Tree Nut Allergy Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

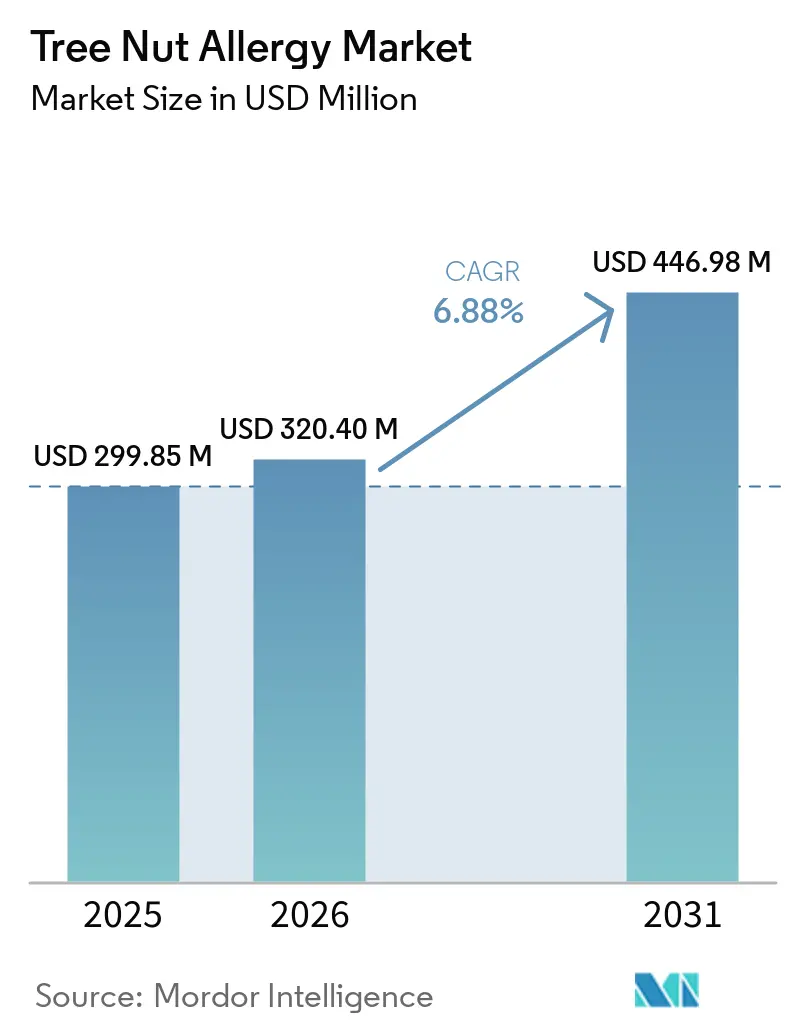

| Market Size (2026) | USD 320.40 Million |

| Market Size (2031) | USD 446.98 Million |

| Growth Rate (2026 - 2031) | 6.88% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Tree Nut Allergy Market Analysis by Mordor Intelligence

The Tree Nut Allergy Market size is projected to expand from USD 299.85 million in 2025 and USD 320.40 million in 2026 to USD 446.98 million by 2031, registering a CAGR of 6.88% between 2026 to 2031.

Regulatory approvals for disease-modifying immunotherapies have facilitated their early adoption. Additionally, the broader application of component-resolved diagnostics and the development of connected epinephrine devices that monitor real-world adherence are driving this growth. Omalizumab's February 2024 approval for multi-food allergy has accelerated payer adoption pathways, provided patients meet specific baseline IgE and diagnostic confirmation criteria.[1]American Academy of Allergy, Asthma & Immunology, “Consensus Guidance on Omalizumab Use,” aaaai.org At the same time, venture funding in precision-allergy platforms is supporting the development of oral, epicutaneous, and intranasal treatment options that aim to deliver durable tolerance. Furthermore, the introduction of smart autoinjectors is reducing administration errors, particularly in the acute management segment.

Key Report Takeaways

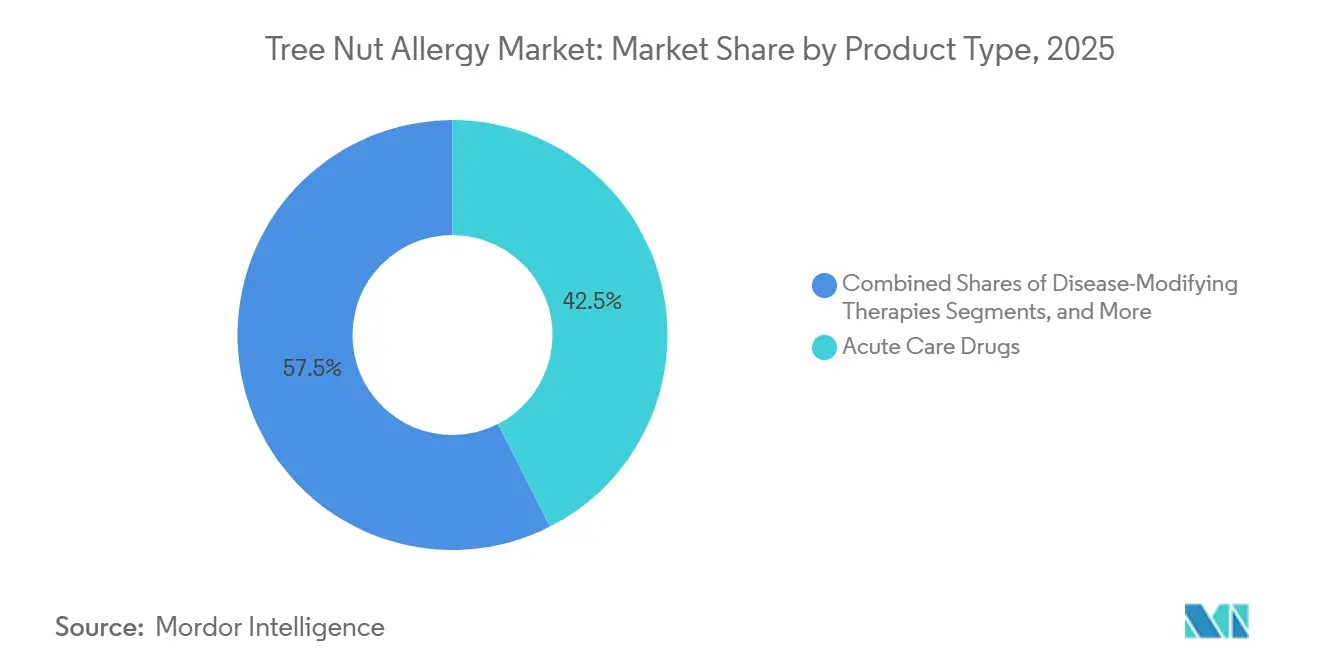

- By product type, acute-care drugs held 42.50% of the tree nut allergy market share in 2025 and disease-modifying therapies are forecast to expand at an 8.88% CAGR through 2031.

- By tree-nut type, walnut accounted for a 28.55% slice of the tree nut allergy market size in 2025, while cashew is expected to grow at a 6.99% CAGR during 2026-2031.

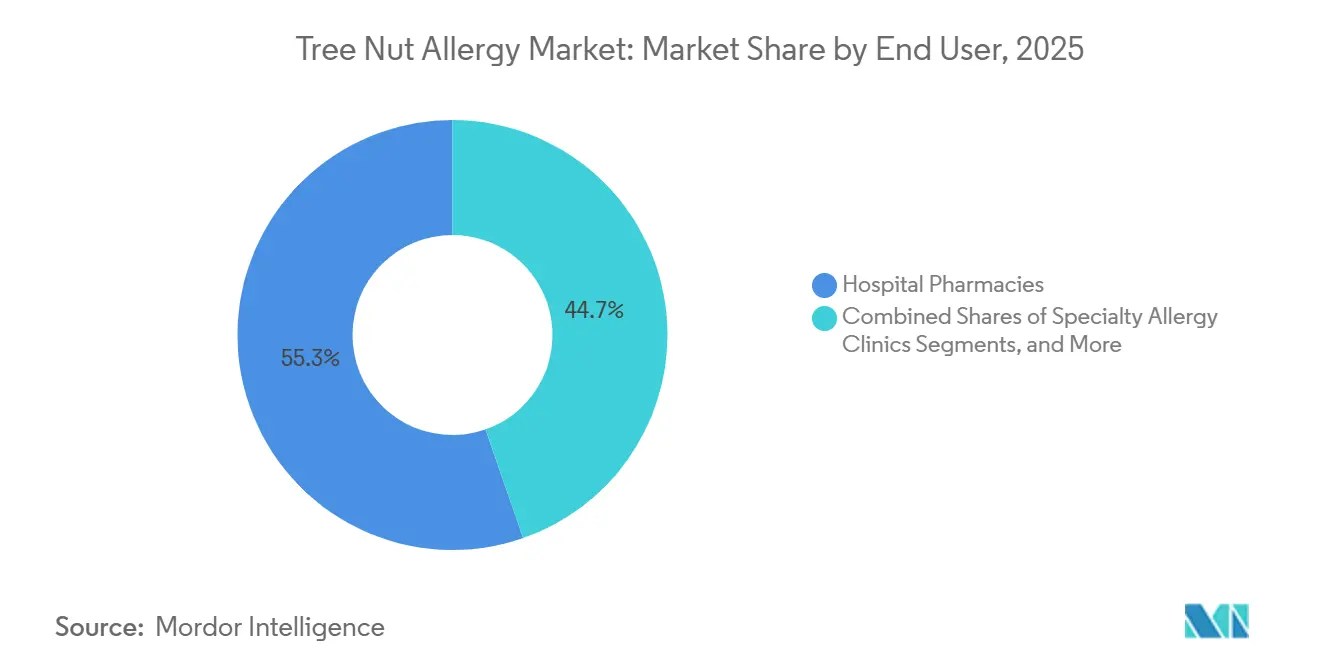

- By end user, hospital pharmacies dominated with 55.34% revenue in 2025; specialty allergy clinics represent the fastest trajectory at an 8.34% CAGR.

- By age group, pediatric patients represented 60.43% of 2025 revenues and are projected to expand at a 7.56% CAGR to 2031.

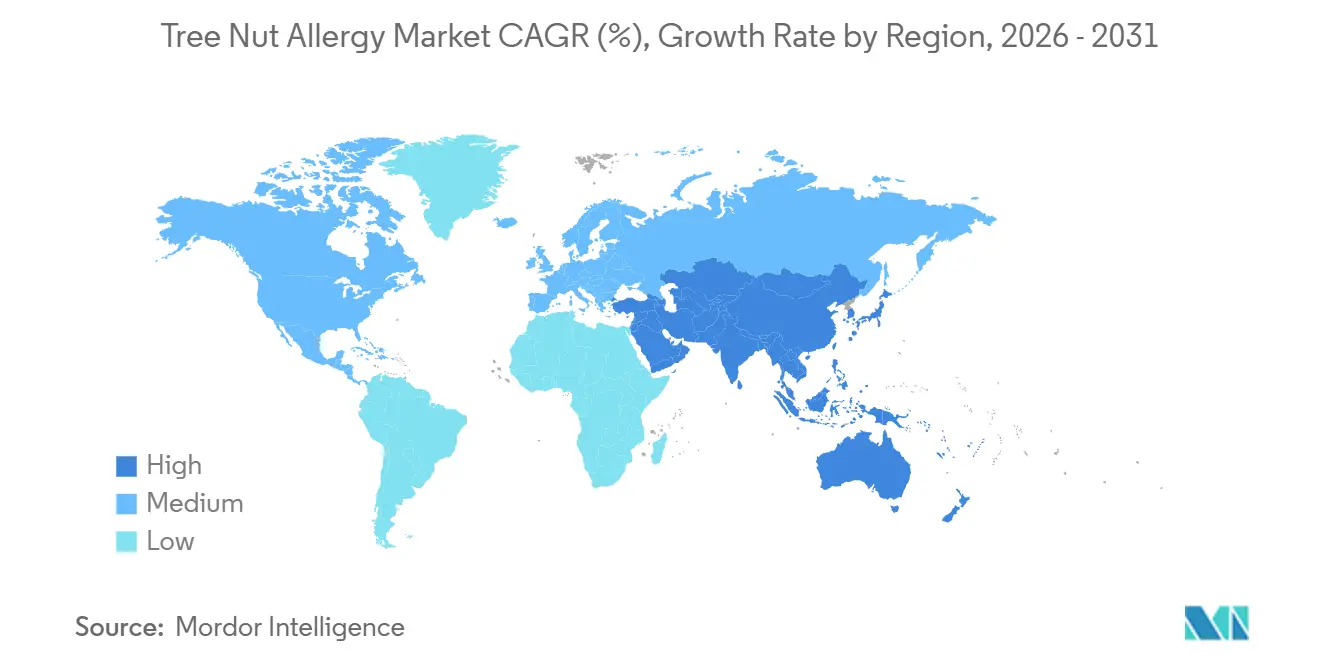

- By geography, North America generated 39.67% of global revenue in 2025, whereas Asia-Pacific is on track for a 7.90% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Tree Nut Allergy Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising pediatric prevalence of IGE-mediated tree-nut allergy | +1.2% | Global, with highest rates in North America, Europe, Asia-Pacific | Medium term (2–4 years) |

| Accelerated approvals of disease-modifying immunotherapies | +1.8% | North America & EU, early adoption in Australia | Short term (≤2 years) |

| Expansion of component-resolved diagnostics (CRD) in clinical practice | +0.9% | Global, led by North America & EU | Medium term (2–4 years) |

| Launch of smart, connected epinephrine autoinjectors with adherence analytics | +0.7% | North America, EU, Japan | Short term (≤2 years) |

| Surging venture capital into AI-enabled precision-allergy platforms | +1.1% | North America, with spill-over to EU and APAC | Long term (≥4 years) |

| Westernization of Asian diets increasing nut exposure | +1.3% | APAC core (China, Japan, South Korea), spill-over to India | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rising Pediatric Prevalence of IgE-Mediated Tree-Nut Allergy

A 2024 Turkish cohort reported that 60% of newly diagnosed tree-nut allergic children experienced multi-system reactions requiring epinephrine.[2]Turkish Journal of Pediatrics, “Multi-system Tree Nut Allergy Presentations in Turkish Children,” turkishjournalpediatrics.org Additionally, a 2025 European registry identified hazelnut, walnut, and cashew as the cause of 73% of pediatric anaphylaxis cases across Germany, France, and Italy.[3]European Allergy Registry, “Pediatric Tree Nut Anaphylaxis in Europe,” eaaci.org The POSEIDON Phase 3 trial demonstrated a 68.4% desensitization rate to 1,000 mg of peanut protein in children aged 1–4 years, highlighting the significance of early-life intervention.[4]Journal of Allergy and Clinical Immunology: Global, “Eliciting Doses Among Japanese Children,” jacionline.org Furthermore, real-world data from France associated sublingual immunotherapy with a 38% reduction in asthma risk, reinforcing its preventive potential.

Accelerated Approvals of Disease-Modifying Immunotherapies (OIT, SLIT, EPIT)

In 2026, DBV Technologies submitted a Biologics License Application following positive VITESSE Phase 3 results, which demonstrated significant desensitization in children aged 4–7 years. In February 2024, Omalizumab became the first anti-IgE therapy approved for multiple food allergies, driving a shift in treatment guidelines toward the integration of biologics. Additionally, ALK-Abelló’s successful peanut-tablet Phase 2 results in April 2026 indicated further diversification in administration methods.

Expansion of Component-Resolved Diagnostics in Clinical Practice

Component-level assays now effectively differentiate high-risk seed-storage proteins, such as Ana o 3 in cashew and Jug r 1 in walnut, from pollen cross-reactive proteins, enabling tailored oral-food challenges. At the 2025 AAAAI symposium, Ana o 3 titers above 0.32 kUA/L were identified as predictive of cashew anaphylaxis. Research from Belgium demonstrated that adopting Component-Resolved Diagnostics (CRD) reduced unnecessary challenges by 34% and facilitated the re-introduction of tolerated nuts in 28% of cases.

Launch of Smart, Connected Epinephrine Autoinjectors with Adherence Analytics

Kaleo’s voice-guided Auvi-Q expanded its product line to include a 0.1 mg infant dose designed for toddlers weighing 7.5–15 kg. Data from 2025 indicated a 19% reduction in hospitalization rates within 24 hours of anaphylaxis when using these advanced devices compared to traditional options. Aquestive Therapeutics is re-submitting Anaphylm, a sublingual epinephrine film, after addressing regulatory feedback in January 2026. If approved, it could become the first needle-free emergency solution.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High cost & limited reimbursement for biologic therapies | -1.4% | Global, most acute in North America & EU | Medium term (2–4 years) |

| Safety & adherence challenges with multi-year immunotherapy protocols | -0.9% | Global | Short term (≤2 years) |

| Frequent shortages in global epinephrine auto-injector supply chain | -0.6% | North America, intermittent in EU and APAC | Short term (≤2 years) |

| Lack of harmonized treatment guidelines across regions & centers | -0.5% | Global, fragmentation highest in APAC and Latin America | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

High Costs & Limited Reimbursement Hurdles for Biologic Therapies

Omalizumab, a leading biologic therapy, is priced at over USD 2,000 per month. U.S. payers enforce prior-authorization requirements, including the submission of serum-IgE documentation and prescriptions from allergists. Medicare Part D beneficiaries face coinsurance rates of 25-33%, resulting in monthly out-of-pocket expenses ranging from USD 500 to 700. By 2025, 14 state Medicaid plans are expected to mandate step therapy through oral immunotherapy before approving biologics, potentially restricting access for low-income families.

Safety Concerns & Adherence Issues with Extended Immunotherapy Protocols

A 2025 survey reported a 5% dropout rate from oral immunotherapy due to intolerable side effects, with 13% of patients requiring dose adjustments after severe reactions. Data also indicated that 71.8% of patients experienced adverse events, most of which were mild; however, concerns about anaphylaxis remain a key factor driving discontinuation. Additionally, social factors such as the inconvenience of daily dosing and gastrointestinal discomfort further exacerbate challenges in adherence to treatment protocols.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Disease-Modifying Therapies Challenge Acute-Care Dominance

Acute-care drugs, including epinephrine autoinjectors, antihistamines, and corticosteroids, accounted for 42.50% of 2025 revenue, highlighting their critical role in emergency management. The demand for epinephrine has been strengthened by the introduction of infant-dose products and affordable generics. However, disease-modifying agents, led by oral immunotherapy and omalizumab, are growing at an 8.88% CAGR, shifting the clinical focus from emergency interventions to preventive care. Guidelines emphasize that biologics are preventive in nature and should not replace epinephrine in acute situations.

By Tree-Nut Type: Cashew Expands Amid Dietary Shifts

Walnuts captured 28.55% of the 2025 segment revenue, reflecting their widespread use in baked goods and plant-based milks. Hazelnut oral immunotherapy achieved a high desensitization rate but provided minimal cross-protection to other nuts, underscoring the need for nut-specific treatment approaches. Rising cashew consumption in Asia is driving a 6.99% CAGR, with increasing demand for cashew-specific allergy treatments as exposure grows.

By End User: Specialty Clinics Lead Immunotherapy Growth

Hospital pharmacies accounted for 55.34% of 2025 sales, driven by the need for emergency equipment and trained personnel during supervised treatment phases. However, specialty allergy clinics are experiencing an 8.34% CAGR, driven by integrated care models that combine oral immunotherapy, biologics, diagnostics, and clinical trial enrollment. These clinics differentiate themselves through value-based care contracts and remote-monitoring tools that enhance treatment adherence.

By Age Group: Pediatric Cohort Anchors Market Expansion

Pediatric patients represented 60.43% of the projected demand for 2025 and are expected to grow at a compound annual growth rate (CAGR) of 7.56%. This growth is attributed to advancements in early diagnostics and increased caregiver willingness to invest in tolerance-inducing therapies. The observed efficacy in preschool-age children during the POSEIDON trial highlights the significance of initiating interventions before school entry. Furthermore, the anticipated Viaskin Peanut application for children aged 1 to 3 years reflects the regulatory focus on addressing the needs of the youngest patient segment.

Geography Analysis

In 2025, North America secured 39.67% of the geographic revenue, driven by the United States' rapid adoption of omalizumab following its FDA approval in February 2024. This growth was supported by the widespread availability of epinephrine auto-injectors through retail and specialty pharmacies and a well-established network of allergy clinics providing Oral Immunotherapy (OIT). In January 2025, the American Academy of Allergy, Asthma & Immunology issued consensus guidance on omalizumab, standardizing patient selection criteria and dosing regimens. Additionally, the 2024 AAAAI-EAACI PRACTALL update aligned oral food challenge protocols, reducing variability across centers and facilitating multi-site clinical trials. Europe, accounting for approximately 28% of the market in 2025, saw Germany, the United Kingdom, France, Italy, and Spain leading in OIT adoption. However, a regulatory gap emerged as the European Medicines Agency's Committee for The EAACI 2024 guidelines recommended omalizumab and OIT for peanut allergies but highlighted limited evidence for tree nuts, which slowed reimbursement and broader adoption.

Asia-Pacific, experiencing a 7.90% CAGR through 2031, is driven by dietary westernization, which has increased tree nut consumption and sensitization rates. A 2025 study documented that eliciting doses for walnut and cashew in Japanese children are now approaching Western thresholds, attributed to rising nut consumption over the past decade. Additionally, China's tree nut import volume grew significantly between 2015 and 2024. The Middle East and Africa, led by Gulf Cooperation Council countries and South Africa, along with South America, anchored by Brazil and Argentina, collectively represent approximately 10% of the market. Growth in these regions is constrained by a limited number of specialists, low awareness of immunotherapy, and high out-of-pocket costs for biologics and diagnostics. However, urbanization and rising incomes are expected to narrow these gaps over the forecast period.

Competitive Landscape

The tree nut allergy market is characterized by moderate fragmentation. Leading players in the acute-care autoinjector segment include manufacturers of products such as EpiPen, Auvi-Q, generic epinephrine injectors, and Adrenaclick. Disease-modifying therapies are concentrated among companies specializing in peanut oral immunotherapy (OIT), epicutaneous immunotherapy (EPIT), and monoclonal antibody treatments. Innovation in the market is centered around portfolio breadth, diverse administration routes, and advancements in precision medicine. For instance, voice-guided interfaces in autoinjectors help reduce user errors, while efforts are underway to develop needle-free epinephrine delivery systems to address injection aversion.

AI-engineered proteins are emerging as next-generation precision therapeutics, significantly reducing epitope-design cycles to six months, which is half the historical average. Regulatory timelines are a key factor in competitive positioning, with some companies seeking accelerated approvals for pediatric use and others advancing peanut allergy treatments into late-stage clinical trials. New entrants in the market are focusing on multi-allergen formulations and digital adherence tools to address existing gaps in therapy options.

Tree Nut Allergy Industry Leaders

Bayer AG

Teva Pharmaceutical Industries Ltd.

Pfizer Inc.

Kaleo, Inc.

Amneal Pharmaceuticals

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Health Canada approved Neffy 2 mg for emergency anaphylaxis treatment in patients ≥ 30 kg.

- April 2026: ALK-Abelló announced positive Phase 2 results for its peanut allergy tablet, enabling progression to Phase 3 studies.

- January 2026: Aquestive Therapeutics received an FDA Complete Response Letter for Anaphylm and plans a Q3 2026 resubmission.

- December 2025: DBV Technologies reported favorable Phase 3 VITESSE outcomes and filed a Biologics License Application for Viaskin Peanut.

Global Tree Nut Allergy Market Report Scope

As per scope of the report, tree nut allergy is a food allergy in which the immune system mistakenly identifies proteins in tree nuts (such as almonds, cashews, walnuts, pecans, pistachios, and hazelnuts) as harmful, triggering allergic reactions that can range from mild hives to life-threatening anaphylaxis.

The market is segmented by product type, tree nut type, end user, age group, and geography. By product type, the market is segmented into acute care medications (epinephrine auto-injectors, antihistamines, corticosteroids), disease-modifying treatments, oral immunotherapy (OIT), sublingual immunotherapy (SLIT), epicutaneous immunotherapy (EPIT), biologic monoclonal antibodies (Anti-IgE, Anti-IL-4/13), and diagnostic tools (skin prick assessments, serum-specific IgE evaluations, component-resolved diagnostics (CRD), at-home digital testing kits). By tree nut type, the market is segmented into walnut, cashew, almond, hazelnut, pecan, pistachio, macadamia, brazil nut, and others (e.g., chestnut, pine nut). By end user, the market is segmented into hospital pharmacies, retail pharmacies, specialty allergy clinics, and homecare/direct-to-patient services. By age group, the market is segmented into pediatric (<18 yrs), adult (18–64 yrs), and geriatric (≥65 yrs). By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers estimated market sizes and trends for 17 countries across major regions worldwide. The report offers market size and forecasts in value (USD) for the above segments.

| Acute Care Drugs | Epinephrine Auto-Injectors |

| Antihistamines | |

| Corticosteroids | |

| Disease-Modifying Therapies | Oral Immunotherapy (OIT) |

| Sublingual Immunotherapy (SLIT) | |

| Epicutaneous Immunotherapy (EPIT) | |

| Biologic Monoclonal Antibodies (Anti-IgE, Anti-IL-4/13) | |

| Diagnostics | Skin Prick Tests |

| Serum-specific IgE Tests | |

| Component-Resolved Diagnostics (CRD) | |

| At-home Digital Test Kits |

| Walnut |

| Cashew |

| Almond |

| Hazelnut |

| Pecan |

| Pistachio |

| Macadamia |

| Brazil Nut |

| Others (e.g., Chestnut, Pine Nut) |

| Hospital Pharmacies |

| Retail Pharmacies |

| Specialty Allergy Clinics |

| Homecare / Direct-to-Patient |

| Paediatric (<18 yrs) |

| Adult (18-64 yrs) |

| Geriatric (>65 yrs) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Acute Care Drugs | Epinephrine Auto-Injectors |

| Antihistamines | ||

| Corticosteroids | ||

| Disease-Modifying Therapies | Oral Immunotherapy (OIT) | |

| Sublingual Immunotherapy (SLIT) | ||

| Epicutaneous Immunotherapy (EPIT) | ||

| Biologic Monoclonal Antibodies (Anti-IgE, Anti-IL-4/13) | ||

| Diagnostics | Skin Prick Tests | |

| Serum-specific IgE Tests | ||

| Component-Resolved Diagnostics (CRD) | ||

| At-home Digital Test Kits | ||

| By Tree Nut Type | Walnut | |

| Cashew | ||

| Almond | ||

| Hazelnut | ||

| Pecan | ||

| Pistachio | ||

| Macadamia | ||

| Brazil Nut | ||

| Others (e.g., Chestnut, Pine Nut) | ||

| By End User | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Specialty Allergy Clinics | ||

| Homecare / Direct-to-Patient | ||

| By Age Group | Paediatric (<18 yrs) | |

| Adult (18-64 yrs) | ||

| Geriatric (>65 yrs) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current market value for treatments that address allergic reactions to tree nuts?

The tree nut allergy market size reached USD 299.85 million in 2025 and is projected to approach USD 446.98 million by 2031, according to Mordor Intelligence.

Which geography is expanding the fastest for tree-nut allergy therapies?

Asia-Pacific is forecast to advance at a 7.90% CAGR through 2031 as nut consumption rises and immunotherapy guidelines harmonize.

How dominant are acute-care drugs compared with disease-modifying options?

Acute-care drugs held 42.50% of global revenue in 2025, while disease-modifying therapies are the fastest-growing segment at an 8.88% CAGR.

Which nut type currently commands the largest treatment demand?

Walnut-specific therapies accounted for 28.55% of segment revenue in 2025, the largest share among individual tree nuts.

What role do specialty clinics play in future growth?

Specialty allergy clinics are expected to grow at an 8.34% CAGR as they integrate oral immunotherapy, biologics, and diagnostics into single-site care pathways that attract traveling patients.

How will biologics pricing affect patient access?

High monthly costs and specialty-tier insurance placement create reimbursement hurdles, but broader payer acceptance may improve as outcomes data accumulate.

Page last updated on: