Peanut Allergy Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

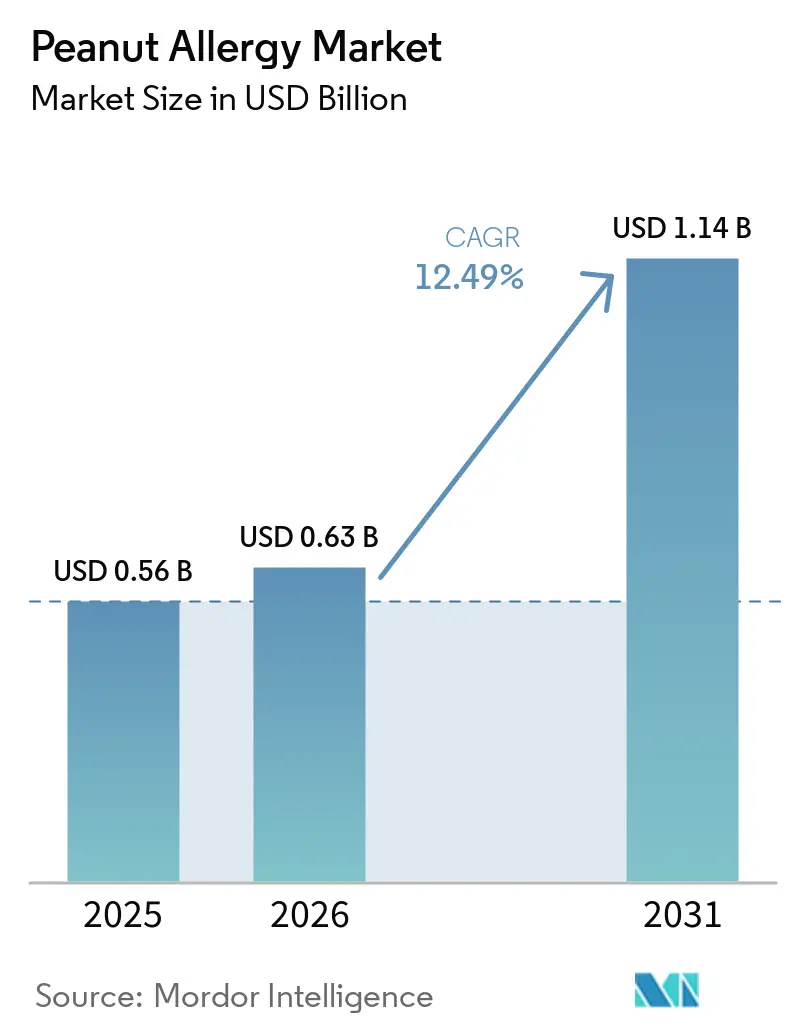

| Market Size (2026) | USD 0.63 Billion |

| Market Size (2031) | USD 1.14 Billion |

| Growth Rate (2026 - 2031) | 12.49% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Peanut Allergy Market Analysis by Mordor Intelligence

The Peanut Allergy Market size is expected to increase from USD 0.56 billion in 2025 to USD 0.63 billion in 2026 and reach USD 1.14 billion by 2031, growing at a CAGR of 12.49% over 2026-2031.

Momentum reflects a shift from strict avoidance and episodic rescue to preventive approaches that reduce reaction risk and raise thresholds, led by biologics and immunotherapy options that broaden eligibility beyond families willing to accept frequent reactions. The February 2024 approval of omalizumab for IgE-mediated food allergy created the first pharmacologic layer of protection for accidental exposures across multiple allergens, which repositions treatment goals for many patients and clinicians. New non-oral modalities are progressing with pediatric tolerability advantages, offering families options that align better with daily routines and safety preferences. Meanwhile, rescue treatment is innovating toward needle-free delivery that encourages timely administration and addresses device hesitancy, especially among caregivers. Reimbursement rules, REMS obligations, and site capacity remain gating factors, shaping how quickly the peanut allergy market converts latent demand into treated volume.

Key Report Takeaways

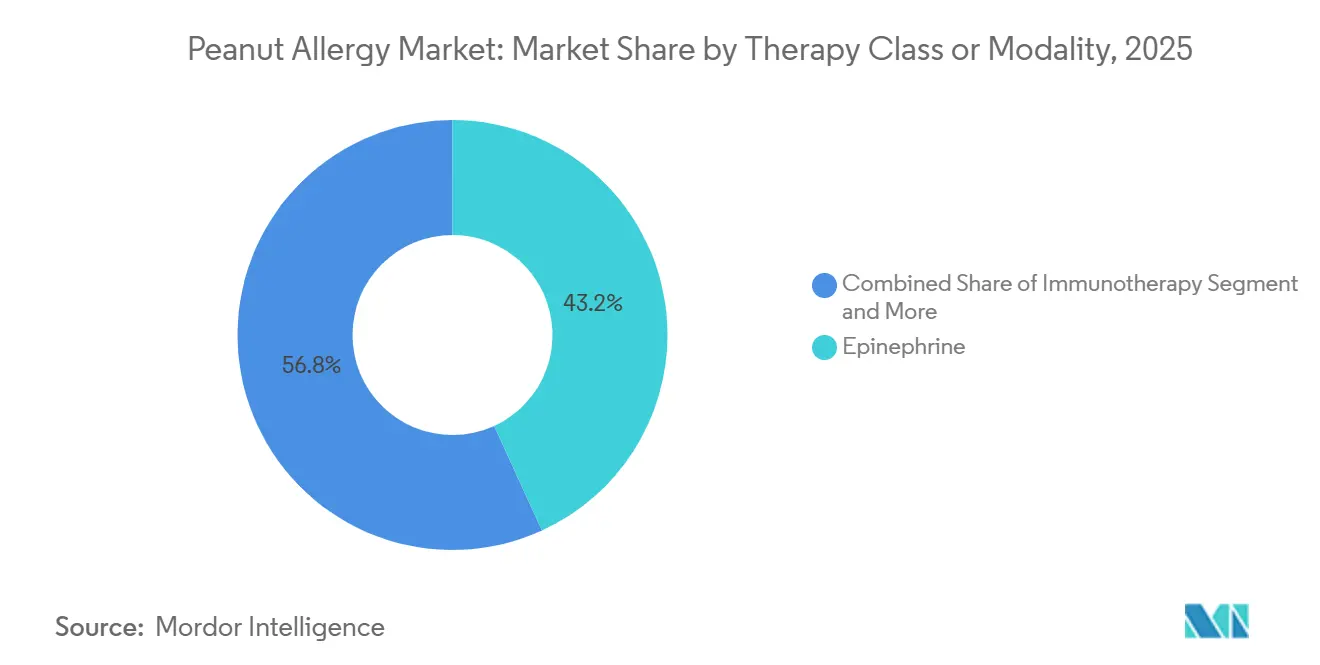

- By therapy class/modality, epinephrine led with 43.16% share in 2025. Immunotherapy is projected to grow the fastest at a 15.63% CAGR to 2031 in the peanut allergy market.

- By route of administration, oral formulations held 56.18% share in 2025. Injectables are projected to record the highest growth at a 14.37% CAGR to 2031.

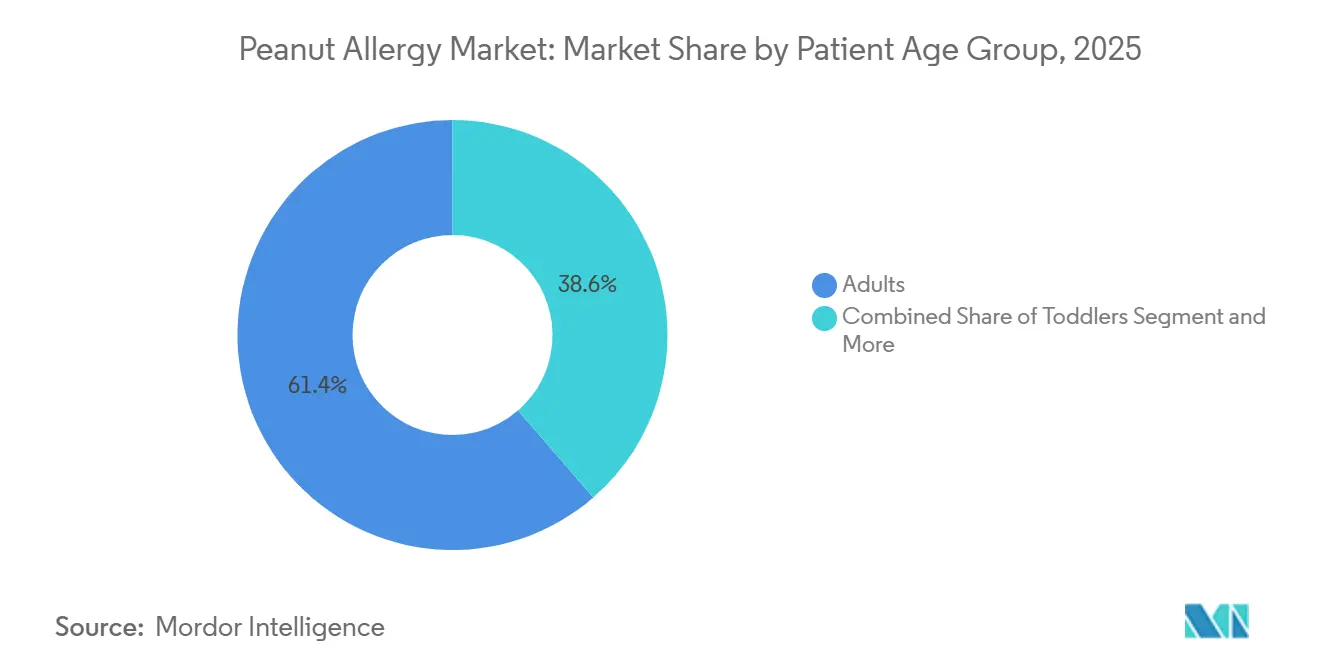

- By patient age group, adults accounted for 61.37% share in 2025. Children and adolescents are projected to post the fastest expansion at a 14.13% CAGR to 2031 in the peanut allergy market.

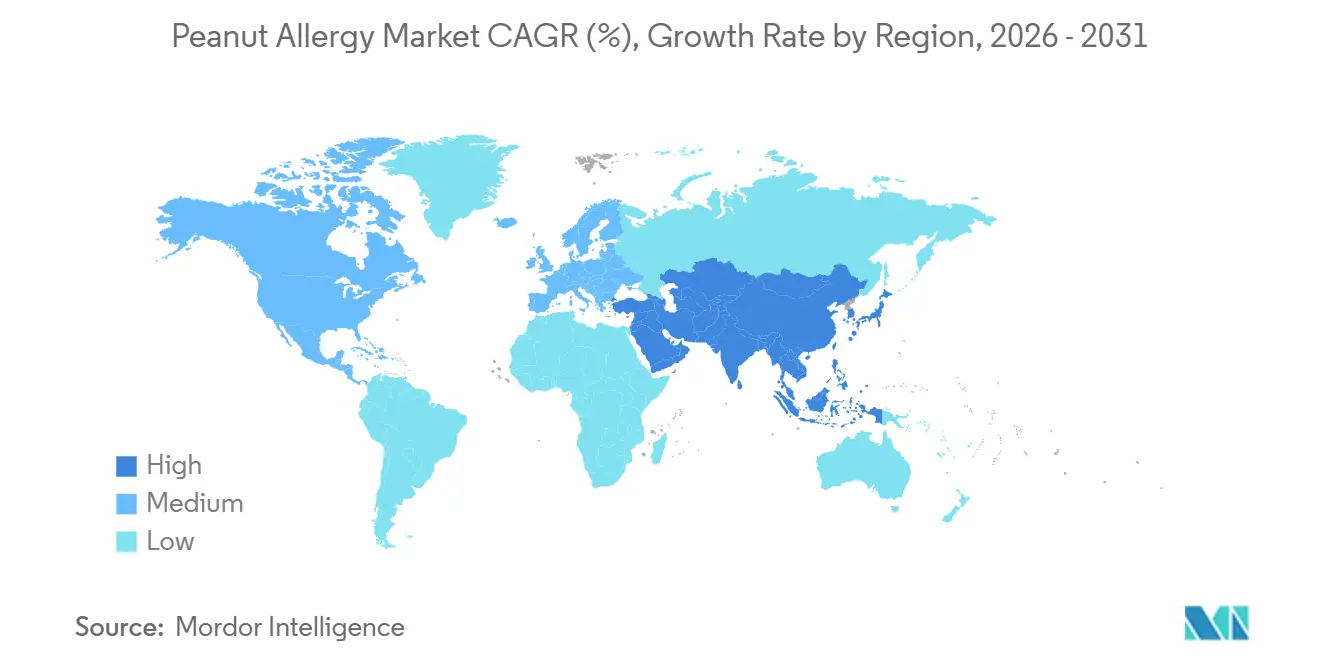

- By region, North America captured 36.53% share in 2025. Asia-Pacific is projected to expand at a 16.57% CAGR through 2031 in the peanut allergy market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Peanut Allergy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Anti-IgE Biologic Approval Expands Eligible Treated Population | +2.8% | Global, with early gains in North America, Western Europe | Short term (≤ 2 years) |

| Toddler Expansion in OIT Indications Accelerates Earlier Initiation and Uptake | +2.1% | North America, EU core markets; regulatory lag in Asia-Pacific | Medium term (2-4 years) |

| Non-Oral Modalities (EPIT, SLIT) Progress Toward Approval With Favorable Tolerability | +1.6% | Global; EPIT traction strongest in pediatric-focused EU markets | Medium term (2-4 years) |

| At-home/Self-Injection Pathways Reduce Visit Burden and Improve Persistence | +1.3% | Asia-Pacific urban centers, US telehealth-enabled regions | Long term (≥ 4 years) |

| Adjunct Biologic + OIT Regimens Improve OIT Tolerability and Pass Rates | +0.9% | Academic medical centers in North America, select EU hubs | Long term (≥ 4 years) |

| Multi-stakeholder Infrastructure (REMS-certified centers) Streamlines Implementation | +0.7% | National, concentrated in metropolitan allergy networks | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Anti-IgE Biologic Approval Expands Eligible Treated Population

The approval of omalizumab for IgE-mediated food allergy in February 2024 shifted care from single-allergen desensitization toward protection against accidental exposures across multiple foods, which aligns with day-to-day risk management for families who juggle several co-allergies. Pivotal OUTMATCH data showed that 68% of treated participants tolerated at least 600 mg of peanut protein without moderate-to-severe symptoms compared with 5% on placebo, while demonstrating concurrent gains for milk, egg, and cashew at thresholds relevant to real-world exposures, which reframed discussions about comprehensive protection versus single-allergen desensitization.[1]U.S. Food and Drug Administration, “FDA Approves First Medication to Help Reduce Allergic Reactions to Multiple Foods After Accidental Exposure,” Stage 2 results released in March 2025 reported no serious adverse events in patients receiving omalizumab monotherapy, compared with higher event rates in oral immunotherapy, and lower epinephrine use among omalizumab-treated patients, which reinforced the appeal of a safety-first strategy for families wary of frequent reactions during dose escalation.[2]Genentech, “Phase III Study Shows Xolair May Be More Effective With Fewer Side Effects Than Oral Immunotherapy for the Treatment of Food Allergies,”

The ability to protect across allergens at dosing intervals every 2 to 4 weeks can attract patients who previously avoided therapy due to daily dosing demands and lifestyle disruptions, broadening practical eligibility. The clinical profile sets a new baseline for shared decision-making by allowing families to pursue meaningful protection without navigating daily reaction risk inherent in oral protocols. As more centers integrate biologics into pathways, the peanut allergy market is expected to capture patients who value steady-state safety over maximal desensitization.

Toddler Expansion in OIT Indications Accelerates Earlier Initiation and Uptake

The July 2024 extension of Palforzia’s indication to ages 1 to 3 leveraged immune plasticity in very young children, which supports higher tolerance thresholds and improved safety signals during supervised escalation in eligible toddlers.[3]Stallergenes Greer, “FDA Approves U.S. Pediatric Indication Extension for Palforzia Oral Immunotherapy for the Treatment of Peanut Allergy,” The POSEIDON trial reported that 61.2% of treated toddlers tolerated 2,000 mg of peanut protein at exit challenge compared with 2.1% on placebo, and noted immunologic signals consistent with blunting of sensitization trajectories when started early, which supports a front-loaded approach to care for newly diagnosed families. Access workflows remained complex under REMS, since each escalation step required supervised dosing at certified centers with observation, which created scheduling friction in regions with limited pediatric allergists and long appointment backlogs.[4]PALFORZIA HCP, “POSEIDON Trial | Peanut Allergy Clinical Trial Data for HCPs,”

Accessibility varied by state, and multiple regions lacked fellowship training programs to replenish the pipeline, which constrained scaling during the indication’s early window. The January 2026 discontinuation decision, with final availability through July 31, 2026, disrupted continuity for existing patients and paused new starts, which shifted focus to non-oral modalities that can operate outside REMS while maintaining pediatric tolerability advantages. This sequence preserves the clinical rationale for early intervention while redirecting operational momentum toward modalities that fit within practice capacity.

Non-Oral Modalities (EPIT, SLIT) Progress Toward Approval With Favorable Tolerability

Epicutaneous immunotherapy advanced with the Phase 3 VITESSE trial showing a statistically significant responder rate of 46.6% in children ages 4 to 7 compared with 14.8% on placebo, and a safety profile centered on mild to moderate local skin reactions with very low treatment-related anaphylaxis, which is a compelling alternative for families concerned about systemic reactions during up-dosing. Regulatory interactions progressed in the United States and Europe, with plans for a 2026 Biologics License Application that could accelerate access in pediatric-focused markets that prioritize tolerability and caregiver convenience in daily life. Clinical differentiation rests on day-to-day usability as much as on desensitization speed, which positions patches as a bridge between safety and meaningful threshold gains. As clinicians harmonize shared decision-making around safety, lifestyle burden, and threshold goals, EPIT can carve a durable role alongside biologics and oral pathways. As this category matures, the peanut allergy market is likely to segment by family preferences rather than by a single efficacy hierarchy, which sustains multi-modality growth.

At-home/Self-Injection Pathways Reduce Visit Burden and Improve Persistence

Rescue treatment transitioned with FDA approval of neffy for patients at least 30 kg in 2024 and later for pediatric patients weighing 15 to less than 30 kg in 2025, which eliminated needles and simplified caregiver readiness during emergencies. Pharmacokinetic comparability to auto-injectors, combined with shelf life and temperature stability attributes disclosed in company materials, can help schools and families maintain readiness without the anxiety associated with needle use, which supports faster time to dose during high-stress events. As home-based dosing and self-directed pathways gain traction, adherence and persistence should improve in populations affected by clinic access barriers or device hesitancy. Coupled with telehealth integration in allergy practices, streamlined rescue readiness can complement preventive regimens by stabilizing emergency response behavior. Over time, these at-home and self-injection advances can reduce the visit burden, which indirectly boosts initiation and follow-through for complementary preventive options in the peanut allergy market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Boxed Warnings, Anaphylaxis Risk, and EoE Concerns Constrain OIT Adoption | -1.8% | Global; heightened regulatory scrutiny in EU, risk-averse prescribing in Japan | Short term (≤ 2 years) |

| Coverage Variability and Delistings Hinder Access and Continuity | -1.4% | US commercial/Medicaid fragmentation, NHS England resource constraints | Medium term (2-4 years) |

| Allergy/Immunology Workforce and Certified-Site Capacity Bottlenecks | -0.9% | Rural/underserved US, UK devolved nations, emerging Asia-Pacific | Long term (≥ 4 years) |

| Regional Product Withdrawals/Supply Transitions Disrupt Availability | -0.6% | Europe (Palforzia discontinuation), selective Asia-Pacific EAI unavailability | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Boxed Warnings, Anaphylaxis Risk, and EoE Concerns Constrain OIT Adoption

Oral immunotherapy raises thresholds through repeated exposure, which also raises the risk of treatment-related reactions during escalation and maintenance, and this tradeoff requires extensive counseling and careful monitoring. Clinical experience and society guidance emphasize the possibility of eosinophilic esophagitis and the need to interrupt therapy if symptoms emerge, which adds procedural steps and specialist involvement that many community practices find hard to sustain at scale. Lifestyle constraints attached to dosing, including activity modifications after administration and strict adherence to protocols during illness, reduce day-to-day flexibility for families. Practices also face documentation and medicolegal overhead whenever severe reactions occur, which nudges smaller centers to limit offerings or refer to academic hubs that maintain robust escalation infrastructure. The REMS framework around standardized oral peanut products aimed to reduce risk, but it also introduced center certification, monitoring, and inventory management steps that increased operational friction. Over time, this set of clinical and operational considerations has directed some families and clinicians toward modalities with lower systemic reaction risk, which influences patient flow within the peanut allergy market.

Coverage Variability and Delistings Hinder Access and Continuity

Eligibility checks, prior authorization requirements, and payer-specific documentation have elongated the time to therapy, which deters families who anticipate delays or repeated appeals. A representative commercial policy requires prescriber certification, documented attempts at avoidance, and exclusion of certain comorbidities, which can postpone starts and increase abandonment risk when administrative steps feel burdensome to caregivers. In England, national resource constraints after NICE approval limited commissioning for standardized oral peanut immunotherapy, and the subsequent product withdrawal left many families without a clear path to continuity, which underscores why authorization is only the first step toward access. Budget impact models in several systems remain focused on near-term acquisition costs rather than on quality-of-life gains and emergency care offsets that accrue over years, which tilts decisions away from prevention. While biologics and patches may ultimately show durable value to payers, current fragmentation delays adoption curves in multiple regions. These payer frictions slow the pace at which the peanut allergy market can unlock latent demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Therapy Class/Modality: Immunotherapy Momentum Outpaces Rescue Interventions

Immunotherapy’s 15.63% CAGR signals a durable shift toward preventive care, even as epinephrine retained 43.16% share in 2025, given its role in anaphylaxis rescue. Epicutaneous immunotherapy posted favorable Phase 3 results in children, with a 46.6% responder rate and few treatment-related severe events, which makes it attractive for families that want threshold gains with lower systemic reaction risk. Omalizumab’s approval for IgE-mediated food allergy added an option for cross-allergen protection at regular intervals, which supports families that prioritize safety and fewer clinic events during maintenance. Oral immunotherapy achieves higher desensitization for some patients but requires daily adherence and tolerance for more frequent reactions, which narrows the pool of families willing to initiate or persist.

As standardized oral peanut immunotherapy exits the market in mid-2026, practices are planning transition pathways that emphasize patches or biologics for eligible patients, which could expand treated volume through better alignment with caregiver risk tolerance. Rescue and supportive medications remain foundational but do not modify disease, which caps their contribution to long-run threshold changes. As a result, the peanut allergy market is reallocating growth toward modalities that reduce day-to-day exposure risk, with multiple age-tailored options. The evidence base for EPIT and biologics will continue to mature, and both modalities pair with family-centered tradeoffs that are easier to accept than daily oral dosing for many households. Immunotherapy’s trajectory remains strongest in pediatric cohorts, and ongoing regulatory interactions for patch-based products and real-world registry experience for biologics are expected to deepen adoption patterns in centers that balance safety, practicality, and clinical thresholds. During this transition, clinician workflow and payer policy will remain the main governors of pace. Where practices can stand up efficient protocols and achieve predictable coverage windows, initiation rates tend to improve. Where authorization and site capacity remain tight, practices keep families on robust rescue plans while evaluating preventive fit. This dynamic keeps both tracks relevant, but the direction of growth within the peanut allergy market favors preventive care.

By Route of Administration: Oral Holds Share Despite Injectable Innovation

Oral formulations commanded 56.18% share in 2025 due to patient familiarity, legacy pathways, and the historical presence of a standardized oral peanut product, though the withdrawal decision in 2026 will shift the mix. Injectables are the fastest-growing route at a 14.37% CAGR, supported by omalizumab for preventive protection and by needle-free neffy for emergency rescue, which together change how families perceive readiness and risk. Neffy’s approvals broaden caregiver comfort in emergencies and may lift rates of timely administration, which is a key determinant of outcomes. Patches offer a pragmatic alternative for long-term prevention that limits systemic exposure, and their day-to-day usability can attract families who prefer steady routines over daily oral dosing. With oral formulations, taste and adherence burdens add friction for younger children in real-world settings, which affects initiation and persistence. The peanut allergy market is therefore diversifying routes so that patient lifestyle and safety preferences can drive selection rather than force a single standard.

Subcutaneous delivery for biologics fits into structured clinic workflows that maintain observation protocols. As experience accumulates, practices may move more injections into predictable, low-burden schedules that fit family life. Nasal administration for rescue eliminated needle phobia and simplified caregiver decision-making, which should lift real-world effectiveness by reducing hesitation time. Patches reduce daily variability and lower the risk of systemic events, and their development path is tuned to pediatric tolerability, which matches the demographic where preventive demand is strongest, DBV. Oral options remain important for families that value maximal desensitization potential and who can accept the tradeoffs. The near-term transition in product availability shifts share within the peanut allergy market toward injectable and transdermal options that better fit daily life.

By Patient Age Group: Pediatric Plasticity Drives Fastest Gains Amid Adult Inertia

Children and adolescents are the fastest-growing cohort at a 14.13% CAGR, supported by trials and regulatory actions that center on early intervention and caregiver priorities. Toddler eligibility under Palforzia’s extension leveraged immune plasticity and led to higher tolerance achievements under supervised conditions, which validated early action for recently diagnosed families. EPIT results in 4 to 7-year-olds confirmed a favorable tolerability profile with meaningful responder rates, which is critical for long-term adherence in school-aged children and for caregiver confidence in structured regimens. These options align with family goals of restoring normalcy for school activities, social events, and travel. As pediatric pathways mature, more households are likely to combine preventive regimens with modern rescue solutions, which improves resilience to accidental exposures. The peanut allergy market is therefore capturing pediatric momentum through modalities that fit childhood routines and safety needs.

Adults retained 61.37% of the peanut allergy market share in 2025, though their growth rate trails pediatric cohorts as long-embedded avoidance behaviors and schedule complexity reduce enthusiasm for daily protocols. Adults who do initiate often seek fewer clinic visits and lower reaction risk during escalation, which steers preference toward biologic protection and away from daily oral dosing in many cases. Clinicians are therefore adapting decision trees to emphasize safety, convenience, and practical threshold goals rather than maximal desensitization targets for adult patients. Older adults remain underserved because trials tend to exclude those with multiple comorbidities, which limits evidence that would support coverage and routine prescribing in this group. As more real-world data emerges on biologics and patches, adult participation should expand in centers that build structured, lower-burden pathways. This evolution will broaden eligibility and improve persistence, supporting steady adult participation in the peanut allergy market.

Geography Analysis

North America held 36.53% of the 2025 market value. Dense specialty networks and reimbursement pathways that can accommodate high-cost preventive therapies support early adoption, while payer steps can still slow starts when prior authorization is complex. Workforce capacity remains a flashpoint, and national societies continue to advocate for more graduate medical education slots to close access gaps in underserved states. Canada’s public coverage model supports equitable goals, yet provincial formularies evaluate new products cautiously and can delay funded access until more outcome and budget impact data is assembled. In this context, biologics and emerging patches should gain share where centers harmonize scheduling, monitoring, and authorization steps into reliable flows. The peanut allergy market will continue to expand as practice models standardize and payer pathways stabilize.

Asia-Pacific is projected to be the fastest-growing region at a 16.57% CAGR through 2031, driven by urbanization-linked exposure patterns, rising diagnoses, and expanding specialist training. In China, published work highlights meaningful peanut sensitization among children in metropolitan areas but also documents capacity limits in specialty care, which complicates access to gold-standard oral food challenges and narrows real-world treatment pathways. Emergency readiness varies across the region, and published analyses show low rates of pre-hospital epinephrine in specific locales, which underscores the role of caregiver training and device availability in outcomes. Japan presents a distinct pattern where risk-averse prescribing culture and daily dosing aversion have tempered oral immunotherapy uptake despite documented sensitization in very young children, which may shift gradually as non-oral modalities grow their evidence base. Southeast Asian health systems have been active in anaphylaxis education, and clinical settings that equip caregivers with reliable rescue plans are laying groundwork for preventive pathways. As authorized preventive options expand, the peanut allergy market should accelerate in urban hubs with strong pediatric focus and growing middle-class demand.

Europe combines mature allergy infrastructure in Germany, the UK, and France with uneven commissioning for standardized oral products and variable capacity for follow-up escalation visits. The January 2026 decision to discontinue standardized oral peanut immunotherapy affected families mid-treatment and reversed momentum in centers that had built small pipelines, which pushed attention toward non-oral preventive alternatives and biologic protection. Southern Europe retains more conservative treatment patterns, with gradual adoption of preventive modalities as coverage pathways and clinic workflows evolve. Central and Eastern Europe are still scaling specialty capacity and reimbursement frameworks that could support structured escalation visits and monitoring. The Middle East and Africa display concentrated demand in Gulf economies that import advanced therapeutics and lean on expatriate-driven specialty services, while many sub-Saharan markets are earlier in the readiness curve due to competing health priorities. South American growth is strongest in major urban centers with private specialty networks, where awareness is rising among middle-income families. Collectively, these dynamics support steady regional expansion of the peanut allergy market as modalities map onto local coverage, capacity, and caregiver preferences.

Competitive Landscape

The competitive structure blends innovation leadership among a few biologic and immunotherapy developers with fragmentation at the service level across thousands of independent allergy clinics. Genentech and Novartis co-market omalizumab, which was approved for IgE-mediated food allergy in 2024 and delivered data showing favorable tolerability compared with oral immunotherapy in later-stage analysis, which reinforced differentiation on safety and practicality. Technologies advanced epicutaneous immunotherapy with positive Phase 3 results in 2025 and is aligned for U.S. regulatory submission in 2026 under its Breakthrough Therapy Designation, which could establish a lower-burden preventive option in pediatric care. ARS Pharmaceuticals established a new rescue category with needle-free epinephrine nasal spray, which positions the brand as a catalyst for better caregiver readiness and faster emergency response.

Strategic adjustments followed shifts in product availability and clinical evidence. Stallergenes Greer’s decision to discontinue the standardized oral peanut product by July 31, 2026, moved the focus in many clinics to biologics and EPIT for continuity pathways, particularly in geographies where commissioning or credentialing had constrained earlier uptake. Genentech emphasized the comparative safety profile of omalizumab versus oral immunotherapy in Stage 2 analysis, which shaped positioning with risk-averse families who value fewer systemic events during treatment. DBV Technologies secured financing in March 2025 to advance U.S. submission and launch planning, which signals commercialization preparation aligned to regulatory timing. ARS Pharmaceuticals executed a pediatric label expansion in March 2025, which deepened its role within school systems and family emergency kits.

Peanut Allergy Industry Leaders

Aimmune Therapeutics, Inc.

DBV Technologies S.A.

F. Hoffmann‑La Roche Ltd

Regeneron Pharmaceuticals, Inc.

Alladapt Immunotherapeutics, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Regeneron Pharmaceuticals presented 36 abstracts at the AAAAI Annual Meeting, including first-time Phase 3 data for investigational allergen-blocking antibodies targeting cat and birch allergies, signaling potential expansion into additional IgE-mediated allergy indications beyond food. The company also shared long-term analyses from a Phase 3 trial showing that early and sustained Dupixent treatment in children with moderate-to-severe atopic dermatitis impacted sensitization to common food allergens, including peanut, with IgE levels measured over 1.5 years of treatment.

- December 2025: DBV Technologies reported positive topline results from the Phase 3 VITESSE trial evaluating the Viaskin Peanut patch in children aged 4 to 7 years. The study met its primary endpoint with 46.6% of treated patients achieving responder criteria versus 14.8% placebo, with a safety profile characterized by mild to moderate local skin reactions and only 0.5% treatment-related anaphylaxis. The company plans BLA submission in 1H 2026 and may qualify for priority review under its Breakthrough Therapy Designation.

- September 2025: IgGenix completed enrollment for its Phase 1 clinical trial "ACCELERATE Peanut" evaluating IGNX001, a high-affinity monoclonal antibody designed to prevent allergic reactions by blocking peanut allergens from binding to IgE antibodies. The company anticipates topline data in the coming months.

Global Peanut Allergy Market Report Scope

As per the scope of the report, peanut allergy is a type of food allergy in which the immune system mistakenly identifies peanut proteins as harmful and triggers an abnormal response. It is typically mediated by IgE antibodies, leading to symptoms such as hives, swelling, digestive issues, or respiratory problems. In severe cases, it can cause anaphylaxis, a life-threatening reaction requiring immediate treatment (e.g., epinephrine). It is one of the most common and persistent food allergies, especially in children.

The peanut allergy market is segmented by therapy class/modality, route of administration, patient age group, and geography. By therapy class/modality, the market is segmented into immunotherapy, epinephrine, antihistamines, and others. By route of administration, the market is segmented into oral, injectable, and others. By patient age group, the market is segmented into toddlers, children & adolescents, and adults. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers estimated market sizes and market trends for 17 countries across major regions worldwide. The report offers market value (in USD) for the above segments.

| Immunotherapy |

| Epinephrine |

| Antihistamines |

| Others |

| Oral |

| Injectable |

| Others |

| Toddlers |

| Children & Adolescents |

| Adults |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Therapy Class / Modality | Immunotherapy | |

| Epinephrine | ||

| Antihistamines | ||

| Others | ||

| By Route of Administration | Oral | |

| Injectable | ||

| Others | ||

| By Patient Age Group | Toddlers | |

| Children & Adolescents | ||

| Adults | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the peanut allergy market growth outlook to 2031?

The peanut allergy market size was USD 0.56 billion in 2025 and is projected to reach USD 1.14 billion by 2031 at a 12.49% CAGR over 2026-2031.

Which therapy class leads and which is growing fastest?

Epinephrine led with 43.16% share in 2025, while immunotherapy is projected to grow the fastest at a 15.63% CAGR to 2031.

How is route of administration shifting in peanut allergy care?

Oral formulations held 56.18% share in 2025, while injectables are projected to post the highest growth at a 14.37% CAGR through 2031 due to biologics and needle-free rescue options.

Which patient group is expanding most quickly?

Children and adolescents are projected to expand at a 14.13% CAGR, supported by pediatric-centered trials and evolving regulatory actions.

Which region currently leads and which will grow fastest?

North America held 36.53% share in 2025, while Asia Pacific is projected to grow the fastest at a 16.57% CAGR through 2031.

What recent regulatory events are shaping the landscape?

Omalizumab gained approval for IgE-mediated food allergy in 2024, neffy secured FDA approvals in 2024 and 2025, DBV Technologies reported positive Phase 3 EPIT results in 2025, and the standardized oral peanut product is scheduled to be discontinued by July 31, 2026.

Page last updated on: