Perennial Allergic Rhinitis Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

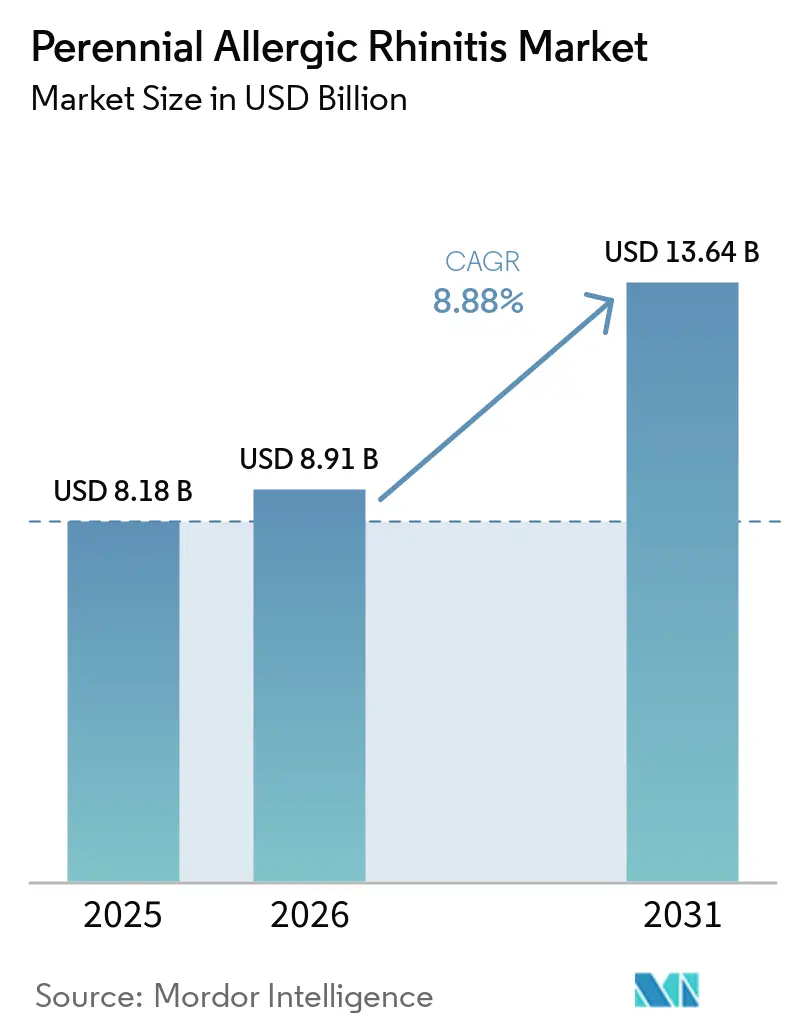

| Market Size (2026) | USD 8.91 Billion |

| Market Size (2031) | USD 13.64 Billion |

| Growth Rate (2026 - 2031) | 8.88% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Perennial Allergic Rhinitis Market Analysis by Mordor Intelligence

The Perennial Allergic Rhinitis Market size is projected to be USD 8.18 billion in 2025, USD 8.91 billion in 2026, and reach USD 13.64 billion by 2031, growing at a CAGR of 8.88% from 2026 to 2031.

Perennial allergic rhinitis, unlike seasonal rhinitis, is caused by year-round indoor allergens such as house dust mites, pet dander, mold spores, and cockroach residues. This constant exposure drives continuous treatment demand and increases annual spending on symptomatic drugs and immunotherapy per patient. Underdiagnosis remains a significant challenge in this market, as many individuals normalize chronic symptoms and delay seeking formal care. In 2025, a UK study revealed that patients reporting rhinitis symptoms outnumbered formal diagnoses by 4.9 times. However, advancements in indoor allergen testing, proactive physician screenings, and clearer treatment pathways are narrowing this gap. The market is further supported by earlier interventions in children, growing acceptance of disease-modifying therapies, and increased awareness of the overlap between untreated upper and lower airway diseases.

Key Report Takeaways

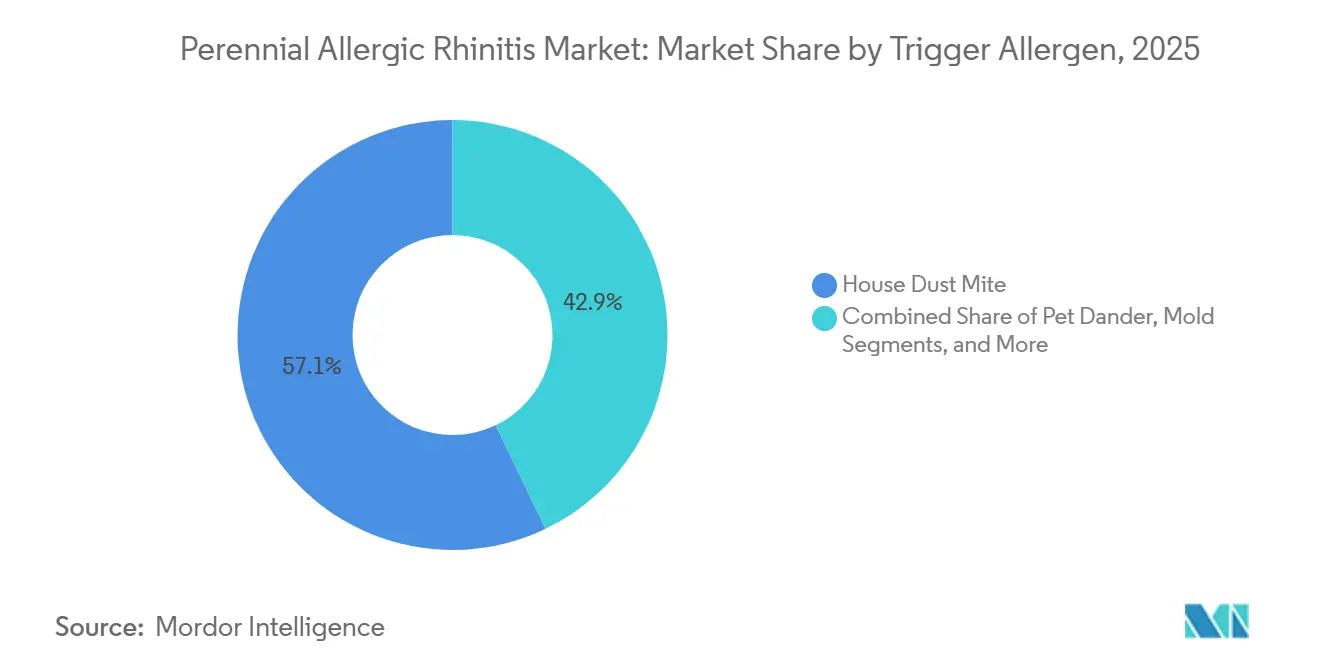

- By trigger allergen, house dust mite held 57.12% of revenue in 2025 and is also projected to expand at an 8.90% CAGR through 2031.

- By treatment class, symptomatic pharmacotherapy held 71.7% of revenue in 2025, while symptomatic pharmacotherapy is projected to be the fastest-growing treatment class, with a CAGR provided in the draft.

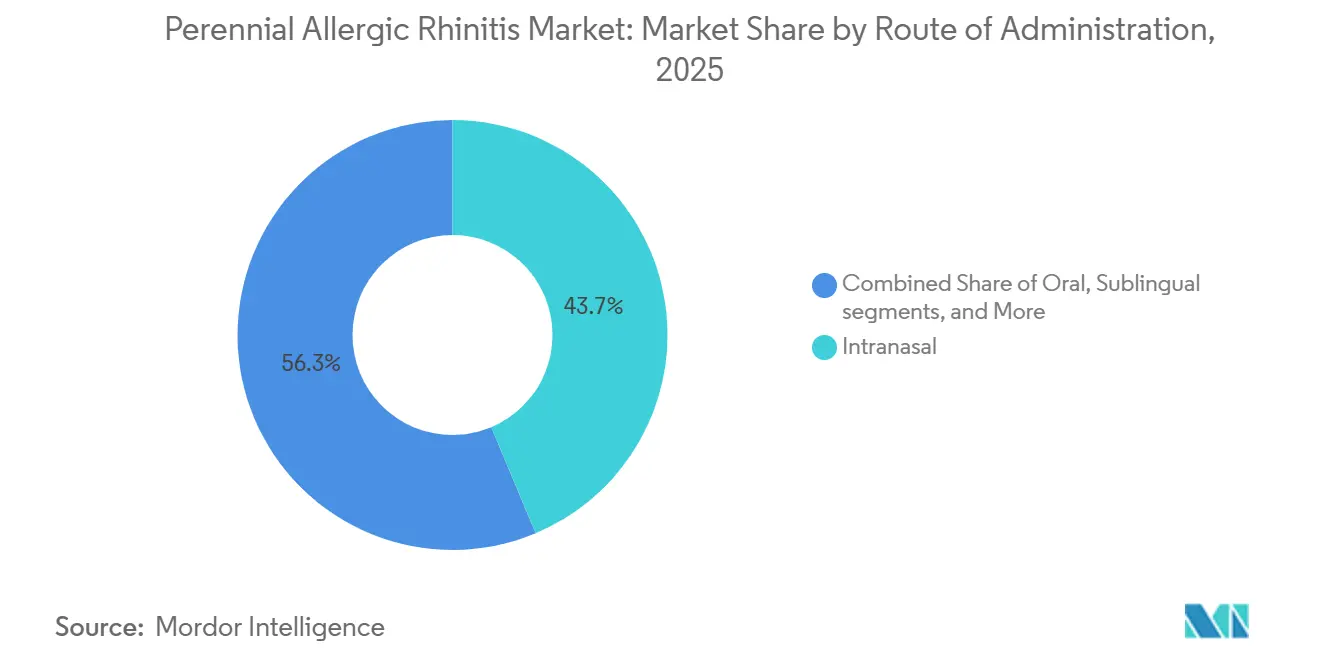

- By route of administration, the intranasal route held 43.67% of revenue in 2025, while the sublingual route is projected to grow at a 9.75% CAGR through 2031.

- By patient group, adults accounted for 56.45% of revenue in 2025, while the pediatric segment is forecasted to expand at a 10.10% CAGR through 2031.

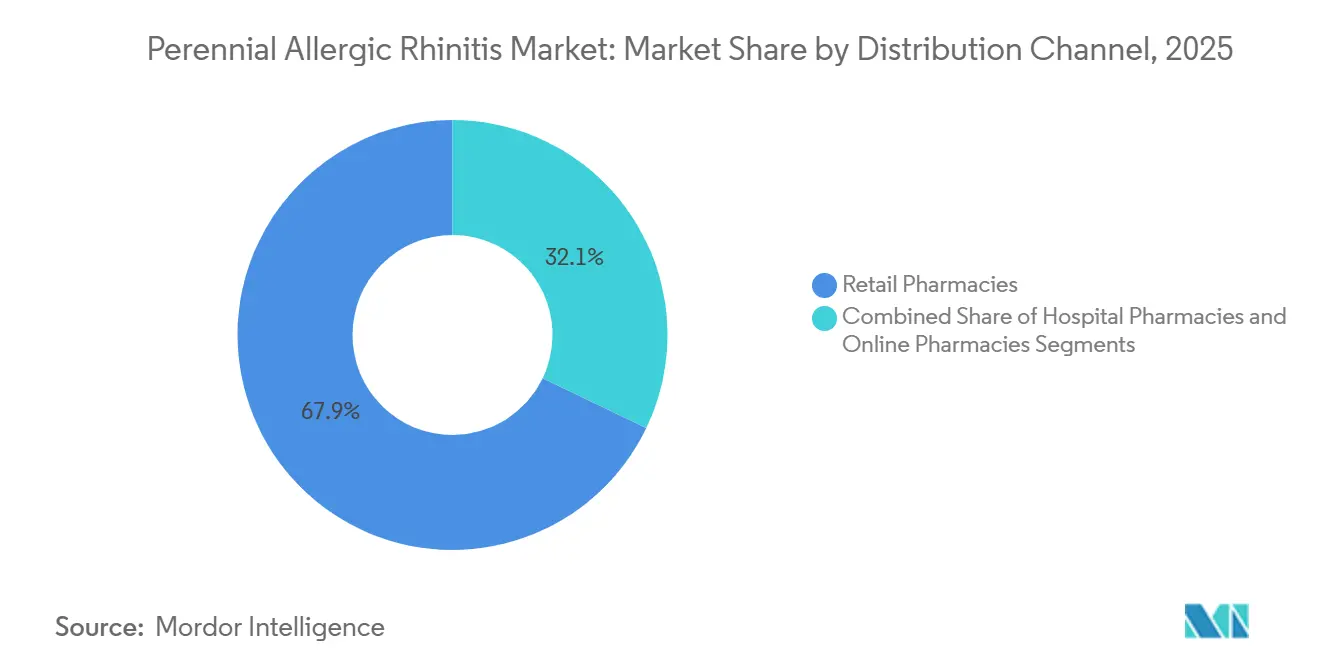

- By distribution channel, retail pharmacies held 67.88% of revenue in 2025, while online pharmacies are projected to grow at a 10.45% CAGR through 2031.

- By geography, North America held 38.47% of global revenue in 2025, while Asia-Pacific is projected to grow at a 9.66% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Perennial Allergic Rhinitis Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising indoor allergen sensitization | +1.8% | Global, strongest in humid Asia-Pacific urban centers and dense European housing stock | Medium term (2-4 years) |

| Preference for intranasal corticosteroids and combination sprays | +1.2% | Global, with strong relevance in North America and Europe | Short term (≤ 2 years) |

| Expansion of house dust mite immunotherapy | +1.5% | Global, especially Europe, North America, Japan, and China | Medium term (2-4 years) |

| Higher diagnosis of rhinitis-asthma overlap | +1.0% | Global, led by higher-income healthcare systems | Medium term (2-4 years) |

| Pediatric expansion of SLIT tablet eligibility | +1.1% | North America, Europe, and Japan | Medium term (2-4 years) |

| Biomarker-led identification of local allergic rhinitis | +0.6% | North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Indoor Allergen Sensitization Creates Permanent, Year-Round Demand

The perennial allergic rhinitis market benefits from the persistent presence of indoor allergens, which are harder to avoid compared to seasonal pollen. House dust mites thrive in specific temperature and humidity conditions, affecting 4-6% of the global population, with sensitization rates as high as 60-80% in humid regions. In Europe, 49% of allergic rhinitis patients are sensitized to house dust mites, making it the leading perennial trigger. Urban housing trends and pet dander further exacerbate allergen exposure, creating a consistent demand for effective treatments.[1]Jones et al., “UK Real-World Study on Rhinitis Symptoms and Diagnosis Gap, November 2025,” Frontiers in Allergy, frontiersin.org

Expansion of House Dust Mite Immunotherapy Redefines PAR's Disease-Modifying Standard of Care

The perennial allergic rhinitis market is evolving as house dust mite immunotherapy becomes a mainstream treatment. In February 2025, the US FDA approved ODACTRA for children aged 5 to 11, following a trial showing a 22% improvement over placebo. Similarly, ACARIZAX gained approval across 21 European countries, expanding its reach.[2]ALK, “ODACTRA Pediatric Label Expansion Announcement, February 2025,” ALK, alk.net Real-world evidence shows immunotherapy reduces medication use by 37.7% and transitions patients from persistent to intermittent rhinitis. Updated asthma guidelines also endorse house dust mite SLIT as an add-on for uncontrolled asthma, reinforcing its role in comprehensive airway management.

Higher Diagnosis of Rhinitis-Asthma Overlap Compounds PAR's Per-Patient Treatment Burden

The perennial allergic rhinitis market benefits from the growing recognition of rhinitis-asthma overlap. Studies indicate 40-50% of perennial allergic rhinitis patients may develop asthma due to sustained inflammatory activity. Research also shows that treating allergic rhinitis with antihistamines and corticosteroids improves asthma outcomes like FEV1 and peak expiratory flow. This overlap drives longer treatment durations, closer monitoring, and broader prescriptions, supporting earlier referrals and structured care for patients.[3]Tameeris et al., “Systematic Review of Allergic Rhinitis Treatment and Asthma Outcomes, January 2025,” npj Primary Care Respiratory Medicine, nature.com

Pediatric Expansion of SLIT Tablet Eligibility Is Structurally Consequential for Perennial Disease

The pediatric segment presents significant growth opportunities in the perennial allergic rhinitis market. House dust mite sensitization often begins early, with up to 68.3% of children affected by age 6. The 2025 ODACTRA label extension in the US opened treatment options for children aged 5 to 11. Studies show subcutaneous immunotherapy reduces asthma exacerbations by 69% and hospitalization rates by 65.2%, highlighting the long-term benefits of early intervention in pediatric perennial allergic rhinitis.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Long immunotherapy duration and adherence drop-off | -1.3% | Global, especially in year-round perennial treatment settings | Long term (≥ 4 years) |

| OTC and generic price pressure | -0.9% | Asia-Pacific, emerging markets, Europe, and North America | Medium term (2-4 years) |

| Mixed-rhinitis misclassification | -0.5% | Global | Medium term (2-4 years) |

| Reimbursement and supervision frictions for advanced therapies | -0.8% | Europe and North America, with limited Asia-Pacific coverage | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Long Immunotherapy Duration and Adherence Drop-Off Are Amplified in Perennial Disease

The perennial allergic rhinitis market faces adherence challenges as house dust mite immunotherapy requires year-round treatment for 3-5 years, leading to patient fatigue compared to shorter seasonal regimens. A Dutch study reported that only 66.7% of patients continued treatment beyond one year, with 18.3% discontinuing due to motivational or logistical issues. Additionally, patients stopping before two years failed to achieve sustained immunological benefits. Development programs, such as the PROACAROS Phase III trial involving 250 patients in Spain, aim to address these gaps, with recruitment expected to conclude by December 2025.

Reimbursement and Supervision Frictions for Advanced Therapies Constrain Disease-Modifying PAR Market Potential

The perennial allergic rhinitis market is hindered by inconsistent reimbursement for long-course SLIT and advanced therapies, even in regions with strong allergy care systems. In the UK, NICE's approval of ACARIZAX for patients aged 12 to 65 marked progress, but access remains uneven across Europe. The EMA's revised allergen immunotherapy guideline, effective January 2026, may support tailored products for less common indoor allergens. However, the requirement for supervised initial doses and post-dose observation slows adoption, keeping the market reliant on referral networks and clinic capacity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Trigger Allergen: House Dust Mite Dominance Reflects the Market's Indoor Exposure Core

In 2025, House Dust Mite accounted for 57.12% of the revenue and is projected to grow at an 8.90% CAGR through 2031, making it the largest and fastest-growing segment in the perennial allergic rhinitis market. Its dominance stems from being the most common indoor allergen and the focus of leading immunotherapy products, now expanding into pediatric care. Clinical evidence links house dust mite sensitization to chronic nasal obstruction and persistent symptoms, reinforcing its central role in both symptomatic and disease-modifying therapies.

By Treatment Class: Continuous Use Keeps Symptomatic Therapy in the Lead

Symptomatic Pharmacotherapy held 71.7% of the revenue in 2025, driven by year-round reliance on intranasal corticosteroids and antihistamines. Fixed-combination intranasal products are increasingly preferred for moderate-to-severe cases, reinforcing their role in routine management. Disease-modifying therapies, while smaller in scale, offer long-term benefits by addressing immune responses and are gaining traction in severe cases with chronic inflammation.

By Route of Administration: Sublingual Expands as a Preferred Disease-Modifying Option

The Intranasal route accounted for 43.67% of the revenue in 2025, reflecting its role as the primary method for long-term symptom control. Its popularity is supported by physician familiarity, over-the-counter availability, and strong guideline endorsements. The Sublingual route, projected to grow at a 9.75% CAGR through 2031, is gaining traction due to the convenience of home-based SLIT tablets, which offer effective disease-modifying treatment with better compliance compared to drops.

By Patient Group: Pediatric Expansion Adds the Strongest Growth Layer

Adults represented 56.45% of the revenue in 2025, driven by established treatment patterns, including continuous corticosteroid use and immunotherapy maintenance. Adults often transition to specialist care, resulting in higher treatment intensity per patient. However, the Pediatric segment is projected to grow at a 10.10% CAGR through 2031, supported by early-onset allergic rhinitis and regulatory approvals enabling earlier interventions. Trial data highlights the link between pediatric allergic rhinitis and asthma, emphasizing the importance of early treatment. Long-term allergen immunotherapy in children has been shown to reduce asthma risk, further supporting growth in this segment. Geriatric patients remain a smaller group due to shifting allergen patterns and treatment complexities.

By Distribution Channel: Retail Still Leads While Online Refill Behavior Expands

Retail Pharmacies accounted for 67.88% of the revenue in 2025, reflecting their role as the primary point of access for patients seeking relief from nasal symptoms. Pharmacists play a key role in guiding patients toward sustainable treatment options like intranasal corticosteroids. Online Pharmacies are projected to grow at a 10.45% CAGR through 2031, driven by subscription and home-delivery models that align with year-round disease management.

Geography Analysis

In 2025, North America accounted for 38.47% of global revenue, maintaining its position as the largest regional contributor in the perennial allergic rhinitis market. The United States drives this dominance with extensive treatment access, high diagnosis rates, and established use of intranasal corticosteroids, antihistamines, and house dust mite immunotherapy in care protocols. Canada complements this with approvals for Acarizax and support for intranasal corticosteroids and allergen immunotherapy in managing persistent diseases. Europe remains a key revenue contributor, supported by updated guidelines, active immunotherapy adoption across countries, and reimbursement progress in the UK for moderate-to-severe house dust mite conditions.

Asia-Pacific is projected to grow at a 9.66% CAGR through 2031, making it the fastest-growing region in the perennial allergic rhinitis market. The region's humid climates promote year-round mite proliferation, creating a strong base for market expansion. Japan exemplifies this with a 24.5% prevalence of perennial allergic rhinitis and insurance-backed use of house dust mite SLIT tablets. Southeast Asia and China also show high sensitization rates, with underdiagnosed cases presenting significant growth opportunities. The region combines heavy exposure, rising awareness, and expanding treatment pathways, driving sustained growth.

The Middle East, Africa, and South America are smaller markets but show potential for gradual growth. In the Gulf region, house dust mites are the most common indoor allergen, with a 77.8% prevalence in Saudi homes, while air-conditioned spaces sustain exposure. South America shares similar conditions, with warm, humid environments supporting high allergen burdens. As screening and physician awareness improve, these regions are expected to see an expanding treated patient base, highlighting emerging demand for addressing indoor allergen diseases.

Competitive Landscape

The perennial allergic rhinitis market demonstrates an uneven competitive structure. Branded immunotherapy faces high technical and regulatory barriers, while symptomatic pharmacotherapy is more open to generic and over-the-counter competition. This creates a market where the disease-modifying segment is more protected, but the symptom-control segment remains fragmented among multiple suppliers. Companies with standardized allergen extracts, pediatric labeling, or established reimbursement positions hold a stronger strategic advantage compared to those focusing solely on routine antihistamines or intranasal sprays. The market is shaped by product depth, label breadth, and strategic positioning across treatment layers.

Stallergenes Greer showcases a focused strategy in this market. In September 2025, the company partnered with Nuance Pharma for Actair in China, targeting a significant house dust mite-driven patient base in the Asia-Pacific region. In January 2026, it acquired Entomon in Italy, enhancing allergen extract manufacturing and strengthening its supply-side capabilities. Additionally, its iPUMP adherence tool improved daily observance by 15% in a 2024 study, addressing a key challenge in long-duration therapies. These initiatives highlight the shift from molecule access to persistence, service quality, and geographic expansion.

ALK strengthens its position with pediatric house dust mite tablet expansions, including the February 2025 ODACTRA extension in the U.S. and the December 2024 ACARIZAX authorization across 21 European countries, enabling earlier interventions. Sanofi and Regeneron add competitive pressure with advanced therapies, as seen with the February 2026 FDA approval of dupilumab for allergic fungal rhinosinusitis. EVEREST data presented in June 2025 further supported dupilumab's efficacy over omalizumab for chronic rhinosinusitis with nasal polyps, driving momentum for biologics in inflammatory airway care.

Perennial Allergic Rhinitis Industry Leaders

ALK-Abelló A/S

Allergy Therapeutics plc

Stallergenes Greer

GSK plc

Bayer AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Sanofi and Regeneron secured US FDA approval for dupilumab (Dupixent) as the first treatment for allergic fungal rhinosinusitis (AFRS) in adults and children aged 6 and above.

- January 2026: Stallergenes Greer acquired Entomon s.r.l. to enhance its allergen extract manufacturing capabilities for indoor and perennial allergen products.

- October 2025: Stallergenes Greer's Phase IIIb YOBI study for Staloral Birch achieved a 41% improvement in total combined score for children and adolescents aged 5 to 17.

- September 2025: Stallergenes Greer partnered with Nuance Pharma to market Actair SLIT tablet for house dust mite-induced allergic rhinitis in China.

Global Perennial Allergic Rhinitis Market Report Scope

As per the scope of the report, perennial allergic rhinitis is a chronic nasal inflammation that persists year-round, unlike seasonal allergies. It occurs when your immune system overreacts to indoor allergens constantly present in your home or workplace, causing symptoms like persistent congestion, sneezing, and a runny nose.

The perennial allergic rhinitis market is segmented by trigger allergen, treatment class, route of administration, patient group, and distribution channel. By trigger allergen, the market includes house dust mite, pet dander, mold, and cockroach and rodent allergens. By treatment class, the market is segmented into symptomatic pharmacotherapy (oral antihistamines, intranasal corticosteroids, combination nasal sprays, decongestants, leukotriene receptor antagonists) and disease-modifying therapy (advanced biologics). By route of administration, the market is categorized into oral, intranasal, sublingual, and subcutaneous. By patient group, the market is segmented into pediatric, adult, and geriatric. By distribution channel, the market is analyzed across hospital pharmacies, retail pharmacies, and online pharmacies. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| House Dust Mite |

| Pet Dander |

| Mold |

| Cockroach and Rodent Allergens |

| Symptomatic Pharmacotherapy | Oral Antihistamines |

| Intranasal Corticosteroids | |

| Combination Nasal Sprays | |

| Decongestants | |

| Leukotriene Receptor Antagonists | |

| Disease-Modifying Therapy | |

| Advanced Biologics |

| Oral |

| Intranasal |

| Sublingual |

| Subcutaneous |

| Pediatric |

| Adult |

| Geriatric |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Trigger Allergen | House Dust Mite | |

| Pet Dander | ||

| Mold | ||

| Cockroach and Rodent Allergens | ||

| By Treatment Class | Symptomatic Pharmacotherapy | Oral Antihistamines |

| Intranasal Corticosteroids | ||

| Combination Nasal Sprays | ||

| Decongestants | ||

| Leukotriene Receptor Antagonists | ||

| Disease-Modifying Therapy | ||

| Advanced Biologics | ||

| By Route of Administration | Oral | |

| Intranasal | ||

| Sublingual | ||

| Subcutaneous | ||

| By Patient Group | Pediatric | |

| Adult | ||

| Geriatric | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

Which allergen type drives the largest share of revenue?

House Dust Mite led the trigger allergen segment with 57.12% of revenue in 2025 and is also the fastest-growing trigger segment at an 8.90% CAGR through 2031.

Why is Asia-Pacific growing faster than other regions?

Asia-Pacific is projected to grow at a 9.66% CAGR because humid climates support year-round house dust mite exposure and diagnosis and treatment pathways are expanding across the region.

Which treatment route is growing the fastest?

The sublingual route is the fastest-growing route of administration, with a projected CAGR of 9.75% through 2031, supported by wider adoption of house dust mite SLIT tablets.

Which patient group offers the strongest growth opportunity?

The pediatric group is projected to grow at a 10.10% CAGR through 2031, supported by earlier sensitization, new label expansions, and the long-term value of early intervention.

What is the biggest barrier to wider immunotherapy adoption?

The main barrier is long treatment duration, because perennial regimens often require daily adherence for 3-5 years, which reduces persistence and slows full commercial uptake.

Page last updated on: