Intraoperative Imaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.75 Billion |

| Market Size (2031) | USD 5.43 Billion |

| Growth Rate (2026 - 2031) | 7.65% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

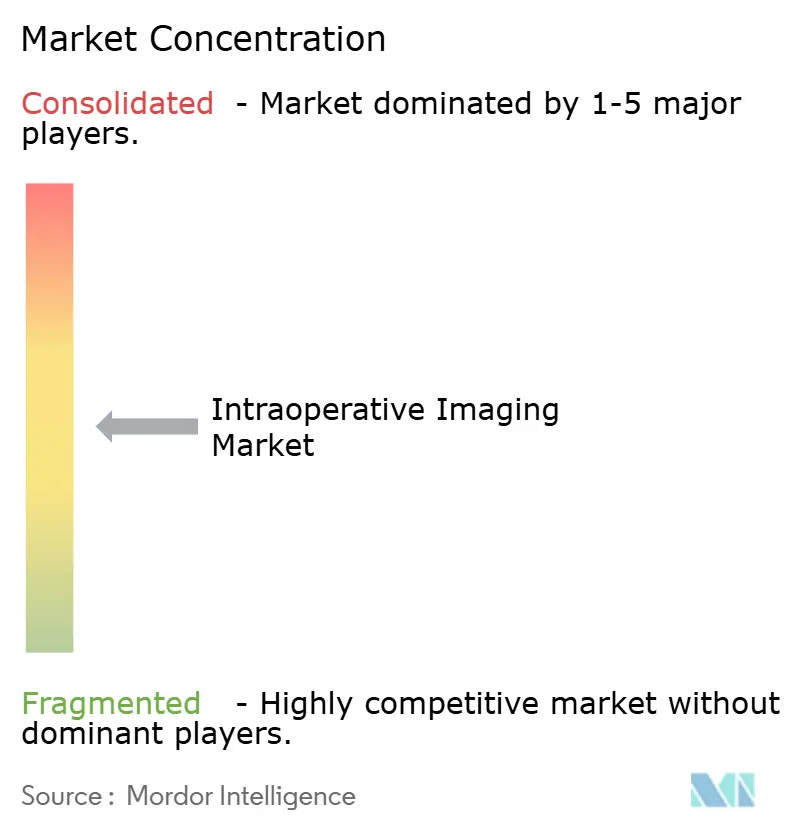

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Intraoperative Imaging Market Analysis by Mordor Intelligence

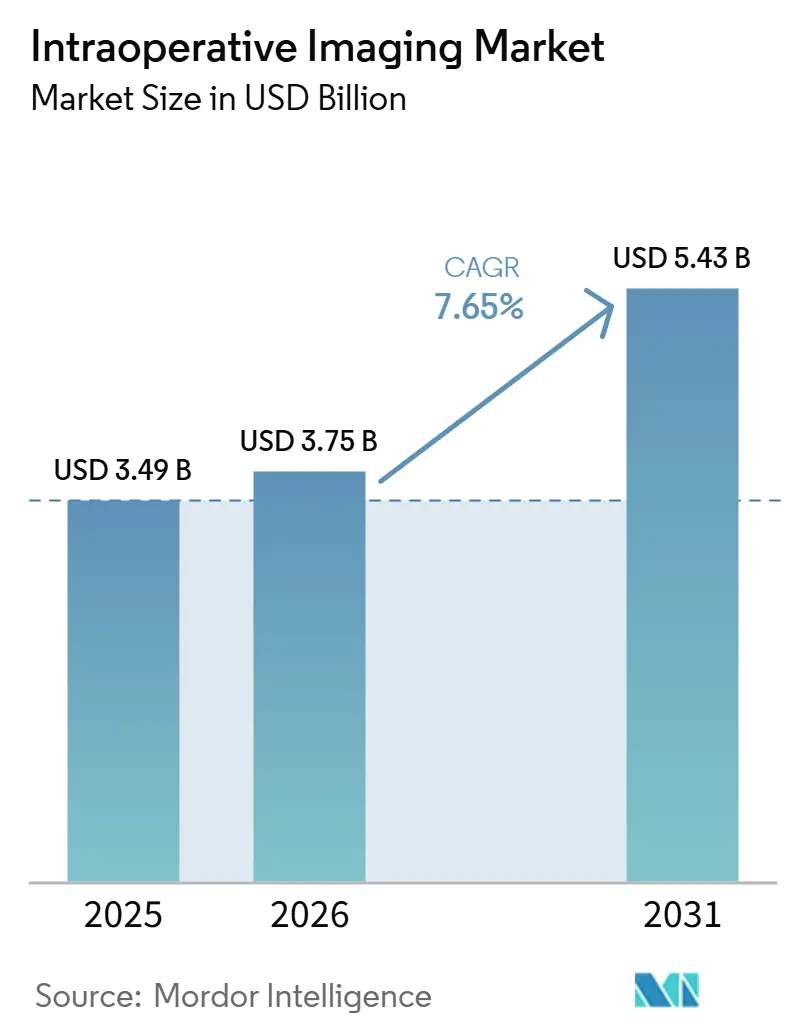

The Intraoperative Imaging Market size was valued at USD 3.49 billion in 2025 and is estimated to grow from USD 3.75 billion in 2026 to reach USD 5.43 billion by 2031, at a CAGR of 7.65% during the forecast period (2026-2031).

The intraoperative imaging market is being supported by the rising use of minimally invasive procedures, where surgeons depend more on live visualization because direct exposure is reduced, and Intuitive Surgical reported 3.15 million da Vinci procedures in 2025.[1]Intuitive Surgical, “Preliminary Fourth Quarter and Full Year 2025 Results” The intraoperative imaging market is also gaining from faster AI use inside surgical workflows, as recent peer-reviewed work and product launches show progress in image reconstruction, radiation reduction, and navigation support during live procedures. Vendor strategy is shifting toward modular upgrades and software-led revenue, and GE HealthCare’s June 2026 Allia upgrade pathway shows how manufacturers are trying to modernize installed systems without forcing full room replacement. The intraoperative imaging market also benefits from steady demand for neurosurgery, spine, cardiovascular, and hybrid OR imaging, where hospitals continue to value workflow efficiency, navigation accuracy, and room utilization over standalone hardware features.

Key Report Takeaways

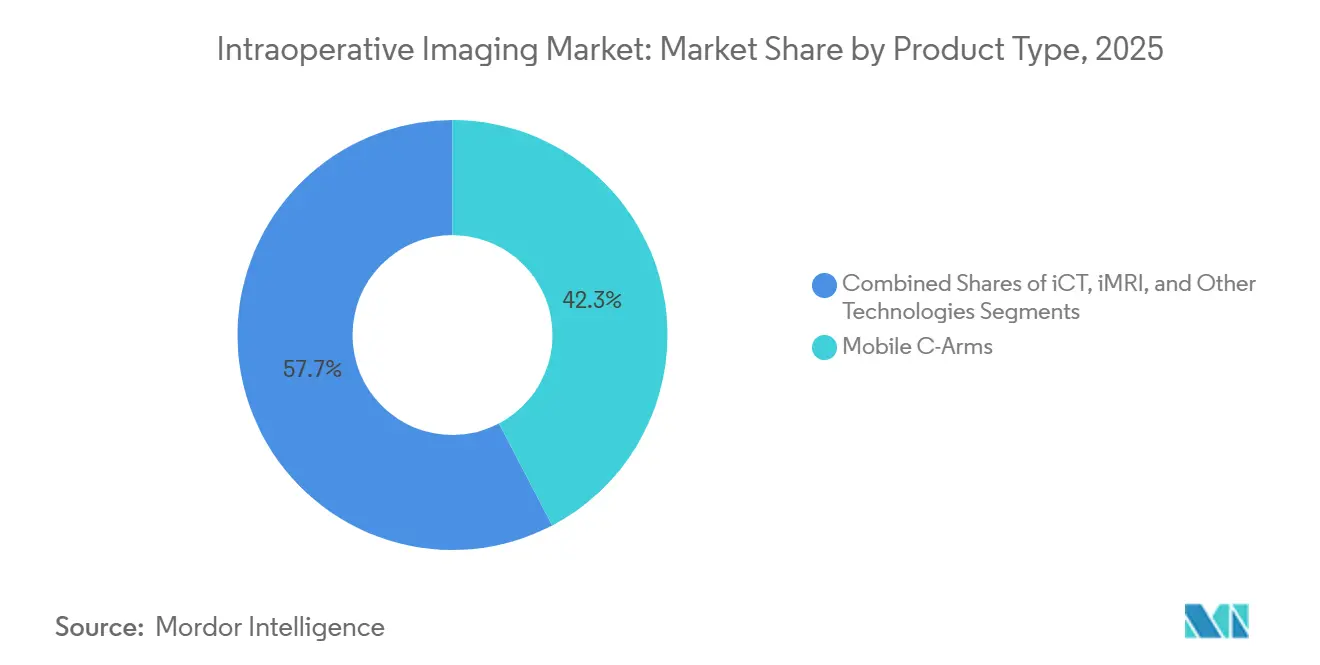

- By product type, mobile C-arms held 42.32% of the intraoperative imaging market size in 2025, while intraoperative MRI is projected to expand at a 7.78% CAGR through 2031.

- By application, neurosurgery accounted for 29.36% of revenue in 2025, while spine surgery is forecast to grow at a 7.33% CAGR through 2031.

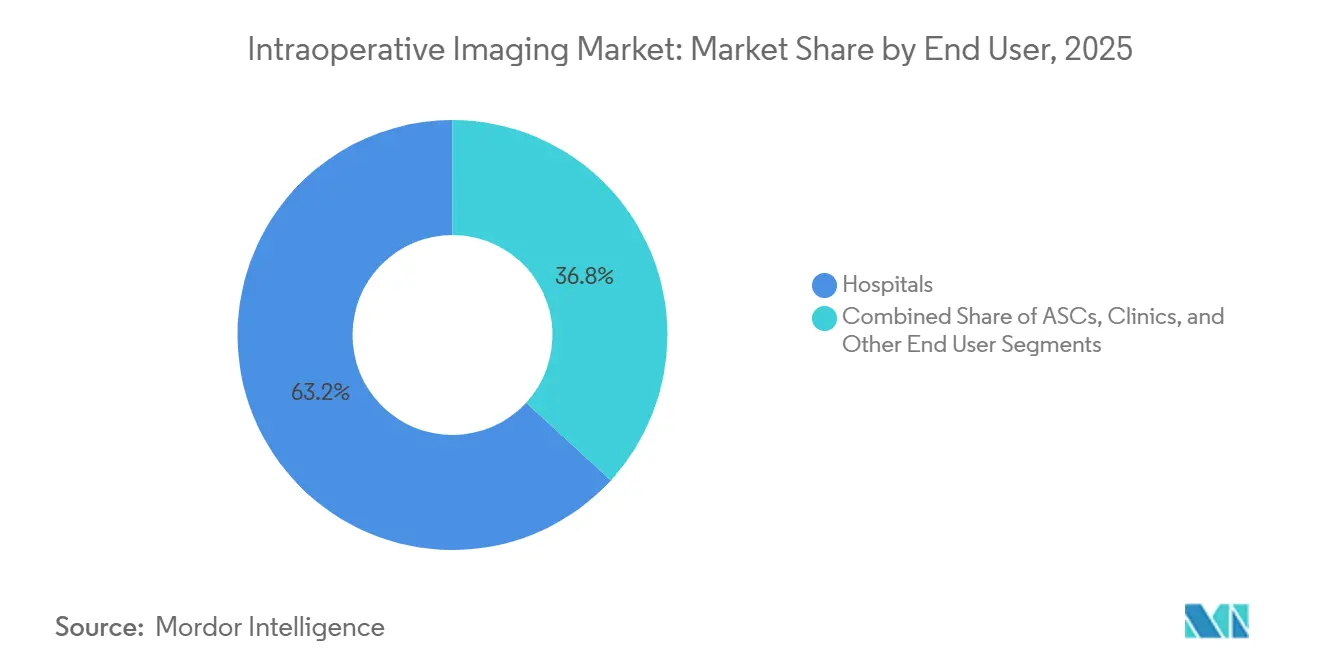

- By end user, hospitals held 63.18% of the intraoperative imaging market share in 2025, while ambulatory surgical centers are projected to grow at a 7.47% CAGR through 2031.

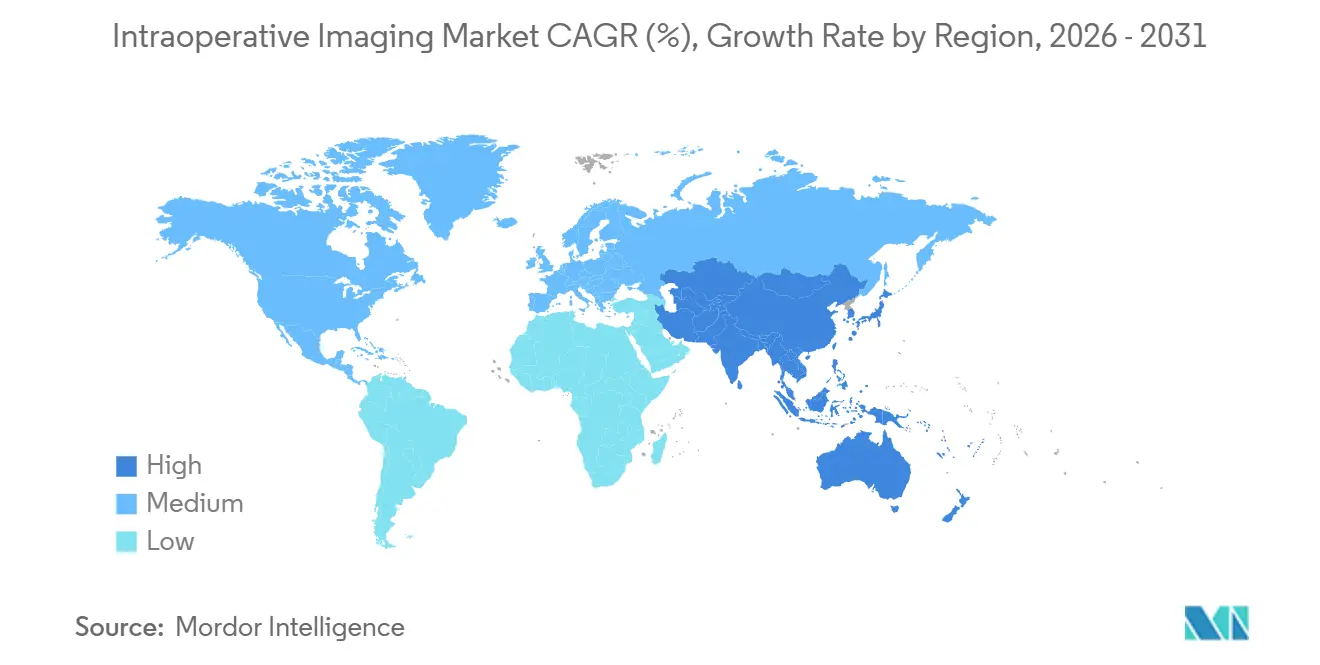

- By geography, North America represented 42.87% of revenue in 2025, while Asia-Pacific is expected to expand at a 7.73% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Intraoperative Imaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Minimally Invasive Surgery | +1.8% | Global | Short term (≤ 2 years) |

| Wider Use of Real-Time Surgical Navigation and Image Guidance | +1.6% | Global, with leading adoption in North America and Europe | Medium term (2-4 years) |

| AI-Enabled Intraoperative Decision Support | +1.4% | North America and Europe, with spill-over to APAC | Medium term (2-4 years) |

| Hybrid Operating Room Retrofit Cycles in Tertiary Hospitals | +1.1% | North America, Europe, and Japan | Medium term (2-4 years) |

| Expansion of Same-Day Complex Procedures in Ambulatory Settings | +0.9% | North America, with early gains in Australia and South Korea | Short term (≤ 2 years) |

| Increase in the Prevalence of Chronic Diseases | +0.8% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Minimally Invasive Surgery

The shift from open procedures to minimally invasive surgery remains the clearest volume driver for the intraoperative imaging market because surgeons need live imaging when the operative field is smaller and direct visualization is limited. Intuitive Surgical reported 3,153,000 da Vinci procedures in 2025, up 18% from the prior year, and it expects another 13-15% increase in 2026. That growth rate indicates that robotic and image-guided surgical capacity is still expanding faster than many hospital capital replacement cycles. A 2024 study in the Pakistan Journal of Surgical and Neurological Sciences reported that advanced intraoperative imaging reduced neurological complications to 5.3% from 19.1% and bleeding complications to 2.1% from 7.4% when compared with conventional guidance.[2]Advanced Intraoperative Imaging Techniques to Enhance Surgical Precision in Spine Procedures As hospitals place more weight on measurable outcomes and procedural efficiency, the intraoperative imaging market is likely to see continued demand from centers that want fewer complications, better navigation, and stronger surgeon confidence during technically constrained cases.

AI-Enabled Intraoperative Decision Support

AI is improving the practical value of the intraoperative imaging market by reducing the time between image acquisition and surgical interpretation. A 2026 narrative review reported that Medtronic’s FDA-cleared Spine Smart Dose protocol can reduce radiation dose by 70% versus standard O-arm 3D imaging while maintaining navigation accuracy. The same review described the X23D method, which reconstructs a 3D lumbar vertebra model from 4 intraoperative 2D X-rays in 4 seconds, making advanced navigation more accessible in sites without dedicated intraoperative CT suites. Peer reviewed studies cited in that review also showed that MRI-based synthetic CT can support pedicle screw placement safety comparable to conventional CT, which points to a future pathway with less radiation exposure. A 2025 Journal of Clinical Medicine paper further noted that AI, fluorescence, and extended reality are starting to converge into a single guidance layer, which makes AI a workflow enhancer rather than a separate add-on for the intraoperative imaging market.

Hybrid Operating Room Retrofit Cycles in Tertiary Hospitals

Hybrid operating rooms remain the highest-value setting in the intraoperative imaging market because they combine advanced imaging with open surgery access in one procedural environment. These rooms carry major capital commitments, often in the USD 2-5 million range per suite, yet hospitals continue to back them when they can improve throughput, reduce patient transfers, and support higher-acuity case mix. The intraoperative imaging market is therefore seeing growth not only from new installations, but also from retrofit demand in hospitals that already have active interventional or surgical imaging programs. GE HealthCare’s June 2026 launch of modular Allia upgrade pathways shows how vendors are pursuing this opportunity by modernizing existing interventional suites without full capital displacement. Once a hybrid room is installed, vendors also gain a longer revenue stream from software, service, and follow-on upgrades, which strengthens the commercial case for aggressive competition during the initial tender.

Expansion of Same-Day Complex Procedures in Ambulatory Settings

The movement of more complex procedures into ambulatory settings is creating a new demand layer for the intraoperative imaging market, especially for systems that are compact, fast to position, and simple to integrate. MedPAC reported that 168 new ambulatory surgical centers were certified in 2024, showing that outpatient surgical capacity is still expanding in the United States. This shift matters because many outpatient cases in orthopedics, pain, cardiovascular care, and spine still require dependable imaging even when facilities do not have room for fixed CT or MRI systems. Stryker’s October 2025 launch of IP BRAVoE reflects that change, as the platform was designed for simplified multi-device workflow and real-time decision support in hybrid OR and ASC environments. As outpatient teams stay lean and room turnover becomes more important, the intraoperative imaging market should continue to reward vendors that prioritize portability, ease of use, and workflow integration over maximum hardware complexity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital and Lifecycle Service Cost | -2.2% | Global, most acute in MEA, South America, and rural North America | Short term (≤ 2 years) |

| Reimbursement Pressure on High-Cost Imaging Procedures | -1.5% | North America and Europe | Medium term (2-4 years) |

| Sterile Workflow and OR Integration Complexity | -0.9% | Global | Short term (≤ 2 years) |

| Safety Concerns and Regulatory Hurdles | -0.7% | APAC and MEA, with EU MDR compliance in Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital and Lifecycle Service Cost

High acquisition and ownership costs remain the most visible barrier in the intraoperative imaging market, especially for modalities at the top end of the capability range. Intraoperative MRI suites can require USD 1-5 million per installation, while O-arm systems typically sit in the USD 750,000-1.2 million range, before service contracts, software licensing, and training are added. These cost layers matter because the buying decision is rarely limited to the scanner alone, and hospitals must account for room design, specialist staffing, maintenance, and downtime exposure. The result is a market where large academic systems can justify premium platforms more easily than mid-tier hospitals, rural buyers, or smaller private groups. This cost gap also favors global OEMs that can spread R&D and service infrastructure over a wider installed base, which keeps the intraoperative imaging market tilted toward scale players in the most advanced product categories.

Reimbursement Pressure on High-Cost Imaging Procedures

Reimbursement pressure narrows the addressable ceiling of the intraoperative imaging market even when clinical interest remains strong. A 2025 PubMed-indexed study found that Medicare reimbursement for imaging modalities declined substantially from 2003 through 2025, with MRI showing the steepest erosion.[3]Evolution of Medicare/Medicaid imaging reimbursements from 2003 to 2025 For high-cost intraoperative imaging, hospitals often have to absorb imaging expense inside broader surgical payment bundles, which weakens the payback case for premium platforms. This issue is most relevant for facilities that do not have the procedure mix, surgeon concentration, or financial reserves needed to support high utilization. As AI upgrades and advanced navigation become more central to vendor positioning, the intraoperative imaging market will depend even more on reimbursement models that can recognize the value of better visualization, lower revision risk, and improved operative efficiency.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Mobile C-Arms Anchor Volume as Intraoperative MRI Drives Premium Growth

Mobile C-arms held 42.32% of the intraoperative imaging market size in 2025, making them the largest product category by revenue. Their position reflects broad use across orthopedic, trauma, cardiovascular, and general surgery, where hospitals want versatile systems that fit many rooms and case types. Lower capital cost and a smaller physical footprint also make them easier to adopt than fixed systems, especially in facilities that cannot support dedicated CT or MRI suites. This keeps mobile imaging at the center of the intraoperative imaging market, particularly where hospitals are balancing utilization, room flexibility, and replacement budgets.

The rest of the product mix is moving toward tighter software and navigation integration rather than simple hardware upgrades alone. GE HealthCare’s April 2026 commercial launch of the bkActiv iUS and Medtronic Stealth AXiS digital link shows how ultrasound is gaining relevance by giving surgeons live intraoperative images alongside pre-operative MRI or CT data during cranial procedures. Intraoperative MRI is projected to grow at 7.78% CAGR through 2031, the fastest pace in the product mix, and IMRIS received FDA 510(k) clearance in August 2025 for its InVision 3T Recharge Operating Suite, which lets hospitals upgrade legacy Siemens Magnetom Verio systems to the AI-integrated Skyra Fit platform without reconstructing the facility. Canon Medical’s November 2025 FDA 510(k) clearance for Alphenix 4D CT reinforced the continuing role of intraoperative CT as a strong mid-tier modality inside the intraoperative imaging market.

By Application: Neurosurgery Leads on Share, Spine Surgery On Growth

Neurosurgery accounted for 29.36% of the intraoperative imaging market share in 2025, which kept it as the largest application segment. This leadership is tied to the way brain shift can quickly reduce the accuracy of pre-surgical planning images once the procedure begins. In that setting, surgeons rely on live imaging and navigation as a core part of the procedure rather than an optional support tool. Brainlab’s Elements 7.0 suite received FDA clearance in June 2025 for image fusion, fiber tracking 3.0, and BOLD MRI mapping, which expanded navigation intelligence into functional neurosurgery and strengthened software-led competition inside the intraoperative imaging market.

Other application groups continue to support broad revenue demand, even if they do not lead the share table. Orthopedic and trauma surgery still rely heavily on mobile fluoroscopy, while cardiovascular procedures continue to favor image guidance that can fit both hospital and ambulatory workflows. The May 2026 United States launch of the Aplio i800 EUS Premium Ultrasound System by Olympus and Canon Medical also shows how endoscopic and ultrasound-guided imaging are expanding in gastroenterology and pulmonary applications with AI-supported image enhancement. Spine surgery is projected to grow at 7.33% CAGR through 2031, and Brainlab’s September 2025 FDA 510(k) clearance for Spine Mixed Reality Navigation, together with peer reviewed evidence on MRI-derived synthetic CT for pedicle screw placement, indicates that the intraoperative imaging market is moving toward more immersive and lower-radiation guidance in this segment.

By End User: Hospitals Remain Dominant While ASCs Gain Ground

Hospitals held 63.18% of the intraoperative imaging market share in 2025, which kept them as the dominant end-user group. Their lead reflects access to complex patient volumes, stronger capital budgets, and the ability to support intraoperative CT, intraoperative MRI, and hybrid OR installations under one institutional structure. Academic medical centers sit at the top of this group because they can combine high-acuity case mix with multi-vendor software integration and advanced imaging room design. This makes hospitals the main anchor of the premium intraoperative imaging market, especially for neurosurgery, spine, and image-intensive cardiovascular workflows.

Ambulatory surgical centers are projected to grow at 7.47% CAGR through 2031, making them the fastest-growing end-user category. The end-user mix inside the intraoperative imaging industry is therefore widening, because ASCs increasingly need imaging support for orthopedics, pain care, cardiovascular procedures, and selected spine interventions without the space or shielding needed for the largest fixed systems. Stryker’s October 2025 launch of IP BRAVoE, built to simplify device connectivity and support real-time clinical decisions in hybrid OR and ASC environments, fits that buyer profile and highlights how the intraoperative imaging market is adapting to leaner procedural settings.

Geography Analysis

North America held 42.87% of the intraoperative imaging market size in 2025, which kept it as the largest regional contributor. The United States remains the main driver because the FDA clearance flow in 2025 and 2026 covered major platforms from Brainlab, IMRIS, Canon Medical, and Philips across neurosurgery, spine, MRI, CT, and interventional guidance. This product cycle density gives hospitals more upgrade options and supports faster replacement decisions in modalities where software capability is becoming as important as detector or scanner hardware.

Europe remained the second-largest regional base in 2025, supported by mature hospitals, established imaging standards, and demand for advanced surgical workflow tools. Philips launched IntraSight Plus in March 2026 after simultaneous FDA 510(k) clearance and CE marking, which shows that Europe continues to matter as a first-wave commercial region for premium guidance platforms. The region also remains important for AI-enabled navigation and dose management, where recent clinical literature has emphasized better reconstruction speed, lower radiation exposure, and closer integration between imaging and guidance layers. CE marking under the Medical Device Regulation framework supports broader commercialization, but the evidence burden around software and algorithm updates will keep vendor execution discipline high inside the intraoperative imaging market.

Asia-Pacific is projected to grow at 7.73% CAGR through 2031, making it the fastest-growing region in the intraoperative imaging market. The growth profile is broader than in North America because it combines first-time placements in expanding surgical centers with selective uptake of premium systems in high-acuity hospitals. This creates room for both mobile C-arm expansion and longer-term demand for integrated navigation, intraoperative CT, and intraoperative MRI platforms.

Competitive Landscape

The intraoperative imaging market is moderately consolidated at the premium platform level, where a small group of global OEMs competes across hardware, software, and navigation layers. GE HealthCare, Siemens Healthineers, Philips, and Medtronic remain the clearest reference points in this premium tier because they can combine imaging equipment with workflow software, integration capability, and service coverage. GE HealthCare’s April 2026 commercial integration between bkActiv intraoperative ultrasound and Medtronic’s Stealth AXiS navigation system shows how vendors are building linked workflows that become harder to replace than a single device purchase. That approach matters because buyer stickiness in the intraoperative imaging market increasingly depends on interoperability, installed-base support, and surgeon familiarity rather than on scanner specifications alone.

Brainlab follows a software-led route that gives it influence across multiple hardware environments inside the intraoperative imaging market. Its June 2025 FDA clearance for Elements 7.0 and September 2025 clearance for Spine Mixed Reality Navigation strengthened its role in neurosurgery and spine without requiring the company to control every major imaging modality. IMRIS has taken a different position by using the InVision 3T Recharge Operating Suite to extend the life of legacy Siemens MRI assets, which lowers disruption for hospitals that already have iMRI infrastructure. Philips is also deepening its foothold through IntraSight Plus, which brings IVUS, physiology, co-registration, and real-time device visualization into one interface and reinforces the importance of clinical workflow integration.

Competitive room still exists in the intraoperative imaging market despite the strength of the premium leaders. The clearest openings are in ASC-ready mobile systems, compact ultrasound, and modular upgrades that let hospitals add capability without replacing an entire room. Canon Medical and Stryker remain relevant in adjacent workflow areas through interventional imaging and OR integration. At the same time, Chinese suppliers such as Mindray and Shenzhen Anke continue to matter in price-sensitive regions where portability and value often outweigh the broadest feature set. Financing structure is another point of competition because many mid-tier hospitals need software and service access, but cannot justify a full premium suite on day 1. If MRI-derived synthetic CT moves from validated studies into scaled regulatory clearance, it could also create a new standard for low-radiation spine navigation and reshape positioning across the intraoperative imaging market.

Intraoperative Imaging Industry Leaders

GE HealthCare

Siemens Healthineers AG

Koninklijke Philips N.V.

Medtronic plc

FUJIFILM Holdings Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: GE HealthCare introduced modular Allia upgrade pathways to modernize existing interventional suites without full capital displacement, extending AI imaging capabilities to its global installed base and establishing a recurring software licensing revenue stream.

- April 2026: GE HealthCare announced commercial availability of a digital integration between its bkActiv intraoperative ultrasound system and Medtronic's FDA-cleared Stealth AXiS surgical navigation system. The plug-and-play architecture delivers live iUS imaging within the navigation interface for cranial procedures, directly addressing intraoperative brain shift, a leading cause of navigation inaccuracy in neurosurgery.

- March 2026: Philips launched IntraSight Plus, its next-generation interventional guidance platform, following simultaneous FDA 510(k) clearance and CE marking. The system integrates IVUS with iFR/FFR physiology, co-registration, and real-time device visualization on a single screen. Clinical evaluations demonstrated up to 47% reduction in system operation time.

- November 2025: Canon Medical received FDA 510(k) clearance for the Alphenix 4D CT with Aquilion ONE/INSIGHT Edition, its most advanced interventional imaging system, scheduled for commercial availability in summer 2026. Canon simultaneously received clearance for the Alphenix/Evolve Edition with αEvolve Imaging for interventional cardiology precision.

Global Intraoperative Imaging Market Report Scope

The intraoperative imaging market refers to the imaging systems and technologies used during surgical procedures to provide real-time visualization of anatomical structures and enable accurate surgical navigation and decision-making. It includes image-guided imaging systems used across various surgical specialties. The market comprises imaging services used in operating rooms to improve surgical precision, patient safety, and clinical outcomes.

The intraoperative imaging systems market is segmented by product type, application, end user, and geography. By product type, it is further divided into mobile C-arms, intraoperative computed tomography, intraoperative magnetic resonance imaging, and others. By application, it is segmented into neurosurgery, orthopedic and trauma surgery, spine surgery, cardiovascular surgery, and others. By end user, the market is segmented into hospitals, ambulatory surgical centers, clinics, and others. The geography segment is further divided into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market size and forecasts in value (USD) for the above segments.

| Mobile C-Arms |

| Intraoperative Computed Tomography |

| Intraoperative Magnetic Resonance Imaging |

| Intraoperative Ultrasound |

| Others (Intraoperative Endoscopic Imaging Systems and Intraoperative X-ray Systems, among others) |

| Neurosurgery |

| Orthopedic and Trauma Surgery |

| Spine Surgery |

| Cardiovascular Surgery |

| Other Applications (Gastrointestinal Surgery and Pediatric Surgery, among others) |

| Hospitals |

| Ambulatory Surgical Centers |

| Clinics |

| Others (Academic & Research Institutes and Specialty Surgical Centers, among others) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Mobile C-Arms | |

| Intraoperative Computed Tomography | ||

| Intraoperative Magnetic Resonance Imaging | ||

| Intraoperative Ultrasound | ||

| Others (Intraoperative Endoscopic Imaging Systems and Intraoperative X-ray Systems, among others) | ||

| By Application | Neurosurgery | |

| Orthopedic and Trauma Surgery | ||

| Spine Surgery | ||

| Cardiovascular Surgery | ||

| Other Applications (Gastrointestinal Surgery and Pediatric Surgery, among others) | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Clinics | ||

| Others (Academic & Research Institutes and Specialty Surgical Centers, among others) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the intraoperative imaging market?

The intraoperative imaging market is valued at USD 3.75 billion in 2026 and is projected to reach USD 5.43 billion by 2031 at a 7.65% CAGR.

Which product category leads revenue in intraoperative imaging?

Mobile C-arms lead the product mix with 42.32% revenue share in 2025 because they offer broad procedural use and a lower capital burden than fixed systems.

Which application area is growing fastest?

Spine surgery is the fastest-growing application, with a projected 7.33% CAGR through 2031, supported by growing use of 3D navigation and mixed reality guidance.

Why are hospitals still the largest end users?

Hospitals held 63.18% of revenue in 2025 because they manage higher-acuity cases and can support intraoperative CT, MRI, and hybrid OR investments.

What is driving demand in outpatient settings?

Ambulatory surgical centers are projected to grow at 7.47% CAGR through 2031 as more procedures move to leaner outpatient settings that still need mobile and compact imaging support.

Which region offers the strongest growth outlook?

Asia-Pacific has the strongest growth outlook with a 7.73% CAGR through 2031, while North America remains the largest regional base with 42.87% share in 2025.

Page last updated on: