Global Pediatric Medical Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

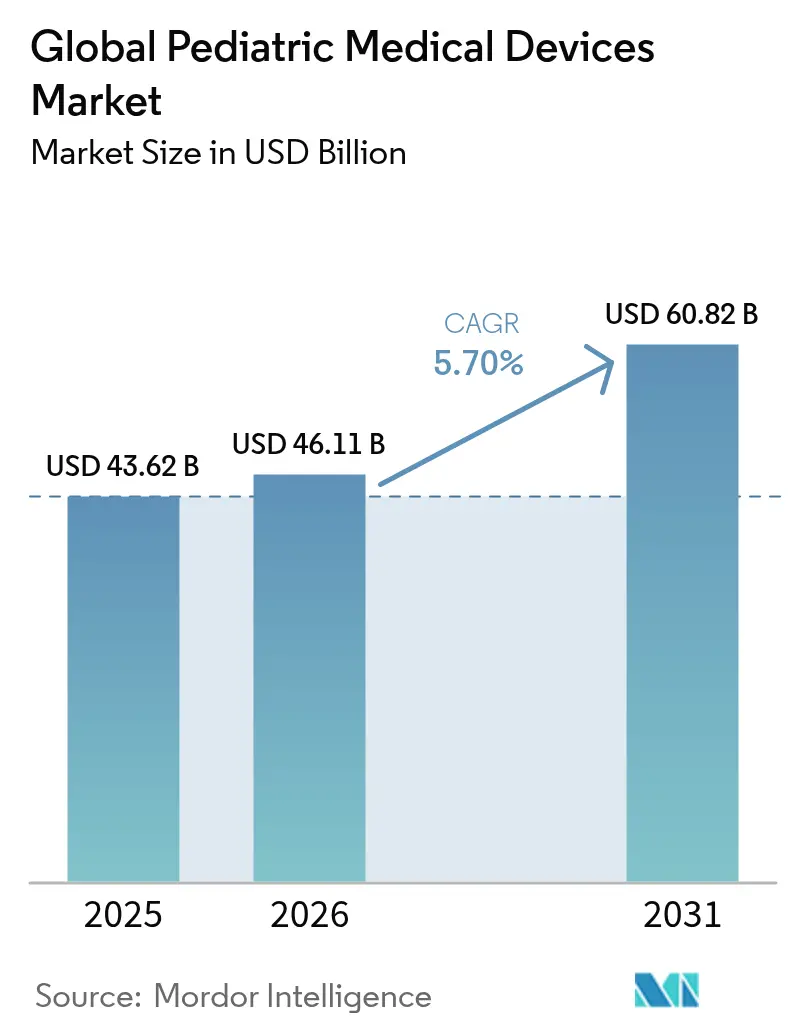

| Market Size (2026) | USD 46.11 Billion |

| Market Size (2031) | USD 60.82 Billion |

| Growth Rate (2026 - 2031) | 5.70% CAGR |

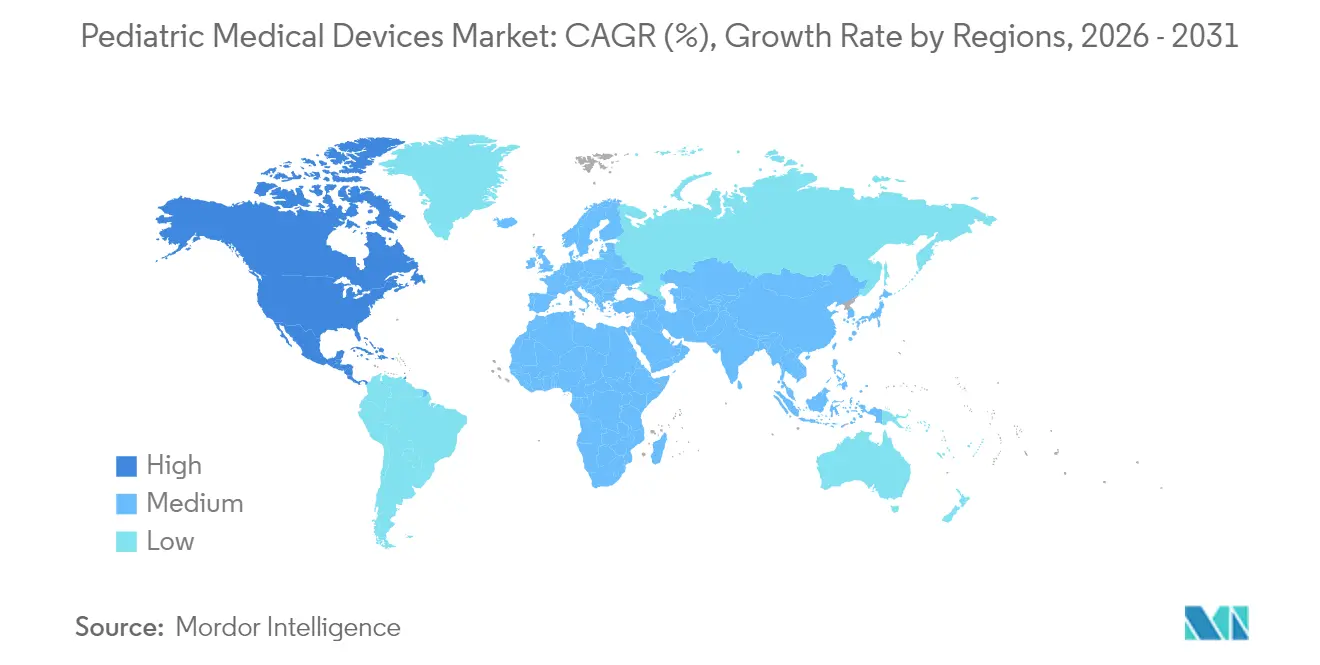

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Pediatric Medical Devices Market Analysis by Mordor Intelligence

The pediatric medical devices market size was valued at USD 43.62 billion in 2025 and estimated to grow from USD 46.11 billion in 2026 to reach USD 60.82 billion by 2031, at a CAGR of 5.70% during the forecast period (2026-2031). Rising preterm birth rates, growing demand for minimally invasive interventions sized for children, and steady regulatory clearances for breakthrough products keep the growth trajectory intact. North America continues to lead on account of mature reimbursement rules and dedicated children’s hospitals, while Asia-Pacific gains momentum on the back of demographic tailwinds and targeted public-health spending. Rapid uptake of AI-enabled monitoring tools pushes device makers to integrate software intelligence into legacy hardware, opening new revenue streams. At the same time, the need to secure pediatric-grade biomaterials, comply with expanded supply-chain reporting rules, and invest in long-term safety studies creates operational complexity that only the most agile players can navigate.

Key Report Takeaways

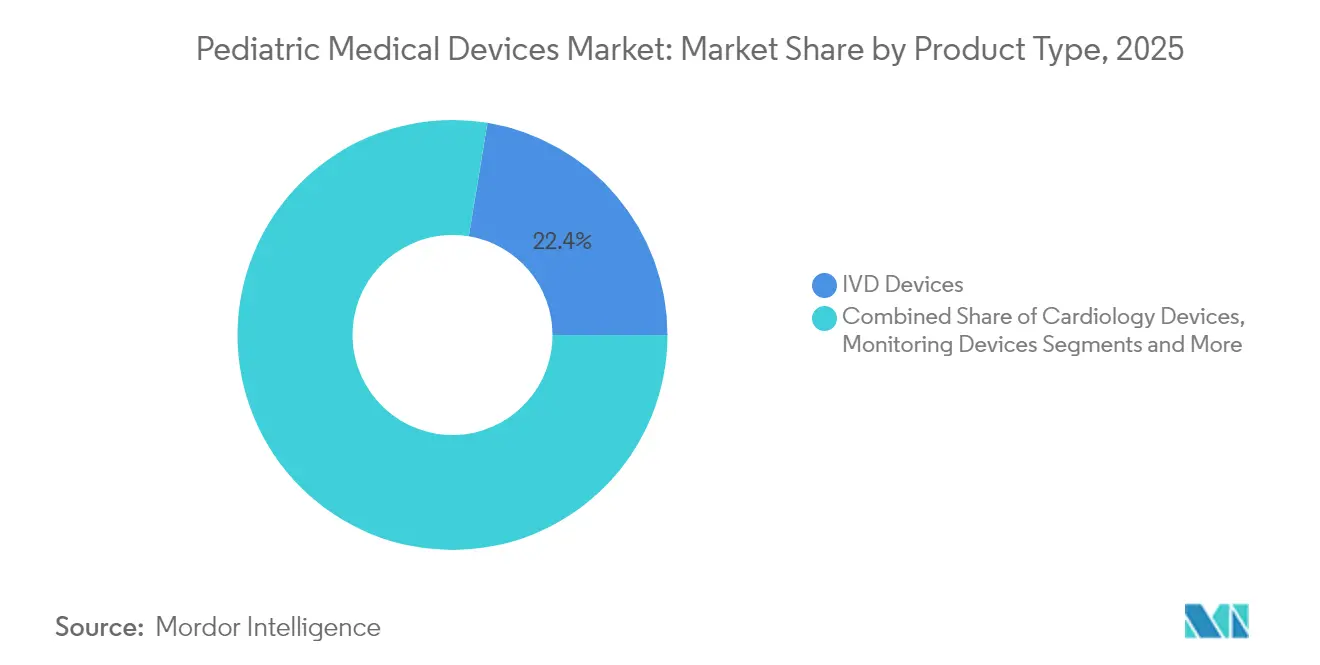

- By product type, IVD devices held 22.40% of the pediatric medical devices market share in 2025, whereas monitoring devices are projected to post the fastest 6.15% CAGR to 2031.

- By end user, hospitals captured 53.70% revenue share in 2025 and homecare settings are expected to grow at a 6.55% CAGR through 2031.

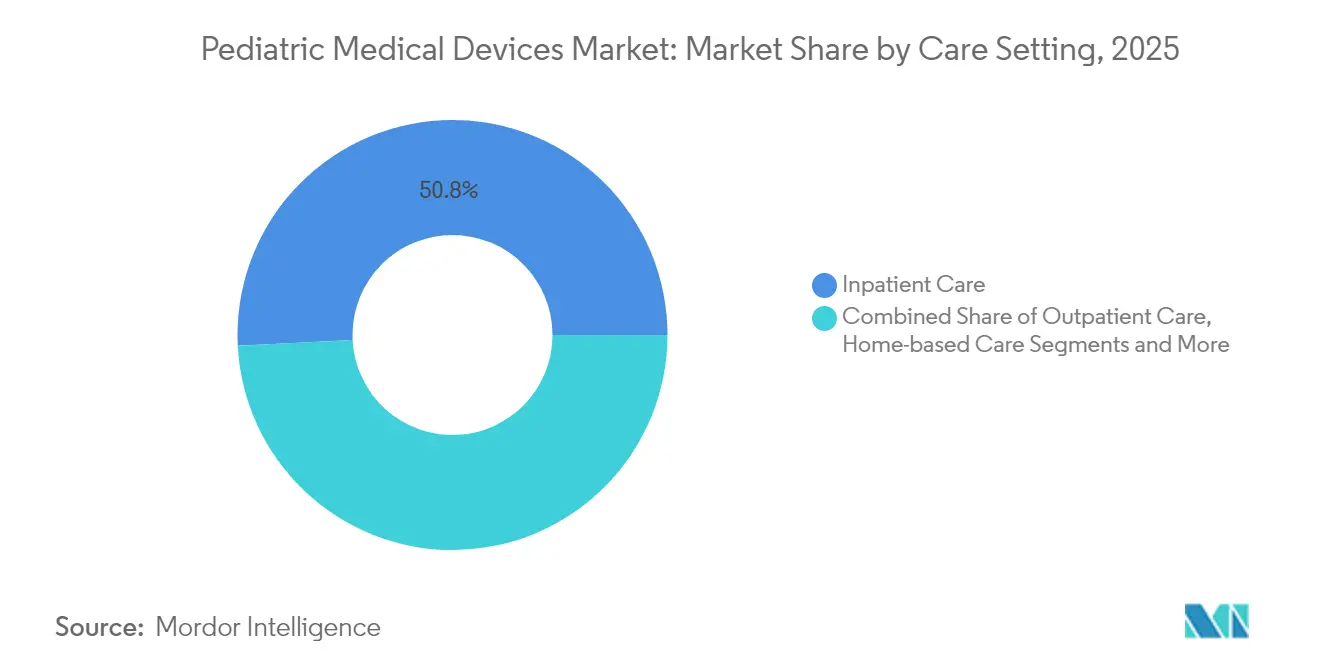

- By care setting, inpatient settings commanded 50.80% share of the pediatric medical devices market size in 2025, while home-based care will expand at a 6.95% CAGR between 2026-2031.

- By technology, conventional devices controlled 48.20% of the 2025 market and AI-enabled devices are forecast to rise at a 7.05% CAGR.

- By geography, North America accounted for 43.10% of the 2025 pediatric medical devices market share; Asia-Pacific is the fastest-growing region at a 7.08% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Pediatric Medical Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising pre-term birth incidence | +1.2% | Global, with highest impact in North America and developing regions | Medium term (2-4 years) |

| Expansion of pediatric-focused hospital infrastructure | +0.8% | Asia-Pacific core, spill-over to MEA and Latin America | Long term (≥ 4 years) |

| Rapid adoption of minimally-invasive cardiac interventions | +1.0% | North America & EU, expanding to APAC | Short term (≤ 2 years) |

| Home-based remote monitoring reimbursement roll-outs | +0.7% | North America, early adoption in EU | Medium term (2-4 years) |

| New reimbursement codes in the US and parts of Europe | +0.5% | North America & EU | Short term (≤ 2 years) |

| 3D-printed patient-specific implants for rare anomalies | +0.6% | Global, led by North America and EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Pre-term Birth Incidence

Preterm births reached 10.4% in the United States for the third straight year. India records roughly 1.5 million premature deliveries each year, driving sustained demand for incubators, tubes, and ventilators. Such statistics oblige manufacturers to miniaturize devices and extend durability for lengthier neonatal care cycles, directly fueling the pediatric medical devices market.

Expansion of Pediatric-Focused Hospital Infrastructure

China’s “years of pediatric and mental health services” (2025-2027) program lists eight initiatives that strengthen dedicated children’s wards and specialist centers. India’s Rainbow Children’s Medicare now runs 1,715 beds across 17 hospitals with occupancy up from 44.6% to 55.4% in two fiscal years, signaling faster throughput and procurement intensity. Multilateral lenders such as the Asian Infrastructure Investment Bank finance new pediatric towers in the Philippines, where bed density remains low at 0.89 per 1,000 residents. These bricks-and-mortar expansions translate into continuous capital-equipment refreshes that underpin the pediatric medical devices market.

Rapid Adoption of Minimally Invasive Cardiac Interventions

The FDA cleared the Minima Stent System for neonates as light as 1.5 kg, posting a 97.6% procedural success rate without major complications. The Amplatzer Piccolo Occluder closes patent ductus arteriosus in premature infants with more than 98% efficacy [1]Abbott, “Amplatzer Piccolo Occluder Clinical Data,” abbott.com. Modified vascular plug techniques deliver 91% success in pulmonary flow restriction procedures, cutting operating time when clinicians choose the transjugular route. These outcomes shorten ICU stays and spark a long-term shift toward catheter-based solutions, enlarging the pediatric medical devices market.

Home-Based Remote Monitoring Reimbursement Roll-Outs

In its 2025 rule set, CMS raised home health payments by 2.7% and ordered agencies to publish their pediatric service capabilities. AI-enabled epidermal electronic biosensors now stick to fragile neonatal skin with minimal irritation while maintaining high-fidelity signals. The SONU Band, green-lit by the FDA in June 2025, delivers acoustic vibrational therapy and reports 80% symptom relief for congested children within 15 minutes. These reimbursements and product launches accelerate technology transfer from hospital to home, expanding addressable volume for the pediatric medical devices market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Small addressable patient pools limit ROI | -0.9% | Global, particularly affecting rare disease segments | Long term (≥ 4 years) |

| Stringent FDA & EU safety evidence requirements | -0.6% | North America & EU, with spillover effects globally | Medium term (2-4 years) |

| Scarcity of large, high-quality pediatric datasets | -0.4% | Global, with acute impact in emerging markets | Medium term (2-4 years) |

| Supply-chain shortages of pediatric-grade biomaterials | -0.3% | Global, with highest impact in North America & EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Small Addressable Patient Pools Limit ROI

Humanitarian approvals cover devices that treat conditions faced by fewer than 200,000 US patients annually, such as SeaStar Medical’s cartridge for pediatric acute kidney injury [2]Food and Drug Administration, “Guidance on Pediatric Medical Device Development,” fda.gov. OrthoPediatrics, focused solely on young patients, has installed 71 orthopedic systems yet still leans on premium pricing and acquisitions to scale. Limited volumes dilute R&D payback, slowing new-product launches that would otherwise enlarge the pediatric medical devices market.

Stringent FDA & EU Safety Evidence Requirements

October 2024 FDA guidance now asks for long-term neurodevelopmental studies on neonatal devices, driving up trial costs and timelines. EU MDR 2024/1860 obliges manufacturers to log supply disruptions and extends legacy-device deadlines to 2028, adding documentation burdens [3]EUR-Lex, “Regulation (EU) 2024/1860,” eur-lex.europa.eu . Enforcement actions such as the 2024 warning letter to Trexo Robotics over design-control lapses show real financial stakes. These barriers slow market entry and temper growth in the pediatric medical devices market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: IVD Leadership with Monitoring Momentum

IVD devices captured 22.40% of the pediatric medical devices market share in 2025, underlining their centrality in clinical decision-making. Monitoring devices are projected to clock a 6.15% CAGR through 2031 as care teams transition from episodic sampling to continuous data feeds. The AI-equipped plush toy that grades infant neuro-development underscores how ambient sensors migrate into child-friendly form factors. Cardiology devices keep benefitting from catheter-based breakthroughs such as the Minima Stent. Respiratory and anesthesia platforms hold steady given the high volume of premature births that need ventilatory support. Supply tightness in specialty polymers occasionally forces clinicians to repurpose adult lines, highlighting the importance of material innovation for the pediatric medical devices market.

Diagnostic imaging players add deep-learning modules to ultrasound and X-ray consoles, while ENT and mobility aids receive a boost from wearables such as the SONU Band. Collectively these innovations anchor the diversification that sustains the pediatric medical devices market size across hospital and home settings.

By End User: Hospital Dominance Confronts Home-Care Surge

Hospitals controlled 53.70% of revenue in 2025 thanks to high-complexity procedures and integrated supply contracts. Yet homecare settings are set to rise 6.55% annually as reimbursement and technology converge to allow advanced interventions outside hospital walls. Laboratories face shrinking sample volumes as point-of-care analyzers and minimally invasive sensors redirect testing closer to patients. Children’s clinics adopt compact ultrasound units that quicken triage and improve throughput. The pediatric medical devices market size for ambulatory surgeries inches up as transcatheter approaches remove the need for open repair. AI-supported wound vacuums and biosensors enable families to manage recovery at home, easing the inpatient load and reshaping demand patterns in the pediatric medical devices market.

By Care Setting: Inpatient Stability Versus Home-Based Innovation

Inpatient facilities still house 50.80% of the 2025 market by value but growth is subdued compared with other settings. Emergency rooms and critical-care bays remain indispensable for fragile neonates, maintaining baseline equipment cycles. Outpatient suites gain share through same-day transcatheter fixes that sidestep overnight admission. Above all, home-based care, forecast to grow 6.95% a year, unlocks new procurement channels for wireless monitors, wearable stimulators, and AI-guided therapy apps. The SONU Band’s clearance illustrates how software-defined hardware now qualifies for reimbursements traditionally reserved for durable equipment. As a result, the pediatric medical devices market keeps tilting toward distributed use environments that favor lightweight, user-friendly designs.

By Technology: AI-Enabled Devices Disrupt Conventional Workflows

Conventional platforms still represent 48.20% of 2025 spend because they fit entrenched care protocols and carry broad regulatory familiarity. However, AI-enabled devices are forecast to climb 7.05% annually as algorithms improve accuracy and personalize therapy. Nanowear’s cuffless blood-pressure patch secured 510(k) status and targets pediatric hypertension monitoring. 3D-printed implants, including bioresorbable heart valves from Georgia Tech partners, aim to negate repeat surgeries by adapting to growth. Catheter-based innovations extend minimally invasive therapy into younger cohorts. Hybrid designs that layer analytics over mechanical components stand to widen the value proposition, deepening the footprint of the pediatric medical devices market.

Geography Analysis

North America held 43.10% of the pediatric medical devices market in 2025, a position powered by reliable reimbursement and an active regulatory pipeline. The FDA’s breakthrough label for the Minima Stent and the June 2025 green light for the SONU Band show how rapid clearances translate research into bedside tools fda.gov. CMS’s 2025 payment rule further strengthens home-based adoption. Canada benefits from harmonized rules and cross-border device flows, while Mexico’s infrastructure gap leaves headroom for foreign suppliers.

Asia-Pacific is forecast to grow at 7.08% through 2031, outpacing all other regions. China’s 2025-2027 pediatric service drive sets a policy anchor, whereas India’s pediatric segment, equal to 33% of national healthcare spending, should reach USD 33.5 billion by 2026. South Korea’s escalating preterm costs and Japan’s early adoption of catheter therapies create fertile ground for high-end devices. Regional research alliances are harmonizing practice standards and expanding the pediatric medical devices market size for multinational and domestic vendors alike.

Europe leverages EU MDR 2024/1860 to tighten safety while offering transition windows to 2028. Germany, France, and the United Kingdom spearhead R&D programs, whereas Spain and Italy scale pediatric ICUs. Lebanon’s zero-mortality outcome in hybrid palliation of hypoplastic left heart syndrome underscores how clinical excellence can emerge beyond traditional hubs. South America and the Middle East & Africa record slower adoption but draw support from global lenders and multinational donations that gradually grow the pediatric medical devices market.

Competitive Landscape

The pediatric medical devices market shows moderate fragmentation, with the top five suppliers holding an estimated 45-50% combined share. Abbott and Medtronic expand automated insulin delivery partnerships, integrating sensors and pumps for young diabetics. GE HealthCare teams with NVIDIA to embed real-time AI into portable ultrasound, and Cincinnati Children’s Hospital co-creates innovation hubs that trial these tools in situ. Edwards Lifesciences recently purchased Innovalve Medical to lock in mitral-valve IP aimed at small-body implants.

Focused players use specialization to punch above their size. OrthoPediatrics dedicates its entire catalogue to children and bolstered capacity by acquiring Boston Orthotics & Prosthetics. SeaStar Medical works the Humanitarian Device Exemption route to commercialize filtration cartridges for pediatric acute kidney injury. Disruptors such as SoundHealth prove niche breakthroughs can scale once a clear reimbursement path emerges. Supply-chain resilience now factors into bidding, with buyers favoring vendors that meet the EU’s new disruption-reporting rule.

Competition is shifting from pure hardware to solution ecosystems that fuse AI, connectivity, and personalized geometry. Vendors that master rapid regulatory filings and material substitutes for constrained polymers gain pricing leverage and defensive moats in the evolving pediatric medical devices market.

Global Pediatric Medical Devices Industry Leaders

TSE MEDICAL

Hamilton Medical

Fritz Stephan GmbH

GE Healthcare

Ningbo David Medical Device Co. Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: SoundHealth received FDA approval for the SONU Band, the first AI-enabled wearable for moderate-to-severe nasal congestion in children aged 12 and older.

- April 2025: Edwards Lifesciences obtained the CE mark for the Sapien M3 transcatheter mitral valve replacement system aimed at pediatric cohorts.

- February 2025: Children’s National Hospital signed a collaboration agreement with Compremium AG to co-develop non-invasive diagnostic devices for children.

- December 2024: Children’s National Hospital and the FDA’s Office of Science and Engineering Laboratories entered a five-year agreement to design regulatory-science tools that streamline the evaluation of pediatric and perinatal devices.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the pediatric medical devices market as every FDA- or CE-cleared diagnostic, monitoring, life-support, and therapeutic device that is purpose-built or specifically labeled for patients from birth through eighteen years. The basket covers in-vitro diagnostic kits, imaging platforms, cardiology implants, neonatal ICU hardware, plus anesthesia and respiratory care sets, matching the scope presented by Mordor Intelligence.

Scope Exclusion: Adult devices only repurposed for children, single-use disposables, and stand-alone software sit outside this analysis.

Segmentation Overview

- By Product Type

- IVD Devices

- Cardiology Devices

- Anesthesia & Respiratory Care Devices

- Neonatal ICU Devices

- Monitoring Devices

- Diagnostic Imaging Devices

- Others (ENT, Ortho, Mobility Aids)

- By End-User

- Hospitals

- Diagnostic Laboratories

- Pediatric Clinics

- Ambulatory Surgical Centers

- Homecare Settings

- By Care Setting

- Inpatient Care

- Outpatient Care

- Home-based Care

- Emergency & Critical Care

- By Technology

- Conventional Devices

- Wearable & Connected Devices

- AI-Enabled Devices

- 3D-Printed Patient-Specific Devices

- Minimally-Invasive Catheter-Based

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts then interviewed pediatric surgeons, respiratory therapists, and supply managers in North America, Europe, Asia-Pacific, and Latin America, followed by short email surveys with device regulators. These dialogues confirmed utilization rates, average selling prices, and approval timelines where public data ran thin.

Desk Research

We started by extracting yearly clearance logs from the US FDA 510(k) and PMA files, European MDR listings, and Japan PMDA records to map product inflow. UNICEF live-birth tables, WHO pre-term incidence, UN Comtrade trade codes, and hospital bed counts from OECD Health Data helped us chart demand footprints. Patent analytics from Questel signaled innovation pace, while company 10-Ks, child-health association white papers, and paid feeds we license, namely D&B Hoovers and Dow Jones Factiva, refined price corridors. The sources named are illustrative only, and many others informed validation.

Market-Sizing & Forecasting

A top-down addressable population model converts live-birth cohorts, pre-term share, congenital heart surgery counts, asthma prevalence, and NICU admission ratios into unit demand. Results are reconciled with selective bottom-up roll-ups of sampled supplier revenue times regional ASPs. Forecasts blend multivariate regression with scenario analysis so reimbursement shifts, technology diffusion, and currency moves are captured. Three-year moving averages and neighboring country proxies bridge any residual gaps before figures are frozen.

Data Validation & Update Cycle

Outputs pass variance checks against trade statistics and independent hospital purchase audits, after which a senior Mordor reviewer signs off. Reports refresh each year, interim updates follow material events, and a last inspection just before release guarantees clients see the latest view.

Why Mordor's Pediatric Medical Devices Baseline Stays Reliable

Published values often diverge because publishers select different device baskets, apply distinct ASP rules, and refresh at uneven cadences. Our disciplined scope alignment, yearly back-testing, and transparent variable set keep Mordor's numbers balanced and dependable.

Key gap drivers observed elsewhere include the exclusion of monitoring kits, modest treatment of emerging market capital spend, and currency conversions fixed at 2020 rates, all of which suppress their totals.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 43.62 B (2025) | Mordor Intelligence | - |

| USD 28.40 B (2022) | Global Consultancy A | Narrow product list, flat ASP growth |

| USD 17.03 B (2024) | Research Portal B | Omits monitoring devices, small hospital sample |

Together, the comparison shows that Mordor Intelligence delivers a transparent baseline traceable to clear variables and repeatable steps, giving decision-makers confidence to act.

Key Questions Answered in the Report

How big is the Global Pediatric Medical Devices Market?

The Global Pediatric Medical Devices Market size is expected to reach USD 46.11 billion in 2026 and grow at a CAGR of 5.70% to reach USD 60.82 billion by 2031.

Which product segment leads the market?

IVD devices held the top position with 22.40% market share in 2025.

Who are the key players in Global Pediatric Medical Devices Market?

TSE MEDICAL, Hamilton Medical, Fritz Stephan GmbH, GE Healthcare and Ningbo David Medical Device Co. Ltd are the major companies operating in the Global Pediatric Medical Devices Market.

Which is the fastest growing region in Global Pediatric Medical Devices Market?

Asia-Pacific is projected to expand at a 7.08% CAGR through 2031 on the back of demographic growth and targeted healthcare investments.

Which region has the biggest share in Global Pediatric Medical Devices Market?

In 2025, the North America accounts for the largest market share in Global Pediatric Medical Devices Market.

Page last updated on: