Intraoral Scanners Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

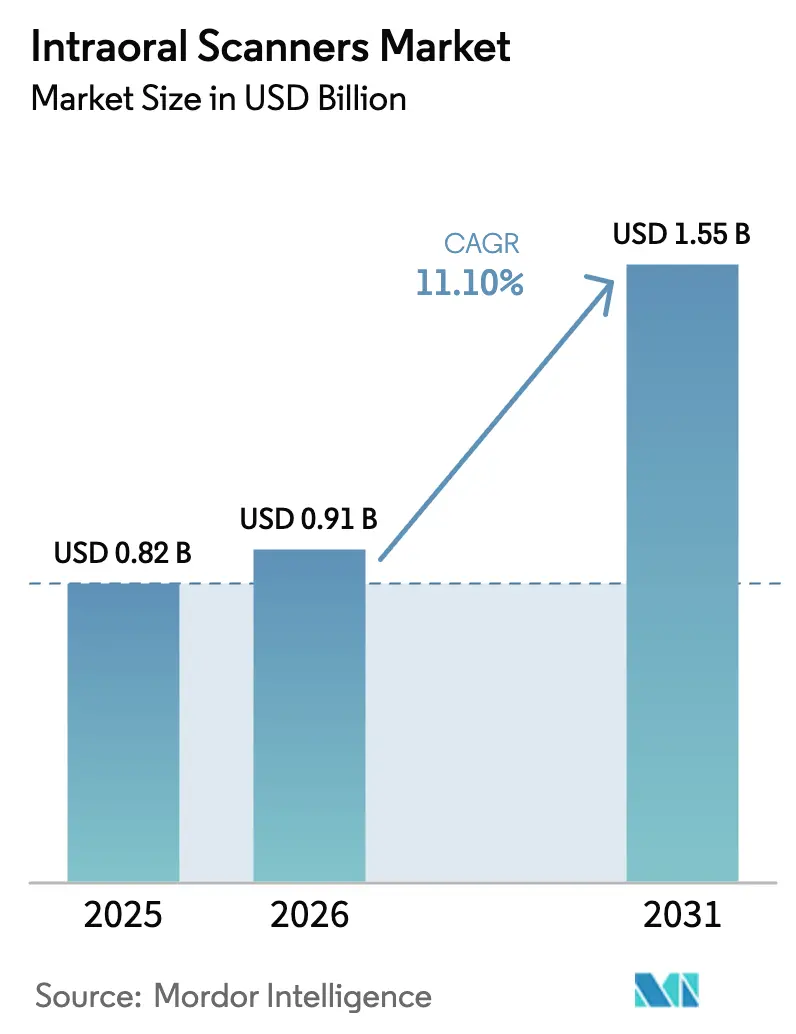

| Market Size (2026) | USD 0.91 Billion |

| Market Size (2031) | USD 1.55 Billion |

| Growth Rate (2026 - 2031) | 11.10% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Intraoral Scanners Market Analysis by Mordor Intelligence

The intraoral scanners market size is projected to be USD 0.82 billion in 2025, USD 0.91 billion in 2026, and reach USD 1.55 billion by 2031, growing at a CAGR of 11.10% from 2026 to 2031. Dental practices are shifting from analog trays to digital impression capture that feeds directly into CAD/CAM milling, clear-aligner workflows, and guided surgery, streamlining treatment and opening new revenue channels. Powder-free optics dominate current demand because they shorten chair time, improve patient comfort, and integrate seamlessly with advanced AI stitching algorithms. Portable wireless units are gaining traction among solo practitioners and mobile clinics, while hospitals and large DSOs continue to favor stand-alone carts that support high scan throughput. Regionally, North America leads in reimbursement clarity and early adoption; however, the Asia-Pacific region offers the steepest growth trajectory, as China and India accelerate investment in digital health infrastructure.

Key Report Takeaways

- By type, powder-free systems captured an 85.00% revenue share of the intraoral scanners market in 2025 and are projected to advance at an 11.00% CAGR through 2031.

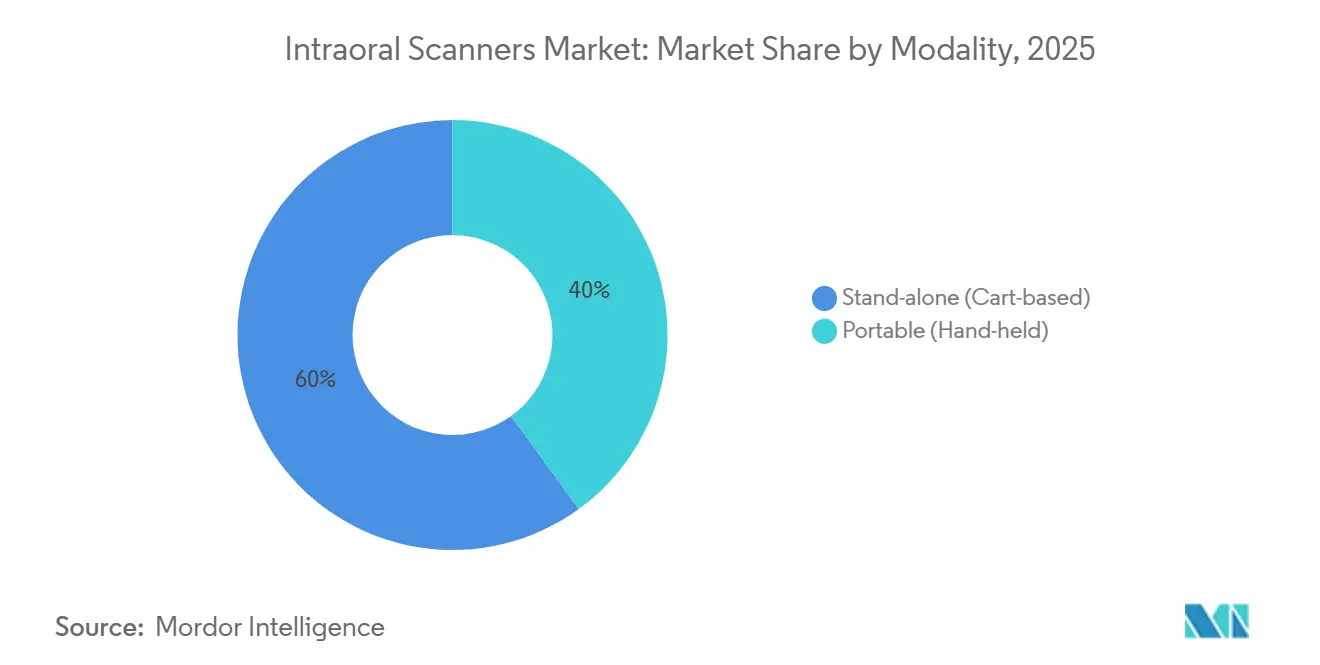

- By modality, cart-based scanners held a 60.00% market share of the intraoral scanners market in 2025, while portable handheld units are projected to grow at a 13.00% CAGR through 2031.

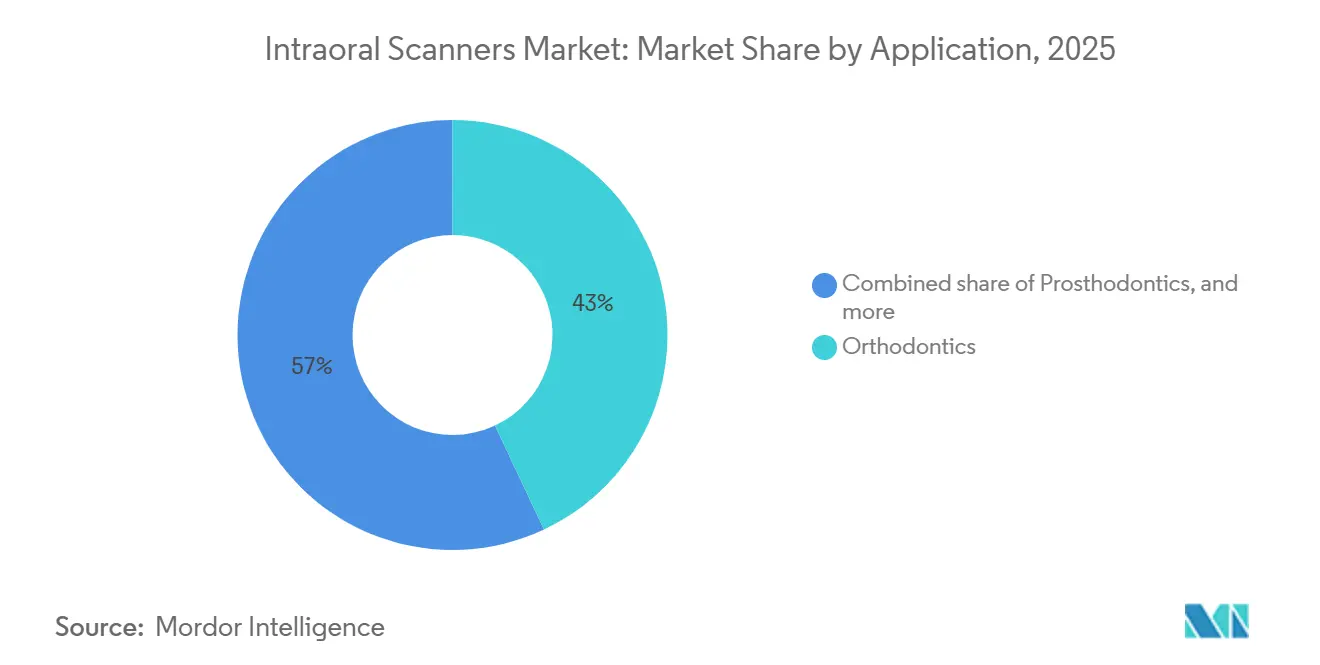

- By application, orthodontics led the intraoral scanners market, accounting for 43.00% of the market size in 2025; implantology is forecast to expand at a 14.30% CAGR through 2031.

- By end user, hospitals accounted for a 55.00% share of the intraoral scanners market size in 2025, whereas dental clinics are expected to record the fastest CAGR of 13.80% from 2026 to 2031.

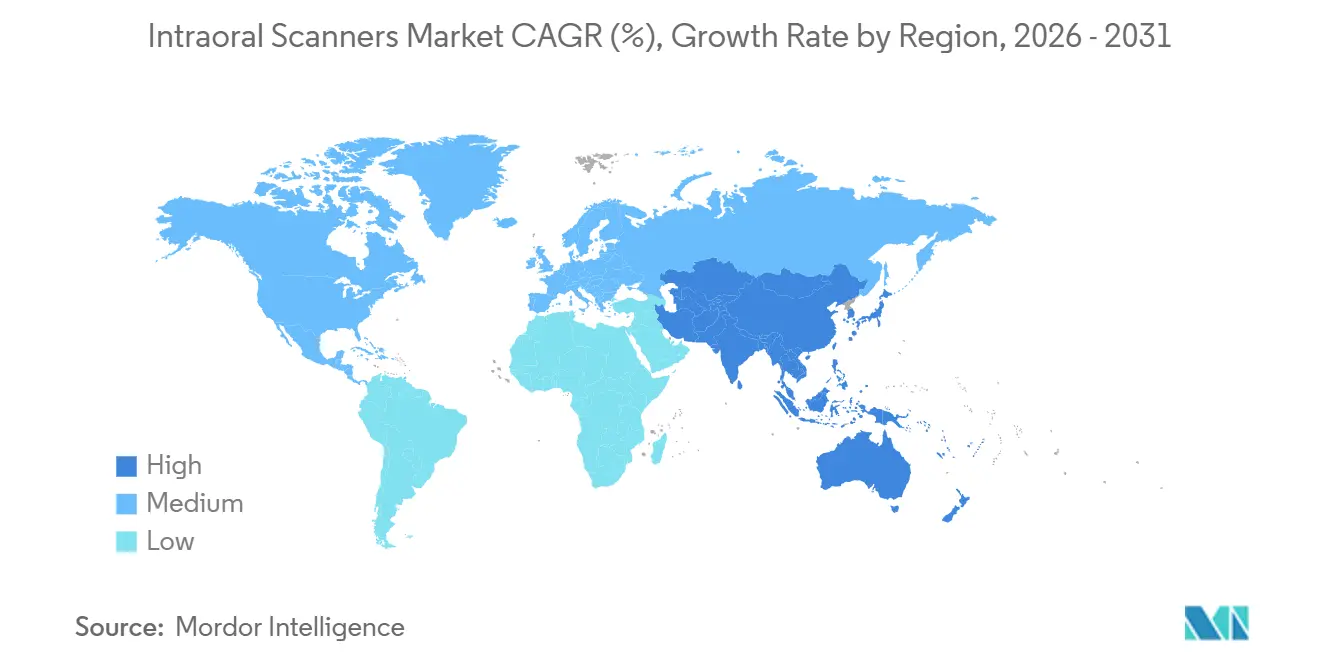

- By geography, North America retained a 42.20% share of the intraoral scanners market in 2025, and the Asia-Pacific region is expected to grow at a 12.80% CAGR from 2065 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Intraoral Scanners Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital dentistry and CAD/CAM workflows | +3.2% | Global, strongest in North America and Western Europe | Medium term (2-4 years) |

| Demand for cosmetic and aesthetic procedures | +2.1% | Urban centers in North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Improvements in scan speed, accuracy, AI | +2.8% | Global | Medium term (2-4 years) |

| Expansion of teledentistry | +1.9% | North America, Europe, Australia, emerging Asia-Pacific | Short term (≤ 2 years) |

| Flexible financing and subscription models | +2.4% | Global, most impactful in Asia-Pacific and Latin America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Adoption of Digital Dentistry and CAD/CAM Workflows

The turnaround time for crown delivery has dropped from weeks to same-day service, enabling high-volume clinics to capture incremental revenue and reduce patient attrition.[1]Health Policy Institute, “2024 Survey of U.S. Dental Practices,” Ada.org United States scanner penetration reached 62% of practices in 2024, driven by lab mandates that now require STL submissions and by orthodontic simulation software that operates exclusively on digital impressions. Global laboratories, such as Glidewell, received 78% of the 2025 crown orders as STL files, forcing late adopters to digitize or risk losing key lab relationships. Clear-aligner ecosystems also make scanners a virtual prerequisite, further integrating devices into routine workflows.

Increasing Demand for Cosmetic and Aesthetic Dental Procedures

Urban clinics report a surge in veneer and bonding cases as patients expect rapid visualizations of smile outcomes. Digital mock-ups generated directly from intraoral scans increase elective consultations at higher rates and enable providers to command fee premiums of more than 20%. Social-media-driven image consciousness drives younger demographics to seek minimally invasive restorations, pressuring practices to invest in scanners that deliver chairside previews within a single visit. Growth remains skewed towards high-income metros, while rural demand remains nascent.

Technological Improvements in Scan Speed, Accuracy, and AI Automation

Next-generation hardware reduced full-arch capture times to below 40 seconds, while real-time AI stitching cuts rescans to single-digit percentages. Integrated near-infrared imaging enhances diagnostic capabilities for caries detection, creating new billing codes and accelerating the return on investment. Performance convergence between entry-level and flagship models is narrowing hardware differentiation, making bundled software ecosystems the primary battleground among vendors.

Growth of Teledentistry and Remote Treatment Planning

Government reimbursement extensions for virtual care ensure that remote consultations remain billable when accompanied by encrypted scan uploads. In Australia and parts of the United States, regulators now require calibrated intraoral scans for orthodontic treatment plans submitted remotely, thereby increasing demand for cemented devices in rural outreach programs. Connectivity constraints persist in low-bandwidth regions, but portable scanners are helping mobile units reach underserved populations.

Restraints Impact Analysis of Intraoral Scanners Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital expenditure and ownership cost | −2.1% | Global, most acute in emerging markets and small practices | Short term (≤ 2 years) |

| Proprietary file formats and interoperability | −1.4% | Global | Medium term (2-4 years) |

| Cybersecurity and bandwidth limitations | −0.9% | Rural areas worldwide, low-infrastructure markets | Medium term (2-4 years) |

| Limited reimbursement outside mature regions | −1.6% | Asia-Pacific (ex-Japan, Korea), Latin America, Middle East & Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Initial Capital Expenditure and Total Cost of Ownership

Entry pricing starts at around USD 15,000 and can exceed USD 50,000 when bundled with advanced diagnostics, representing up to 100% of a median U.S. dentist’s net income[2]“American Dental Association CDT Code Guide,” Ada.org. Add-on software, disposable tips, and service contracts lift total ownership costs, lengthening payback periods for low-volume clinics. Tariffs and financing rates raise effective prices in lower-income markets, further deterring adoption.

Limited Interoperability and Proprietary File Formats Across Scanner Ecosystems

Despite common STL exports, embedded metadata often degrades outside native platforms, forcing users to adopt multiple subscriptions or accept reduced functionality. File-conversion errors lengthen chair time and erode workflow gains. Open-format alliances exist, but they remain voluntary, and market leaders hesitate to dilute their ecosystem lock-in advantages.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Intraoral Scanners Market Segment Analysis

By Modality:

Portability Gains Ground Despite Cart DominanceCart systems controlled 60.00% of the intraoral scanners market in 2025 because centralized stations lower per-chair capital cost in multi-operatory settings. Portable hand-held units are forecast to rise at a 13.00% CAGR as mobile dentistry and tight urban real estate prioritize space savings. The intraoral scanners market size tied to portable models is projected to reach USD 0.73 billion by 2031, driven by wireless operation times exceeding 90 minutes per charge. Yet implantologists still favor carts for superior thermal management and higher scan fidelity, thereby maintaining modality diversity.

Hybrid designs blur the line: detachable handpieces that shift between wired and wireless modes help practices optimize for case complexity without making duplicate purchases. Hospitals and teaching institutions still prefer tethers for network security, indicating a stable dual-modality landscape through the forecast horizon.

By Type:

Powder-Free Dominance Reflects Workflow EfficiencyPowder-free optics accounted for 85.00% of the revenue in 2025 and mirrored overall growth with an 11.00% CAGR. Eliminating titanium dioxide dust reduces scan times, enhances patient comfort, and eliminates the inhalation risk flagged under European chemical regulations. Powder-based devices primarily reside on resold secondary markets and in specialty use cases that require reflective-surface compensation. As AI-controlled exposure improves, even those niches are shrinking. By 2030, analysts expect powder-based share to dip below 5%, effectively consolidating the category into a single dominant technology.

By Connectivity:

Wireless Adoption AcceleratesWired units still comprise 90% of the installed base, yet wireless scanners are growing at a 14.50% CAGR, driven by Wi-Fi 6E and 5G. Construction savings of up to USD 1,200 per operatory attract new clinics, while cable-free ergonomics enhance infection control. Hospital IT policies that block Wi-Fi devices slow uptake in institutional settings, so wired models will remain relevant for the foreseeable future. Vendors now bundle dedicated routers that operate on isolated channels, mitigating interference and security worries for smaller clinics.

By Application:

Implantology Outpaces OrthodonticsOrthodontics contributed 43.00% of the intraoral scanners market share in 2025 as clear-aligner workflows rely exclusively on digital impressions. Implantology is projected to grow at a faster rate of 14.30% CAGR to 2031, as merging real-time scan data with CBCT enables flapless placement and surgical guide fabrication, which reduces chair time by up to 40%. Growth is contingent upon complementary CBCT investment; however, high implant volumes in aging populations support strong demand.

By End User:

Dental Clinics Gain ShareHospitals retained 55.00% of the intraoral scanner market share in 2025 due to centralized capital budgets and higher reimbursement rates. Dental clinics, however, are accelerating at a 13.80% CAGR as DSOs standardize scanners across extensive networks, leveraging subscription pricing to reduce upfront cash outlay. The shift will elevate clinics to nearly match hospitals in absolute unit demand by 2031, although hospitals will continue to command premium configurations tied to complex cases.

Geography Analysis

North America Intraoral Scanners Market

North America captured 42.20% of 2025 revenue, propelled by FDA 510(k) regulatory clarity and private insurance codes that reimburse digital impressions. Market penetration surpassed 60%, transitioning regional focus from first-time purchases to replacement cycles and AI-powered software upgrades. Canada trails the United States but is narrowing the gap as provincial insurers pilot digital-impression reimbursement schemes.

APAC Intraoral Scanners Market

The Asia-Pacific region is the fastest-growing, with a 12.80% CAGR. China’s State Council is expanding the dental base and mandating modern diagnostic capabilities, while India’s private chains deploy a scanner network-wide to capture in-house lab fees[3]. Penetration is over 50% in Japan and South Korea, thanks to national health insurance support. Price sensitivity and fragmented regulation continue to limit uptake in Southeast Asia; however, targeted financing and subscription models are helping to close the affordability gap.

Europe Intraoral Scanners Market

Europe holds a roughly 30% share with strong adoption in Germany, the U.K., and Scandinavia. The EU Medical Device Regulation has raised compliance costs, but cross-border dental tourism motivates Central European clinics to invest in scanners and improve signal quality to attract incoming patients. Southern Europe remains slower due to lower spending power, though targeted subsidies in Italy and Spain are starting to encourage digital upgrades.

MEA and South America Intraoral Scanners Market

Middle East & Africa and South America each represent under 8% of sales but feature high-growth urban clusters. Government-backed clinics in the UAE and Saudi Arabia are adopting scanners to align with global best practices. In contrast, the Latin American uptake is centered in Brazil’s private sector, despite tariff-driven price premiums.

Competitive Landscape

The top three players, 3Shape, Align Technology, and Dentsply Sirona, collectively held approximately 55.00% of the intraoral scanners market share in 2025, indicating moderate market concentration. Each leverages proprietary software to lock in customers: TRIOS 5 bundles Implant Studio, iTero integrates with Invisalign, and Primescan requires DS Core for full functionality. Challenger brands MEDIT and Shining 3D undercut incumbents on price and promote open STL exports, winning share in cost-sensitive segments. Subscription models reduce switching friction, intensifying performance-based rivalry and prompting vendors to expand their training and support offerings.

Patent filings highlight a pivot from hardware innovation to AI-driven software. In 2024, the top three firms filed 47 U.S. patents on machine-learning algorithms for automatic margin detection and artifact correction. White space remains in the pediatric and geriatric niches, where smaller tips and ruggedized housings can open up new demand.

Intraoral Scanners Industry Leaders

3Shape A/S

Align Technology, Inc.

Dentsply Sirona Inc.

Planmeca Oy

MEDIT Corp.

- *Disclaimer: Major Players sorted in no particular order

Intraoral Scanners Market Companies Covered in this Report

- 3 Shape

- Align Technology

- Condor Technologies NV

- Densys Ltd.

- Dentsply Sirona

- GC Corporation

- Guangdong Launca Medical Device Tech Co., Ltd.

- Straumann Group

- Ivoclar Vivadent

- MEDIT Corp.

- Owandy Radiology

- Planmeca

- Shining 3D Tech Co., Ltd.

- Vatech Co., Ltd.

- Zimmer Biomet

Recent Industry Developments in Intraoral Scanners Market

- November 2025: Shining 3D Dental launched the Aoralscan Elf, emphasizing its status as one of the lightest intraoral scanners at just 106 grams. This new model builds on the technology of the previous Aoralscan Elite series, targeting a different market segment with a price point around USD 12,000. The launch expands Shining 3D's lineup, aiming to broaden its reach in the dental scanning industry.

- October 2025: Dandy, a fully digital dental lab in New York City, introduced the Dandy Vision intraoral scanner. The device enhances scanning speed, accuracy, and clarity by leveraging AI-powered analysis and advanced optics. This innovation aims to improve efficiency and precision in dental workflows.

- July 2025: Medit introduced the i900 Mobility, a new intraoral scanner designed for versatile use in various treatment settings. The device supports wireless scanning and easy setup, making it suitable for multi-chair practices, chairside, and mobile care. This advancement enhances flexibility and efficiency in dental workflows.

Intraoral Scanners Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the intraoral scanners market as all new, factory-built digital devices that capture three-dimensional images of teeth and gingival tissues inside the mouth, streaming these data to CAD/CAM or cloud platforms for diagnosis and restorative workflows. According to Mordor Intelligence, values are reported in USD at the manufacturer selling price level and cover stand-alone cart systems as well as portable hand-held units that operate on optical or confocal imaging.

Scope Exclusion: The sizing excludes intraoral cameras, radiographic sensors, impression materials, and any refurbished or rental scanners.

Segments Covered in This Report

- By Modality

- Stand-Alone (Cart-Based)

- Portable (Hand-Held)

- By Type

- Powder-Free

- Powder-Based

- By Connectivity

- Wired

- Wireless

- By Application

- Orthodontics

- Prosthodontics

- Implantology

- Other Applications

- By End User

- Dental Clinics

- Hospitals

- Other End Users

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle-East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Primary Research

Mordor analysts interviewed practicing dentists, dental-lab managers, regional distributors, and product trainers across North America, Europe, and Asia-Pacific. These conversations validated unit penetration, learning-curve barriers, and true ASP erosion that secondary sources only hint at.

Desk Research

We first built a knowledge base from open, authoritative sources such as the US Centers for Medicare & Medicaid Services, Eurostat trade codes for "dental instruments," national dental association fee surveys, and patent analytics from Questel. Industry journals, FDA 510(k) filings, and company 10-Ks helped us benchmark shipments, average selling prices, and replacement cycles. Supplementary insights were accessed through D&B Hoovers and Dow Jones Factiva for financial signals. The sources listed illustrate, not exhaust, the wide set consulted by Mordor analysts; many more aided data checks and clarification.

Market-Sizing & Forecasting

Top-down reconstruction began with yearly production and import-export records for scanners, which were then adjusted for average distributor mark-ups to reach end-market value. Bottom-up cross-checks sampled supplier roll-ups and channel checks tightened totals. Key variables modeled include chairside CAD/CAM adoption, scanner replacement interval, orthodontic case volumes, per-capita dental expenditure, and regulatory approvals. A multivariate regression blended with scenario analysis projects each variable through 2030; anomalies are reconciled through expert re-contact before figures lock.

Data Validation & Update Cycle

Outputs pass a multi-step review that flags variance versus independent trade data and prior editions. Reports refresh yearly, with interim updates triggered by material events such as major product launches or reimbursement changes, ensuring buyers always receive our latest view.

How Mordor Intelligence's Intraoral Scanners Market Size Compares to Other Published Estimates

Published estimates often diverge because firms choose different device mixes, price assumptions, and refresh cadences.

Key gap drivers include varying inclusion of accessories, use of end-user versus manufacturer pricing, differing CAGR assumptions for replacement demand, and the fact that Mordor updates its model annually while some peers carry older benchmarks.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 820 million (2025) | Mordor Intelligence | - |

| USD 600 million (2023) | Global Consultancy A | Uses 2023 base year and excludes portable systems |

| USD 641 million (2025) | Industry Platform B | Applies clinic purchase prices without deducting dealer margins |

| USD 708 million (2024) | Trade Journal C | Forecast based on scanner shipments only, omits software licensing revenue |

These contrasts show that Mordor's disciplined scope definition, dual-track modeling, and quicker refresh cadence deliver the balanced, transparent baseline decision-makers can depend on.

Key Questions Answered in the Report

What was the intraoral scanners market size in 2026?

It reached USD 0.91 billion and is projected to grow to USD 1.55 billion by 2031.

Which application area is expanding fastest?

Implantology leads with a 14.30% CAGR through 2031 due to integration with guided surgery systems.

How quickly are wireless intraoral scanners being adopted?

Wireless units are forecast to rise at a 14.50% CAGR as Wi-Fi 6E and 5G reduce latency and cabling costs.

Which region is growing the fastest for intraoral scanners?

Asia-Pacific is the fastest, advancing at a 12.80% CAGR thanks to China and India's investment in digital dentistry.

Why do dental clinics increasingly invest in intraoral scanners?

Subscription pricing removes large upfront costs and DSOs use bulk procurement to standardize equipment, driving a 13.80% CAGR among clinics.

Page last updated on: