Market Overview

| Study Period | 2020 - 2031 |

|---|---|

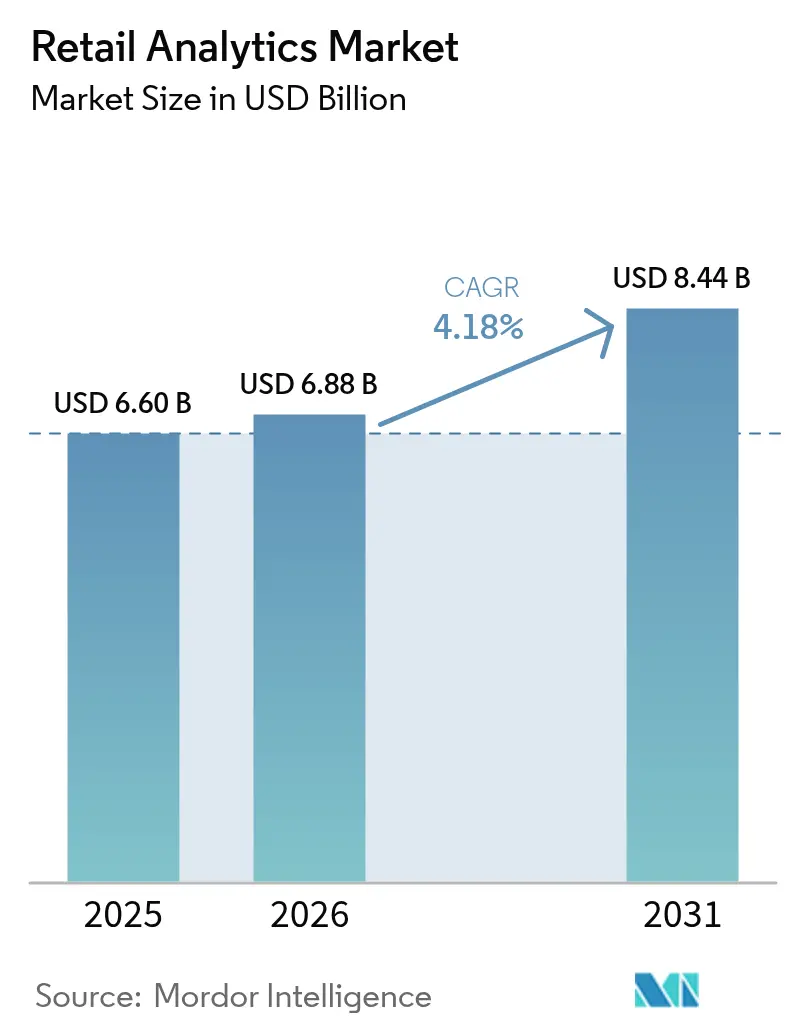

| Market Size (2026) | USD 6.88 Billion |

| Market Size (2031) | USD 8.44 Billion |

| Growth Rate (2026 - 2031) | 4.18% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Retail Analytics Market Analysis by Mordor Intelligence

The retail analytics market size in 2026 is estimated at USD 6.88 billion, growing from 2025 value of USD 6.60 billion with 2031 projections showing USD 8.44 billion, growing at 4.18% CAGR over 2026-2031. Broader omnichannel commerce, surging data volumes, and rapid adoption of AI-driven decision engines are encouraging retailers to embed analytics into day-to-day processes. Cloud delivery models are cutting ownership costs and trimming deployment cycles, which allows mid-tier chains to access capabilities once limited to global leaders. Real-time personalization, prescriptive inventory tools, and advanced promotion optimisation are lifting conversion rates and order profitability even as margins tighten. Competitive advantage is shifting toward platforms that integrate predictive, prescriptive, and generative capabilities, signaling that analytics has moved from a discretionary spend to a fundamental retail requirement. [1]Adobe Staff, “Adobe 2025 AI and Digital Trends Report,” Adobe, adobe.com

Key Report Takeaways

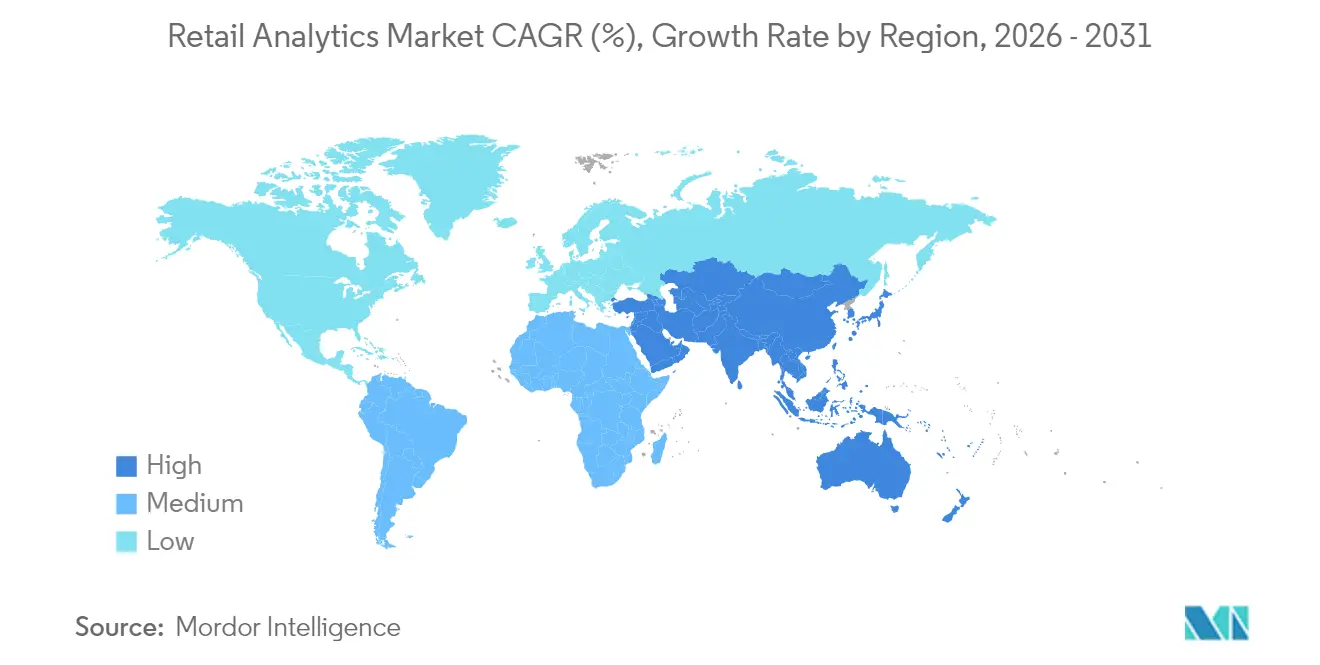

- By geography, North America held 38.05% of revenue in 2025, while Asia-Pacific is forecast to record the fastest expansion at a 6.09% CAGR through 2031.

- By solution, software commanded 72.40% of expenditure in 2025; services represent the quickest growth path with a 7.45% CAGR to 2031.

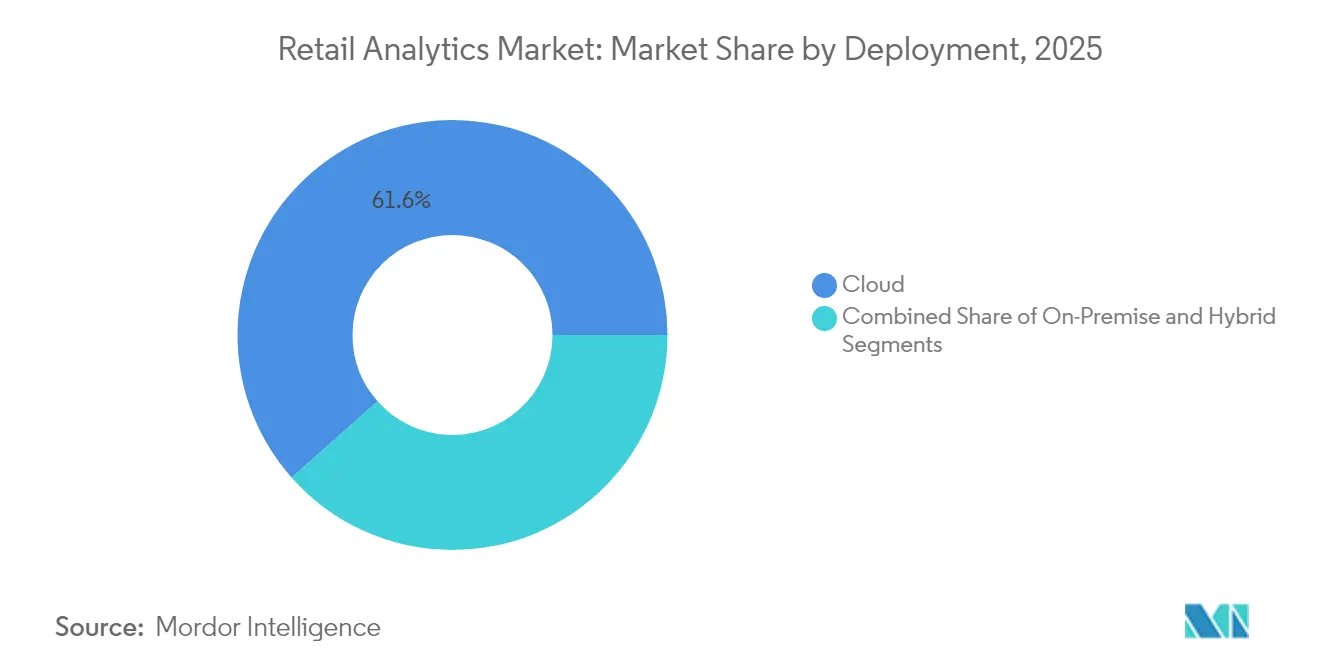

- By deployment, cloud implementations accounted for 61.55% of activity in 2025 and are expected to rise at a 9.22% CAGR over the outlook.

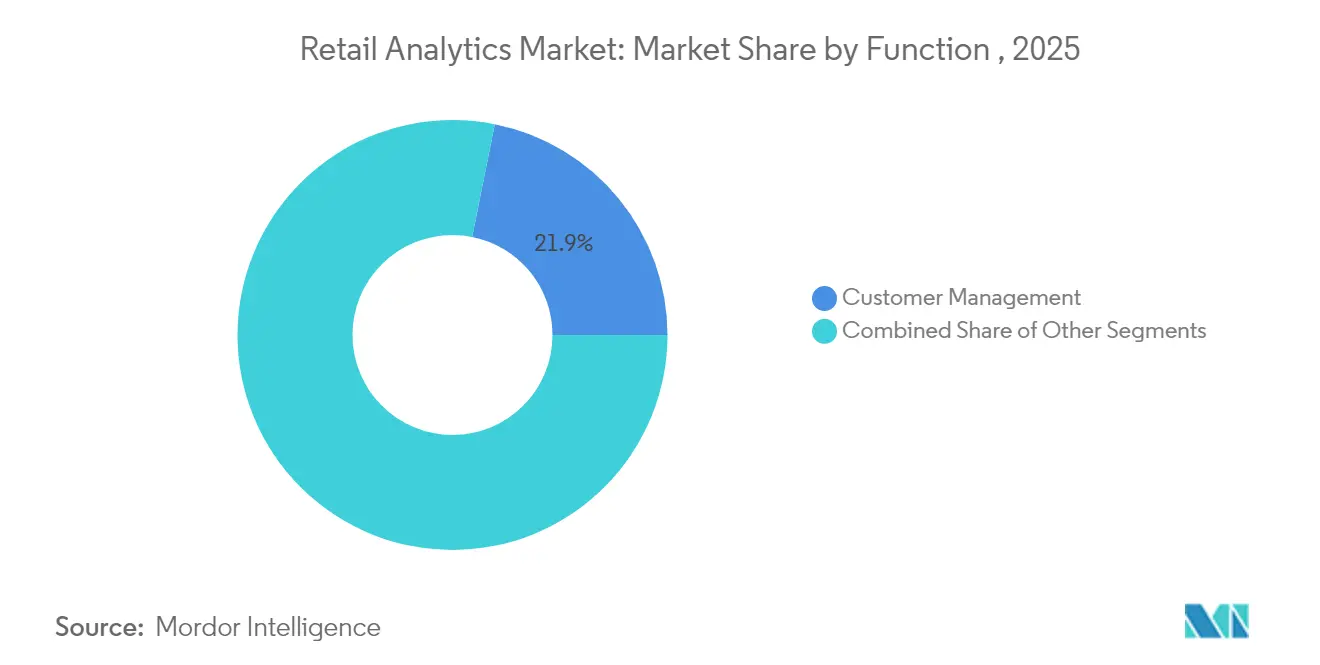

- By function, customer management analytics captured a 21.85% slice in 2025, whereas marketing and merchandising analytics are on course for the sharpest lift at an 7.86% CAGR.

- By retail format, pure-play e-commerce operators led with 59.30% penetration in 2025 and should continue to outpace others at a 8.85% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Retail Analytics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Omnichannel data-volume explosion | +1.2% | Global; highest in North America and Europe | Medium term (2-4 years) |

| AI/ML advances for real-time prescriptive insights | +1.0% | North America, Europe, advanced Asia-Pacific markets | Long term (≥ 4 years) |

| Uptake of cloud analytics lowering ownership costs | +0.9% | Global; early adoption in North America | Short term (≤ 2 years) |

| Demand for hyper-personalised shopping journeys | +0.8% | North America, Europe, urban Asia-Pacific centres | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Omnichannel data-volume explosion

Retailers now ingest vast pools of transaction, behavioural, and social signals that dwarf prior years and mandate scalable analytics platforms. The pace of data growth is prompting investments in unified data lakes that consolidate store, e-commerce, and third-party feeds to support near real-time reporting. Operators that master rapid pattern recognition improve pricing agility, sharpen demand forecasts, and raise inventory turns, which collectively push gross-margin lift. Managing this surge also accelerates cloud demand because elastic infrastructure prevents performance bottlenecks during peak events. Consequently, analytic maturity becomes a barometer for commercial resilience.

AI/ML advances enabling real-time prescriptive insights

Machine-learning-powered demand sensing is reducing supply-chain errors and missed sales opportunities, while computer vision applications extend intelligence to the sales floor. Retailers that embed AI into recommendation engines capture new cross-sell revenue streams and improve lifetime customer value as output moves from descriptive dashboards to automated decisions. Multimodal models that blend language, vision, and structured data produce unified intelligence layers that break down functional silos. These shifts are redefining the talent profiles retailers seek and are reshaping vendor selection criteria, with emphasis now on pre-built, explainable models.

Uptake of cloud analytics lowering TCO

Subscription-based pricing aligns costs with usage and allows seasonal traders to flex capacity without over-investing in under-utilised hardware. Continuous software updates remove the need for disruptive upgrade projects so that retailers can adopt new features such as generative AI faster. Cloud ecosystems improve data-sharing across partners, which supports collaborative forecasting and vendor-managed inventory programs. In addition, built-in security and compliance tooling eases the burden of emerging privacy mandates, which is central for global retailers balancing multiple jurisdictions.

Demand for hyper-personalised shopping journeys

Consumers expect brands to anticipate intent in real time, leading retailers to orchestrate one-to-one experiences across channels. Unified customer profiles fuel marketing, merchandising, and product development decisions that create consistent journeys from discovery through fulfilment. Integrating contextual signals such as location and weather fine-tunes engagement, raising basket size, and reducing churn. Personalisation also guides assortment curation, enabling targeted markdowns that protect margins. The trend reinforces the strategic link between robust customer data architectures and revenue growth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-privacy regulation and compliance costs | -0.7% | Europe, North America; expanding globally | Medium term (2-4 years) |

| Legacy IT stacks and analytics skills gap | -0.6% | Global; heavier in emerging markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Data-privacy regulation and compliance costs

Tightening privacy laws such as GDPR and CCPA compel retailers to re-engineer data pipelines to uphold consent and minimisation rules. Modernisation budgets now allocate growing shares to security tooling that encrypts and governs sensitive information, diverting funds from analytics innovation. Cross-border retailers face complex compliance matrices that elongate deployment cycles for global rollouts. Privacy-by-design frameworks help reduce regulatory exposure but also limit data granularity, which may curb the scope of advanced analytics in high-stringency markets. The interplay between protection mandates and analytics ambitions, therefore, remains a key strategic balancing act. [2]RIB Software, "Top 10 Analytics & Business Intelligence Trends For 2025," RIB Software, December 23, 2024, rib-software.com.

Legacy IT stacks and analytics skills gap

Many longstanding chains operate fragmented point-of-sale, inventory, and loyalty systems that resist seamless data exchange, which delays advanced analytics projects. Integrating modern cloud platforms with on-premises systems often extends timelines and inflates costs. Compounding technical debt is a shortage of personnel who can bridge strategy, data engineering, and data science competencies. Scarce talent raises wage pressure and can slow the rollout of sophisticated use cases such as autonomous pricing or computer-vision-based shelf analytics. Retailers are mitigating risk with low-code tools and managed services, yet the constraint remains a drag on adoption speed.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment: Cloud Gains Momentum While Hybrid Models Mature

Cloud deployments captured 61.55% of projects in 2025 and will grow at a 9.22% CAGR to 2031. Subscription pricing minimises capital commitments, and elastic compute equips retailers to handle promotional peaks without performance dips. Although some chains retain sensitive data on-site to satisfy sovereignty and latency requirements, hybrid architectures that blend local data storage with cloud compute are emerging as a strategic middle ground. These hybrid designs reduce round-trip times for mission-critical workloads such as fraud detection while leveraging cloud economics for analytics model training. As a result, deployment choices increasingly hinge on workload characteristics rather than a blanket cloud-first or on-premises stance.

By Retail Format: E-commerce Players Set the Pace

Pure-play e-commerce retailers captured 59.30% of deployments in 2025 and will continue to outgrow other formats at a 8.85% CAGR. Their digital-native architectures enable rapid adoption of predictive models without legacy integration hurdles, allowing them to refine experiences at every click. Brick-and-mortar operators are bridging the data gap by adding sensors, RFID, and computer vision to convert in-store behaviour into actionable data. Omnichannel chains adopt unified commerce analytics that merge online and store insights to improve cross-channel stock allocation and fulfilment routing. These varied priorities illustrate that business model dictates analytics roadmaps, yet all formats converge on the need for faster, more granular insights.

By Function: Customer Management Leads; Marketing Accelerates

Customer-management analytics held 21.85% of the 2025 total as brands focus on acquisition efficiency, conversion optimisation, and lifetime-value expansion. Unified data platforms feed cross-channel engagement engines that personalise offers and content. Marketing and merchandising analytics are projected to advance at an 7.86% CAGR through 2031, powered by dynamic pricing and AI-driven promotion algorithms that react to real-time demand signals. Inventory and supply-chain-oriented analytics also gain relevance as companies use prescriptive insights to align stock with omnichannel orders. Consequently, decision-support tools are moving beyond siloed departmental deployments toward enterprise-wide intelligence layers that align planning, merchandising, and fulfilment.

By Solution: Software Dominates Despite Services Growth

Software platforms accounted for 72.40% of 2025 spending, underscoring a preference for scalable engines that support multiple retail functions without a linear cost increase. Vendors embed AI modules for customer segmentation, demand forecasting, and price optimisation, which strengthens software’s appeal. The services sub-segment is expanding at a 7.45% CAGR as retailers acknowledge that algorithms alone cannot unlock full value without domain expertise. Managed analytics, implementation consulting, and model-governance support now command a larger slice of project budgets. Retailers adopting outcome-based services report faster time-to-value because partners tailor insights to business objectives rather than generic dashboards.

Geography Analysis

North America led the retail analytics market with 38.05% revenue share in 2025, supported by robust cloud infrastructure, deep e-commerce penetration, and proximity to leading analytics vendors. United States retailers plan to raise technology budgets in 2025, directing the largest allocations to customer-data platforms and AI-based decision engines. Canada trails slightly yet invests heavily in customer analytics to differentiate in a mature market, while Mexico emphasises supply-chain optimisation to address logistics volatility.

Asia-Pacific is set to post the fastest CAGR at 6.09% through 2031, propelled by explosive e-commerce growth, increasing smartphone adoption, and ambitious digital transformation programs. China pioneers social-commerce analytics that integrate payment, delivery, and community engagement data, producing end-to-end insight loops. India’s diverse consumer landscape encourages retailers to deploy predictive models that tailor assortments across urban and rural zones. Japan and South Korea emphasise store-centric analytics such as computer-vision footfall measurement to revitalise physical outlets. Europe retains a meaningful footprint anchored by sophisticated retail systems in the United Kingdom, Germany, and France. Stringent privacy rules drive adoption of hybrid deployments that balance data residency with cloud scalability. Sustainability analytics is gaining traction as retailers use environmental metrics to guide sourcing and packaging decisions. Latin American growth concentrates in Brazil and Argentina, where analytics helps manage currency volatility and optimise localised promotions. Middle East and Africa remain smaller but active in markets such as Israel and the United Arab Emirates, where luxury retail and tourism accelerate the adoption of customer experience analytics.

Regulatory Landscape

Retail analytics deployments operate under tightening data-protection regimes that affect what customer, loyalty, location, and behavioral data can be collected and how it can be used for personalization and measurement. In the European Union, GDPR continues to set the baseline for consent, purpose limitation, and data minimization. Cross-border transfers rely on mechanisms such as Standard Contractual Clauses (SCCs) and related transfer impact assessments, or the EU-US Data Privacy Framework where applicable, and regulator activity such as European Data Protection Board guidance (July 2026 guidelines on anonymisation) reinforces the need for defensible anonymisation and privacy-by-design controls in analytics stacks.

Beyond privacy, cross-border commerce rules also affect retail analytics data models through changes to landed-cost and taxation assumptions that feed pricing, promotion, and demand planning. For example, changes to the United States de minimis treatment for Chinese-origin goods, highlighted in 2026 tariff coverage, and ongoing EU VAT enforcement via the One-Stop Shop (OSS) regime increase the need for accurate duty, tax, and shipment-level attribution within retail decision systems, pushing retailers toward analytics solutions that can operationalize compliance signals alongside commercial KPIs.

Value Chain Analysis

The retail analytics value chain starts with multi-source data generation and ingestion across point-of-sale (POS), e-commerce clickstream, loyalty and CRM, inventory and order management, and growing in-store sensor streams (cameras, electronic shelf labels, RFID). The data is then unified through integration and identity resolution layers, followed by modeling and governance in cloud and hybrid data platforms before being applied through function-specific applications. These include customer management analytics, marketing and merchandising analytics (pricing and yield), store operations analytics, and supply chain analytics. Service partners and managed analytics teams remain critical for implementation, model governance, and change management, particularly for retailers dealing with fragmented legacy systems and analytics skills gaps.

Downstream, activation and measurement increasingly connect analytics to monetization and operational execution, including retail media and closed-loop attribution that ties audience activation to purchase outcomes. Recent ecosystem moves reflect this convergence, with dunnhumby partnerships with Synerise (February 2025) and Bridg (May 2025) focused on real-time behavioral prediction and identity resolution for personalization and retail media activation. NielsenIQ alliances such as VusionGroup (May 2025) and a multi-year data sharing agreement with Sephora (June 2025) also point to linkage between shelf and POS data with AI-driven optimization. Separately, Crisp acquisitions of Atheon Analytics and ClearBox Analytics (April 2025) reinforce ongoing consolidation around SKU-level visibility and supply chain performance analytics.

Competitive Landscape

The retail analytics market shows moderate concentration. Enterprise software providers such as SAP, IBM, Oracle, and Microsoft leverage entrenched ERP and cloud relationships to cross-sell analytics modules that span planning, merchandising, and fulfilment. Retail-specialist vendors, including Blue Yonder, RetailNext, and Dunnhumby, compete with deeper functional playbooks that address pricing, shelf optimisation, and customer journey mapping. Cloud hyperscalers Amazon Web Services and Google package native BI tools with their infrastructure, raising price-performance pressure on independent platforms.

Competitive strategies show a split between all-in-one suites and best-of-breed components. Large chains favour integrated platforms to reduce vendor complexity, while mid-size retailers adopt modular tools for rapid returns. AI infusion is now a baseline expectation. Vendors embed natural-language querying, automated anomaly detection, and scenario modelling that convert raw data into recommended actions, supporting labour productivity gains across merchandising and marketing. Start-ups that specialise in unified commerce analytics, real-time store monitoring, or assortment localisation are securing footholds by addressing pain points left open by broader suites. Consolidation is likely as incumbents acquire niche players to fill capability gaps.

Regulatory compliance and data sovereignty add a layer of differentiation, as vendors that offer pre-configured privacy controls appeal to European and multinational chains. Open platform architectures that integrate first-party data with third-party feeds are also valued because they permit retailers to extend analytics models without extensive coding. These trends collectively indicate that vendor selection hinges not only on technical features but also on the ability to deliver rapid, measurable business outcomes.

Retail Analytics Industry Leaders

-

SAP SE

-

IBM Corp.

-

Oracle Corp.

-

Salesforce (Tableau)

-

SAS Institute

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A key whitespace is the shift from descriptive reporting to decision automation across merchandising, supply chain, and store operations. Retailers are looking for agentic workflows that translate multi-source data into actions such as replenishment, allocation, price and promotion changes, and fulfillment-risk interventions. Product moves in 2026 support this direction, including Impact Analytics launching CortexEye (March 2026) to aggregate POS, inventory, ERP, and external signals using agentic AI, and SAP introducing AI-enhanced retail innovations tied to its data foundation at NRF 2026 (January 2026), reflecting demand for integrated data and embedded decision support rather than stand-alone dashboards.

Store-intelligence and retail media intelligence also offer near-term expansion as retailers connect physical-world signals and advertising ROI back to core merchandising. Standard AI acquiring Pathr.ai (January 2026) supports spatial intelligence and computer vision coverage for in-store analytics use cases, while SymphonyAI launching CINDE Retail Media Intelligence (June 2026) connects merchandising and media metrics for grocers seeking closed-loop measurement. Alongside this, measurement providers are expanding omnichannel and regional datasets, including NIQ completing the acquisition of Flywheel’s China and Southeast Asia e-commerce data and insights business (July 2026) and launching Precision Solutions in the US (April 2026). These steps open further opportunities for retail analytics platforms that can normalize third-party commerce data and localize insights while maintaining privacy and data-residency controls.

Recent Industry Developments

- July 2026: IBM announced an agreement to deploy retail analytics across more than 8,100 Walgreens locations to support field service efficiency. The scale of rollout shows analytics being operationalized beyond corporate BI, with store-level execution and uptime becoming core value drivers for enterprise deployments.

- March 2025: SAP launched SAP S/4HANA Cloud Public Edition for retail, fashion, and vertical business. By standardizing retail data and processes in cloud ERP, the release strengthens the data foundation needed for faster rollouts of embedded analytics across merchandising, fulfillment, and finance.

- January 2024: IBM and SAP announced a collaboration to develop generative AI solutions for consumer packaged goods and retail industries using IBM watsonx and SAP Business Technology Platform. The partnership highlighted the strategic direction to combine enterprise data platforms with AI tooling to accelerate retail-specific analytics and automation use cases.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the retail analytics market is defined as the revenue earned from software and related services that help retailers collect, unify, and analyze retail data to improve decisions across stores and digital channels.

Scope exclusions: We exclude custom in-house analytics builds and broad enterprise data platforms that are not packaged and sold as retail analytics solutions.

Segmentation Overview

-

By Solution

- Software

- Services

-

By Deployment Model

- Cloud

- On-premise

- Hybrid

-

By Function

- Customer Management

- In-store Operation - Inventory Management

- In-store Operation - Performance Management

- Supply Chain Management

- Marketing and Merchandising - Pricing/Yield

- Other Functions - Transportation Management

- Other Functions - Order Management

-

By Retail Format

- Brick-and-Mortar Stores

- Pure-play E-commerce

- Omnichannel Retailers

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

Europe

- United Kingdom

- Germany

- France

- Italy

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

-

Middle East

- Israel

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

-

Africa

- South Africa

- Egypt

- Rest of Africa

-

South America

- Brazil

- Argentina

- Rest of South America

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to establish the fact base and avoid building the model on assumptions alone. We reviewed public statistics and reference documents that can anchor demand signals, including US Census Bureau retail sales releases, US Bureau of Labor Statistics price and employment series, Eurostat retail trade indicators, OECD digital economy publications, and World Bank macroeconomic data.

To translate these signals into a market model, we also used materials that describe how retailers budget and deploy analytics, such as annual reports and investor presentations from listed retailers and solution providers, product documentation, earnings call transcripts, and updates from retail and data science associations. For company-level cross-checks where disclosures were limited, we referenced a paid subscription for company financials and a separate news and financials database. These desk sources are illustrative only, and we consulted additional public references to collect, validate, and clarify inputs.

Primary Interviews and Surveys

Primary work was used to convert the desk fact base into realistic adoption and pricing assumptions. We spoke with retail decision makers, IT and data leaders, analytics managers, and implementation partners across major regions, so gaps around deployment mix, typical contract sizing, and usage intensity could be closed and then stress-tested.

Interview questions were also used to clarify what is counted as retail analytics versus adjacent tooling, and to confirm how quickly cloud migration, omnichannel programs, and data governance requirements are changing buying patterns.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 16% | APAC: 52% |

| Mid tier: 40% | Functional/Unit leaders: 37% | EMEA: 29% |

| Smaller Players: 21% | Managers: 47% | Americas: 19% |

Market-Sizing & Forecasting

Sizing starts with a top-down demand reconstruction where retail IT and digital spend signals are filtered through analytics spending share, then adjusted using primary inputs on adoption by retailer size and channel maturity. Once that demand pool is built, we apply selective bottom-up checks using supplier revenue disclosures, sampled contract values, and typical user or store counts multiplied by observed pricing ranges, which helps correct for under-reporting in any one data series.

Key inputs that are tracked include the split of cloud versus on-premise deployments, the share of retailers running omnichannel programs, the number of stores and online order volumes as a proxy for data intensity, the maturity of loyalty and customer data programs, and the implementation and managed-service mix that changes total contract value. Where bottom-up signals are missing for smaller geographies, we apply ratio-based allocation using retail sales scale and digital penetration indicators, then confirm reasonableness through follow-up expert calls.

For forecasting, we use scenario analysis supported by regression-style sensitivity checks on drivers like retail sales growth, e-commerce share, and cloud adoption, and then we align the final curve with what practitioners expect for budget cycles and rollout timelines. The outputs are kept repeatable, so the same variable set can be updated quickly when new public data is released.

Data Validation & Update Cycle

Validation is done through triangulation across independent signals, followed by variance checks at the region and component level so the totals do not hide inconsistencies. When an output looks unusual, we trace it back to a small set of drivers, such as pricing, adoption, or deployment mix, and then recheck assumptions through targeted re-contacts with industry participants.

Before sign-off, the model and narrative go through multi-step analyst reviews to confirm that definitions are applied consistently and that unit economics match how contracts are bought in practice. Reports are refreshed annually, and interim updates are made when material events occur, including major regulatory shifts, step changes in retailer tech spending, or large platform changes. Right before delivery, a final pass is completed so clients receive the latest view using the newest available public indicators.

Mordor Intelligence's Retail Analytics Market Size Measured Against Other Published Estimates

Published retail analytics market numbers often differ, even when they appear to cover the same topic, because the counted revenue items and the timing of the base year are not always aligned. Differences also come from how firms treat services, cloud subscription recognition, and whether their models are tied back to retailer demand signals or mostly built from supplier narratives.

Custom in-house analytics builds sit outside Mordor Intelligence's scope, which narrows the model to packaged retail analytics software and related services that are sold or subscribed, and then validates the approach using retailer-side adoption and budget checks. Other estimates can expand the total by folding in broader data platforms, more aggressive cloud ramp assumptions, or by using different currency timing and refresh cycles, which can move the starting value up or down before forecasting begins.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 6.88 B (2026) | |

| Global Consultancy A | USD 10.20 B (2025) | Uses an earlier base year and a wider functional umbrella that can capture adjacent enterprise analytics and platform spending, which lifts the counted revenue pool compared with a packaged retail analytics-only view. |

| Industry Research Group B | USD 9.10 B (2024) | Anchors the estimate in a different year and can apply faster assumed adoption and service attach rates, which increases totals without the same level of retailer budget and deployment-mix validation. |

The spread in the table is mainly explained by what gets counted and the year used for the starting point, followed by how fast cloud and services are assumed to scale. By keeping inputs tied to observable retailer demand signals and then cross-checking with supplier disclosures, the final number remains easy to trace and update when the same drivers move.

Key Questions Answered in the Report

How big is the Retail Analytics Market?

The Retail Analytics Market size is expected to reach USD 6.88 billion in 2026 and grow at a CAGR of 4.18% to reach USD 8.44 billion by 2031.

Who are the key players in Retail Analytics Market?

IBM Corporation, Oracle Corporation, SAP SE, SAS Institute Inc. and Salesforce.com Inc. (Tableau Software Inc.) are the major companies operating in the Retail Analytics Market.

Which is the fastest growing region in Retail Analytics Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which region has the biggest share in Retail Analytics Market?

In 2026, the North America accounts for the largest market share in Retail Analytics Market.

What years does this Retail Analytics Market cover, and what was the market size in 2025?

In 2025, the Retail Analytics Market size was estimated at USD 6.88 billion. The report covers the Retail Analytics Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Retail Analytics Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

What is the fastest-growing functional segment within retail analytics?

Marketing and merchandising analytics is forecast to increase at an 7.86% CAGR through 2031.

Which retail format invests most heavily in analytics?

Pure-play e-commerce retailers hold 59.30% of usage and are converting data advantages into a 8.85% growth pace through 2031

Page last updated on: