Protein Binding Assays Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

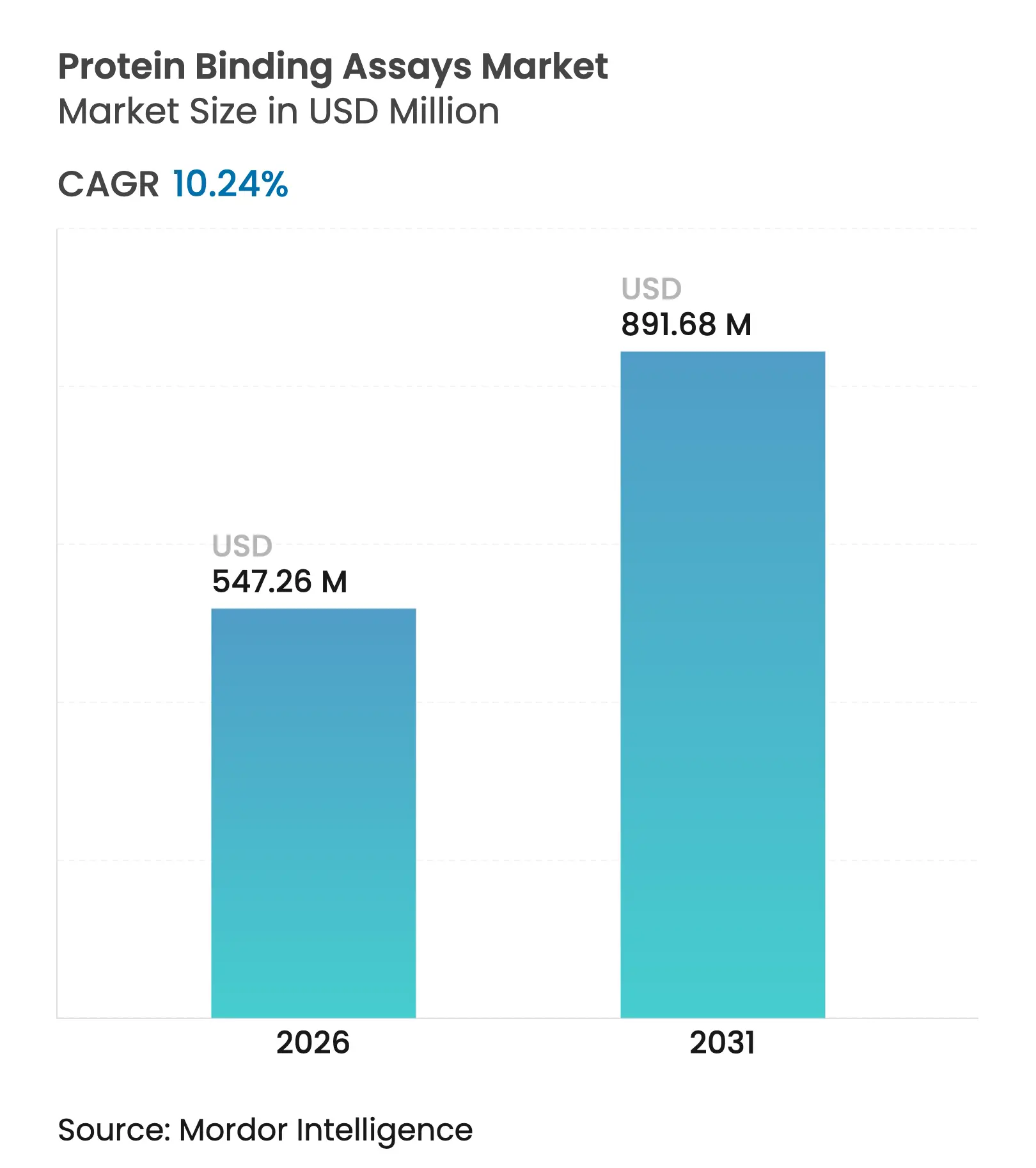

| Market Size (2026) | USD 547.26 Million |

| Market Size (2031) | USD 891.68 Million |

| Growth Rate (2026 - 2031) | 10.24 % CAGR |

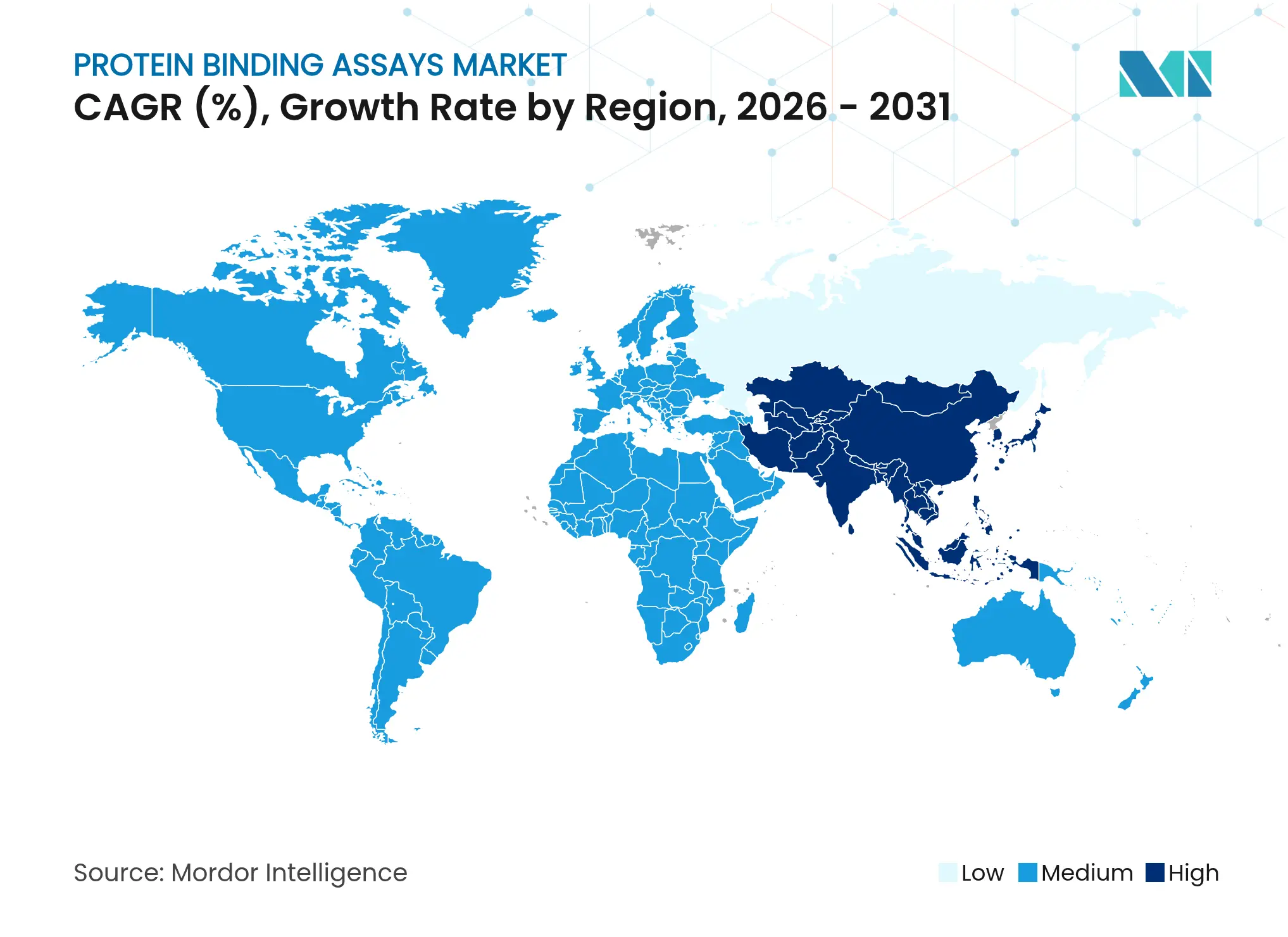

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

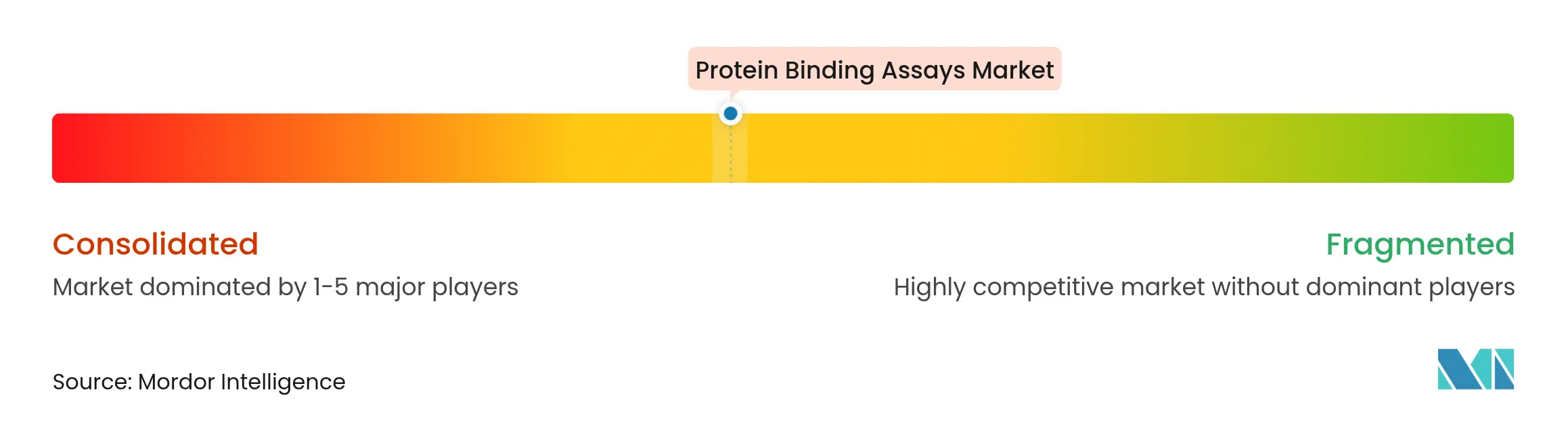

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Protein Binding Assays Market Analysis by Mordor Intelligence

The protein binding assays market size was valued at USD 496.43 million in 2025 and estimated to grow from USD 547.26 million in 2026 to reach USD 891.68 million by 2031, at a CAGR of 10.24% during the forecast period (2026-2031). Accelerating demand for precise drug-development tools, especially for targeted protein degradation programs such as PROTACs and molecular glues, is the chief growth catalyst.[1]Hsia O., “Targeted protein degradation via intramolecular bivalent glues,” Nature, nature.com Heightened adoption of artificial-intelligence (AI) models that shorten lead-optimization cycles by 25-50% and the rapid roll-out of micro-fluidic high-throughput screening (HTS) systems that curb reagent use are reshaping operational economics.[2]Wong A., “Generative AI in drug discovery and development,” Annals of Medicine and Surgery, journals.lww.com Government grants aimed at rare-disease translational research add fresh momentum, while rising strategic investments—exemplified by Novartis’s USD 256 million expansion in Singapore—underline the market’s globalisation pathway. Although supply-chain fragility for niche reagents and limited multi-omics standardisation temper progress, the long-run trajectory of the protein binding assays market remains firmly upward.

Key Report Takeaways

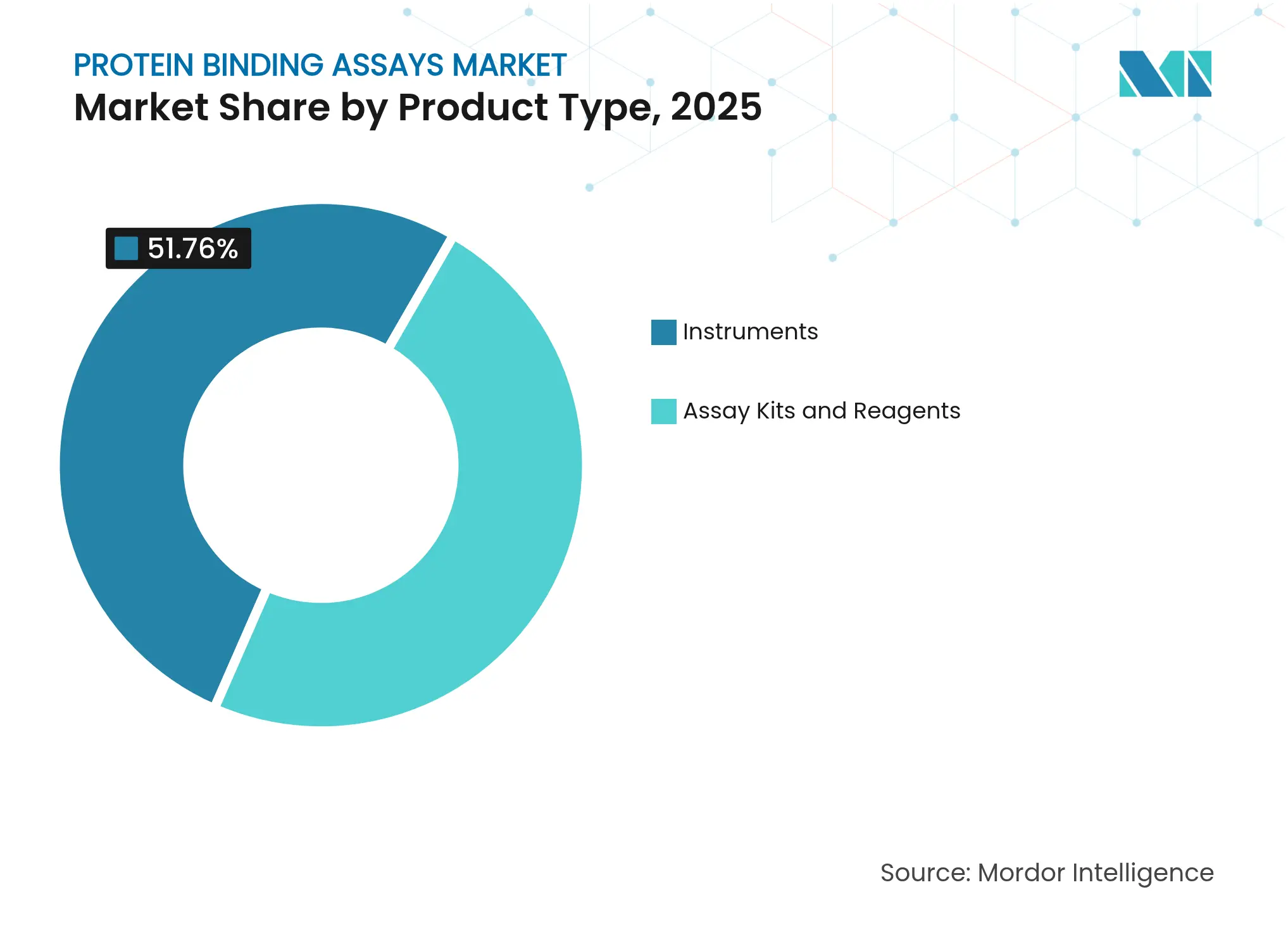

- By product type, instruments led with 51.76% of protein binding assays market share in 2025; assay kits & reagents post the fastest 12.63% CAGR to 2031.

- By technology, equilibrium dialysis commanded 36.85% share of the protein binding assays market size in 2025, while surface plasmon resonance is projected to grow at a 13.19% CAGR.

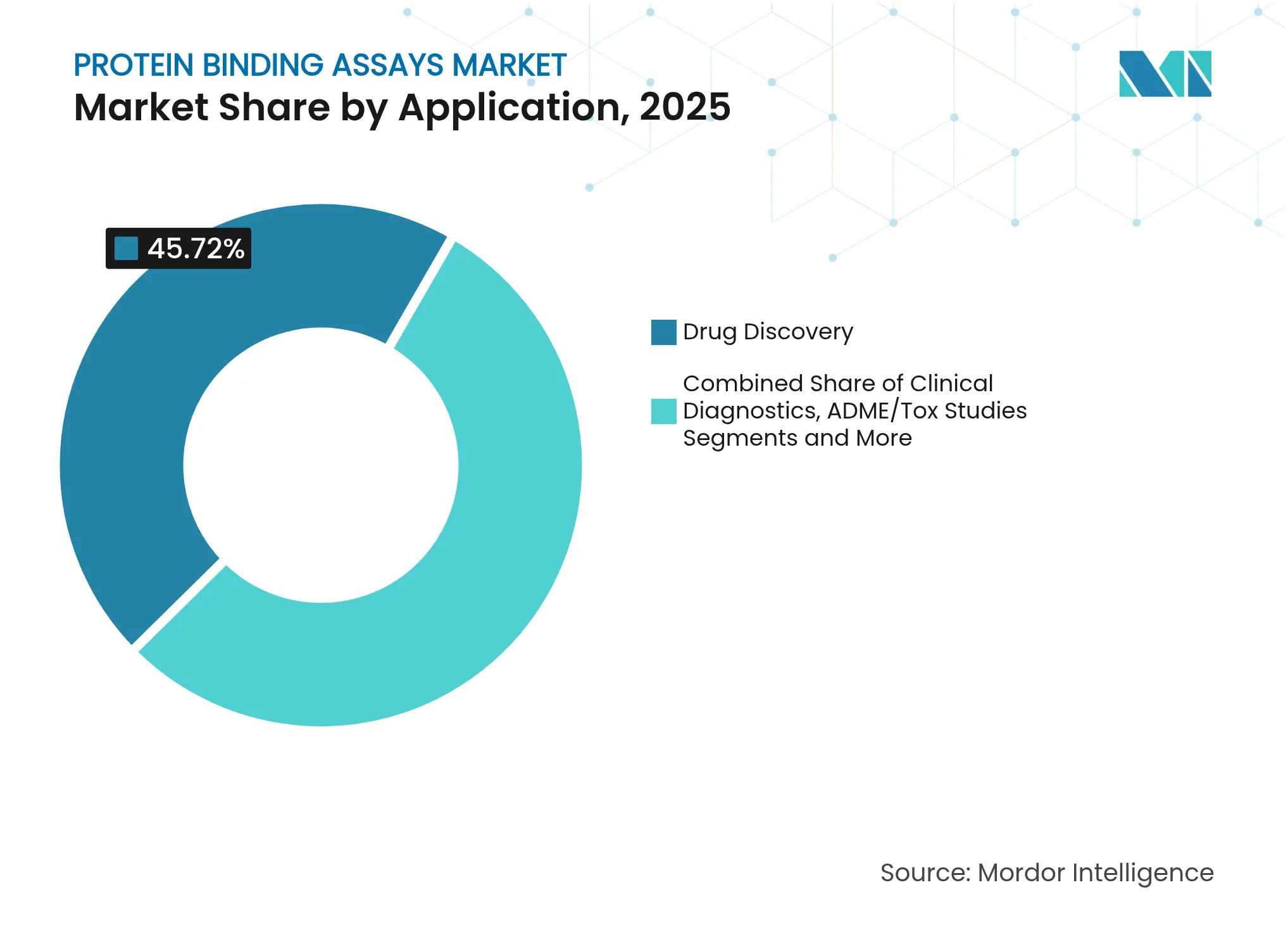

- By application, drug discovery held 45.72% share in 2025; clinical diagnostics advances at a 14.54% CAGR through 2031.

- By end-user, pharmaceutical & biotechnology companies accounted for 48.62% in 2025; contract research organisations (CROs) record the strongest 12.67% CAGR.

- By geography, North America captured 40.98% share in 2025, whereas Asia-Pacific is set to expand at a 12.01% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Protein Binding Assays Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising drug-development pipeline

Rising drug-development pipeline

| +2.1% | Global | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:

+2.1%

|

Geographic Relevance

:

Global

|

Impact Timeline

:

Medium term (2-4 years)

|

Expansion of CRO bioanalytical

capacity

Expansion of CRO bioanalytical

capacity

| +1.8% | North America & EU, APAC core | Short term (≤ 2 years) | |||

Adoption of micro-fluidic HTS

platforms

Adoption of micro-fluidic HTS

platforms

| +1.5% | Global, early gains in North America & EU | Medium term (2-4 years) | |||

AI-guided lead-optimization

workflows

AI-guided lead-optimization

workflows

| +1.3% | Global | Long term (≥ 4 years) | |||

Emergence of PROTAC &

molecular-glue assays

Emergence of PROTAC &

molecular-glue assays

| +1.1% | North America & EU | Long term (≥ 4 years) | |||

Government grants for rare-disease

research

Government grants for rare-disease

research

| +0.9% | North America & EU | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Drug-Development Pipeline

Pipeline expansion demands deeper characterisation of complex therapeutics, pushing companies to examine ternary complex formation between targets, E3 ligases and degraders. The FDA’s 2024 adoption of ICH M10 aligned validation rules requires cross-validation and parallelism studies, heightening assay sophistication. Sponsors are therefore moving binding assessments earlier in discovery to avert late-stage attrition, embedding high-quality assays as regulatory staples.

Expansion of CRO Bioanalytical Capacity

CROs are scaling rapidly; Synexa Life Sciences’ 2024 acquisition of Alderley Analytical added MS-based ligand-binding services, mirroring broader outsourcing appetite. Mega-deals like Lonza’s USD 1.2 billion purchase of Roche’s Vacaville site reinforce the trend. Expanded capacity lets sponsors tap validated platforms for PROTAC studies without investing in-house.

Adoption of Micro-fluidic HTS Platforms

Micro-fluidics shrinks reaction volumes to 0.1 nL, slashing reagent spend while boosting throughput. Droplet-based devices integrate kinetics, thermodynamics and competition assays in one chip, enabling screens of thousands of compounds on scarce protein samples.[3]Du G., “Microfluidics for cell-based high-throughput screening platforms,” Analytica Chimica Acta, sciencedirect.com Momentum is building for organ-on-chip variants that mimic physiological environments for more predictive results.

AI-Guided Lead-Optimization Workflows

Machine-learning models predict affinities and refine assay parameters, compressing discovery timelines by as much as half. Recent AI models outperform legacy algorithms on benchmark datasets, and coupling their predictions with crystallography validation preserves accuracy. Wider AI uptake is expected to normalise data-driven assay design across the protein-binding assays market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High assay-development cost &

validation complexity

High assay-development cost &

validation complexity

| -1.4% | Global | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:

-1.4%

|

Geographic Relevance

:

Global

|

Impact Timeline

:

Short term (≤ 2 years)

|

Limited standardisation across

multi-omics formats

Limited standardisation across

multi-omics formats

| -1.1% | Global | Medium term (2-4 years) | |||

Supply-chain vulnerability for specialty

reagents

Supply-chain vulnerability for specialty

reagents

| -0.9% | Global, acute in APAC | Short term (≤ 2 years) | |||

Data-integrity & IP-ownership

concerns in cloud labs

Data-integrity & IP-ownership

concerns in cloud labs

| -0.7% | North America & EU | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

High Assay-Development Cost & Validation Complexity

Stringent ICH analytical validation guidelines require developers to demonstrate specificity, accuracy, and robustness across the full analytical lifecycle, increasing costs and timelines. Novel modalities lack historical validation templates, forcing bespoke approaches that strain emerging biotechs.

Limited Standardisation Across Multi-Omics Formats

Varying calibration protocols hinder data comparability; international bodies now push for harmonised protein biomarker standards. Mass-spectrometry workflows face alignment issues with conventional clinical chemistry, complicating regulatory acceptance.

Segment Analysis

By Product Type: Instruments Anchor Core Infrastructure

Instruments generated 51.76% of the protein binding assays market in 2025, underlining the foundational role of capital equipment such as surface-plasmon-resonance (SPR) systems and equilibrium-dialysis rigs. Integration of AI and robotics into these instruments is driving incremental value through unattended operation and real-time analytics. Consumables, however, outpace hardware; assay kits & reagents are projected to grow at 12.63% CAGR, propelled by recurring demand and the shift toward kit-based standardised workflows.

Assay developers now bundle validated protocols, buffers and detection reagents that streamline adoption for PROTAC studies and fluorescence-based screens. Innovations like CoraFluor TR-FRET kits offer turnkey solutions for degrader profiling. This consumable-centric growth pattern highlights recurring revenue potential within the protein binding assays market.

Note: Segment shares of all individual segments available upon report purchase

By Technology: Surface Plasmon Resonance Accelerates

Equilibrium dialysis retained 36.85% of protein binding assays market share in 2025 owing to its label-free simplicity and reliable measurement of free ligand fractions. Nevertheless, SPR is the fastest climber at a 13.19% CAGR, buoyed by biosensor upgrades that detect as little as 0.099 ng/mL of analyte—surpassing legacy UPLC-UV benchmarks.

Fluorescence assays keep a niche in ultra-sensitive applications, whereas ultrafiltration remains useful for selective sample prep. CETSA and other “other technologies” offer label-free in-cell validation, expanding analytical options for the protein binding assays market.

By Application: Diagnostics Picks Up Pace

Drug discovery controlled 45.72% of the protein binding assays market size in 2025, reflecting entrenched use in hit-to-lead and candidate selection. The FDA’s clearer route for lab-developed tests is catalysing diagnostics, the fastest segment at 14.54% CAGR, as validated biomarkers migrate from research to clinical use.

Proteomics research leverages mass-spectrometry-based assays for biomarker discovery, while ADME/Tox studies sustain consistent demand due to mandatory safety profiling. Precision-medicine initiatives spur “other applications,” reinforcing diversified uptake.

Note: Segment shares of all individual segments available upon report purchase

By End-User: CROs Capture Outsourcing Wave

Pharmaceutical & biotechnology firms accounted for 48.62% of the protein binding assays market in 2025 thanks to their central R&D mandates. However, CROs are advancing with a 12.67% CAGR as outsourcing becomes a strategy for cost control and specialised expertise. Synexa’s Alderley Analytical buyout typifies the push to bolster ligand-binding capabilities.

Academic institutes fuel methodological innovation, while hospitals and reference labs ramp usage for clinical validation studies. Government facilities round out demand, especially for regulatory dossiers that need cross-validated binding data.

Geography Analysis

North America held 40.98% of the protein binding assays market in 2025, helped by FDA-driven standardisation and dense clusters of biotech firms. Ongoing investments such as Thermo Fisher Scientific’s new 140-job Gothenburg laboratory underscore sustained capacity expansion. NIH funding for rare-disease assays further entrenches regional leadership.

Asia-Pacific is the growth engine, forecast to log a 12.01% CAGR through 2031. Novartis’s USD 256 million Singapore upgrade illustrates multinational commitment to regional biologics demand. China’s strategic outreach to Southeast Asia is reinforcing supply chains for active pharmaceutical ingredients and spurring uptake of advanced assays. Supportive regulatory reforms and unique genetic diversity position the region for rapid adoption of precision binding technologies.

Europe maintains steady trajectory on the back of mature pharma clusters and ICH-aligned regulations. Eastern European nations offer fresh capacity as infrastructure matures. Middle East & Africa and Latin America trail but show upside tied to healthcare build-out and local manufacturing incentives, gradually widening the global footprint of the protein binding assays market.

Competitive Landscape

Market Concentration

The protein binding assays market is moderately fragmented. Conglomerates such as Thermo Fisher Scientific, Danaher and Merck KGaA wield scale advantages through integrated platforms and global service networks. Mid-tier innovators differentiate on micro-fluidics and AI-enabled analytics. Synexa’s acquisition spree spotlights CRO consolidation aimed at full-service bioanalysis.

White-space exists in assays tailored to PROTACs and molecular glues, where few fully validated solutions yet exist. Quantum-computing partnerships (e.g., Classiq and Quantum Intelligence Corp) signal future disruption potential, targeting accelerated ligand design with next-gen computation. Vendors increasingly bundle cloud-based data management with hardware, making software prowess a key competitive lever.

Strategic moves include Sartorius’s launch of the Octet R8e BLI system offering enhanced detection, and Nordic Bioscience’s automated Endotrophin assay expanding high-precision fibrosis biomarker testing. Collectively these developments indicate rising emphasis on speed, throughput and integration across the protein binding assays market.

Protein Binding Assays Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Quantum-Si unveils a single-molecule binding-kinetics method using its Platinum® sequencing platform,•

- Jun 2025: Quantum-Si releases a single-molecule binding-kinetics workflow on the Platinum® instrument, allowing parallel analysis of tens of nanobody variants.

- May 2025: Sartorius introduces the Octet R8e biolayer-interferometry system, delivering higher-throughput real-time interaction analysis.

- May 2025: Nordic Bioscience debuts nordicEndotrophin, a fully automated CAP/CLIA-certified assay for intact Endotrophin quantification.

Table of Contents for Protein Binding Assays Industry Report

1. Introduction

- 1.1Study Assumptions and Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rising Drug-Development Pipeline

- 4.2.2Expansion of CRO Bioanalytical Capacity

- 4.2.3Adoption of Micro-Fluidic HTS Platforms

- 4.2.4AI-Guided Lead-Optimization Workflows

- 4.2.5Emergence of PROTAC & Molecular-Glue Assays

- 4.2.6Government Grants for Rare-Disease Translational Research

- 4.3Market Restraints

- 4.3.1High Assay-Development Cost & Validation Complexity

- 4.3.2Limited Standardisation Across Multi-omics Formats

- 4.3.3Supply-Chain Vulnerability for Specialty Reagents

- 4.3.4Data-Integrity & IP-Ownership Concerns in Cloud Labs

- 4.4Value / Supply-Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technology Outlook

- 4.7Porter’s Five Forces Analysis

- 4.7.1Bargaining Power of Suppliers

- 4.7.2Bargaining Power of Buyers

- 4.7.3Threat of New Entrants

- 4.7.4Threat of Substitutes

- 4.7.5Intensity of Competitive Rivalry

5. Market Size and Growth Forecasts (Value-USD)

- 5.1By Product Type

- 5.1.1Assay Kits & Reagents

- 5.1.2Instruments

- 5.2By Technology

- 5.2.1Fluorescence-based Assays

- 5.2.2Equilibrium Dialysis

- 5.2.3Ultrafiltration

- 5.2.4Surface-Plasmon Resonance

- 5.2.5Other Technologies

- 5.3By Application

- 5.3.1Drug Discovery

- 5.3.2Clinical Diagnostics

- 5.3.3Proteomics Research

- 5.3.4ADME/Tox Studies

- 5.3.5Other Applications

- 5.4By End-User

- 5.4.1Pharmaceutical & Biotechnology Companies

- 5.4.2Contract Research Organizations (CROs)

- 5.4.3Academic & Research Institutes

- 5.4.4Hospitals & Reference Labs

- 5.4.5Other End-Users

- 5.5By Geography

- 5.5.1North America

- 5.5.1.1United States

- 5.5.1.2Canada

- 5.5.1.3Mexico

- 5.5.2Europe

- 5.5.2.1Germany

- 5.5.2.2United Kingdom

- 5.5.2.3France

- 5.5.2.4Italy

- 5.5.2.5Spain

- 5.5.2.6Rest of Europe

- 5.5.3Asia-Pacific

- 5.5.3.1China

- 5.5.3.2Japan

- 5.5.3.3India

- 5.5.3.4Australia

- 5.5.3.5South Korea

- 5.5.3.6Rest of Asia-Pacific

- 5.5.4Middle East and Africa

- 5.5.4.1GCC

- 5.5.4.2South Africa

- 5.5.4.3Rest of Middle East and Africa

- 5.5.5South America

- 5.5.5.1Brazil

- 5.5.5.2Argentina

- 5.5.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.3.1Thermo Fisher Scientific Inc.

- 6.3.2Danaher Corp (Cytiva & Beckman Coulter)

- 6.3.3Merck KGaA (MilliporeSigma)

- 6.3.4Revvity

- 6.3.5Bio-Rad Laboratories Inc.

- 6.3.6Abcam plc

- 6.3.7Promega Corp.

- 6.3.8Enzo Biochem Inc.

- 6.3.9BioLegend Inc.

- 6.3.10Cell Signaling Technology Inc.

- 6.3.11GE HealthCare

- 6.3.12Sartorius AG

- 6.3.13Eurofins Scientific

- 6.3.14Charles River Laboratories

- 6.3.15Bachem Holding AG

- 6.3.16Creative BioMart

- 6.3.17Cayman Chemical

- 6.3.18LI-COR Biosciences

- 6.3.19RayBiotech Life Sciences

- 6.3.20BioVision Inc.

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-Need Assessment

Global Protein Binding Assays Market Report Scope

As per the scope of the report, protein binding assays refer to a set of laboratory techniques designed to measure the interaction between proteins and other molecules, such as drugs, ligands, small molecules, nucleic acids, or other proteins. These assays assess how strongly and specifically a molecule binds to a protein of interest.

The protein binding assays market is segmented by product type, technology, application, end users, and geography. By product type, the market is segmented into assay kits and reagents and instruments. By technology, the market is segmented into fluorescence-based assays, equilibrium dialysis, ultrafiltration, and other technologies. By application, the market is segmented into drug discovery, clinical diagnostics, proteomics research, and other applications. By end user, the market is segmented into academic and research institutes, pharmaceutical and biotechnology companies, contract research organizations, and other end users. By geography, the market is segmented into North America, Europe, Asia-Pacific, and the Rest of the world. The report offers the value (in USD) for the above segments.