Packaging Machinery For Snack, Bakery And Confectionery Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

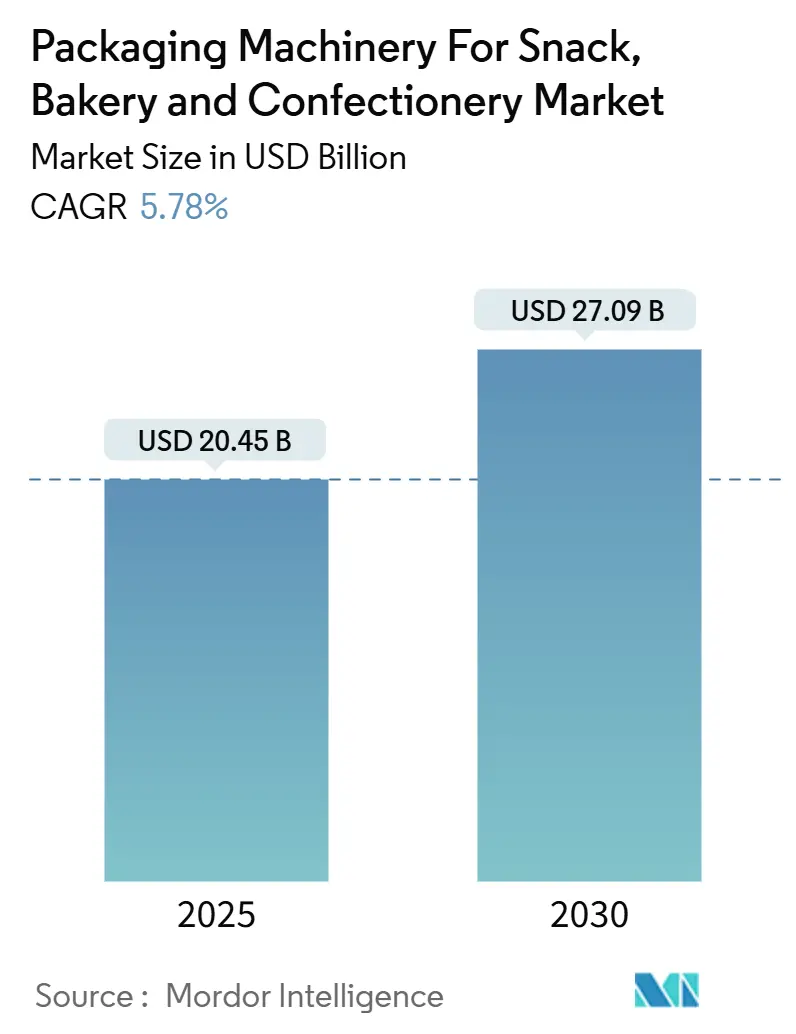

| Market Size (2025) | USD 20.45 Billion |

| Market Size (2030) | USD 27.09 Billion |

| Growth Rate (2025 - 2030) | 5.78% CAGR |

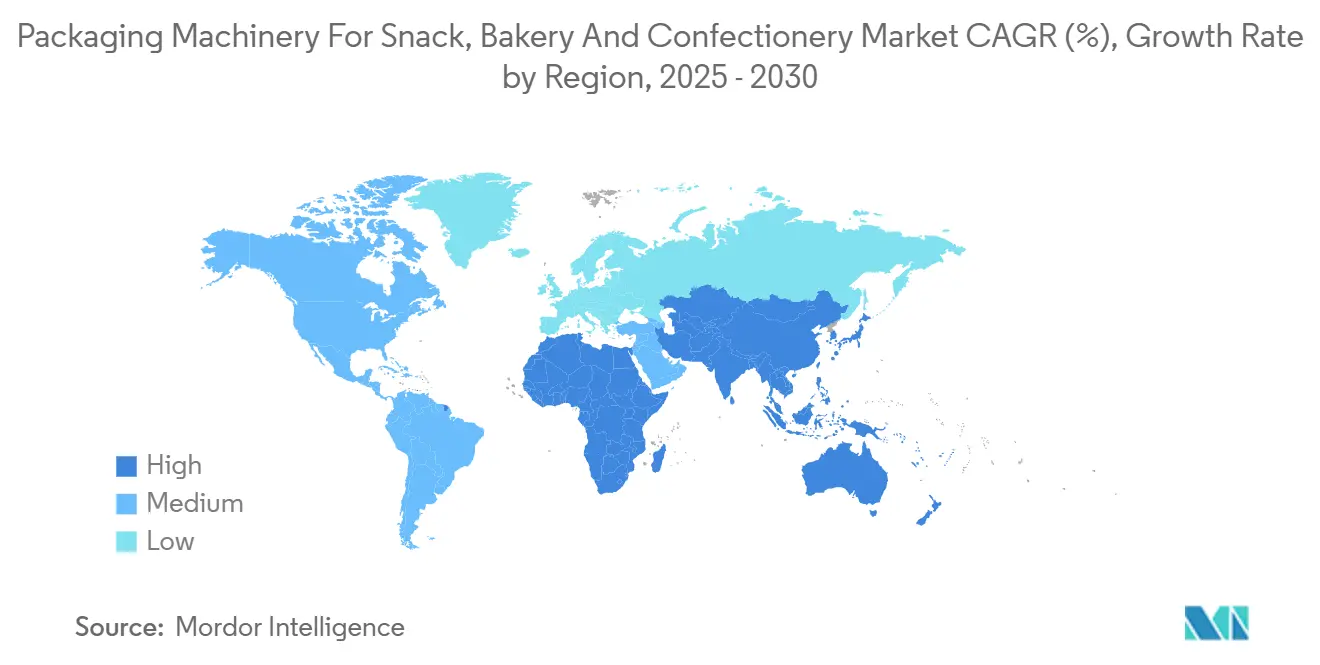

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Packaging Machinery For Snack, Bakery And Confectionery Market Analysis by Mordor Intelligence

The packaging machinery market for the snack, bakery, and confectionery industries is projected to reach USD 27.09 billion by 2030, advancing at a 5.78% CAGR from USD 20.45 billion in 2025. Demand stems from the rising consumption of convenient, portion-controlled foods, the sector’s rapid shift toward fully automated equipment that offsets labor shortages, and tighter hygiene-design regulations that necessitate capital upgrades. Sustainability mandates favor machinery that can handle bio-based and recyclable films, while predictive-maintenance software is gaining traction as manufacturers seek to maximize asset uptime. Intensifying competition among global and regional OEMs is also driving the adoption of modular designs, which enable buyers to scale capacity without requiring full line replacements.[1]Packaging Machinery Manufacturers Institute, “Packaging Machinery Outlook 2024,” PMMI.ORG

Key Report Takeaways

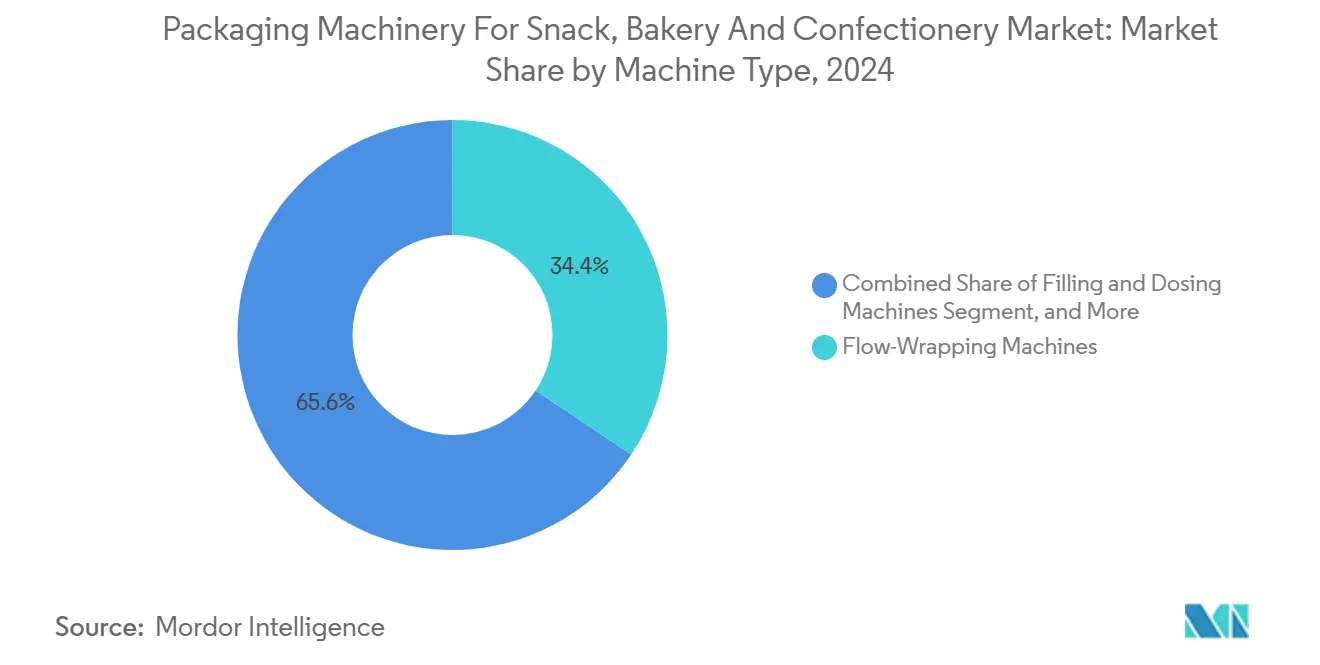

- By machine type, the flow-wrappers segment captured 34.37% of the Packaging Machinery for Snack, Bakery and Confectionery Market share in 2024.

- By automation level, the Packaging Machinery for Snack, Bakery and Confectionery Market size for semi automatic is projected to grow at a 7.46% CAGR between 2025–2030.

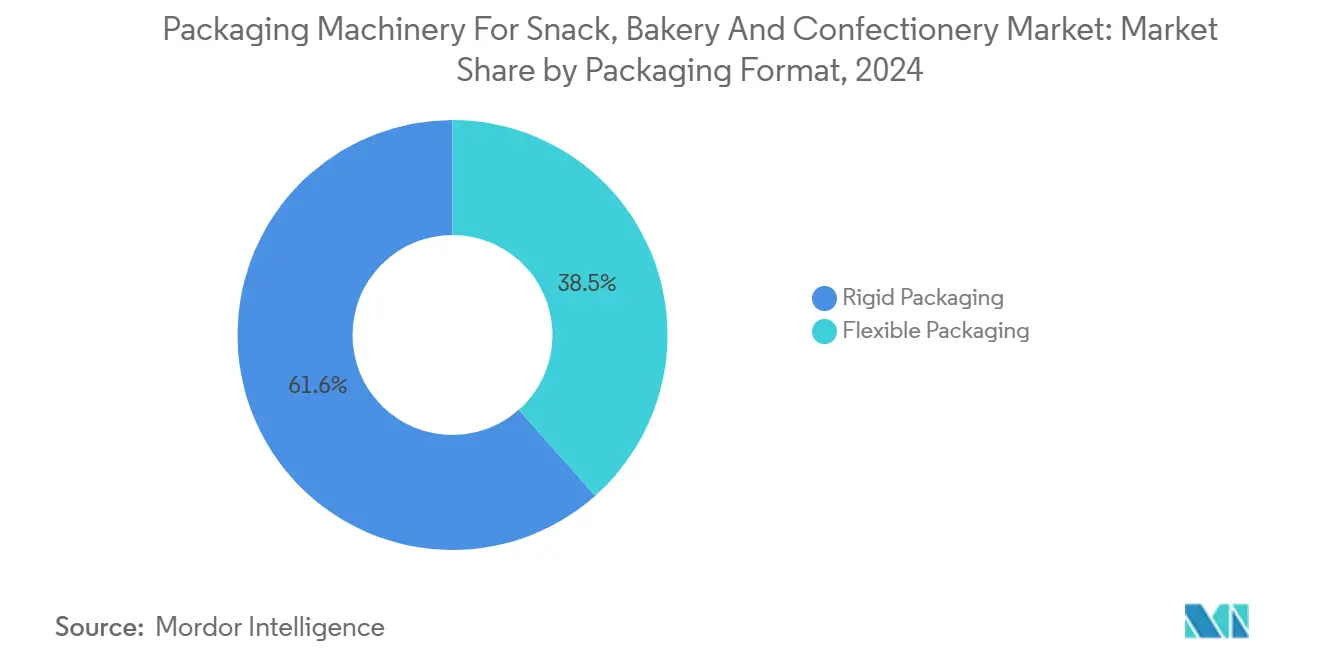

- By packaging format, the flexible solutions segment captured 38.45% of the Packaging Machinery for Snack, Bakery and Confectionery Market share in 2024.

- By application, the Packaging Machinery for Snack, Bakery and Confectionery Market size for confectionery is projected to grow at a 7.61% CAGR between 2025–2030.

- By geography, the Asia-Pacific segment captured 36.48% of the Packaging Machinery for Snack, Bakery and Confectionery Market share in 2024.

Global Packaging Machinery For Snack, Bakery And Confectionery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Single-serve demand surge | +1.2% | North America and Europe highest | Medium term (2-4 years) |

| Stricter hygienic-design rules | +0.9% | EU and North America | Long term (≥ 4 years) |

| Workforce shortages spur automation | +1.5% | Core in Asia-Pacific | Short term (≤ 2 years) |

| Material-flexible machinery for sustainability | +0.8% | Europe and North America | Medium term (2-4 years) |

| Functional snacks need MAP | +1.1% | Developed markets | Medium term (2-4 years) |

| D2C artisanal boom needs compact units | +0.7% | North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Single-Serve and Portion-Controlled Snacks

Manufacturers report that 92% of snack producers expect further growth in single-serve lines, with 88% budgeting new machinery by 2027. The packaging machinery for the snack, bakery, and confectionery market benefits from high-speed flow-wrappers and multi-lane fillers, which address varied shapes without lengthy changeovers, thereby protecting margins that are 15-20% higher than those of multipack formats. Regulatory labeling rules from the FDA accelerate the adoption of integrated weighing verification that guarantees declared serving sizes.[2]U.S. Food and Drug Administration, “FSMA Final Rule on Preventive Controls for Human Food,” FDA.GOV The net result is sustained investment in flexible machines that process small packs at industrial throughputs.

Stringent Food-Safety and Hygienic-Design Regulations

The Food Safety Modernization Act in the United States and the EU Directive 2006/42/EC oblige OEMs to build washdown-ready frames, sloped surfaces, and tool-free access points. Compliance adds 8-12% to capital outlay yet lowers contamination risk and reduces recall exposure. Firms that incorporate sanitary design from the outset gain a competitive edge because retrofitting legacy lines often costs more than installing new ones. The demand for hygienically engineered equipment, therefore, reinforces premium pricing and lengthens replacement cycles within the packaging machinery for the snack, bakery, and confectionery markets.

Workforce Shortages Accelerating Automation Adoption

Seventy-eight percent of food manufacturers were unable to fill entry-level plant roles in 2024, and 84% lacked skilled machine operators. For Asia-Pacific processors, the gap extends to maintenance crews, prompting factories to adopt fully automatic packaging cells equipped with predictive-maintenance analytics that reduce unplanned downtime. OEMs respond with modular automation platforms allowing staged upgrades as labor constraints intensify. Lower sensor costs further reduce payback times, supporting the swift penetration of lights-out operations across the packaging machinery for the snack, bakery, and confectionery markets.

Sustainability Mandates Driving Material-Flexible Machinery

The EU Single-Use Plastics Directive and state-level U.S. plastics bills compel packagers to shift to mono-material or bio-based films. Machines equipped with adaptive heat-seal controls automatically adjust dwell time and pressure for each substrate, limiting scrap and maintaining seal integrity. Buyers willingly pay 10-15% premiums for equipment that future-proofs compliance and backs ESG goals, reinforcing the outlook for sustainable-ready systems within the packaging machinery for snack, bakery, and confectionery markets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capex for advanced automated lines | -1.8% | Emerging markets | Medium term (2-4 years) |

| Raw-material and component volatility | -1.1% | Global | Short term (≤ 2 years) |

| Shortage of skilled maintenance technicians | -0.9% | Emerging markets | Long term (≥ 4 years) |

| Fragmented export-market standards | -0.6% | Multi-region exporters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital Expenditure for Advanced Automated Lines

State-of-the-art packaging systems can require USD 500,000 to USD 2 million, plus another 20-30% for plant utilities upgrades. Payback periods of 3-5 years deter mid-sized processors in capital-scarce economies and temper uptake of cutting-edge technology. Financial barriers hinder the overall velocity at which packaging machinery for the snack, bakery, and confectionery markets reaches full automation.

Raw-Material and Component Price Volatility

Hot-rolled coil steel prices swung between USD 600-900 per metric ton during 2024. Similar swings hit aluminum and precision servo components, forcing OEMs to add escalation clauses or risk margin erosion on long-lead orders. Uncertain pricing complicates plant budgeting and occasionally delays purchase decisions, which in turn hinders short-term growth for packaging machinery in the snack, bakery, and confectionery markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Machine Type: Flow-Wrappers Retain Versatility Lead

Flow-wrappers accounted for 34.37% of the 2024 base, reflecting their ability to wrap delicate pastries and high-end confectionery under modified atmospheres without damaging product appearance. This share equates to the largest slice of the packaging machinery market for snacks, bakery, and confectionery, positioning the technology as the go-to solution for tamper-evident, shelf-life-extending wraps. Artificial-intelligence-enabled cameras now feed real-time adjustments that minimize film use and reject rates, driving further adoption.

Filling and dosing machines, clocking a 7.83% forecast CAGR, ride the wave of protein-fortified snacks that require gram-level accuracy for nutrient labeling. Servo-driven augers handle viscous batters and particulate-rich mixes with equal precision, broadening appeal across bakery fillings and nut-butter inclusions. Meanwhile, form-fill-seal remains popular in high-volume salty snack lines, whereas cartoners and case packers benefit from e-commerce’s demand for ship-ready secondary packs. Collectively, machine-type diversity keeps supplier competition lively in the packaging machinery market for snacks, bakery, and confectionery products.

By Automation Level: Full Automation Dominates Efficiency Push

Fully automatic solutions accounted for 46.72% of 2024 revenues, a testament to their ability to reduce labor minutes per pack. Plants that migrated from manual steps noted 15-25% labor savings and up to 10-15% extra throughput, anchoring total cost-of-ownership advantages that underpin the packaging machinery market share of automated lines for the snack, bakery, and confectionery industries. Safety interlocks and hygienic stainless steel guards meet global standards, facilitating multinational deployments.

Semi-automatic platforms, however, post the briskest growth at 7.46% CAGR as SMEs embrace modular upgrades. Collaborative robots increasingly aid in pick-and-place tasks, creating hybrid cells where humans focus on judgment-intensive steps. Manual gear remains relevant for micro-bakeries and premium chocolatiers whose low volumes cannot yet absorb high capital expenditures, illustrating the tiered progression of automation across the packaging machinery for snack, bakery, and confectionery markets.

By Packaging Format: Flexible Gains, Rigid Premiumizes

Flexible films captured 38.45% share in 2024, buoyed by pouch reseal features and film-to-product ratios that curb material use. Oxygen-scavenging mono-material structures now rival traditional laminates in terms of barrier performance, and machines with rapid seal-parameter shift capabilities minimize downtime when processors switch substrates. Consequently, flexible often forms the entry point for sustainability within the packaging machinery for the snack, bakery, and confectionery market.

Rigid containers, particularly composite cans and PET jars, are projected to grow at a rate of 7.39% annually, driven by the demand for gifting-friendly confectionery and e-commerce protection needs. Equipment makers add in-line quality vision to detect micro-cracks in rigid walls, preserving shelf appeal. Material choice, therefore, aligns with marketing strategy, underscoring how branding goals influence equipment investment in packaging machinery for the snack, bakery, and confectionery markets.

By Application: Savory Snacks Hold Commanding Presence

Savory snacks generated 37.93% of 2024 revenues as better-for-you chips and seasoned nuts found mainstream acceptance. Degassing valves and nitrogen-flush systems prevent staling, thereby sustaining the largest slice of the packaging machinery market for the snack, bakery, and confectionery categories. Customizable seasoning drum integration also speeds up formulation changeovers, keeping SKU portfolios fresh.

Confectionery advances at the fastest rate, with a 7.61% CAGR, driven by premium chocolates that require temperature-controlled wrapping. Delicate shell-molded treats now travel global supply chains thanks to foil-on-film combinations sealed inside low-oxygen environments, proving the role of precise packaging in product preservation. Bakery, nuts and dried fruit, and emerging plant-based snacks round out the opportunity set that keeps OEM R&D pipelines active across the packaging machinery for snack, bakery, and confectionery markets.

Geography Analysis

Asia-Pacific led with a 36.48% footprint in 2024, underpinned by China’s USD 15 billion automation spend and India’s Production Linked Incentive subsidies.[3]China Food Industry Association, “Food Processing Industry Investment Report 2024,” CFNA.ORG.CN The regional CAGR of 7.26% from 2020 to 2030 is driven by supermarket expansion, rising disposable incomes, and stricter food-safety audits that necessitate the use of modern equipment. Japan spearheads the development of AI-enabled weighing systems, while South Korea channels investment toward export-grade, hygienic lines. Australia’s blossoming artisanal scene fuels purchases of compact, configurable machines, showcasing the variety of demand within the packaging machinery market for snacks, bakeries, and confectioneries.

North America ranks second in size, where the FDA’s sanitation rules and consumer appetite for high-protein snacks favor intelligent, hygienic equipment. U.S. processors continue to push for 24/7 uptime, pushing OEMs to bundle remote diagnostics for immediate troubleshooting. Mexico gains from USMCA duty-free parts flows, luring multinational producers to establish near-shore snack plants that require world-class packaging lines.

Europe’s policy environment centers on circular economy targets that penalize non-recyclable packaging. Germany exports turnkey solutions globally, and Italy’s craftsmanship propels niche chocolate and specialty-bakery machinery. The United Kingdom, aligning post-Brexit trade, directs funding toward adaptable equipment to satisfy EU and Commonwealth standards, rounding out geographic drivers for the packaging machinery for snack, bakery and confectionery market.

Competitive Landscape

The sector remains moderately fragmented, with the top five suppliers accounting for roughly 30-35% of global sales, leaving room for regional specialists. Syntegon, Ishida, and MULTIVAC differentiate via predictive analytics platforms that flag bearing wear before downtime occurs. MULTIVAC’s 2025 purchase of Tecnovac boosted its vacuum-pack range and Mediterranean footprint, exemplifying horizontal expansion.

Sustainability compliance now functions as a bid qualifier; OEMs that are able to validate biofilm compatibility win long-term preferred-vendor status. Disruptors target functional-food pack lines that require micro-dosing and modified-atmosphere modules, eroding the incumbent's share in niche applications. Concurrently, service networks expand into emerging hubs. Ilapak’s 2024 centers in Thailand and Vietnam illustrate the global race to secure after-sales revenue.

Compact, tabletop machines aimed at D2C bakeries mark a white-space battleground. Cavanna and Reiser rolled out sub-USD 100,000 units with tool-free changeovers in 2025, challenging manual workflows. Continual innovation at multiple price tiers thus shapes the competitive landscape of packaging machinery for the snack, bakery, and confectionery markets.

Packaging Machinery For Snack, Bakery And Confectionery Industry Leaders

Syntegon Technology GmbH

Ishida Co., Ltd.

TNA Solutions Pty Ltd.

Bühler AG

GEA Group AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Syntegon Technology invested USD 50 million to enlarge its German plant, adding capacity for AI-driven food-packaging lines.

- September 2025: MULTIVAC acquired Tecnovac for USD 75 million to bolster vacuum-pack expertise in confectionery.

- August 2025: Ishida launched an AI-Vision inspection module reaching 99.9% foreign-object detection accuracy on snack lines.

- July 2025: Bühler AG won a USD 120 million order for automated chocolate MAP systems across three Asia-Pacific factories.

Global Packaging Machinery For Snack, Bakery And Confectionery Market Report Scope

| Form-Fill-Seal Machines |

| Filling and Dosing Machines |

| Flow-Wrapping Machines |

| Cartoning and Case-Packing Machines |

| Labeling and Palletizing Machines |

| Other Machine Types |

| Fully Automatic |

| Semi Automatic |

| Manual |

| Rigid Packaging |

| Flexible Packaging |

| Bakery |

| Confectionery |

| Savory Snacks |

| Nuts and Dried Fruits |

| Other Applications |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Machine Type | Form-Fill-Seal Machines | ||

| Filling and Dosing Machines | |||

| Flow-Wrapping Machines | |||

| Cartoning and Case-Packing Machines | |||

| Labeling and Palletizing Machines | |||

| Other Machine Types | |||

| By Automation Level | Fully Automatic | ||

| Semi Automatic | |||

| Manual | |||

| By Packaging Format | Rigid Packaging | ||

| Flexible Packaging | |||

| By Application | Bakery | ||

| Confectionery | |||

| Savory Snacks | |||

| Nuts and Dried Fruits | |||

| Other Applications | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the packaging machinery for snack, bakery and confectionery market?

The market is valued at USD 20.45 billion in 2025.

How fast is the packaging sector for snack, bakery and confectionery products growing?

It is expected to register a 5.78% CAGR between 2025 and 2030.

Which machine type leads sales in this packaging equipment space?

Flow-wrappers dominate with 34.37% share of 2024 revenues.

Which region holds the largest share in packaging machinery for snack, bakery and confectionery?

Asia-Pacific leads with 36.48% of global sales in 2024.

What is the biggest restraint on the adoption of advanced packaging lines?

High capital expenditure, ranging from USD 500,000 to USD 2 million per line, slows investment for smaller processors.

Which application will grow fastest through 2030?

Confectionery applications are set to expand at a 7.61% CAGR as premium chocolates and candies gain traction.

Page last updated on: