Automotive Ventilated Seats Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

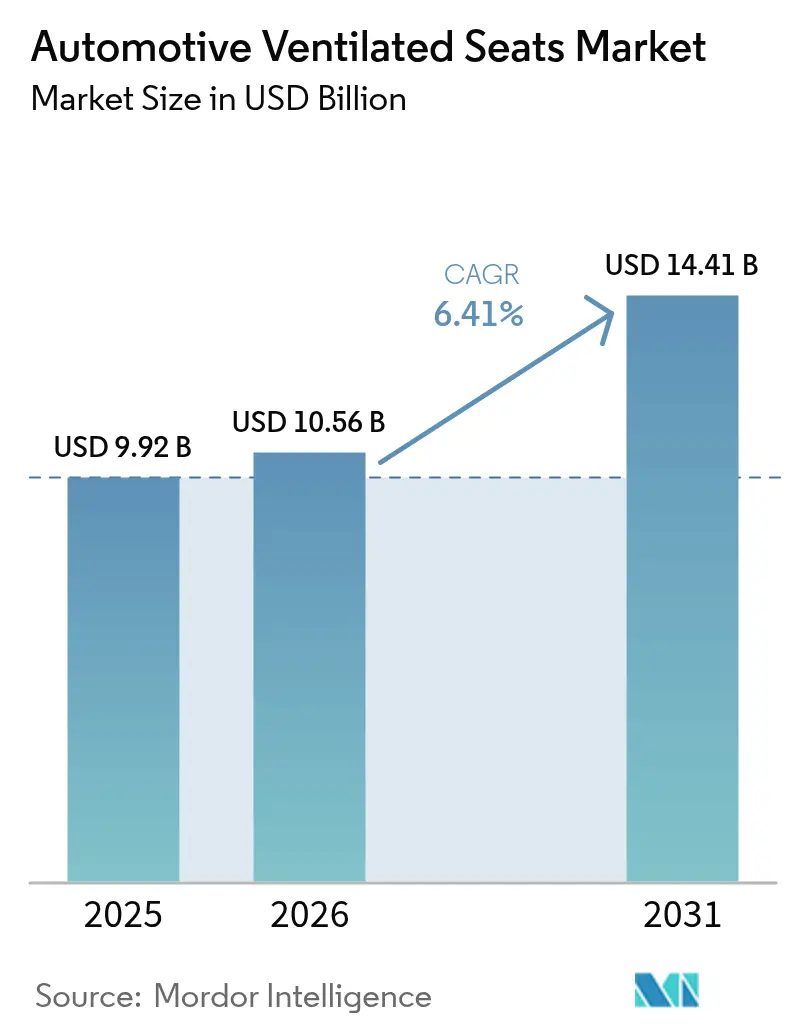

| Market Size (2026) | USD 10.56 Billion |

| Market Size (2031) | USD 14.41 Billion |

| Growth Rate (2026 - 2031) | 6.41% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Ventilated Seats Market Analysis by Mordor Intelligence

The Automotive ventilated seats market size was valued at USD 9.92 billion in 2025 and estimated to grow from USD 10.56 billion in 2026 to reach USD 14.41 billion by 2031, at a CAGR of 6.41% during the forecast period (2026-2031). Current growth comes from automakers pairing seat-level HVAC with broader electrification strategies, micro-blower efficiency gains, and falling perforated-foam costs. Asia-Pacific leads demand as Chinese electric-vehicle production scales, while North American and European OEMs widen fit rates in mid-range models. Competitive dynamics remain moderate because established thermal-comfort suppliers still control core component technology, but start-ups focused on sustainable materials and energy-saving algorithms are adding pressure. Over the next five years, regulatory attention on driver fatigue, along with premium shared-mobility upgrades, is set to keep the ventilated seats market on a steady expansion path.

Key Report Takeaways

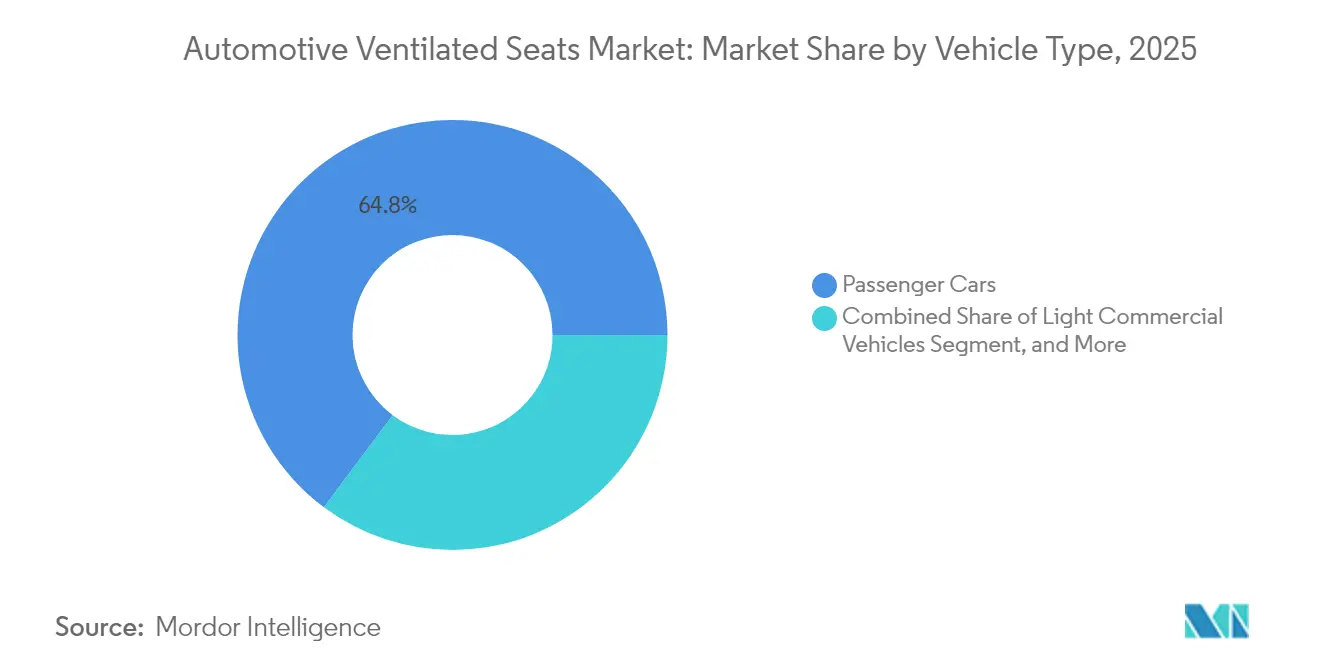

- By vehicle type, passenger cars held 64.80% of the ventilated seats market share in 2025; the segment also records the fastest 8.05% CAGR through 2031.

- By propulsion, the Internal Combustion Engine held 78.60% of the market share. On the other hand, battery electric vehicles are projected to post a 12.10% CAGR to 2031, the quickest pace among powertrains in the ventilated seats market.

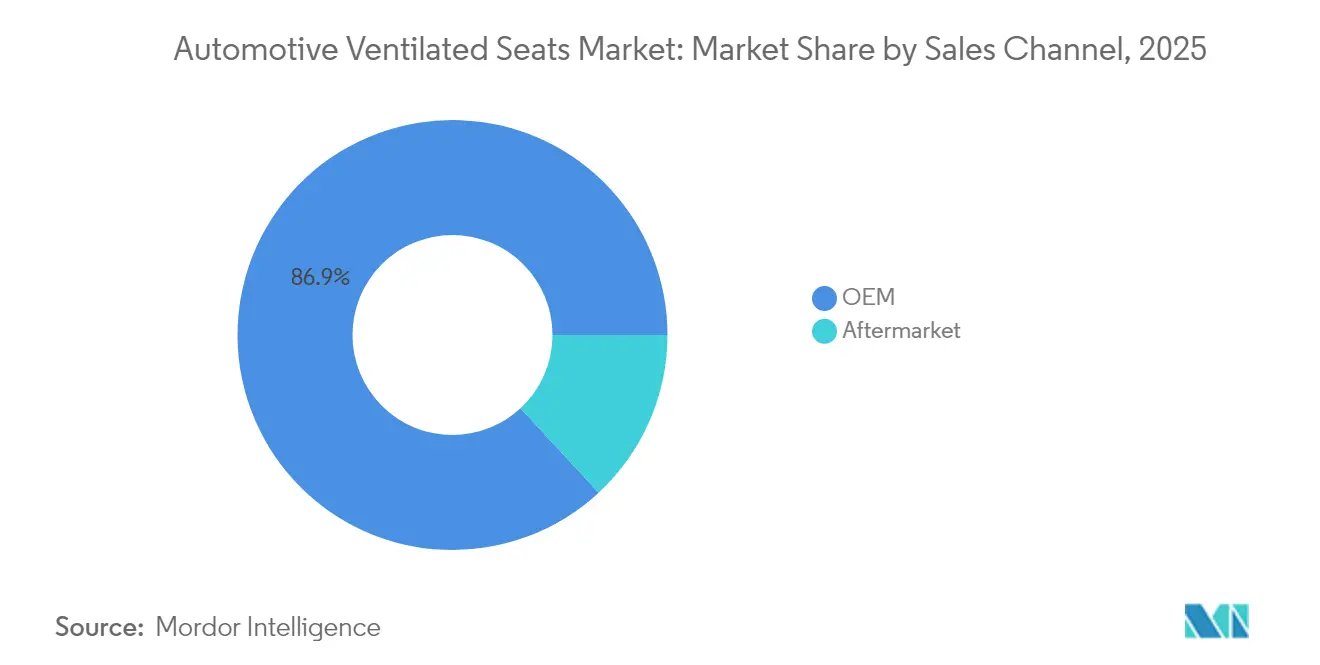

- By sales channel, the OEM segment commanded 86.90% share of the ventilated seats market size in 2025, while the aftermarket is forecast to expand at 8.95% CAGR through 2031.

- By seat-trim material, synthetic leather accounted for 47.80% of the ventilated seats market size for seat materials in 2025 and is expected to grow at an 7.98% CAGR.

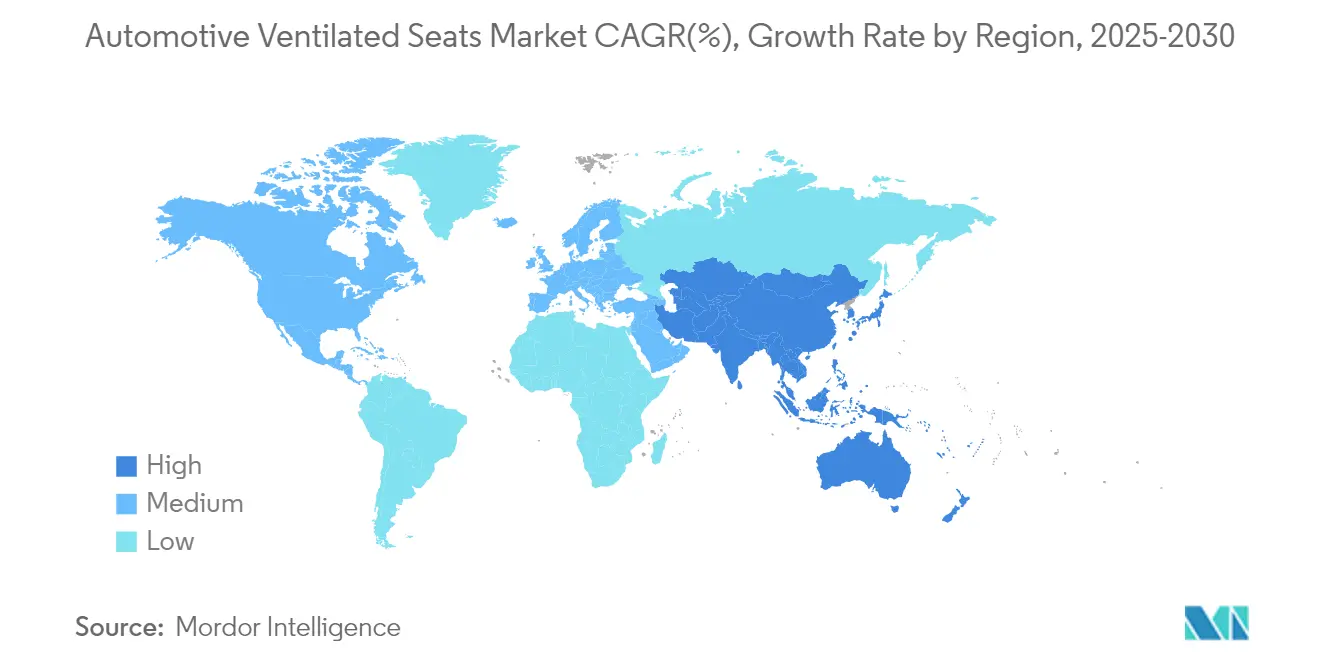

- By geography, Asia-Pacific dominated with a 45.00% share in 2025 and is advancing at an 8.45% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive Ventilated Seats Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in EV sales enabling seat-level HVAC | +2.1% | China, Europe, North America | Long term (≥ 4 years) |

| Rising consumer demand for enhanced cabin comfort | +1.8% | Global; premium uptake in North America & Europe | Medium term (2 – 4 years) |

| OEM feature-differentiation in mid-range models | +1.2% | Asia-Pacific core; spill-over to North America | Short term (≤ 2 years) |

| Cost decline in micro-blower and perforated-foam technologies | +0.9% | Global manufacturing hubs, especially Asia-Pacific | Medium term (2 – 4 years) |

| Fatigue-health regulations | +0.6% | Europe, North America; expanding to Asia-Pacific | Long term (≥ 4 years) |

| Premium shared-mobility fleet upgrades | +0.4% | Urban centers worldwide, led by China & North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Consumer Demand for Enhanced Cabin Comfort

Cabin expectations have shifted as cars become mobile living spaces. Ventilated seats now rank among the three most requested comfort features in hot-climate purchase surveys, and ownership cycles extending beyond a decade reinforce demand for upgrades. In high-temperature regions, localized seat cooling delivers faster relief than conventional air-conditioning, making it a critical differentiator in retail showrooms. Ride-sharing passengers add further pressure by normalizing premium amenities across price segments. Collectively, these factors place comfort at the center of brand-loyalty strategies and extend the addressable ventilated seats market.

OEM Feature-Differentiation in Mid-Range Models

Automakers in the USD 25,000–40,000 bracket are bundling ventilated seats to raise transaction prices without a luxury-brand badge. Lear’s ComfortMax modules, reaching production in 2025, deliver 40% quicker thermal response while cutting seat part count by half, lowering assembly complexity[1]Lear Corporation, “ComfortMax Seats Deliver Faster Thermal Response,” learnercorp.com. Modular kits allow wider model-mix coverage, accelerating penetration in Asia-Pacific, where value-conscious buyers accept moderate price premiums for tangible comfort.

Surge in EV Sales Enabling Seat-Level HVAC

Electric-vehicle architectures lack waste engine heat, making localized climate control vital for range preservation. Hyundai’s radiant heating concept trims HVAC energy draw by 17% yet keeps cabin comfort intact. Chinese battery-electric vehicles combine perforated foam with predictive software that pre-conditions seating surfaces, offsetting up to 30% of range loss in extreme weather. As EV sales climb, ventilated seats shift from optional luxury to functional energy-efficiency hardware, lifting the long-term growth curve of the ventilated seats market.

Cost Decline in Micro-Blower and Perforated-Foam Technologies

High-volume production in Xiamen and Suzhou is lowering micro-blower pricing while raising airflow and lowering noise. Delta Electronics’ PWM-controlled seat blowers now ship with EMC shielding and compact vibration mounts[2]Delta Electronics, “Automotive Seat Ventilation Blower Series,” delta.com. Parallel advances in laser-perforated synthetic leather and low-density polyurethane foams reduce component weight by 15% while preserving tactile quality. The resulting bill-of-materials savings unlock a broader mid-range customer base.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High system cost and complex integration | −1.4% | Global; particularly impacting emerging markets | Medium term (2 – 4 years) |

| Reliability and maintenance concerns | −0.8% | All regions; higher impact in harsh climates | Long term (≥ 4 years) |

| EV range anxiety over HVAC energy draw | −0.6% | EV-adopting regions, primarily Europe and China | Short term (≤ 2 years) |

| Cabin acoustic targets limiting fan noise levels | −0.4% | Premium vehicle segments globally | Medium term (2 – 4 years) |

| Source: Mordor Intelligence | |||

High System Cost and Complex Integration

Factory installations require tailored seat frames, wiring, and software calibration, keeping unit costs elevated for emerging-market models. Retrofit packages add hurdles such as air-path routing and controller CAN bus adaptation. Safety certification under Federal Motor Vehicle Safety Standard 207 mandates structural integrity checks whenever ventilation modules are inserted, prolonging validation cycles and constraining the ventilated seats market’s reach[3]National Highway Traffic Safety Administration, “Federal Motor Vehicle Safety Standard 207,” nhtsa.gov.

Reliability and Maintenance Concerns

Long service life in dusty or humid regions can cause clog perforations and fatigue in blower assemblies. Peer-reviewed HVAC reliability studies show blower modules account for half of all thermal-system failures, underscoring design-for-durability priorities. OEMs now embed self-diagnostics that flag restricted airflow, while Hyundai Transys’ eco-friendly slab padding improves wear resistance and VOC performance in one step. Even so, maintenance complexity still tempers buyer confidence outside premium segments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Passenger Cars Drive Premium Adoption

Passenger cars generated the majority share in 2025, capturing 64.80% of the ventilated seats market share amid an 8.05% CAGR outlook through 2031. Sport Utility Vehicle drive volume by bundling the feature in popular trim packs. Extended commute times and growing interest in driver-assistance packages amplify demand for seat-level climate control, especially where summer heatwaves lengthen. Fleet operators of light commercial vans are beginning to evaluate reduced fatigue benefits, yet upfront price gaps continue restraining adoption in heavy trucks and buses.

The segment’s momentum is set to expand the overall ventilated seats market size as mid-range sedans and compact Sport Utility Vehicles introduce value-grade modules that reuse premium components. Specialist suppliers are offering scalable platforms that drop into multiple body styles without major redesign, accelerating time to market. Over the forecast period, regional mandates targeting driver wellness could lift penetration in commercial passenger shuttles and ride-hailing fleets, reinforcing the passenger-car segment’s leadership.

By Propulsion Type: Electric Vehicles Accelerate Innovation

Internal-combustion platforms still dominate at 78.60% in 2025, yet battery electric vehicles are on a steeper trajectory with a 12.10% CAGR to 2031. The BEV tacker is propelled by the need to mitigate HVAC-induced range loss, prompting integration of seat ventilation with battery-thermal strategies. Yanfeng’s Smart Cabin Seats create individual micro-climates to cut cabin heat-soak before the main HVAC starts, exemplifying how BEV packaging flexibility benefits ventilated seat design. Hybrid and plug-in hybrid models play a transitional role, offering OEMs a testbed for advanced comfort algorithms without full EV constraints.

Rapid BEV growth means the ventilated seats market size linked to electric drivetrains is set to outpace the overall market. Suppliers that can miniaturize blowers and unify heating, cooling, and haptic feedback into one module stand to gain from tight EV packaging envelopes. Regulatory incentives that reward energy-efficient HVAC will further tilt development budgets toward BEV-optimized seating systems.

By Sales Channel: Aftermarket Momentum Builds

OEM-installed systems retained 86.90% share in 2025, consistent with manufacturer warranty expectations and seamless design integration. Yet, the aftermarket is projected to post a 8.95% CAGR as owners of older vehicles seek comfort upgrades without replacing the entire car. Universal retrofit kits with plug-and-play controllers and slim blower modules are reducing labor time, broadening installer networks.

Despite momentum, aftermarket penetration faces obstacles including dependent air-path requirements and compatibility with airbag sensors. Seat suppliers are addressing these issues through detailed fitment guides and pre-tested wiring harnesses. As vehicle lifespans extend, the sizeable parc of eligible vehicles will keep the aftermarket a relevant growth pocket within the overarching ventilated seats market.

By Seat-Trim Material: Synthetic Leather Dominates Performance

Synthetic leather accounted for 47.80% of the ventilated seats market in 2025 and is forecast to grow 7.98% annually as engineered permeability supports stronger airflow than natural hides. Surface treatments resist UV degradation and staining, making them suitable for high-traffic ride-sharing fleets. Genuine leather retains prestige value but remains cost-intensive and difficult to perforate uniformly.

Material science advances are now aligning durability with sustainability. Dow’s collaboration with Adient and JLR is piloting closed-loop recycled foams that cut carbon while maintaining mechanical resilience. Such circularity efforts strengthen the synthetic category’s cost-competitiveness and environmental profile, supporting broader OEM adoption across segments.

Geography Analysis

Asia-Pacific held 45.00% of the ventilated seats market in 2025 and is expanding at an 8.45% CAGR through 2031. China anchors regional demand: electric vehicles already comprise 45% of its new-car sales, and localized suppliers such as QIANZE deliver 1,000 ventilated seat sets each month, helping OEMs contain costs. Japanese and South-Korean firms add technology depth; Hyundai Transys, for example, earned national certification for VOC-reduced padding that enhances airflow. Hot and humid Southeast-Asian climates further boost user appeal, while government subsidies on energy-efficient components align with ventilated seat adoption.

North America’s mature passenger-car parc fosters steady replacement demand as comfort features migrate down-segment. Extended vehicle ownership cycles encourage retrofit activity, and collaborative programs between General Motors and Lear Corporation bring modular ComfortMax units to high-volume nameplates. Commercial fleets are evaluating ventilated driver seats to comply with forthcoming fatigue-management guidelines, creating new volume opportunities.

Europe focuses on premium integration and life-cycle emissions. FORVIA’s truck seat solution trimming CO₂ impact by 40% is emblematic of regional sustainability evolution. Legislative pressure on recyclability drives adoption of foam and cover stocks derived from post-consumer waste, positioning European OEMs at the forefront of circular seat component sourcing.

Emerging markets across Latin America, the Middle East, and Africa show latent demand, but price sensitivity and service-network gaps slow penetration; localized assembly partnerships are expected to ease these hurdles by the late forecast years.

Competitive Landscape

The ventilated seats market features a cluster of large incumbents centered on thermal management technology. Gentherm, posting USD 1.5 billion in 2023 and adding USD 2.6 billion in fresh automotive awards. Lear, Adient, and Faurecia (FORVIA) are integrating blower control, massage, and heating into unified modules; Lear’s latest iteration cuts component count by 50% while exceeding previous airflow metrics. These firms also pursue vertical control of foam chemistry and electronic drivers to secure supply continuity.

Start-up competition centers on energy-optimized algorithms and sustainable cover stocks. Material specialists are trialing shape-memory alloys and bio-based polyurethane blends that promise lower operating currents. Delta Electronics and other Tier-II motor suppliers are climbing the value chain by adding turnkey airflow subsystems. Patent filings on low-pressure airflow paths and smart control logic are rising, signaling intensifying R&D. Moderate market concentration is likely to persist as new entrants capture niche contracts. At the same time, top suppliers defend scale advantages through multi-year sourcing agreements.

Automotive Ventilated Seats Industry Leaders

Faurecia

Adient PLC

Lear Corporation

Toyota Boshoku Corporation

Gentherm Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Lear Corporation confirmed ComfortMax integration with General Motors, delivering 40% faster thermal response and a 50% parts reduction ahead of Q2 2025 production.

- November 2024: Dow, JLR, and Adient began closed-loop recycled foam trials for seating under JLR’s Reimagine strategy, aiming for carbon-neutral-zero by 2039.

- September 2024: Hyundai Motor Group showcased radiant heating cutting cabin energy use by 17% in the Genesis Neolun concept.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the automotive ventilated seats market as the yearly value of factory-installed or like-for-like replacement seat assemblies that actively push air through perforated cushions to cool or heat occupants in passenger cars and light and medium commercial vehicles. The build counts are multiplied by blended OEM and premium-grade aftermarket average selling prices to yield market value.

Scope Exclusion: Retro-fit blower kits fitted to legacy seats and seat-climate systems for buses or off-road machinery are not included.

Segmentation Overview

- By Vehicle Type

- Passenger Cars

- Hatchback

- Sedan

- Sport Utility Vehicle

- Multi-Purpose Vehicle

- Light Commercial Vehicles

- Medium and Heavy Commercial Vehicles

- Buses and Coaches

- Passenger Cars

- By Propulsion Type

- Internal Combustion Engine (ICE)

- Hybrid & Plug-in Hybrid

- Battery Electric Vehicle (BEV)

- By Sales Channel

- OEM

- Aftermarket

- By Seat-Trim Material

- Genuine Leather

- Synthetic Leather (PU, PVC)

- Fabric

- By Geography

- North America

- United States

- Canada

- Rest of North America

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Spain

- Italy

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- South Africa

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interview seat-engineering managers at global OEMs, Tier-1 sales directors in Asia-Pacific and North America, and aftermarket distributors in Europe. Insights on option pricing, expected EV share, and warranty failure rates allow us to validate secondary ratios, plug data gaps, and fine-tune regional conversion factors.

Desk Research

We start by mapping vehicle production, model mix, and trim-level penetration from public sources such as OICA vehicle output tables, UN Comtrade seat component trade codes, and regional road-worthiness statistics. Safety filings, 10-Ks, and investor decks by leading seat suppliers help us tease out program launches and average selling prices. Comfort-feature take-rates are benchmarked from new-car registration data released by transport ministries, while patent families in Questel reveal cost trends for micro-blower modules. To cross-check geographic demand, analysts review monthly news flows in Dow Jones Factiva and regional trade journals. This list is illustrative; many additional sources are screened and logged before use.

Market-Sizing & Forecasting

A top-down build starts with light-vehicle production and in-use parc, adjusted by ventilated-seat fitment rates and ASP corridors. Selective bottom-up checks, supplier revenue roll-ups and sampled ASP multiplied by volume for major models, are applied to reconcile totals. Key variables include new vehicle output, EV share (higher cabin HVAC efficiency demand), trim-level penetration of comfort options, micro-blower cost curves, and regulatory incentives for energy-saving HVAC. Forecasts use multivariate regression layered on ARIMA filters, with scenario analysis to stress energy price and consumer income swings. Gaps where aftermarket data run thin are bridged by region-specific replacement cycle assumptions vetted in interviews.

Data Validation & Update Cycle

Outputs pass a three-stage review: automated variance scans against historical series, peer review by a second analyst, and senior sign-off. The model refreshes annually; mid-year updates trigger when supply chain shocks or policy moves alter volume or ASP by more than five percent. A last-mile sense check is run before each client delivery.

Why Our Automotive Ventilated Seats Baseline Commands Reliability

Published estimates often differ because firms choose dissimilar feature scopes, pricing ladders, and refresh cadences.

Key gap drivers include whether aftermarket value is counted, how EV adoption is modeled, and the vintage of production data used for extrapolation.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 9.92 B (2025) | Mordor Intelligence | - |

| USD 9.20 B (2024) | Global Consultancy A | Older base year and limited material split dilute OEM price premiums |

| USD 9.28 B (2024) | Industry Association B | Excludes BEV growth and applies straight-line growth from 2019 data |

The comparison shows that, by selecting the latest production counts, modeling EV-led penetration shifts, and blending OEM plus high-quality aftermarket revenues, Mordor delivers a balanced, transparent baseline that decision makers can trace back to clear variables and repeatable steps.

Key Questions Answered in the Report

How big is the ventilated seats market in 2026?

The ventilated seats market size stands at USD 10.56 billion in 2026.

Which vehicle segment leads adoption of ventilated seating?

Passenger cars dominate with 64.80% market share in 2025 and show an 8.05% CAGR through 2031.

Why are ventilated seats important for electric vehicles?

Localized seat cooling cuts HVAC energy demand and helps protect driving range, making the technology integral to EV comfort strategies.

Which region offers the highest growth potential?

Asia-Pacific leads with 45.00% revenue share and the fastest 8.45% CAGR thanks to China’s expanding EV base and deep manufacturing capacity.

What materials are most used in ventilated seat covers?

Synthetic leather holds 47.80% of segment revenue because engineered perforations boost airflow while containing costs.

Page last updated on: