Asthma Drugs Market Size and Share

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

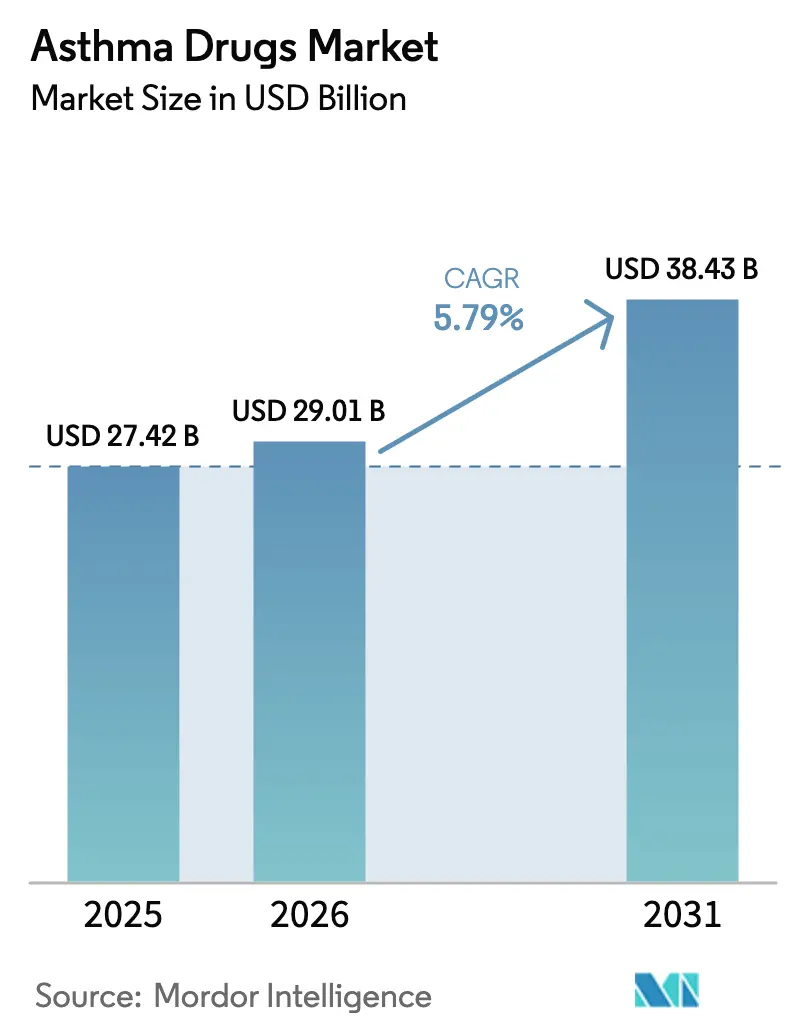

| Market Size (2026) | USD 29.01 Billion |

| Market Size (2031) | USD 38.43 Billion |

| Growth Rate (2026 - 2031) | 5.79% CAGR |

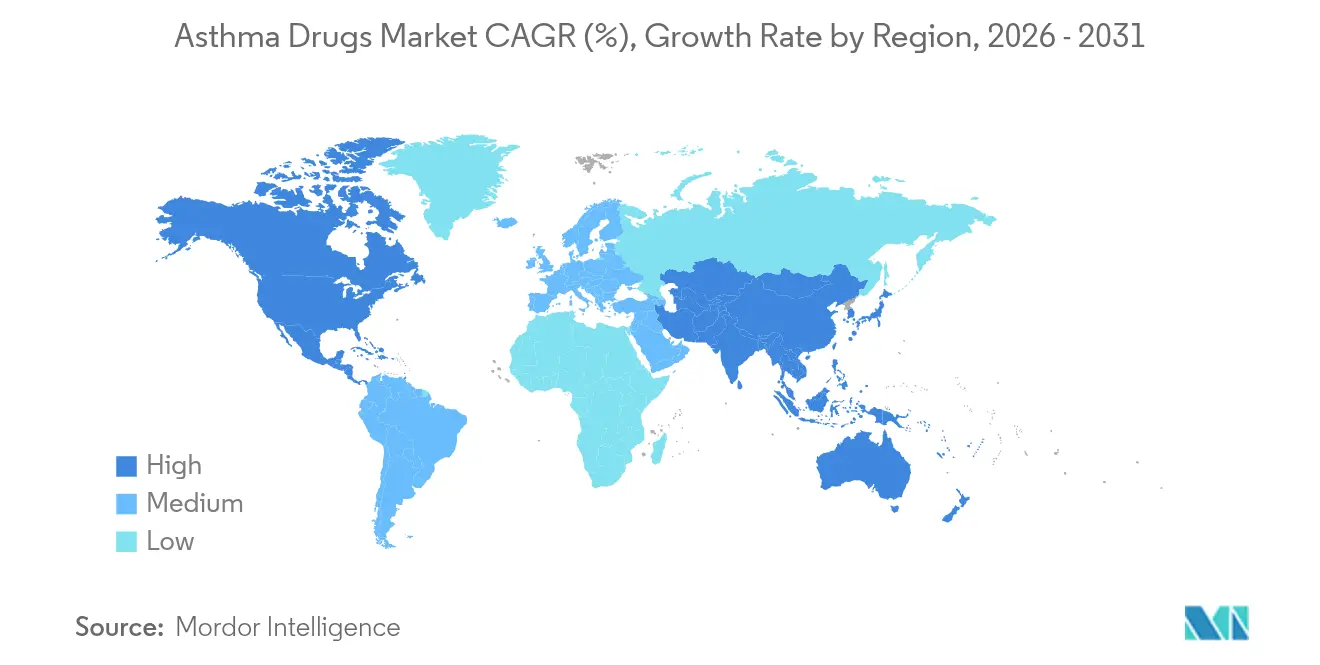

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asthma Drugs Market Analysis by Mordor Intelligence

The asthma drugs market size was valued at USD 27.42 billion in 2025 and estimated to grow from USD 29.01 billion in 2026 to reach USD 38.43 billion by 2031, at a CAGR of 5.79% during the forecast period (2026-2031). Growth stems from precision-medicine biologics, green-propellant inhalers and smart devices that lift adherence while easing regulatory pressure on hydrofluoroalkanes. Manufacturers are pairing artificial-intelligence phenotyping with targeted monoclonal antibodies, raising per-patient spend and lengthening product life cycles. North America keeps the largest regional hold, yet Asia-Pacific delivers the fastest expansion as reimbursement widens for home monitoring and digital therapeutics. Adult patients dominate demand, but pediatric prescriptions climb fastest because early biologic intervention is filling the post-Flovent therapy gap. Competition centers on balancing generic-pressured bronchodilators with premium biologics, while online channels scale quickly as post-pandemic buyers favor direct-to-home supply models.

Key Report Takeaways

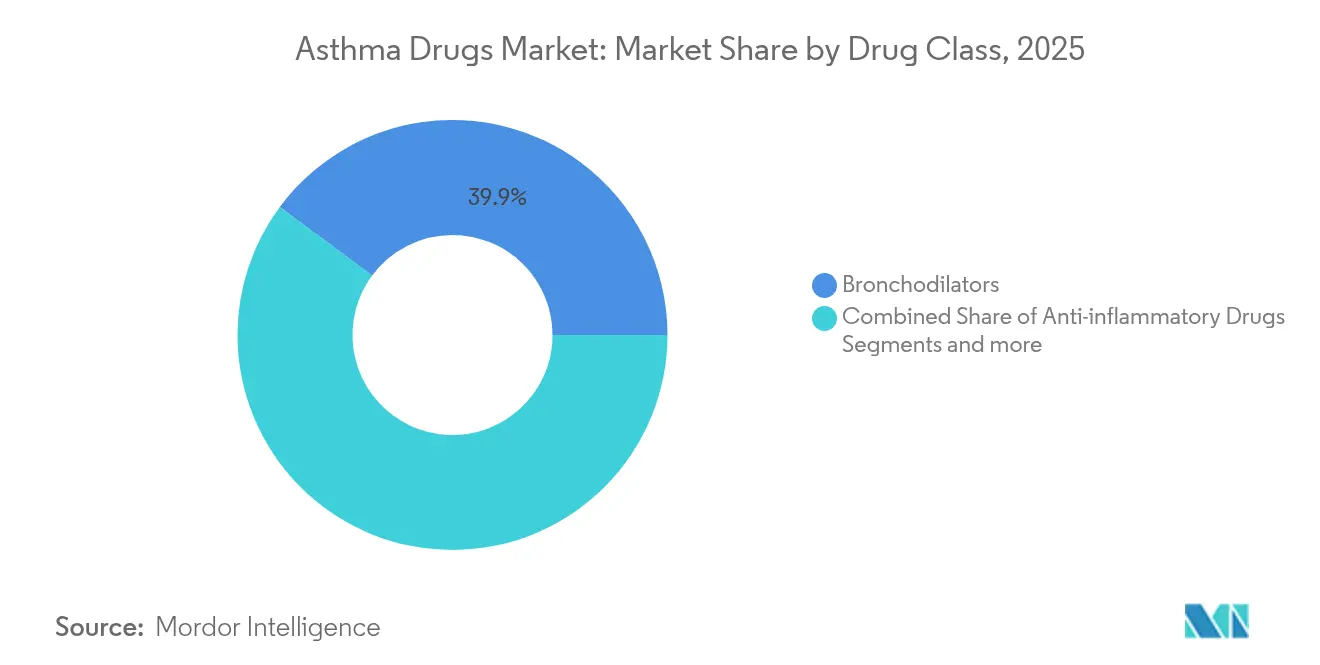

- By drug class, bronchodilators led with 39.85% of the asthma drugs market share in 2025, while monoclonal antibodies and biologics are projected to expand at a 6.56% CAGR to 2031.

- By route of administration, inhaled therapies accounted for 67.60% share of the asthma drugs market size in 2025; injectable products are advancing at a 6.44% CAGR through 2031.

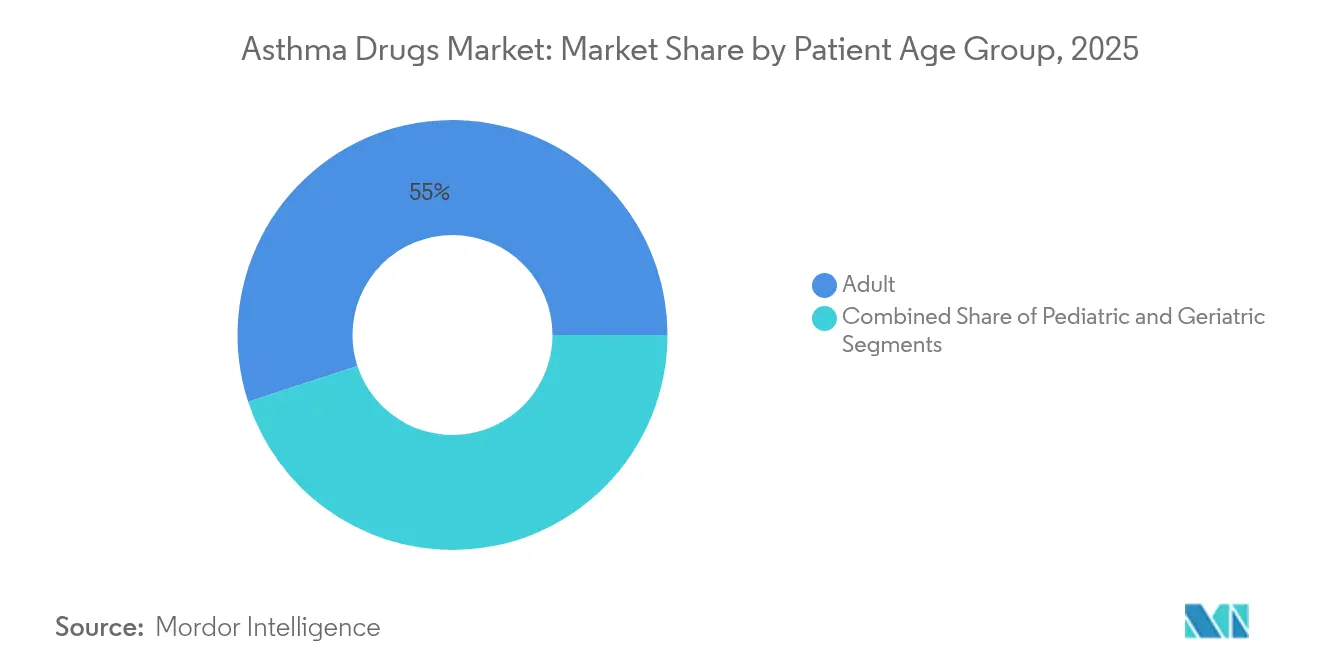

- By patient age group, adults held 55.02% of the asthma drugs market share in 2025, whereas pediatric treatments post the highest 6.58% CAGR toward 2031.

- By distribution channel, hospital pharmacies captured 40.92% revenue share in 2025, yet online pharmacies record the strongest 6.73% CAGR through 2031.

- By geography, North America occupied 39.20% of the asthma drugs market in 2025, and Asia-Pacific registers the quickest 6.69% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Asthma Drugs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increase in incidence & prevalence of asthma | +1.2% | Global, with highest impact in APAC and MEA | Long term (≥ 4 years) |

| Technological advancements in smart & digital inhalers | +0.8% | North America & EU core, spill-over to APAC | Medium term (2-4 years) |

| Growing geriatric population with higher asthma burden | +0.9% | North America, Europe, Japan | Long term (≥ 4 years) |

| Eco-friendly propellant mandates driving inhaler replacement | +1.1% | Global, led by EU regulations, US following | Short term (≤ 2 years) |

| AI-driven phenotyping enabling precision biologic prescriptions | +0.7% | North America & EU initially, expanding globally | Medium term (2-4 years) |

| Home-based smart monitoring reimbursement expansion (APAC) | +0.5% | APAC core, with early adoption in Singapore, Taiwan | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increase in incidence & prevalence of asthma

Urbanization, pollution and lifestyle change continue to enlarge the global patient pool, securing lasting demand for maintenance and rescue regimens. Multinational firms therefore view the asthma drugs market as a stable platform to fund biologic pipelines. In lower-income regions inconsistent access to inhaled corticosteroids exposes latent volumes, encouraging value-priced formulations. Broader phenotyping now detects severe phenotypes sooner, steering clinicians toward targeted antibodies that lift revenue per script. The expansion ultimately anchors a predictable baseline that supports long-horizon R&D investment across the asthma drugs market.

Technological advancements in smart & digital inhalers

Sensor-equipped inhalers capture dose timing, flow rate and ambient triggers, then relay data to clinicians, cutting non-adherence that affects 43% of patients. Drug makers bundle devices, software and medicines into service contracts, shifting their role from pill suppliers to outcomes partners. Artificial-intelligence algorithms mine inhaler feeds to anticipate exacerbations, positioning connected devices as diagnostic adjuncts. These innovations forge sticky ecosystems inside the asthma drugs market, because competing products without data loops appear less valuable to payers.

Growing geriatric population with higher asthma burden

Elderly patients experience more severe attacks and comorbidities, moving rapidly from inhaled corticosteroids to high-price biologics. Combination injectables with infrequent dosing help minimize polypharmacy risk, aligning with clinicians’ drive to simplify regimens. Manual-dexterity decline also tilts preference toward injections that bypass inhaler technique issues. Health systems incentivize therapies that keep seniors out of hospitals, supporting premium pricing for drugs showing real-world reductions in admissions. Consequently, geriatric demand strengthens revenue density within the asthma drugs market.

Eco-friendly propellant mandates driving inhaler replacement

The phase-out of high global-warming-potential propellants compels full portfolio reformulation. Early movers such as AstraZeneca, which completed phase III trials for a 99.9% lower-impact Breztri, gain a compliance edge [1]AstraZeneca, “Breztri Next-Generation Propellant Clinical Data,” astrazeneca.com. Rapid device changeovers open a quasi-patent cliff for incumbents yet erect fresh entry barriers for firms lacking reformulation capital. Demand also shifts toward dry-powder inhalers that avoid propellants, widening choice for environmentally minded purchasers and accelerating churn inside the asthma drugs market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulatory approval timelines | -0.6% | Global, with highest impact in US and EU | Medium term (2-4 years) |

| Adverse effects & safety concerns of existing drugs | -0.4% | Global, particularly affecting biologics adoption | Long term (≥ 4 years) |

| Supply-chain pressure on HFA propellants after 2027 bans | -0.8% | Global, with acute impact in regions dependent on MDIs | Short term (≤ 2 years) |

| High cost of biologics restricting uptake in LMICs | -0.7% | LMICs, particularly sub-Saharan Africa and South Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent regulatory approval timelines

Complex endpoints, mandatory real-world evidence and longer safety surveillance now stretch biologic reviews by several years. Tezspire’s 4,848-day pathway illustrates the drag on cash flows. Start-ups struggle to finance decade-long programs, raising barriers and consolidating the asthma drugs market around capital-rich incumbents [2]GSK, “FDA Accepts Depemokimab BLA,” gsk.com. Rising trial size further boosts development cost, which in turn feeds into higher launch prices that can provoke payer resistance.

High cost of biologics restricting uptake in LMICs

Annual antibody therapy often exceeds USD 30,000, a price unreachable where essential inhalers already demand weeks of wages. Tiered pricing and assistance programs soften but do not erase the gap, leaving large volumes unpenetrated. Biosimilar entrants such as ADL018 aim to narrow cost spreads yet still depend on complex cold-chain logistics. Without broader affordability, the asthma drugs market loses a share of its potential growth in populous LMIC regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: Biologics Reshape Treatment Paradigms

Bronchodilators controlled 39.85% of the asthma drugs market in 2025 by meeting first-line rescue needs, although patent expiries squeeze margins. Monoclonal antibodies, propelled by better biomarker screening, deliver the swiftest 6.56% CAGR and steadily erode reliance on daily inhaled steroids. GSK’s depemokimab cut severe exacerbations by 54% with semiannual dosing, framing a new adherence benchmark . Anti-inflammatory dual agents, typified by Airsupra, merge symptom relief with disease control, giving prescribers a bridge therapy while patients await biologics.

Pipeline diversity sustains competition inside the asthma drugs industry as firms hedge risk across bronchodilators, corticosteroids and antibody franchises. Combination products gain traction when they simplify regimens and trim device counts, a trend attractive to payers evaluating total-cost metrics. The incremental shift from reactive bronchodilation to proactive inflammation suppression means biologics are set to anchor premium tiers of the asthma drugs market for the next decade.

By Route of Administration: Injectable Biologics Challenge Inhalation Dominance

Inhaled formats still held 67.60% of 2025 sales because patients and clinicians value direct lung delivery and fast onset. Yet the asthma drugs market size for injectable routes is projected to expand briskly alongside biologic uptake, outpacing all other modes at 6.44% CAGR. Sanofi’s Dupixent illustrates how subcutaneous delivery broadens beyond asthma into COPD, maximizing platform leverage.

Device complexity, cold weather performance and propellant regulation collectively nudge stakeholders toward injectables. Meanwhile smart inhalers may slow but not stop share loss by making aerosol devices easier for older users. The next phase of competition hinges on ultra-long-acting injectables that can reduce clinic visits to two per year, an attractive proposition for overstretched health systems and for the premium segment of the asthma drugs market.

By Patient Age Group: Pediatric Biologics Drive Premium Growth

Adults account for 55.02% revenue, reflecting high diagnosis rates and insurance penetration. The asthma drugs market size for pediatric care, however, enjoys the steepest 6.58% CAGR as regulators extend antibody labels down to six years. FDA clearance of benralizumab for 6-11-year-olds opened a wide therapeutic window. Loss of legacy inhaled steroids like Flovent amplifies unmet need, encouraging early biologic initiation.

Parents and clinicians accept higher prices when drugs cut emergency visits and school absenteeism. For geriatric cohorts biologics bring triple wins: lower attack frequency, fewer hospital stays and easier administration than metered-dose inhalers. Together these trends reinforce patient-segment diversity and sustain growth momentum across the asthma drugs market.

By Distribution Channel: Digital Transformation Accelerates Online Growth

Hospital pharmacies commanded 40.92% of 2025 turnover because they integrate infusion suites and biologic cold chain logistics. Online outlets post the fastest 6.73% CAGR, mirroring consumer e-commerce habits and insurer endorsement of lower dispensing fees. Automated refills and data-rich adherence dashboards further entice chronic users of inhaled corticosteroids.

Retail chains remain pivotal for immediate-need bronchodilators but face erosion as specialty injectables migrate to direct-to-home care. Taiwan’s pay-for-performance program, which boosted inhaled steroid adherence and cut emergency visits, shows that aligned incentives can switch channel preferences. Digital delivery efficiency therefore underpins a re-shaping of value flows within the asthma drugs market.

Geography Analysis

North America dominates the asthma drugs market through 2025 because large commercial and Medicare plans reimburse high-priced biologics, while ongoing R&D keeps the region at the innovation frontier. Market participants nonetheless watch patent cliffs and inflation-linked price caps that can erode margins. Canada’s public coverage and Mexico’s IMSS system provide steady basal volumes that complement US premium sales. The region’s future momentum will hinge on successful transition to green-propellant devices ahead of anticipated federal climate mandates.

Asia-Pacific registers the swiftest expansion as China and India scale respiratory clinics and diagnostics, while Japan, Australia and South Korea pay for next-gen biologics. Asian Development Bank programs supporting digital primary care will accelerate adoption of smart inhalers and remote monitoring. Taiwan’s pay-for-performance model already demonstrates drops in hospitalizations when adherence tools are reimbursed, setting a template for neighbors. Regional environmental pollution acts as an inexorable demand driver so companies localize supply chains and craft tiered biologic prices tailored to emerging middle classes.

Europe’s asthma drugs market grows steadier than high-growth APAC but benefits from universal payer systems that ensure consistent uptake of effective drugs. Eco-regulations speed the switch from hydrofluoroalkane-based inhalers to dry-powder devices, adding conversion revenues even as legacy items decline. Shortages of salbutamol until mid-2025 underscore supply-chain vulnerability. Country-specific health-technology-assessment bodies scrutinize cost effectiveness, pushing firms to showcase real-world data before premium pricing approval. Smaller markets inside the European Economic Area leverage joint procurement schemes, giving them negotiating heft that can influence continent-wide list prices.

Competitive Landscape

The asthma drugs market shows moderate consolidation, led by AstraZeneca, GSK and Sanofi. These incumbents protect inhaled franchises while rolling out long-duration antibodies that command superior margins. AstraZeneca aims for USD 80 billion global sales by 2030 on the back of 20 product launches that include respiratory blockbusters. Larger players deploy cash to reformulate inhalers with low-GWP propellants, a capital-intensive race that smaller firms struggle to finance.

White-space entrants exploit technology adjacencies. Adherium partners with manufacturers to embed sensors that transform inhalers into telehealth nodes, creating data-centric revenue streams independent of drug volumes. Aerami and similar start-ups develop nebulized biologics aimed at needle-averse patients, blurring historic lines between device and drug categories. Non-pharma acquirers such as Molex are stepping in, snapping up respiratory specialists like Vectura to vertically integrate electronics and delivery know-how.

Digital enablement has become a differentiator. Companies mine real-world inhaler and claims data to segment patients more precisely, refine trial design and negotiate outcomes-based contracts. Novartis highlights 19% volume growth for Xolair in emergent economies via combined digital outreach and physician education. The upshot is an increasingly data-rich competitive arena where success depends on marrying drug efficacy, device usability and cloud analytics throughout the asthma drugs market lifecycle.

Asthma Drugs Industry Leaders

AstraZeneca

Boehringer Ingelheim GmbH

Novartis AG

Sanofi

Merck & Co. Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: AstraZeneca’s Airsupra cut severe exacerbations by 47% in mild asthma patients in the BATURA study, supporting anti-inflammatory rescue positioning.

- March 2025: FDA accepted GSK’s depemokimab BLA for type 2 asthma and chronic rhinosinusitis with a December 2025 PDUFA date.

- July 2024: Kashiv BioSciences licensed ADL018, a proposed Xolair biosimilar, to Amneal for US commercialization.

- April 2024: FDA approved benralizumab (Fasenra) for severe pediatric asthma in patients aged 6–11 years.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global asthma drugs market as all prescription and approved over-the-counter medicines formulated to prevent or relieve asthma symptoms, including short- and long-acting bronchodilators, inhaled or systemic corticosteroids, leukotriene modifiers, combination therapies, and emerging monoclonal antibodies delivered through inhaled, oral, injectable, or transdermal routes.

Scope Exclusions: Non-pharmacological devices (e.g., inhalers or spirometers), herbal remedies, and drugs indicated only for COPD fall outside this study.

Segmentation Overview

- By Drug Class

- Bronchodilators

- Short-acting ?2 Agonists

- Long-acting ?2 Agonists

- Anticholinergic Agents

- Anti-inflammatory Drugs

- Inhaled Corticosteroids (ICS)

- Leukotriene Modifiers

- PDE-4 Inhibitors

- Others

- Monoclonal Antibodies / Biologics

- Combination Drugs

- Bronchodilators

- By Route of Administration

- Inhaled

- Oral

- Injectable

- Others

- By Patient Age Group

- Pediatric

- Adult

- Geriatric

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts held structured discussions with pulmonologists, hospital pharmacists, wholesale distributors, and payor advisors across North America, Europe, Asia-Pacific, and the Gulf. Their insights on prescription mix shifts, biologic uptake, tender pricing, and rebate practices closed data gaps highlighted during secondary work and strengthened assumption checks.

Desk Research

We first mapped the landscape with open datasets from the World Health Organization, Global Asthma Network, national health portals such as the CDC and Eurostat, drug-approval records from the US FDA and EMA, United Nations Comtrade trade flows, and peer-reviewed clinical journals. Company filings accessed through D&B Hoovers and news archives within Dow Jones Factiva, coupled with Questel patent intelligence, clarified revenue splits, price corridors, and upcoming generic entry. These references illustrate the breadth of material consulted; numerous additional public and paid sources underpinned further validation.

Market-Sizing & Forecasting

A top-down prevalence-to-treated-patient construct converts diagnosed cases into annual drug demand pools, which are then cross-checked against sampled average selling price × volume roll-ups from distributor interviews. Key variables like diagnosed prevalence, controller-to-reliever ratios, biologic penetration, generic price erosion, and adherence rates feed a multivariate regression that projects 2025-2030 sales, with scenario tweaks for patent cliffs and reimbursement changes. Selective bottom-up adjustments correct outliers where local procurement data diverge.

Data Validation & Update Cycle

Model outputs undergo multi-step peer review, variance screening against quarterly manufacturer revenues and prescription audits, and re-runs whenever major approvals, recalls, or tenders occur. Reports refresh annually and receive interim patches for material events, ensuring clients receive the latest view.

Why Mordor's Asthma Drugs Baseline Figures Inspire Confidence

Published estimates often vary because analysts choose different drug baskets, price bases, or currency dates. By anchoring on a clearly disclosed scope and annually refreshed epidemiology, Mordor provides a balanced, decision-ready baseline that buyers can retrace with ease.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 27.42 B (2025) | Mordor Intelligence | - |

| USD 25.17 B (2024) | Global Consultancy A | Excludes newest biologics; fixed 2023 FX rates |

| USD 24.93 B (2025) | Trade Journal B | Captures hospital procurement only; omits retail & OTC |

These contrasts show that once scope, channel coverage, and currency choices align, Mordor's estimate stands as the most transparent midpoint, giving executives a dependable starting point for strategy.

Key Questions Answered in the Report

What is the current value of the asthma drugs market and how fast is it growing?

The asthma drugs market stands at USD 29.01 billion in 2026 and is projected to grow at a 5.79% CAGR to USD 38.43 billion by 2031.

Which drug class is expanding the fastest?

Monoclonal antibodies and other biologics lead growth with a 6.56% CAGR, driven by wider biomarker screening and longer-acting formulations.

Why are injectable routes gaining share when inhalers have been dominant?

Injectable biologics bypass complex inhaler techniques, deliver longer dosing intervals and are unaffected by new propellant regulations, so they post the highest 6.44% CAGR among administration routes.

Which region offers the strongest growth opportunity for suppliers?

Asia-Pacific leads with a 6.69% CAGR thanks to rising reimbursement, pollution-driven prevalence and rapid digital-health adoption.

How are environmental regulations affecting product design?

EU-led mandates to eliminate high-GWP propellants are forcing complete inhaler reformulations, accelerating the switch to dry-powder devices and next-generation propellants with 99.9% lower climate impact.

What channel shift should companies anticipate after the pandemic?

Online pharmacies, supported by automated refill services and direct-to-patient delivery, register the fastest 6.73% CAGR and will keep eroding traditional retail share over the forecast period.

Page last updated on: