Protein Crystallization Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

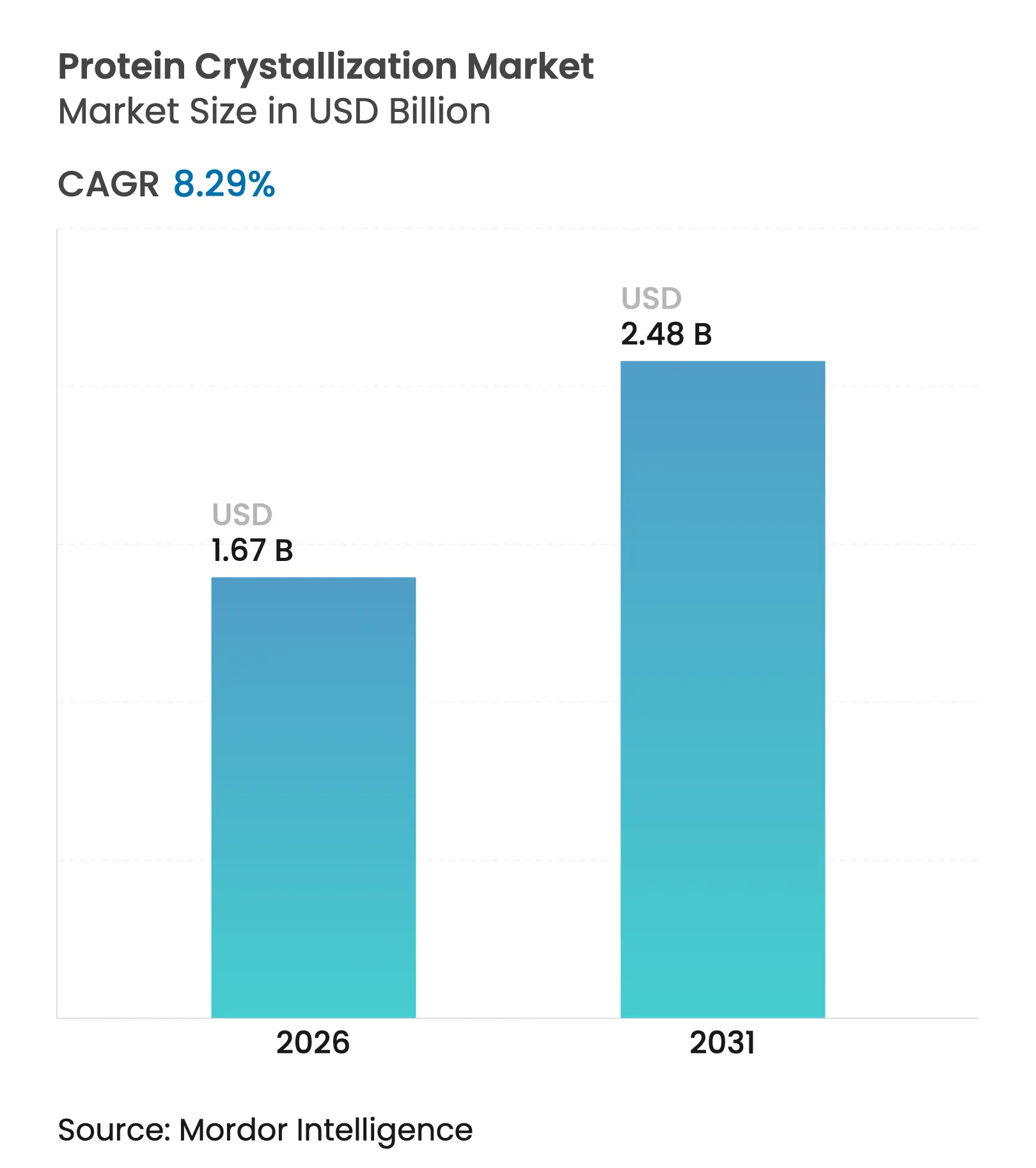

| Market Size (2026) | USD 1.67 Billion |

| Market Size (2031) | USD 2.48 Billion |

| Growth Rate (2026 - 2031) | 8.29 % CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Protein Crystallization Market Analysis by Mordor Intelligence

The protein crystallization market size was valued at USD 1.54 billion in 2025 and estimated to grow from USD 1.67 billion in 2026 to reach USD 2.48 billion by 2031, at a CAGR of 8.29% during the forecast period (2026-2031). Uptake of AI-enhanced structural-biology platforms, expanding synchrotron capacity, and growing public-sector R&D outlays underpin this trajectory. The 2024 Nobel Prize in Chemistry for AlphaFold reinforced confidence in computational–experimental hybrids that shorten hit-to-lead timelines.[1]Philip Ball, “Chemistry Nobel Awarded for an AI System That Predicts Protein Structures,” Physics, physics.aps.org In parallel, the U.S. National Science Foundation earmarked USD 40 million for protein-design acceleration, signalling durable budget support for structure-based discovery.[2]NSF Staff Writer, “New $40 M Funding Opportunity Accelerates the Translation of Novel Approaches to Protein Design,” National Science Foundation, nsf.gov Pharmaceutical makers now treat advanced crystallography instruments as core infrastructure, sustaining premium demand even as software and services scale faster than hardware sales. Investments in Asia–Pacific beamlines and microfluidic workflows further widen the addressable base, although a shortage of skilled crystallographers and capital-intensive equipment temper outright growth.

Key Report Takeaways

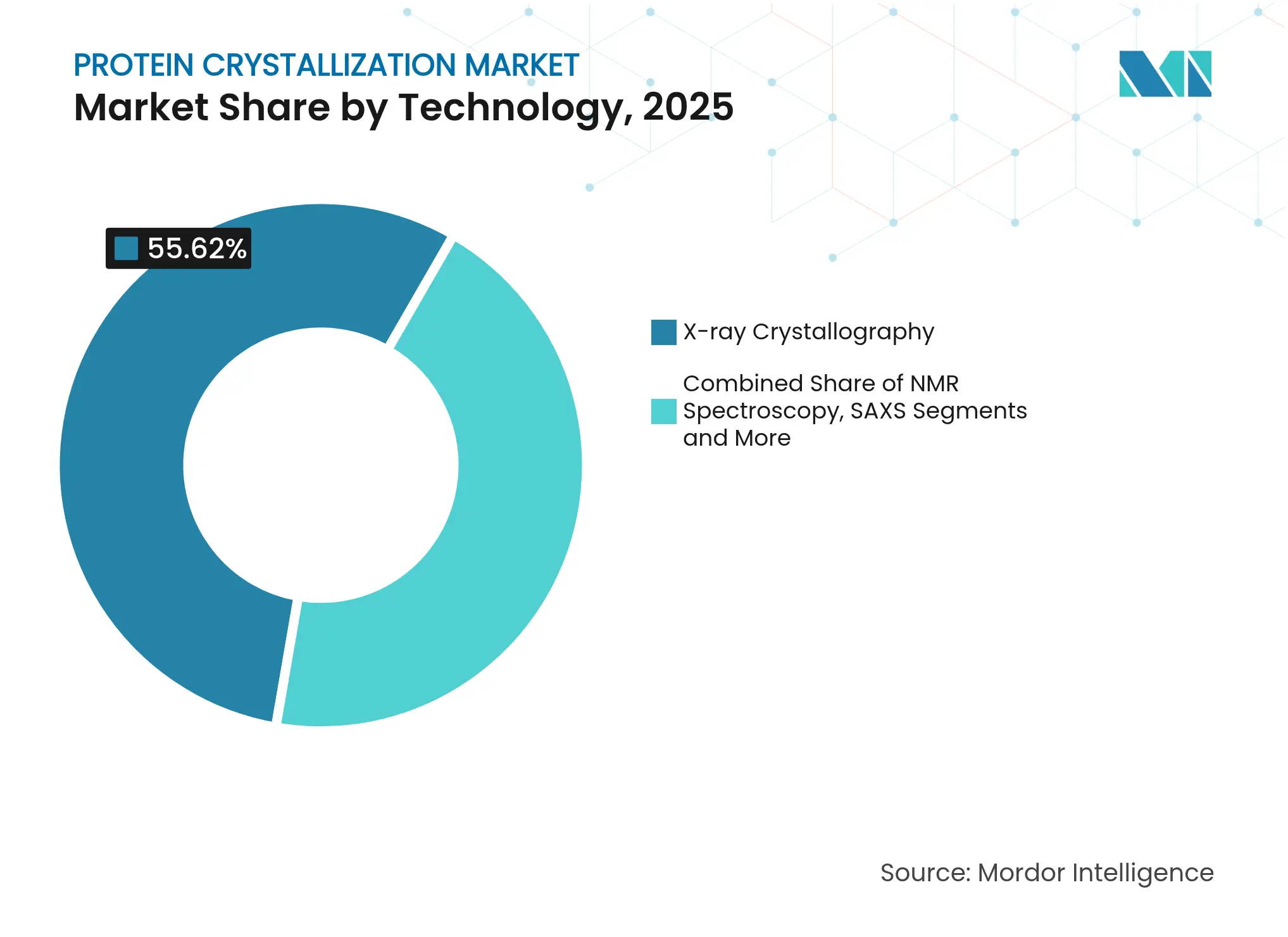

- By technology, X-ray crystallography led with 55.62% of protein crystallization market share in 2025, while microfluidic chip-based screening is projected to expand at 11.26% CAGR through 2031.

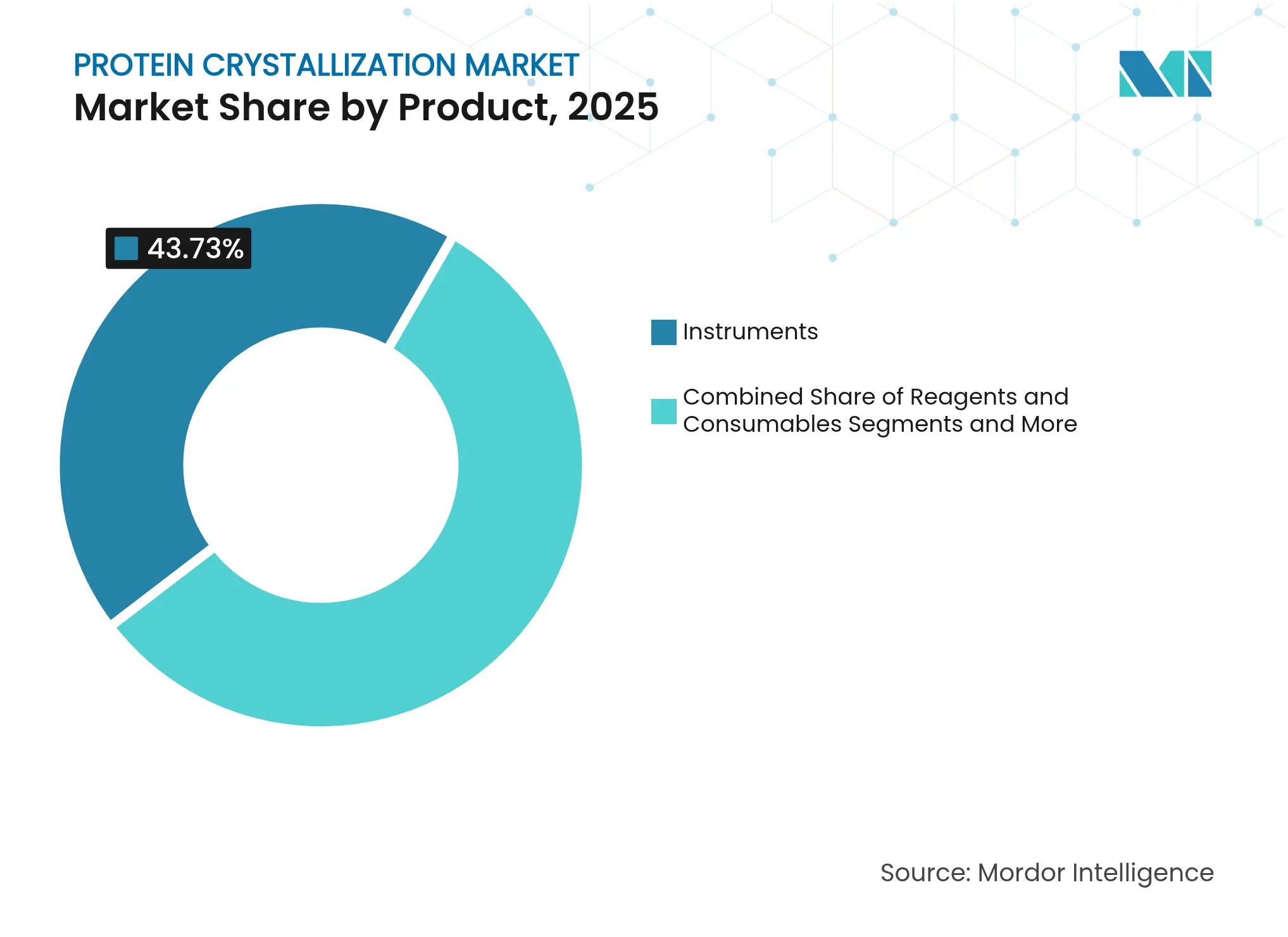

- By product, instruments captured 43.73% share of the protein crystallization market size in 2025; software & services are set to advance at 11.82% CAGR to 2031.

- By end user, pharmaceutical & biotech companies held 53.78% share of the protein crystallization market in 2025; contract research organizations show the fastest trajectory at 10.04% CAGR.

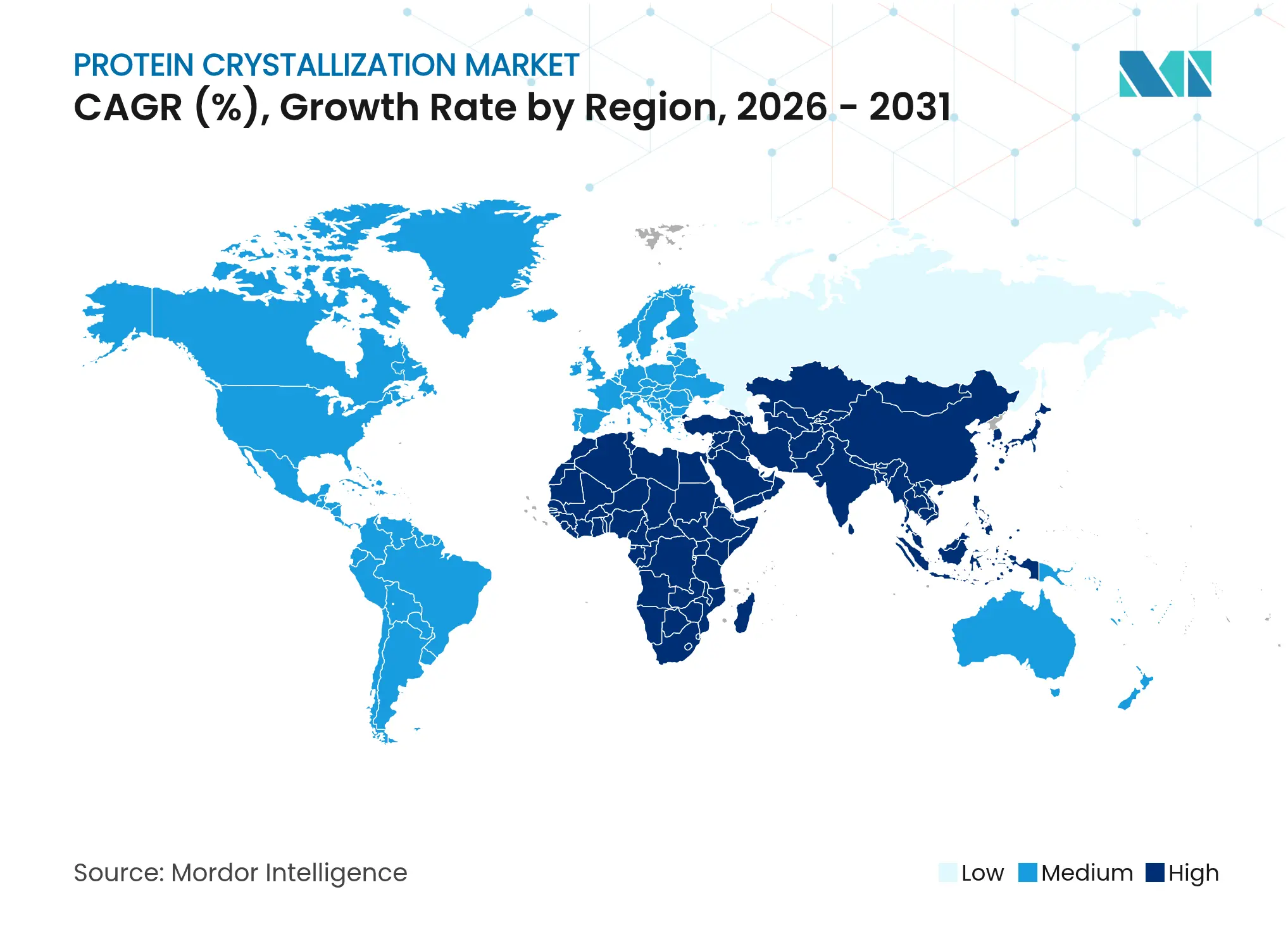

- By geography, North America accounted for 35.78% of 2025 revenue, whereas Asia–Pacific is poised for a 9.75% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Protein Crystallization Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising Investment In Biopharma

R&D

Rising Investment In Biopharma

R&D

| +1.8% | Global, with concentration in North America & EU | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:

+1.8%

|

Geographic Relevance

:

Global, with concentration in North

America & EU

|

Impact Timeline

:

Medium term (2-4 years)

|

Growing Adoption Of Protein

Therapeutics

Growing Adoption Of Protein

Therapeutics

| +1.5% | Global, led by North America, expanding in APAC | Long term (≥ 4 years) | |||

Expansion Of Structural-Genomics

Consortia

Expansion Of Structural-Genomics

Consortia

| +1.2% | North America & EU core, spill-over to APAC | Medium term (2-4 years) | |||

Miniaturised Microfluidic Screening

Platforms

Miniaturised Microfluidic Screening

Platforms

| +1.0% | Global, with early adoption in North America | Short term (≤ 2 years) | |||

AI-Driven In-Silico Lattice Prediction

AI-Driven In-Silico Lattice Prediction

| +0.9% | Global, concentrated in research-intensive regions | Short term (≤ 2 years) | |||

Continuous-Flow Crystallisation For

Biologics

Continuous-Flow Crystallisation For

Biologics

| +0.8% | North America & EU, expanding to APAC | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising investment in biopharma R&D

Accelerating pharmaceutical R&D spend drives steady demand for high-throughput crystallography as firms integrate structure-guided design into every discovery program. NSF’s USD 40 million Use-Inspired Protein Design initiative exemplifies policy-level support that elevates structural biology budgets in academic and corporate labs alike. FDA encouragement of continuous manufacturing encourages producers to install crystallisation analytics that monitor real-time quality. Thermo Fisher Scientific spent USD 1.3 billion on R&D in 2023, with a substantive share devoted to protein-analysis platforms. These signals legitimise capital outlays on automation, detectors, and AI-driven pipelines, lifting the overall protein crystallization market.

Growing adoption of protein therapeutics

As monoclonal antibodies, engineered enzymes, and other biologics dominate the clinical pipeline, sponsors require atomic-level proofs for regulatory filings, reinforcing crystallography demand. The NIH CRSTAL-ID network solved multiple SARS-CoV-2 structures, underscoring how rapid access to diffraction data accelerates emergency counter-measures. With the Protein Data Bank informing over 80% of antineoplastic approvals from 2019-2023, structural evidence now sits at the center of drug dossiers.[3]Stephen K. Burley, “Impact of Structural Biology and the Protein Data Bank on US FDA New Drug Approvals,” Nature, nature.com Biosimilar developers mirror this need, fuelling outsourcing to CROs that specialise in crystallography workflows.

Expansion of structural-genomics consortia

Government-funded consortia standardise high-throughput pipelines, lowering adoption barriers and pushing equipment utilisation up across shared facilities. The PSI:Biology program transitioned from basic method work to disease-focused structure output, anchoring long-term grant flows that stabilise beamline usage. Europe’s GBP 500 million Diamond-II upgrade will add cutting-edge beamlines accessible to the wider community. Such cooperative ecosystems guarantee sample throughput and data volumes that translate into recurring reagent and software revenues for vendors.

Miniaturised microfluidic screening platforms

High materials cost and scarce membrane proteins have long throttled crystal growth. Microfluidic chips reduce sample needs by an order of magnitude and screen thousands of conditions within 30 minutes.[4]Meenesh R. Singh, “Advanced Continuous-Flow Microfluidic Device for Parallel Screening of Crystal Polymorphs,” Royal Society of Chemistry, pubs.rsc.org Patents covering 3-D-printed continuous-flow devices align droplet generation with XFEL pulses, advancing serial femtosecond crystallography into routine mode. Affordable fabrication lets mid-tier universities adopt advanced workflows, broadening the protein crystallization market’s user base.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Shortage Of Highly-Skilled

Crystallographers

Shortage Of Highly-Skilled

Crystallographers

| -1.2% | Global, acute in North America & EU | Long term (≥ 4 years) | (~) % Impact on CAGR Forecast:

-1.2%

|

Geographic Relevance

:

Global, acute in North America &

EU

|

Impact Timeline

:

Long term (≥ 4 years)

|

High Capital Cost Of Imaging &

Robotics

High Capital Cost Of Imaging &

Robotics

| -1.0% | Global, particularly affecting emerging markets | Medium term (2-4 years) | |||

Membrane-Protein Crystallisation

Bottlenecks

Membrane-Protein Crystallisation

Bottlenecks

| -0.8% | Global, concentrated in pharmaceutical research | Long term (≥ 4 years) | |||

IP Complexity In Microfluidic Chip

Designs

IP Complexity In Microfluidic Chip

Designs

| -0.6% | North America & EU, expanding to APAC | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Shortage of highly skilled crystallographers

Demand for lattice-growth expertise outstrips supply, with only a handful of universities offering dedicated PhD tracks. The University of Pittsburgh’s program is one of the rare North American pipelines for new crystallographers. Beamline operators face understaffing, forcing booking backlogs that slow project timelines. Although AI tools assist data interpretation, complex membrane targets still demand human judgment, constraining the protein crystallization market’s capacity to absorb rising sample loads.

High capital cost of imaging & robotics

Cutting-edge diffractometers and cryo-EM rigs can cost USD 7 million each, beyond the reach of many institutions. Even academic service centers charge USD 150–450 per sample to cover depreciation. Leasing eases cashflow but introduces scheduling conflicts that undermine rapid-turnover studies essential to biotech programs.

Segment Analysis

By Technology: AI integration accelerates traditional methods

X-ray crystallography controlled 55.62% of protein crystallization market share in 2025, a position rooted in decades of beamline optimisation and automated data capture. Ongoing detector upgrades such as DECTRIS EIGER2 have raised frame rates and quantum efficiency, tightening experimental cycle times. Cryo-EM-assisted crystallography and SAXS complement these workflows by revealing conformational ensembles, but neither displaces diffraction in regulatory settings. AI-guided sample screening further entrenches incumbency by boosting first-attempt success, keeping X-ray platforms central to the protein crystallization market.

Microfluidic chip-based screening, growing at 11.26% CAGR, offers dramatic reductions in sample volume. Crystal hits emerge in minutes, not days, cutting queue times on shared robots and lowering per-target consumable spend. Hybrid pipelines that marry chip platforms with AI lattice prediction close the loop from in-silico design to diffraction readout within a single week, redefining acceptable timelines for structure-enabled lead optimisation. As costs fall, microfluidics stand to capture a larger slice of protein crystallization market size while acting as a feeder for high-resolution synchrotron sessions.

Note: Segment shares of all individual segments available upon report purchase

By Product: Software & services drive innovation

Instruments represented 43.73% of protein crystallization market size in 2025, reflecting multiyear depreciation schedules that stabilise vendor revenue. Purchasers prioritise photon-counting detectors and robotic samplers that raise beamline uptime and enable overnight unattended runs. Nonetheless, software & services, tracking a 11.82% CAGR, outpace hardware. Cloud-native suites offer automated phasing, model validation, and AI-assisted refinement, allowing remote collaboration across time zones. Subscription pricing converts periodic license upgrades into steady cashflows, widening margins for providers.

Reagents and consumables show steady mid-single-digit growth as screens, kits, and cryoprotectants scale with experiment volume. Sodium-malonate formulations that double as cryoprotectants and precipitants illustrate incremental innovation that keeps margins healthy. Integration of robotic liquid handlers such as SPT Labtech’s mosquito crystal aligns with software-driven protocols to reduce failed plates, conserving reagents and lifting effective throughput.

Note: Segment shares of all individual segments available upon report purchase

By End User: CROs capture outsourcing trend

Pharmaceutical & biotech companies owned 53.78% of protein crystallization market share in 2025 as they rely on internal beamlines for IP-sensitive targets. Yet cost-conscious smaller firms increasingly outsource to contract research organizations, giving CROs the highest projected CAGR at 10.04%. Full-service CROs bundle cloning, crystallisation, and structure-guided medicinal chemistry, positioning themselves as one-stop discovery accelerators.

Academic and research institutes anchor basic methodological innovation, benefiting from sustained NIH Common Fund grants that underwrite beamline upgrades and trainee programs. Government labs and niche service providers fill specialist gaps, offering neutron crystallography or room-temperature serial data collection that complements mainstream X-ray pipelines.

Geography Analysis

North America contributed 35.78% of global revenue in 2025, supported by NIH and NSF programs that subsidise instrumentation and drive sample throughput. Mature pharma clusters in Massachusetts and California anchor commercial demand, while synchrotrons like APS and SSRL provide state-of-the-art beamlines. Workforce-development grants partially ease the crystallographer shortage, but demand still exceeds supply.

Asia–Pacific is the fastest-growing region at 9.75% CAGR through 2031. China’s next-generation synchrotron in Shanghai offers sub-micron beams ideal for micro-crystals, drawing regional users and underpinning service-provider growth. Japanese and Australian facilities add complementary capabilities such as high-pressure or ambient-temperature diffraction, diversifying the regional technology stack.

Europe sustains significant share through coordinated investment exemplified by the Diamond-II upgrade, which will extend beamline count and brightness once operational in 2027. The European Spallation Source promises neutron macromolecular crystallography for hydrogen-sensitive systems, filling a gap in the global infrastructure. Emerging projects in South America and Africa remain in planning, but successful funding could unlock fresh demand late in the forecast window.

Competitive Landscape

Market Concentration

The protein crystallization market is moderately fragmented. Rigaku deepened solution-state analysis with its 2024 opening of the Cambridge BioScience Lab, showcasing MoleQlyze technology that sidesteps crystal growth for hard-to-crystallise proteins. Bruker reinforced its diffractometer line by integrating DECTRIS photon-counting detectors, improving signal-to-noise and shortening exposure times. Thermo Fisher channels rising cryo-EM demand into adjacent diffraction offerings, cross-selling consumables and software.

Competition increasingly pivots on automation and AI. Patents in microfluidic crystallisation and machine-learning–driven lattice prediction differentiate new entrants. Vendors invest in field-service coverage and financing packages to ease capital hurdles, while partnerships with CROs extend reach into small-company pipelines. Sub-USD 1 million cryo-EM prototypes under development may democratise advanced imaging, although time-to-market and performance trade-offs remain uncertain.

Protein Crystallization Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: BioOrbit aims to commence pre-clinical trials on monoclonal-antibody crystals manufactured in micro-gravity conditions aboard a dedicated space factory.

- November 2024: Rigaku Corporation opened the Rigaku BioScience Lab in Cambridge, Massachusetts, featuring MoleQlyze technology that analyses proteins in solution without classical crystallisation requirement

Table of Contents for Protein Crystallization Industry Report

1. Introduction

- 1.1Study Assumptions and Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rising Investment In Biopharma R&D

- 4.2.2Growing Adoption Of Protein Therapeutics

- 4.2.3Expansion Of Structural-Genomics Consortia

- 4.2.4Miniaturised Microfluidic Screening Platforms

- 4.2.5AI-Driven In-Silico Lattice Prediction

- 4.2.6Continuous-Flow Crystallisation For Biologics

- 4.3Market Restraints

- 4.3.1Shortage Of Highly-Skilled Crystallographers

- 4.3.2High Capital Cost Of Imaging & Robotics

- 4.3.3Membrane-Protein Crystallisation Bottlenecks

- 4.3.4IP Complexity In Microfluidic Chip Designs

- 4.4Value / Supply-Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technology Outlook

- 4.7Porter’s Five Forces Analysis

- 4.7.1Bargaining Power of Suppliers

- 4.7.2Bargaining Power of Buyers

- 4.7.3Threat of New Entrants

- 4.7.4Threat of Substitutes

- 4.7.5Intensity of Competitive Rivalry

5. Market Size and Growth Forecasts (Value-USD)

- 5.1By Technology

- 5.1.1X-ray Crystallography

- 5.1.2NMR Spectroscopy

- 5.1.3Cryo-EM-assisted Crystallography

- 5.1.4Microfluidic Chip-based Screening

- 5.1.5Small-angle X-ray Scattering (SAXS)

- 5.2By Product

- 5.2.1Instruments

- 5.2.1.1Imaging Systems

- 5.2.1.2Liquid-Handling Robotics

- 5.2.1.3Crystallisation Plates & Chips

- 5.2.1.4Incubators/Temperature Controllers

- 5.2.2Reagents & Consumables

- 5.2.3Software & Services

- 5.3By End User

- 5.3.1Pharmaceutical & Biotech Companies

- 5.3.2Academic & Research Institutes

- 5.3.3Contract Research Organizations

- 5.3.4Others

- 5.4By Geography

- 5.4.1North America

- 5.4.1.1United States

- 5.4.1.2Canada

- 5.4.1.3Mexico

- 5.4.2Europe

- 5.4.2.1Germany

- 5.4.2.2United Kingdom

- 5.4.2.3France

- 5.4.2.4Italy

- 5.4.2.5Spain

- 5.4.2.6Rest of Europe

- 5.4.3Asia-Pacific

- 5.4.3.1China

- 5.4.3.2Japan

- 5.4.3.3India

- 5.4.3.4Australia

- 5.4.3.5South Korea

- 5.4.3.6Rest of Asia-Pacific

- 5.4.4Middle East and Africa

- 5.4.4.1GCC

- 5.4.4.2South Africa

- 5.4.4.3Rest of Middle East and Africa

- 5.4.5South America

- 5.4.5.1Brazil

- 5.4.5.2Argentina

- 5.4.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.3.1Rigaku Corporation

- 6.3.2Bruker Corporation

- 6.3.3Thermo Fisher Scientific Inc.

- 6.3.4Hampton Research Corp.

- 6.3.5Tecan Trading AG

- 6.3.6Agilent Technologies Inc.

- 6.3.7Art Robbins Instruments LLC

- 6.3.8MiteGen LLC

- 6.3.9SARomics Biostructures AB

- 6.3.10Corning Incorporated

- 6.3.11Charles River Laboratories Intl.

- 6.3.12Molecular Dimensions Ltd

- 6.3.13Jena Bioscience GmbH

- 6.3.14Formulatrix Inc.

- 6.3.15QIAGEN N.V.

- 6.3.16Mettler-Toledo International Inc.

- 6.3.17Danahar

- 6.3.18Bio-Rad Laboratories Inc.

- 6.3.19Creative Biostructure

- 6.3.20Calibre Scientific

7. Market Opportunities and Future Outlook

- 7.1White-Space and Unmet-Need Assessment

Global Protein Crystallization Market Report Scope

As per the scope of this report, protein crystallization is the act and method of creating structured, ordered lattices for complex macromolecules. The most common reason for creating protein crystals is to support structural biology investigations via different techniques such as X-ray crystallography, NMR spectrometry, and others. It is also a method to produce pure, stable, solid dosage forms and several injected and infused therapeutics that are associated with protein crystals. The protein crystallization market is segmented by technology (X-ray crystallography, NMR spectroscopy, and others), product (instruments, reagents or consumables, and services and software), end-user (pharmaceutical and biotechnology industries and others), and geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends of 17 countries across major regions globally. The report offers values in USD for the above segments.