Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.3 Billion |

| Market Size (2031) | USD 5.59 Billion |

| Growth Rate (2026 - 2031) | 5.38% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Insulin Infusion Pumps Market Analysis by Mordor Intelligence

The Insulin Infusion Pumps Market size was valued at USD 4.08 billion in 2025 and estimated to grow from USD 4.3 billion in 2026 to reach USD 5.59 billion by 2031, at a CAGR of 5.38% during the forecast period (2026-2031).

Sustained demand arises from the convergence of continuous glucose monitoring with automated insulin delivery, the transition from tethered to closed-loop platforms, and broader adoption among Type 2 diabetes patients. Patch pumps and hybrid closed-loop systems now set performance benchmarks, while reimbursement expansion and pediatric approvals enlarge the user base. Cybersecurity vigilance, supply-chain pressures, and regulatory complexity continue to temper growth, yet the insulin infusion pumps market remains pivotal to global diabetes management.

Key Report Takeaways

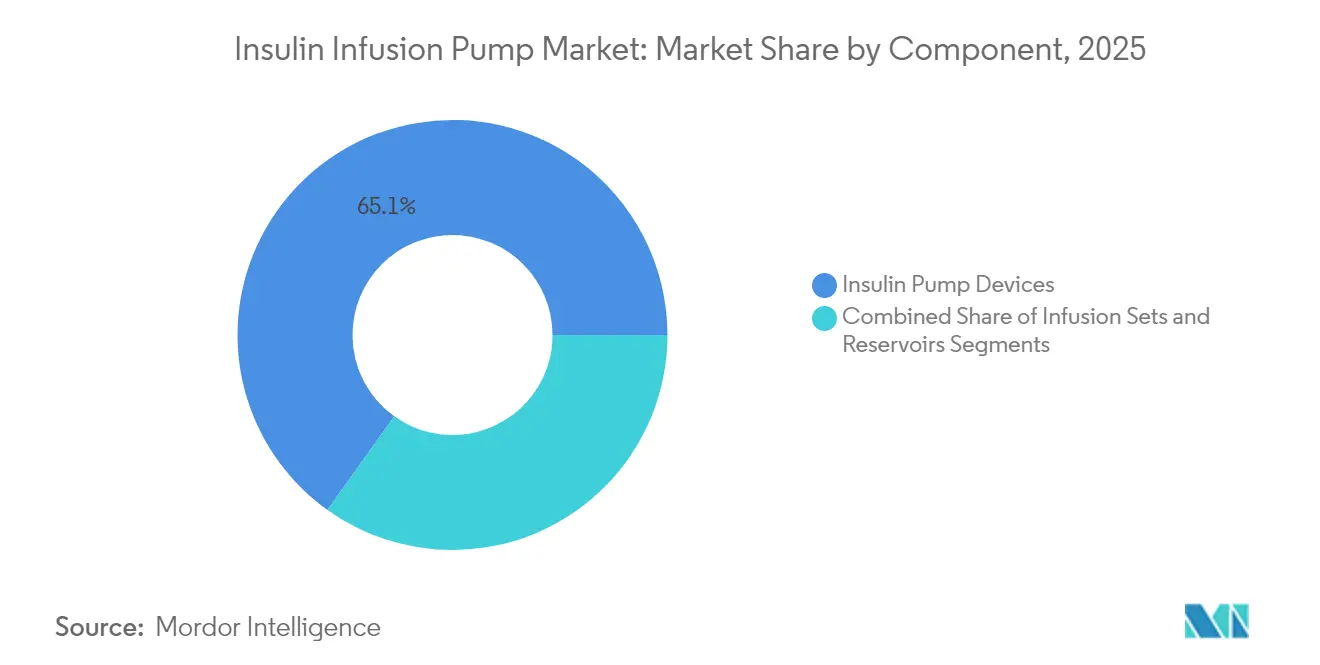

- By component, insulin pump devices led with 65.12% revenue share in 2025; reservoirs are projected to expand at an 7.62% CAGR through 2031.

- By pump type, patch pumps held 52.05% of the insulin infusion pumps market share in 2025, while the segment accelerates at an 8.28% CAGR to 2031.

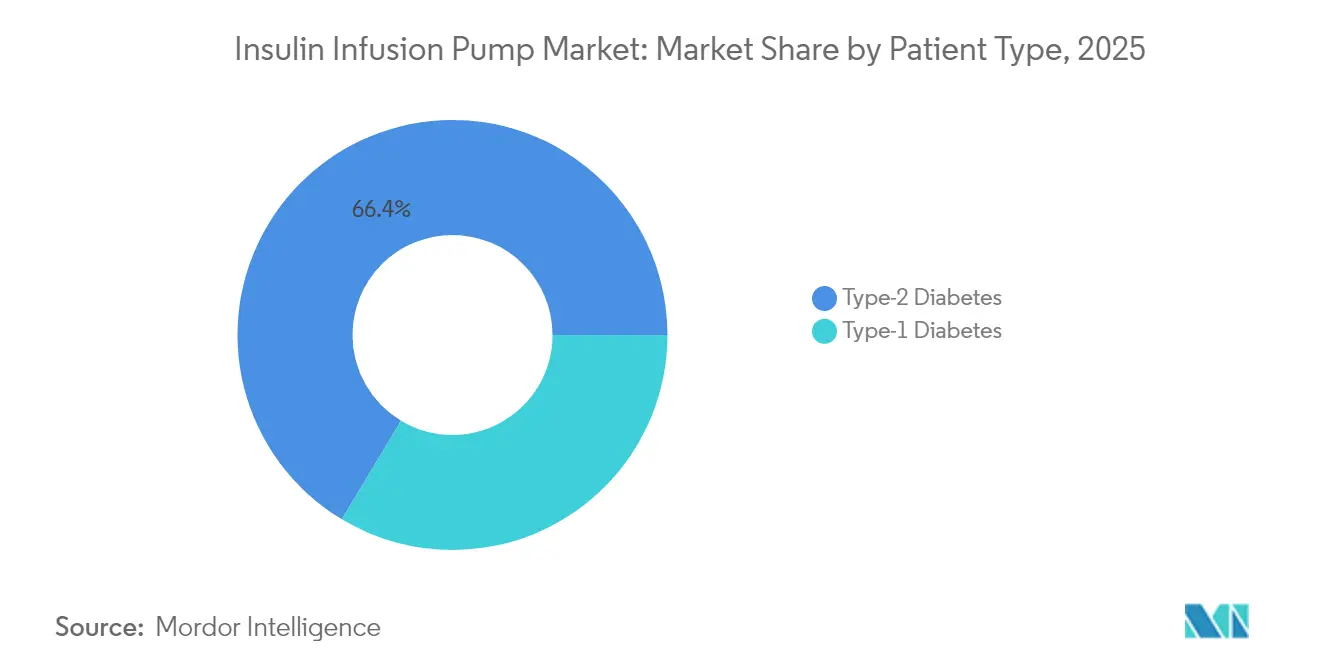

- By patient type, Type 2 diabetes accounted for 66.40% share of the insulin infusion pumps market size in 2025 and is advancing at a 9.55% CAGR through 2031.

- By end user, homecare settings captured 55.98% share in 2025 and represent the fastest growth at a 8.85% CAGR to 2031.

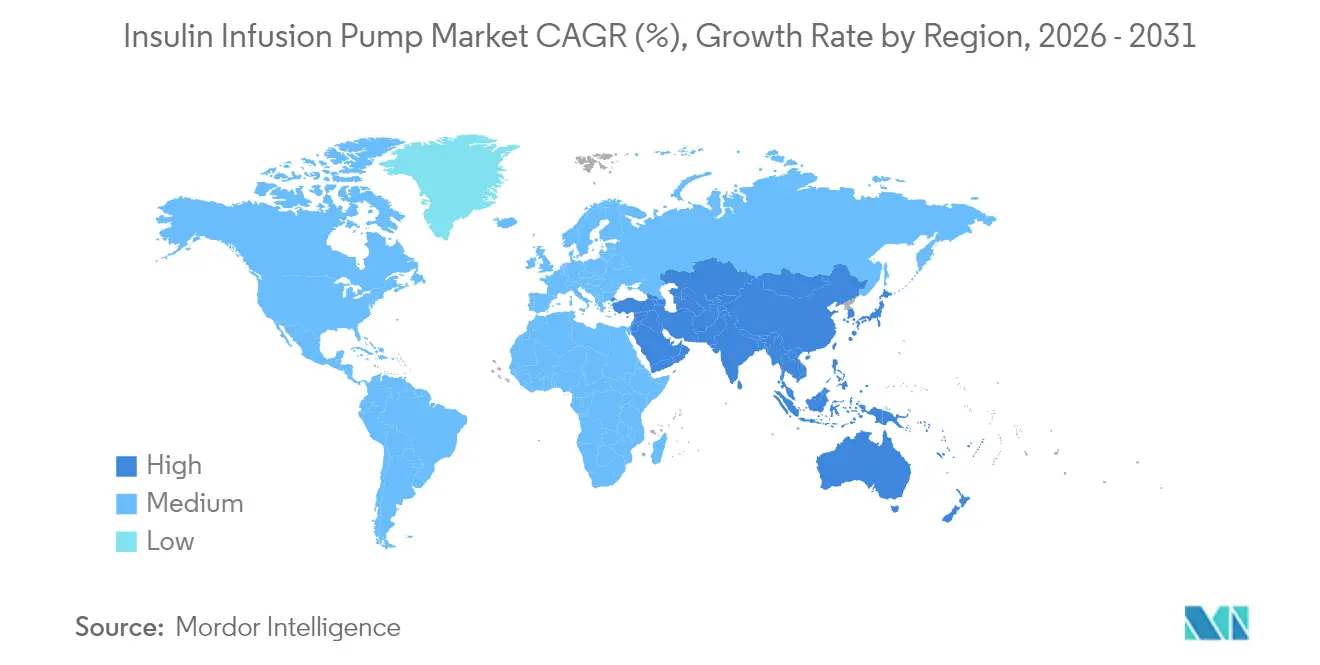

- By geography, North America held 36.95% share in 2025, whereas Asia-Pacific is expanding at a 6.72% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Insulin Infusion Pumps Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Adoption of Closed-Loop "Artificial Pancreas" Systems | +1.8% | Global, with North America and Europe leading | Medium term (2-4 years) |

| Rising Prevalence of Type 1 Diabetes in Youth | +1.2% | Global, with highest impact in developed markets | Long term (≥ 4 years) |

| Reimbursement Expansion for Tubeless Pumps | +0.9% | North America, Europe, select APAC markets | Short term (≤ 2 years) |

| Growth of the DIY Looping Community | +0.5% | Global, concentrated in tech-savvy demographics | Medium term (2-4 years) |

| Bluetooth-Enabled Analytics and Mobile Integration | +0.7% | Global | Short term (≤ 2 years) |

| Inclusion in Corporate Wellness Programs | +0.4% | North America, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption of Closed-Loop “Artificial Pancreas” Systems

FDA approval of Medtronic’s MiniMed 780G in April 2025 underscored the value of automated meal detection and five-minute insulin adjustments, pushing time-in-range figures above 70% among large user cohorts. Tandem’s Control-IQ platform shows comparable benefits, highlighting a technology race that rewards algorithm accuracy and sensor reliability. Artificial intelligence enables dose personalization that mimics physiologic insulin patterns, positioning closed-loop platforms as the future standard of care. Growing clinical proof amplifies payer confidence and broadens eligibility criteria. As marketing emphasizes lifestyle simplicity instead of device mechanics, patient receptivity rises, driving incremental units and recurring consumable sales.

Rising Prevalence of Type 1 Diabetes in Youth

Incidence rates among children now exceed 3.5 per 1,000 in the United States, with similar uptrends in Europe and parts of Asia.[1]JAMA Network, “Incidence of Type 1 Diabetes in US Youth,” jamanetwork.com Pediatric societies recommend pump therapy as first-line treatment, citing superior glycemic control and reduced nocturnal hypoglycemia.[2]International Society for Pediatric and Adolescent Diabetes, “Clinical Practice Guidelines 2024,” ispad.org FDA clearance of automated insulin delivery for ages two and above widens the pediatric addressable pool. Regional registries reveal adoption gaps, suggesting unmet demand where clinical support lags. Manufacturers respond with smaller reservoirs, simplified user interfaces, and colorful patch adhesives that resonate with younger users and caregivers.

Reimbursement Expansion for Tubeless Pumps

Medicare’s 2023 coinsurance cap and the Senior Savings Model materially lowered monthly insulin costs for pump users.[3]Centers for Medicare & Medicaid Services, “Insulin and the Senior Savings Model,” cms.gov Commercial formularies have catalogued patch pumps as preferred options, citing total-cost-of-care reductions from fewer emergency visits and hospitalizations. Several state Medicaid programs now bypass historic three-year replacement rules, accelerating upgrade cycles. Payer alignment on value-based outcomes creates predictable revenue streams for suppliers while mitigating patient expense anxiety. Broader coverage has a cascading impact on clinician prescribing habits, cementing tubeless technology in routine practice.

Rising Adoption of DIY Looping Systems

Open-source algorithms gave early proof that fully automated insulin delivery could be achieved with repurposed pumps and consumer electronics. These grass-roots experiments pressured commercial vendors to speed closed-loop launches and adopt interoperable architecture. Regulatory acknowledgment of patient-driven innovation, reflected in FDA guidance documents, legitimizes collaboration between citizen developers and device makers. The DIY ethos also fosters inclusive language, user-friendly dashboards, and frequent software updates all of which shape product roadmaps. While home-built systems are not broadly reimbursed, their influence on design expectations remains profound.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cybersecurity Risks in Connected Devices | -0.8% | Global, with heightened concern in developed markets | Short term (≤ 2 years) |

| High Out-of-Pocket Costs in Emerging Markets | -1.1% | APAC, Latin America, Middle East & Africa | Long term (≥ 4 years) |

| Supply Chain Disruptions for Sterile Tubing and Components | -0.6% | Global | Medium term (2-4 years) |

| Regulatory Delays for Next-Gen Devices | -0.4% | Global, with varying impact by region | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cybersecurity Risks in Connected Devices

In 2024 the FDA flagged vulnerabilities in certain wireless pumps that could allow unauthorized access and unintended insulin delivery, prompting multiple Class I recalls. Academic analyses have since documented potential exploit pathways via unsecured Bluetooth channels, underscoring the need for end-to-end encryption and tamper-proof firmware. New FDA premarket guidance requires threat-mitigation plans and postmarket monitoring, adding development cost and elongating approval timelines. Hospitals now press suppliers for detailed cybersecurity certifications before procurement. Although no catastrophic patient harm has been reported publicly, lingering risk perception may slow adoption among risk-averse payers.

High Out-of-Pocket Costs in Emerging Markets

Insurance penetration for durable diabetes technologies remains limited in large parts of Asia, Latin America, and Africa. Surveys reveal that many patients ration insulin and test strips, leaving little disposable income for premium pump hardware. Adoption sits below 5% in some high-burden countries, despite clear clinical gains among users. Manufacturers that wish to tap these markets must tailor price points and financing terms while advocating for broader public reimbursement. Without systemic funding solutions, the insulin infusion pumps market will struggle to fulfill its preventive potential in regions where diabetes prevalence rises fastest.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Devices Anchor Revenue While Reservoirs Accelerate Growth

Insulin pump devices retained 65.12% of 2025 revenue, underscoring their premium pricing and embedded software complexity. Consumable reservoirs, however, expanded faster at an 7.62% CAGR as hybrid closed-loop algorithms modulated insulin micro-boluses more frequently. Integration of smart sensors inside reservoirs to detect occlusions and air bubbles heightens patient safety and gives vendors cross-selling leverage. Strategic partnerships, such as Medtronic pairing its pumps with Abbott glucose sensors, exemplify an ecosystem approach that influences procurement.

Consumable dynamics also strengthen recurring revenue visibility. Manufacturers introduce extended-wear infusion sets aimed at seven-day site usage, reducing insertion trauma and driving brand loyalty. Competitive differentiation now hinges on frictionless cartridge loading, lower residual insulin waste, and antimicrobial linings that curb infection risk. These incremental innovations stabilize unit volume outlook, even when device replacement cycles lengthen in mature markets.

By Pump Type: Patch Technology Steers Market Evolution

Patch pumps captured 52.05% share in 2025 and are on track for an 8.28% CAGR, validating patient preference for tubeless, discreet wearables. Sleek industrial design, waterproof housing, and automated cannula insertion raise user comfort and minimize social stigma. Tethered pumps, while declining, still serve high-dose users who need large reservoirs or dual-hormone research protocols. Implantable systems remain experimental due to surgical hurdles.

Competition within the patch segment intensifies as Tandem’s Mobi challenges Insulet’s incumbency with a thinner profile and smartphone-only interface. Emerging entrants position low-cost patch alternatives for Asia-Pacific, bundling simplified feature sets with subscription pricing. Firmware upgrades delivered over the air enhance functionality without physical replacements, reinforcing user stickiness.

By Patient Type: Type 2 Diabetes Expansion Reshapes Demand

Type 2 diabetes patients comprised 66.40% of users in 2025 and drive the highest 9.55% CAGR, transforming the pump landscape. Evidence from the SECURE-T2D trial showed HbA1c reductions from 8.2% to 7.4% when Omnipod 5 supplanted multiple daily injections. FDA clearance of Tandem’s Control-IQ+ for adults with Type 2 diabetes validates algorithmic dosing for insulin-resistant physiology. Providers increasingly transition intensively managed patients onto pumps to relieve injection fatigue and stabilize glucose variability.

Type 1 diabetes remains foundational for early adoption of experimental features and supplies a loyal user base that advocates product refinements. Nevertheless, as prevalence growth tilts toward Type 2, device makers recalibrate messaging to emphasize ease of onboarding, limited carbohydrate logging, and telehealth-enabled coaching suited for older or comorbid populations.

By End User: Homecare Settings Lead Uptake and Growth

Homecare settings generated 55.98% of revenue in 2025 and expand at a 8.85% CAGR, propelled by user-friendly mobile apps and remote patient monitoring. Telehealth growth during the COVID-19 pandemic demonstrated that most titration and troubleshooting can occur virtually, reducing the need for frequent clinic visits. Hospitals concentrate on initiation and acute troubleshooting but cede routine management to community endocrinologists and certified diabetes educators.

Ambulatory surgical centers cater to implantable and complex revision procedures, carving out a modest yet specialized niche. Integration with electronic health records enables automated data sharing, allowing multidisciplinary teams to adjust care plans without geographic constraints. As payers reimburse virtual consultations, home-based pump adoption becomes financially rational, sustaining momentum for the insulin infusion pumps market.

Geography Analysis

North America remained the largest market in 2025 with a 36.95% share, underpinned by widespread insurance coverage, advanced supply chains, and early demand from both Type 1 and Type 2 populations. The region’s mature infrastructure supports swift adoption of closed-loop upgrades and interoperable component ecosystems, though unit growth now mirrors replacement cycles more than net new users. Cybersecurity regulations also originate here, influencing global design standards.

Europe contributes steady volumes thanks to universal healthcare and robust clinical registries that benchmark outcomes. Reimbursement frameworks vary but generally favor technology proven to cut hospitalization costs. Rapid CE-mark pathways for integrated pumps and continuous glucose monitors promote competitive diversity. The Middle East and Africa lag in penetration, yet investment initiatives in Saudi Arabia and the UAE spark pilot programs that introduce patch pumps into public diabetes centers. Asia-Pacific posts the fastest 6.72% CAGR through 2031 due to rising diabetes prevalence, urbanization, and expanding middle-class insurance pools. China’s tiered hospital system now reimburses select patch pumps for pediatric Type 1 users, while India experiments with low-cost subscription bundles for Type 2 adults. Latin America sits between growth extremes, with Brazil and Mexico leading regional adoption as private insurers pilot value-based diabetes programs. Market entrants target localized language support, hotter-climate adhesive formulations, and flexible financing to fit each region’s socioeconomic profile.

Regulatory Landscape

Regulation of insulin infusion pumps is tightening around connected, interoperable automated insulin delivery (AID) ecosystems that combine a pump, CGM, and algorithm/controller. In the United States, ACE (Alternate Controller Enabled) insulin pumps are regulated as Class II devices under 21 CFR 880.5730, while interoperable automated glycemic controllers and automated insulin dosing functions fall under special controls (including communication interface validation) under 21 CFR 862.1356, which keeps verified interoperability across system components at the center of submissions.

Cybersecurity and quality-system compliance are now key regulatory anchors for product updates and submissions. The FDA Quality Management System Regulation (QMSR) took effect on February 2, 2026, incorporating ISO 13485:2016 by reference, and FDA guidance on Cybersecurity in Medical Devices (premarket content and QMS considerations) raises the documentation bar for connected pumps. In Europe, insulin pumps are generally treated as higher-risk Class IIb devices under EU MDR 2017/745 (Annex VIII, Rule 12), and Article 117 combination-product provisions can require Notified Body involvement for device components tied to medicinal product administration, adding lifecycle obligations such as post-market surveillance and periodic safety updates.

Value Chain Analysis

The insulin infusion pumps value chain is an ecosystem spanning pump OEMs (for example, Medtronic, Insulet, and Tandem Diabetes Care), critical component suppliers (electronics, batteries, plastics, adhesives), and sterile disposables (infusion sets and reservoirs/cartridges). Software and algorithm development increasingly differentiates automated insulin delivery performance. Manufacturers typically keep system architecture, algorithm/software, and final product stewardship in-house, while using specialized contract partners for precision molding, sterile assembly, and scalable consumables manufacturing, then distribute through durable medical equipment and pharmacy channels supported by patient training and customer service infrastructure.

Interoperability partnerships with CGM companies (notably Abbott and Dexcom) influence downstream commercialization, reimbursement acceptance, and patient stickiness, because closed-loop performance depends on the sensor-pump-controller interface as much as on pump hardware. Supply continuity remains a strategic constraint, and recent capacity actions show how vendors and partners are responding: in May 2026, ViCentra initiated commercial-scale production of Kaleido pump consumables at Phillips Medisize (a Molex company), tripling capacity to support a larger installed base. In the United States, pump platforms are also widening integrated CGM options, including new FreeStyle Libre 3 Plus compatibility for Tandem's t:slim X2 ecosystem.

Competitive Landscape

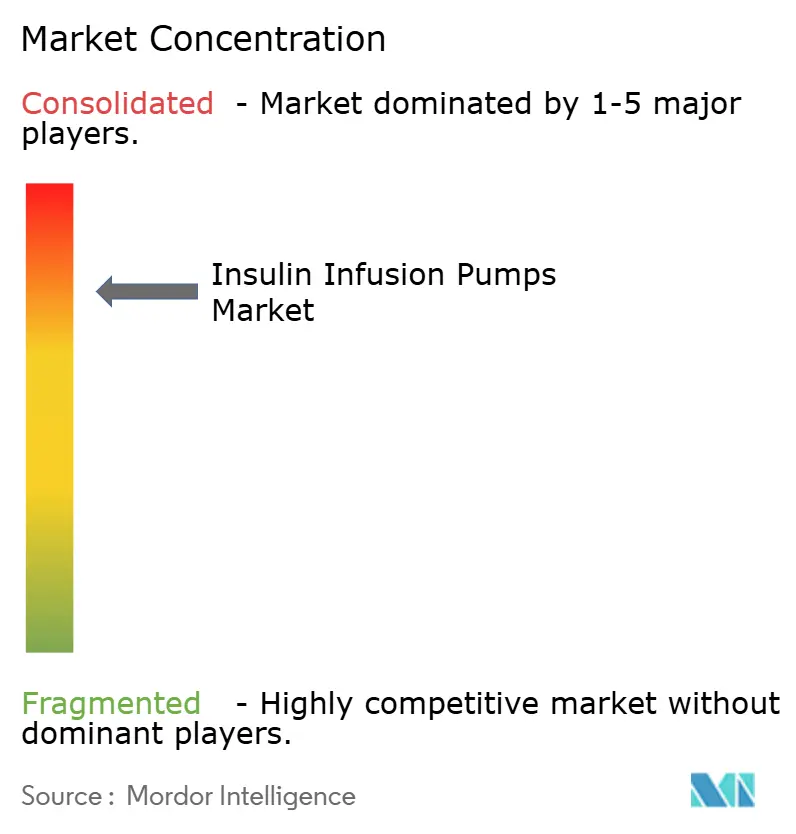

The insulin infusion pump market demonstrates consolidation. Three vendors Medtronic, Insulet, and Tandem Diabetes Care collectively holds significant share of global revenues, establishing a moderately concentrated structure. Medtronic’s MiniMed 780G paired with the Simplera Sync CGM accounts for the largest installed base, driving Q2 FY25 diabetes revenue to USD 686 million. Insulet maintains leadership in patch pumps; its 2024 sales reached USD 2 billion on the strength of Omnipod 5 expansion into Type 2 cohorts Insulet. Tandem leverages the t:slim X2 platform and Control-IQ algorithm, reporting USD 282.6 million in Q4 2024 revenue and outlining 2025 guidance near USD 1 billion.

Emerging player Beta Bionics differentiates with the iLet Bionic Pancreas, which removes carbohydrate counting and posted 36% revenue growth in Q1 2025. Market rivalry centers on algorithm performance, mobile UX, and supply-chain resilience. Strategic moves include Medtronic’s plan to spin off its diabetes business into an autonomous company within 18 months, expected to improve capital allocation and partnership agility. Tandem and Abbott inked a 2025 pact to integrate dual glucose-ketone sensing and pump automation, aiming to reduce diabetic ketoacidosis episodes.

Component suppliers also shape competition. Adhesive innovators develop hypoallergenic patches, while sensor makers pursue factory-calibrated CGMs that shorten pump onboarding. Interoperability labeling lets niche vendors bolt their technologies onto multiple pump brands, fragmenting certain sub-segments. Despite brisk innovation, regulatory hurdles and cybersecurity expectations restrict market entry speed, reinforcing the advantage of incumbents with deep compliance experience and global service footprints.

Insulin Infusion Pumps Industry Leaders

Insulet Corporation

Tandem Diabetes Care

Ypsomed

Ascensia Diabetes Care

Medtronic

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Type 2 diabetes indication expansions and simplified, smartphone-centric form factors are creating actionable whitespace for automated insulin delivery beyond the traditional Type 1 core. In February 2026, Medtronic received FDA clearances that expanded MiniMed 780G use into insulin-requiring Type 2 diabetes and enabled use with ultra-rapid-acting insulins (Fiasp and Lyumjev). In March 2026, FDA clearance for a screenless, smartphone-controlled MiniMed Flex pump reinforced the shift toward lower-burden user experiences that fit homecare-led adoption.

Manufacturing scale-up and international rollout initiatives offer a second opportunity layer by supporting recurring consumables demand and access constraints that can limit uptake in newer geographies. Insulet disclosed a USD 200 million investment (January 2026) to establish a production facility in Heredia, Costa Rica, and ViCentra started higher-volume consumables production in May 2026 through Phillips Medisize, pointing to ongoing efforts to expand supply and improve unit economics. On the product roadmap side, clinical and conference disclosures on next-generation fully closed-loop capabilities (for example, Omnipod 6 data shared in June 2026 and Medtrum updates presented at ATTD 2026) show vendors pushing toward reduced meal input and broader use-case coverage, keeping competition centered on algorithm automation and ecosystem breadth rather than pump mechanics alone.

Recent Industry Developments

- July 2026: Insulet launched Omnipod 5 and Omnipod Discover in Spain, extending its tubeless insulin delivery ecosystem into its 26th international market. The paired commercialization of a pump platform and a companion data experience supports localized onboarding and can shorten time-to-adoption by aligning patient education, clinician workflows, and ongoing engagement in a new geography.

- June 2026: Tandem Diabetes Care received CE mark clearance for its t:slim X2 and Tandem Mobi automated insulin delivery systems for adults with type 2 diabetes and for use in type 1 diabetes during pregnancy in Europe. This regulatory milestone broadens addressable segments under a unified platform strategy, strengthening Tandem's position in regions where reimbursement and clinical pathways often follow CE-marked indications.

- March 2024: The US FDA issued a safety communication highlighting cybersecurity vulnerabilities affecting certain connected insulin pump systems, which contributed to heightened scrutiny and recalls across wireless-enabled devices. The resulting focus on secure connectivity and postmarket monitoring increased compliance requirements for manufacturers and influenced procurement diligence among providers and payers.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as revenue generated from insulin infusion pump systems used to deliver insulin for diabetes management, including the pump device and the required disposable delivery components used with it.

Scope exclusions: We exclude insulin pens and syringes, software-only algorithms, general infusion accessories not specific to insulin pumps, veterinary use, and hospital multi-drug infusion systems.

Segmentation Overview

- By Component

- Insulin Pump Devices

- Infusion Sets

- Reservoirs

- By Pump Type

- Tethered Pumps

- Patch Pumps

- Implantable Pumps

- By Patient Type

- Type-1 Diabetes

- Type-2 Diabetes

- By End User

- Hospitals & Clinics

- Homecare Settings

- Ambulatory Surgical Centers

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market guardrails and to build the first version of the demand pool. We mainly relied on public health and epidemiology references, such as CDC diabetes statistics, WHO diabetes fact sheets, and peer-reviewed diabetes technology journals, to understand the insulin-requiring population and therapy patterns.

To connect demand with real-world adoption, we also reviewed sources such as OECD health indicators, national health payer or reimbursement bulletins, and medical device regulatory databases (for clearance timing and product availability). Company annual reports, investor presentations, and reputable press coverage were used to cross-check product positioning and geographic exposure, and patent databases helped spot feature shifts that can affect replacement cycles and pricing. For numeric backstops like company financial splits and tracked news events, a paid subscription database was referenced where applicable. These examples are illustrative, and they are not exhaustive because several other public sources were also used for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary work focused on validating pump adoption, pricing patterns, and replacement behavior across major regions, and then stress-testing the desk assumptions that most often create sizing errors. We spoke with a mix of manufacturers, distributors, clinicians, and diabetes care stakeholders so coverage included both supply-side realities and patient pathway signals. Where major gaps appeared, we re-checked them with follow-up conversations before finalizing inputs.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 14% | APAC: 44% |

| Mid tier: 56% | Functional/Unit leaders: 32% | EMEA: 34% |

| Smaller Players: 16% | Managers: 54% | Americas: 22% |

Market-Sizing & Forecasting

The core sizing started with a top-down build that converts the insulin-requiring diabetes demand pool into pump users, and then values that usage using observed price bands for pump systems and ongoing disposable consumption. To keep the model practical, we used a small set of repeatable inputs, including the insulin-requiring population, pump penetration by therapy setting, replacement cycle for the pump device, average annual disposable usage per user, and regional reimbursement intensity that shifts uptake and price.

Once the first pass totals were produced, they were corroborated with selective bottom-up approximations, such as rolling up a sampled set of supplier revenues by region and checking implied units using average selling prices. Where bottom-up signals were incomplete, gaps were handled by applying interview-validated coverage ratios and then rebalancing to match the wider demand indicators. Forecasts were built using scenario analysis supported by expert views on reimbursement direction, technology adoption (including automation features), and expected pricing progression, and then a final pass was done to keep growth consistent with underlying patient and utilization trends.

Data Validation & Update Cycle

Outputs were validated through triangulation that compares the final market value with independent signals like implied pump user counts, per-user disposable consumption, and regional pricing bands, before the numbers are signed off. Any outliers were flagged and reviewed in a second analyst check, and if the variance could not be explained by scope or timing, the relevant assumptions were revisited and revalidated through additional calls.

The report is refreshed annually, and interim adjustments are made when major events materially change demand or pricing, such as reimbursement shifts or meaningful product launches and recalls. Before delivery, a final review pass is completed so clients receive an updated view aligned with the latest available public information and primary feedback.

Mordor Intelligence's Insulin Infusion Pumps Market Sizing Compared With Other Published Estimates

Published market numbers for insulin infusion pumps can look far apart, even when they describe the same therapy area, because the counted items and the valuation logic are not always consistent. Differences usually come from what is included around the pump system, which year is treated as the current base, and how pricing and adoption are assumed to move over time.

The main gap drivers here are scope and how recurring disposables are treated, since some estimates bundle a broader insulin pump ecosystem (including a wider accessory basket) or apply faster adoption and price step-ups without matching them to reimbursement and replacement cycles. Another common reason is timing, where currency conversion windows and refresh cadence can shift a current-year value, especially when device pricing is stable but disposable mix is changing. Counting only CE or FDA-cleared electromechanical insulin infusion pumps with dedicated infusion sets and reservoirs, and excluding pen injectors and software-only items, explains why the 2026 value anchors differently for Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 4.3 B (2026) | |

| Global Consultancy A | USD 5.90 B (2024) | Uses a broader insulin pump framing and appears to include a wider accessories basket, and it also anchors on a different base year, which lifts the reported current value versus a 2026 device plus required disposables scope. |

| Industry Publisher B | USD 5.9 B (2024) | Reported value is tied to a longer 2025 to 2035 outlook and a 2024 base, with limited public detail on exclusions, which can lead to wider inclusions around technology and end-use that inflate the near-term total. |

The table shows that year selection and what gets counted around the pump system are the main reasons for the spread across published numbers. By keeping the steps traceable to patient demand, pump penetration, replacement timing, and recurring disposable usage, the final market value is easier to reproduce and to reconcile with on-the-ground adoption signals.

Key Questions Answered in the Report

What is the current size of the insulin infusion pumps market and how fast is it growing?

The market stood at USD 4.3 billion in 2026 and is forecast to reach USD 5.59 billion by 2031, reflecting a 5.38% CAGR.

Which pump type captures the largest share of the insulin infusion pumps market?

Patch pumps dominate with 52.05% market share in 2025 and lead growth at an 8.28% CAGR through 2031.

How are Type 2 diabetes patients influencing future demand?

Type 2 diabetes users already account for 66.40% of 2025 revenue and drive the highest 9.55% CAGR as guidelines now recommend pump therapy for insulin-dependent adults.

What geographic region offers the fastest growth opportunity?

Asia-Pacific posts the quickest expansion at a 6.72% CAGR to 2031, propelled by rising diabetes prevalence and improving healthcare reimbursement.

What major risk could slow near-term adoption?

Cybersecurity vulnerabilities in connected pumps have triggered recent FDA recalls and add compliance costs that may temper short-term growth.

Page last updated on: