Maritime Information Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

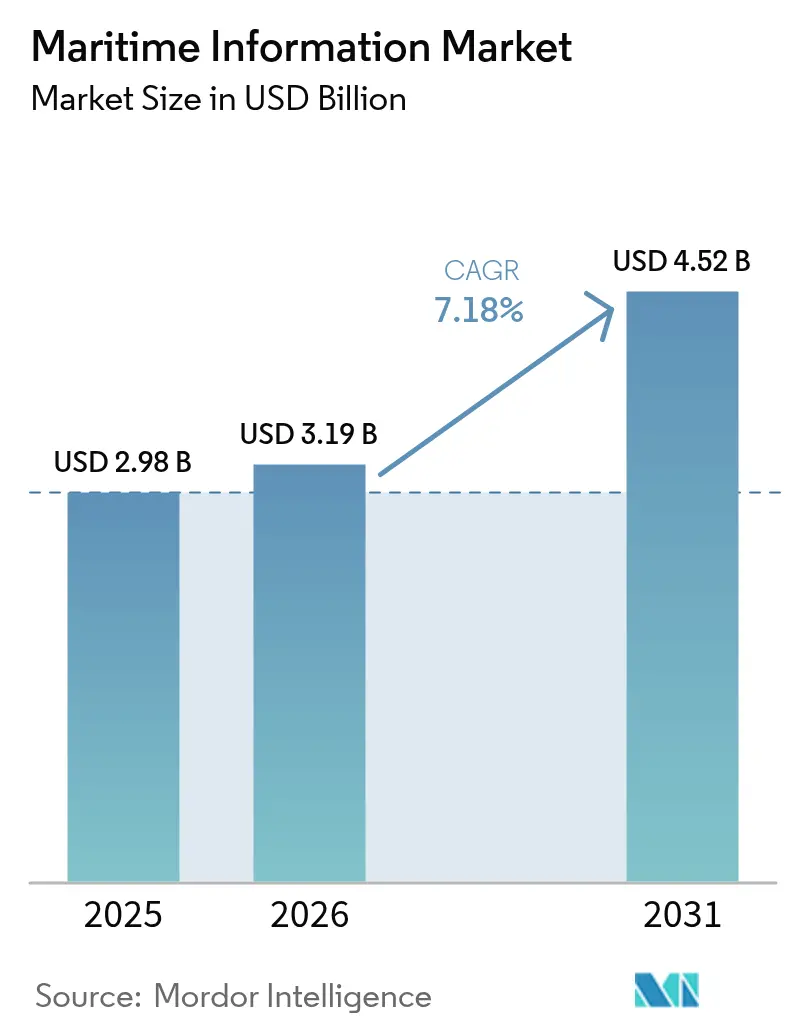

| Market Size (2026) | USD 3.19 Billion |

| Market Size (2031) | USD 4.52 Billion |

| Growth Rate (2026 - 2031) | 7.18% CAGR |

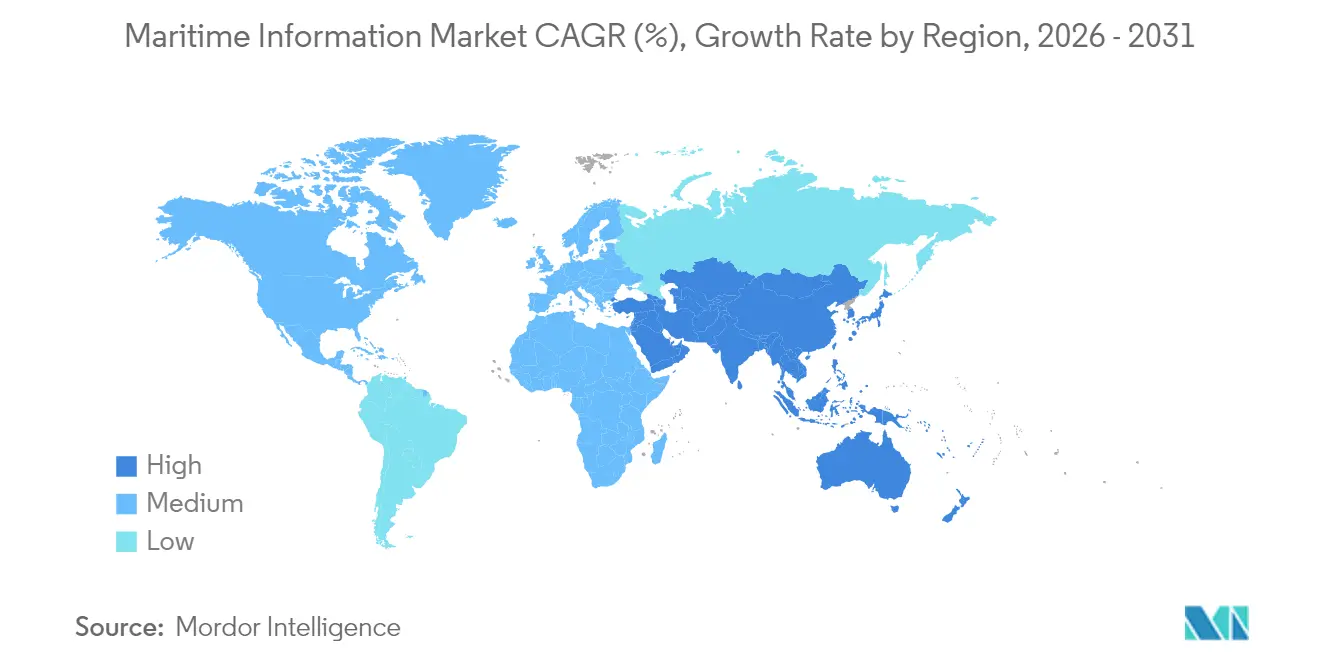

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Maritime Information Market Analysis by Mordor Intelligence

maritime information market size in 2026 is estimated at USD 3.19 billion, growing from 2025 value of USD 2.98 billion with 2031 projections showing USD 4.52 billion, growing at 7.18% CAGR over 2026-2031. This expansion underscores how fast-tracking regulatory mandates, falling costs for satellite data capture, and ubiquitous cloud connectivity are reshaping the maritime information market. Widespread digitization of port operations, rising climate-related compliance obligations, and continuous advances in artificial intelligence have created a fertile environment for fleet owners, insurers, and governments to embed data-driven decision making into day-to-day operations. Competitive intensity is building as traditional defense contractors and specialist analytics vendors race to integrate low-latency vessel tracking, predictive maintenance, and carbon reporting features on unified cloud platforms. The maritime information market is also drawing new entrants from the small-satellite ecosystem whose constellations deliver multi-source, near-real-time insights at falling price points.

Key Report Takeaways

- By application, Automatic Identification Systems led with a 37.54% maritime information market share in 2025, while Maritime Weather Analytics posted the fastest 7.52% CAGR through 2031.

- By end-user, Government and Defence held 44.55% of 2025 revenue, yet Insurance and Risk Managers are advancing at an 7.93% CAGR to 2031.

- By deployment, Cloud deployments captured 62.11% of 2025 spending and will extend leadership with a 7.36% CAGR to 2031.

- By geography, Europe accounted for 28.61% of 2025 revenue; Asia Pacific is projected to expand at an 7.86% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Maritime Information Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising maritime domain awareness mandates | +1.2% | Global, led by North America and Europe | Medium term (2-4 years) |

| Growing digitization of port logistics | +1.1% | Global, concentrated in major port hubs | Short term (≤ 2 years) |

| Declining cost of small-satellite AIS payloads | +0.9% | Global | Short term (≤ 2 years) |

| Mainstream adoption of cloud-based analytics | +1.0% | Global, led by developed markets | Medium term (2-4 years) |

| Climate-risk scoring demanded by insurers | +0.8% | Europe and North America | Medium term (2-4 years) |

| CO₂-based voyage taxation regulations | +1.3% | Europe now, global reach by 2026 | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Maritime Domain Awareness Mandates

Governments are broadening investment in multi-layer surveillance to protect strategic waterways, catalyzing fresh spending across the maritime information market.[1]U.S. Maritime Administration, “Maritime Domain Awareness,” maritime.dot.govThe U.S. Maritime Administration’s focus on resilient navigation is mirrored in NATO’s coordinated monitoring programs that stitch together AIS, radar, and optical feeds. The International Maritime Organization requires cyber-risk controls for all flagged vessels, raising baseline technology standards fleet-wide. Together these mandates enlarge procurement budgets for solutions that blend machine learning with sensor fusion to identify dark vessels and detect spoofed signals. Suppliers able to deliver sovereign-hosted, artificial-intelligence-ready platforms are moving to the front of tender lists, reinforcing the maritime information market’s growth trajectory.

Growing Digitisation of Port Logistics

Smart-port initiatives in Singapore, Rotterdam, and Hamburg prove that integrated data platforms can shave 15% off turnaround times by synchronizing vessel arrival, crane deployment, and truck movements.[2]TBA Group, “Terminal Operating Systems,” tbagroup.com Terminal Operating Systems now extend beyond yard gates, connecting to shipboard AIS, customs filings, and real-time weather feeds. COVID-19 disruptions highlighted the vulnerability of paper-based workstreams, compelling port authorities to adopt cloud dashboards to coordinate remotely. The ensuing efficiency gains and carbon-reduction benefits create a strong return on investment, encouraging even second-tier ports to join the digital wave. As a result, demand for unified maritime information solutions stretches well beyond major transshipment hubs, embedding growth for the maritime information market.

Mainstream Adoption of Cloud-Based Maritime Analytics

More than 70% of 2024 maritime software contracts specified Software-as-a-Service delivery, underlining the maritime information market’s pivot to cloud.[3]TAINA Technology, “On-Premise Deployments or SaaS-Trends and How to Choose,” taina.tech Fleet operators prefer cloud because automatic updates eliminate dry-dock software installs, while elastic compute allows high-resolution weather routing that was once cost-prohibitive. Hyperscale providers bundle AI toolkits, enabling developers to roll out predictive hull-fouling or fuel-optimization algorithms in weeks instead of months. Cloud also underpins remote operations, a critical capability during pandemic travel restrictions. Given the 62.78% revenue share already achieved in 2024, cloud platforms remain the core engine propelling the maritime information market.

CO₂-Based Voyage Taxation Regulations

The EU Emissions Trading System added shipping in 2024, and the International Maritime Organization will enforce universal carbon-intensity criteria from 2026. Vessel operators now need granular emissions data to avoid penalty costs, prompting them to fit sensors that stream fuel, engine torque, and AIS position data into auditable dashboards. Vendors with emissions modules are expanding subscription tiers, while insurers bundle carbon-footprint scores into premium models. These rules lock in long-term data requirements, ensuring sustained expansion of the maritime information market as operators scramble for compliant, real-time reporting tools.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High integration cost of legacy fleet IT | -0.7% | Global, acute for older fleets | Medium term (2-4 years) |

| Data latency for congested sea lanes | -0.4% | High-traffic corridors | Short term (≤ 2 years) |

| GNSS jamming and spoofing incidents | -0.6% | Regional hotspots, expanding globally | Short term (≤ 2 years) |

| Shortage of maritime cyber-talent | -0.5% | Global, severe in developing markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Integration Cost of Legacy Fleet IT

Older tonnage carries disparate bridge consoles, analog engine monitors, and first-generation VSAT terminals. Converting these vessels so they can stream structured telemetry into cloud dashboards can cost more than USD 100,000 per hull and usually has to occur during narrow dry-dock windows, causing scheduling bottlenecks. Smaller owners often lack technical staff and rely heavily on outside integrators, stretching payback periods. The heterogeneous mix of vendor protocols further complicates upgrades and discourages smaller fleets from immediate digitization, tempering near-term expansion of the maritime information market.

GNSS Jamming and Spoofing Incidents

The International Association of Marine Aids to Navigation and Lighthouse Authorities logged a sharp rise in spoofing events across conflict-prone regions in 2024.[5]International Association of Marine Aids to Navigation and Lighthouse Authorities, “GNSS Vulnerabilities and Maritime Navigation,” iala-aism.org False position feeds disrupt AIS integrity and undermine the trust insurers and regulators place in real-time tracking. Operators have begun fitting inertial backups and multi-constellation receivers, but such hardware raises capital outlay and does not fully neutralize sophisticated attacks. Persisting uncertainty about signal quality makes some smaller carriers reluctant to invest in fully automated routing tools, exerting a measurable brake on maritime information market uptake.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: AIS Supremacy Meets Weather Analytics Momentum

Automatic Identification Systems retained a commanding 37.54% maritime information market share in 2025, underpinned by Safety of Life at Sea mandates and port-state enforcement. That slice equated to a USD 1.12 billion maritime information market size, covering vessel tracking, collision avoidance, and traffic management. AIS vendors now layer behavioral analytics that flag suspicious course changes or speed anomalies, adding intelligence value without swapping transponders.

Maritime Weather Analytics is accelerating with a 7.52% CAGR through 2031 as charterers and insurers quantify climate exposure using fine-grained sea-state, wind, and swell predictions. Operators trim bunkers by rerouting around adverse conditions, while underwriters feed loss-probability models with weather-adjusted transit data. Synthetic aperture radar services are gaining traction for dark-vessel detection in illegal fishing hotspots, complementing AIS feeds. Growing fusion of satellite imaging, port logbooks, and cargo manifests broadens functionality, ensuring that weather-driven intelligence will remain a core growth lever for the maritime information market.

By End-User: Defence Strength Faces Insurance Dynamism

Government and Defence organizations accounted for 44.55% of 2025 revenue, translating to a USD 1.33 billion maritime information market size anchored by coastal surveillance and critical-infrastructure protection. Sovereign customers demand encrypted links, domestic data hosting, and dedicated sensor fusion centers that cross-reference radar, sonar, and AIS inputs.

Insurance and Risk Managers, though smaller, are expanding at an 7.93% CAGR to 2031. Platforms such as Breeze and Insurwave integrate AIS positions, machinery telemetry, and port congestion metrics to enable live premium adjustments. As predictive models mature, underwriters use condition-based scoring to pre-empt machinery failures, shifting focus from loss indemnification to loss prevention. Commercial Shipping Lines and Offshore Energy Operators also deepen digital spend to meet emissions requirements and to safeguard offshore assets, collectively reinforcing long-term breadth for the maritime information market.

By Deployment: Cloud Ascendancy Now Structural

Cloud-hosted offerings captured 62.11% of 2025 revenue, locking in first position within the maritime information market. That tally equates to a USD 1.85 billion maritime information market size and is projected to rise at a 7.36% CAGR as fleet operators migrate analytics workloads off shipboard servers. Cloud economies of scale slash total cost of ownership, and shared-service architectures accelerate continuous deployment of AI-driven route optimization, emissions dashboards, and regulatory updates.

On-premises deployments still appeal to navies and intelligence agencies that require air-gapped operation or strict data-sovereignty compliance, but their share of new contracts is shrinking. Hybrid designs-edge compute aboard ship feeding regional cloud hubs-are emerging as a compromise, but overall preference for pure SaaS is solidifying, keeping the maritime information market’s center of gravity firmly in the cloud.

Geography Analysis

Europe generated 28.61% of 2025 revenue, equal to USD 853 million of maritime information market size, and maintains leadership thanks to stringent EU emissions rules and advanced port digitization. Rotterdam and Hamburg deploy integrated arrival management systems that shave idle time and cut emissions, while Nordic suppliers pioneer encrypted radar-AIS fusion for both civil and military users. Carbon reporting under the EU Emissions Trading System keeps data spending elevated, and port authorities leverage digital twins for berth and yard planning.

Asia Pacific is on course for an 7.86% CAGR through 2031, delivering the maritime information market’s strongest regional expansion. Port modernization programs in China, Singapore, and India anchor demand, and Belt and Road infrastructure extends surveillance networks across the Indian Ocean and the South Pacific. The region’s distant-water fishing fleets need persistent tracking to curb illegal, unreported, and unregulated catches, while Japan and South Korea invest in autonomous navigation software and edge-AI modules. These overlapping drivers secure Asia Pacific’s long-term status as the maritime information market’s most dynamic geography.

North America benefits from heavy Coast Guard spending on cyber-resilient navigation aids and Arctic-route monitoring. U.S.-based defense contractors export integrated command-and-control suites that couple AIS, radar, and optical feeds, while Canadian authorities implement satellite AIS for polar coverage. Middle East and Africa along with South America offer smaller but rising opportunities tied to port expansions in the Gulf and Brazil’s offshore energy projects. Collectively, the geographic mosaic provides balanced growth pillars for the maritime information market.

Competitive Landscape

The maritime information market is moderately fragmented, with overlapping footprints across defense primes, specialized data providers, and satellite operators. Saab, Thales, and Northrop Grumman leverage decades-old radar and electronic-warfare expertise to serve national security clients demanding end-to-end surveillance and threat analysis. Pure-play analytics vendors such as Windward, exactEarth, and MarineTraffic focus on commercial shipping, port optimization, and insurance, differentiating through agile cloud architectures and proprietary machine-learning models.

S & P Global’s April 2025 purchase of ORBCOMM’s AIS division illustrates a vertical-integration strategy designed to control both raw data and the analytics layers that monetize it. Low-cost CubeSat operators like Spire Global democratize global tracking, putting price pressure on legacy satellite networks while opening doors for fresh applications such as dark-ship detection at scale. Cross-industry alliances pair data originators with AI specialists; Windward’s tie-up with Dataminr merges maritime feeds with geopolitical alerting, yielding richer risk intelligence.

Market players increasingly bundle cybersecurity, emissions analytics, and supply-chain risk modules into unified dashboards, positioning themselves as one-stop shops. As buyers favor platforms that combine sensor fusion, compliance reporting, and predictive decision support, smaller niche suppliers must either specialize deeply or join consortia. Consolidation is expected to intensify, yet the long tail of regional service providers and emergent satellite entrants ensures the maritime information market retains competitive tension.

Maritime Information Industry Leaders

Windward Limited

SAAB Group

Thales Group

ORBCOMM Inc.

Spire Global

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: S & P Global completed its acquisition of ORBCOMM’s Automatic Identification System business, expanding global vessel-tracking coverage and reinforcing its analytics value chain

- December 2024: Windward partnered with Dataminr to deliver real-time correlations between vessel behavior and geopolitical or weather events.

- October 2024: Thales won a multi-year contract to deploy maritime cybersecurity solutions across European port authorities.

- September 2024: Marsh and McLennan Companies launched Sentrisk, integrating maritime data with geospatial intelligence to map supply-chain vulnerabilities.

Global Maritime Information Market Report Scope

The maritime industry has been on the cusp of evolution in response to constant changes in the economic, political, and technological trends governing the industry's growth. Information exchange forms the basis for different segments within the maritime industry to coordinate with each other to enable smooth functioning.

The maritime information market is segmented by application (automatic identification systems, synthetic aperture radar, vessel identification and tracking, satellite imaging), by end-user (government, commercial), and by geography (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Automatic Identification Systems |

| Synthetic Aperture Radar |

| Vessel Identification and Tracking |

| Satellite Imaging |

| Maritime Weather Analytics |

| Port and Terminal Intelligence |

| Government and Defence |

| Commercial Shipping Lines |

| Offshore Energy Operators |

| Insurance and Risk Managers |

| Cloud-based |

| On-premises |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Egypt | |

| Rest of Africa |

| By Application | Automatic Identification Systems | |

| Synthetic Aperture Radar | ||

| Vessel Identification and Tracking | ||

| Satellite Imaging | ||

| Maritime Weather Analytics | ||

| Port and Terminal Intelligence | ||

| By End-user | Government and Defence | |

| Commercial Shipping Lines | ||

| Offshore Energy Operators | ||

| Insurance and Risk Managers | ||

| By Deployment | Cloud-based | |

| On-premises | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current value of the maritime information market in 2026?

The market stands at USD 3.19 billion in 2026, reflecting the sector's accelerating digitalization.

How fast is the sector expected to grow through 2031?

The maritime information market is forecast to post a 7.18% CAGR, reaching USD 4.52 billion by 2031.

Which region leads spending today?

Europe leads with 28.61% of 2025 revenue, anchored by strict emissions and port-digitization initiatives.

Which segment is expanding the quickest?

Maritime Weather Analytics is advancing at a 7.52% CAGR as insurers and operators incorporate climate-risk scoring.

Why are cloud deployments dominant?

Cloud offerings combine scalability, lower upfront costs, and integrated AI toolkits, capturing 62.11% of 2025 spending.

What is the chief restraint to wider adoption?

High retrofit costs for legacy fleet IT present a -0.7% drag on CAGR as older vessels need costly hardware upgrades.

Page last updated on: