Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 10.06 Billion |

| Market Size (2026) | USD 10.42 Billion |

| Market Size (2031) | USD 12.44 Billion |

| Growth Rate (2026 - 2031) | 3.61% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Cane Sugar Market Analysis by Mordor Intelligence

The China cane sugar market size is expected to grow from USD 10.06 billion in 2025 to USD 10.42 billion in 2026 and is forecast to reach USD 12.44 billion by 2031 at 3.61% CAGR over 2026-2031. The market continues to face structural supply deficits, as domestic production is limited to 11.0 million metric tons, while consumption reaches 15.6 million metric tons, creating a reliance on imports to cover the 4.6 million metric ton shortfall. Guangxi, Yunnan, and Guangdong remain the primary production regions; however, mechanization rates are below 6%, which restricts yield improvements despite the adoption of high-sucrose sugarcane varieties. To support domestic refiners, the government has increased the Most Favored Nation (MFN) tariff on sugar syrups to 20%, addressing the surge in liquid imports that exceeded 2.1 million metric tons in the marketing year 2023/24. Furthermore, specialty and organic sugars are growing at a faster pace compared to the overall market, driven by urban consumers who are willing to pay a premium for traceable products. At the same time, demand for liquid syrups is rising in the beverage and dairy industries due to their faster dissolution properties.

Key Report Takeaways

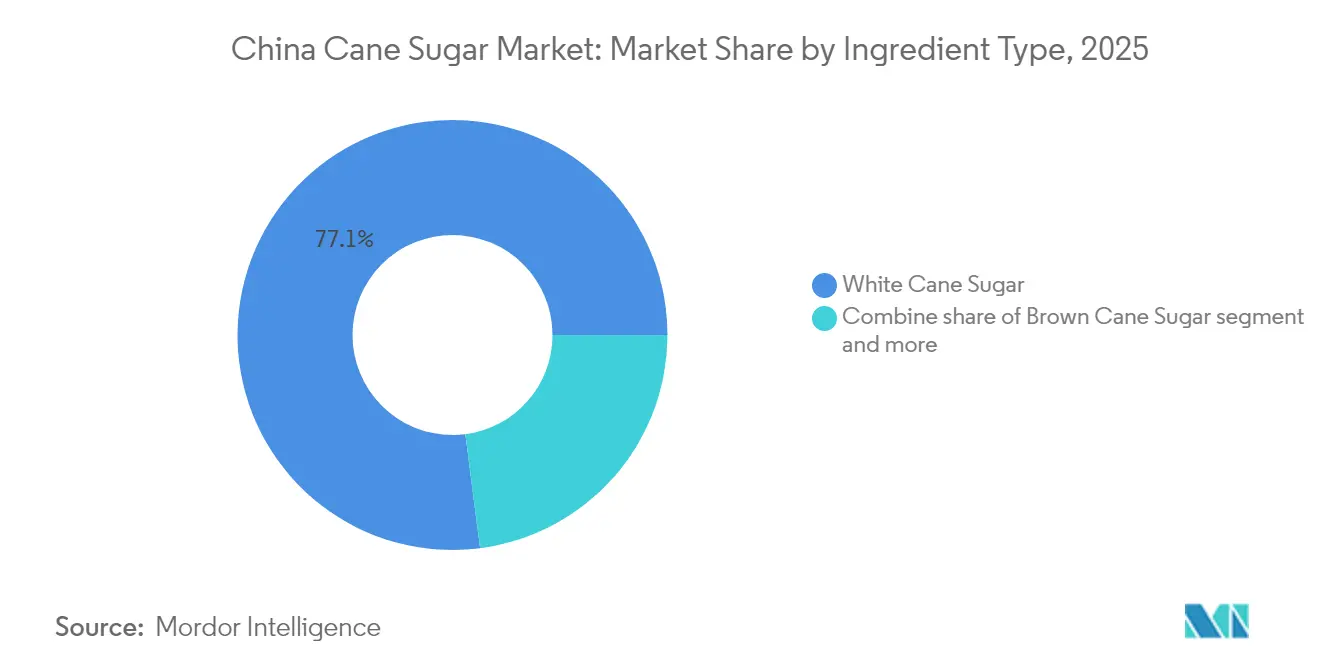

- By ingredient type, white cane sugar led with 77.05% of China cane sugar market share in 2025, whereas brown sugar is projected to expand at a 4.69% CAGR to 2031.

- By category, the conventional segment accounted for 84.05% of the China cane sugar market size in 2025, while organic sugar posts the fastest 4.87% CAGR through 2031.

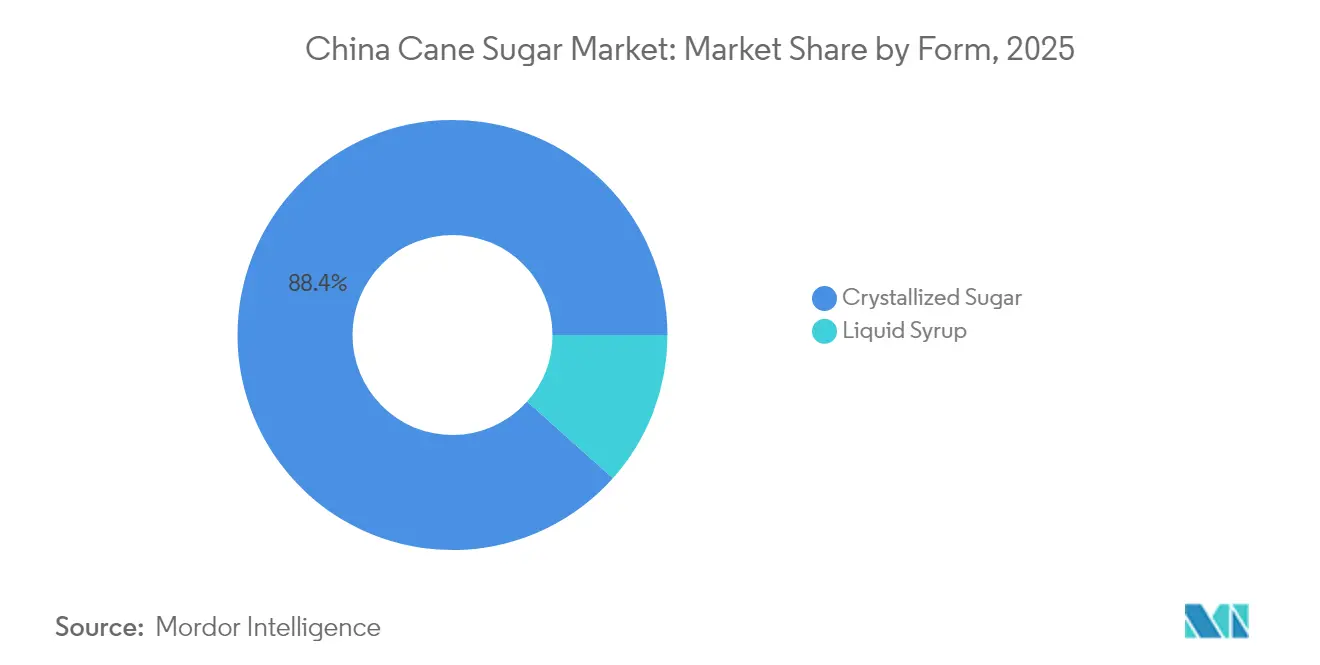

- By form, crystallized sugar commanded 88.40% share of the China cane sugar market size in 2025; liquid syrup is growing at a 4.32% CAGR to 2031.

- By application, bakery and confectionery captured 36.75% of China cane sugar market share in 2025 and is advancing at a 4.41% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Cane Sugar Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand from food and beverage industries | +0.8% | National, concentrated in coastal urban centers (Shanghai, Guangzhou, Shenzhen) | Medium term (2-4 years) |

| Technological advancements in cultivation and harvesting | +0.5% | Guangxi, Yunnan, Guangdong provinces | Long term (≥ 4 years) |

| Growing demand for specialty sugars and organic products | +0.6% | Tier-1 and Tier-2 cities nationwide | Medium term (2-4 years) |

| Sustainable farming practices gaining traction | +0.3% | Guangxi and Yunnan (major cane regions) | Long term (≥ 4 years) |

| Regional climate conditions favoring cane cultivation | +0.4% | Southern provinces (Guangxi, Yunnan, Guangdong, Hainan) | Short term (≤ 2 years) |

| Enhanced quality standards boosting consumer preference | +0.3% | National, with early gains in premium urban markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising demand from food and beverage industries

China's food processing market is anticipated to grow by 2.2% year-on-year in 2024, with the bakery segment expected to achieve an annual growth rate of 8.8%. By 2029, industrial users are projected to account for nearly two-thirds of the total sugar consumption, while household usage will make up the remaining portion [1]Source: USDA Foreign Agricultural Service, “Food Processing Ingredients – China,” USDA.gov. This creates a structural demand base that is less sensitive to price fluctuations compared to retail channels, as industrial users typically rely on sugar as a key input for consistent production processes. Beverage manufacturers are forecasted to expand their output by approximately 6% in 2025, driven by the increasing production of carbonated soft drinks and ready-to-drink (RTD) tea formulations. These beverages depend on sugar to achieve the desired balance of taste and texture, which are critical to consumer satisfaction. Additionally, the ongoing shift toward premiumization in the confectionery market, as demonstrated by Oreo's introduction of Zero variants that incorporate maltitol and dietary fiber as sugar substitutes, indirectly supports the demand for cane sugar in standard product lines. Manufacturers are strategically maintaining dual portfolios to address the diverse preferences of health-conscious consumers and those who continue to favor traditional options, ensuring they cater to a broad customer base.

Technological advancements in cultivation and harvesting

Precision agriculture tools are increasingly being adopted in China's fragmented sugarcane sector. In 2025, AI-powered disease recognition systems utilizing the XEffDa model achieved 97.62% accuracy, enabling farmers to detect diseases such as leaf scald and mosaic virus weeks earlier than traditional visual inspections. Automatic seed-cutting machines, equipped with IoT sensors and RGB cameras, now identify seed nodes with 95-100% precision and process up to 1,200 seeds per hour, addressing labor shortages that have hindered planting efficiency in Guangxi's smallholder-dominated landscape. BeiDou satellite-guided tractors and harvesters with machine vision are being piloted on larger estates; however, adoption remains primarily limited to state-owned mills and joint ventures due to high capital requirements. Additionally, new cane varieties, including GT66, LC05-136, and YZ05-51, offer 12-15% higher sucrose content and improved ratooning performance, extending replanting cycles from every 3-4 years to 5-6 years and reducing per-ton production costs by an estimated 8-10%.

Growing demand for specialty sugars and organic products

China's organic market benefits from 2.9 million hectares of certified organic farmland, which provides a robust foundation for the country's expanding role in the global organic industry. Organic sugar exports to the European Union (EU) and the United States (US) have been increasing as Chinese producers focus on capturing premium pricing opportunities in developed markets. Within the domestic market, the demand for brown sugar is growing at a faster rate compared to white sugar. This growth is primarily driven by consumer perceptions that less-refined products, such as brown sugar, offer higher mineral content and associated health benefits. These perceptions have been further strengthened by the influence of social media personalities and influencers who actively promote "natural" sweeteners, thereby shaping consumer preferences and increasing awareness of these products. Additionally, pharmaceutical-grade sucrose has emerged as a high-margin niche market that the China National Cereals, Oils and Foodstuffs Corporation (COFCO) is actively targeting. The company has made notable progress by establishing an injection-grade pharmaceutical sucrose pilot line and initiating the certification process for Good Manufacturing Practice (GMP) systems for excipients. Samples of this pharmaceutical-grade sucrose have already been distributed to several pharmaceutical clients, demonstrating COFCO's commitment to innovation and quality. Furthermore, COFCO's children's pharmaceutical sucrose has successfully received approval from China's Center for Drug Evaluation, achieving top-tier status for use in marketed formulations. Importantly, the impurity control standards for this product exceed the rigorous requirements outlined in the Chinese Pharmacopoeia, reflecting COFCO's dedication to surpassing industry standards.

Sustainable farming practices gaining traction

The majority of Chinese sugar mills use bagasse, the fibrous residue left after cane crushing, for cogeneration. This process generates electricity that meets a significant portion of the mills' energy needs, reducing their dependence on coal-fired power. The sugar industry has collectively committed to reducing carbon emissions substantially by 2030, using 2020 as the baseline year. Larger companies, such as China National Cereals, Oils and Foodstuffs Corporation and Guangxi Guitang, are actively investing in carbon audits and green power procurement to align with their Environmental, Social, and Governance (ESG) commitments. Vinasse, a byproduct of fermentation with high Biochemical Oxygen Demand, is increasingly being utilized as organic fertilizer on cane fields. Additionally, filter cake is applied as a soil amendment, recycling nutrients and reducing the use of chemical fertilizers on participating farms. China National Cereals, Oils and Foodstuffs Corporation achieved an AA rating from Wind ESG in 2025, marking its highest rating to date. This accomplishment reflects progress under its "SWEET" ESG strategy and the attainment of Ecovadis bronze certifications at multiple facilities. These initiatives contribute to reducing operating costs over time and improving compliance with environmental regulations, particularly in provinces with stricter enforcement. However, significant upfront capital requirements remain a considerable challenge for smaller mills.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Reduction of arable land due to urbanization | -0.5% | Guangxi, Yunnan, Guangdong (peri-urban zones) | Long term (≥ 4 years) |

| Inconsistent quality standards across regions | -0.3% | National, acute in smaller mills in inland provinces | Medium term (2-4 years) |

| Market volatility causing uncertain investment climate | -0.4% | National, affecting all producers and traders | Short term (≤ 2 years) |

| Tariffs and trade barriers affecting exports/imports | -0.3% | National, with spillover to ASEAN trade partners | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Reduction of arable land due to urbanization

Sugarcane cultivation in Guangxi and Yunnan is declining as urban expansion encroaches on traditional farming zones. Over recent years, the increasing value of peri-urban land has encouraged farmers to sell or lease their land for industrial and residential development. The National Development and Reform Commission's urbanization targets aim for seventy percent urban residency by 2030, up from approximately 65% percent in 2024, indicating a continued conversion of agricultural land [2]Source: National Development and Reform Commission, “Urbanization Policy Framework 2024-2030,” ndrc.gov.cn. Guangxi's sugarcane cultivation area reached its peak in the early 2010s but has since declined by an estimated 8 to 10 percent. However, productivity gains from new sugarcane varieties have partially mitigated the reduction in cultivated area. Smallholder farmers, who form the backbone of the sugarcane supply chain, are facing rising labor costs as rural wages steadily increase. Additionally, the farming population is aging, with the average sugarcane farmer now over 50 years old. While provincial governments have introduced land-use zoning policies to protect prime agricultural areas, enforcement remains inconsistent. Local officials often prioritize gross domestic product (GDP) growth over farmland preservation, complicating efforts to safeguard agricultural land. Looking ahead, China's sugarcane sector will need to achieve annual yield improvements of 2 to 3 percent to maintain current production levels. Meeting this target will require sustained investment in mechanization and agronomy, areas where progress has been limited so far.

Inconsistent quality standards across regions

Smaller mills in inland provinces often lack the financial resources to upgrade refining equipment, producing sugar that meets basic GB (Guobiao) standards but fails to meet the stricter specifications required by multinational food companies and pharmaceutical users. Variability in moisture content, which ranges from 0.05% to 0.15% among different producers, creates challenges in downstream processing for confectionery and bakery applications, where precise sugar-to-water ratios are essential for maintaining texture and shelf life. Additionally, color inconsistency, measured in International Commission for Uniform Methods of Sugar Analysis (ICUMSA) units, remains a recurring issue for mills using outdated clarification and filtration systems, limiting their ability to cater to premium market segments. Companies such as COFCO and Guangxi Guitang have invested in advanced technologies like online syrup sampling systems and near-infrared spectroscopy to enhance quality control. However, mid-tier producers often lack the scale to justify such investments. The fragmented supply base, which includes over 100 sugar mills in China, many operating below optimal capacity, further complicates efforts to enforce industry-wide standardization. This quality gap restricts export opportunities to markets such as Japan, South Korea, and Southeast Asia, where buyers demand traceability and consistent batch quality, which only a limited number of Chinese producers can reliably provide.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ingredient Type: White Sugar Anchors Volume, Brown Sugar Captures Premium Growth

White cane sugar accounted for 77.05% of the market share in 2025, highlighting its established role in industrial applications where color neutrality and consistent performance are prioritized over origin or processing methods. Brown cane sugar is projected to grow at a compound annual growth rate (CAGR) of 4.69% through 2031, marking the fastest growth within this segment. This growth is driven by health-conscious consumers who associate less-refined products with higher mineral content. Brown sugar contains two to three times more magnesium, potassium, and calcium compared to white sugar. Additionally, social media campaigns promoting the "natural" sweetener narrative have further supported this trend. The "Others" category, which includes raw sugar and specialty grades, caters to niche markets such as craft brewing and artisanal confectionery. However, it remains below 10% of the market due to limited distribution and higher unit costs.

White sugar's dominance is further supported by GB/T 317-2018 standards, which enforce strict tolerances for moisture, ash, and color. These standards make white sugar the preferred choice for pharmaceutical excipients and injection-grade formulations, where impurity control is critical. China National Cereals, Oils and Foodstuffs Corporation (COFCO) has developed pharmaceutical-grade white sugar that exceeds the impurity control requirements of the Chinese Pharmacopoeia. This innovation has created a high-margin market opportunity, with 59 pharmaceutical clients currently sourcing this specialized product from the company.

By Category: Conventional Dominates, Organic Surges on Export and Domestic Premiumization

Conventional sugar accounted for 84.05% of the market share in 2025, supported by cost advantages and the extensive scale of existing production infrastructure. However, organic sugar is anticipated to grow at a compound annual growth rate (CAGR) of 4.87% through 2031, marking the fastest growth within this segment.

China's organic farmland has expanded, with organic sugar exports to the European Union (EU) and the United States (US) increasing as Chinese producers target premium pricing in developed markets . Domestic demand for organic sugar is also rising, driven by urban millennials and Generation Z (Gen Z) consumers who value sustainability and traceability. These attributes command price premiums of 30 to 40 percent over conventional grades, according to user research data. Despite this growth, certification costs and the three-year transition period required for organic conversion remain significant barriers. These challenges limit participation to larger estates and cooperatives capable of absorbing the upfront expenses and revenue losses during the transition period.

By Form: Crystallized Sugar Leads on Versatility, Liquid Syrup Gains in Automated Lines

Ease of handling and faster dissolution rates are driving the Liquid Syrup market to a compound annual growth rate (CAGR) of 4.32% through 2031. At the same time, Crystallized Sugar is projected to retain an 88.40% market share in 2025 due to its widespread use in bakery, confectionery, and household applications. Beverage manufacturers, particularly those producing carbonated soft drinks and ready-to-drink coffee, prefer liquid syrup as it eliminates the dissolution step. This reduces production cycle times by 10-15% and minimizes undissolved particulates that could clog filling nozzles.

Dairy processors utilizing liquid sugar in ice cream and yogurt formulations report enhanced consistency and reduced batch-to-batch variability, as liquid sugar integrates more uniformly with milk solids and stabilizers. COFCO recorded a 41% year-on-year growth in small-pack crystallized sugar production during the first half of 2025, focusing on household and food-service channels where portion control and shelf stability are key priorities.

By Application: Bakery and Confectionery Leads and Accelerates, Beverages Face Reformulation Pressure

Bakery and Confectionery accounted for 36.75% of the market share in 2025 and is growing at a Compound Annual Growth Rate (CAGR) of 4.41% through 2031, the fastest rate within the application segmentation. This growth is driven by China's bakery market, which experienced an 8.8% annual increase in 2024 and is projected to grow further by 2029. Within this segment, cakes and pastries consume the largest sugar volumes due to their dependence on sugar for structure, moisture retention, and Maillard browning. Meanwhile, chocolates and candies require stricter specifications for particle size and color to ensure smooth textures and consistent coatings.

Beverages, the second-largest application, are undergoing reformulation pressures. Sugar-free tea, which previously experienced high growth, is now stabilizing. Additionally, 96% of food and beverage businesses in Asia have initiated or plan to implement sugar-reduction strategies, according to the Asia Food and Beverage Alliance. While carbonated drinks and fruit juices continue to use sugar as the primary sweetener, coffee and tea sweeteners are increasingly incorporating blends with stevia and erythritol to lower calorie content while maintaining sweetness intensity.

Geography Analysis

China's cane sugar production is concentrated in the southern provinces, with Guangxi contributing 60-70% of the national output, followed by Yunnan at 17% and Guangdong at 11%. This geographic concentration makes the supply base susceptible to regional weather conditions and policy changes. Guangxi's leading position is attributed to its subtropical monsoon climate, extensive irrigation infrastructure, and provincial government support. For example, the region allocated RMB 2 billion (USD 280 million) in subsidies for sugarcane farmers during 2024-2025 to stabilize incomes and encourage cultivation.

Yunnan's sugar production is growing due to favorable rainfall and the adoption of high-sucrose varieties such as YZ05-51. However, the province faces competition for arable land from coffee and rubber plantations, which offer higher returns per hectare. Consumption patterns vary significantly between coastal urban centers such as Shanghai, Guangzhou, and Shenzhen, where per capita sugar intake reaches 15-16 kilograms annually, and inland rural areas, where consumption remains below 8-9 kilograms. These differences reflect income disparities and varying levels of processed food consumption.

Provincial policy differences further complicate the market. Yunnan has implemented a floor price guarantee of RMB 550 (USD 77) per ton for sugarcane in 2024, providing farmers with income stability but potentially encouraging overproduction during high-price years. In contrast, Guangxi relies more on direct subsidies and input support. These differing approaches influence mill profitability and farmers' planting decisions. While the National Development and Reform Commission (NDRC) oversees sugar policy at the national level, enforcement of tariff-rate quotas and import licenses is decentralized, leading to inconsistent application across provinces and ports. Favorable weather conditions in Guangxi during the 2024/25 season boosted production to 11.0 million metric tons, up from 9.96 million metric tons in Marketing Year (MY) 2023/24. This highlights the sector's sensitivity to climatic factors and underscores the importance of investments in irrigation and drainage infrastructure.

Competitive Landscape

The China cane sugar industry exhibits moderate market consolidation, with key players such as state-owned COFCO and regional companies like Guangxi Guitang, Wilmar, and Louis Dreyfus holding significant production capacity. However, these companies face margin pressures due to volatile international sugar prices and competition from high-fructose corn syrup, which is priced at approximately one-third of white sugar. Strategic approaches in the industry focus on vertical integration and product differentiation. For instance, COFCO operates 13 domestic sugar mills across Guangxi and Yunnan, along with overseas assets in Australia, allowing the company to balance domestic production with import arbitrage. Additionally, COFCO is diversifying into pharmaceutical-grade and liquid sugar to mitigate the impact of commodity pricing.

Guangxi Guitang's acquisition of Laibin Dongmen Sugar Factory in 2024 highlights the trend of consolidation among provincial players aiming to achieve economies of scale and improve bargaining power with cane farmers. Similarly, Wilmar's 2024 acquisition of two sugar beet processing factories through IMHWA reflects a diversification strategy to reduce reliance on cane sugar, although beet sugar remains a minor component of its China portfolio.

Opportunities for growth exist in the pharmaceutical excipients segment. For example, COFCO's GMP certification for injection-grade sucrose and its children's pharmaceutical sucrose achieving "A" status with China's Center for Drug Evaluation demonstrate the potential for technical differentiation. These specialized products can command premiums of 40-50% over food-grade sugar, highlighting the value of innovation in this market.

China Cane Sugar Industry Leaders

COFCO Corporation

Tereos S.A.

Guangxi Feng Sugar Group Co., Ltd.

Guangxi Nanning Sugar Industry Co., Ltd.

Yunnan Yingfu Sugar Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Guangxi Sungain Sugar Industry Group advanced a green, diversified industrialisation blueprint in 2024/25, emphasizing mechanised planting, bagasse‑based power generation, and deeper processing of sugarcane by‑products to strengthen regional sugar competitiveness.

- December 2024: Guangxi mills expanded sugarcane cultivation to 11.35 million mu in the 2024/25 season, up 110,000 mu year-on-year. Regional government initiatives supporting acreage expansion and full-process mechanization drove growth, reinforcing Guangxi's position as China's leading sugar producer with 60% national market share.

- July 2024: COFCO Sugar’s new refinery in Zhangzhou Development Zone, Fujian, reportedly began operations at “record speed,” adding new refining capacity to China’s coastal sugar supply

China Cane Sugar Market Report Scope

The Chinese cane sugar market has been segmented by category into organic and conventional. The market is divided based on form into crystallized sugar and liquid sugar syrup. Based on the application, the market is segmented into bakery and confectionery, dairy, beverages, and other applications.

By Ingredient Type

| White Cane Sugar |

| Brown Cane Sugar |

| Others |

By Category

| Organic |

| Conventional |

By Form

| Crystallized Sugar |

| Liquid Syrup |

By Application

| Bakery and Confectionery | Cakes and Pastries |

| Cookies | |

| Candies | |

| Chocolates | |

| Others | |

| Dairy | Ice Cream |

| Yogurt | |

| Milkshakes | |

| Others | |

| Beverages | Carbonated Drinks |

| Fruit Juices | |

| Coffee and Tea Sweeteners | |

| Alcoholic Beverages | |

| Others | |

| Sauces and Condiments | |

| Savory Snacks | |

| Other Applications |

| By Ingredient Type | White Cane Sugar | |

| Brown Cane Sugar | ||

| Others | ||

| By Category | Organic | |

| Conventional | ||

| By Form | Crystallized Sugar | |

| Liquid Syrup | ||

| By Application | Bakery and Confectionery | Cakes and Pastries |

| Cookies | ||

| Candies | ||

| Chocolates | ||

| Others | ||

| Dairy | Ice Cream | |

| Yogurt | ||

| Milkshakes | ||

| Others | ||

| Beverages | Carbonated Drinks | |

| Fruit Juices | ||

| Coffee and Tea Sweeteners | ||

| Alcoholic Beverages | ||

| Others | ||

| Sauces and Condiments | ||

| Savory Snacks | ||

| Other Applications | ||

Key Questions Answered in the Report

What is the current value of the China cane sugar market?

The market is valued at USD 10.42 billion in 2026 and is projected to hit USD 12.44 billion by 2031.

Which segment leads demand within China’s cane sugar consumption?

Bakery and confectionery products lead, holding 36.75% share in 2025 and growing at a 4.41% CAGR.

How fast is organic sugar growing in China?

Organic sugar is expanding at a 4.87% CAGR through 2031, outpacing conventional categories.

What tariff change affected liquid sugar imports in 2025?

China raised the MFN tariff on sugar syrups and premixes from 12% to 20% in January 2025.

Page last updated on: