Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

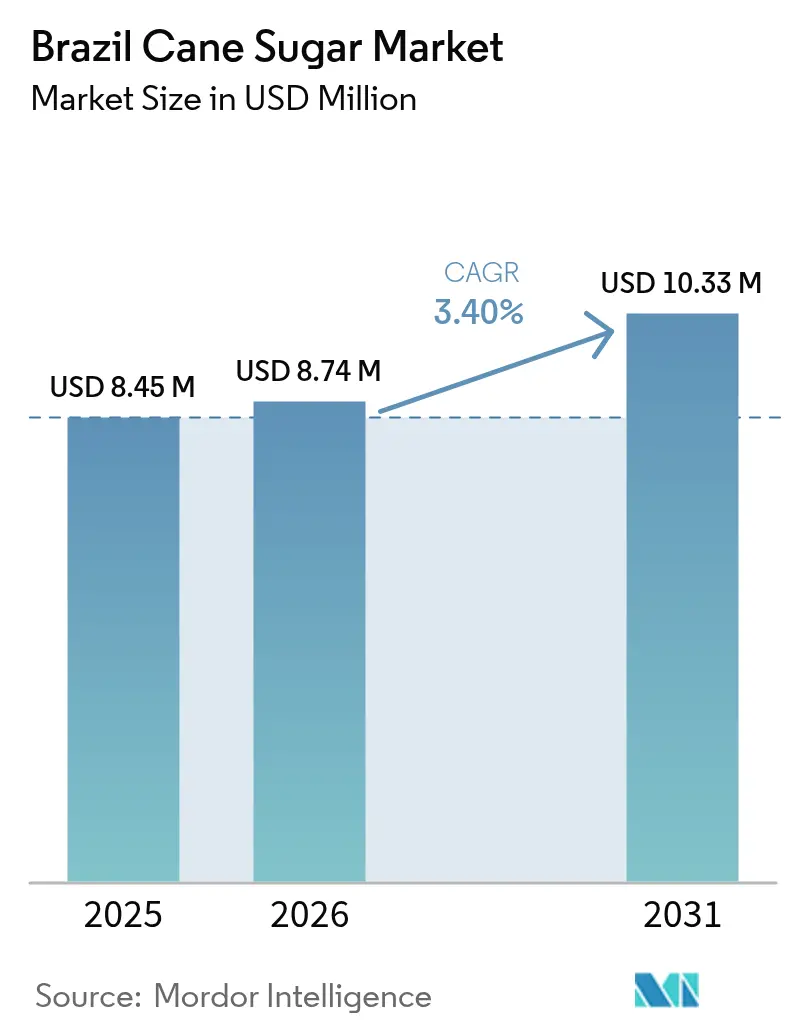

| Base Year Market Size (2025) | USD 8.45 Million |

| Market Size (2026) | USD 8.74 Million |

| Market Size (2031) | USD 10.33 Million |

| Growth Rate (2026 - 2031) | 3.40% CAGR |

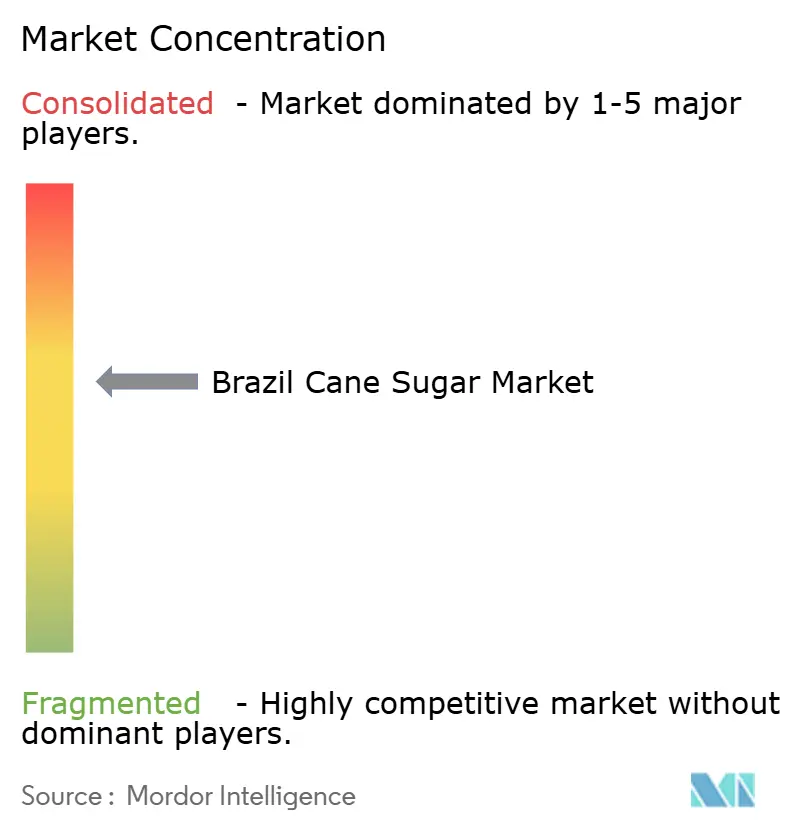

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Brazil Cane Sugar Market Analysis by Mordor Intelligence

The Brazil cane sugar market size is expected to grow from USD 8.45 billion in 2025 to USD 8.74 billion in 2026 and is forecast to reach USD 10.33 billion by 2031 at 3.40% CAGR over 2026-2031. The steady headline growth hides an ongoing resource reallocation as ethanol blending mandates divert additional cane from crystal sugar toward biofuel output. The 30% gasoline–ethanol mix scheduled for 2025 underpins a fresh supply–demand balance that favors integrated sugar-ethanol plants. São Paulo’s dominant production base is facing land-cost pressures, permitting the Center-West states to lure new investments. Liquid sugar, premium organic certifications, and technology-enabled yield gains form the leading revenue-expansion themes. Foreign capital, illustrated by Cargill’s USD 518 million takeover of SJC Bioenergia, signals long-term confidence despite input-cost volatility

Key Report Takeaways

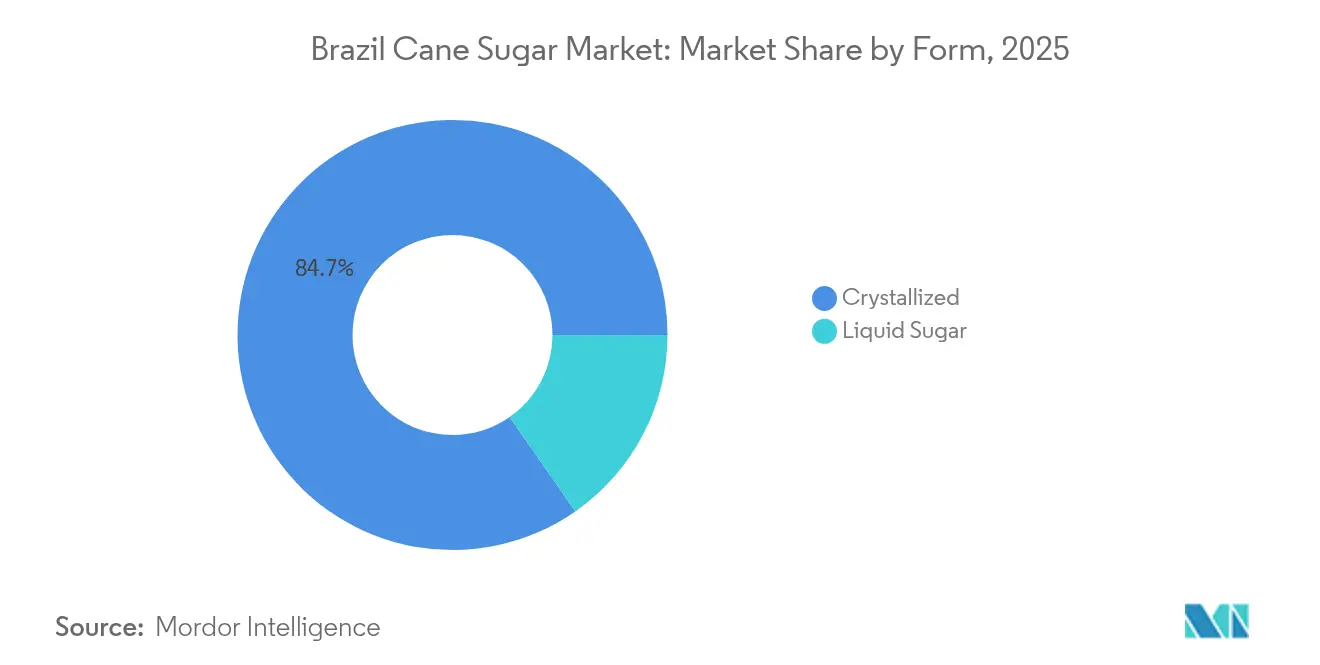

- By form, crystallized sugar led with an 84.68% Brazil cane sugar market share in 2025, while liquid sugar logged the fastest 4.34% CAGR for 2026-2031.

- By product category, raw sugar accounted for 52.85% of Brazil's cane sugar market share in 2025; organic and fair-trade variants are set to expand at a 5.03% CAGR through 2031.

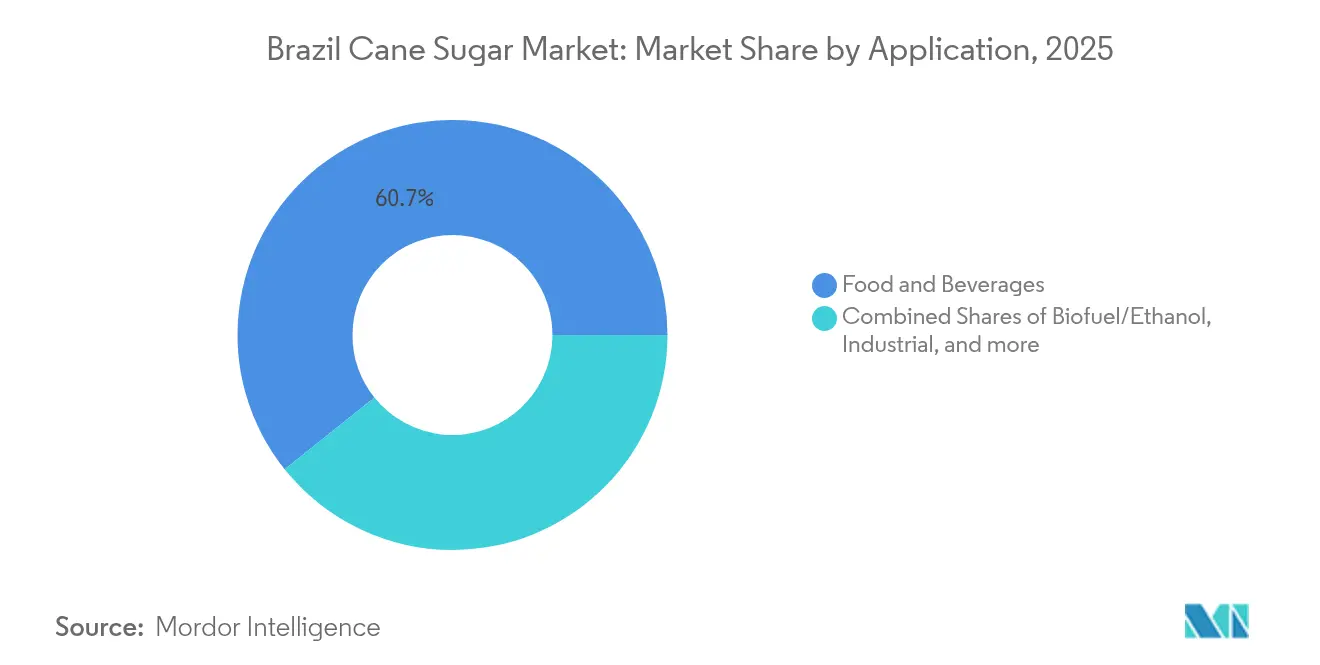

- By application, food and beverage retained a 60.74% share in 2025, whereas biofuel/ethanol demand is poised for a 4.48% CAGR.

- By state, São Paulo held a 48.75% share in 2025, but Goiás is projected to post the fastest 4.82% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Brazil Cane Sugar Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding ethanol blending mandates in Brazil | +1.2% | National, with concentrated impact in Center-South production regions | Short term (≤ 2 years) |

| Government Support and Policies | +0.8% | National, with enhanced benefits for Northeast and emerging regions | Medium term (2-4 years) |

| Advancements in Agricultural Technologies | +0.7% | São Paulo, Goiás, Minas Gerais core regions | Long term (≥ 4 years) |

| Strong Export Performance and Global Supply Role | +0.5% | Global, with primary benefits to Santos port corridor | Medium term (2-4 years) |

| Growing demand for non-GMO "native sugar" in craft beverages | +0.2% | North America, Europe export markets | Long term (≥ 4 years) |

| Expansion into New Applications and Markets | +0.3% | Asia-Pacific markets, domestic industrial applications | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expanding Ethanol Blending Mandates in Brazil

Brazil is set to boost its ethanol blending in gasoline from 27% to 30% by 2025. This move isn't just a minor policy tweak; it's reshaping the economics of sugarcane allocation throughout the production chain. With the Ministry of Mines and Energy confirming the technical feasibility of the E30 blend, Brazil is looking at an annual demand surge of 1.2 to 1.4 billion liters for anhydrous ethanol. This surge effectively sidelines an equivalent amount of sugar production capacity from the export market. Such a shift in demand underscores the growing biofuel applications, expanding at a rate of 4.56% annually, even as sugar has historically held sway. Notably, the timeline for this mandate aligns with Brazil's ambitious decarbonization goals under the RenovaBio program. With a target of 50 billion liters of ethanol production by 2030, Brazil is poised for a significant overhaul of its sugarcane supply chain.

Government Support and Policies

Federal and state-level support programs are evolving, moving beyond traditional agricultural subsidies to embrace initiatives that drive technological transformation and reshape competitive dynamics. Through the Plano Safra program, international players like BP Bunge have tapped into USD 1.24 billion in investments. Notably, BP Bunge's USD 98.17 million expansion in Tocantins boosts its milling capacity by 30%, reaching an annual total of 3.4 million tonnes. However, the establishment of a new regulatory framework for bioinsumos under Law No. 15.070/2024 stands out as a more strategic move. This framework streamlines the registration of biological inputs and curtails reliance on imported chemical fertilizers. Such regulatory advancements give Brazil a leg up, sidestepping the bureaucratic hurdles prevalent in U.S. and European markets. This not only offers Brazil a competitive edge but also aligns with sustainable production methods that fetch premium prices in export markets.

Advancements in Agricultural Technologies

The Sugarcane Technology Center (CTC) has announced groundbreaking advancements that could generate USD 111.14 billion in economic value through new sugarcane varieties and biotechnology platforms. The Advana varieties developed by CTC exhibit up to 16% higher productivity compared to existing cultivars, offering a significant leap in yield optimization. Additionally, the VerdePro2 biotechnology platform facilitates the stacking of traits, which enhances disease resistance and glyphosate tolerance, ensuring better crop resilience. Furthermore, the synthetic seed project currently under development is poised to transform planting practices by improving efficiency and significantly reducing establishment costs. This innovation directly addresses labor shortages, a critical challenge that has limited expansion in emerging regions. These technological advancements are particularly crucial as Brazil aims to increase sugarcane productivity from 75 tonnes per hectare to 100 tonnes per hectare by 2040. Notably, this ambitious target is set to be achieved without expanding the planted area, thereby supporting the country’s domestic ethanol production goals while maintaining its competitive position in export markets.

Strong Export Performance and Global Supply Role

In 2024, Brazil's sugar export revenue soared to USD 10.74 billion. Notably, April alone saw exports surge to a record 1.89 million tonnes—a staggering 94.7% jump from the prior year. This uptick underscores the sector's resilience amidst global supply chain upheavals. Data from the Observatory of Economic Complexity[1]Observatory of Economic Complexity, " Raw Sugar in Brazil Trade", www.oec.world in 2024 highlighted that Brazil's raw sugar exports were valued at a substantial USD 18.6 billion. Santos, responsible for 75% of Brazil's sugar exports, grapples with port infrastructure constraints, leading to bottlenecks during the peak shipping season from March to September. However, northern ports are stepping in, with expanding logistics solutions to alleviate these pressures. Holding a commanding 40% share of the global sugar export market, Brazil wields significant pricing power. This advantage helps counterbalance domestic production cost fluctuations, especially as international sugar prices remain buoyed by supply disruptions in rival regions.

Restraints Impact Analysis*

| Restraints | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Production Costs | -0.9% | National, with acute impact in high-input regions | Short term (≤ 2 years) |

| Impact of Sugar Tax Policies | -0.3% | Global export markets, domestic consumption | Medium term (2-4 years) |

| Sustainability and Environmental Concerns | -0.4% | Amazon and Pantanal border regions | Long term (≥ 4 years) |

| Increasing Competition from Alternative Sweeteners | -0.5% | Domestic and North American markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Production Costs

Sector profitability is under pressure due to rising input costs, particularly in fertilizers and mechanization. Fertilizer prices have increased by up to 96.4% in key producing regions, while mechanization costs have jumped by 110%. Labor costs, which constitute 34% of operational expenses in some areas, are climbing due to mechanization transitions and a shortage of rural labor. Energy costs for processing operations remain volatile, influenced by fluctuations in oil prices. This creates a hedging challenge for mills as they balance ethanol and sugar production ratios. Although the depreciation of the Brazilian real enhances export competitiveness, it also raises the cost of imported inputs, such as specialized machinery and chemicals. To address these challenges, mills are implementing vertical integration strategies and securing long-term supply contracts. However, smaller producers are experiencing margin compression, which could accelerate industry consolidation.

Impact of Sugar Tax Policies

Sugar tax policies in Brazil pose a significant restraint on the cane sugar market primarily due to their potential to reduce domestic sugar consumption. The Brazilian government has introduced and adjusted taxes on sugar-sweetened beverages (SSBs) multiple times, reflecting a complex regulatory environment. While some tax rates on SSBs have been decreased in the past, recent measures indicate a trend toward increasing excise taxes to curb sugar intake for public health reasons. These taxes, especially excise taxes that target high sugar content products, create financial disincentives for consumers to purchase sugary beverages, thereby potentially reducing demand for sugar derived from cane.Moreover, the presence of tax policies specifically aimed at reducing sugar consumption—backed by regulations such as advertising restrictions and prohibitions on sales of sugary drinks in schools—limits market growth opportunities for the cane sugar industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Crystallized Dominance Faces Processing Evolution

Crystallized sugar's commanding 84.68% market share in 2025 reflects Brazil's export-oriented production strategy and established processing infrastructure optimized for bulk commodity handling. However, liquid sugar applications are expanding at 4.34% annually through 2031 as food manufacturers seek to reduce processing steps and improve operational efficiency in beverage and confectionery production. The shift toward liquid forms is particularly pronounced in the domestic market, where proximity to end-users enables just-in-time delivery systems that reduce inventory costs. Industrial applications increasingly favor liquid sugar for its consistent quality parameters and reduced handling requirements, though crystallized forms maintain advantages in export logistics and storage stability.

Technological innovations in liquid sugar production, including advanced filtration and concentration systems, are enabling mills to capture higher margins through value-added processing. The integration of liquid sugar production with ethanol facilities creates operational synergies that optimize resource utilization during seasonal production cycles. Smaller regional producers are investing in liquid sugar capabilities to differentiate their offerings and establish direct relationships with food manufacturers, bypassing traditional commodity trading channels that compress margins.

By Product Category: Raw Sugar dominates the market, while organic sugar emerges

Raw sugar maintains 52.85% market share in 2025, reflecting Brazil's strategic positioning as the world's primary supplier to global refining operations. This commodity-focused approach provides volume stability and currency hedging benefits through international pricing mechanisms, yet limits value capture compared to refined product alternatives. White refined sugar serves primarily domestic and regional markets, where consumer preferences and regulatory requirements favor processed products. VHP (Very High Polarization) sugar represents a quality premium segment that commands higher prices in specific export markets requiring enhanced purity levels.

The organic segment's 5.03% growth rate through 2031 signals emerging opportunities in premium positioning, particularly for mills pursuing sustainability certifications like Bonsucro and Fair for Life standards. These certifications enable access to European and North American markets where environmental and social governance requirements create barriers to entry for conventional producers. The premium segment's growth is constrained by certification costs and compliance requirements that favor larger, well-capitalized operations over smallholder producers.

By Application: Food Beverage Leadership Coexists with Biofuel Expansion

Food and beverage applications account for 60.74% market share in 2025, driven by Brazil's large domestic market and established export relationships with global food manufacturers. Within this segment, bakery and confectionery applications provide stable demand patterns, while beverage applications face increasing competition from alternative sweeteners and health-conscious consumer trends. Dairy and frozen food applications offer growth potential through product innovation and premium positioning strategies that leverage Brazil's reputation for agricultural quality.

Biofuel and ethanol applications are expanding at 4.48% annually, reflecting the structural demand shift created by ethanol blending mandates and renewable energy policies. According to the Govrnment of Brazil data from 2023, ethanol and biodiesel production was 43 billion liters in Brazil. This growth rate accelerates as mills optimize their sugar-ethanol production mix based on relative pricing and government incentives. Pharmaceutical applications represent a smaller but high-margin segment that requires specialized processing capabilities and regulatory compliance. Industrial applications, including chemical feedstock uses, provide diversification opportunities for mills seeking to reduce commodity price exposure through value-added processing strategies.

Geography Analysis

In 2025, São Paulo, with a 48.75% market share, continues to lead Brazil's cane sugar production. However, the state is encountering structural issues that are reshaping its competitive environment. Limited land availability and increasing environmental compliance costs are prompting established mills to enhance their current operations rather than pursue new expansions. São Paulo's strengths in processing expertise, research, and port access via Santos remain significant, but emerging regions are introducing cost structures that challenge its dominance. According to 2024 data from the United States Department of Agriculture, São Paulo remains Brazil's largest producer of cane sugar and ethanol, contributing 52% and 36% of the total production, respectively.

Goiás is emerging as a key growth area, with a projected 4.82% CAGR through 2031. This growth is driven by abundant arable land, a favorable climate, and strategic government support for agricultural development. Located in Brazil's Center-West, Goiás benefits from logistical advantages for domestic consumption and northern export routes that bypass the traditional bottlenecks at Santos. Investments in infrastructure, including transportation and processing facilities, are attracting both domestic and international stakeholders. New mills are focusing on integrated production models that combine sugar, ethanol, and energy. However, a sustainability assessment of sugarcane expansion in Goiás indicates medium-level environmental performance, highlighting opportunities for improvement through better management practices.

Minas Gerais, despite facing drought-related challenges, maintains its position as Brazil's second-largest cane sugar producer. The state expects a 7.1% decline in the 2025/26 harvest, reducing output to 77.2 million tonnes. To address this, Minas Gerais plans to expand its cultivated area by 9.8% to 1.23 million hectares, with a stronger emphasis on cane sugar production over ethanol. The Companhia Mineira de Açúcar e Álcool's R$3.5 billion investment commitment through 2033 reflects confidence in the region's long-term potential, aiming to boost production capacity and create 1,350 jobs. Meanwhile, Paraná and Mato Grosso do Sul are positioning themselves as emerging production centers through infrastructure improvements and technological advancements. The Northeast region, supported by improved rainfall and expanded cultivation, forecasts a 3.1% production increase for the 2023/24 harvest.

Regulatory Landscape

Brazil's cane sugar market operates under a combined framework covering food-safety rules for sugars as ingredients and identity and quality standards for traded sugar. ANVISA governs sanitary and labeling requirements, including nutrition labeling obligations under RDC No. 429/2020 for the declaration of total sugars and added sugars on packaged foods and beverages, a key compliance point for downstream users of liquid and crystallized sugar. ANVISA also set sanitary requirements specific to sugars and related products under RDC No. 818/2023, tightening quality, contaminant, and specification alignment for manufacturers and importers.

On the upstream and trade side, MAPA sets identity, classification, and quality parameters for sugar through Instrução Normativa No. 47/2018, which supports standardized grading across domestic commercialization and export contracting. Market access is also shaped by external trade regimes, including the United States sugar tariff-rate quota, where Brazil holds a fixed allocation of 155,993 metric tons raw value for FY2026, reinforcing the importance of quota management and compliance documentation in export planning.

Value Chain Analysis

The value chain begins with seedling and variety development (including domestic breeding programs), followed by farm inputs such as fertilizers, crop protection, and mechanization, then cultivation and harvesting, and finally milling at integrated sugar-ethanol plants where cane is converted into raw/VHP and refined sugars, ethanol, and co-products (bagasse for cogeneration and vinasse for fertigation). Milling concentration and vertical integration are central to Brazil's model, as large groups and trading platforms coordinate cane origination, crushing schedules, product mix decisions, and hedging for export-linked price exposure.

From mills, sugar moves via bulk logistics to export corridors and domestic industrial buyers. Santos remains a critical outlet, but it is exposed to seasonal bottlenecks and competition for berths and storage with grains. Operational responses have included terminal process upgrades and tighter rail-terminal coordination, such as VLI measures at integrating terminals (TIGU/TIUB) in the 2024/2025 harvest to reduce handling losses and manage sugar compaction. Policy actions also influence upstream resilience: on June 30, 2026, the federal government signed MP 1374 authorizing R$ 270 million in subsidies for independent cane producers in the Northeast (R$ 12 per tonne for the 2025/2026 harvest), supporting cane supply continuity into mills serving that region.

Competitive Landscape

Brazil's cane sugar market, with a moderate concentration, reflects a competitive environment. Established players maintain strong market positions but face challenges from consolidation efforts and rising international investments. The different players in the market are trying to improve their presence among consumers. The market is dominated by some of the key players like Tate & Lyle, Tereos SA, Louis Dreyfus Company, Agro Betel, and Cosan Limited, among others.

The sector's strategic focus increasingly revolves around vertical integration, combining sugar production, ethanol processing, and energy generation within unified operations. Key players like Raízen and Copersucar capitalize on scale efficiencies in procurement, processing, and distribution. However, they encounter competition from specialized firms targeting premium segments or specific geographic areas. Technology adoption has become a critical differentiator. Companies are investing in precision agriculture, biotechnology, and digital solutions to enhance yields and reduce costs. The Sugarcane Technology Center's innovation pipeline, valued at R$60 billion in potential economic impact, offers significant opportunities for mills capable of adopting new varieties and production techniques.

International players are expanding their presence through acquisitions and partnerships, as seen in Cargill's purchase of SJC Bioenergia and BP Bunge's investment in expansion. These developments bring global expertise and increased capital access, heightening competitive pressures on domestic operators, as noted by Reuters. Additionally, premium segments such as organic certification, direct trade relationships, and value-added processing present white-space opportunities, offering higher margins compared to traditional commodity sugar production.

Brazil Cane Sugar Industry Leaders

-

Tereos S.A.

-

Louis Dreyfus Company

-

Tate & Lyle Plc

-

Raízen

-

Cosan S.A.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Value capture is widening beyond commodity raw sugar through co-products and higher-specification ingredients. Bagasse valorization provides a concrete pathway: in July 2026, CNPEM reported a scalable process to produce nanocellulose from sugarcane bagasse, creating a commercialization route for mills and technology partners to monetize residues that already sit inside integrated sugar-energy operations. This complements existing mill strategies around bioelectricity export and next-generation biofuels, where operational flexibility between sugar and ethanol remains a key lever when cane availability and relative price signals shift.

On the sugar side, opportunities focus on improving throughput and TRS recovery, along with market access for differentiated grades used by food and beverage manufacturers (including liquid sugar supply models closer to end users). Execution capacity is visible in Centre-South output scale, where UNICA closed the 2025/2026 harvest at 40.43 million tonnes of sugar, while association data in May 2026 pointed to rapid early-season production momentum. Trading and offtake networks also help smaller and mid-sized mills reach export markets: in June 2026, Copersucar reported that 42 affiliated mills planned to process 125 to 128 million tonnes of cane in the 2026/2027 season following an expansion of its network base, underscoring ongoing platform-led commercialization and logistics coordination.

Recent Industry Developments

- June 2026: Raizen reported actions to simplify its portfolio and focus on core fuel and lubricant distribution and ethanol production, alongside BRL 12 billion in divestments during the 2025/26 crop year. The move reallocates capital away from non-core positions and supports balance-sheet flexibility for integrated sugar-ethanol operations operating under weather and input-cost volatility.

- June 2025: Contegran announced a USD 185.34 million investment to build a new integrated sugar, ethanol, and energy plant in Bahia aimed at export markets. Adding a new unit in the Northeast strengthens regional processing capacity and diversifies Brazil's supply footprint beyond the Center-South corridor.

- April 2024: Bonsucro signed a cooperation agreement with ORPLANA to advance sustainability practices in Brazil's sugarcane sector. The collaboration strengthens certification readiness and producer alignment on environmental and social requirements that influence access to premium and regulated export channels.

Research Methodology Framework and Report Scope

Market Definition and Coverage

We define the Brazil cane sugar market as the value of sugar produced from sugarcane and sold within Brazil or exported, counted at the product level across major forms used by food, beverage, and industrial buyers.

Scope exclusions: Sugar from sugar beet, artificial sweeteners, and finished packaged consumer foods that only use sugar as an ingredient are not counted.

Segmentation Overview

-

By Form

- Crystallized Sugar

- Liquid Sugar

-

By Product Category

- Raw Sugar

- White Refined

- VHP Sugar

- Organic

-

By Application

-

Food and Beverage

- Bakery and Confectionery

- Beverages

- Dairy and Frozen Foods

- Others

- Pharmaceuticals

- Industrial

- Biofuel / Ethanol

- Other Applications

-

Food and Beverage

-

By State

- São Paulo

- Goiás

- Minas Gerais

- Paraná

- Mato Grosso do Sul

- Other States

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with mapping Brazil sugarcane crushing, sugar output, and trade flows, so the demand and supply sides can be cross-checked before any modeling begins. Public datasets and official releases are used to build these anchors, such as UN Comtrade trade statistics, FAOSTAT, USDA GAIN Sugar Annual notes, and Brazil government agriculture and trade publications (for example, CONAB and customs summaries).

We also review broad signals such as inflation and exchange-rate series from official sources, plus industry association updates and reputable press coverage that explains crop conditions, logistics constraints, and policy moves. Company filings and investor presentations help validate operating logic, such as how mills allocate cane between sugar and ethanol, and what drives realizations by season. Where gaps remain, we use paid subscriptions for company financials and intelligence, news and financials, patent databases, and shipment-level import-export views to tighten assumptions. The sources listed above are illustrative only, and many other references were consulted to collect data, validate it, and clarify open questions.

Primary Interviews and Surveys

Primary work focuses on speaking with producers, traders, distributors, large buyers, and technical specialists who track cane allocation, product mix, and realized pricing by contract type. These conversations help confirm what portion of output is marketed as crystallized versus liquid sugar, how organic premiums behave, and which states are gaining or losing share due to agronomy and milling economics. Since this is a single-country market, we also make sure views are balanced across the key producing belts and the main consuming channels, so assumptions do not lean on one region or one end-use.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 15% | |

| Mid tier: 46% | Functional/Unit leaders: 29% | |

| Smaller Players: 21% | Managers: 56% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach where Brazil sugarcane crush and recovery, together with sugar production and trade signals, reconstruct the value pool for cane sugar sold in and out of the country. The model then applies form and use splits using a mix of public disclosures and interview feedback, and it is checked against observed movements in export volumes, port shipments, and reported season outcomes.

A selective bottom-up pass is used to keep the total realistic, mainly through sampled realizations and volumes by channel, plus supplier and trader sense-checks on typical price ranges by form. Inputs that matter most include cane crushing volumes, the sugar recovery rate, the sugar versus ethanol allocation, export share versus domestic sales, and price differences between crystallized, liquid, and higher-polarization sugar. For forecasting, we use scenario analysis tied to crop outlook, policy-linked ethanol demand, and expected price direction, and then we reconcile the scenarios to what primary respondents see as the most probable operating case. When data is missing for smaller states or niche grades, the gap is handled through proportional allocation from validated production and trade totals, followed by a second review against interview-led ranges.

Data Validation & Update Cycle

Validation is done through triangulation across production, trade, and pricing signals, and then through step-by-step variance checks at each layer of the model. If a segment total moves outside what crop outcomes or export data can support, the drivers are rechecked, and experts are re-contacted when the mismatch cannot be explained by seasonality or currency effects.

Before sign-off, the model and written assumptions go through multiple internal reviews so arithmetic, unit conversions, and scope logic stay consistent. Reports are refreshed annually, and interim updates are added when material events occur, such as large policy changes on ethanol blending, major crop shocks, or unusually sharp price shifts. Right before delivery, a final pass is completed so the latest public releases and market signals are reflected in the numbers.

Mordor Intelligence's Brazil Cane Sugar Market Size Compared Against Other Published Estimates

Published values for Brazil cane sugar can vary widely, even when the same years are referenced, because the scope and the valuation point are not always aligned. Differences commonly come from whether the figure reflects cane sugar as a product market, a broader sugar economy, or only a refined subset, and also from how price timing and currency conversion are handled.

The main gap comes from whether sugarcane-based ethanol value is folded into the total, where Mordor Intelligence counts only cane sugar revenue and uses ethanol mainly as a demand pull that changes how much cane is available for sugar in a given season. Another driver is how forms are priced, since using a single blended price can overstate liquid sugar in some years and understate crystallized sugar during export-led seasons. Timing also matters because some estimates apply annual average FX rates, while others use spot periods that shift USD values noticeably in Brazil.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 8.45 M (2025) | |

| Global Research Publisher A | USD 4.10 B (2025) | This figure appears to use a broader value pool for cane sugar and may be closer to a downstream market view, and it does not clearly separate sugar revenue from adjacent sugarcane outputs when presenting totals. |

| Sector Analytics Firm B | USD 1.20 B (2024) | This estimate is for refined cane sugar only, so raw and high-polarization grades are not in scope, and the year is different, which makes the total structurally smaller and not directly comparable to an all-grade cane sugar market view. |

The spread in the table is largely explained by scope choices, especially refined-only versus all cane sugar grades, and by whether adjacent sugarcane outputs are blended into the same value number. By keeping the model tied to observable sugar production, trade flows, and form-level price behavior, the result stays traceable to inputs that can be checked and repeated.

Key Questions Answered in the Report

What is the projected value of the Brazil sugar market in 2031?

The Brazil sugar market is forecast to reach USD 10.33 billion by 2031 at a 3.40% CAGR.

Which state is expected to post the fastest production growth?

Goiás is projected to expand output at a 4.82% CAGR through 2031 due to greenfield investments and lower land costs.

What share did crystallized sugar hold in 2025?

Crystallized sugar commanded 84.68% of 2025 production, underscoring its importance in bulk exports.

Which premium segment is growing fastest?

Organic sugar volumes are rising at a 5.03% CAGR, supported by sustainability-focused export demand.

Page last updated on: