Allergic Rhinitis Drugs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 13.23 Billion |

| Market Size (2031) | USD 16.47 Billion |

| Growth Rate (2026 - 2031) | 4.48% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

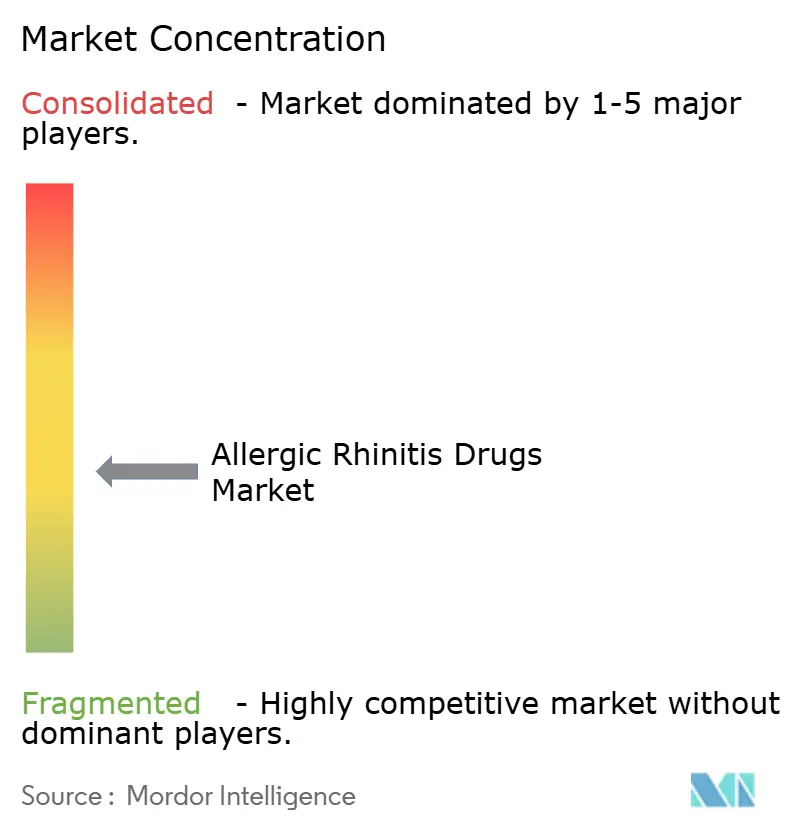

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Allergic Rhinitis Drugs Market Analysis by Mordor Intelligence

The Allergic Rhinitis Drugs Market size was valued at USD 12.72 billion in 2025 and is estimated to grow from USD 13.23 billion in 2026 to reach USD 16.47 billion by 2031, at a CAGR of 4.48% during the forecast period (2026-2031).

Escalating pollen loads linked to climate change, rising urban air-pollution indices, and a steady stream of Rx-to-OTC switches are enlarging the allergic rhinitis drugs market by drawing previously undertreated patients into formal pharmacologic care. Portfolio realignment following the FDA’s move against oral phenylephrine is channeling investment toward intranasal corticosteroids, second-generation antihistamines, and dual-action sprays, while pediatric label extensions in sublingual immunotherapy expand the total addressable base. Digital pharmacies add volume by lowering purchase friction, and biologics such as dupilumab are redefining severe-disease management despite premium pricing. Competitive intensity is shaped by generics eroding tablet margins and originators protecting high-value spray and biologic franchises through lifecycle patents.

Key Report Takeaways

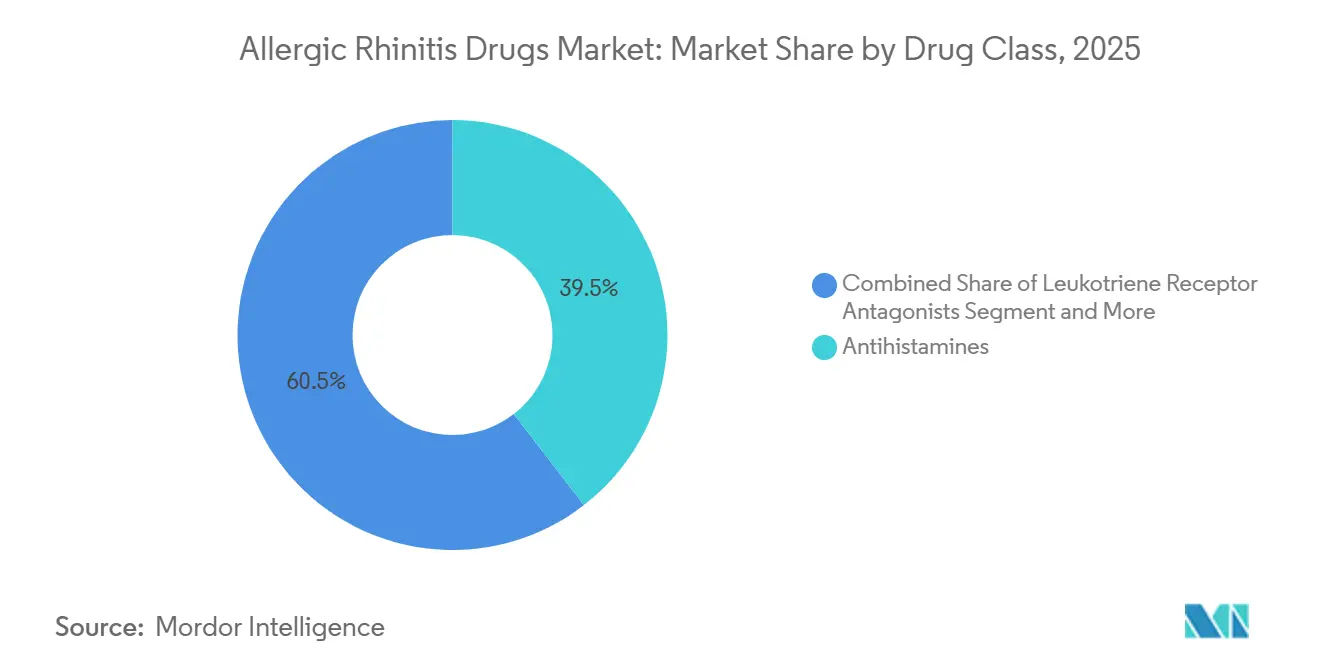

- By drug class, antihistamines led with 39.52% revenue share in 2025, while leukotriene receptor antagonists are projected to record the highest 5.87% CAGR through 2031.

- By dosage form, tablets and capsules accounted for 46.87% of the allergic rhinitis drugs market size in 2025, yet sublingual immunotherapy tablets and drops are advancing at a 5.92% CAGR to 2031.

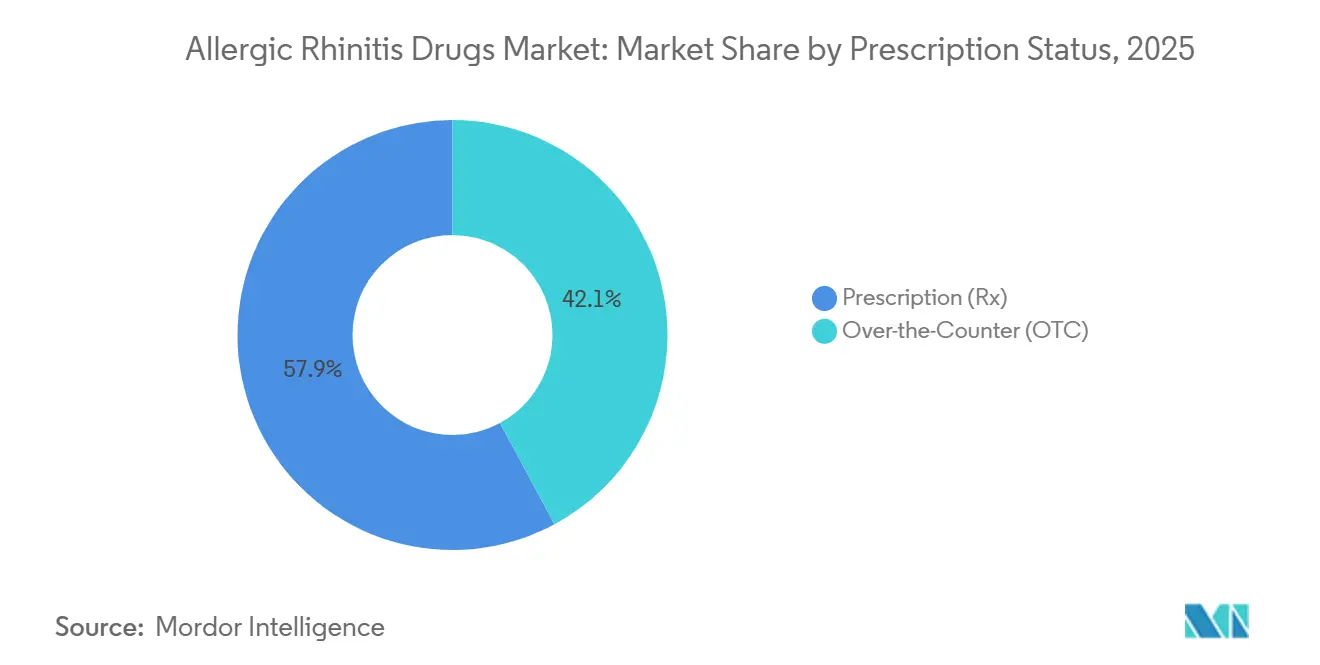

- By prescription status, prescription products captured 57.87% share in 2025, whereas OTC items are forecast to expand at 5.67% CAGR owing to recent Rx-to-OTC switches.

- By distribution channel, hospital pharmacies held 44.29% revenue in 2025; online pharmacies are poised for a 5.71% CAGR as e-commerce permeates chronic-therapy refills.

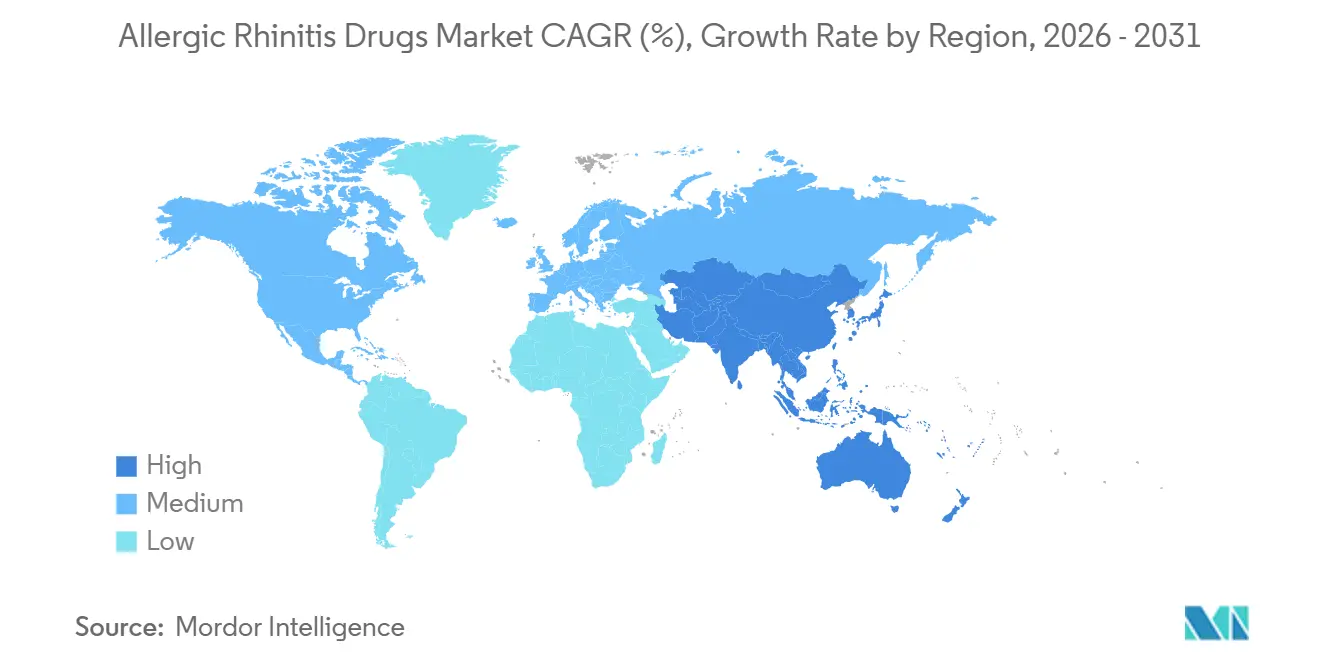

- By geography, North America commanded 38.95% allergic rhinitis drugs market share in 2025, yet Asia-Pacific is on track for the fastest 5.21% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Allergic Rhinitis Drugs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Longer pollen seasons intensify symptom burden | +0.8% | North America and Europe | Medium term (2-4 years) |

| Air pollution exacerbates symptom severity | +0.7% | China, India, wider Asia-Pacific | Long term (≥ 4 years) |

| E-commerce and online pharmacies expand access | +0.6% | North America, Europe, urban Asia-Pacific | Short term (≤ 2 years) |

| Rx-to-OTC switches and dual-action sprays | +0.5% | North America, Europe | Short term (≤ 2 years) |

| Non-sedating daytime regimens | +0.4% | Global | Medium term (2-4 years) |

| SLIT launches and pediatric labels | +0.9% | North America, Europe, emerging Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Longer Pollen Seasons Intensify Symptom Burden

Since 1990, the U.S. pollen season has lengthened by roughly three weeks, with spring arriving earlier and the first fall frost coming later[1]Climate Central, “Pollen Season and Climate Change,” CLIMATECENTRAL.ORG. Europe shows a similar trend, with pollen counts now starting one to two weeks sooner than they did twenty years ago. A longer exposure window pushes many seasonal sufferers to take medicine for a larger part of the year. Work-safety rules also nudge employers to recommend non-sedating antihistamines and fast-acting nasal sprays instead of older, drowsiness-inducing drugs. Together, these forces steer patients toward once-daily leukotriene tablets or even multi-year sublingual immunotherapy, which lifts annual spending per patient.

Air Pollution Exacerbates Symptom Severity and Duration

Fine particles and nitrogen dioxide make pollen grains stickier and more irritating, which worsens allergic rhinitis symptoms. In Singapore, house-dust-mite sensitization touches 85% to 90% of residents, and more than half of people in humid Chinese coastal cities test positive as well. Weed pollen, particularly mugwort and ragweed, reaches up to 50% positivity in northern China skin tests. India shows a 20% to 30% allergic-rhinitis rate, with Parthenium pollen affecting up to one-third of patients in some regions. Elevated air pollution primes the nasal lining for quicker flare-ups and longer recovery, helping to explain why Asia-Pacific is projected to grow faster than any other region.

E-commerce and Online Pharmacies Expand OTC Access

Digital platforms let shoppers compare prices, set up auto-refills, and avoid extra trips during peak allergy season. Streamlined e-pharmacy rules in the European Union and a growing patchwork of reciprocal state licenses in the United States further support the shift. Brick-and-mortar pharmacies respond by matching web prices and pushing private labels, which squeezes margins but broadens the overall market as cost-conscious buyers step up their use of modern antihistamines and nasal sprays.

Rx-to-OTC Switches and Dual-Action Combination Sprays

The FDA cleared Perrigo’s Nasonex 24HR Allergy, a mometasone nasal spray, for direct retail sale, bringing prescription-strength relief to store shelves. Combination sprays that blend an antihistamine with a corticosteroid offer faster relief than steroids alone; Glenmark’s Ryaltris and Sandoz’s azelastine-fluticasone product demonstrate this advantage. As more brands jump categories, long-standing prescription products lose volume, yet the overall market grows because casual sufferers now treat themselves sooner. Generic makers such as Apotex, Amneal, and Padagis quickly filed for competing versions, pointing to sharper price competition ahead.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| FDA move against oral phenylephrine | -0.5% | United States | Short term (≤ 2 years) |

| Montelukast boxed warning | -0.3% | North America and Europe | Medium term (2-4 years) |

| Adherence gaps for intranasal steroids | -0.4% | Global | Long term (≥ 4 years) |

| Reimbursement and logistical barriers to AIT | -0.5% | North America, Europe, emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

FDA Move Against Oral Phenylephrine Undercuts Decongestants

In late 2024, the FDA proposed pulling oral phenylephrine from the OTC monograph after advisors ruled the standard 10 mg dose ineffective. This ruling threatens hundreds of multi-symptom cold-and-allergy tablets and forces drugmakers to reformulate or exit the aisle[2]United States Food and Drug Administration, “Advisory Committee Meeting on Oral Phenylephrine,” FDA.GOV. Pseudoephedrine still works but stays behind the counter because of methamphetamine controls, limiting spontaneous buys. Some companies are eyeing topical sprays such as oxymetazoline, yet the risk of rebound congestion after just a few days of use tempers long-term demand. Diversified firms like Haleon can pivot to antihistamine-steroid blends, while smaller brands that leaned on phenylephrine face shelf cuts and tighter margins.

Montelukast Boxed Warning Cools Prescriber Enthusiasm

The FDA added a boxed warning to montelukast over neuropsychiatric risks, causing doctors to reserve the drug for patients who fail antihistamines or nasal steroids. Despite the caution, cheap generics from companies such as Teva and Cipla keep monthly costs below USD 10 in the United States, so volume remains steady. Insurers, however, now require prior authorization, and some European regulators echo the U.S. stance, further dampening first-line use. This climate opens the door for safer leukotriene-pathway drugs, though none have reached late-stage trials yet.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: Shift From Mature Antihistamines to Targeted Therapies

Antihistamines generated the largest allergic rhinitis drugs market size with 39.52% contribution in 2025, yet leukotriene receptor antagonists and biologics are escalating faster with 5.87% CAGR through 2031. Second-generation oral agents remain everyday staples, but boxed warnings and emerging IL-4/IL-13 inhibitors reshape clinician algorithms. Dupilumab’s new rhinosinusitis label shows biologics can carve specialized niches with high reimbursement acceptance. Competitive pressure pushes innovators toward dual-action sprays and novel pathways, while generics sustain affordability for volume-driven antihistamines, keeping the allergic rhinitis drugs market balanced between accessibility and innovation.

Legacy decongestants face uncertainty, accelerating the pivot to combination nasal sprays that merge rapid relief with anti-inflammatory efficacy. Sublingual immunotherapy gains credibility through pediatric data and streamlined EU trial guidance, positioning the class to lift the allergic rhinitis drugs market share of disease-modifying treatments albeit from a low base.

By Dosage Form: Tablets Dominate, Nasal and Sublingual Lead Growth

Oral dosage forms such as tablets & capsules commanded nearly 46.87% share of 2025 revenue, reflecting the convenience premium consumers place on once-daily tablets. Yet nasal sprays and sublingual tablets headline innovation, posting the highest CAGRs as they align with patient desires for rapid onset or needle-free disease modification. The allergic rhinitis drugs market share for sprays is fortified by OTC switches, while SLIT tablets benefit from new pediatric indications.

Injectable SCIT retains a procedural niche but carries time burdens that hinder uptake; conversely, Health Canada’s approval of a nasal epinephrine spray highlights patient enthusiasm for on-demand, device-free delivery modalities. These dynamics signal continued diversification of formats inside the allergic rhinitis drugs market.

By Prescription Status: OTC Channel Captures Incremental Users

Prescription items still anchor absolute revenue with 57.87% share in 2025, owing to biologics, SLIT, and physician-mandated sprays, yet OTC growth of 5.67% CAGR through 2031 outpaces as Rx-to-OTC switches intensify consumer self-direction. The allergic rhinitis drugs market size attached to OTC platforms climbs on digital pharmacy penetration, expansion of private-label generics, and extended allergy seasons that spur impulse shopping.

Regulatory divergence influences the tempo; the FDA’s monograph system streamlines U.S. switches, whereas the EMA requires formal variation dossiers, delaying European shelf debuts. Nevertheless, value-priced generics proliferate globally, broadening allergic rhinitis drugs market reach among cost-conscious consumers.

By Distribution Channel: Hospitals Hold Complexity, Online Adds Convenience

Hospital and specialty pharmacies manage biologics and in-office immunotherapy, retaining the largest allergic rhinitis drug market share with 44.29% in 2025 for high-acuity therapies. Yet online pharmacies post the fastest gains with 5.71% CAGR through 2031, capturing chronic tablet and spray refills through subscription bundles and real-time price comparison tools.

Retail chains respond with private labels and omnichannel loyalty programs, aiming to defend foot traffic. Payer policies, such as retail-only SLIT dispensing, create geographic channel asymmetries that modulate allergic rhinitis drugs market evolution. Over the forecast period, e-commerce is expected to shift an expanding slice of volume away from brick-and-mortar formats without entirely displacing them.

Geography Analysis

North America remains the largest regional node, responsible for 38.95% of 2025 revenue, buoyed by insurance coverage for biologics and entrenched OTC culture, but CMS fee-schedule cuts and phenylephrine delisting temper near-term upside. Longer pollen seasons extend treatment windows, enlarging the allergic rhinitis drugs market beyond traditional spring peaks. Canada’s approval of needle-free epinephrine and pediatric SLIT underscores regulatory openness to novel delivery, while Mexico’s urbanization enlarges demand against a backdrop of rising private insurance.

Europe benefits from broadly reimbursed intranasal steroids and immunotherapy, yet national formularies vary, influencing uptake heterogeneity. Germany’s full SLIT reimbursement contrasts with selective NHS coverage in the UK, shaping an uneven allergic rhinitis drugs market landscape. The EMA’s low-sample guideline eases smaller-manufacturer entry, and OTC dual-action launches ahead of allergy seasons illustrate agile commercialization.

Asia-Pacific is the fastest-growing arena at 5.21% CAGR as house-dust-mite sensitization surpasses 85% in many coastal cities and weed-pollen positivity rises in northern China. Glenmark’s China approval for Ryaltris and multinational alliances on SLIT herald deeper penetration of premium sprays and immunotherapies, yet affordability constraints keep generics pivotal. Regulatory agencies in China, Japan, and South Korea quicken reviews for pediatric formulations, further enlarging the allergic rhinitis drugs market. Middle East, Africa, and South America trail but show urban-center pockets of accelerated growth as disposable incomes climb.

Competitive Landscape

The allergic rhinitis drugs market features moderate concentration; top multinationals defend high-margin biologics and intranasal franchises while generics manufacturers commoditize oral and single-agent sprays. Sanofi’s dupilumab achieved a ninth indication in February 2026, proving biologics’ ability to open new revenue layers through indication stacking, and gaining 99% private U.S. coverage. Glenmark leverages dual-action sprays to expand in China and prepares direct U.S. marketing to elevate global brand imprint.

Generic wave intensity rose in 2024-2025, with ANDA approvals for azelastine, fluticasone, mometasone, and levocetirizine, compressing prices and redistributing value toward innovation cycles[3]Robins Kaplan LLP, “ANDA Approvals Q2 2024,” ROBINSKAPLAN.COM. Biosimilar entrants, exemplified by Celltrion’s omalizumab analogue Omlyclo, open competition in biologic niches while maintaining high scientific-bar entry.

Lifecycle management centers on pediatric label expansions, device-enabled adherence tools, and Rx-to-OTC transitions. Emerging players target underserved allergens under the EMA’s streamlined guideline, aiming for first-to-market status in narrow indications. Digital adherence platforms and connected nasal devices may become differentiators, though reimbursement models for software-as-a-medical-device remain nascent. Collective activity underscores a market steadily shifting from volume-driven antihistamines to value-driven targeted and combination therapies, sustaining overall allergic rhinitis drugs market momentum.

Allergic Rhinitis Drugs Industry Leaders

Bayer AG

Sandoz

Organon

Haleon plc

Sanofi SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: China Medical System filed an NDA for Comekibart injection, an anti-IL-4Rα monoclonal antibody targeting seasonal allergic rhinitis.

- November 2025: Glenmark won China NMPA approval for Ryaltris, a fixed-dose olopatadine-mometasone nasal spray for adults and children aged ≥ 6 years for treatment of moderate to severe seasonal allergic rhinitis.

Global Allergic Rhinitis Drugs Market Report Scope

As per the scope of the report, allergic rhinitis drugs are medications used to treat allergic rhinitis, a condition caused by an allergic response to airborne allergens such as pollen, dust, or pet dander. These drugs help relieve symptoms like sneezing, nasal congestion, runny nose, itchy eyes, and throat.

The allergic rhinitis drugs market is segmented by drug class, dosage form, prescription status, distribution channel, and geography. By drug class, the market includes antihistamines, immunotherapy, corticosteroids, decongestants, leukotriene receptor antagonists, and others. By dosage form, the segmentation covers tablets and capsules, liquids and syrups, nasal sprays, nasal drops, sublingual tablets/drops (AIT), and injectables (SCIT). Based on prescription status, the market is divided into over-the-counter (OTC) and prescription (Rx) drugs. The distribution channel segmentation includes drugstores and retail pharmacies, hospital pharmacies, online pharmacies/e-commerce, and supermarkets/hypermarkets. Geographically, the market is categorized into North America, Europe, Asia Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Antihistamines |

| Immunotherapy |

| Corticosteroids |

| Decongestants |

| Leukotriene Receptor Antagonists |

| Others (Combination Therapy, Anticholinergics, etc.) |

| Tablets & Capsules |

| Liquids & Syrups |

| Nasal Sprays |

| Nasal Drops |

| Sublingual Tablets/Drops (AIT) |

| Injectables (SCIT) |

| Over-the-Counter (OTC) |

| Prescription (Rx) |

| Drugstores & Retail Pharmacies |

| Hospital Pharmacies |

| Online Pharmacies / E-commerce |

| Supermarkets/Hypermarkets |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Drug Class | Antihistamines | |

| Immunotherapy | ||

| Corticosteroids | ||

| Decongestants | ||

| Leukotriene Receptor Antagonists | ||

| Others (Combination Therapy, Anticholinergics, etc.) | ||

| By Dosage Form | Tablets & Capsules | |

| Liquids & Syrups | ||

| Nasal Sprays | ||

| Nasal Drops | ||

| Sublingual Tablets/Drops (AIT) | ||

| Injectables (SCIT) | ||

| By Prescription Status | Over-the-Counter (OTC) | |

| Prescription (Rx) | ||

| By Distribution Channel | Drugstores & Retail Pharmacies | |

| Hospital Pharmacies | ||

| Online Pharmacies / E-commerce | ||

| Supermarkets/Hypermarkets | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the estimated value of allergic rhinitis drugs in 2026 and the forecast for 2031?

Spending is projected to rise from USD 13.23 billion in 2026 to USD 16.47 billion by 2031, reflecting a 4.48% CAGR.

Which therapeutic class shows the fastest growth through 2031?

Leukotriene receptor antagonists are set to advance at about 5.87% CAGR through 2031, outpacing antihistamines and steroids.

How quickly are over-the-counter allergy products expanding compared with prescription options?

OTC formulations are on track for roughly 5.67% CAGR through 2031, faster than prescription counterparts, thanks to Rx-to-OTC switches and online sales.

Why is the Asia-Pacific region expected to lead growth?

Rapid urbanization, high dust-mite sensitization, and rising household incomes push the region toward a forecast 5.21% CAGR through 2031.

What has the FDA's move against oral phenylephrine meant for decongestant pills?

The planned revocation of phenylephrine's OTC monograph forces reformulations and trims a once-significant revenue stream.

Which drug-delivery formats are gaining acceptance for allergen immunotherapy?

Needle-free nasal sprays and pediatric-approved sublingual tablets are expanding access and adherence for long-term disease modification.

Page last updated on: