Passenger Service System Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 14.01 Billion |

| Market Size (2031) | USD 30.46 Billion |

| Growth Rate (2026 - 2031) | 16.83% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Passenger Service System Market Analysis by Mordor Intelligence

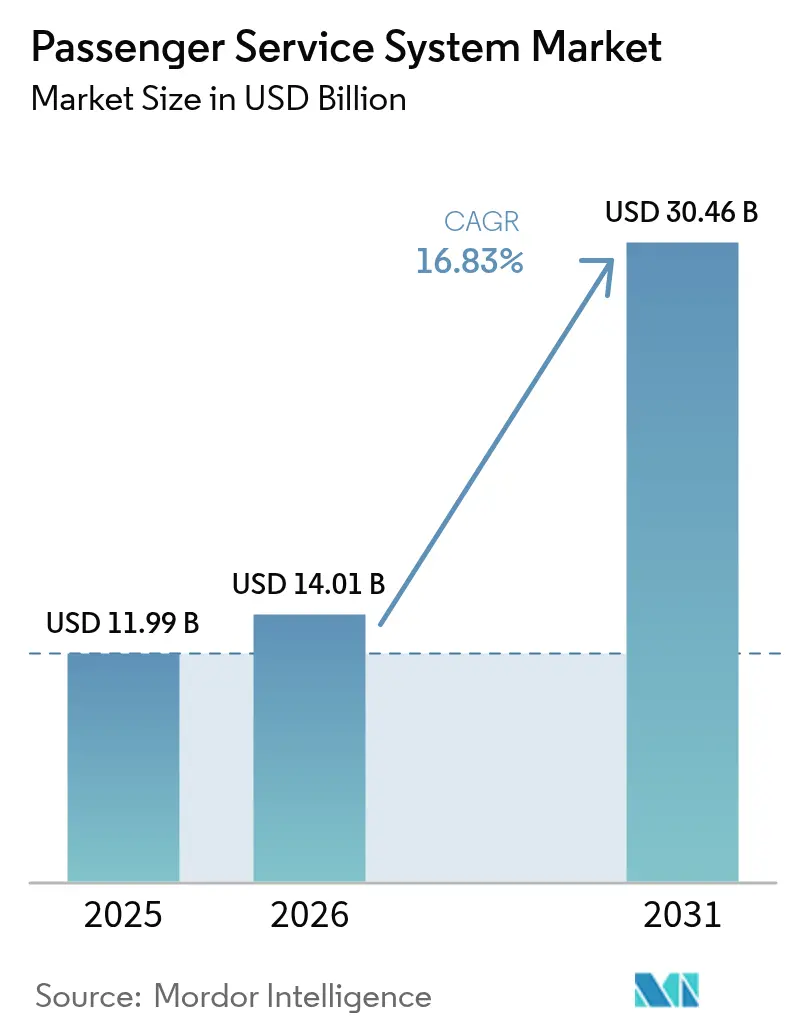

The Passenger Service System market size was valued at USD 11.99 billion in 2025 and estimated to grow from USD 14.01 billion in 2026 to reach USD 30.46 billion by 2031, at a CAGR of 16.83% during the forecast period (2026-2031). This vigorous expansion reflects airlines’ accelerated shift toward cloud-native architectures, AI-driven retailing and offer-and-order management platforms. Airlines are routing part of the USD 37 billion technology budget released in 2024 toward next-generation Passenger Service System market upgrades that cut legacy infrastructure outlays and unlock dynamic revenue streams. Full-service carriers rely on large-scale migrations to modernize mainframe-bound applications, while low-cost carriers spearhead agile roll-outs that shorten time-to-market for new ancillary products. Regionally, North American incumbents continue to lead standardization around IATA ONE Order, yet Asia-Pacific airlines supply the strongest volume uplift and the highest rate of new system adoptions. Competitive intensity rises as cloud-born specialists integrate modular APIs into existing Passenger Service System market deployments, pushing traditional vendors to invest heavily in R&D and strategic partnerships with hyperscale providers.

Key Report Takeaways

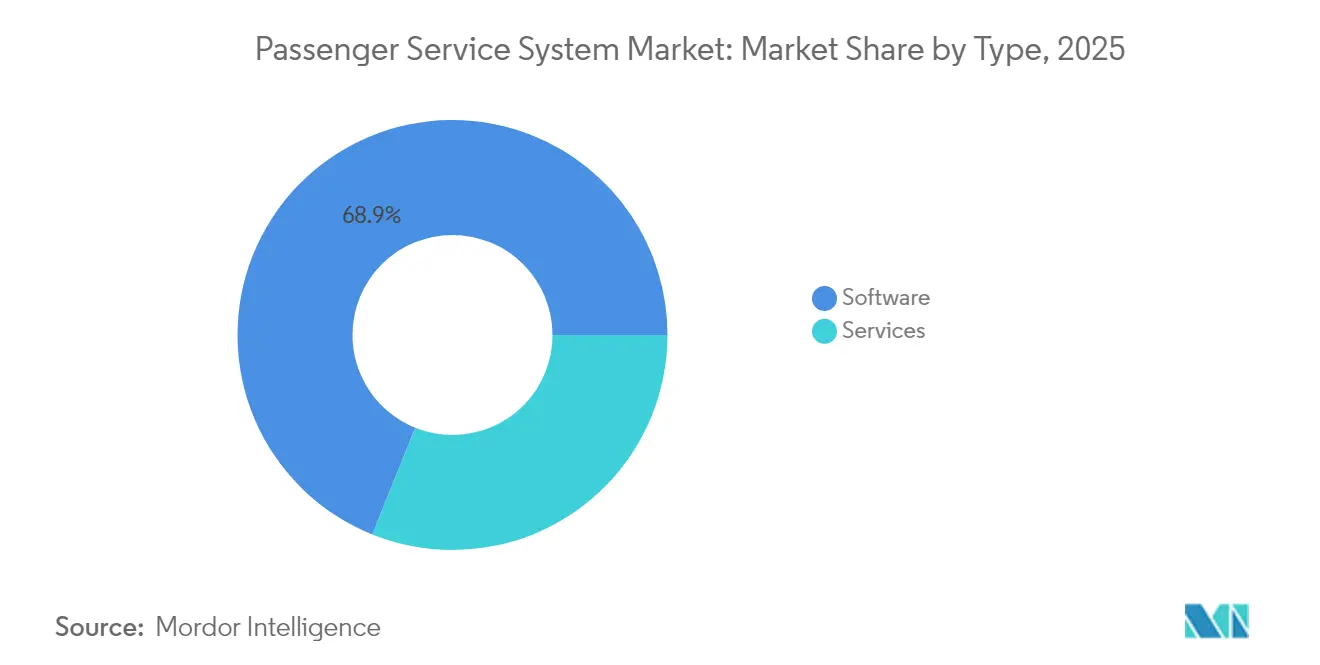

- By type, software held 68.92% of Passenger Service System market share in 2025 while services are projected to grow at an 17.98% CAGR to 2031.

- By deployment, cloud models accounted for 52.88% of the Passenger Service System market size in 2025 and are set to expand at an 18.35% CAGR through 2031.

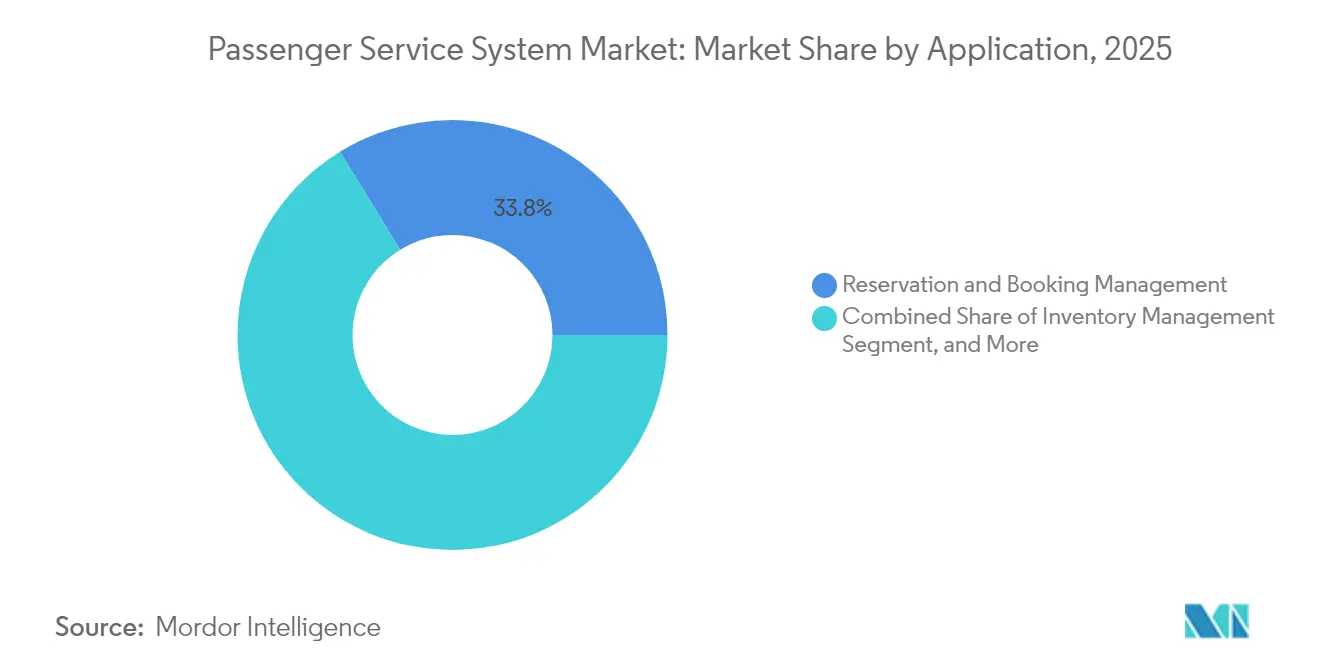

- By application, reservation and booking management captured 33.76% of Passenger Service System market share in 2025; loyalty management is forecast to rise at an 17.71% CAGR over the same period.

- By airline type, full-service carriers dominated with 39.88% revenue share in 2025, whereas low-cost carriers are advancing at a 19.42% CAGR to 2031.

- By geography, North America commanded 33.15% of 2025 revenue, but Asia-Pacific is growing the fastest at a 18.97% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Passenger Service System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise in air-travel passengers | +4.2% | Global – Asia-Pacific leads | Medium term (2-4 years) |

| Rapid cloud adoption across airline IT stacks | +3.8% | North America and EU, Asia-Pacific catching up | Short term (≤ 2 years) |

| Growing appetite for ancillary-revenue merchandising | +3.1% | Global – led by LCCs | Medium term (2-4 years) |

| Mandates for seamless omni-channel passenger experience | +2.7% | EU spearheads, worldwide uptake | Long term (≥ 4 years) |

| IATA ONE Order accelerating end-to-end PSS upgrades | +2.4% | Global – early adopters in Middle East | Long term (≥ 4 years) |

| Airport CUTE/CUPPS sunset pushing modern PSS APIs | +1.0% | Asia-Pacific airports | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rise in Air-Travel Passengers

Global passenger numbers are projected to reach 5.2 billion in 2025, placing unprecedented load on legacy reservation architectures. United Airlines’ migration from 50-year-old mainframes to an Amazon Bedrock-enabled stack shows how carriers now translate complex passenger name records into plain-language objects that scale elastically [1]Amazon Web Services, “United Airlines Uses Amazon Bedrock to Modernize Legacy Systems,” aws.amazon.com. Asia-Pacific airports such as Bangkok’s Suvarnabhumi and Phuket are targeting over 130 million passengers, prompting USD 18 billion in PSS-aligned infrastructure programs. Larger trip volumes multiply transaction requests, forcing airlines to adopt cloud-native Passenger Service System market deployments capable of real-time inventory orchestration and dynamic pricing.

Rapid Cloud Adoption Across Airline IT Stacks

Ninety-five percent of airlines list cloud migration as a top CIO priority, citing 40% cuts in total cost of ownership and faster release cycles once mainframe dependencies disappear. Sabre completed retirement of its proprietary mainframe in favor of Google Cloud, removing USD 100 million in annual operational costs while unlocking micro-services for personalized offers Delta Air Lines’ AWS partnership equips its revenue-management algorithms with on-demand compute power for seat-level pricing decisions. Together, these moves confirm that airlines embracing cloud-native Passenger Service System market frameworks gain measurable agility and margin upside.

Growing Appetite for Ancillary-Revenue Merchandising

Ancillary revenue topped USD 118 billion in 2024. Carriers such as Ryanair generate more than 30% of total income from paid add-ons, necessitating Passenger Service System market upgrades to support AI-powered bundling and real-time upselling. AirBaltic recorded a 6% rise in seat revenue after implementing machine-learning-driven dynamic ancillary pricing. Virgin Atlantic subsequently selected FLYR’s revenue operating system to extend personalized offers across mobile, kiosk and agent channels [2]FLYR, “Virgin Atlantic Selects FLYR for Ancillary Optimization,” flyr.com. Modern PSS modules now integrate recommendation engines and granular customer segmentation, allowing airlines to fine-tune margins on luggage, seats and priority services without disrupting the core booking flow.

IATA ONE Order Accelerating End-to-End PSS Upgrades

ONE Order replaces fragmented PNR-based processes with single-record orders, simplifying settlement, servicing and analytics. Riyadh Air is launching operations directly on SabreMosaic, avoiding legacy complexity and achieving traveler-centric retailing from day one. British Airways is rolling out Amadeus Nevio to convert flight-centric workflows into modular offers linked to unified order management. Early adopters report shorter servicing times, cleaner revenue accounting and lower middleware costs, pushing many network carriers toward comprehensive Passenger Service System market realignments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront licence and migration costs | -2.1% | Global – smaller carriers hardest hit | Medium term (2-4 years) |

| Legacy mainframe lock-in among Tier-1 carriers | -1.8% | North America and EU | Long term (≥ 4 years) |

| Growing data-sovereignty rules | -1.3% | China, EU GDPR zones | Medium term (2-4 years) |

| Talent shortage in NDC integration | -0.9% | Global STEM shortfall | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Licence and Migration Costs

Comprehensive PSS modernization can exceed USD 100 million for a major carrier, discouraging many regionals from abandoning legacy contracts. Airlines often phase migrations over 3–5 years to contain cash-flow shocks, yet still face dual-run expenses during cut-over periods. Smaller operators struggle to negotiate favorable terms with dominant vendors, perpetuating vendor lock-in across the Passenger Service System market. Cloud OPEX models offset some capital burden, but licence fees for sophisticated offer-and-order modules remain a hurdle until transaction volumes scale sufficiently.

Legacy Mainframe Lock-in Among Tier-1 Carriers

Large carriers rely on codebases written in COBOL and TPF during the 1960s, with 30% of their support engineers expected to retire within this decade. Re-platforming carries operational risk: downtime can strand millions of passengers and cost carriers USD multi-million in penalties. Consequently, some airlines postpone upgrades, ceding agility to newer rivals that deploy cloud-first Passenger Service System market solutions. Market momentum still favors modernization, but mainframe lock-in slows the overall adoption curve and suppresses short-term ROI for digital initiatives.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Services Unlock Rapid Modernization

Passenger Service System market size figures underline software’s 68.92% revenue contribution in 2025. Airlines continue renewing core licences for platforms such as Amadeus Altéa and SabreSonic, yet they increasingly bundle consulting and migration assistance in multi-year service engagements. The services segment’s 17.98% CAGR stems from carriers demanding cloud architecture design, NDC schema mapping and AI model training beyond mere implementation. Tier-one carriers now structure partnerships that combine shared code-bases with DevOps squads from suppliers, transferring knowledge that accelerates feature releases.

The changing procurement mix highlights a pivot to outcome-based contracts measurable by ancillary revenue uplift or downtime reduction. Vendors respond by packaging managed services with uptime SLAs and continuous optimization cycles. As a result, software revenues grow steadily, but service-driven differentiation sets the competitive tempo. Airlines that secure high-quality integration support compress migration timelines and unlock early mover gains in dynamic retailing—advantages that ripple through the wider Passenger Service System market.

By Deployment: Cloud Models Dominate New Contracts

Cloud deployments claimed 52.88% of the Passenger Service System market share in 2025 and they lead with an 18.35% CAGR. Carriers prefer OPEX-aligned subscription models that scale with ticket volumes and sidestep capital-heavy data-center upgrades. Sabre’s strategic partnership with Google Cloud allows airlines to plug into natural-language AI APIs without provisioning on-prem infrastructure. United Airlines reports sub-second response times for complex itinerary searches after refactoring its shopping engine on AWS, demonstrating operational upside accessible only via hyperscale resources.

On-premise installations persist mainly among transatlantic legacy carriers bound by historical investments and strict data-residency rules. Even here, hybrid deployments emerge: transactional cores stay local for latency, while forecasting and personalization run in the cloud. The growing proportion of cloud contracts signals that future Passenger Service System market upgrades will default to micro-service architectures, allowing airlines to activate new modules—loyalty, disruption management, sustainability reporting—through simple API toggles rather than extensive code rewrites.

By Application: Loyalty Management Accelerates Revenue Diversification

Reservation and booking management accounted for 33.76% of 2025 revenue, yet loyalty systems register the fastest 17.71% CAGR as airlines pivot from transactional fares toward relationship-driven monetization. Philippine Airlines adopted Amadeus Loyalty Management to deliver targeted offers that extend beyond flights into hotels, ground transport and financial partnerships. Full integration enables redemption and accrual in real time, elevating customer lifetime value and strengthening direct-channel sales.

Check-in, boarding and inventory applications mature incrementally, incorporating biometrics and AI allocation algorithms. Emerging modules track sustainable aviation fuel consumption to meet ESG reporting obligations. Within this diversified suite, loyalty management is positioned to command a larger slice of the Passenger Service System market size as carriers mine granular behavioral data for hyper-personalized bundles—bundles that outrun basic seat-and-bag merchandising in profitability.

By Airline Type: Low-Cost Carriers Set the Agility Benchmark

Full-service carriers held 39.88% of global revenue in 2025, leveraging scale to fund multi-cloud deployments. Yet low-cost carriers register a 19.42% CAGR because their lean structures embrace greenfield deployments free of technical debt. Vendors like Radixx and Hitit supply turnkey solutions that can be configured in months, enabling LCCs to launch premium ancillaries such as priority security or lounge day-passes.

Hybrid models blur traditional labels: Gulf carriers mix unbundled fares with luxury add-ons, demanding PSS flexibility to switch between bundled and à-la-carte merchandising. Charter and regional operators rely on shared platforms to spread costs, often outsourcing completely to managed-service specialists. This convergence in service propositions forces the Passenger Service System market to deliver configurable rule engines that let an airline toggle between LCC and FSC characteristics without disrupting reservations integrity.

Geography Analysis

North America controlled 33.15% of global revenue in 2025, propelled by early adoption of cloud-native stacks and sustained investment programs such as Southwest’s USD 1.7 billion modernization roadmap. Carriers exploit robust regional hyperscale infrastructure to deploy AI-enhanced disruption management, dynamic pricing and biometric boarding across extensive domestic networks. However, deep customization around mainframe remnants slows down full adoption of ONE Order, requiring phased migration strategies that temper short-term agility gains. The Passenger Service System market now experiences a dual-speed trajectory in the region: legacy majors inch toward modular architectures while newer entrants leapfrog directly to offer-and-order models.

Asia-Pacific is the fastest-growing theatre, posting a 18.97% CAGR as governments pour over USD 18 billion into airport upgrades that embed standardized CUPPS and CUSS interfaces. Rising middle-class leisure demand and aggressive fleet expansion create fertile ground for greenfield digital stacks. Airlines such as Riyadh Air, Vietravel and Akasa opt for cloud-native platforms from inception, avoiding the mainframe drag faced elsewhere. The region’s surge in low-cost travel also encourages sophisticated ancillary merchandising, channeling more transactions into the Passenger Service System market than seat growth alone would indicate.

Europe remains a critical innovation lab thanks to stringent data-protection and passenger-rights frameworks driving omni-channel and ESG functionality. British Airways’ Nevio adoption highlights a continent-wide emphasis on offer and order convergence, while Air France-KLM’s planned majority stake in SAS signals further consolidation and platform harmonization . Meanwhile, the Middle East and parts of Africa attract attention for state-led airline launches equipped with brand-new cloud platforms that sidestep legacy hurdles. Collectively, these dynamics reinforce a multipolar Passenger Service System market in which regulatory maturity, investment cycles and passenger demographics shape adoption speed and functionality focus.

Competitive Landscape

The Passenger Service System market exhibits moderate consolidation: Amadeus, Sabre and SITA collectively account for roughly 70% of global revenue, benefiting from deep integration footprints and long-term contracts. Each pours significant sums into R&D—Amadeus alone allocated EUR 1.4 billion in 2024—to pivot monolithic code toward modular cloud services. Sabre’s joint development with Google Cloud embeds generative AI into retailing workflows, allowing carriers to script bespoke micro-services on secure multi-tenant foundations[5]Sabre, “Sabre and Google Cloud Deepen Collaboration,” sabre.com.

Competition intensifies as venture-backed entrants offer specialized modules that plug into existing PSS via open APIs. FLYR secured USD 30 million to commercialize an AI revenue-operating system that optimizes ancillaries and fares in real time . Fetcherr’s generative-AI pricing engine helps carriers elevate Revenue per Available Seat Kilometre by constantly recalibrating fares based on live demand signals. Such niche leaders focus narrowly on value-added domains where they can outperform broadly scoped incumbents, forcing larger vendors to open their ecosystems or risk share erosion.

Strategic alliances multiply: SITA collaborates with airports on biometrics, while Hitit partners regionals that require low-footprint deployments. Airlines increasingly adopt multi-vendor strategies—core PSS from a major, revenue-management from a niche player, payment orchestration from a fintech—to avoid lock-in and accelerate innovation. This mix raises switching flexibility but also amplifies integration-management complexity, thus reinforcing demand for orchestrators capable of stitching disparate services into cohesive traveler experiences across the expanding Passenger Service System market.

Passenger Service System Industry Leaders

Amadeus IT Group SA

Sabre Corporation

Société Internationale de Télécommunications Aéronautiques (SITA) N.V.

Hitit Bilgisayar Hizmetleri A.Ş.

Lufthansa Systems GmbH & Co. KG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Air France-KLM Group announced plans to raise its stake in SAS to 60.5% to expand Nordic presence and harmonize Passenger Service System capabilities across the enlarged network.

- June 2025: Vietravel Airlines renewed its five-year PSS agreement with Sabre, reaffirming the Radixx platform as its growth backbone.

- May 2025: Delta Air Lines and Korean Air jointly invested USD 550 million for a 25% equity stake in WestJet, opening a pathway toward multi-carrier PSS alignment on transpacific routes.

- April 2025: BermudAir completed a full Radixx implementation, enabling the start-up to run offer-and-order processes from launch day.

Global Passenger Service System Market Report Scope

The passenger service system market is segmented by software and services. The basic modules offered in the software are the reservation system, inventory management, and departure control system. The deployment model depends on the scale of adoption and the infrastructure required to support it.

The passenger service system market is segmented into type (software, service), deployment (on-premise, cloud), and geography (North America, Europe, Asia Pacific, Latin America, and Middle East and Africa). The report offers market forecasts and size in value (USD) for all the above segments.

| Software |

| Services |

| On-premise |

| Cloud |

| Reservation and Booking Management |

| Inventory Management |

| Check-in and Boarding |

| Loyalty Management |

| Others |

| Full-Service Carrier |

| Low-Cost Carrier |

| Hybrid Carrier |

| Charter and Regional Operator |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Type | Software | ||

| Services | |||

| By Deployment | On-premise | ||

| Cloud | |||

| By Application | Reservation and Booking Management | ||

| Inventory Management | |||

| Check-in and Boarding | |||

| Loyalty Management | |||

| Others | |||

| By Airline Type | Full-Service Carrier | ||

| Low-Cost Carrier | |||

| Hybrid Carrier | |||

| Charter and Regional Operator | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the Passenger Service System market by 2031?

The market is expected to reach USD 30.46 billion by 2031 on the back of a 16.83% CAGR.

Which deployment model is expanding the fastest?

Cloud deployment leads with an 18.35% CAGR as airlines migrate away from capital-intensive on-premise infrastructures.

Why are low-cost carriers important to market growth?

Low-cost carriers adopt cloud-native platforms without legacy constraints, driving a 19.42% CAGR and pushing vendors to deliver agile, modular functionality.

How does loyalty management impact airline profitability?

Advanced loyalty platforms enable real-time personalization, boosting ancillary sales and supporting the fastest 17.71% CAGR within application segments.

Page last updated on: