Dairy Packaging Machinery Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

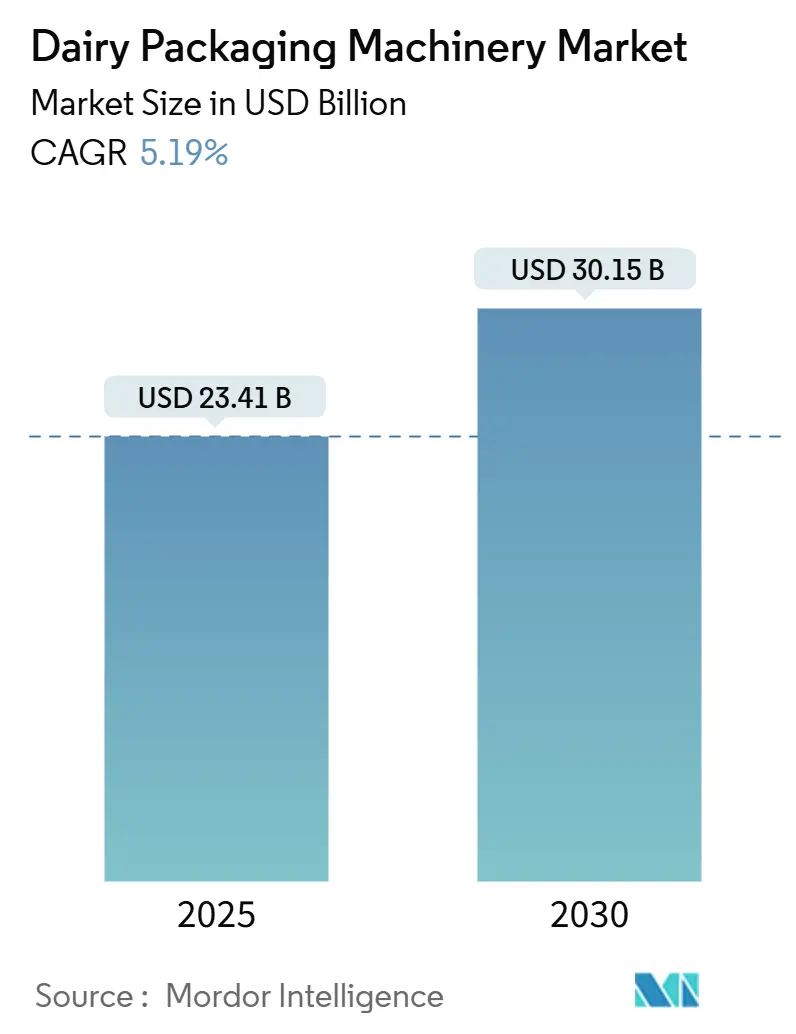

| Market Size (2025) | USD 23.41 Billion |

| Market Size (2030) | USD 30.15 Billion |

| Growth Rate (2025 - 2030) | 5.19% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

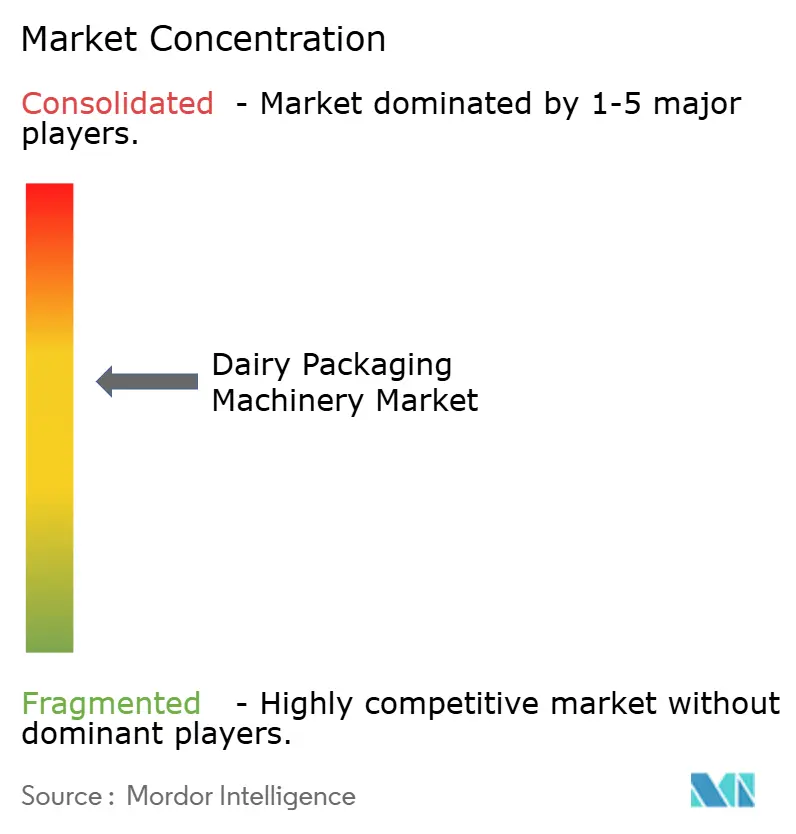

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dairy Packaging Machinery Market Analysis by Mordor Intelligence

The dairy packaging machinery market size stood at USD 23.41 billion in 2025 and is forecast to reach USD 30.15 billion by 2030, advancing at a 5.19% CAGR during the period. This momentum reflects sustained investments in integrated filling, sealing, and palletizing solutions that boost line efficiency while aligning with global sustainability mandates. Persistent labor shortages have elevated fully automatic systems to a dominant role in large plants, even as semi-automatic alternatives attract mid-tier processors balancing cost and capacity. Carton and pouch formats continue to split demand: cartons hold firm in liquid milk, whereas pouches surge on portion-control trends that resonate with health-conscious consumers. Europe remains the largest regional hub thanks to mature manufacturing ecosystems and stringent waste rules, while Asia-Pacific delivers the most dynamic growth underpinned by cold-chain expansion and rising per-capita dairy intake. Competitive intensity is moderate, with leading vendors accelerating M&A to add flexible formats, digital printing, and recyclable-material handling to their portfolios.

Key Report Takeaways

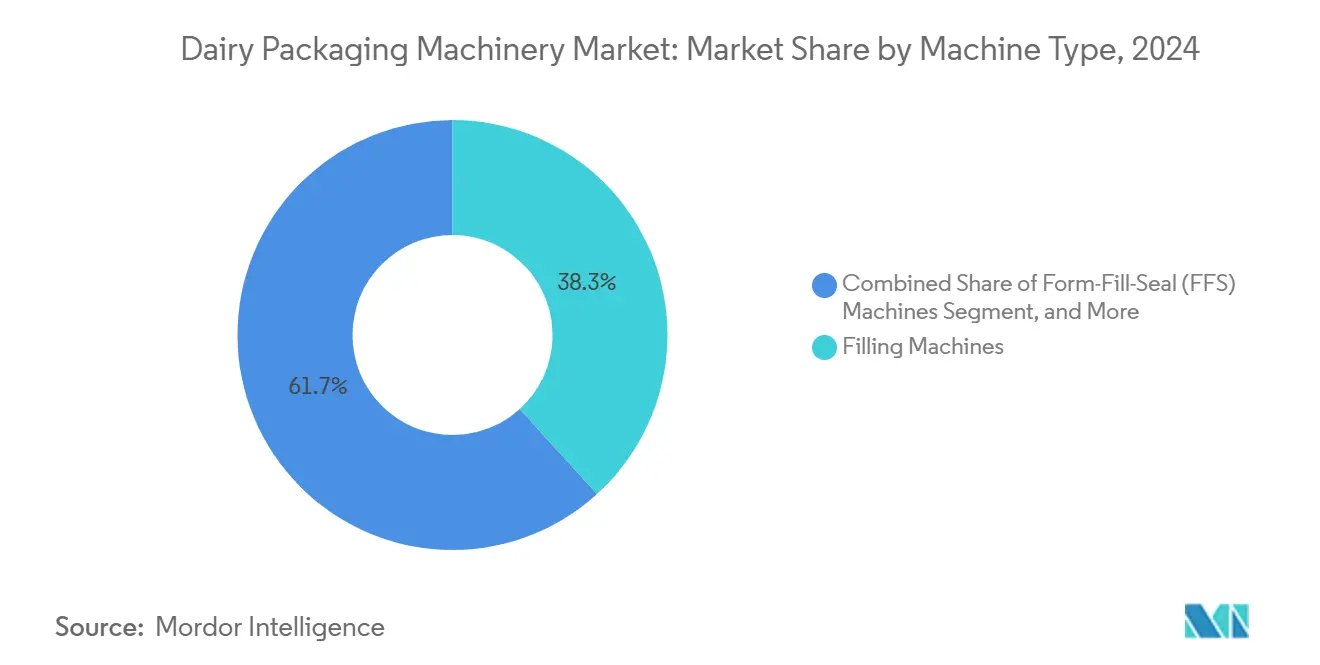

- By machine type, the filling equipment segment captured 38.26% of the Dairy Packaging Machinery Market share in 2024.

- By packaging type, the Dairy Packaging Machinery Market size for pouches and sachets is projected to grow at a 7.09% CAGR between 2025–2030.

- By automation level, the fully automatic lines segment captured 67.52% of the Dairy Packaging Machinery Market share in 2024.

- By application, the Dairy Packaging Machinery Market size for yogurt and cultured products is projected to grow at a 6.83% CAGR between 2025–2030.

- By geography, Europe captured 29.48% of the dairy packaging machinery market share in 2024.

Global Dairy Packaging Machinery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for single-serve dairy formats | +2.8% | Global, with strongest impact in North America and APAC | Medium term (2-4 years) |

| Automation to offset dairy-sector labor shortages | +3.2% | Global, particularly acute in Europe and North America | Short term (≤ 2 years) |

| Sustainability mandates driving lightweight packages | +2.1% | Europe and North America core, expanding to APAC | Long term (≥ 4 years) |

| Expansion of cold-chain logistics in emerging markets | +2.9% | APAC, MEA, Latin America | Medium term (2-4 years) |

| Digital printing enabling SKU proliferation | +1.7% | Global, led by developed markets | Short term (≤ 2 years) |

| Government food-safety regulations tightening | +2.4% | Global, with varying compliance timelines | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Single-Serve Dairy Formats

Urban consumers prefer portion-controlled yogurt cups, milk bottles, and cheese sticks that cater to their busy lifestyles. Single-serve launches accounted for more than 40% of all new dairy SKUs in 2024, prompting processors to invest in high-speed fillers that maintain accuracy at smaller volumes. Packagers adopt precision dosing valves and quick-changeover tooling to minimize material waste and maximize uptime. The trend also raises the adoption of smart conveyors that handle lighter primary packs without scuffing. Machinery builders capitalize on this shift to upsell integrated inspection modules that verify seal integrity on every pack before it is sent for downstream case packing. As retailers expand their shelf assortments, the dairy packaging machinery market gains long-term stability from recurring upgrades that support SKU proliferation.

Automation to Offset Dairy-Sector Labor Shortages

Food manufacturing employment fell 3.2% in 2024, and unfilled skilled-operator roles drive pay inflation in packaging halls. Large processors respond by deploying robots for case packing, palletizing, and secondary sealing, cutting labor hours by up to 60%. Machine suppliers are noting a rising demand for plug-and-play cobots that can retrofit existing lines without lengthy downtime. Smaller dairies, meanwhile, adopt semi-automatic fillers that require one attendant per lane rather than three. Vendor roadmaps now emphasize intuitive HMIs and remote diagnostics that shorten operator learning curves. The dairy packaging machinery market thus benefits from both ends of the automation spectrum: high-capex fully automatic solutions and cost-contained semi-automatic lines.

Sustainability Mandates Driving Lightweight Packages

The European Union’s 2024 Packaging and Packaging Waste Regulation compels 30% recycled-content plastic by 2030 and imposes progressive weight-reduction targets. OEMs respond with servo-driven forming modules that enable the use of thinner gauges without compromising top-load strength. Interest in mono-material solutions escalated by 45% in 2024 as processors sought easy-to-recycle packs, spurring orders for adaptable sealing jaws and vacuum systems that accommodate new film chemistries. Suppliers enhance design software to simulate stress loads, allowing customers to validate downgauged concepts before making tooling investments. These shifts reinforce the trend in the dairy packaging machinery market toward material-sparing engineering.

Expansion of Cold-Chain Logistics in Emerging Markets

India increased its cold-storage capacity to 37.5 million metric tons in 2024, while China expanded its chilled distribution into lower-tier cities. With reliable refrigeration, processors utilize aseptic and ESL packs that can travel further without spoiling. Horizontal FFS lines producing shelf-stable pillow pouches gain favor for flavored milk, yogurts, and probiotic drinks. OEMs integrate in-line UHT modules, creating turnkey systems that compress processing and packaging footprints. As cold-chain penetration expands in Southeast Asia and Latin America, the dairy packaging machinery market is experiencing a new wave of first-time equipment purchases, which amplifies installed-base revenues.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront CAPEX for advanced machinery | -1.8% | Global, most pronounced in developing markets | Short term (≤ 2 years) |

| Volatility in stainless-steel and resin prices | -1.4% | Global, with regional supply chain variations | Short term (≤ 2 years) |

| Skilled-operator shortage in developing regions | -1.1% | APAC, MEA, Latin America | Medium term (2-4 years) |

| Machine downtime from complex multi-format lines | -0.9% | Global, affecting high-volume operations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront CAPEX for Advanced Machinery

Turnkey aseptic fillers can cost USD 10 million, equating to roughly four years of cash flow for a mid-sized dairy. In 2024, 34% of processors delayed upgrades, citing budget limits. Financing gaps spur demand for modular machines that expand capacity in phases. Vendors introduce subscription-style ownership models that bundle maintenance and software updates, thereby flattening expenditure curves. Although such models ease adoption, they lengthen sales cycles, mildly tempering the growth of the dairy packaging machinery market in capital-constrained geographies.

Volatility in Stainless-Steel and Resin Prices

Nickel supply disruptions drove stainless-steel price swings of up to 20% in 2024. Similarly, polyethylene spot prices spiked due to feedstock shortages, leading to increased material surcharges in machine quotes. Large OEMs hedge their risks with multi-year supply contracts, but smaller fabricators must pass surcharges to buyers, thereby inflating project costs. Processors respond by extending bid validity periods, negotiating index-linked pricing, and delaying purchase decisions, thereby dampening the near-term acceleration of the dairy packaging machinery market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Machine Type: Integration Fuels FFS Momentum

Filling equipment held the largest 38.26% slice of the dairy packaging machinery market in 2024, reflecting its indispensability across liquid milk, yogurt, and cream. These machines anchor most high-speed lines, which can top 40,000 packs per hour, sustaining consistent demand for retrofitting nozzle upgrades and CIP systems. In contrast, Form-Fill-Seal units are scaling fastest at a 6.55% CAGR because they consolidate forming, dosing, and sealing into a single chassis, thereby reducing floor space needs. The dairy packaging machinery market size for FFS solutions is projected to climb from USD X billion in 2025 to USD Y billion by 2030, underscoring processor appetite for single-vendor integration. Horizontal variants target stick packs and pillow pouches, while vertical counterparts dominate grated cheese and powdered milk. With robotics now directly embedded into FFS discharge stations, downstream buffering is streamlined, making the technology even more attractive to cost-conscious operators.

Sealing, wrapping, and cartoning modules remain vital but evolve into plug-in blocks that tether to a common line-control platform. Palletizers are increasingly equipped with end-of-arm tooling that enables switching between crates and shrink-wrapped bundles in under five minutes, thereby safeguarding uptime in plants that handle multiple SKUs. Niche machines such as stretch blow-molders for PET yogurt bottles contribute stable but modest revenue, enriching the broader dairy packaging machinery market through tailored application expertise.

By Packaging Type: Flexible Formats Accelerate

Cartons retained a 41.49% share in 2024, powered by entrenched usage in UHT milk, where aseptic integrity is critical. Their renewable fiber content aligns with retail eco-scores, helping sustain volume despite upticks in rivals. Yet pouches and sachets are charting a 7.09% CAGR, translating to the fastest incremental gain in the dairy packaging machinery market. Pouches offer 25% lower material use than rigid bottles, which resonates strongly in emerging economies where the cost per liter is scrutinized. Processors like Amul deploy stick packs for chocolate milk to target school-age consumers, while Milky Mist uses doy packs for drinkable yogurt. These shifts increase demand for multi-lane horizontal FFS systems equipped with die-cut change kits that can switch between 90 mL and 200 mL fill volumes within an hour.

Bottle lines remain central to premium flavored milk and probiotic shots, supported by Sidel’s 15% PET-lightweighting breakthrough announced in 2024. Cup and tub formats cater to spoonable yogurt and desserts; servo-driven denesters now permit four-across tooling, which raises throughput without enlarging footprints. Specialized vacuum skin packs for cheese introduce high oxygen barriers, demanding thermoformers fitted with inline gas-flushing. Together, these diverse needs fuel technology variety while reinforcing the comprehensive scope of the dairy packaging machinery market.

By Automation Level: Dual-Track Demand

Fully automatic lines amassed 67.52% of 2024 installations. They knit fillers, sealers, and case packers into closed-loop data environments that alert technicians before faults escalate. Cloud dashboards enable line managers to monitor OEE across multiple sites, a feature prized by multinational dairies. This connectivity premium safeguards the top-end pricing that buoys average selling prices in the dairy packaging machinery market.

Semi-automatic configurations are growing at a 6.26% CAGR, particularly in Southeast Asia and sub-Saharan Africa, where processors transition from manual to mechanized operations. These units typically comprise a volumetric filler paired with manual lidding, shaving capital needs by 40% compared with full automation. OEMs now offer upgrade kits, allowing plants to add robotic pick-and-place capabilities later, thereby future-proofing the purchase decision. The split trajectory confirms that the dairy packaging machinery market serves a wide range of maturity levels, minimizing cyclical swings.

By Application: Yogurt Spurs Innovation

Milk commandeered 31.71% of revenue in 2024 and remains the anchor category for the dairy packaging machinery market, sustaining bread-and-butter orders for high-volume fillers and carton closers. Refill projects cycle every seven years as fillers wear, guaranteeing baseline OEM revenue. Yogurt, however, is scaling the fastest at a 6.83% CAGR, driven by digestive-health claims and indulgent dessert crossovers. Portion cups, ranging from 80 g protein shots to 150 g Greek variants, demand agile tooling that can rapidly swap rim diameters. Machines with dual dosing heads now swirl fruit purees into yogurt in-line, eliminating pre-mix steps and raising throughput. This complexity raises aftermarket parts revenue for OEMs, an often-overlooked but material contributor to the size of the dairy packaging machinery market.

Cheese machinery orders focus on vacuum thermoformers that shape variable loaf sizes, while butter commands foil-wrapping lines delivering premium brick aesthetics. Ice-cream cups capitalize on intermittent fillers capable of marbling sauces without smearing. Specialty dairy products, such as kefir and lassi, utilize hygienic piston fillers equipped with anti-foaming nozzles, demonstrating that nuanced product rheology influences machine selection in the dairy packaging machinery market.

Geography Analysis

Europe accounted for 29.48% of global sales in 2024, primarily driven by German and Italian machine builders that supply turnkey lines across the continent. EU eco-design rules fast-track adoption of recycled-PET-capable equipment, compelling processors to swap legacy metal-detectors for X-ray units that distinguish recycled flake contaminants. France and the United Kingdom continue to modernize their yogurt lines with robot-ready case packers, while the Nordics invest in plant-based dairy that requires lower-foaming filling technologies. Eastern European processors tap EU funds for automation grants, sustaining a solid replacement pipeline that undergirds the dairy packaging machinery market.

The Asia-Pacific region is projected to register a 7.36% CAGR through 2030, the fastest among all regions. Chinese dairy groups are adding aseptic brick lines that can reach 48,000 packs per hour as part of their rural penetration strategies, while Indian cooperatives are commissioning modular pouch fillers that they can expand in tranches. The expansion of cold chains across Indonesia and Vietnam creates new demand for ESL bottle fillers. Simultaneously, local OEMs emerge, but global suppliers maintain an edge through proven sterility validation and global service parts. These dynamics collectively elevate the Asian share of the dairy packaging machinery market size year by year.

North America exhibits steady growth, driven by labor-saving robotics and digital-printing retrofits. U.S. processors pay premiums for inline inspection that meets FDA’s evolving traceability rule, stimulating upgrades in existing plants. Mexico shows rising traction for case-erecting robots as export-oriented dairies seek U.S. certifications. South America, led by Brazil, witnesses gradual mechanization of cheese wrapping as domestic brands court modern retail. The Middle East and Africa record pockets of high growth where governments subsidize milk self-sufficiency, catalyzing purchases of entry-level fillers. Altogether, geographic diversification mitigates concentration risk in the dairy packaging machinery market.

Competitive Landscape

Industry concentration is moderate, with the top five suppliers, Krones AG, Sidel Group, Syntegon Technology, GEA Group, and Tetra Pak, capturing roughly 45% of the global revenue. Each firm blends core filling expertise with bolt-on acquisitions to widen flexible-format offerings. Krones’ 2024 takeover of Neostarpack bolstered its pouch portfolio, while Sidel emphasized bottle lightweighting technology that trims PET by 15%. Syntegon unveiled a recycled-PET-ready line, aiming squarely at EU PPWR compliance.

GEA expanded its Chinese plant by 40%, shortening lead times in the region. Tetra Pak invested USD 218 million in closed-loop carton recycling R&D, further deepening its end-to-end ecosystem. Mid-tier players leverage regional intimacy and niche specialization, such as Italianpack’s cartoners, to secure plant-specific orders. Competitive differentiation now pivots on digital twins, OEE analytics, and sustainability consulting wrapped around machinery. As processors consolidate globally, vendors that deliver multi-site standardization and predictive maintenance platforms are poised to strengthen their market share within the dairy packaging machinery market.

Start-ups targeting smart sensors for seal verification or AI-driven line balancing find receptive OEM partners eager to embed such modules and broaden service revenue. Pricing competition intensifies in commoditized end-of-line equipment, prompting providers to bundle extended warranties. Overall, rivalry is constructive, spurring innovation without triggering margin-eroding price wars across the dairy packaging machinery market.

Dairy Packaging Machinery Industry Leaders

Krones AG

Sidel Group

SIG Combibloc Group AG

IMA Industria Macchine Automatiche S.p.A.

GEA Group AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Krones AG completed the EUR 85 million (USD 92.6 million) acquisition of Neostarpack, expanding pouch and sachet capabilities.

- September 2024: Syntegon Technology has launched a sustainable line capable of processing 100% recycled PET.

- August 2024: ProMach acquired HMC Products for USD 45 million, strengthening horizontal FFS coverage in dairy.

- May 2024: Tetra Pak announced a EUR 200 million (USD 218 million) investment in recycling technology.

Global Dairy Packaging Machinery Market Report Scope

| Filling Machines |

| Form-Fill-Seal (FFS) Machines |

| Sealing Machines |

| Wrapping Machines |

| Cartoning and Case Packing Systems |

| Palletizing Machines |

| Other Machine Types |

| Cartons |

| Bottles |

| Pouches and Sachets |

| Cups and Tubs |

| Other Packaging Type |

| Fully Automatic |

| Semi Automatic |

| Milk |

| Cheese |

| Yogurt and Cultured Products |

| Butter and Spreads |

| Ice Cream and Frozen Desserts |

| Other Applications |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Machine Type | Filling Machines | ||

| Form-Fill-Seal (FFS) Machines | |||

| Sealing Machines | |||

| Wrapping Machines | |||

| Cartoning and Case Packing Systems | |||

| Palletizing Machines | |||

| Other Machine Types | |||

| By Packaging Type | Cartons | ||

| Bottles | |||

| Pouches and Sachets | |||

| Cups and Tubs | |||

| Other Packaging Type | |||

| By Automation Level | Fully Automatic | ||

| Semi Automatic | |||

| By Application | Milk | ||

| Cheese | |||

| Yogurt and Cultured Products | |||

| Butter and Spreads | |||

| Ice Cream and Frozen Desserts | |||

| Other Applications | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the dairy packaging machinery market in 2025?

It is valued at USD 23.41 billion and is projected to climb to USD 30.15 billion by 2030.

Which equipment segment leads current demand?

Filling machines hold the largest 38.26% revenue share due to their universal role across liquid and cultured dairy lines.

Why are pouches growing faster than cartons?

Pouches use 25% less material, align with portion-control trends, and enable cost-efficient distribution in emerging markets.

Which region is expanding quickest?

Asia-Pacific is forecast to post a 7.36% CAGR through 2030 on the back of cold-chain infrastructure upgrades and rising dairy consumption.

How are labor shortages influencing machinery purchases?

Plants are investing heavily in fully automatic lines and robotics that reduce operator headcount by up to 60%.

What role do sustainability regulations play?

EU and North American rules mandating recycled content and lightweighting are steering demand toward machines capable of processing thinner, mono-material packs.

Page last updated on: