Inhalation And Nasal Spray Generic Drugs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

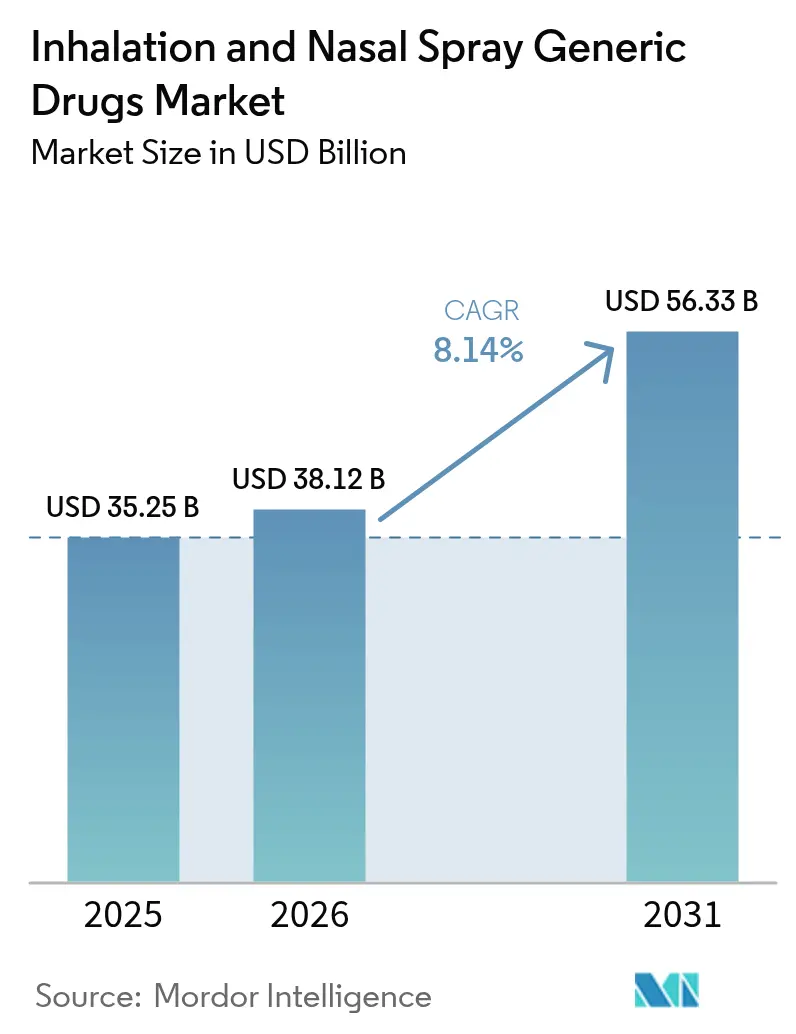

| Market Size (2026) | USD 38.12 Billion |

| Market Size (2031) | USD 56.33 Billion |

| Growth Rate (2026 - 2031) | 8.14% CAGR |

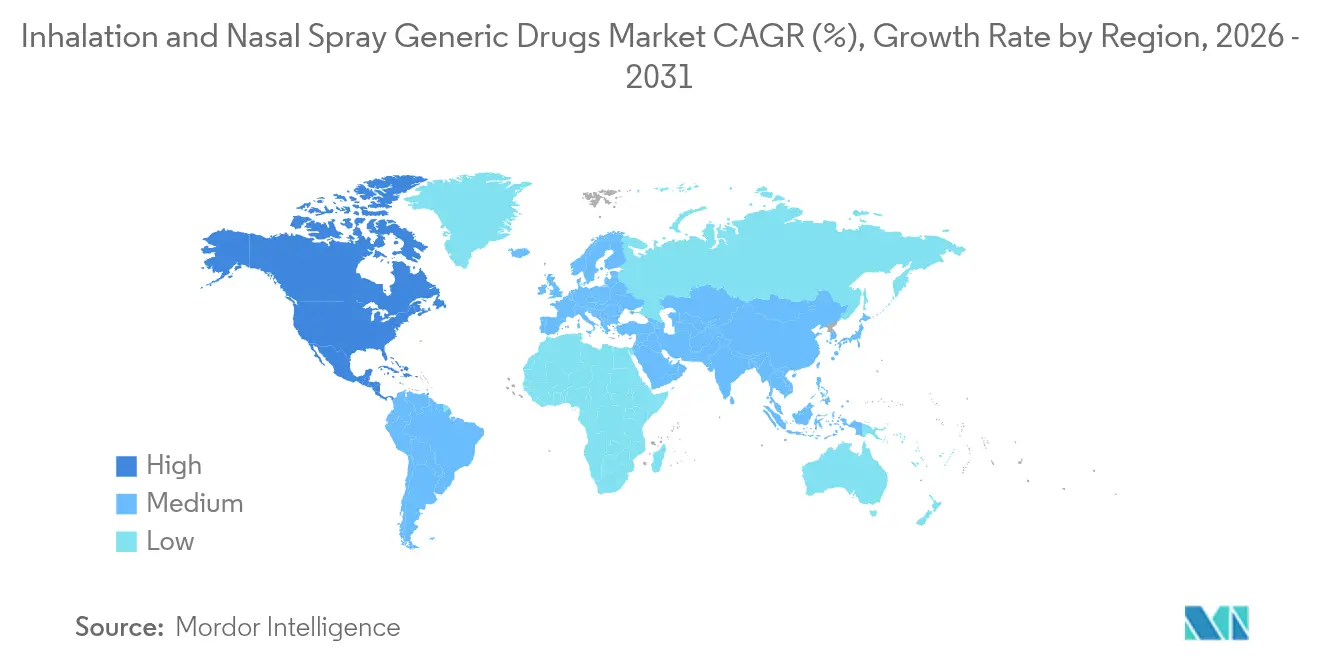

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

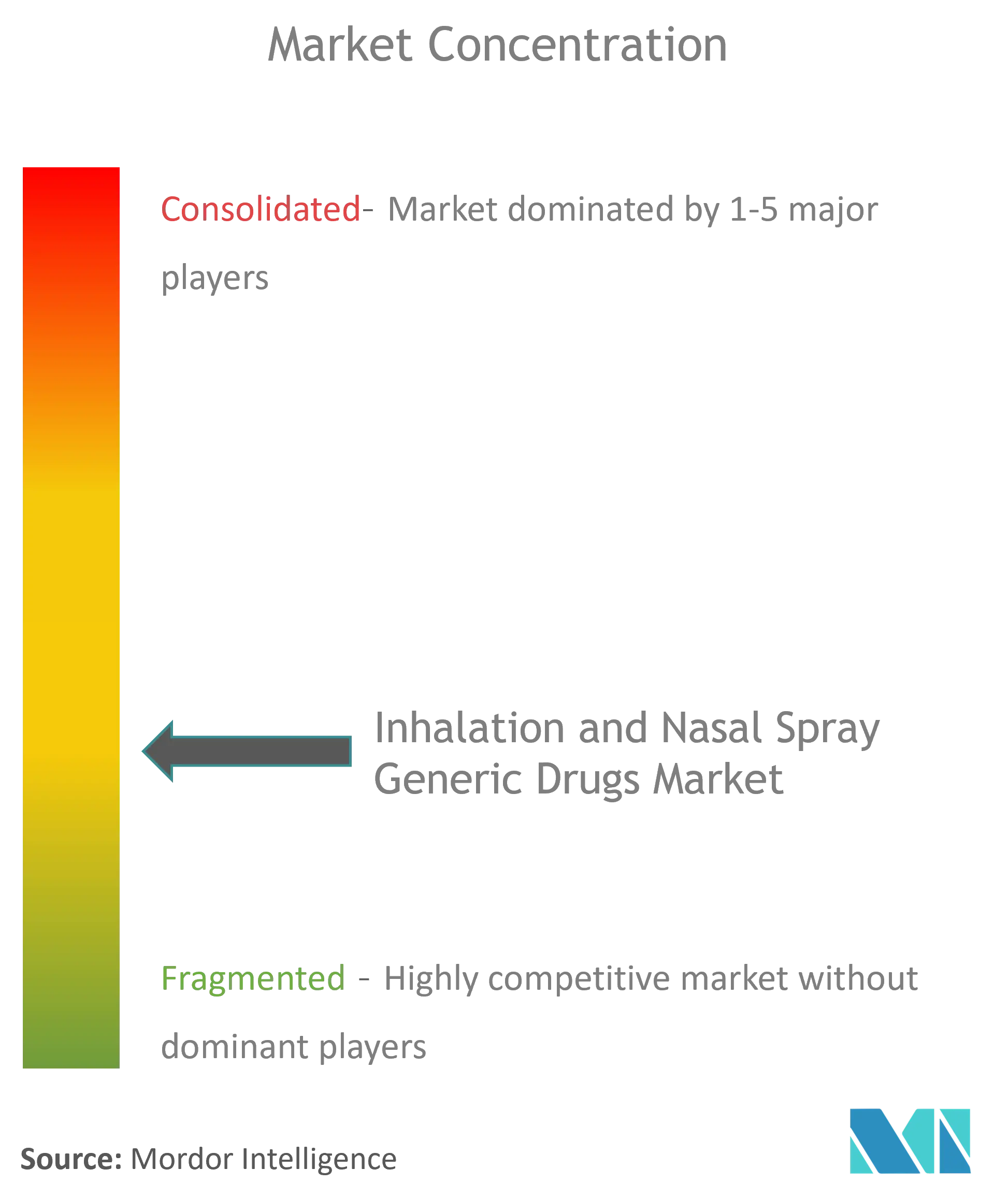

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Inhalation And Nasal Spray Generic Drugs Market Analysis by Mordor Intelligence

The inhalation and nasal spray generic drugs market size in 2026 is estimated at USD 38.12 billion, growing from 2025 value of USD 35.25 billion with 2031 projections showing USD 56.33 billion, growing at 8.14% CAGR over 2026-2031. Robust growth reflects the sharp patent cliff facing blockbuster inhalers, streamlined fast-track ANDA pathways, and mounting environmental regulations that push manufacturers toward propellant‐efficient formulations. Generic entrants are capitalizing on expiring asthma and COPD franchises, while contract development and manufacturing organizations (CDMOs) supply end-to-end expertise that lowers development risk for smaller companies. Regulatory harmonization across the United States, Europe, and key Asia-Pacific markets narrows approval timelines, and smart-inhaler add-ons help payers justify wider generic adoption. Meanwhile the shift to low-GWP propellants is accelerating product switch-outs, favoring manufacturers that master new formulation science and device compatibility.

Key Report Takeaways

- By drug class, corticosteroids led with 34.92% revenue share in 2025; combination ICS/LABA products are poised to expand at a 9.11% CAGR to 2031.

- By indication, asthma applications held 46.20% of the inhalation and nasal spray generic drugs market share in 2025, while COPD is projected to grow the fastest at 8.98% CAGR through 2031.

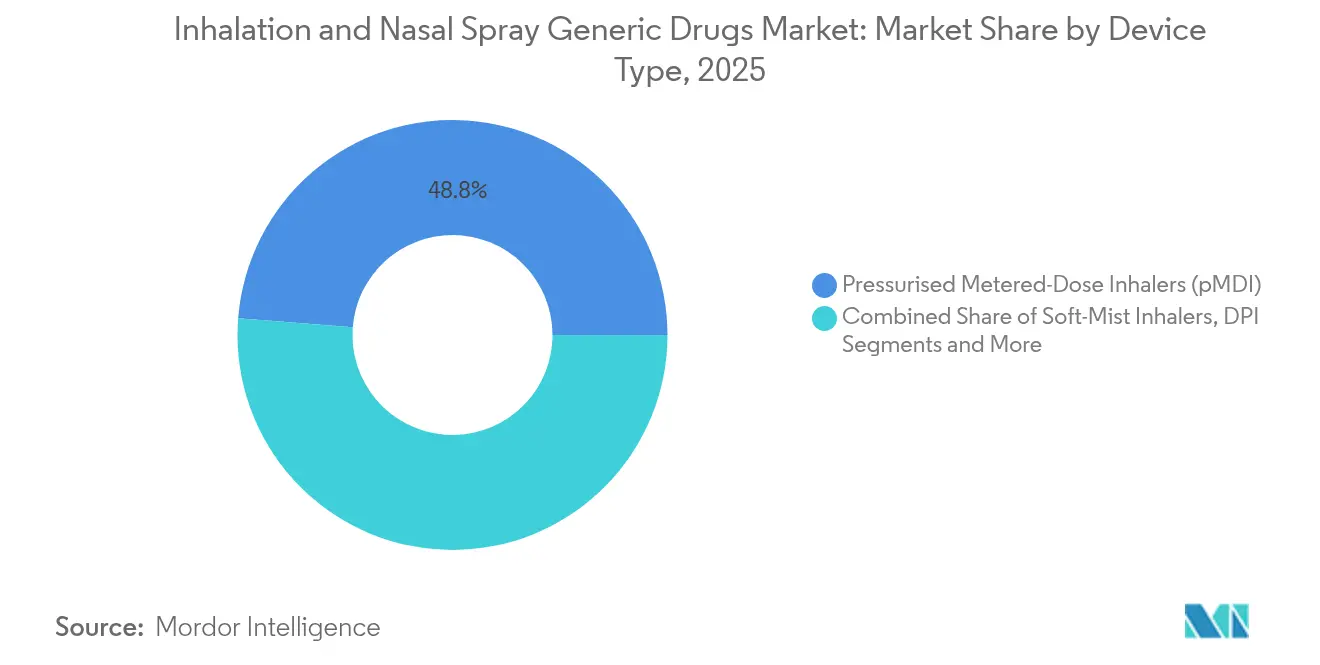

- By device type, pressurized metered-dose inhalers commanded 48.75% of the inhalation and nasal spray generic drugs market size in 2025; soft-mist inhalers are advancing at a 9.56% CAGR between 2026-2031.

- By distribution channel, retail pharmacies held 58.10% share of the inhalation and nasal spray generic drugs market size in 2025, whereas online pharmacies are projected to rise at a 9.98% CAGR to 2031.

- North America accounted for 42.90% of 2025 revenue, while Asia-Pacific is forecast to climb at a 10.18% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Inhalation And Nasal Spray Generic Drugs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Prevalence of Asthma & COPD | +1.8% | Global, with highest impact in Asia-Pacific and emerging markets | Long term (≥ 4 years) |

| Affordable Pricing Post-Patent-Expiry | +2.1% | North America & Europe primarily, spillover to global markets | Medium term (2-4 years) |

| Favorable Fast-Track ANDA Pathways | +1.2% | North America, with regulatory harmonization benefits globally | Short term (≤ 2 years) |

| Transition to Low-GWP Propellants Accelerates Product Switch-Outs | +0.9% | Global, led by EU regulatory requirements | Medium term (2-4 years) |

| CDMO One-Stop Inhalation Platforms Lower Entry Barriers | +1.1% | Global, with concentration in established manufacturing hubs | Medium term (2-4 years) |

| Smart-Inhaler Add-Ons Boost Payer Acceptance of Generics | +0.5% | North America & Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Prevalence of Asthma & COPD

Worldwide, asthma affects 262 million people, and COPD mortality is rising sharply in low- and middle-income countries where 85% of cases occur. Aging populations in developed economies compound the clinical burden, while treatment affordability gaps in emerging markets make low-priced generics indispensable. The World Health Organization places inhaled corticosteroids and bronchodilators on the essential medicines list, reinforcing policy momentum for broad generic availability [1]World Health Organization, “Model List of Essential Medicines,” who.int. As payers pursue value-based care, cost-effective respiratory generics remain recession-resistant necessities that underpin the inhalation and nasal spray generic drugs market.

Affordable Pricing Post-Patent-Expiry

The approval of Breyna, the first generic Symbicort, in March 2025 illustrates how patent expiries cut branded inhaler prices by 40-60% within a year. Formulary resets following the Flovent withdrawal further accelerate substitution to authorized generics, with Texas Medicaid lifting prior-authorization blocks on generic fluticasone. Tiered reimbursement frameworks consistently place generics at preferred levels, driving durable share gains across the inhalation and nasal spray generic drugs market.

Favorable Fast-Track ANDA Pathways

FDA’s Competitive Generic Therapy designation and 2024 in-vitro data-integrity guidance reduce approval cycles by up to eight months for complex inhalers. Parallel EMA updates issued in February 2025 align Europe with U.S. standards, enabling cross-regional dossiers that save development cost for smaller firms [2]European Medicines Agency, “Guideline on the Pharmaceutical Quality of Inhalation Medicinal Products,” ema.europa.eu. These reforms lower regulatory uncertainty and inject new competitors into the inhalation and nasal spray generic drugs market.

Transition to Low-GWP Propellants Accelerates Product Switch-Outs

The Kigali Amendment and EU F-gas rules are phasing down hydrofluorocarbons, prompting firms like Chiesi to invest EUR 350 million in HFA-152a inhalers that achieve 90% emission cuts. Supply constraints for legacy HFA-134A raise raw-material costs, nudging prescribers toward dry-powder or soft-mist devices. Sustainability targets embedded in hospital tenders mean early adopters can displace incumbents throughout the inhalation and nasal spray generic drugs market.

CDMO One-Stop Inhalation Platforms Lower Entry Barriers

Integrated CDMOs such as Catalent now manage formulation, device design, and commercial fill-finish under one roof, producing 100 million DPI capsules annually at Boston facilities. These high-capacity hubs cut program costs and shorten launch timelines, thereby expanding supply options for private-label brands that seek entry into the inhalation and nasal spray generic drugs market.

Smart-Inhaler Add-Ons Boost Payer Acceptance

Digital sensors from Adherium and Hailie track adherence and feed data into payer dashboards, improving outcomes without inflating costs. This tech alignment strengthens formulary positions for generics that bundle smart-caps, making them clinically competitive with premium branded devices.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Bio-Equivalence & Device Sameness Tests | -1.4% | Global, with highest complexity in North America & Europe | Medium term (2-4 years) |

| 'Device–Patent Thickets' Delaying Generic Launches | -0.8% | North America primarily, with spillover effects globally | Short term (≤ 2 years) |

| Impending HFA-134A Supply Squeeze Under F-Gas Rules | -0.6% | Global, with acute impact in Europe | Short term (≤ 2 years) |

| Post-Flovent Withdrawal Formulary Volatility & Stocking Gaps | -0.4% | North America primarily | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Bio-Equivalence & Device Sameness Tests

FDA now requires in-vitro plus in-vivo crossover trials that cost USD 15-25 million per candidate, extending timelines by up to two years. EMA’s 2025 inhaler guidance demands full comparative data when excipient or device differences exist. The capital hurdle restrains smaller entrants, narrowing the competitive field within the inhalation and nasal spray generic drugs market.

‘Device-Patent Thickets’ Delaying Generic Launches

Actuator, dose-counter, and mouthpiece patents can extend protection well after molecule exclusivity ends. Teva and Cipla’s Qvar settlement showcases the multi-year litigation that can stall generics. First-to-file challengers must spend heavily on legal battles, delaying access and slowing price erosion for the inhalation and nasal spray generic drugs market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: Corticosteroid Dominance Sustains, Combination Therapies Surge

Corticosteroids accounted for 34.92% of 2025 revenue, making them the anchor of the inhalation and nasal spray generic drugs market. Market acceptance rests on proven anti-inflammatory efficacy across asthma and COPD protocols, aided by widespread familiarity among prescribers. Following key patent expirations, generic fluticasone and budesonide realized rapid uptake, creating significant cost savings for payers and driving volume growth.

Combination ICS/LABA therapies show the fastest 9.11% CAGR through 2031 as clinicians embrace dual-mechanism control that improves lung-function metrics, adherence, and quality of life. The Symbicort generic launch paved the way, and additional combos await imminent patent cliffs. For manufacturers, the higher margin of complex blends offsets the investment in bioequivalence trials and device alignment, bolstering profitability across the inhalation and nasal spray generic drugs industry.

Bronchodilators continue steady demand as rescue medications, whereas antihistamines and decongestant sprays occupy narrower seasonal niches. Emerging classes such as leukotriene modifiers and anticholinergics diversify pipelines, but their current base is small compared with flagship corticosteroids. Nevertheless, each class contributes incremental revenue that collectively enlarges the inhalation and nasal spray generic drugs market size over the forecast horizon.

By Indication: Asthma Leads, COPD Accelerates

Asthma represented 46.20% of 2025 sales and remains the single largest clinical application. Decades of guideline-driven therapy have normalized inhaled generics in both pediatric and adult populations. Fast-track approvals guarantee ready substitutes whenever branded supply disruptions occur, safeguarding patient access.

COPD treatments are expanding at a 8.98% CAGR thanks to demographic aging and better diagnostics that uncover previously untreated segments. Combination maintenance inhalers dominate this growth. The inhalation and nasal spray generic drugs market size for COPD drugs is projected to widen sharply as payers demand lower-cost maintenance regimens for an enlarging elderly cohort.

Rhinitis, nasal polyposis, and sinusitis applications maintain moderate growth based on allergen exposure cycles and incremental innovation in nasal spray technology. Smoking cessation and pulmonary arterial hypertension represent nascent but high-value segments where inhalation delivery offers pharmacokinetic advantages, promising future diversification within the inhalation and nasal spray generic drugs market.

By Device Type: pMDI Supremacy Faces Eco-Driven Disruption

Pressurized metered-dose inhalers held 48.75% of the inhalation and nasal spray generic drugs market share in 2025 owing to decades of clinical adoption. However, their reliance on HFC propellants exposes cost risks under tightening F-gas quotas. Manufacturers must swiftly migrate to HFA-152a or HFO-1234ze to sustain competitiveness.

Soft-mist inhalers are the fastest-growing device class at 9.56% CAGR. They provide propellant-free delivery and improved lung deposition, winning physician endorsement amid sustainability mandates. Dry-powder inhalers remain stable, valued for portability and simpler regulatory paths, while nebulizers occupy niche hospital settings for severe cases.

Device innovation now centers on smart-caps and companion apps that monitor dose adherence. Successful digital integration will reshape prescriber preference, adding a fresh dimension to differentiation in the inhalation and nasal spray generic drugs market.

By Distribution Channel: Retail Stays Dominant as Digital Upshifts

Retail pharmacies handled 58.10% of 2025 volumes, leveraging face-to-face counseling pivotal for complex inhaler devices. Chain coverage and insurance billing expertise keep brick-and-mortar venues indispensable even as online platforms grow.

Online pharmacies and direct-to-consumer portals rise at a 9.98% CAGR, propelled by telehealth adoption and the convenience of home delivery. Platforms like ZipHealth supply albuterol inhalers for USD 29 per inhaler, bypassing conventional insurance hurdles. Hospital pharmacies focus on acute indications, but their centralized procurement power shapes formulary decisions that influence the broader inhalation and nasal spray generic drugs market.

Geography Analysis

North America generated 42.90% of global 2025 revenue, underpinned by FDA fast-track ANDA pathways, established coverage systems, and high asthma and COPD prevalence. The post-Flovent withdrawal episode underscored the region’s agility, with authorized generics rapidly filling supply gaps. Policymakers emphasize domestic manufacturing resilience after finding that 83 of the top 100 generics have no U.S. API source . These dynamics secure continued leadership for the inhalation and nasal spray generic drugs market in North America.

Asia-Pacific is the fastest-growing region at 10.18% CAGR through 2031, driven by healthcare expansion, regulatory harmonization, and cost-efficient manufacturing in India and China. Local governments integrate generics into universal health schemes, yet medication still exceeds daily wages for many patients, leaving substantial unmet need. Affordable inhalers therefore play a critical public-health role, propelling the inhalation and nasal spray generic drugs market across Asia-Pacific.

Europe faces dual challenges of environmental compliance and supply shortages. A June 2024 salbutamol deficit across 21 EU member states exposed reliance on limited suppliers. Simultaneously, the region enforces strict carbon reduction targets, spurring investment in low-GWP devices that could tilt share toward early adopters. Though generic medicine revenues slipped 26% over the past decade, propellant transition mandates reinvigorate innovation within the inhalation and nasal spray generic drugs market. South America benefits from regulatory modernization and wider insurance coverage. Together, these emerging territories add depth and diversification to the global inhalation and nasal spray generic drugs market, albeit from smaller revenue bases.

Regulatory Landscape

US FDA relies on Product-Specific Guidances (PSGs) and quality guidances for metered-dose inhalers, dry powder inhalers, and nasal sprays that emphasize in vitro performance alongside chemistry, manufacturing, and controls rigor for locally acting products. A notable update is the February 2024 PSG revision for formoterol fumarate and glycopyrrolate inhalation metered aerosol, which formalized model-informed approaches such as PBPK modeling and CFD in regulatory submissions.

In Europe, EMA guidance for inhalation and nasal medicinal products has been updated with a revised pharmaceutical quality guideline that consolidates quality expectations and aligns elements with device-related requirements, used alongside EU therapeutic-equivalence guidance for orally inhaled products in asthma and COPD. EU/EEA development sits within established procedural pathways for generic and hybrid applications and clinical trial requirements under Regulation (EU) 536/2014, reinforcing harmonized medicinal-product and device documentation across dossiers for complex inhalation formats.

Value Chain Analysis

The value chain for generic inhalation and nasal sprays spans API sourcing, specialty excipients, and device-component procurement (actuators, canisters, valves, dose counters, and polymers), followed by formulation development, analytical characterization, device performance testing, and high-precision fill-finish and assembly. Regulatory-linked testing requirements (for example, in vitro spray and aerosol performance and, where needed, in vivo bioequivalence studies) add cost and time, increasing reliance on specialist partners and CDMOs that can bundle formulation, device work, and commercial manufacturing. Integrated platforms such as Catalent, which operates high-throughput inhalation capacity (including large-scale DPI capsule output at its Boston facilities), illustrate how scale manufacturing and device know-how concentrate among a limited set of qualified suppliers.

Supply continuity has proven sensitive to product discontinuations and distribution changes, with downstream channel impacts that affect generic uptake and stocking. The June 2024 withdrawal of Flovent is an example of how brand exits can trigger near-term substitution pressure while also exposing payer and formulary frictions, and EMA shortage communications (such as the October 2024 Bronchitol distribution-transition disruption in the EU/EEA) highlight the operational risk of single-source components and distributor handoffs. These events keep dual-sourcing of critical components, regionalized manufacturing footprints, and distributor resilience central to procurement and commercialization strategies for generic inhalers and nasal sprays.

Competitive Landscape

Consolidation is accelerating. Molex-Phillips-Medisize closed the USD 1.1 billion acquisition of Vectura in January 2025, securing integrated drug-device expertise that supports full-service CDMO offerings. Altaris merged Kindeva Drug Delivery with Meridian Medical Technologies to create a scale player spanning pMDI, soft-mist, and injectable formats. These moves signal recognition that bioequivalence costs and strict device sameness rules favor companies able to control every step from formulation to final assembly.

CDMOs are pivotal. Catalent’s Boston site alone can output 100 million DPI capsules yearly, providing turnkey services for sponsors lacking inhalation infrastructure. This capability lowers the barrier for new entrants, enriching competitive dynamics within the inhalation and nasal spray generic drugs market.

Technology strategies diverge. Smart inhaler pioneers such as Adherium partner with AstraZeneca to embed adherence sensors, creating data-driven value propositions for payers. Environmental innovation is another frontier; Chiesi and GSK allocate hundreds of millions of EUR to low-carbon propellants, pursuing procurement advantages in eco-conscious markets. Patent analysis from Synapse PatSnap shows filings shifting from simple albuterol clones to integrated delivery systems featuring connectivity, indicating that future advantage rests on technological sophistication rather than sheer manufacturing scale. Overall, competitive intensity remains high as firms vie for share in the expanding inhalation and nasal spray generic drugs market.

Inhalation And Nasal Spray Generic Drugs Industry Leaders

Akorn, Inc.

Cipla Inc.

Novartis AG (Sandoz )

Teva Pharmaceuticals Inc

Apotex Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Market opportunities in the immediate term include high-volume rescue and maintenance inhalers where new approvals and launches expand the generic choice set and intensify price competition. In April 2026, Cipla received final US FDA approval for albuterol sulfate inhalation aerosol (90 mcg/actuation), the first AB-rated generic equivalent of Ventolin HFA, and Amneal began U.S. commercial launch of albuterol sulfate inhalation aerosol and beclomethasone dipropionate HFA inhalation aerosol (April 14, 2026).

A second opportunity sits in regulatory and technical enablement for complex, locally acting products, where clearer roadmaps and scientific tools reduce development friction. FDA PSG processes and GDUFA III mechanisms, including PSG-related teleconferences, support earlier alignment on bioequivalence packages, while the adoption of PBPK and CFD in guidance reinforces a path for programs that can validate model-informed evidence alongside established in vitro metrics. On the supply side, environmental compliance pressures on propellants and the associated device and formulation transitions create whitespace for manufacturers and CDMOs with validated low-GWP-compatible capabilities, particularly in pMDI-heavy portfolios where propellant selection and device compatibility can dictate commercial continuity.

Recent Industry Developments

- April 2026: Cipla received final US FDA approval for albuterol sulfate inhalation aerosol (90 mcg/actuation), the first AB-rated generic equivalent of Ventolin HFA. The approval expands competition in a high-volume rescue-inhaler segment and supports payer substitution where AB-rated interchangeability is prioritized. Cipla also signaled commercial launch timing in the first half of FY 2026-27, indicating near-term channel activity around contracting and formulary placement.

- January 2025: Molex-Phillips Medisize completed its acquisition of Vectura Group, strengthening an integrated drug-device services platform spanning formulation and inhaler technology. The deal reinforced CDMO scale advantages in complex inhalation generics, where device development, analytical testing, and fill-finish expertise materially influence timelines and approval readiness.

- May 2024: Amphastar Pharmaceuticals received US FDA approval for an albuterol sulfate inhalation aerosol ANDA, adding another affordable rescue-therapy option in the United States. Additional approved sources can help reduce supply and pricing volatility for high-turnover inhalers, while also raising competitive pressure on incumbent branded and authorized-generic offerings.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenue generated from generic medicines delivered through inhalation devices or nasal spray formats, where the product is marketed as a generic drug and sold through standard healthcare channels across major regions.

Scope exclusions: Branded-only inhalers or sprays, and standalone delivery devices sold without a corresponding generic medicine, are excluded from this sizing.

Segmentation Overview

- By Drug Class

- Corticosteroids

- Bronchodilators (LABA, SABA)

- Combination ICS/LABA

- Antihistamines

- Decongestant Sprays

- Others (Leukotriene modifiers, Anticholinergics)

- By Indication

- Asthma

- COPD

- Allergic & Non-allergic Rhinitis

- Nasal Polyposis & Sinusitis

- Smoking Cessation & PAH

- By Device Type

- Pressurised Metered-Dose Inhalers (pMDI)

- Dry-Powder Inhalers (DPI)

- Soft-Mist Inhalers

- Unit/Bi-Dose Nasal Sprays

- Nebulisers

- By Distribution Channel

- Retail Pharmacies

- Hospital Pharmacies

- Online Pharmacies & DTC Platforms

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

For desk research, we first build a clean fact base on respiratory disease burden and medication use, and then align it with policy, approvals, and channel realities for generics. Public sources such as the US FDA (ANDA and product listings), the EMA, the WHO, and the CDC helped us anchor the market to real therapy demand, not just company narratives. We also referenced sources such as OECD health statistics and national health agencies to understand prescription access and reimbursement patterns that can change generic uptake.

To connect demand to commercial activity, we reviewed annual reports, investor decks, and regulated filings for companies active in inhaled and nasal dosage forms, along with reputable press and association updates that track launches and supply topics. Where needed, a paid subscription for company financials and news intelligence was used to confirm revenue exposure and timeline signals, and a patent database was used to sense the pace of loss of exclusivity in key molecules. This list is not exhaustive, and many other public sources were used for data collection, cross-checking, and clarification.

Primary Interviews and Surveys

Primary work was used to validate the demand pool and translate it into a practical market model, especially where public data is broad or delayed. We spoke with a mix of generic drug manufacturers, contract development and manufacturing stakeholders, distributors, pharmacists, and clinicians to confirm product coverage, pricing direction, and substitution behavior across the main regions. Regional feedback helped us correct for differences in regulatory timing, device switching, and tendering effects that are not visible in a single public dataset.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 21% | APAC: 43% |

| Mid tier: 45% | Functional/Unit leaders: 35% | EMEA: 33% |

| Smaller Players: 22% | Managers: 44% | Americas: 24% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where therapy demand for asthma, COPD, and allergic rhinitis is reconstructed from prevalence and treated-patient patterns, then filtered through generic penetration and route-of-administration suitability. Those demand pools are converted into value using price and mix assumptions across inhalation formats (such as DPI and pMDI) and nasal sprays, followed by adjustments for channel mix across retail, hospital, and online pharmacies.

We then corroborate the totals with selective bottom-up checks, including sampled product-level price points multiplied by estimated volumes, plus supplier and channel checks on where the highest-selling generics sit in the mix. Key inputs used in the model include treated patient counts, generic substitution rates after exclusivity loss, mix shifts across device types, regional pricing pressure from tenders and reimbursement, and the timing of approvals and launches. Forecasts rely mainly on scenario analysis, because uptake can move sharply when new generics launch, or when device switching and propellant transitions change prescribing habits, and those scenarios were tuned using expert consensus from interviews. When data gaps appear at country or segment level, we use proxy indicators from comparable markets and then re-test the output with primary feedback before finalizing.

Data Validation & Update Cycle

Validation is handled through multiple checks so that one weak data point does not drive the full outcome. We compare the model outputs against independent signals such as respiratory prescription direction, approval and launch timing, and regional channel mix, and then investigate large variances before sign-off. If an assumption changes materially, like a high-impact launch, a pricing event, or a policy update, the team re-contacts sources to confirm the direction and magnitude.

Reports are refreshed annually, and interim updates are made when major events can alter the near-term view. Before delivery, an analyst does a fresh review pass so the numbers reflect the latest available public information and any validated market shifts.

Mordor Intelligence's Inhalation and Nasal Spray Generic Drugs Market Size Measured Against Other Published Estimates

Published market sizes for this space can look different even when the topic name is the same, because each study chooses its own boundaries for what counts as generic, which dosage forms are in scope, and how pricing and uptake are projected. Differences also come from the year used as the starting point, the way currencies are converted, and how fast assumptions are refreshed after approvals and launches.

The key gap drivers here usually come down to whether a study treats device-related value as part of the drug market, how it handles combination products and newer inhaler formats, and whether it assumes faster or slower generic substitution after loss of exclusivity. Some estimates also lean heavily on a single region or apply broad pricing trends without checking tender-driven drops, which can move the value line even if volume is steady.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 38.12 B (2026) | |

| Global Consultancy A | USD 32.55 B (2025) | Uses an earlier year and a different time window, and the public summary does not clearly separate drug value from device-related value inside marketed products across regions, which can pull down the total. |

| Trade Journal B | USD 30.08 B (2024) | Anchors the market to a 2024 base and can miss later-cycle generic launches, and it typically applies broad pricing and uptake assumptions without showing how reimbursement and tender effects were validated by country. |

The table shows a spread that mostly comes from base-year choice and from how combination products, inhaler formats, and device-related value are treated, and in Mordor Intelligence's model, only generic inhalation and nasal spray medicines sold as drug-device products are counted, with pricing and substitution checks refreshed using approval timing and channel feedback so the total stays tied to the treated demand pool.

Key Questions Answered in the Report

What is the current Inhalation and Nasal Spray Generic Drugs Market size?

The market is valued at USD 38.12 billion in 2026 and is forecast to reach USD 56.33 billion by 2031.

Who are the key players in Inhalation and Nasal Spray Generic Drugs Market?

Akorn, Inc., Cipla Inc., Novartis AG (Sandoz ), Teva Pharmaceuticals Inc and Apotex Inc. are the major companies operating in the Inhalation and Nasal Spray Generic Drugs Market.

Which is the fastest growing region in Inhalation and Nasal Spray Generic Drugs Market?

Asia-Pacific is projected to expand at a 10.18% CAGR, driven by healthcare access expansion and regulatory harmonization.

Which drug class holds the largest share?

Corticosteroids command 34.92% of 2025 revenue due to their central role in anti-inflammatory therapy.

Page last updated on: