Autotransfusion Systems Market Size and Share

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

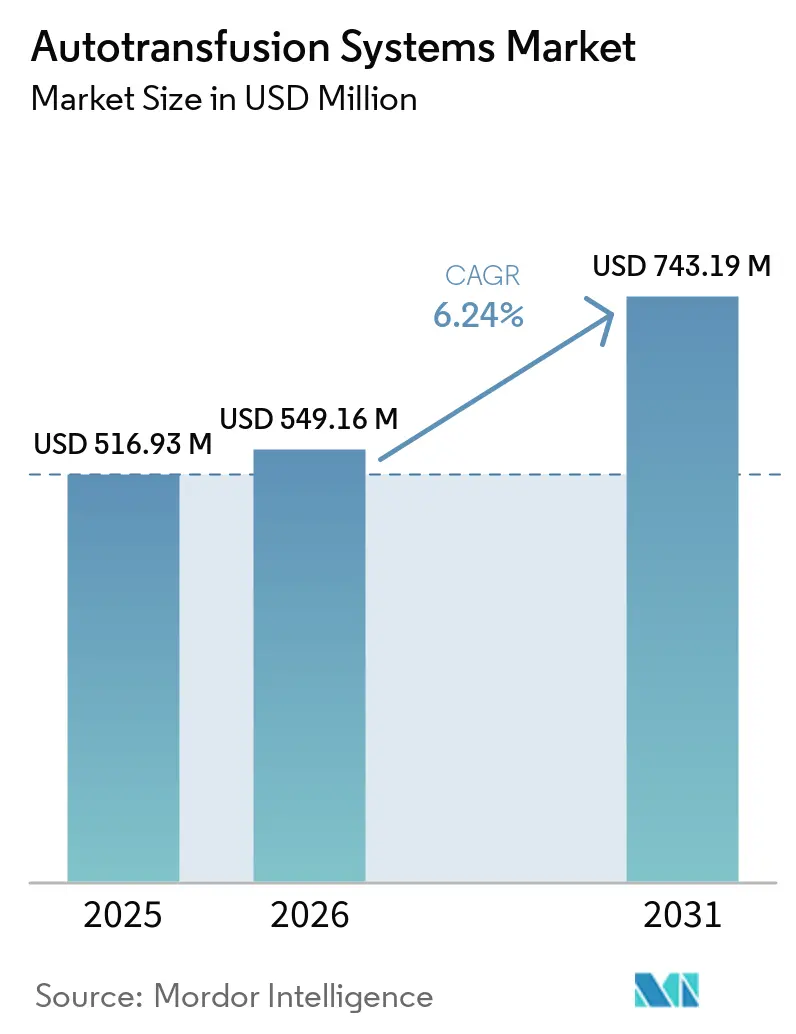

| Market Size (2026) | USD 549.16 Million |

| Market Size (2031) | USD 743.19 Million |

| Growth Rate (2026 - 2031) | 6.24% CAGR |

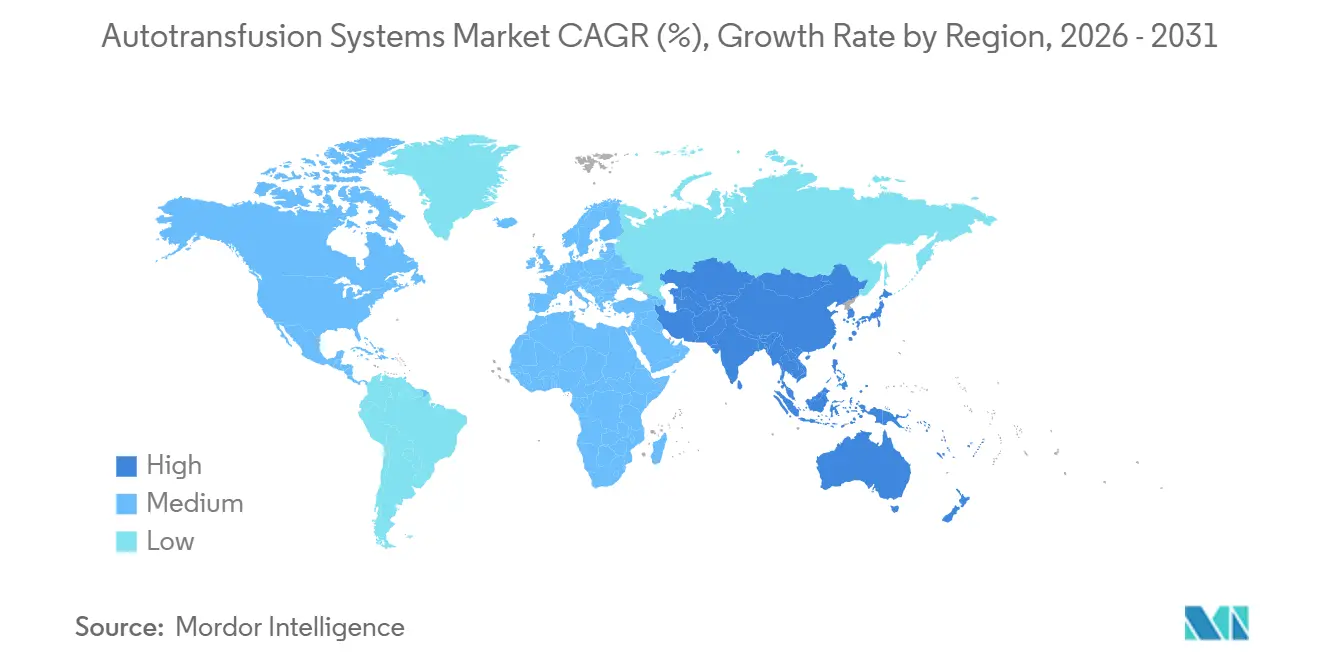

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Autotransfusion Systems Market Analysis by Mordor Intelligence

The Autotransfusion Systems Market size was valued at USD 516.93 million in 2025 and is estimated to grow from USD 549.16 million in 2026 to reach USD 743.19 million by 2031, at a CAGR of 6.24% during the forecast period (2026-2031).

This expansion is underpinned by surging surgical volumes, stricter blood-sparing protocols, and steady innovation in automated cell-salvage systems that cut reliance on donor blood. Hospitals deploy these systems to counter rising allogeneic blood costs, while developers embed artificial-intelligence algorithms that anticipate hemorrhage risk and trigger real-time salvage cycles. Regulatory tailwinds—such as Medicare coverage of patient-blood-management technologies—provide critical reimbursement clarity. Simultaneously, Asia-Pacific investment of USD 225 billion in health infrastructure by 2030 accelerates demand for compact, lower-priced units suited to capacity-strapped facilities. Competitive intensity remains moderate; leading suppliers sharpen their edge through portfolio pruning and targeted R&D, enabling high-margin consumable streams to flourish while new entrants explore 3-D-printed disposables and portable devices for battlefield or disaster deployment.

Key Report Takeaways

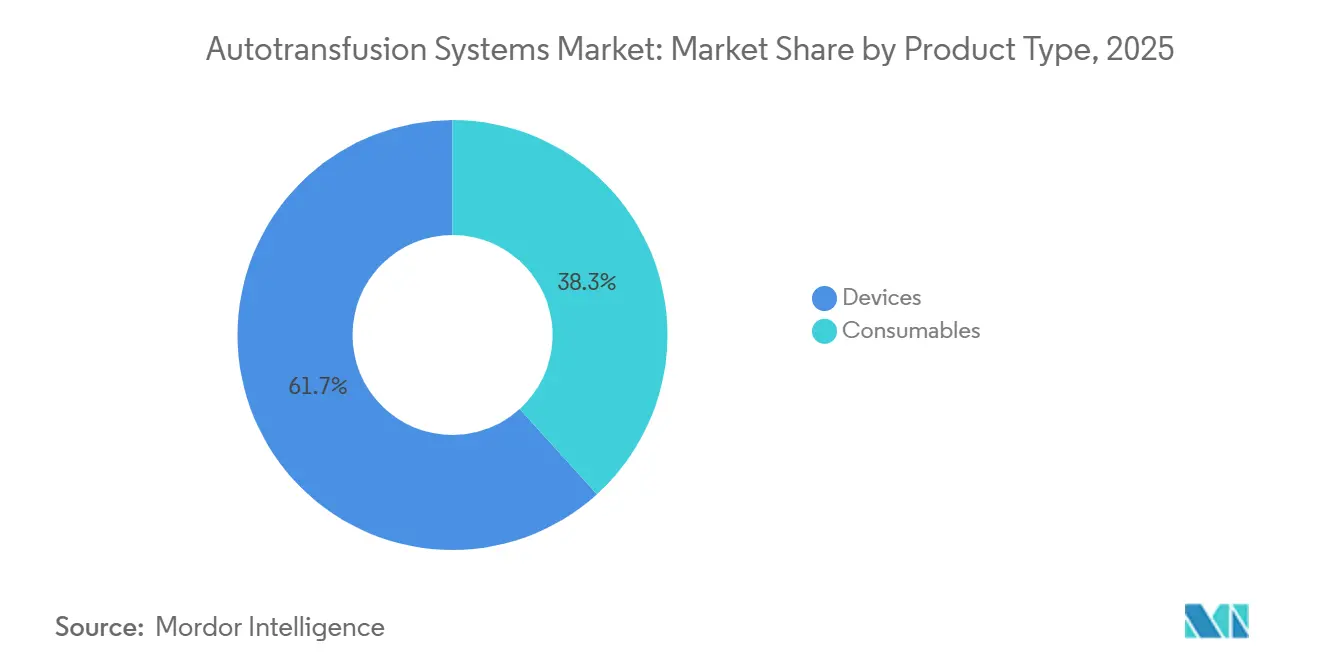

- By product category, devices held 61.72% of the autotransfusion systems market share in 2025, while consumables are projected to post the fastest 7.03% CAGR to 2031.

- By procedure phase, intraoperative applications accounted for 35.42% of the autotransfusion systems market size in 2025, whereas preoperative PAD & ANH are anticipated to grow at 6.79% CAGR through 2031.

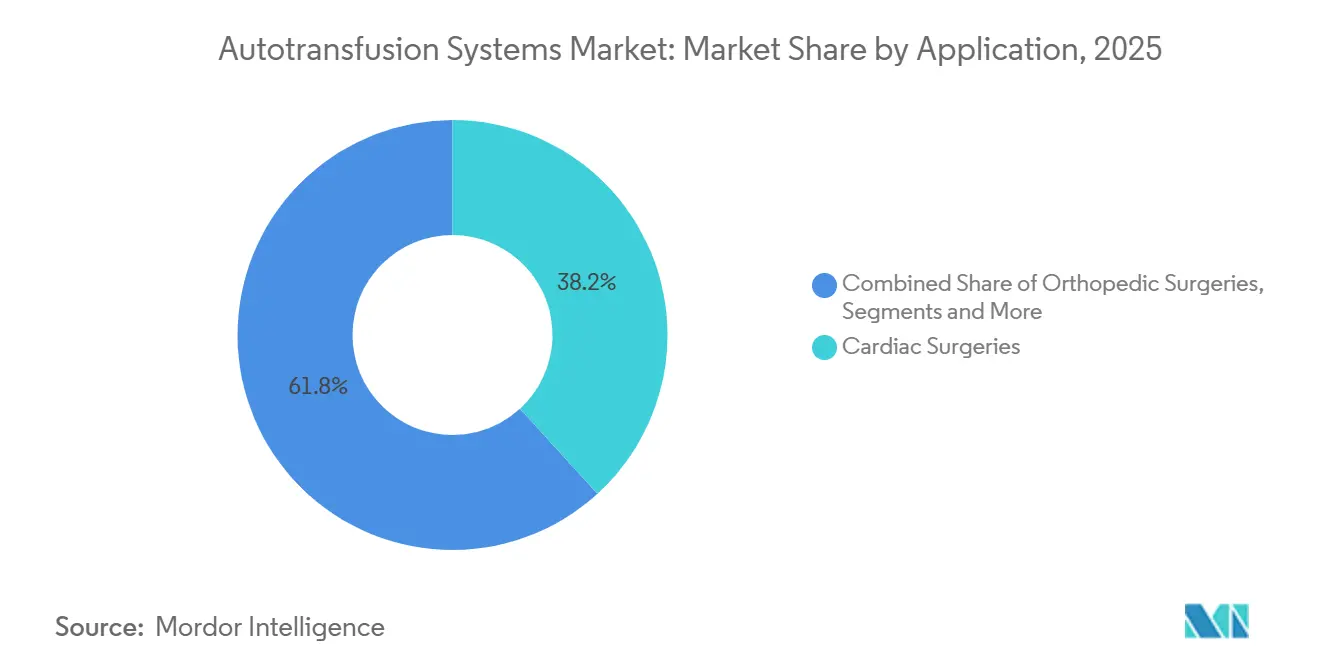

- By application, cardiac surgeries led with 38.21% of the autotransfusion systems market share in 2025 and trauma procedures are forecast to advance at a 7.12% CAGR to 2031.

- By end-user, hospitals retained 67.61% of the autotransfusion systems market share in 2025, while ambulatory surgical centers are positioned for the quickest 7.44% CAGR over the next five years.

- By geography, North America commanded 42.78% of the autotransfusion systems market share in 2025; Asia-Pacific is on track to rise at an 8.53% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Autotransfusion Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising volume & complexity of cardiac and orthopedic surgeries | +1.8% | North America, Europe, APAC | Medium term (2-4 years) |

| Global donor-blood shortfall & stricter transfusion guidelines | +1.5% | Global | Short term (≤ 2 years) |

| Hospital cost-containment pressures | +1.2% | North America, EU, APAC | Medium term (2-4 years) |

| Shift to fully automated, low-volume cell-salvage devices | +0.9% | Developed markets | Long term (≥ 4 years) |

| Additive-manufactured disposables lowering device capex | +0.6% | North America, EU, APAC | Long term (≥ 4 years) |

| Military & disaster-medicine protocols mandating portable kits | +0.3% | Conflict & disaster zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Volume & Complexity of Cardiac and Orthopedic Surgeries

Cardiac and orthopedic procedures grow in complexity, generating sizeable blood-loss volumes that make cell salvage indispensable. Cardiac operating rooms alone created 38.75% of 2024 demand, buoyed by uptake of transcatheter aortic valve replacements and multi-level spinal reconstructions. European trauma guidelines now instruct teams to deploy cell-salvage in severe bleeding, formalizing best practice [1]Journal Critical Care, “European Guideline on Management of Major Bleeding and Coagulopathy,” ccforum.biomedcentral.com. Aging populations amplify case volumes even as donor pools contract. Meta-analysis confirms a 39% cut in allogeneic transfusions when salvage is used across specialties. Consequently, the autotransfusion systems market becomes foundational operating-room infrastructure rather than an elective add-on.

Global Shortfall of Donor Blood and Stricter Transfusion Guidelines

The World Health Organization’s patient-blood-management framework elevates autologous conservation to first-line status, compelling providers to adopt salvage systems as routine rather than contingency. In many African and Asian nations, annual donation deficits exceed 200,000 units, forcing hospitals to conserve every milliliter. Salvaged blood delivers fresher red cells and fewer immune reactions than stored alternatives, a benefit validated in controlled trials. Economically, each avoided unit saves hospitals upward of USD 500 in acquisition and complication costs, and full programs can return USD 1,367 per patient. With reimbursement aligning, the autotransfusion systems market benefits from a rare overlap of clinical, economic, and regulatory imperatives.

Cost-Containment Pressures in Hospitals

Value-based payment models reward institutions that shorten stays and avert transfusion-linked adverse events. Centers running comprehensive blood-management programs have reported USD 2 million in annual savings. Ambulatory surgery centers accentuate the economics: they operate at up to 60% lower cost yet must match inpatient quality, making onsite salvage attractive. Predictive AI modules now alert care teams before massive hemorrhage, enabling proactive salvage and further reducing emergency blood spend. Particularly in emerging economies, managing costs and shortages simultaneously makes the autotransfusion systems market an essential purchase rather than a discretionary upgrade.

Technological Shift to Fully Automated, Low-Volume Cell-Salvage Devices

Next-generation units like Medtronic’s autoLog IQ automatically tune hematocrit and wash cycles without perfusionist intervention, slashing staffing demands. Algorithms also forecast when to initiate salvage in high-risk cases with 81% accuracy. Importantly, compact modules process as little as 100 mL, extending cell-salvage benefits to pediatrics and minimally invasive procedures that previously fell below volume thresholds. Manufacturers embed robotics in production to lower cost and boost consistency, widening access to emerging markets. These advances grow the autotransfusion systems market by unlocking new procedure types and facility tiers.

Additive-Manufactured Disposables Lowering Device Capex

Manufacturers now 3-D-print reservoirs, filters, and tubing, trimming per-unit costs and easing supply-chain bottlenecks—especially vital during crises that disrupt traditional logistics. Hospitals can stock on-demand or contract local printing hubs, reducing warehousing overhead. Lower disposable prices translate to competitive razor-and-blade models, enticing buyers hesitant to invest capital but willing to commit to consumable plans. This innovation enlarges the autotransfusion systems market footprint among budget-conscious facilities, particularly where financing options remain limited.

Restraints Impact Analysis*

| Restraint | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront cost of devices & consumables bundles | -1.4% | Global (acute in emerging markets) | Short term (≤ 2 years) |

| Lack of skilled perfusionists/technicians | -0.8% | APAC, MEA, Latin America | Medium term (2-4 years) |

| Hemolysis risk in hemolytic-anemia & pediatric cohorts | -0.6% | Global | Medium term (2-4 years) |

| Limited evidence & reimbursement in obstetrics/low-resource settings | -0.5% | Emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost of Devices & Consumables Bundles

Turn-key systems range from USD 50,000 to USD 150,000, a steep outlay for budget-constrained clinics. Consumables add USD 200-400 per case, straining margins where reimbursement lags. Leasing and pay-per-use models mitigate sticker shock, yet adoption slows in smaller and public hospitals until such financing scales. Transitional Medicare coverage can offset risk, but global diffusion depends on broader payer alignment[2]Federal Register, “Medicare Program; Transitional Coverage for Emerging Technologies,” federalregister.gov. The paradox remains: the sites that most need autotransfusion, those with severe donor shortages, often lack funds, tempering near-term market acceleration.

Lack of Skilled Perfusionists or Technicians in Emerging Markets

Operating and troubleshooting salvage equipment demands specialized training absent in many fast-growing regions. Certification programs cluster in North America and Europe, leaving gaps elsewhere. Manufacturers sponsor remote learning, yet safe competence still requires hands-on mentorship. Skill shortages stall adoption unless automation progresses to near-push-button simplicity. Partnerships with medical universities and deployment of AI-guided interfaces aim to close the gap, but workforce maturation will take several years.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Technology-Rich Devices Drive Revenue While Consumables Accelerate Growth

Devices contributed 61.72% of 2025 revenue, underscoring hospitals’ reliance on durable capital platforms. Meanwhile, consumables are projected to deliver a 7.03% CAGR, reflecting rising procedure counts and razor-and-blade pricing. The autotransfusion systems market size attributed to devices reached USD 319.07 million in 2025, whereas consumables reached USD 197.86 million. Manufacturers invest in miniaturization and intuitive user interfaces, removing elective hardware features to lower prices without compromising safety. On the consumables side, printable reservoirs and color-coded tubing sets simplify setup and cut waste. Over the forecast horizon, widespread installed bases will create predictable repeat demand that underwrites R&D returns.

Second-order growth stems from the alignment of flexible financing with consumable contracts. Hospital networks increasingly prefer low-commitment device leases that scale to volume, a model that simultaneously locks in consumable supply at negotiated rates. This combination stabilizes revenue and shields providers from one-time capital hits, fueling expansion of the autotransfusion systems market among community hospitals.

By Procedure Phase: Intraoperative Dominance Meets Preoperative Innovation

Intraoperative salvage delivered 35.42% of 2025 revenue, validating its entrenched role during high-blood-loss cases. Yet proactive strategies—preoperative autologous donation and acute normovolemic hemodilution—are climbing at 6.79% CAGR, an indicator that surgical teams aim to curb allogeneic exposure before the first incision. Hospitals that integrate preoperative modules report double-digit declines in transfusion volume and smoother OR workflows. The autotransfusion systems market share for preoperative solutions remains modest but is widening as evidence crystallizes.

Post-operative drainage recovery sees steady uptake in cardiac and joint replacement wards where chest-tube or wound-vac outputs justify the incremental effort. Standardizing salvage across the perioperative continuum maximizes patient blood management, preparing institutions for heightened scrutiny under value-based reimbursement.

By Application: Cardiac Leadership Faces Trauma Surge

Cardiac surgery cemented its leadership with 38.21% contribution in 2025, propelled by continued growth in transcatheter and open-heart procedures. However, trauma care is on the fastest trajectory, expanding 7.12% annually through 2031 as mobile response teams integrate rugged salvage kits and urban trauma centers adopt whole-blood resuscitation protocols. Orthopedics remains a dependable contributor, with bilateral knee and hip replacements plus complex spine cases driving consistent consumable uptake. Obstetric adoption, though nascent, draws momentum from high-risk postpartum hemorrhage evidence that shows safe outcomes in 299 tracked uses.

By End-User: Hospital Dominance Challenged by ASC Growth

Hospitals controlled 67.61% of 2025 revenue, anchored by broad surgical portfolios and cross-department blood-management mandates. The ambulatory surgical-center segment, however, is gaining at 7.44% CAGR, mirroring the outpatient migration of arthroscopy, spine, and cardiovascular procedures. ASC operators value compact platforms that fit limited space and staff profiles. To compete, hospitals partner in joint-venture ASC models, pooling capital and standardizing protocols around shared salvage equipment. The autotransfusion systems market size for ASCs is projected to exceed USD 214.6 million by 2031 as reimbursement parity tightens.

Geography Analysis

North America retained 42.78% revenue share in 2025 thanks to entrenched clinical protocols, Medicare reimbursement, and measured ASC expansion that generated USD 57.6 billion in projected savings over the next decade . U.S. hospitals documented USD 2 million in annual savings from comprehensive patient-blood-management initiatives, justifying continued investment in advanced salvage hardware. Canada exhibits parallel uptake within its publicly funded system as provinces set provincial blood-management targets.

Asia-Pacific is the growth locomotive, with an 8.53% CAGR projected through 2031. China’s maternity hospitals demonstrate successful cell-salvage rollouts that halve allogeneic transfusions. Japan pioneers hemoglobin-vesicle substitutes now in human trials, a potential adjunct to, rather than replacement for, salvage systems by 2030. India, Indonesia, and Vietnam allocate development funds to equip tier-2 cities with modular ORs, creating prospects for entry-level but upgradeable devices.

Europe sustains mid-single digit growth as unified trauma and anesthesiology guidelines cement salvage as standard of care. Re-certification under the EU Medical Device Regulation spurs suppliers to update quality systems, weeding out non-compliant legacy equipment and favoring modern, automation-rich models.

The Middle East & Africa and South America remain under-penetrated but attract humanitarian and development-bank funding aimed at blood-security self-sufficiency. Portable, battery-operated kits gain traction in conflict-affected zones where donor pools are unstable. Over time, skill-building alliances between global manufacturers and local nursing schools will unlock these frontier markets.

Competitive Landscape

The autotransfusion systems market hosts moderately fragmented competition. Haemonetics, LivaNova, and Medtronic anchor the high-end segment with sophisticated automation and predictive-analytics add-ons.

Haemonetics exited lower-margin whole-blood collections for USD 67.8 million, redirecting capital toward apheresis and cell-salvage R&D. Medtronic logged 6.9% cardiovascular growth in Q1 FY25, citing the autoLog IQ as a core contributor. Patent filings trend toward real-time quality sensors and closed-loop wash algorithms, exemplified by Labrador Diagnostics’ bodily-fluid transport patent.

Strategic playbooks revolve around bundling: competitively priced devices paired with locked-in consumable contracts. Additive manufacture of disposables supports regional hubs that reduce logistics overhead and offer custom kits. Emerging challengers position compact, sub-USD 40,000 units targeting ASCs and military buyers. Long-term disruption could stem from artificial blood pursuits; incumbents hedge by partnering with biotech firms to integrate hybrid solutions that mix synthetic and autologous options.

Autotransfusion Systems Industry Leaders

Becton, Dickinson and Company.

Beijing ZKSK Technology Co., Ltd.

Braile Biomédica

Medtronic

Zimmer Biomet

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2024: ProCell Surgical obtained ISO 13485:2016 certification under MDSAP and CE-marked its Sponge Blood Recovery Unit, aligning with EU 2017/745 requirements.

- January 2024: Medtronic showcased its blood-management portfolio, including the autoLog IQ system, at Arab Health 2024.

- June 2023: idsMED Indonesia and LivaNova jointly launched the ATS XTRA autotransfusion system in Jakarta under the banner “Autotransfusion Improves Outcomes”.

Global Autotransfusion Systems Market Report Scope

As per the scope of the report, autotransfusion is an autologous blood transfusion process where the patient receives their own blood after component separation, washing and filtration. The Autotransfusion Systems Market is Segmented by Product Type (Devices and Consumables), Application (Cardiac Surgeries, Orthopedic Surgeries, Organ Transplantation, and Others), End-User (Hospitals, Ambulatory Surgical Centers, and Others), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (in USD million) for the above segments.

| Devices |

| Consumables |

| Intra-operative |

| Post-operative |

| Pre-operative (PAD & ANH) |

| Cardiac Surgeries |

| Orthopedic Surgeries |

| Organ Transplantation |

| Trauma Procedures |

| Others |

| Hospitals |

| Ambulatory Surgical Centers |

| Specialty & Orthopedic Clinics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Devices | |

| Consumables | ||

| By Procedure Phase | Intra-operative | |

| Post-operative | ||

| Pre-operative (PAD & ANH) | ||

| By Application | Cardiac Surgeries | |

| Orthopedic Surgeries | ||

| Organ Transplantation | ||

| Trauma Procedures | ||

| Others | ||

| By End-User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Specialty & Orthopedic Clinics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current Autotransfusion Systems Market size?

The autotransfusion devices market size reaches USD 549.16 million in 2026.

Who are the key players in Autotransfusion Systems Market?

Becton, Dickinson and Company., Beijing ZKSK Technology Co., Ltd., Braile Biomédica, Medtronic and Zimmer Biomet are the major companies operating in the Autotransfusion Systems Market.

Which is the fastest growing region in Autotransfusion Systems Market?

Asia-Pacific is forecast to record an 8.53% CAGR to 2031 as China, India, and Indonesia scale surgical capacity.

Which application area will grow fastest through 2031?

Trauma procedures are expected to post a 7.12% CAGR as portable systems become standard in emergency care.

Page last updated on: