Rail Seats Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

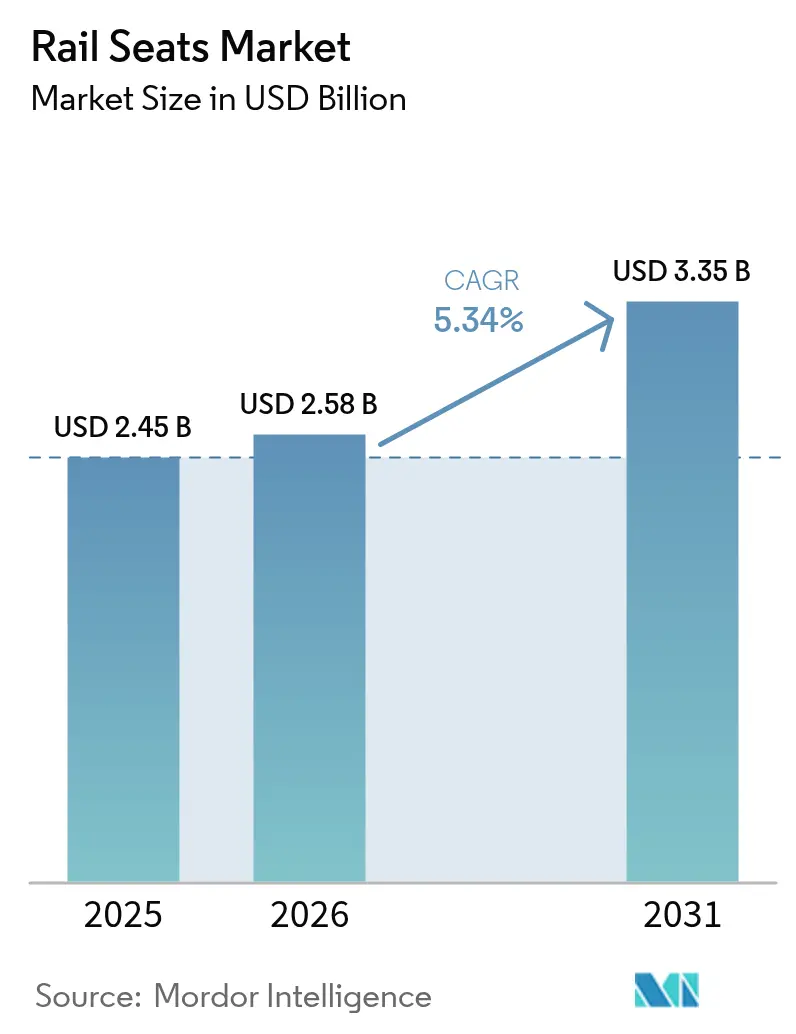

| Market Size (2026) | USD 2.58 Billion |

| Market Size (2031) | USD 3.35 Billion |

| Growth Rate (2026 - 2031) | 5.34% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Rail Seats Market Analysis by Mordor Intelligence

The Rail Seats market size is expected to grow from USD 2.45 billion in 2025 to USD 2.58 billion in 2026 and is forecast to reach USD 3.35 billion by 2031 at 5.34% CAGR over 2026-2031. This train seat market size expansion reflects the momentum of high-speed rail investments, rolling-stock modernization, and a global pivot toward passenger-centric standards. Governments in Asia-Pacific, Europe, and the Gulf continue to allocate multi-year budgets to new corridors and refurbishment programs, anchoring long-term order pipelines. Operators are simultaneously contending with strict fire-safety rules and volatile input prices, which accelerate the shift toward lightweight composites, antimicrobial surfaces, and modular layouts. Competitive dynamics remain moderate as European incumbents defend share with advanced material science while regional suppliers leverage cost advantages and local-content policies.

Key Report Takeaways

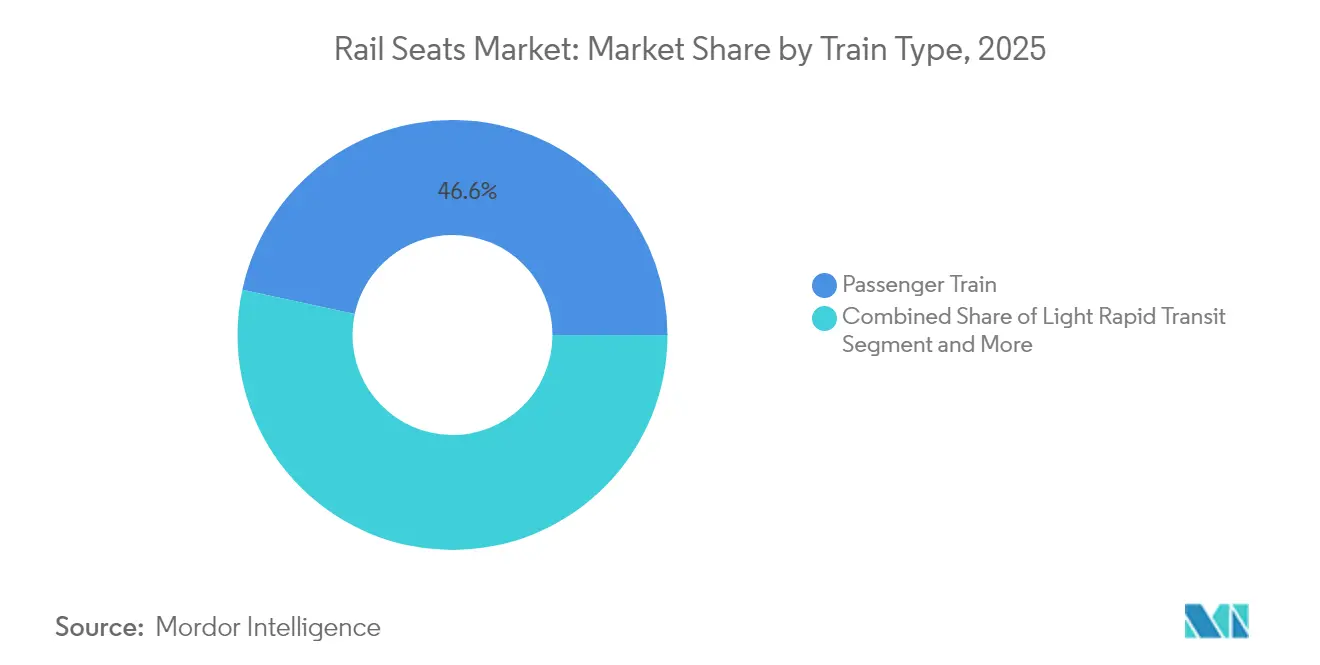

- By train type, passenger trains held 46.62% of the train seats market share in 2025, while the high-speed segment is projected to advance at a 5.46% CAGR by 2031.

- By material, fabric upholstery captured 50.74% of the train seats market share in 2025, whereas composites are forecast to grow at a 5.49% CAGR by 2031.

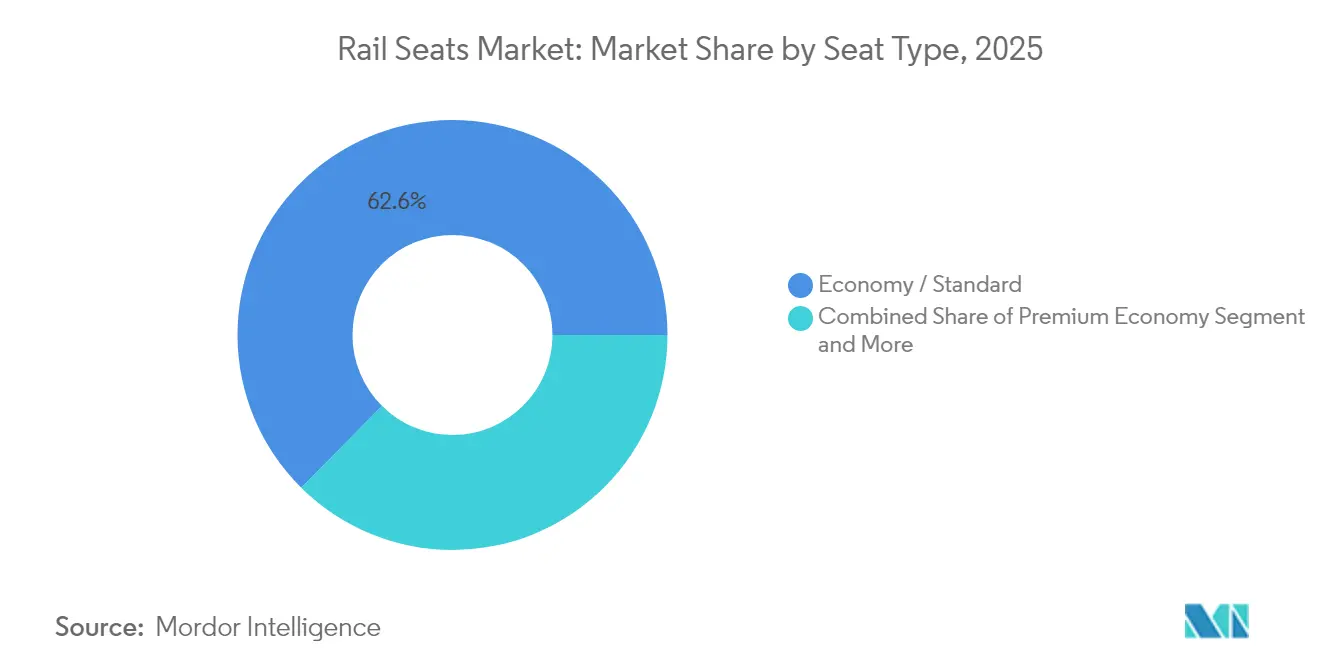

- By seat type, economy/standard configurations commanded 62.58% of the train seats market share in 2025, whereas premium-economy seating is forecast to grow at a 5.40% CAGR by 2031.

- By sales channel, OEM deliveries controlled 72.45% of the train seats market share in 2025; aftermarket replacement is progressing at a 5.52% CAGR by 2031.

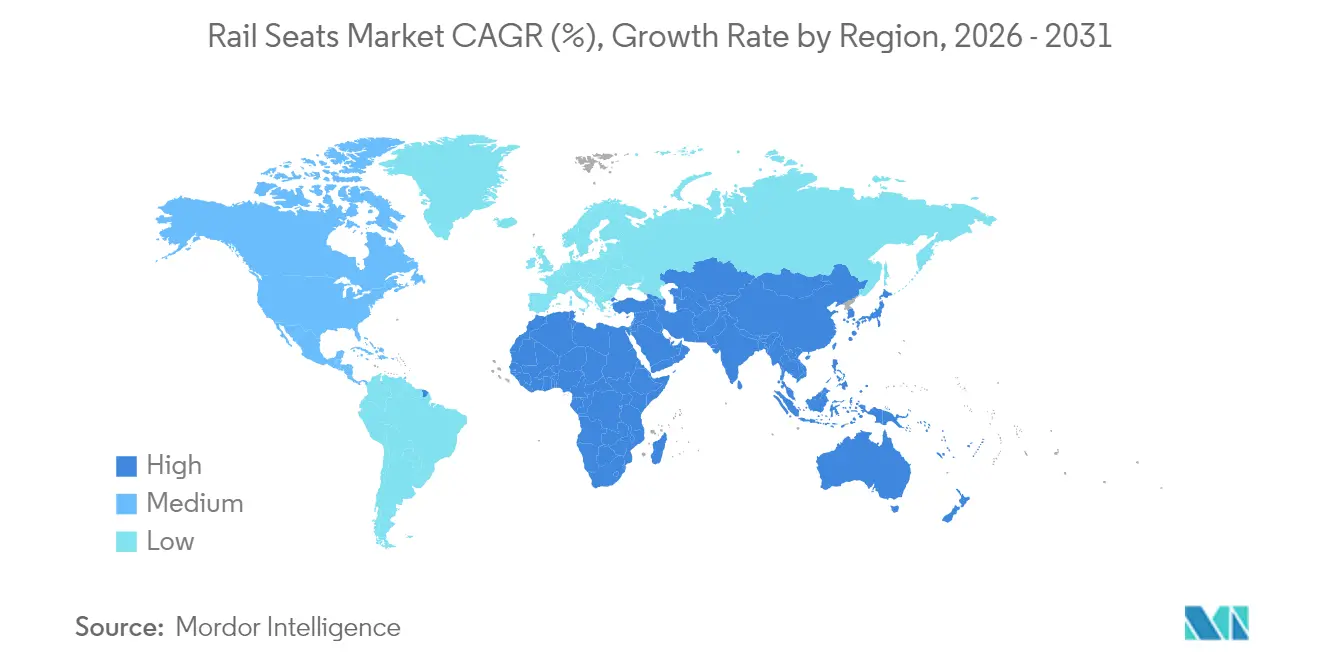

- By region, Asia-Pacific commanded a 37.25% of the train seats market share in 2025; the Middle East and Africa are set to expand at a 5.44% CAGR by 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Rail Seats Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion Of High-Speed Rail Corridors | +1.2% | Asia Pacific core, spill-over to MEA and Europe | Long term (≥ 4 years) |

| Fleet Refurbishment Programs | +0.9% | North America and EU | Medium term (2-4 years) |

| Passenger-Comfort Driven Seat Upgrades | +0.7% | Global | Short term (≤ 2 years) |

| Adoption Of Antimicrobial | +0.6% | Global, with early gains in Asia Pacific, Europe | Medium term (2-4 years) |

| Light-Weight Modular Seat Designs | +0.5% | EU, North America, Asia Pacific leading markets | Long term (≥ 4 years) |

| Smart-Sensor Enabled Predictive-Maintenance Seats | +0.4% | North America and EU, expanding to Asia Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion of High-Speed Rail Corridors

High-speed rail construction elevates seating specifications because higher velocities magnify vibration, noise, and passenger-fatigue risks that legacy seats cannot mitigate. China’s CR450 and Morocco’s Al Boraq extensions require advanced damping foams, all-composite shells, and integrated head-impact zones. Operators quickly realize that ridership growth correlates with seat ergonomics, prompting retrofits across classic intercity fleets. Switzerland’s project pipeline and the Brightline West order for Siemens Velaro trainsets confirm that even mature markets view premium seating as a competitive lever against aviation. Vendors can certify to multiple national technical standards and secure multi-country contracts, anchoring backlog visibility for the train seats market [1]“CR450: China’s Next-Gen 450 km/h High-Speed Train,” CRRC, crrc.com .

Fleet Refurbishment Programs in Mature Markets

Operators in Europe and North America extend fleet lifecycles by replacing interior modules rather than ordering new rolling stock. Deutsche Bahn’s ICE3 upgrade, Alstom’s CrossCountry Voyager program, and SNCF’s double-deck EMU projects allocate more than half of interior budgets to seating. The strategy lowers capital intensity by two-fifths versus new builds while achieving parallel gains in Net Promoter Scores. The aftermarket, therefore, emerges as a structurally resilient revenue stream that grows counter-cyclically to new-train procurement, underpinning the long-run trajectory of the train seats market [2]“ICE3 Modernization Program,” Deutsche Bahn AG, bahn.de .

Passenger-Comfort Driven Seat Upgrades

Post-pandemic travelers prioritize spaciousness, personal device support, and hygienic contact surfaces. India’s Vande Bharat coaches demonstrate a two-fifths fare uplift primarily driven by rotating seats with enhanced cushioning. Urban operators like Denmark’s DSB deploy IoT sensors in seat cushions to visualize real-time occupancy and nudge passengers toward evenly distributed loading. Competitive pressure sharpens as airlines transplant premium-economy service concepts to rail, compelling operators to differentiate through seat ergonomics rather than timetabling alone.

Adoption of Antimicrobial & Low-VOC Seat Materials

Regulators and passengers demand low-toxicity interiors after heightened health awareness. Surface-treatment specialists, such as Microban and BioCote, integrate their products into seat fabrics and armrest polymers, thereby limiting microbial growth during extended service intervals. EN 45545-2 requires multi-stage flame, smoke, and toxicity tests for each seat sub-component, increasing certification costs for each material formulation. Vendors with material-science depth can meet health and flame-retardancy thresholds, reinforcing their competitive moat in the evolving train seat market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Fire-Safety | -0.8% | Global, particularly stringent in EU | Short term (≤ 2 years) |

| Raw-Material Price Volatility | -0.6% | Global | Medium term (2-4 years) |

| Specialty Silicone and Recycled-Fabric Supply Gaps | -0.3% | North America and EU, expanding to Asia Pacific | Medium term (2-4 years) |

| Seat-Footprint Conflict | -0.2% | Global, acute in high-density urban transit | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Fire-Safety & Toxicity Certification Costs

EN 45545-2 mandates multi-stage flame, smoke, and toxicity tests for each seat sub-component, raising the cost by an exceptional price per material recipe. Small and mid-tier suppliers struggle to amortize these expenses, slowing innovation cycles and favoring incumbents with deep R&D budgets. The requirement to recertify after minor formulation tweaks further constrains the speed at which bio-based or recycled materials can enter revenue service. Consequently, certification complexity is a structural headwind that dampens near-term growth in the train seats market.

Raw-Material Price Volatility (PU Foam, Metals)

Prices of toluene di-isocyanate (TDI) and methylene di-isocyanate (MDI) for polyurethane foams jump in tandem with petrochemical feedstock costs. At the same time, aluminum and steel fluctuate with global trade policy and capacity shutdowns. Manufacturers locked into multi-year supply agreements face margin compression or contentious price-escalation clauses with rail operators. The economics are more challenging for aftermarket contracts where operators expect stable pricing. Rising feedstock costs can prompt deferments of significant refurbishment projects, tempering short-term order volumes in the train seats market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Train Type: High-Speed Segments Drive Premium Demand

Passenger trains preserved 46.62% of the train seats market share in 2025, while High-speed services generated the fastest 5.46% CAGR from 2026 to 2031. Operators on new 300 km/h+ corridors often specify composite shells, cold-cure foams, and integrated infotainment that lift average selling prices by one-third. The more dynamic growth trajectory mirrors a multi-continent infrastructure pipeline spanning China, Saudi Arabia, and California. Light rail and metro projects contribute stable unit volumes, yet their lower ASPs dilute revenue share.

Innovation increasingly blurs rigid train-type boundaries. Deutsche Bahn’s IdeasTrain concept trials movable bulkheads and swiveling clusters that allow the same rolling stock to toggle between commuter and long-distance service, illustrating how modularity disrupts legacy seat-specification silos. Vendors who engineer seats to meet high-speed and commuter load cases gain design-reuse collaborations that compress time-to-market and reinforce profitability in the train seats market.

By Material: Composites Accelerate Amid Sustainability Push

Fabric upholstery maintained 50.74% of the train seats market share in 2025, yet composite assemblies are tracking a 5.49% CAGR as operators seek double-digit weight savings. Carbon-fiber reinforced plastics and advanced thermoplastic laminates achieve fire-safety compliance without heavy intumescent coatings, trimming vehicle mass by up to 40 kg per car. Metal frames remain vital for crash-energy absorption but now incorporate hollow extrusions and friction-stir welds to cut density.

Supply chains adapt as tier-one seat manufacturers co-locate autoclave and thermo-forming capacity near rolling-stock plants to minimize logistics emissions. Fabric vendors respond with recycled yarn and antimicrobial finishes but concede volume to composite shells in premium cabins. The irreversible lean toward composites positions material science as a competitive differentiator in the train seat market.

By Seat Type: Premium Economy Emerges as Growth Leader

Economy configurations covered 62.58% of the train seats market share in 2025, yet premium-economy formats record a 5.40% CAGR because moderate upgrades in pitch, recline, and cushion geometry unlock fare premiums. Business and first-class remain niche in unit terms but anchor the highest margins, often commanding ASP multiples of 4–5 versus standard seats.

Airline service concepts seep into rail interior design, with privacy wings, personal charging docks, and wireless-charging armrests redefining passenger expectations for long-distance journeys. Fold-down and bench layouts dominate metros where peak-hour throughput overrides individual comfort. Nevertheless, even urban systems test padded, wipe-clean inserts to elevate user experience, illustrating the widening scope for differentiated products across the train seats market.

By Sales Channel: Aftermarket Gains Momentum Through Fleet Aging

OEM deliveries accounted for 72.45% of the train seat market share in 2025, but the 5.52% CAGR in the aftermarket reflects accelerating seat replacement cycles for 15- to 20-year-old fleets in Europe and North America. Refurbishment programs can upgrade many seats per car at two-thirds the capital expenditure (capex) of buying new rolling stock, while renewing the cabin aesthetic.

Knorr-Bremse’s aftermarket revenue share in rail systems underscores the scale achievable for suppliers that bundle seats with door, brake, and HVAC part packages. Interoperable mounting interfaces and adjustable plinths enable swift swap-outs, allowing for overnight depot operations that minimize service disruptions. The channel shift solidifies the aftermarket as a structural pillar of the train seat market.

Geography Analysis

Asia-Pacific led with 37.25% of the train seats market share in 2025, underpinned by China’s huge high-speed network expansion and India’s Vande Bharat fleet ramp-up. Domestic suppliers such as CRRC and Tata Steel win contracts by aligning with government localization mandates while integrating imported damping foams and flame-retardant fabrics. Japan maintains a premium niche through Shinkansen ergonomics and quality, and South Korea’s urban smart-metro programs adopt sensor-equipped seats for passenger flow optimization across Seoul’s network. These dynamics secure Asia-Pacific’s status as the train seat market's anchor growth engine.

The Middle East & Africa region records the fastest 5.44% CAGR from 2026 to 2031 as cross-border Gulf Cooperation Council rail corridors take shape. Saudi Arabia’s Dream of the Desert luxury concept train and the UAE’s Etihad Rail Phase 2 orders catalyze demand for leather-trimmed business-class pods and modular café arrangements. Egypt’s 41-unit Siemens Velaro order illustrates the pivot toward accessible, high-capacity interior layouts featuring foam-core side supports and wheelchair bays. In Sub-Saharan Africa, durability and low maintenance rank above aesthetics, steering purchasing criteria toward powder-coated steel frames and replaceable PVC pads, a nuance critical to capturing share in the train seats market .

Europe and North America emphasize refurbishment and alignment with sustainability. Operators retrofit interiors to meet EN 45545 fire codes, ADA accessibility requirements, and corporate carbon targets without raising fleet counts. Programs such as Deutsche Bahn’s ICE3 and Amtrak’s Airo Agility orders elevate aftermarket seat volumes, sustaining capacity utilization among European seat producers. Switzerland’s forthcoming high-speed links will layer brand-new rolling stock demand atop the region’s refurbishment baseline, ensuring steady opportunity flow for the train seats market.

Competitive Landscape

Global competition is moderately concentrated. European specialists Grammer AG, Kiel Group, and Compin Fainsa command roughly one-third of global turnover while defending intellectual property in energy-absorbing foams, composite shells, and quick-release anchoring mechanisms. Asian producers, including Jiangsu Fangda and Faiveley Transport (China), leverage labor cost advantages and state procurement preferences to penetrate domestic high-speed orders, gradually scaling quality levels to meet export standards.

Technology integration shapes positioning. Grammer’s smart-cushion sensor suite and Kiel’s antimicrobial vinyl lines illustrate how suppliers bundle value-added features that lift ASPs and create data-monetization streams. Partnerships proliferate between seat OEMs and material companies developing bio-based polyurethanes or halogen-free FR additives to stay ahead of evolving regulations. M&A activity targets specialist composites shops to secure in-house laminate capacity and shorten design cycles, reflecting the strategic importance of material depth in the train seats market.

White space remains in emerging regions, where local manufacturers lack fire-safety certification expertise and durable lightweight know-how. Joint ventures form as incumbent European brands seek tariff-free access and offset obligations, while regional firms desire technology transfer. Suppliers proficient in circular design principles are poised to capture future tenders that require end-of-life recycling plans, an emerging criterion in the train seats market.

Rail Seats Industry Leaders

Grammer AG

Seats Incorporated

Harita Seating System Limited

Sears Manufacturing Company

Kiel Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: A-Train AB completed SEK 5.6 billion refinancing to procure new electric high-speed trains for Sweden’s network, underlining sustained passenger-comfort investment.

- December 2024: Toyota Boshoku showcased thermal-comfort rail seats and accessory covers at Bharat Mobility Global Expo 2025 to accelerate its entry into the Indian market.

- September 2024: Siemens delivered 41 Velaro EGY high-speed trainsets to Egypt, each fitted with 479 seats and two wheelchair spaces, highlighting accessibility and capacity priorities.

Global Rail Seats Market Report Scope

The rail seatsmarket covers the latest trends and technological development in the rail seats market, demand of the train type, material type, geography and market share of major rail seat manufacturers across the world.

| Passenger Train |

| High-Speed Train |

| Light Rapid Transit |

| Monorail |

| Tram |

| Metal Frames |

| Fabric Upholstery |

| Leather Upholstery |

| Composites & Others |

| Economy / Standard |

| Premium Economy |

| Business / First |

| Fold-down / Bench |

| OEM Supply |

| Aftermarket Replacement |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia Pacific | |

| Middle East and Africa | Saudi Arabia |

| UAE | |

| Turkey | |

| South Africa | |

| Egypt | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Train Type | Passenger Train | |

| High-Speed Train | ||

| Light Rapid Transit | ||

| Monorail | ||

| Tram | ||

| By Material | Metal Frames | |

| Fabric Upholstery | ||

| Leather Upholstery | ||

| Composites & Others | ||

| By Seat Type | Economy / Standard | |

| Premium Economy | ||

| Business / First | ||

| Fold-down / Bench | ||

| By Sales Channel | OEM Supply | |

| Aftermarket Replacement | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| UAE | ||

| Turkey | ||

| South Africa | ||

| Egypt | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current global value of the train seats market?

It stands at USD 2.58 billion in 2026, with a forecast of USD 3.35 billion by 2031.

Which region leads to the demand for train seating solutions?

Asia-Pacific holds 37.25% of revenue, powered by China’s and India’s network expansions.

Why are composite seats gaining traction?

They deliver up to 40% weight savings and comply with strict fire-safety rules, supporting net-zero goals.

How fast is the aftermarket segment growing?

Aftermarket seat replacement is advancing at a 5.52% CAGR through 2031 as fleets age.

What regulation most affects seat material choices?

EN 45545-2 dictates flame, smoke, and toxicity thresholds, driving material R&D and certification costs.

Which seat class shows the highest growth rate?

Premium economy formats are expanding at a 5.40% CAGR due to strong passenger willingness to pay for extra comfort.

Page last updated on: