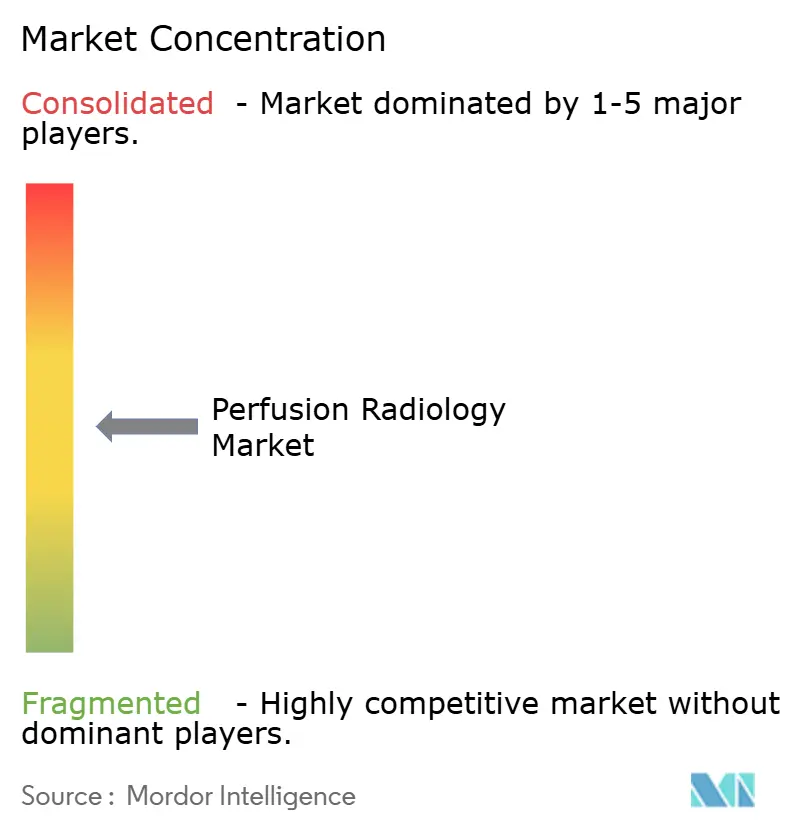

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Perfusion Radiology Market Analysis by Mordor Intelligence

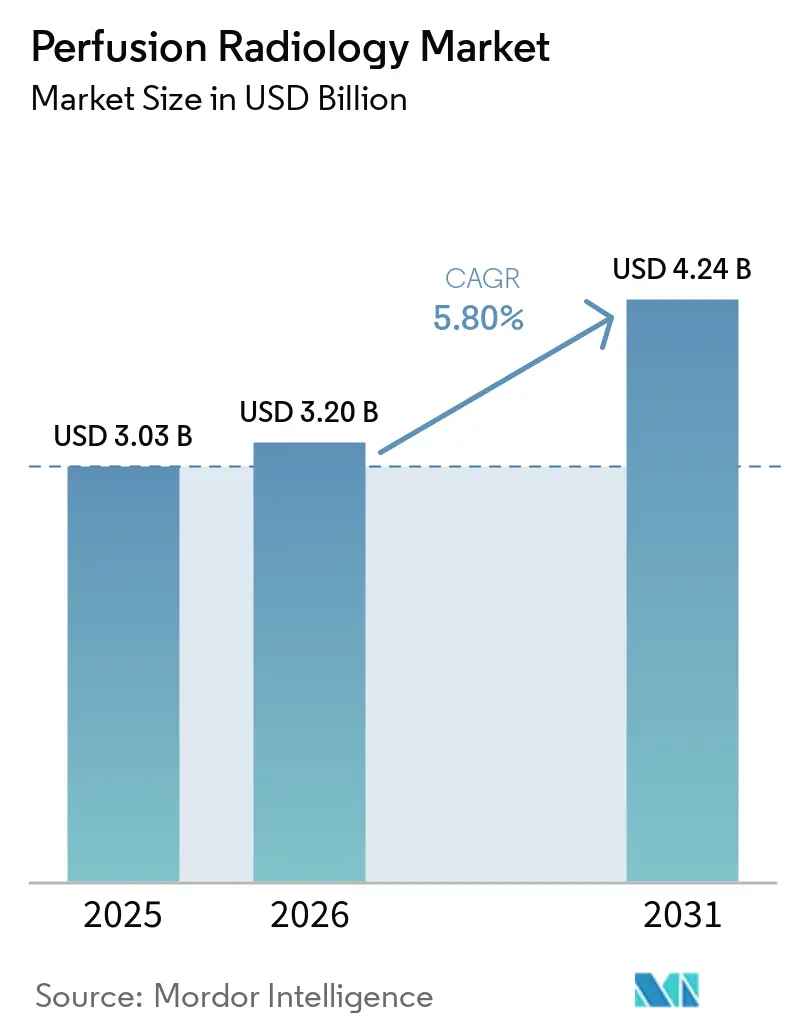

The Perfusion Radiology Market size is expected to increase from USD 3.03 billion in 2025 to USD 3.20 billion in 2026 and reach USD 4.24 billion by 2031, growing at a CAGR of 5.80% over 2026-2031.

Perfusion imaging is increasingly being adopted as a primary diagnostic tool in stroke, cardiac, and oncology pathways, moving beyond its earlier specialist use. Protocol standardization and advanced software ecosystems now enable care teams to convert raw scan data into clinical metrics within minutes, reducing the time between image acquisition and treatment decisions. In 2025, the global annual cost of strokes exceeded USD 890 billion, with this burden projected to rise significantly by 2050, driving institutional investments in faster perfusion-guided triage tools.[1]Valery Feigin et al., “World Stroke Organization Global Stroke Fact Sheet 2025,” International Journal of Stroke, sagepub.com Competition in the perfusion radiology market is intensifying as hardware leaders and AI software specialists compete to dominate the end-to-end workflow, from data acquisition to interpretation and alerting. Additionally, the growing importance of radiotracer and contrast access in cardiac imaging is strengthening the market position of companies with both imaging and radiopharmaceutical capabilities.

Key Report Takeaways

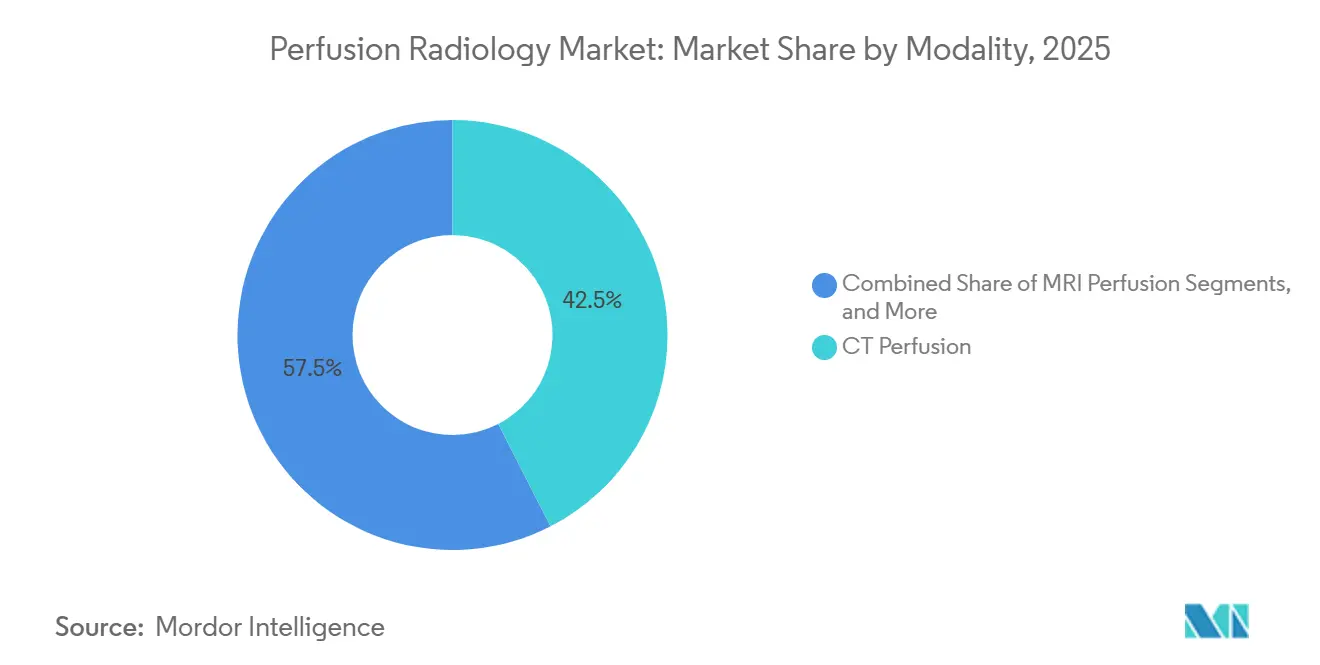

- By modality, CT perfusion held 42.48% revenue share in 2025, while MRI perfusion is projected to expand at a 7.25% CAGR through 2031.

- By application, cardiology accounted for 48.55% share in 2025, while oncology is projected to grow at a 6.55% CAGR through 2031.

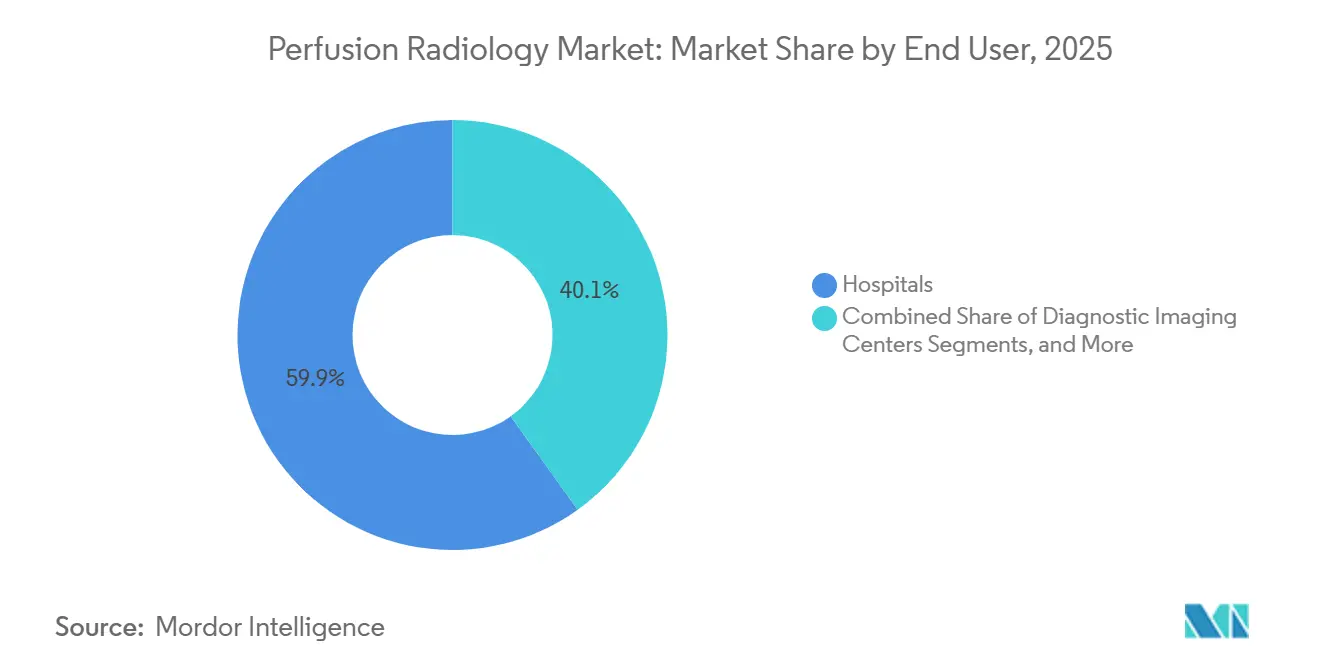

- By end user, hospitals held 59.89% share in 2025, while diagnostic imaging centers are projected to advance at a 6.88% CAGR through 2031.

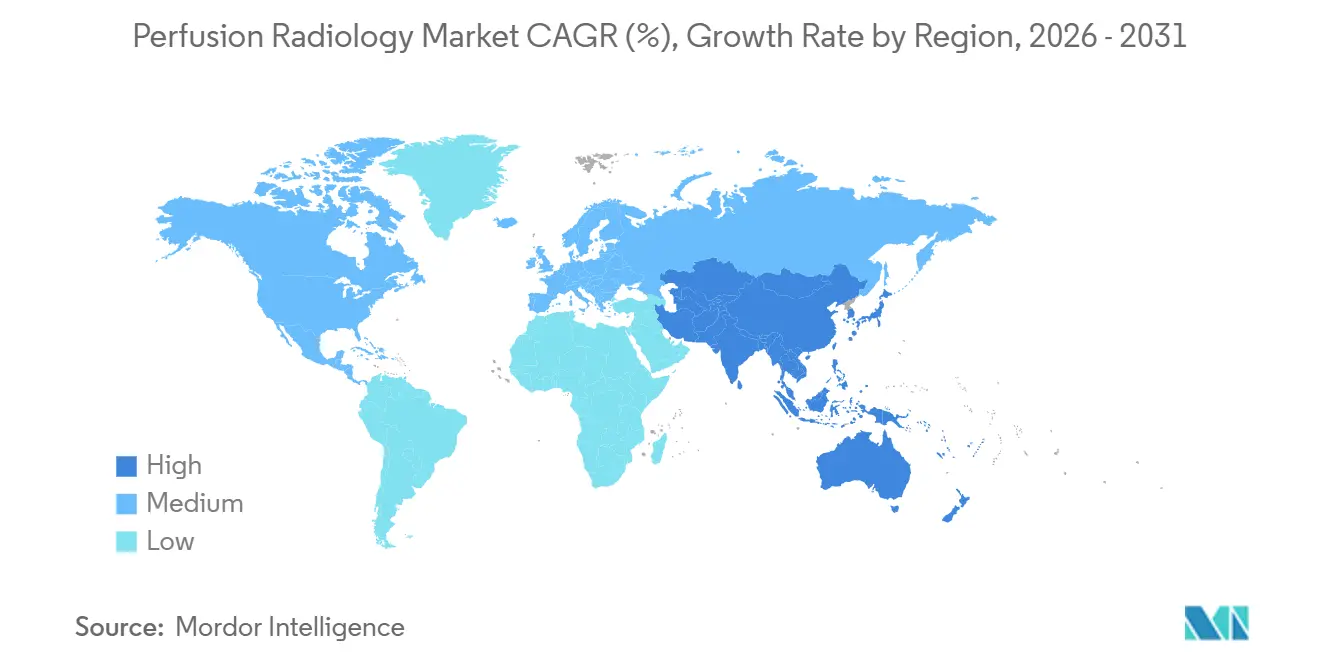

- By geography, North America captured 40.25% of global revenue in 2025, while Asia-Pacific is expected to grow at an 8.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Perfusion Radiology Market Trends and Insights

Drivers Impact Analysis*

| Rising stroke incidence and acute coronary workflow dependence | +1.5% | Global, concentrated in North America, Europe, APAC | Short term (≤ 2 years) |

|---|---|---|---|

| AI-enabled quantitative perfusion analysis platforms | +1.2% | Global, early leadership in North America and Europe with rapid APAC uptake | Short term (≤ 2 years) |

| Imaging department productivity pressure and automation demand | +0.8% | North America and Europe, spill-over to APAC | Medium term (2-4 years) |

| CT Perfusion adoption in emergency and neurology departments | +1.0% | Global, with concentrated growth in China, India, and Southeast Asia | Short term (≤ 2 years) |

| Advanced perfusion analytics for oncology therapy monitoring | +0.7% | North America, Europe, expanding in APAC | Medium term (2-4 years) |

| Reimbursement support for advanced cardiac and neuro perfusion imaging | +0.9% | North America core, spill-over to Western Europe and South Korea | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Stroke Incidence Creates Irreversible Demand for Time-Sensitive Perfusion Tools

Stroke remains the primary driver of demand in the perfusion radiology market, as timely treatment depends on quickly identifying salvageable tissue versus irreversible damage. The 2025 Global Stroke Fact Sheet estimated the annual global cost of strokes at over USD 890 billion, highlighting the need for faster triage tools and standardized imaging protocols. A 2024 forecast from the Journal of the American Heart Association projected global stroke cases to reach 21.43 million by 2050, indicating sustained demand for perfusion evaluations.[2]Lu Xing et al., “Projections of the Stroke Burden at the Global, Regional, and National Levels up to 2050 Based on the Global Burden of Disease Study 2021,” Journal of the American Heart Association, ahajournals.org Comprehensive stroke centers increasingly use real-time CT Perfusion maps to guide thrombectomy decisions, especially for patients presenting beyond the optimal treatment window. In 2024 and 2025, Chinese hospitals adopted 60-second whole-brain CT perfusion with head-to-neck CTA, expanding its use from flagship centers to broader hospital networks under guideline-driven triage models.[3]Diagnostically Competitive Performance of a Physiology-Informed Generative Multi-Task Network for Contrast-Free CT Perfusion,” Frontiers in Human Neuroscience, frontiersin.org This trend reflects the market's focus on addressing rising patient volumes and ensuring consistent acute stroke decision-making across healthcare systems.

AI-Enabled Quantitative Perfusion Analysis Redefines Platform Competition

Quantitative software has become a key competitive factor in the perfusion radiology market, with buyers demanding speed, consistency, and clinically relevant outputs from a single platform. Stroke centers in North America and Europe now expect automated perfusion maps, ischemic core segmentation, and care-team alerts as standard workflow features. A 1,591-case study presented at ESOC 2025 showed RapidAI detected 93% of medium vessel occlusions with CT perfusion imaging, outperforming a competing platform's 70% detection rate.[4AI in Radiology and Interventions, A Structured Narrative Review of Workflow Automation, Accuracy, and Efficiency Gains of Today and What’s Coming,” PubMed, pubmed.ncbi.nlm.nih.gov] Research is advancing toward contrast-free methods, with a 2026 study demonstrating that a generative AI model produced competitive perfusion maps using non-contrast CT data. If validated at scale, this approach could reduce reliance on contrast administration, addressing a key access barrier in the market. FDA clearance pathways remain critical in determining how quickly these innovations transition from research to clinical use.

Imaging Department Automation Addresses Radiologist Capacity Constraints

Rising scan volumes and limited workforce growth are driving demand for automation in the perfusion radiology market, particularly in North America and Europe. Health systems are prioritizing workflow efficiencies to meet demand without proportionately increasing specialist hires. A 2025 structured review indexed in PubMed highlighted AI's ability to automate key radiology workflow steps, with perfusion post-processing among the closest to full autonomy. Automation enhances accuracy, throughput, staffing flexibility, and report consistency while reducing turnaround times in high-volume departments. In early 2025, Philips demonstrated this trend with SmartHeart automating cardiac MR scan planning in under 30 seconds, while CardiacQuant Perfusion integrated non-invasive quantitative myocardial assessment into the same workflow. These advancements underscore the market's shift toward solutions that reduce technologist dependency and alleviate reporting pressures.

Oncology Perfusion Expands the Addressable Clinical Base

Oncology is broadening the clinical scope of the perfusion radiology market, as vascular response often becomes evident before tumor size changes on conventional imaging. DCE-MRI Ktrans values are now used as early biomarkers in anti-angiogenic therapy monitoring across various tumor settings, embedding perfusion imaging into treatment protocols. A 2025 editorial in Frontiers in Oncology highlighted how DCE-MRI helps differentiate tumor recurrence from treatment-related pseudo-progression in brain tumors, directly influencing treatment decisions and follow-up schedules. A 2026 study in BMC Medical Imaging found that an MPI-first pathway before coronary angiography reduced cardiac events and lowered first-visit costs from USD 1,389 to USD 718 per patient in China.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Contrast agent safety and renal risk scrutiny | -0.6% | Global, most acute in CKD-prevalent aging populations in Europe, North America, APAC | Short term (≤ 2 years) |

| Workflow fragmentation across PACS, RIS, and multi-vendor ecosystems | -0.5% | Global, most pronounced in mid-sized health systems in North America and Western Europe | Medium term (2-4 years) |

| High capital and subscription cost of advanced perfusion software | -0.4% | Developing markets in MEA, South America, tier-2 and tier-3 cities in APAC | Long term (≥ 4 years) |

| Limited access to trained radiologists and imaging technologists | -0.3% | APAC, MEA, South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Contrast Agent Safety and Renal Risk Create Sustained Clinical Friction

Contrast administration remains a significant challenge in the perfusion radiology market, as many patients requiring urgent perfusion imaging also face renal risks or have a history of adverse reactions. CT Perfusion relies on iodinated contrast, while MRI perfusion raises concerns about gadolinium exposure, ensuring both methods undergo intense clinical scrutiny. This scrutiny, particularly for elderly patients and those with chronic kidney disease, slows adoption despite the acknowledged diagnostic value of perfusion imaging. Additionally, software supporting automated dosing recommendations faces stricter regulatory scrutiny. Although research into contrast-free methods is advancing, with non-contrast CT showing promise through generative AI models, contrast-related challenges will persist in the near term due to the time required for validation, workflow adjustments, and building clinical trust.

Workflow Fragmentation Limits Scalable Deployment Across Multi-Site Networks

Workflow fragmentation continues to impede the perfusion radiology market. Acquisition hardware, PACS, RIS, and clinical decision support systems often lack seamless integration in hospital environments. Site-specific validation for standalone AI tools adds time and cost, delaying deployment beyond pilot phases. Integrated vendors hold an advantage, as their ecosystems align scanning, archiving, viewing, and analysis tools more efficiently. Accreditation and payment regulations further complicate matters, requiring alignment of modality-specific documentation before coverage activation and reimbursement. These challenges are amplified in multi-site health systems with varying equipment and staffing models, slowing scaled rollouts despite strong clinical demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Modality: CT Perfusion Leads, While MRI Shifts the Strategic Focus

In 2025, CT Perfusion held a 42.45% share, maintaining its leadership in the perfusion radiology market. Its dominance is driven by speed, widespread scanner availability, and seamless integration into emergency stroke workflows, where timely imaging significantly impacts treatment decisions. Hospitals' adoption of 60-second whole-brain acquisition on advanced 512-slice systems further strengthened this position, enabling simultaneous scanning with CTA for acute cerebrovascular cases. Nuclear medicine perfusion remains critical in cardiology and oncology, offering quantitative flow assessments that surpass anatomical evaluations. Doppler and echocardiography-based perfusion continue to be relevant in cost-sensitive cardiac settings and community care environments lacking CT or MRI infrastructure.

MRI Perfusion is projected to grow at a 7.25% CAGR through 2031, making it the fastest-growing modality in the perfusion radiology market. Its advantages include radiation-free imaging and superior soft-tissue characterization, making it essential for oncology follow-ups, pediatric cases, and long-term neurological evaluations. Research at Erlangen is advancing the integration of perfusion measurements and image fusion into multiparametric brain tumor MRIs, enhancing therapy monitoring and differential diagnosis. In 2025, Philips demonstrated that automating scan planning and perfusion quantification within a unified workflow simplifies cardiac MRI scaling. This trend indicates a shift toward routine MRI adoption beyond specialized centers.

By Application: Cardiology Anchors Revenue, Oncology Raises Growth Expectations

In 2025, cardiology accounted for 48.55% of the perfusion radiology market, driven by the global reliance on myocardial perfusion imaging for coronary artery disease diagnosis, risk assessment, and post-intervention follow-ups. Improved payment structures in 2025 and 2026 enhanced the economic viability of advanced radiopharmaceuticals and PET blood flow quantifications in outpatient settings, encouraging investments in cardiac perfusion capabilities. This reimbursement environment is steering providers toward advanced cardiac pathways and driving demand for integrated solutions combining imaging systems, radiotracers, and post-processing tools.

Oncology is expected to grow at a 6.55% CAGR through 2031, making it the fastest-expanding application in the market. Rising demand for perfusion metrics to monitor therapy response, especially in cases where vascular changes precede structural alterations, is driving growth. DCE-MRI biomarkers are aiding in distinguishing tumor recurrence from treatment-induced pseudo-progression, emphasizing the importance of repeat perfusion assessments in brain tumor management. Other fields, including neurology, pulmonology, transplantation, and emergency medicine, are expanding the clinical base, with standardized CT perfusion protocols becoming critical in stroke-receiving institutions.

By End User: Hospitals Retain Share, While Imaging Centers Accelerate

In 2025, hospitals held 59.89% of the perfusion radiology market, reflecting their dominance in high-end imaging and their central role in acute stroke and cardiac pathways. Their stronghold is attributed to the need for immediate access to perfusion tools for thrombectomy triage, cardiac evaluations, and urgent oncology imaging. Hospitals remain the primary venues for deploying integrated scanners, software, and therapeutic workflows, supported by the largest budgets and the broadest use cases. Academic and research institutions, while holding a smaller share, play a critical role in validating new methods before commercial adoption.

Diagnostic Imaging Centers are projected to grow at a 6.88% CAGR through 2031, making them the fastest-growing end-user segment. Their growth is driven by per-scan software licensing models that reduce upfront costs and align with multi-site outpatient operations. Payer pressure to shift procedures to cost-effective settings and the availability of unit-dose PET tracers are further enabling advanced cardiac perfusion in outpatient networks. This trend is creating opportunities for outpatient centers to combine volume, software efficiency, and specialized imaging under a streamlined capital model.

Geography Analysis

In 2025, North America held a dominant 40.25% share of the perfusion radiology market, with the U.S. leading due to advanced stroke centers, AI-driven imaging software, and strong payment support for nuclear and cardiac perfusion. Enhanced reimbursement for radiopharmaceuticals and PET imaging encourages providers to expand capacity and adopt complex workflows. Policy clarity accelerates the transition from equipment purchase to routine use, linking capital investments to clearer revenue models. Europe, particularly Germany, the U.K., and France, serves as a key clinical validation hub, with academic centers standardizing newer perfusion methods.

Asia-Pacific is projected to grow at an 8.12% CAGR through 2031, making it the fastest-growing region in the perfusion radiology market. Countries like China, India, Japan, South Korea, and Australia are driving growth through a combination of disease burdens, hospital investments, and digital healthcare adoption. In China, hospitals are integrating AI-driven perfusion post-processing alongside scanner expansions, streamlining stroke diagnoses and improving workflow consistency. This trend reflects a maturing market in Asia-Pacific, with advancements in workflow sophistication and hardware depth supporting long-term adoption.

The Middle East, Africa, South America, and parts of Asia-Pacific exhibit clear demand for perfusion radiology despite smaller revenue contributions. GCC countries are integrating premium imaging infrastructure into tertiary hospitals, advancing cardiac PET and CT perfusion. Brazil and South Africa act as regional leaders with more developed diagnostic imaging networks. However, challenges like reimbursement fragmentation, high import costs, and low radiologist density hinder broader adoption. These constraints create opportunities for cloud-based and subscription models, reducing on-site expenses and catering to less dense clinical networks.

Competitive Landscape

The perfusion radiology market exhibits moderate concentration at the hardware level, while software and AI remain more fragmented, creating a layered competitive structure. Siemens Healthineers, GE HealthCare, and Philips dominate imaging systems, while Bayer AG, Bracco Imaging, Guerbet, and Lantheus Holdings strengthen their positions with contrast agents and radiopharmaceuticals. Buyers now prioritize managing the entire clinical workflow, from acquisition to treatment support, over comparing individual scanners or software. Vendors that streamline processes, reduce transfer points, and accelerate clinical actions in stroke, cardiac, and oncology use cases are increasingly favored. Algorithm depth, post-processing speed, and integration quality are becoming as critical as hardware in procurement decisions.

Siemens Healthineers enhanced its market position in May 2026 through a global partnership with Cercare Medical, integrating Syngo DynaCT Multiphase with Cercare Medical's Neurosuite for angio-suite perfusion analysis. This collaboration focuses on direct-to-angio stroke workflows, reducing transfer steps for acute cases. GE HealthCare launched Flyrcado in 2025 and expanded cardiac PET MPI access in 2026, aligning radiopharmaceutical supply with imaging platform growth. Philips advanced its cardiac MRI workflow in 2025 by integrating SmartHeart and CardiacQuant Perfusion, improving automation and quantitative myocardial assessment. These developments highlight the market's shift toward tighter workflow ownership rather than hardware upgrades alone.

HeartFlow demonstrates that software-driven companies can scale effectively without hardware ownership, leveraging its coronary assessment base and preparing for a 2025 public market entry. Community hospitals and emerging markets demand lighter deployment models, creating opportunities for subscription-based analytics and cloud solutions. Real-time perfusion monitoring in interventional suites remains a growth area, despite early solutions targeting this workflow. Regulatory requirements like FDA 510(k) clearance and CE marking increase entry costs, favoring established players. However, the steady pace of AI clearances ensures the market remains dynamic, with potential shifts driven by platforms offering superior clinical performance or seamless workflow integration.

Perfusion Radiology Industry Leaders

GE HealthCare Technologies Inc.

Koninklijke Philips N.V.

Siemens Healthineers AG

Canon Medical Systems Corporation

Bracco Imaging S.p.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Cercare Medical secured FDA 510(k) clearance for its Cone-Beam CT Perfusion solution, enabling real-time perfusion assessment during neurointerventional procedures and addressing the "no-reflow" phenomenon without patient transfer.

- May 2026: Cercare Medical and Siemens Healthineers collaborated to integrate CBCT perfusion and metabolic imaging into the angio suite, streamlining acute stroke care with CE-marked and FDA-cleared solutions.

- May 2026: GE HealthCare highlighted expanded cardiac PET MPI capabilities, including the Flyrcado unit-dose model, to drive adoption in community and mobile imaging settings.

- February 2026: Lantheus Holdings reported USD 1.54 billion in 2025 revenue, with PYLARIFY contributing USD 989.1 million, and expanded its PET radiodiagnostics pipeline through acquisitions.

- August 2025: GE HealthCare introduced the Vivid Pioneer, an advanced AI-powered cardiovascular ultrasound system with CE Mark and FDA clearance, targeting cardiac perfusion applications.

Global Perfusion Radiology Market Report Scope

As per the scope of the report, perfusion radiology, often called perfusion imaging, is a medical imaging technique that measures blood flow at the microscopic tissue level (capillaries). It helps doctors quickly locate tissue damage, stroke risks, and tumor activity.

The perfusion radiology market is segmented by modality, application, end-user, and geography. By modality, the market includes CT perfusion, MRI perfusion, nuclear medicine perfusion, and Doppler and echocardiography-based perfusion. By application, the market is segmented into neurology, cardiology, oncology, pulmonology, transplantation, and emergency medicine. By end-user, the market is categorized into hospitals, diagnostic imaging centers, ambulatory surgical centers, and academic and research institutes. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| CT Perfusion |

| MRI Perfusion |

| Nuclear Medicine Perfusion |

| Doppler and Echocardiography-Based Perfusion |

| Neurology |

| Cardiology |

| Oncology |

| Pulmonology |

| Transplantation |

| Emergency Medicine |

| Hospitals |

| Diagnostic Imaging Centers |

| Ambulatory Surgical Centers |

| Academic and Research Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Modality | CT Perfusion | |

| MRI Perfusion | ||

| Nuclear Medicine Perfusion | ||

| Doppler and Echocardiography-Based Perfusion | ||

| By Application | Neurology | |

| Cardiology | ||

| Oncology | ||

| Pulmonology | ||

| Transplantation | ||

| Emergency Medicine | ||

| By End User | Hospitals | |

| Diagnostic Imaging Centers | ||

| Ambulatory Surgical Centers | ||

| Academic and Research Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the 2026 to 2031 growth outlook for perfusion radiology?

The perfusion radiology market stands at USD 3.20 billion in 2026 and is forecast to reach USD 4.24 billion by 2031 at a 5.8% CAGR, supported by wider use in stroke, cardiology, and oncology workflows.

Which modality currently leads revenue generation?

CT Perfusion led with 42.45% share in 2025 because it fits emergency workflows, offers high speed, and aligns well with stroke triage and one-stop scanning protocols.

Which modality is expanding the fastest through 2031?

MRI Perfusion is projected to grow at 7.25% CAGR through 2031, driven by radiation-free imaging, stronger soft-tissue characterization, and rising use in oncology and chronic neurology follow-up.

Why does cardiology remain the largest clinical use case?

Cardiology held 48.55% share in 2025 due to the high global volume of myocardial perfusion imaging and improving reimbursement support for advanced PET and radiopharmaceutical-based pathways.

Which end-user group is growing the fastest?

Diagnostic Imaging Centers are forecast to grow at 6.88% CAGR through 2031 as per-scan software models, outpatient volume shifts, and unit-dose PET tracers lower deployment barriers.

Which region offers the strongest near-term expansion opportunity?

Asia-Pacific is expected to grow at 8.1% CAGR through 2031 as China, India, Japan, South Korea, and Australia add imaging capacity and adopt AI-enabled perfusion workflows more broadly.

Page last updated on: