Atopic Dermatitis Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

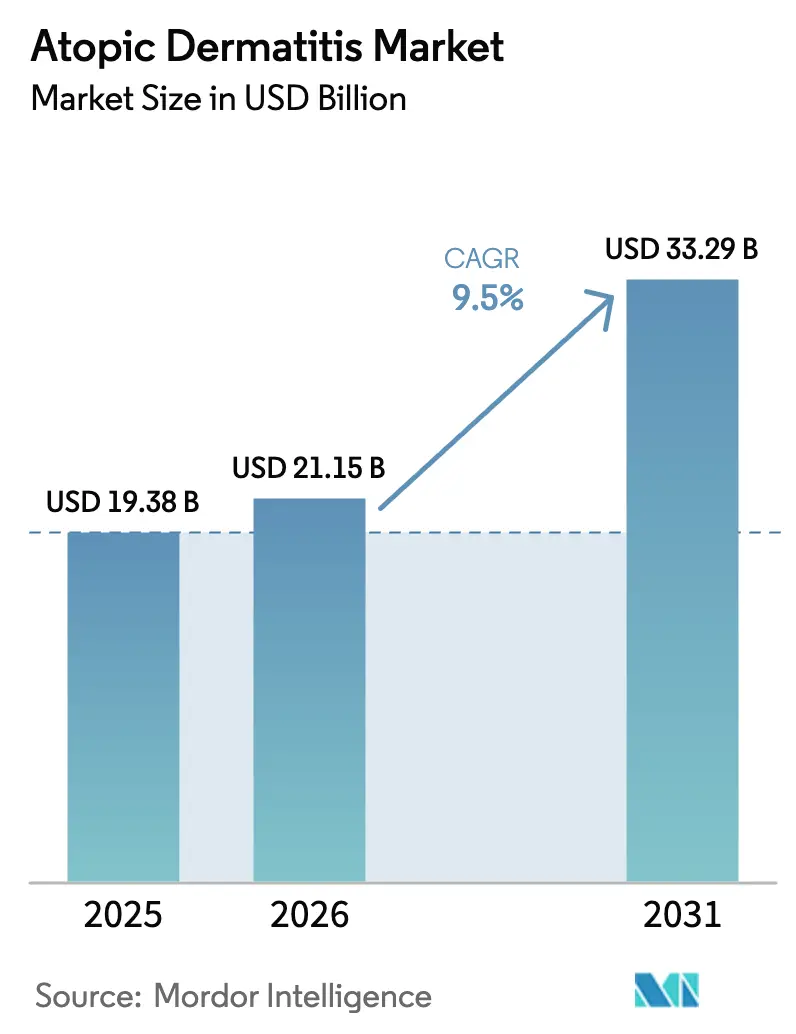

| Market Size (2026) | USD 21.15 Billion |

| Market Size (2031) | USD 33.29 Billion |

| Growth Rate (2026 - 2031) | 9.50% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Atopic Dermatitis Market Analysis by Mordor Intelligence

The Atopic Dermatitis Market size is projected to be USD 19.38 billion in 2025, USD 21.15 billion in 2026, and reach USD 33.29 billion by 2031, growing at a CAGR of 9.5% from 2026 to 2031.

Demand is shifting from corticosteroid monotherapy to targeted biologics and JAK inhibitors that modulate IL-4, IL-13, and JAK-STAT signaling, providing durable control for moderate to severe disease. Regulatory agencies accelerated approvals in 2024-2025, compressing the time from Phase III readout to commercial launch. Payers in China, India, and Southeast Asia began reimbursing biologics soon after approval, ending the long lag that previously slowed uptake. Tele-dermatology and AI-enabled diagnostic tools reduced referral delays, resulting in earlier treatment initiation and higher lifetime therapy value. Competitive strategies center on differentiated dosing schedules, rapid-onset topical delivery systems, and real-world evidence packages that enhance payer negotiations.

Key Report Takeaways

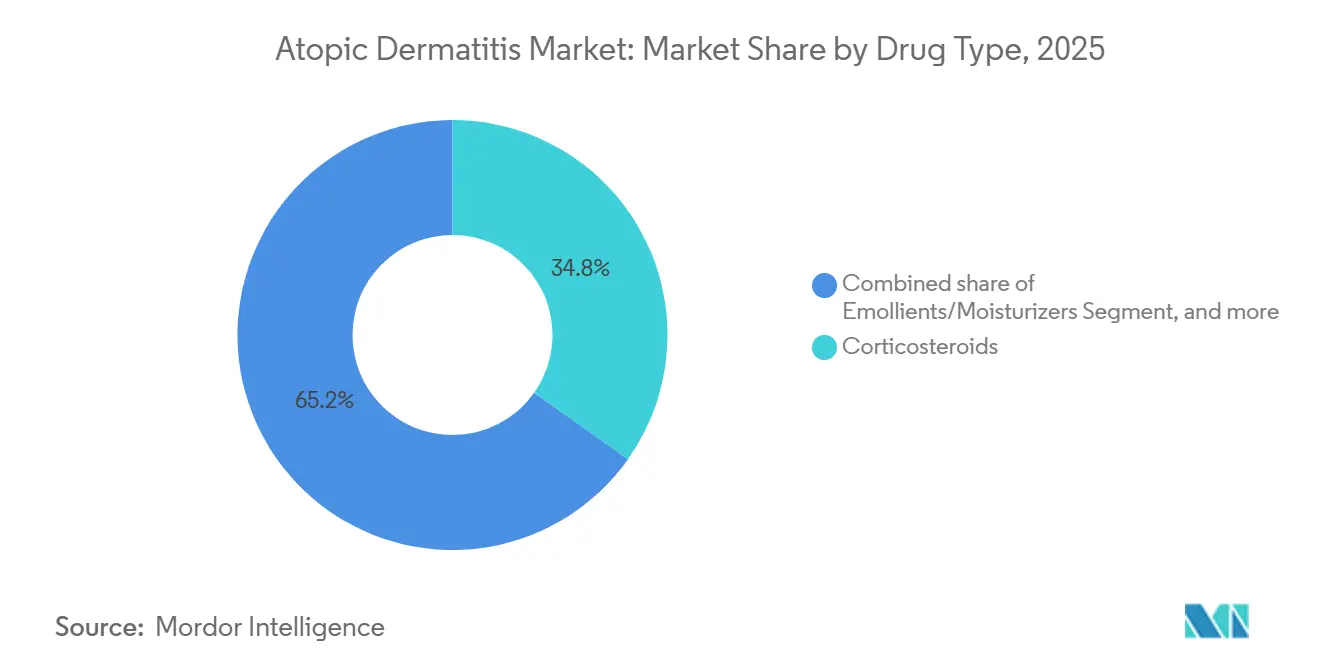

- By drug class, corticosteroids held 34.80% of the atopic dermatitis market share in 2025, while IL-4, IL-13, and JAK inhibitors are forecast to expand at an 11.20% CAGR through 2031.

- By route of administration, topical formulations captured 61.20% share of the atopic dermatitis market size in 2025, whereas injectables are advancing at a 10.5% CAGR to 2031.

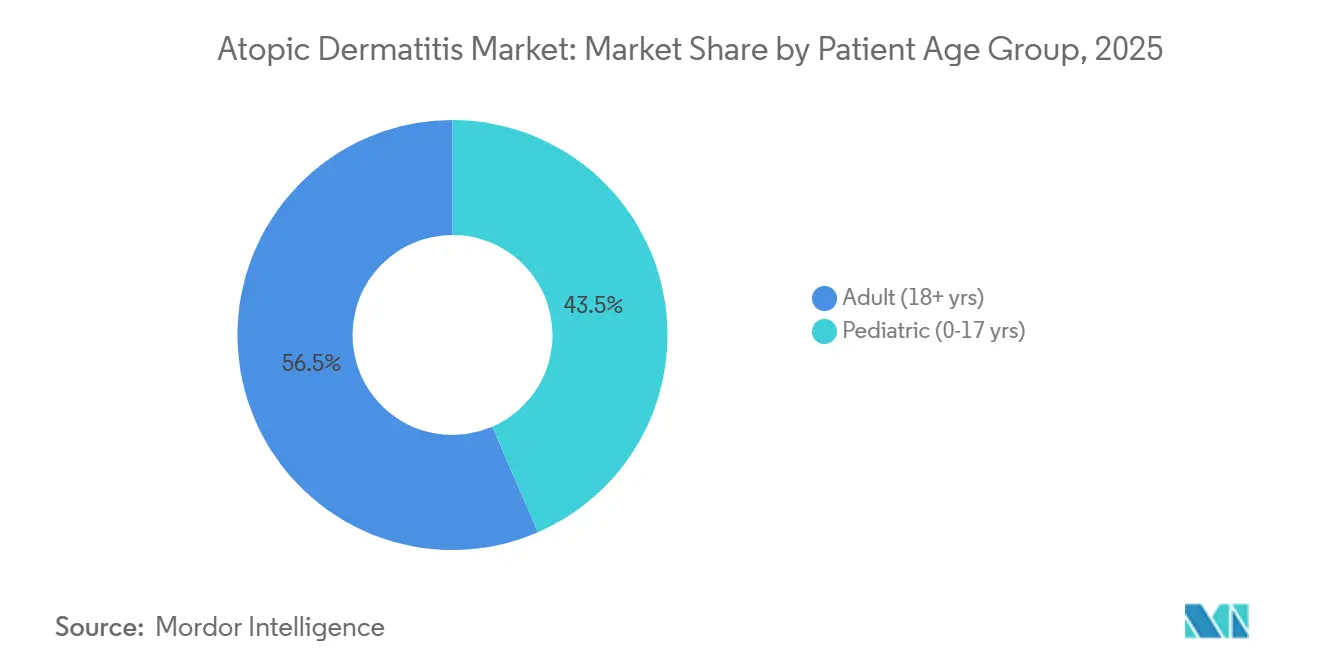

- By patient age group, adults led with 56.50% revenue share in 2025; the pediatric cohort is projected to grow at a 9.90% CAGR through 2031.

- By distribution channel, retail pharmacies accounted for 48.70% of the atopic dermatitis market size in 2025, while online pharmacies and tele-dermatology platforms are projected to scale at an 11.60% CAGR from 2026 to 2031.

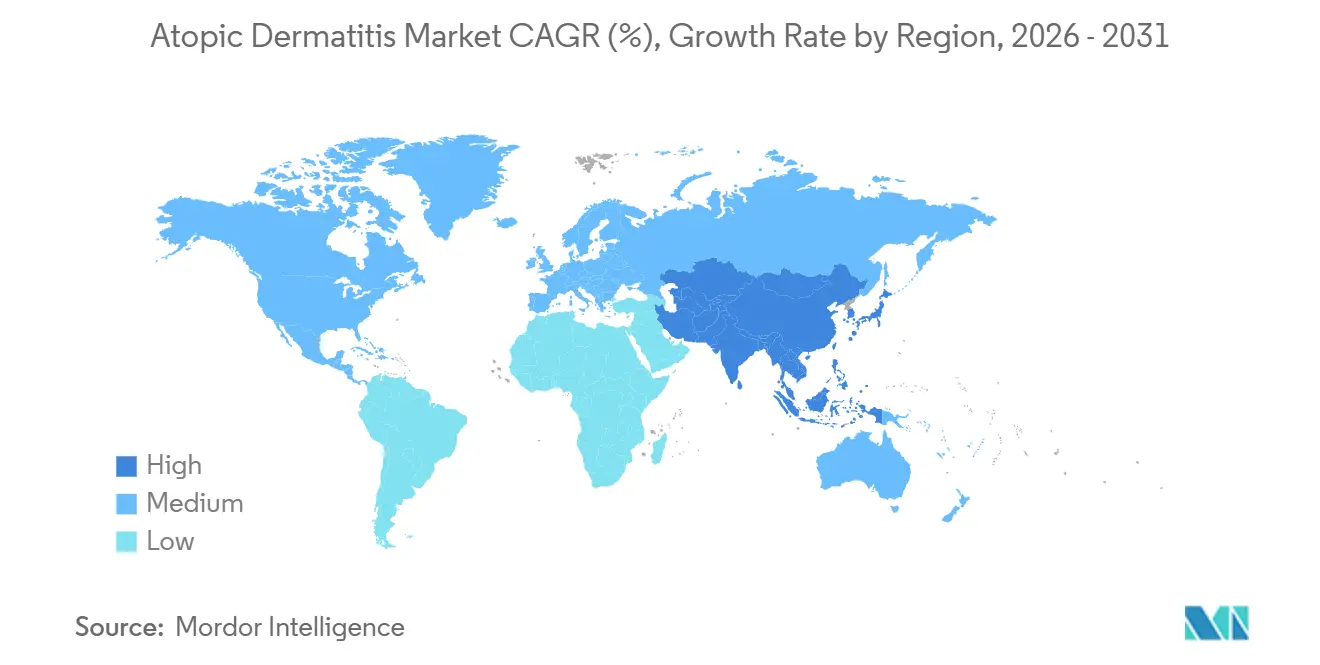

- By geography, North America commanded 41.30% atopic dermatitis market share in 2025; Asia-Pacific is set to post the fastest regional growth at a 10.90% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Atopic Dermatitis Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Global Disease Burden Across Pediatric And Adult Populations | +1.8% | Global, pronounced increases in Asia-Pacific and urban Latin America | Medium term (2-4 years) |

| Accelerated Regulatory Approvals Of First-In-Class Biologics And JAK Inhibitors | +2.3% | North America and Europe lead, Asia-Pacific follows with 12-18 month lag | Short term (≤ 2 years) |

| Expansion Of Universal Healthcare And Private Insurance Coverage In Emerging Markets | +1.5% | Asia-Pacific core (China, India, Thailand) with spill-over to Gulf states | Long term (≥ 4 years) |

| AI-Enabled Decision Support Improving Early Diagnosis And Personalized Treatment | +0.9% | North America and Europe, pilots in Singapore and South Korea | Medium term (2-4 years) |

| Advancements In Skin Microbiome-Modulating Therapeutics | +1.2% | Early trials in North America and Europe, growing interest in Asia-Pacific | Long term (≥ 4 years) |

| Consumer Shift Toward Steroid-Sparing Regimens And Clean-Label Topicals | +1.0% | Global, strongest in North America and Western Europe | Short to medium term |

| Source: Mordor Intelligence | |||

Rising Global Disease Burden Across Pediatric and Adult Populations

Prevalence climbed to 15-20% among children and 7-10% among adults in industrialized nations by 2025, while emerging economies recorded a faster incidence linked to urbanization and diminished early-life microbial exposure[1]World Health Organization, “Global Burden of Atopic Dermatitis Report 2025,” who.int. The expanding patient pool sustains demand for both maintenance therapy and flare management, which reduces exposure to economic cycles. Pediatric onset frequently persists into adulthood, creating lifetime treatment trajectories that raise switching costs once a biologic achieves control. The Asia-Pacific region shows the steepest incidence curve, likely tied to rapid urban migration and air quality degradation. Payers are moving from reactive rescue therapy toward proactive maintenance, favoring long-acting injectables. The demographic tailwind therefore supports both volume and price growth through 2031.

Accelerated Regulatory Approvals of First-In-Class Biologics And JAK Inhibitors

Regulators issued eight key approvals or label expansions between January 2024 and September 2025, tripling the pace of the prior five-year period. The FDA cleared lebrikizumab in September 2024 for the treatment of adults with moderate to severe disease. AbbVie gained U.S. adolescent labeling for upadacitinib in May 2024, enlarging its eligible population by over one million patients. Japan’s PMDA approved abrocitinib for pediatrics in March 2024, confirming JAK1 selectivity as appropriate for younger cohorts. Harmonized review procedures across FDA, EMA, and PMDA shortened global rollout timelines and reduced late-stage capital intensity, which encourages smaller biotechs to push novel mechanisms into Phase III.

Expansion of Universal Healthcare and Private Insurance Coverage in Emerging Markets

China placed tralokinumab on its National Reimbursement Drug List in December 2024 at a price nearly 50% below Western benchmarks. India’s private insurers began covering biosimilar dupilumab in early 2025, slashing out-of-pocket costs for the urban middle class. Thailand’s risk-sharing contract with Sanofi ties reimbursement to patient-reported outcomes, an approach that could be adopted in other ASEAN markets. Gulf Cooperation Council nations are exploring similar value-based frameworks. These changes chip away at historic access gaps and create demand surges that sustain double-digit growth even as North American and European markets mature.

AI-Enabled Decision Support Improving Early Diagnosis And Personalized Treatment

Dermatology clinics now utilize imaging algorithms that can distinguish atopic dermatitis from look-alike disorders with an accuracy rate above 90%. The average diagnostic latency has dropped by three weeks, enabling earlier initiation of targeted therapy. Machine-learning models derived from electronic health records inform first-line treatment decisions between IL-4/IL-13 inhibition and JAK blockade, reducing trial-and-error cycles. Tele-dermatology platforms integrated these algorithms, achieving diagnostic concordance with in-person visits. Payers now reimburse AI-supported pathways at higher rates, reinforcing adoption. Early intervention in pediatrics may alter lifelong disease trajectory, offering long-term economic benefits.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Annual Therapy Costs Limiting Patient Access To Novel Systemic Agents | −1.4% | Global, most acute among uninsured North American patients and cash-pay Asia-Pacific markets | Short term (≤ 2 years) |

| Ongoing Safety And Label Restriction Concerns For JAK Inhibitors | −1.1% | North America and Europe, with scrutiny extending to Asia-Pacific submissions | Medium term (2-4 years) |

| Suboptimal Long-Term Adherence To Injectable Biologics In Real-World Settings | −0.8% | Global, more pronounced where patient-support programs are limited | Medium to long term |

| Cold-Chain And Bioprocess Capacity Constraints Increasing Supply Risk | −0.7% | Global, especially emerging markets lacking robust logistics infrastructure | Short to medium term |

| Source: Mordor Intelligence | |||

High Annual Therapy Costs Limiting Patient Access to Novel Systemic Agents

Wholesale acquisition costs exceeded USD 40,000 for dupilumab and USD 35,000-38,000 for upadacitinib and abrocitinib in the United States during 2025. Assistance programs lower costs for commercial plans but exclude Medicare beneficiaries under anti-kickback rules, leaving gaps for older adults. In India, biosimilar dupilumab priced at USD 12,000 still represents several times the median income, limiting uptake to urban elites. Step-therapy mandates impose 6-12 month delays and may worsen disease. Cold-chain logistics further inflate injectable prices. Biosimilars after 2028 are expected to compress costs, but exclusivity for newer biologics will persist until 2030.

Ongoing Safety and Label Restriction Concerns for JAK Inhibitors

The FDA boxed warning in 2021 highlighted infection, malignancy, and cardiovascular risks observed in rheumatoid arthritis trials[2]U.S. Food and Drug Administration, “JAK Inhibitor Safety Communication,” fda.gov. Although real-world atopic dermatitis data show lower baseline risk, prescribers must document consent and monitor labs, which discourages primary-care adoption. The EMA recommends reserving JAK inhibitors for patients who fail biologics, placing them third line across many EU markets. Parental risk aversion further limits pediatric uptake. Manufacturers will need multi-year post-marketing studies to ease restrictions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: Biologics Outpace Legacy Corticosteroids

Corticosteroids retained 34.8% of the revenue in 2025, yet IL-4, IL-13, and JAK inhibitors are forecast to grow at 11.2% annually through 2031, nearly double the broader atopic dermatitis market's CAGR. Dupilumab alone generated USD 11.6 billion in sales in 2024, of which roughly 60% came from atopic dermatitis. The atopic dermatitis market size for biologics is projected to expand sharply once pediatric and emerging-market coverage deepen. Calcineurin inhibitors and PDE4 topicals occupy mid-tier positions, but newer options, such as ruxolitinib cream, are gaining traction due to their faster itch relief. Patent expiries between 2028 and 2029 will open the space for biosimilars; however, complex antibody manufacturing will limit the field to a handful of entrants.

Broader prescribing authority is sliding toward dermatologists, with allergists and primary-care doctors referring sooner for biologic evaluation. Eli Lilly’s lebrikizumab differs in its monthly dosing regimen after the loading phase, addressing adherence fatigue associated with every-other-week regimens and potentially capturing a larger share of the atopic dermatitis market. Emollients remain foundational but low-revenue. Stewardship programs constrain antibiotic use. Collectively, biologics and JAK inhibitors reshape revenue distribution in the atopic dermatitis market.

By Route Of Administration: Injectables Gain On Adherence Advantage

Topicals accounted for 61.2% of revenue in 2025, yet real-world adherence falls below 50% beyond three months. Injectables are expanding at a rate of 10.5% annually, driven by monthly or bi-weekly biologics that reduce the dosing burden. The atopic dermatitis market size for injectables is expected to grow as biosimilar entry after 2028 reduces cost barriers. Oral JAK inhibitors offer once-daily convenience but face boxed-warning resistance. Arcutis’s once-daily roflumilast foam achieved USD 45 million in 3Q-2024 revenue, driven by strong physician adoption. Leon Pharma’s delgocitinib cream secured FDA Fast Track status in 2024, indicating regulatory acknowledgment of the need for steroid-sparing topicals. Over time, injectables backed by robust patient support programs should continue to gain allocation within the atopic dermatitis market.

By Patient Age Group: Pediatric Approvals Unlock High-Growth Cohort

Adults accounted for 56.5% of the patient volume in 2025; however, pediatric prescriptions are projected to grow at a rate of 9.9% per year. The FDA extended the approval of dupilumab to infants as young as six months in June 2024. Japan approved abrocitinib for adolescents in March 2024. Early biologic use can prevent disease progression, reduce allergen sensitization, and lower lifetime care costs, positioning the pediatric cohort as a strategic accelerator of the atopic dermatitis market. Parental concern about corticosteroid side effects amplifies demand for steroid-free solutions. Adult patients, meanwhile, drive uptake of oral options for convenience during working years. The atopic dermatitis market share for pediatric biologics is expected to advance steadily as coverage expands.

By Distribution Channel: Tele-Dermatology Fuels Online Pharmacy Surge

Retail pharmacies controlled 48.7% of the revenue in 2025, thanks to their widespread storefronts and immediate topical dispensing. Online pharmacies and telehealth platforms are projected to grow at a rate of 11.6% through 2031, as patients increasingly value virtual consultations and home delivery, particularly for cold-chain injectables. Tele-dermatology visits in the United States increased from 5% in 2019 to 28% in 2025. Specialty online pharmacies integrate AI-powered refill alerts and nurse hotlines, which can reduce discontinuation rates by up to 20%. In 2024, FDA guidance allowed the remote prescribing of biologics after a single in-person evaluation, removing a barrier that had previously limited tele-dermatology to topical-centric approaches. Retail chains are launching digital storefronts but face higher overhead than digital natives. As a result, the online segment is poised to capture a growing share of the atopic dermatitis market.

Geography Analysis

North America generated 41.30% of the 2025 revenue, bolstered by broad insurance coverage and early adoption of biologics. Medicare Part D reimburses dupilumab, and commercial plans usually approve biologics after one topical failure. Canada added tralokinumab to provincial formularies in mid-2024, diversifying options. Growth is moderating as penetration nears 40% of eligible moderate-to-severe patients, yet biosimilar entry after 2028 may reopen the pool by reducing cost barriers. The United States tele-dermatology infrastructure also amplifies biologic persistence, fostering steady refill cycles that stabilize the atopic dermatitis market.

Asia-Pacific is projected to grow at a 10.9% CAGR through 2031. China’s December 2024 inclusion of tralokinumab in the reimbursement list and India’s biosimilar dupilumab launch at a 40% discount underpin momentum. Japan subsidizes biologics for topical-refractory cases, though hospital-based administration slows access. South Korea signed data-linked risk-sharing agreements in 2025 that tie payment to real-world outcomes. Australia’s benefits scheme listed lebrikizumab in 2025 as a second-line treatment. Environmental drivers, such as air pollution and dietary changes, continue to elevate the prevalence, reinforcing demand.

Europe shows moderate expansion. Germany reimburses biologics only after a documented failure of both topical steroids and phototherapy, which can extend lead times by up to 12 months. NICE criteria in the United Kingdom restrict prescribing to high-severity cases, suppressing volume. France and Italy focus on the biological use in hospital settings, which reduces convenience. South America remains nascent. Brazil’s private insurers began covering dupilumab in 2024, but public plans did not adopt biologics, resulting in a two-tier market. Gulf states test value-based biologic contracts. Overall, regional divergences in payer policy drive uneven penetration; however, momentum in the Asia-Pacific region compensates for slower European ramp-ups, sustaining global expansion of the atopic dermatitis market.

Competitive Landscape

Sanofi-Regeneron’s dupilumab controlled roughly 55-60% of biologic revenue in 2025 thanks to first-mover status, broad age labels, and over 500,000 patient-years of safety data. AbbVie’s upadacitinib and Pfizer’s abrocitinib share a similar market position by offering oral dosing, yet boxed warnings and step-therapy hurdles temper their growth. Eli Lilly’s lebrikizumab entered the market in late 2024 with monthly maintenance dosing and a 10-15% list price discount to expedite formulary wins. Arcutis and Dermavant seek differentiation through foam and microemulsion topicals that enhance cosmetic acceptability, appealing to patients who are reluctant to escalate to systemic therapy. Patent cliffs for first-generation calcineurin inhibitors invite generic rivals, while biosimilars for dupilumab could reach Europe after 2028.

Real-world evidence is a core battleground. Sanofi sponsors registries to document long-term remission rates, data that anchor value-based payer contracts. AbbVie integrated behavioral therapy modules into its patient app to address pruritus-induced anxiety, providing holistic outcomes that strengthen its negotiation stance. Manufacturing scalability also matters; Sanofi invested USD 250 million in 2024 to expand dupilumab capacity at Framingham, adding two bioreactor lines by late 2026. Emerging mechanisms include microbiome modulators such as Evelo’s EDP1815, now in Phase II with data showing 35% severity reduction at 16 weeks. The field remains moderately concentrated yet dynamic, with differentiation based on dosing convenience, safety perception, and digital support ecosystems.

Atopic Dermatitis Industry Leaders

Sanofi

AbbVie Inc.

Eli Lilly & Co.

Pfizer Inc.

Leo Pharma A/S

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: LEO Pharma A/S submitted a label expansion application to the European Medicines Agency (EMA) to extend the use of Anzupgo (delgocitinib) cream to adolescents aged 12 to 17 with moderate to severe chronic hand eczema in the EU. The application aims to address cases where topical corticosteroids are insufficient or unsuitable. The EMA has accepted the application for review.

- December 2024: FDA approved Nemluvio (nemolizumab-ilto), a biologic developed by Galderma. It is designed for people aged 12 and older with moderate to severe atopic dermatitis. The medication is used in conjunction with topical corticosteroids and/or calcineurin inhibitors when other treatments are insufficient.

- December 2024: FDA granted approval for Vtama (tapinarof) cream (1%), a nonsteroidal topical treatment from Dermavant, an Organon company. It is indicated for managing atopic dermatitis in both adults and children aged 2 years and older. This marks a new option for treating this skin condition.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the atopic dermatitis market as all prescription or over-the-counter pharmacologic products, ranging from basic emollients to advanced biologic or JAK inhibitors, sold for the prevention, control, or long-term management of atopic eczema in human patients across all age groups. According to Mordor Intelligence, digital therapeutics and non-drug cosmetics are kept outside the revenue pool to avoid double counting with adjacent skincare categories.

Scope exclusion: Non-prescription cosmetics marketed purely for cosmetic skin hydration are out of scope.

Segmentation Overview

- By Drug Class

- Corticosteroids

- Emollients / Moisturizers

- IL-4, IL-13 & JAK (PDE4) Inhibitors

- Calcineurin Inhibitors

- Antibiotics & Antiseptics

- Other Drug Classes

- By Route Of Administration

- Topical

- Oral

- Injectable / Parenteral

- By Patient Age Group

- Pediatric (0-17 Yrs)

- Adult (18+ Yrs)

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies & Drug Stores

- Online Pharmacies & Tele-Dermatology Platforms

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest Of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest Of Asia-Pacific

- Middle-East And Africa

- GCC

- South Africa

- Rest Of Middle East And Africa

- South America

- Brazil

- Argentina

- Rest Of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interview practicing dermatologists, payer pharmacists, hospital buyers, and patient advocacy leads across North America, Europe, and Asia-Pacific. Conversations clarify real-world switching triggers, typical biologic dosing regimens, and expected price erosion once biosimilars arrive, which helps us fine-tune model assumptions.

Desk Research

We begin by mapping disease prevalence and therapy adoption from publicly available epidemiology files published by the World Health Organization, the International Eczema Council, the US CDC's National Center for Health Statistics, Eurostat, and Japan's MHLW. Regulatory dossiers (FDA Drugs@, EMA EPARs) and patent trends captured through Questel reveal launch timelines and exclusivity cliffs that influence forecast uptake. Company 10-Ks, D&B Hoovers financials, and Dow Jones Factiva news flows supply baseline sales and pipeline disclosures. Trade associations such as the American Academy of Dermatology and the European Federation of Allergy and Airways Diseases Patients' Associations provide treatment pattern benchmarks. This list is illustrative; many additional secondary sources inform our view.

Market-Sizing & Forecasting

A top-down prevalence to treated cohort reconstruction establishes the demand pool, which is then tested with selective bottom-up roll-ups of sampled average selling price multiplied by volume reported by key suppliers. Core variables feeding the model include diagnosed prevalence by severity band, biologic penetration rates, median annual therapy cost, country-level reimbursement breadth, and anticipated biosimilar launch year. Multivariate regression links therapy volume to economic indicators (GDP per capita) and policy levers (national insurance coverage), while scenario analysis captures upside from pipeline approvals. Gaps in bottom-up inputs are bridged using median proxy values gathered through channel checks and adjusted during validation.

Data Validation & Update Cycle

Outputs pass three layers of variance testing, historical back-casting checks, cross-source triangulation, and peer review. Reports refresh every twelve months; material regulatory or safety events trigger ad hoc revisions. Before client delivery, a fresh analyst pass ensures the file reflects the most recent data cut.

Why Mordor's Atopic Dermatitis Baseline Earns Decision-Maker Trust

Published estimates diverge because firms pick different therapy baskets, price assumptions, and refresh cadences. Our disciplined scope setting and annual model rebuild keep results aligned with verifiable market signals.

Key gap drivers include varying inclusion of OTC moisturizers, inconsistent biologic pricing curves, and differing update schedules. Some publishers report aggressive pipeline uptake without validating reimbursement timings, while others apply flat price corridors that understate biologic inflation.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 19.30 B (2025) | Mordor Intelligence | - |

| USD 17.64 B (2024) | Global Consultancy A | Includes only drug sales tracked through hospital pharmacies, excludes retail and online channels |

| USD 12.10 B (2024) | Industry Publisher B | Omits mild disease emollients and applies uniform 15% biologic discounting absent payer confirmation |

Collectively, these comparisons show that our balanced, transparently sourced baseline, rooted in clear epidemiology and validated price inputs, offers stakeholders a dependable yardstick for sizing opportunities and calibrating strategy.

Key Questions Answered in the Report

How large is the atopic dermatitis market today and how fast is it growing?

The atopic dermatitis market size reached USD 21.15 billion in 2026 and is forecast to grow at a 9.50% CAGR to USD 33.29 billion by 2031.

Which drug class is expanding the fastest?

IL-4, IL-13, and JAK inhibitors are projected to expand at 11.20% per year through 2031, outpacing all other categories.

Why is Asia-Pacific considered the key growth region?

Inclusion of biologics on reimbursement lists in China and India, combined with rising prevalence linked to urbanization, drives a forecast 10.90% CAGR for the region.

What limits adoption of oral JAK inhibitors?

Boxed safety warnings, additional lab monitoring, and payer step-therapy rules weigh on prescriber confidence and slow uptake.

How will biosimilars affect pricing after 2028?

Patent expiries for early biologics should allow biosimilars to enter, which is expected to cut prices by 30-40% and expand access, especially in price-sensitive markets.

Which distribution channel is growing quickest?

Online pharmacies and tele-dermatology platforms are scaling at an 11.60% CAGR as virtual care normalizes and home delivery of biologics becomes routine.

Page last updated on: