Americas Interventional Radiology Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

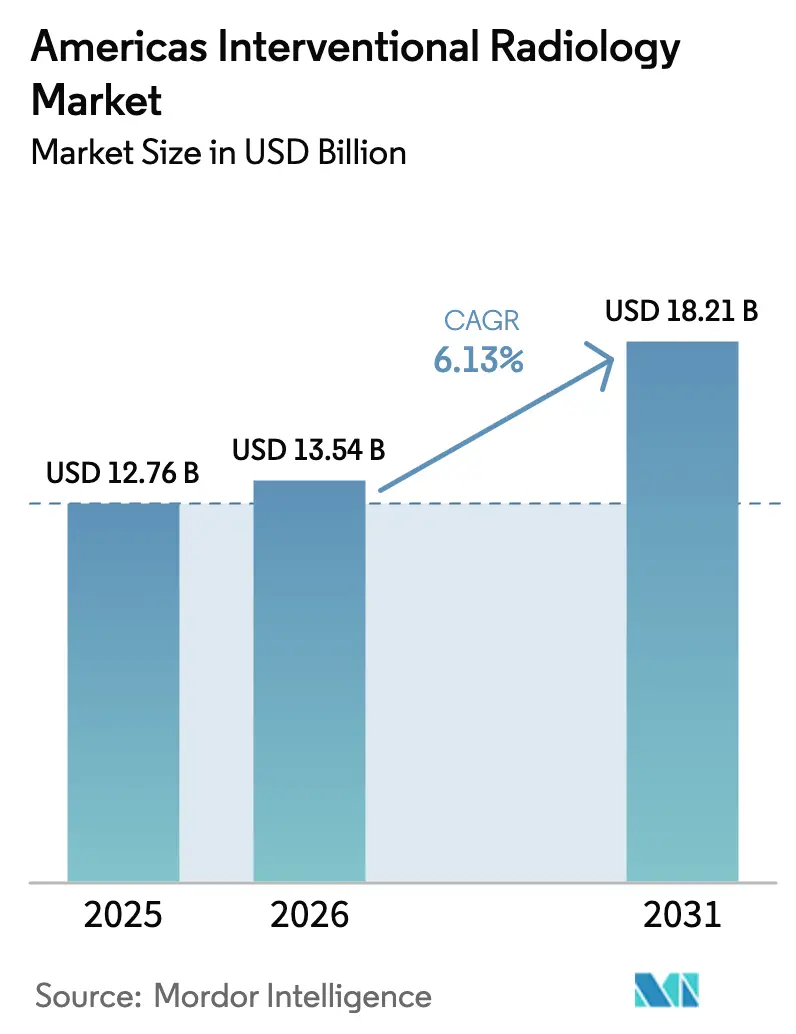

| Base Year Market Size (2025) | USD 12.76 Billion |

| Market Size (2026) | USD 13.54 Billion |

| Market Size (2031) | USD 18.21 Billion |

| Growth Rate (2026 - 2031) | 6.13% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Americas Interventional Radiology Market Analysis by Mordor Intelligence

Americas interventional radiology market size in 2026 is estimated at USD 13.54 billion, growing from 2025 value of USD 12.76 billion with 2031 projections showing USD 18.21 billion, growing at 6.13% CAGR over 2026-2031. Robust adoption of photon-counting CT, artificial intelligence–enabled guidance, and pulsed field ablation systems is shortening procedure times, lowering radiation exposure, and improving therapeutic precision, which together uplift procedure volumes across cardiovascular and oncology indications. Payers’ shift toward value-based reimbursement rewards the minimally-invasive profile of interventional radiology while also encouraging site-of-service migration toward ambulatory settings. Persistent workforce shortages in Latin America, coupled with the high capital cost of hybrid suites, restrain immediate scale-up but simultaneously create openings for equipment financing and training collaborations.

Key Report Takeaways

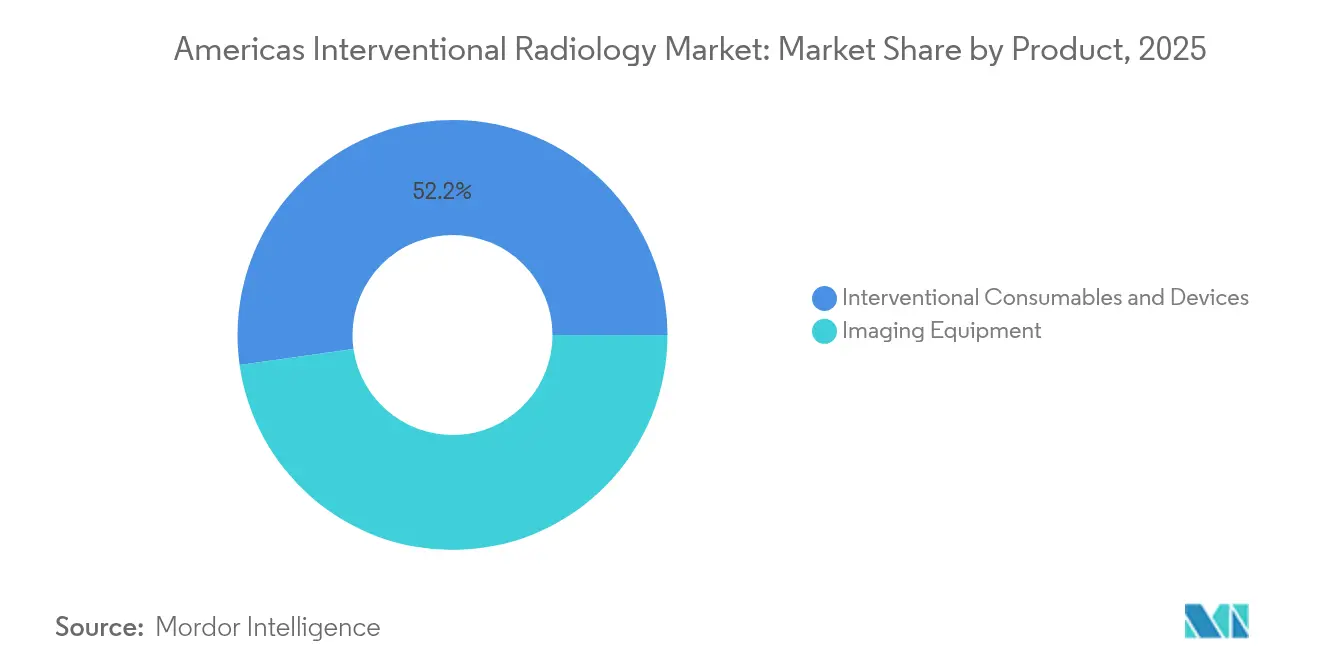

- By product, consumables and devices held 52.22% of America’s interventional radiology market share in 2025, whereas imaging equipment is advancing at a 6.73% CAGR through 2031.

- By application, cardiology led with 38.27% revenue share of America’s interventional radiology market size in 2025, while oncology interventions are projected to climb at 7.22% CAGR to 2031.

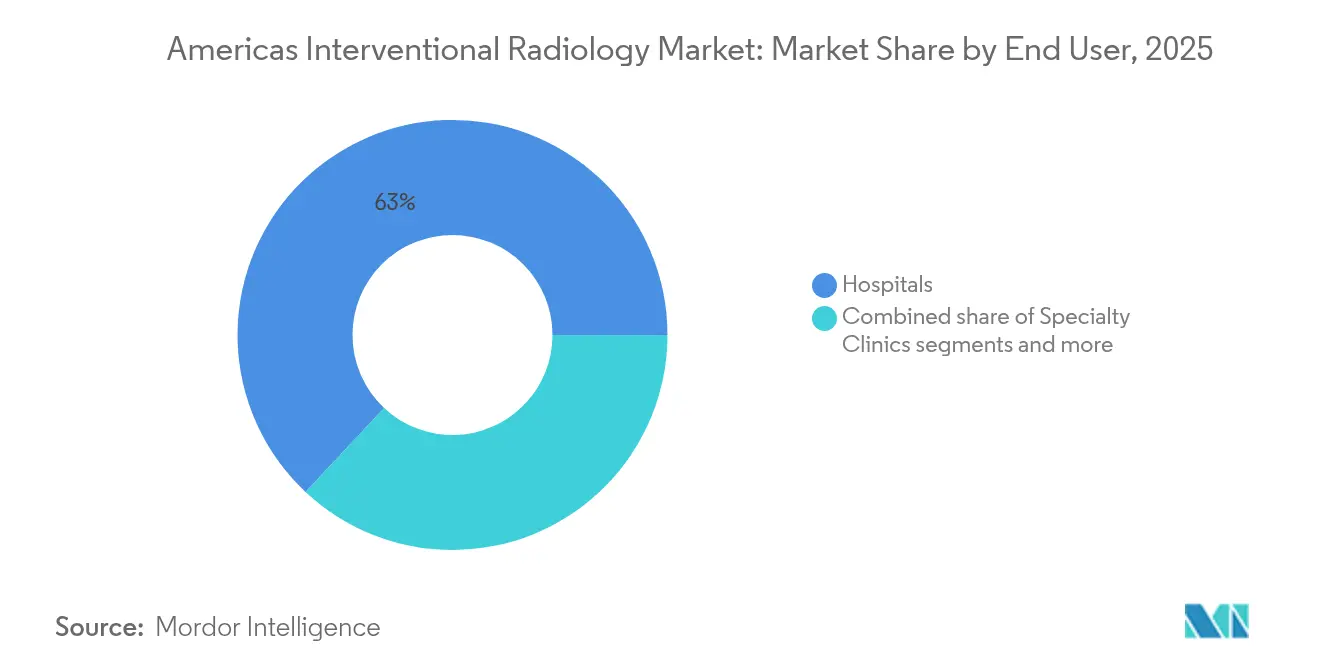

- By end user, hospitals commanded 63.02% share of America’s interventional radiology market in 2025; contract development and manufacturing organizations are set to post the fastest 7.76% CAGR through 2031.

- By geography, North America accounted for 92.90% of America’s interventional radiology market size in 2025 and is forecast to grow at 8.45% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Americas Interventional Radiology Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing burden of chronic cardiovascular & oncological diseases | +1.8% | Global, with highest impact in North America | Long term (≥ 4 years) |

| Technological advances in IR imaging (photon-counting CT, AI, AR) | +1.2% | North America & EU, spill-over to Latin America | Medium term (2-4 years) |

| Rapid expansion of office-based labs (OBL) & ASCs in the Americas (under-reported) | +0.9% | North America core, early adoption in Brazil | Short term (≤ 2 years) |

| Favorable reimbursement revisions for IR codes in U.S. and Brazil | +0.7% | United States and Brazil primarily | Short term (≤ 2 years) |

| Shift to value-based care favouring minimally-invasive IR over surgery (under-reported) | +0.5% | North America primarily, gradual expansion to Latin America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Burden of Chronic Cardiovascular & Oncological Diseases

Hypertension prevalence is projected to climb from 51.2% to 61.0% by 2050, and diabetes from 16.3% to 26.8%, adding a steady pipeline of complex cases amenable to catheter-based interventions. The aging population magnifies disease incidence, while patient preference for shorter recovery dovetails with hospital efforts to lower length of stay. Together these factors increase case volumes for peripheral angioplasty, renal denervation, and tumor embolization. Consequently, America’s interventional radiology market benefits from structural tailwinds that consistently replenish procedural demand.

Technological Advances in IR Imaging (Photon-Counting CT, AI, AR)

Photon-counting detector CT enables higher spatial resolution and intrinsic spectral separation, which improves tissue contrast while cutting radiation dose compared to energy-integrating systems, thereby elevating diagnostic certainty in complex vascular interventions. Clinical studies show vessel-sharpness ratings of 134.7 HU/mm versus 100.9 HU/mm on conventional scanners, facilitating precise device deployment in coronary and neurovascular procedures. AI-enabled robotic platforms overlay real-time trajectory guidance, automate wire manipulation, and reduce fluoroscopy time by up to 56%, which eases radiation safety concerns for staff and patients. Augmented-reality head-mounted displays further shorten learning curves for complex ablation or embolization. Early adopters realize competitive gains through lower complication rates and higher throughput, reinforcing the technological arms race within America’s interventional radiology market.

Rapid Expansion of Office-Based Labs (OBLs) & ASCs in the Americas

More than 700 OBLs were operational in the United States in 2021, and their number is projected to grow at 7.5% annually through 2030 on the strength of bundled payments and patient preference for community-based care. Medicare data confirm that 6,100 ASCs handled 3.3 million beneficiaries in 2022, with procedure volume per beneficiary up 2.8% year on year. Outpatient sites typically deliver 35% lower episode costs than hospital outpatient departments, creating strong payer incentives for migration of angioplasty, uterine fibroid embolization, and port placements. The resulting redistribution of caseload supports double-digit equipment sales into small footprints that rely on compact C-arms and ultrasound guidance. These dynamics underpin near-term revenue growth in America’s interventional radiology market.

Shift to Value-Based Care Favoring Minimally-Invasive IR Over Surgery

The Centers for Medicare & Medicaid Services approved transitional pass-through payment for Medtronic’s Symplicity Spyral renal denervation catheter effective January 2025, signifying regulatory endorsement for novel catheter therapies that reduce downstream hospitalization costs. The 2025 CPT update introduced 270 new codes, including MRI-guided ablation and complex embolization bundles that streamline billing and raise professional fees for image-guided care. Health systems see shorter length of stay and fewer complications with percutaneous options, which increases alignment between clinical outcomes and payment quality metrics. Consequently, procedural referrals tilt toward interventional suites, stimulating durable adoption across vascular, oncologic, and neurologic lines within America’s interventional radiology market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital cost of IR suites & advanced imaging modalities | -1.1% | Global, with acute impact in Latin America | Medium term (2-4 years) |

| Shortage of trained interventional radiologists in Latin America | -0.8% | Latin America primarily, spillover to rural North America | Long term (≥ 4 years) |

| Post-COVID capex deferrals by hospitals (under-reported) | -0.6% | Global, with highest impact in Latin America | Short term (≤ 2 years) |

| Stringent ANVISA-level approval timelines delaying device launches | -0.4% | Latin America, primarily Brazil and Argentina | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital Cost of IR Suites & Advanced Imaging Modalities

Photon-counting CT scanners, robotic C-arms, and hybrid operating rooms each require outlays above USD 2 million, with entire suite buildouts reaching USD 5 million, which strains hospital balance sheets already operating at 1.2% median operating margins. Annual service contracts consume 15 – 20% of purchase price, while software upgrades add incremental costs that small systems struggle to absorb. Latin American hospitals face 30 – 40% price premiums driven by import tariffs and currency volatility, raising barriers to adoption. Deferred-payment leasing and refurbished equipment programs are expanding, yet premium financing charges dilute investment returns. As a result, America’s interventional radiology market encounters localized slowdowns where capital intensity outweighs clinical demand.

Shortage of Trained Interventional Radiologists in Latin America

Only 15.5% of U.S. counties have an interventional radiologist, and 31.2% of the population lacks direct access to interventional expertise, illustrating the depth of workforce scarcity. Latin American training programs face limited fellowship slots, outdated curricula, and funding gaps, thereby prolonging skill deficits despite growing disease burden. The practicing IR cohort in the United States shrank 7% from 2013 to 2020, even as evaluation and management claims climbed 35%, indicating widening imbalances between demand and supply. Workforce expansion lags six years behind fellowship enrollment because of training duration, locking in shortages that constrain procedural capacity across underserved geographies within America’s interventional radiology market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Consumables Drive Revenue While Equipment Spurs Innovation

Consumables and devices accounted for 52.22% of America’s interventional radiology market share in 2025, buoyed by high procedure frequency and single-use mandates that accelerate replacement cycles. Stents, catheters, guidewires, and embolic agents dominate hospital procurement lists because multifaceted procedures require multiple SKUs per case. The stent subsegment gained further traction after Abbott secured FDA clearance for its dissolving Esprit BTK scaffold for below-the-knee disease, a milestone that reshapes peripheral revascularization options. Biopsy and thrombectomy kits also expand as stroke and oncology protocols emphasize early intervention.

Imaging equipment represents the fastest-growing category at a 6.73% CAGR through 2031 as facilities upgrade to photon-counting CT, self-driving C-arms, and AI-integrated MRI that mitigate radiologist shortages and enhance workflow. Hospitals leverage financing partnerships to acquire comprehensive platforms that bundle scanners, software, and analytics services, improving lifetime value. AI-rich ultrasound systems are penetrating office-based labs due to portability and rapid learning curves, while angiography suites adopt radiation-free light-based navigation that can slash fluoroscopy exposure by over half. These trends drive a premium replacement cycle that anchors long-term expansion in America’s interventional radiology market.

By Application: Cardiology Commands the Present, Oncology Fuels the Future

Cardiology dominated America’s interventional radiology market size with 38.27% in 2025, supported by entrenched reimbursement pathways and decades of evidence favoring catheter-based treatments over open surgery for coronary and structural heart disease. Pulsed field ablation systems from Medtronic, Boston Scientific, and Abbott have democratized atrial fibrillation treatment by shortening procedure time and reducing collateral tissue injury, which stimulates incremental device sales. Hypertension trials using renal denervation catheters show sustained blood pressure reduction, adding a new patient pool for interventional treatment.

Oncology interventions are expanding at 7.22% CAGR, the fastest among clinical segments, as image-guided tumor ablation, chemoembolization, and selective internal radiation therapy align with precision medicine strategies that seek localized high-dose delivery with minimal systemic toxicity. Theranostic workflows that integrate diagnostic imaging and localized therapy elevate scanner utilization and consumable turnover, fostering a virtuous cycle for vendors. The rising incidence of hepatocellular carcinoma and lung metastases, combined with improved survival, ensures sustained procedural demand for ablation needles, microspheres, and drug-eluting beads.

By End User: Hospitals Anchor Complexity, Specialized Centers Accelerate Volume

Hospitals retained a 63.02% share of America’s interventional radiology market in 2025, justified by their ability to aggregate multidisciplinary expertise, intensive care backup, and advanced imaging suites necessary for high-risk cases. Complex stroke thrombectomies, large-vessel aneurysm repairs, and pediatric interventions remain hospital mainstays. Moreover, academic centers lead early adoption of photon-counting CT and robotic angiography, driving demand for vendor-bundled service contracts.

Contract development and manufacturing organizations, office-based labs, and ambulatory surgical centers are registering the highest growth at 7.76% CAGR because they capture routine vascular access, dialysis interventions, and pain management procedures under cost-efficient settings. These sites rely on compact fluoroscopy and ultrasound platforms and favor disposable kits that streamline turnover. Specialty clinics focusing on endovascular limb salvage and uterine fibroid embolization thrive on targeted marketing and bundled payment contracts that reward high patient satisfaction. This multisite delivery ecosystem diversifies revenue streams and underpins the long-run scalability of America’s interventional radiology market.

Geography Analysis

North America generated 92.90% of total revenue in 2025 and is forecast to expand at 8.45% CAGR through 2031 as Medicare Advantage enrollment rises and CPT code revisions improve practice economics. The United States leads photon-counting CT installations and has already performed first-in-human procedures with AI-guided transcatheter valves, reinforcing technological leadership. Canada benefits from federal investments in health-system modernization that include dedicated funding for ambulatory stroke services and PET/CT expansion.

South America remains under-penetrated yet strategically important. Brazil accelerated ANVISA approvals by recognizing FDA and Health Canada clearances, which cut regulatory timelines to 6-9 months for qualified devices, supporting faster market entry for stents, ablation systems, and catheter technologies. Currency headwinds and import taxes still inflate equipment costs, but vendor-financed leasing and refurbished platforms help mitigate barriers. Argentina’s economic volatility tempers near-term purchasing power; however, rising private-sector investments in vascular care highlight latent demand for cost-effective, minimally-invasive solutions.

The remainder of South America faces infrastructure gaps and workforce shortages but demonstrates strong appetite for professional education. Cross-border training programs reveal that over 80% of Latin American radiologists prioritize interventional skill acquisition, pointing to future volume growth once capital and regulatory hurdles ease. International equipment vendors with turnkey training, financing, and service bundles are likely to gain early footholds as socioeconomic conditions stabilize, enabling broader expansion of America’s interventional radiology market.

Competitive Landscape

America’s interventional radiology market hosts a moderately concentrated field in which consumable giants Boston Scientific, Medtronic, and Abbott compete alongside imaging leaders GE HealthCare, Philips, and Siemens Healthineers for end-to-end procedural mindshare. FDA authorization of three pulsed field ablation systems in 2024 reignited competitive dynamics similar to early stent battles, prompting rapid share realignment as hospitals evaluate efficacy, workflow, and pricing differentials. Device firms broaden portfolios through tuck-in acquisitions, as shown by Teleflex purchasing BIOTRONIK’s vascular intervention unit for USD 820 million to gain instant coronary balloon scale.

Emerging white-space centers on AI-driven decision support, non-fluoroscopic navigation, and value-based service contracting. Patent filings in robotic catheter guidance and machine-learning-enabled ablation climbed 40% annually since 2022, signaling intense R&D investment by incumbents and venture-backed entrants. Vendors that can demonstrate quantifiable outcome gains and document cost avoidance secure preferential placement on hospital capital budgets, a trend that reinforces competitive pressure yet benefits purchasers through broader solution choice within America’s interventional radiology market.

Americas Interventional Radiology Industry Leaders

Carestream Health

GE Healthcare

Siemens Healthineers AG

Canon Medical Systems Corporation

FUJIFILM Holdings Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Stryker launched the Artix Thrombectomy System combining aspiration with mechanical removal for peripheral arterial thrombus management

- February 2025: Teleflex agreed to acquire BIOTRONIK’s Vascular Intervention business for EUR 760 million, expanding its coronary and peripheral footprint

Americas Interventional Radiology Market Report Scope

As per the scope of the report, interventional radiology is a medical specialty that employs minimally invasive procedures guided by medical imaging technologies to diagnose, treat, and manage a wide range of medical conditions. It involves the use of small instruments, catheters, and needles to access specific areas of the body, often through small incisions or natural body openings, thus reducing the need for traditional open surgery. By utilizing advanced imaging techniques like X-rays, fluoroscopy, ultrasound, CT scans, or MRI, interventional radiologists can visualize internal structures and blood vessels to perform precise and targeted interventions. The Americas Interventional Radiology Market is Segmented by Product (MRI Systems, Ultrasound Imaging Systems, CT Scanners, Angiography Systems, Fluoroscopy Systems, Biopsy Devices, and Other Products), Application (Cardiology, Urology and Nephrology, Oncology, Gastroenterology, and Other Applications), and Geography (North America and South America). The report offers the value (in USD million) for the above segments.

| Imaging Equipment | MRI Systems |

| CT Scanners | |

| Ultrasound Imaging Systems | |

| Angiography Systems | |

| Fluoroscopy Systems | |

| Interventional Consumables & Devices | Stents |

| Catheters & Guidewires | |

| Angioplasty Balloons | |

| Embolization & Thrombectomy Devices | |

| Biopsy Devices | |

| IVC Filters & Accessories |

| Cardiology |

| Oncology |

| Urology & Nephrology |

| Gastroenterology |

| Neurology |

| Hospitals |

| Office-Based Labs (OBLs) / Ambulatory Surgical Centers (ASCs) |

| Specialty Clinics |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Imaging Equipment | MRI Systems |

| CT Scanners | ||

| Ultrasound Imaging Systems | ||

| Angiography Systems | ||

| Fluoroscopy Systems | ||

| Interventional Consumables & Devices | Stents | |

| Catheters & Guidewires | ||

| Angioplasty Balloons | ||

| Embolization & Thrombectomy Devices | ||

| Biopsy Devices | ||

| IVC Filters & Accessories | ||

| By Application | Cardiology | |

| Oncology | ||

| Urology & Nephrology | ||

| Gastroenterology | ||

| Neurology | ||

| By End User | Hospitals | |

| Office-Based Labs (OBLs) / Ambulatory Surgical Centers (ASCs) | ||

| Specialty Clinics | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is America’s interventional radiology market in 2026?

The market stands at USD 13.54 billion in 2026 and is forecast to reach USD 18.21 billion by 2031.

Which clinical area generates the highest procedure volume?

Cardiology leads, accounting for 38.27% of 2025 revenue, thanks to widespread use of coronary and electrophysiology interventions.

What is the fastest-growing application segment?

Oncology procedures expand at a 7.22% CAGR through 2031 as image-guided tumor ablation and chemoembolization gain momentum.

Why are office-based labs important for future growth?

OBLs and ASCs can cut episode costs by up to 35% and are growing 7.76% per year, shifting routine cases out of hospitals.

Which technology is reshaping imaging equipment demand?

Photon-counting CT coupled with AI-enabled guidance is driving a 6.73% CAGR in imaging equipment sales as facilities refresh fleets.

Page last updated on: