Perfusion System Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.37 Billion |

| Market Size (2031) | USD 1.71 Billion |

| Growth Rate (2026 - 2031) | 4.53% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

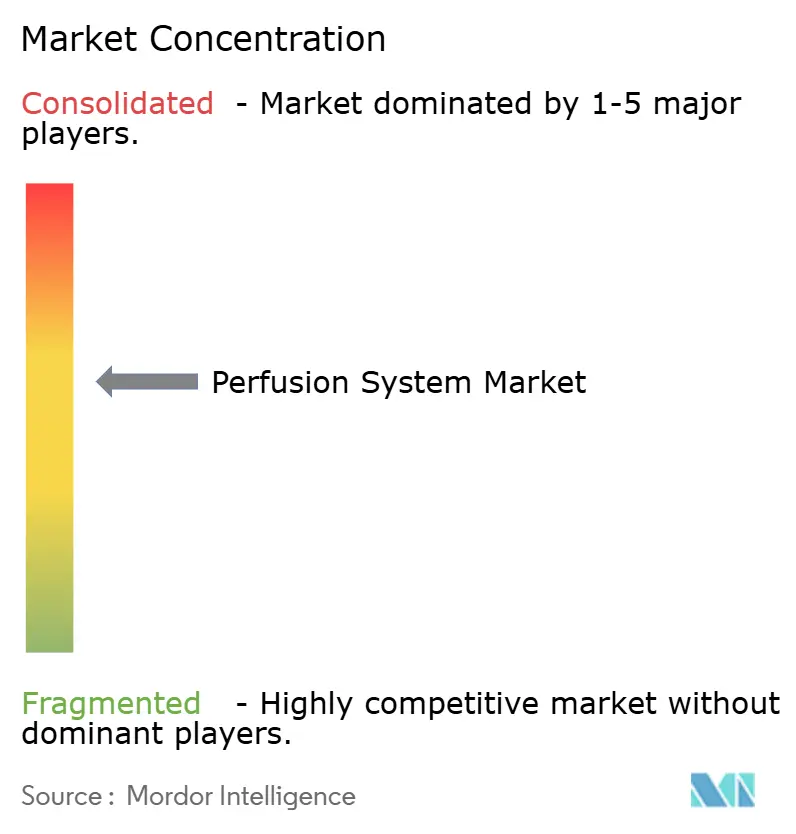

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Perfusion System Market Analysis by Mordor Intelligence

The perfusion system market size was valued at USD 1.31 billion in 2025 and estimated to grow from USD 1.37 billion in 2026 to reach USD 1.71 billion by 2031, at a CAGR of 4.53% during the forecast period (2026-2031). The current expansion mirrors the sector’s shift from experimental preservation toward standardized clinical use, supported by converging regulations and an urgent push to use every viable donor organ. Demand scales further as transplantation programs adopt machine perfusion technologies that keep organs close to physiologic conditions, enabling longer preservation windows and broader donor eligibility. Growing reliance on real-time analytics, wider clinical guidelines, and strategic acquisitions by leading vendors all raise the innovation bar and intensify competition. At the same time, device costs, uneven reimbursement, and a persistent shortage of trained perfusionists restrain adoption, especially in emerging economies where healthcare budgets are under pressure.

Key Report Takeaways

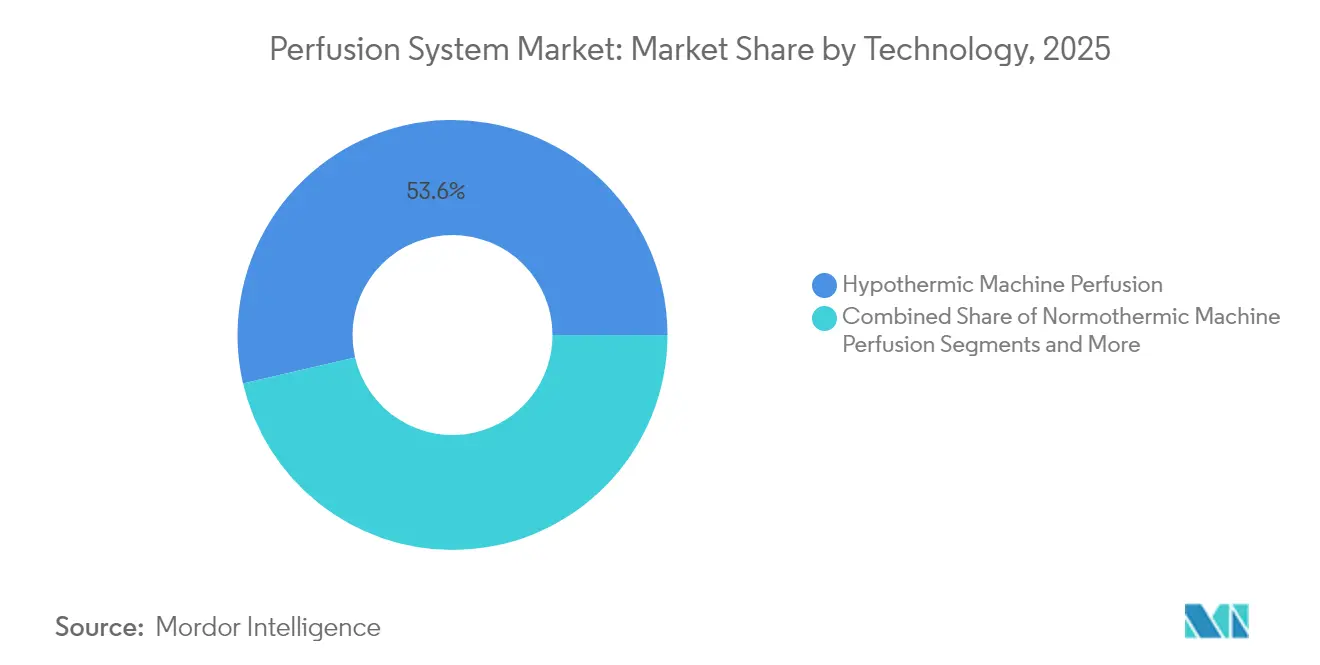

- By technology, hypothermic machine perfusion led with 53.62% of perfusion system market share in 2025; normothermic machine perfusion is expanding at a 6.95% CAGR through 2031.

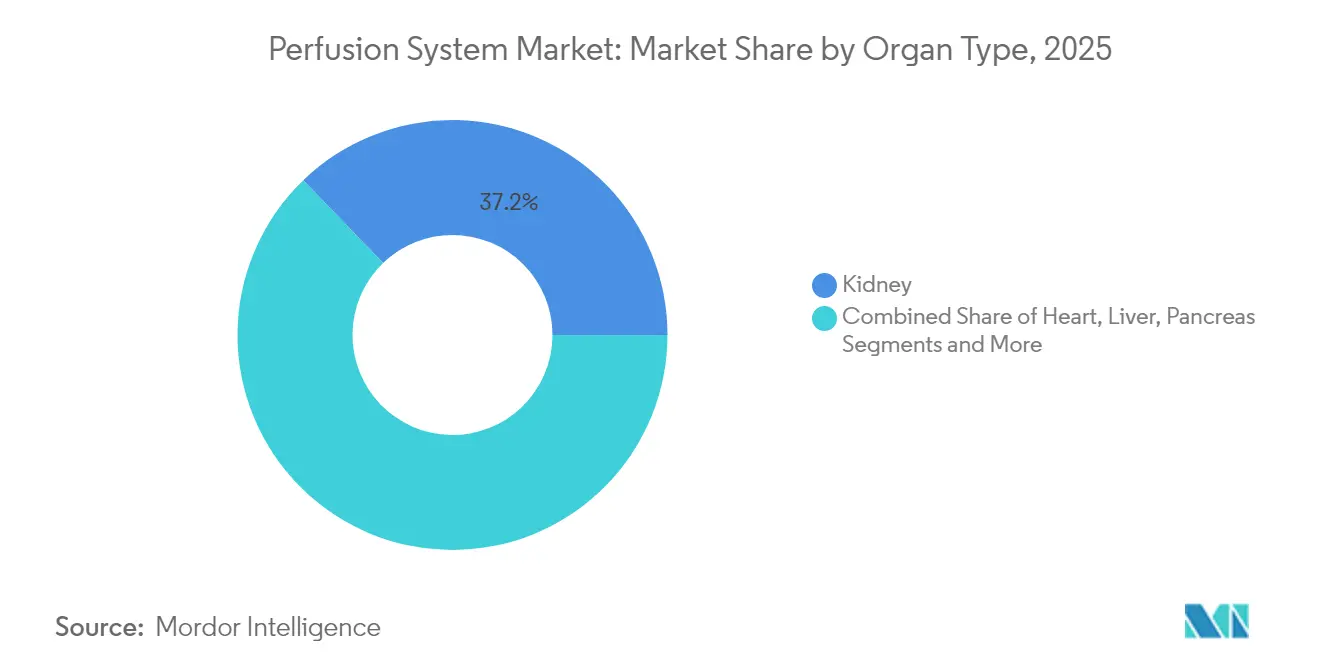

- By organ type, kidney preservation accounted for 37.21% of the perfusion system market size in 2025, while heart preservation is advancing at the fastest 7.18% CAGR to 2031.

- By end user, transplant centers commanded 68.66% revenue share in 2025; hospitals are projected to grow at a 6.12% CAGR as perfusion capabilities decentralize.

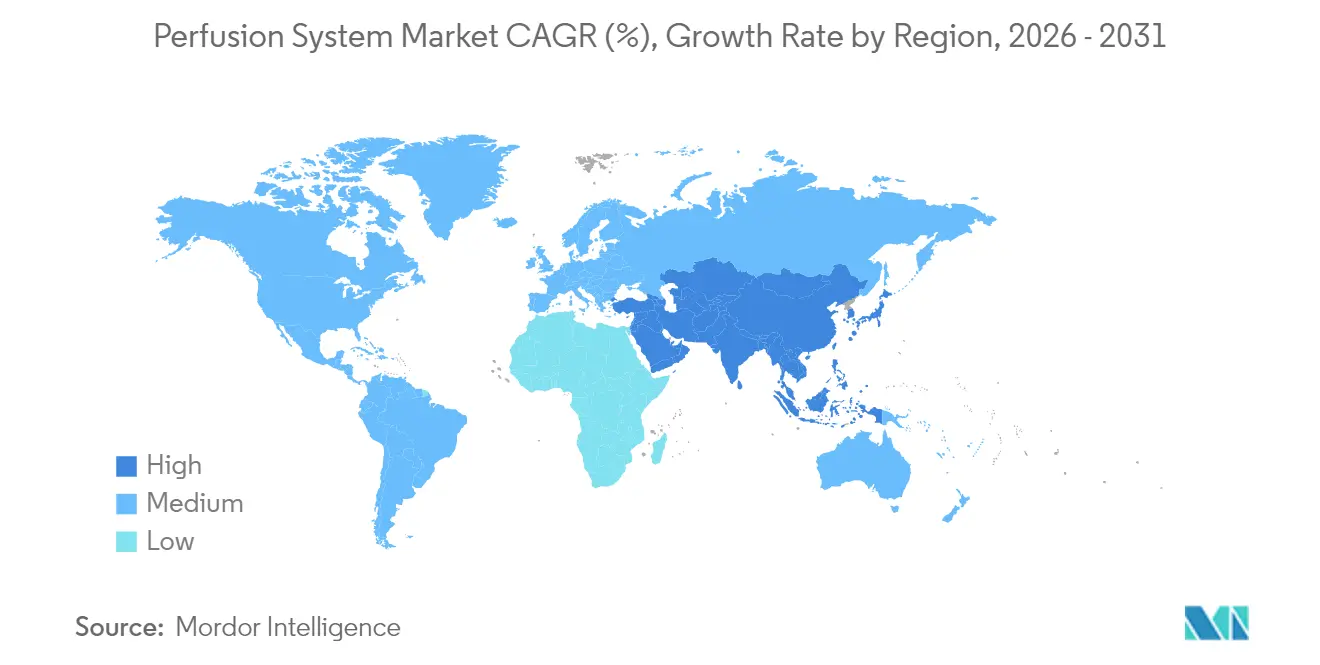

- By geography, North America retained leadership with 34.55% share in 2025; Asia-Pacific exhibits the strongest 7.79% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Perfusion System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand For Organ Transplantation | +1.2% | Global, with concentration in North America & Europe | Long term (≥ 4 years) |

| Increasing Prevalence Of Cardiovascular & Respiratory Diseases | +0.8% | Global, particularly APAC and North America | Medium term (2-4 years) |

| Rising Government & NGO Initiatives For Organ Donation | +0.6% | North America, Europe, emerging APAC markets | Medium term (2-4 years) |

| Adoption Of Perfusion For Marginal/Extended‐Criteria Donor Organs | +0.9% | North America & EU, expanding to APAC | Short term (≤ 2 years) |

| AI-Driven Real-Time Perfusion Analytics Improving Organ Utilization | +0.4% | North America & EU, pilot programs in APAC | Long term (≥ 4 years) |

| Inclusion Of Normothermic And Hypothermic Machine Perfusion In Emerging International Transplant-Care Guidelines | +0.5% | Global, led by WHO and regional transplant societies | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising demand for organ transplantation

More than 103,000 people remain on the U.S. transplant waiting list, with a new registration every 8 minutes, underscoring the relentless supply–demand gap that machine perfusion aims to close.[1]Health Resources and Services Administration, “OPTN Task Force Sets Goal of Achieving 60,000 Transplants by 2026,” hrsa.govOrgan shortage pressures mount further as chronic diseases enlarge the eligible recipient pool faster than donor numbers can keep up. The Increasing Organ Transplant Access Model incentivizes U.S. hospitals to scale surgery volumes, embedding perfusion technology into routine protocols.[2]Centers for Medicare & Medicaid Services, “Biden-Harris Administration Finalizes New Model to Improve Access to Kidney Transplants,” cms.gov These factors keep long-term demand for advanced systems high and stable.

Increasing prevalence of cardiovascular & respiratory diseases

Escalating rates of liver cirrhosis, chronic obstructive pulmonary disease and heart failure expand candidate lists and complicate donor organ quality. Asia-Pacific carries roughly 75% of global chronic Hepatitis B infections, feeding a pipeline of liver transplant demand. Machine perfusion allows metabolic assessment during storage, enabling surgeons to accept marginal livers, hearts and lungs that once failed static cold criteria. Integration of AI algorithms by leading centers further sharpens viability decisions, reducing discard rates and enlarging the effective donor pool.

Rising government & NGO initiatives for organ donation

Brazil executed more than 30,000 transplants in 2024 through Sistema Único de Saúde, an 18% jump over 2022 after digital matching and logistics upgrades that directly rely on perfusion stability. Similar policy moves in Canada and Europe adopt data-driven allocation models, collectively pushing centers toward technologies that document objective improvements in utilization and outcomes.

Adoption of perfusion for marginal/extended-criteria donor organs

Normothermic machine perfusion cut liver discard to 3.5% versus 13.3% under static cold storage, illustrating its role in unlocking high-risk grafts. The FDA’s first xenotransplantation trial of genetically modified pig kidneys adds urgency for platforms able to evaluate non-traditional organs in controlled environments. As consensus guidelines expand, perfusion systems move from optional add-ons to mandatory infrastructure at leading centers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost Of Perfusion Devices & Transplantation Procedures | -1.1% | Global, particularly emerging markets and cost-sensitive systems | Short term (≤ 2 years) |

| Diverse Regulatory & Reimbursement Barriers | -0.7% | Global, with regional variations in approval processes | Medium term (2-4 years) |

| Cross-Border Organ-Logistics Bottlenecks | -0.4% | International corridors, EU-US-APAC transport routes | Medium term (2-4 years) |

| Scarcity Of Specialized Perfusionists And 24/7 Transplant-Team Staffing | -0.6% | Global, acute in emerging markets and rural centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High cost of perfusion devices & transplantation procedures

A kidney procurement in the United States averages USD 35,427 with overhead exceeding 60% of that total; advanced devices raise costs further through single-use circuits and longer machine times.[3]Philip J. Held, “Cost Structures of US Organ Procurement Organizations,” Transplantation, journals.lww.comLiver transplant charges continue to climb, reflecting extra logistics and staffing tied to perfusion protocols. Budget-sensitive centers in Latin America, Africa and parts of Asia delay adoption until capital grants or donor programs offset outlays.

Diverse regulatory & reimbursement barriers

Manufacturers face staggered transition deadlines under the European Medical Device Regulation, separate UKCA labeling rules, and varied U.S. requirements for combination products, which collectively stretch development cycles and compliance costs health.ec.europa.eu. Reimbursement trails clinical evidence, leaving hospitals uncertain about payback—and sometimes forced to absorb consumable costs in bundled payments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Hypothermic dominance faces normothermic disruption

Hypothermic machine perfusion generated 53.62% of total 2025 revenue, underlining its deep clinical roots and multi-organ validation. Historically favored for kidneys and livers, hypothermic protocols cut delayed graft function and shorten ICU stays, helping hospitals justify the investment. The perfusion system market sees normothermic platforms accelerating at a 6.95% CAGR as physicians value the chance to monitor lactate, bile production and hemodynamics in real time. Early data from a leading U.S. center indicate a potential 14% rise in annual liver transplant volume after integrating normothermic protocols, hinting at broader clinical impact. Portable systems that maintain physiologic temperature during air transport remove the six-hour heart-transport ceiling, letting surgeons accept grafts from farther afield and thereby easing urban–rural access disparities.

The Cleveland Clinic successfully transplanted 15 out of 21 livers once deemed unsuitable, demonstrating practical gains in organ yield. Simultaneously, hypothermic oxygenated perfusion (HOPE) shows lungs can remain viable up to 20 hours with no rejections reported in pilot cohorts. As vendors release dual-temperature consoles capable of both modes, purchasing committees weigh one-machine flexibility against higher upfront price tags. Over the next five years, hybrid consoles are likely to capture share, especially at high-volume transplant hubs that process multiple organ types daily.

By Organ Type: Kidney leadership challenged by cardiac innovation

Kidney solutions captured 37.21% of the perfusion system market in 2025 thanks to the enormous transplant volume and mature reimbursement paths. This dominance is rooted in robust evidence; randomized trials show hypothermic perfusion reduces delayed graft function by 43% compared with static cold storage. Yet heart preservation systems post the highest 7.18% CAGR after the FDA cleared a device to accept donation-after-circulatory-death grafts fda.gov. Clinicians now retrieve hearts from donors whose organs were once automatically rejected, a shift that dramatically reshapes supply boundaries. Normothermic platforms keep hearts beating, allow arterial pressure measurement, and can even deliver cardioplegia on board, unlocking grafts transported across 10-hour flights.

Liver perfusion has moved beyond feasibility trials as the OrganOx metra system won Health Canada approval and approaches wider EU uptake. Ex vivo lung perfusion has turned lungs once labeled “high-risk” into transplantable grafts, and single-use devices for pancreata signal niche but rising diversification. The perfusion system market size for composite tissue, such as limbs or faces, remains small but could expand as vascularized allograft procedures gain reimbursement coverage.

By End User: Hospital adoption accelerates beyond transplant centers

Transplant institutes still held 68.66% revenue in 2025 owing to their specialized staff and donor-coordination mandates. Most early-stage clinical trials and technology validations run at these sites, anchoring vendor relationships and training programs. However, the perfusion system market records a 6.12% CAGR among general hospitals, a sign that preservation is migrating upstream into procurement workflows rather than staying confined to destination centers. Regional hospitals now keep organs viable during inter-state transfers, smoothing weekend staffing loads at major hubs.

Large health systems pilot nurse-supervised ECMO and perfusion programs to offset workforce limitations, while academic labs push the envelope by combining perfusion with regenerative techniques. ARPA-H’s PRINT initiative to bioprint personalized organs will rely on optimized perfusion to mature and vascularize complex tissue constructs before implantation.

Geography Analysis

North America commanded 34.55% of global revenue in 2025, benefiting from a robust reimbursement ecosystem and the Organ Procurement and Transplantation Network’s target of 60,000 procedures by 2026. The perfusion system market size for the region is supported by Medicare models that reward volume growth and drive near-universal adoption at Level I centers. TransMedics’ Organ Care System underpins much of this surge, with company revenue up 64% year-on-year and ambitions to reach 10,000 U.S. deployments annually by 2028.

Europe maintains consistent uptake as cross-border sharing via the FOEDUS portal eases organ flow, and MDR transitional rules, though complex, ultimately harmonize technical dossiers across 27 member states. The European Society for Organ Transplantation’s advanced-therapy roadmap likewise removes ambiguity for combination products, giving vendors clearer guidance. Companies such as Paragonix and OrganOx secure CE marks and Health Canada approvals, then roll out commercial launches in Germany, France and the Nordics where centralized procurement agencies fund capital upgrades.

Asia-Pacific registers the fastest 7.79% CAGR through 2031 as governments build transplant capacity and disease prevalence swells the candidate list. India completed the world’s third-largest number of surgeries in 2023 but could meet less than 10% of its kidney demand, underlining the need for technologies that salvage marginal grafts. China, Japan and South Korea invest in portable perfusion fleets that connect rural donor hospitals to urban transplant centers within clinically acceptable timelines. Australia’s National Organ Matching System, integrated with AI-enabled analytics, likewise depends on real-time perfusion data to optimize allocation. In Southeast Asia, pilot public-private partnerships subsidize device leases, accelerating first-time adoption at tertiary hospitals.

Competitive Landscape

Industry concentration is moderate. The major players are leveraging FDA and CE clearances that create high compliance hurdles for newcomers. TransMedics’ Organ Care System spans heart, lung and liver indications and turned in USD 108.8 million for Q3 2024, a 64% leap versus 2023. Getinge’s 2024 acquisition of Paragonix folded proprietary cold-to-warm transport containers into a global channel covering 135 countries.

OrganOx raised USD 142 million in early 2025 to fund metra platform scaling and software refinements aimed at predictive decision support. Device makers also look to AI partnerships: Terumo’s OneView monitor adds cloud telemetry that alerts surgical teams when perfusion parameters drift from targets. United Therapeutics tests xenothymokidney perfusion protocols, signaling a future in which perfusion is integral to genetically engineered organ supply chains.

White-space opportunities include consumable subscription models, integration of blockchain for chain-of-custody tracking, and compact consoles designed for helicopter retrieval missions. Start-ups exploring microsensor arrays and machine-learning scoring will likely license software to established infrastructure players, expanding the perfusion system market while keeping hardware ecosystems relatively consolidated.

Perfusion System Industry Leaders

Organ Recovery Systems, Inc

TransMedics, Inc.

XVIVO Perfusion AB

OrganOx Limited

Getinge (Paragonix Technologies, Inc)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Stanford researchers created vascular networks for 3D bioprinting that run 200× faster than prior methods, paving the way for organ-scale printed tissues.

- February 2025: Sunflower Therapeutics signed its first Asian distribution deal, launching the Daisy Petal perfusion bioreactor through PharmNXT Biotech to broaden regional access.

- January 2025: Paragonix Technologies completed first-in-human cases with the FDA-cleared KidneyVault Portable Renal Perfusion System, marking a milestone in kidney transport portability.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the perfusion systems market as revenue from console-based heart-lung machines, portable normothermic organ perfusion platforms, and integrated monitoring modules that keep blood or perfusate flowing during transplantation, cardiac surgery, or extracorporeal support, all valued at manufacturer selling price.

Scope Exclusion: stand-alone disposable oxygenators and tubing packs sold outside system contracts are not counted.

Segmentation Overview

- By Technology

- Normothermic Machine Perfusion

- Hypothermic Machine Perfusion

- Normothermic Regional Perfusion

- Next-gen Portable Perfusion Platforms

- By Organ Type

- Heart

- Lung

- Kidney

- Liver

- Pancreas

- Composite Tissue (VCA)

- By End User

- Transplant Centers

- Hospitals

- Academic & Research Institutes

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts spoke with transplant surgeons, perfusionists, biomedical engineers, and capital-equipment buyers across North America, Europe, and Asia-Pacific. The conversations refined usage ratios, replacement intervals, and adoption triggers, allowing us to adjust assumptions drawn from desk work.

Desk Research

We began by pulling transplant counts from the Global Observatory on Donation and Transplantation, then matched them with cardiothoracic procedure volumes published by the Society of Thoracic Surgeons to anchor demand. Import codes for perfusion consoles in United Nations Comtrade let us cross-check regional stock additions, and reimbursement tariffs from the Centers for Medicare and Medicaid Services clarified price ceilings.

Next, our team reviewed peer-reviewed papers in Circulation and The Lancet that traced the clinical shift toward normothermic machine perfusion, while company 10-Ks and investor decks revealed average selling prices and installed-base age. Paid repositories such as D&B Hoovers for segment revenues and Questel for patent activity illustrated competitive intensity and innovation. These sources are illustrative; many other public and paid references informed validation.

Market-Sizing & Forecasting

We built a hybrid top-down and bottom-up model. Transplant counts, elective cardiac surgeries, and reported ECMO prevalence sized the demand pool, which our team then corroborated through selective supplier revenue roll-ups. Key variables, global wait-list growth, console replacement cycle, disposable-to-capital ratio, average selling-price erosion, regulatory approvals, and elective-surgery rebound indexes, set the baseline value. Multivariate regression tied to GDP per capita projects value through the forecast period, while scenario analysis tests disruptive portable platforms. Regional gaps were bridged through channel checks before aggregation.

Data Validation & Update Cycle

Outputs pass anomaly filters, peer review, and management sign-off. Models refresh every year, with interim updates triggered by large tenders or device clearances, so clients receive our latest view.

Why Our Perfusion System Baseline Commands Confidence

Published estimates differ because firms mix device baskets, apply list rather than transacted prices, or freeze models on older base years. Our disciplined scope selection, annual recalibration, and transparent variables narrow this spread.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.31 B (2025) | Mordor Intelligence | - |

| USD 5.45 B (2025) | Global Consultancy A | Includes disposables and ECMO kits, uses list prices |

| USD 1.17 B (2024) | Trade Journal B | Earlier base year, omits organ-specific consoles |

| USD 0.99 B (2016) | Industry Association C | Limited geography, no inflation adjustment |

These contrasts show that Mordor's multi-step validation delivers a balanced, reproducible baseline that decision-makers can trust.

Key Questions Answered in the Report

What is the current value of the perfusion system market?

The perfusion system market stands at USD 1.37 billion in 2026, with projections pointing to USD 1.71 billion by 2031.

Which perfusion technology leads global revenue?

Hypothermic machine perfusion currently holds 53.62% market share, driven by longstanding clinical validation across kidney and liver transplants.

Why is Asia-Pacific growing the fastest?

Rapid healthcare infrastructure build-out and high liver disease prevalence push Asia-Pacific to an 7.79% CAGR, making it the fastest-expanding regional market.

What limits broader adoption of perfusion systems?

High device costs, complex regulatory pathways and a shortage of specialized perfusionists are the primary hurdles that slow uptake, especially in emerging economies.

How are AI tools used in perfusion?

AI algorithms analyze perfusion parameters in real time, improving marginal organ assessment and reducing discard rates, thus enhancing transplant success.

Page last updated on: