Market Overview

| Study Period | 2020 - 2031 |

|---|---|

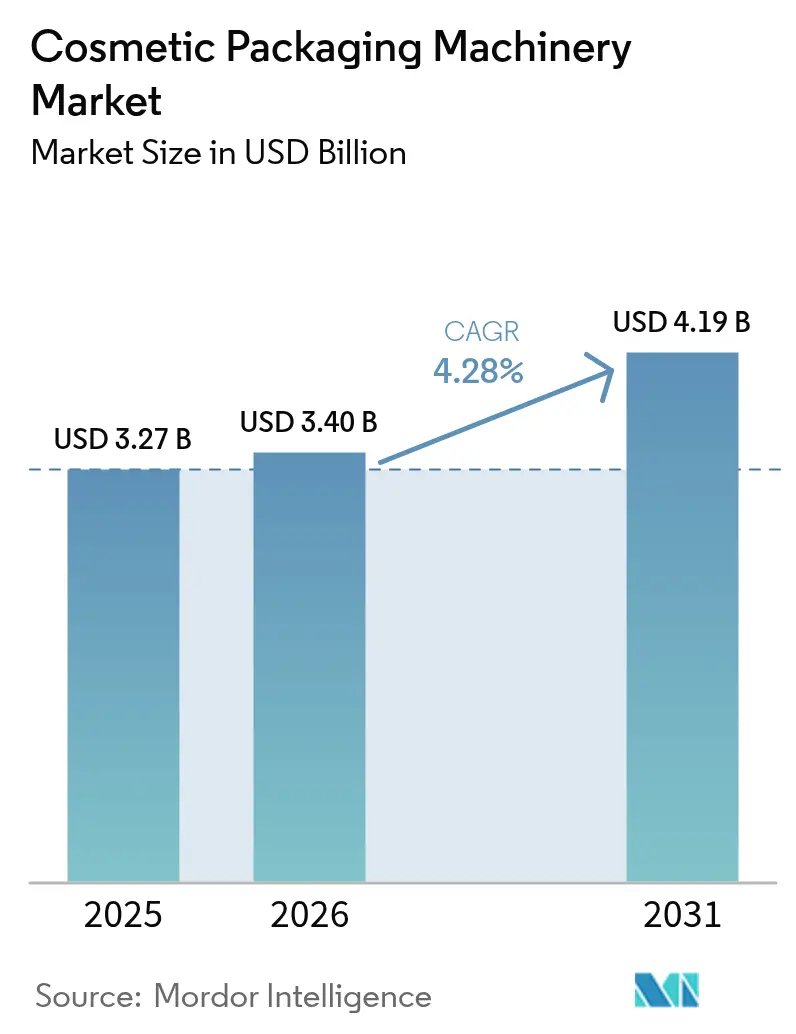

| Market Size (2026) | USD 3.40 Billion |

| Market Size (2031) | USD 4.19 Billion |

| Growth Rate (2026 - 2031) | 4.28% CAGR |

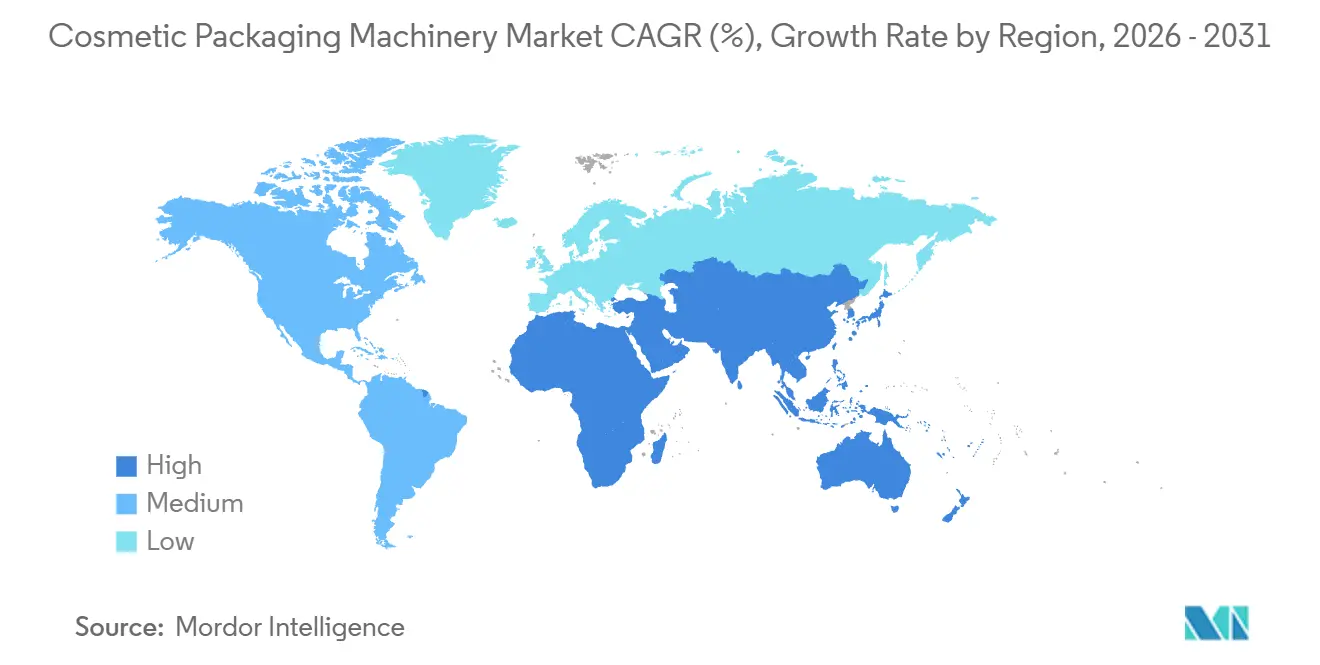

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cosmetic Packaging Machinery Market Analysis by Mordor Intelligence

The cosmetic packaging machinery market size is projected to be USD 3.27 billion in 2025, USD 3.40 billion in 2026, and reach USD 4.19 billion by 2031, growing at a CAGR of 4.28% from 2026 to 2031. Intensifying beauty-product launches, faster changeover expectations, and the need for serialization are reshaping investment priorities across filling, capping, labeling, and inspection lines. Brands are seeking shorter payback horizons, which is pushing original-equipment manufacturers to unbundle automation modules and bundle lease-back financing. Regulatory pressure for recyclable formats is accelerating adoption of mono-material tubes and lightweight pumps that require servo-driven tension control. The skilled-labor deficit continues to lift demand for fully automatic systems with remote diagnostics, while geopolitical restrictions on advanced servo components are bifurcating the supplier landscape.

Key Report Takeaways

- By automation level, fully automatic systems held 62.43% of the cosmetic packaging machinery market share in 2025, while semi-automatic systems recorded the highest projected 5.61% CAGR through 2031.

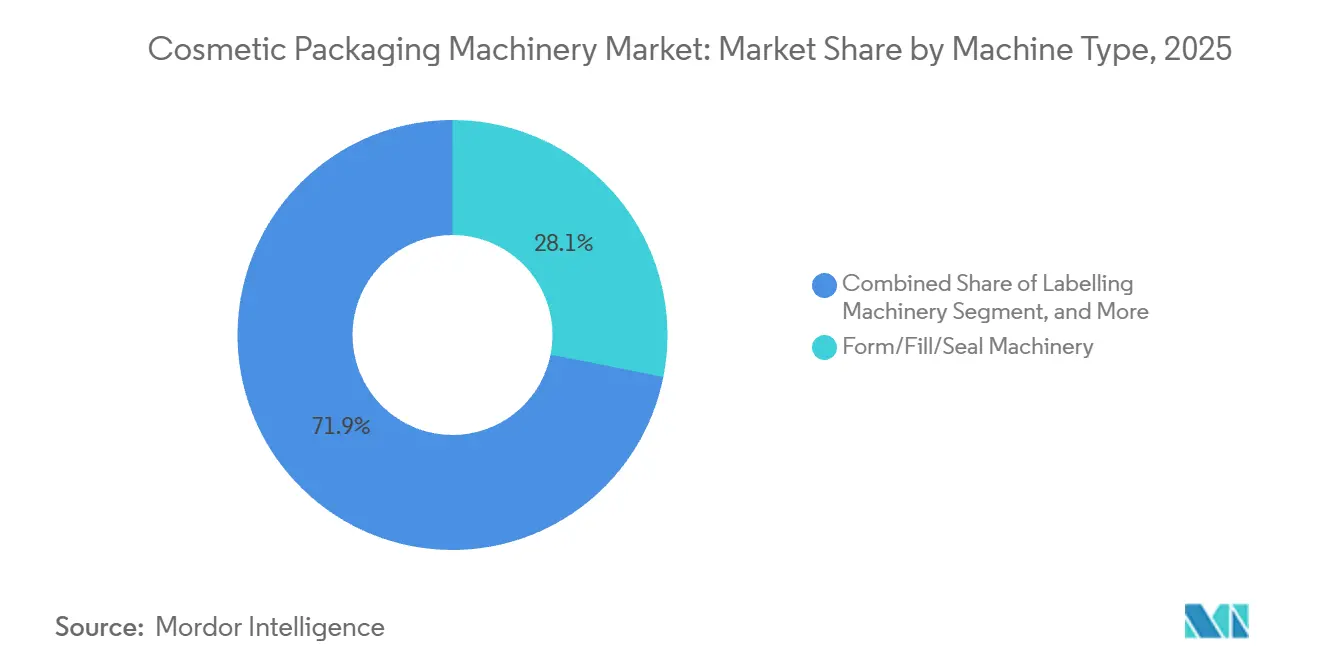

- By machine type, form-fill-seal equipment led with 28.13% of market share in 2025; labeling machines are forecast to expand at a 5.27% CAGR to 2031.

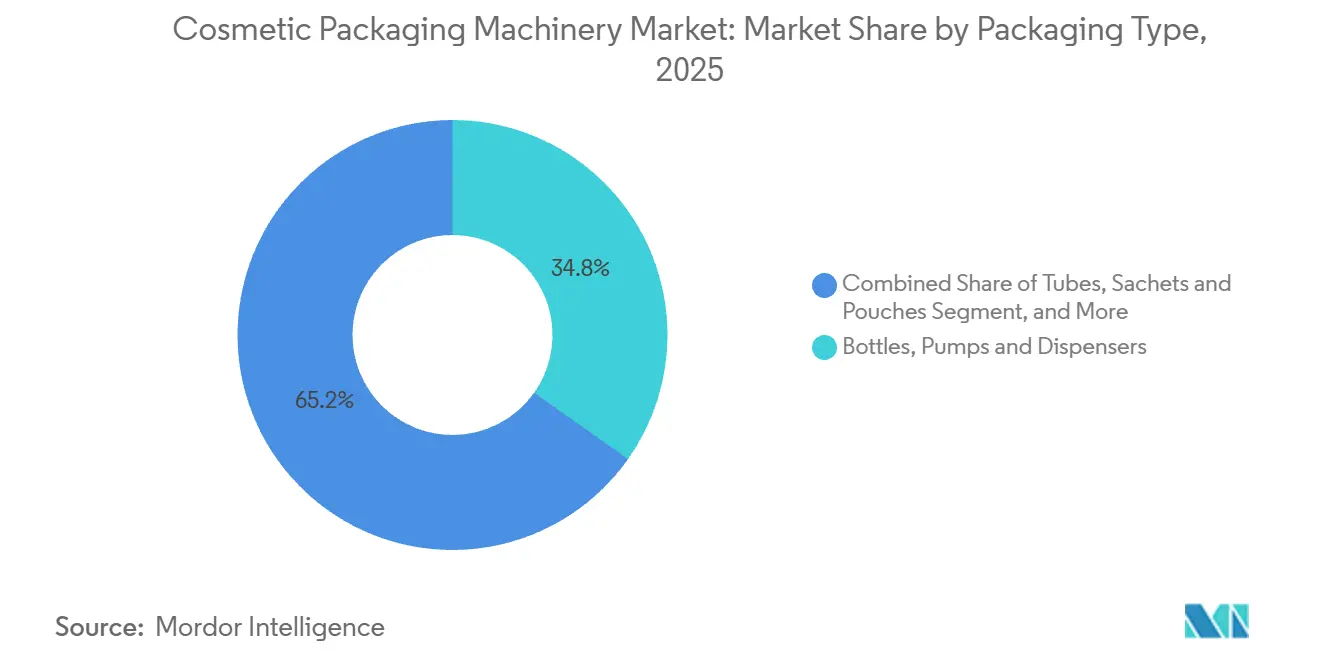

- By packaging type, bottles, pumps, and dispensers accounted for 34.79% of market share in 2025, whereas tubes, sachets, and pouches are advancing at a 5.78% CAGR over 2026-2031.

- By cosmetic product, skin-care products captured 38.94% share in 2025; hair-care is the fastest-growing segment with a 6.02% CAGR through 2031.

- By geography, North America commanded a 39.87% share in 2025, while Asia-Pacific is set to expand at a 6.11% CAGR, driven by domestic fill-finish capacity in China and India.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cosmetic Packaging Machinery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand for Personal Care and Beauty Products | +0.9% | Global, with accelerated growth in Asia-Pacific (China, India, South Korea) and Middle East | Medium term (2-4 years) |

| Increasing Industrial Automation and Smart Packaging Lines | +1.1% | North America, Europe, Asia-Pacific (Japan, South Korea) | Long term (≥ 4 years) |

| E-Commerce Shift Toward Smaller SKUs and Flexible Formats | +0.8% | Global, particularly North America and Europe for direct-to-consumer brands | Short term (≤ 2 years) |

| Sustainability Regulations Pressuring Eco-Friendly Packaging | +0.7% | Europe (EU microplastics ban), North America (state-level extended producer responsibility) | Medium term (2-4 years) |

| AI-Enabled Vision Inspection Boosts Throughput | +0.6% | North America, Europe, Asia-Pacific (advanced manufacturing hubs) | Short term (≤ 2 years) |

| Indie Cosmetic Brands Need Agile Short-Run Equipment | +0.5% | North America, Europe, Australia (localized production) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Personal Care and Beauty Products

Rising disposable income, premiumization, and social-media influence have lifted line-utilization rates above 85 % in mature markets, encouraging contract manufacturers to add second and third shifts rather than build new plants. A German plant using magnetic-transport conveyors cut changeover time from 45 minutes to under 10 minutes, enabling weekly SKU counts to top 120 without sacrificing output.[1]Beckhoff Automation, “XTS Conveying for Cosmetics,” beckhoff.com Asia-Pacific middle-class consumers increasingly insist on halal, vegan, and cruelty-free credentials, so vision systems now verify label claims in real time. Prestige distribution channels tighten acceptable defect levels to below 200 ppm, which is accelerating migration toward fully enclosed, sensor-rich equipment. As beauty companies roll out limited-edition collaborations, machinery that handles multiple container shapes without cross-contamination has become a procurement priority.

Increasing Industrial Automation and Smart Packaging Lines

Packaging cells now ship with embedded IoT sensors that capture cycle-time deviation, torque anomalies, and fill-weight drift, helping operators intervene before deviations trigger batch holds. A deep-learning vision platform launched in 2024 inspects label placement and seal integrity at more than 600 units per minute and reduces false rejects by 40 % compared with rule-based tools.[2]Cognex Engineering, “In-Sight 2800 Performance Note,” cognex.com Digital-twin commissioning shortens on-site installation by up to half, vital when lease agreements penalize late ramp-up. Collaborative robots for case packing reassign human operators to quality audits, while predictive maintenance routines schedule bearing replacements between production sprints. Taken together, these upgrades lift overall equipment effectiveness and justify a two- to three-times capital premium over legacy semi-automatic machinery.

E-Commerce Shift Toward Smaller SKUs and Flexible Formats

Direct-to-consumer channels rely on order sizes below two units, making sachets, trial-size tubes, and single-dose capsules attractive for postal delivery without dimensional-weight penalties. Flexible form-fill-seal lines capable of 15-minute format swaps now allow contract manufacturers to cluster multiple micro-brands on one shift. Digital presses such as the HP Indigo 25K can run cosmetic label jobs as small as 2,500 units, supporting rapid iteration cycles.[3]HP Industrial Press Division, “Indigo 25K Label Success Story,” hp.com Refillable packaging models are further fragmenting SKU counts, prompting OEMs to develop change-part systems that accept asymmetric geometries and nested inserts without manual adjustment. As a result, flexible equipment has evolved from a tactical fix for small orders into a cornerstone of omnichannel fulfillment strategies.

Sustainability Regulations Pressuring Eco-Friendly Packaging

The European Union microplastics ban coming into force in 2027 is accelerating mono-material tube adoption and paper-based laminate trials. New fiber-based tubes with polyethylene liners cut plastic content by 50 % while maintaining barrier integrity. Machinery vendors have responded with servo-driven heat-seal heads that adjust dwell time in real time based on film thickness and ambient humidity. State-level extended-producer-responsibility schemes in the United States impose fees on non-recyclable packs, making lightweight designs that reduce material mass by 20-30 % financially attractive. Together, these policies redirect capital toward equipment that can seal thinner walls, handle post-consumer-recycled resins, and record process data for compliance audits.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Capital Expenditure | -0.7% | Global, acute in South America and Africa | Short term (≤ 2 years) |

| Volatile Prices of Precision Components and Steel | -0.5% | Global supply-chain concentration in Asia-Pacific | Medium term (2-4 years) |

| Shortage of Skilled Mechatronics Technicians | -0.6% | North America, Europe, Australia | Long term (≥ 4 years) |

| Export Controls on Advanced Servo Drives and Sensors | -0.3% | Asia-Pacific, Middle East, Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Capital Expenditure

Fully automatic cosmetic filling lines range from USD 500,000 to USD 2.5 million, a commitment that can stretch payback periods for mid-tier contract manufacturers. Elevated interest rates have made traditional term loans less attractive, so vendors now market 36-month leases with per-unit usage fees. Although these structures align payments with production volume, they embed implicit borrowing costs above 8 % and penalize seasonal operations. Cash-constrained brands often delay automation until utilization rates rise above 70 %, which reinforces a two-tier market; global consumer-goods giants amortize equipment across multiple plants, while regional players rely on refurbished machinery. Component inflation adds further pressure, with servo-drive prices rising faster than headline steel costs.

Shortage of Skilled Mechatronics Technicians

A 2024 industry survey found that 95 % of consumer packaged goods companies struggle to recruit qualified packaging technicians. High turnover erodes institutional knowledge and forces repeated onboarding, depressing overall equipment effectiveness. Only 14 % of firms consider printed standard-operating procedures effective, underscoring the need for interactive, augmented-reality training modules. OEMs now bundle remote-diagnostics agreements that let factory-based specialists guide on-site staff through troubleshooting. While such tools narrow skill gaps, they cannot replace core competencies in programmable-logic controllers and servo tuning. The issue is most acute in regions where vocational curricula lag behind the pace of installed automation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Machine Type: Labeling Equipment Gains Momentum on Serialization Demands

Labeling units are projected to outpace the broader cosmetic packaging machinery market with a 5.27% CAGR through 2031. Form-fill-seal systems held the largest share of 28.13% in 2025, yet brands focusing on traceability now prioritize printers and applicators that integrate QR codes and NFC tags. In consequence, the cosmetic packaging machinery market for labeling lines is growing as governments mandate unique identifiers and shoppers scan packs for authenticity checks. Vision-guided reject stations attached to these lines eliminate manual reinspection, supporting defect thresholds of fewer than 150 ppm. Growth also reflects a pivot toward augmented-reality triggers that unlock digital tutorials and loyalty programs. Machinery suppliers offer modular heads that swap between paper labels and shrink sleeves without tool changes, a design that lowers downtime and aligns with sustainability targets. Integrators bundle cloud-based data capture so brand owners can trace every lot back to plant, line, and operator, satisfying ISO 22716 record-keeping rules. Rising e-commerce penetration further increases label complexity, as fulfillment centers prefer unit-level barcodes that withstand abrasion during automated picking.

Semi-automatic label dispensers remain relevant for indie brands but are gradually ceding ground to servo-driven applicators capable of 600-plus units per minute. Investments focus on camera-based alignment that compensates for bottle wobble and glare from metallic inks. The cosmetic packaging machinery market share commanded by form-fill-seal equipment will persist, yet its growth is closely tied to single-serve sachets and sample pouches. These lines now host ultrasonic sealing jaws and gas-flush modules to preserve vitamin-rich emulsions. Meanwhile, capping, cartoning, and bundling machines plug into unified controls for uninterrupted data hand-off, simplifying validation in regulated export markets.

By Automation Level: Fully Automatic Lines Retain the Performance Edge

Fully automatic systems captured 62.43% of the market share in 2025, and semi-automatic systems recorded the highest projected 5.61% CAGR through 2031. Continuous motion conveyors and multi-axis robots achieve shorter tact times than intermittent machines, enabling contract manufacturers to achieve the throughput needed to service multiple brand owners simultaneously. Predictive-maintenance dashboards stream sensor data to cloud servers, alerting technicians before micro-stops snowball into hour-long outages.

The cosmetic packaging machinery market size associated with semi-automatic lines is not shrinking in absolute terms, yet its relative weight declines as lease-to-own models dilute capital hurdles. Semi-automatic fillers now ship with upgrade paths that add robotic capping modules when volumes justify. This modular strategy reduces obsolescence risk and keeps initial invoices below USD 150,000, an amount compatible with venture-backed start-ups. Nevertheless, once monthly order volumes pass 100,000 units, most operators migrate to fully automatic configurations to recover labor, energy, and scrap savings.

By Packaging Type: Tubes and Pouches Ride Refill Economics

Bottles and pumps hosted 34.79% of the market share in 2025, whereas tubes, sachets, and pouches are advancing at a 5.78% CAGR over 2026-2031. Refillable cartridges and single-dose pouches align with consumers who seek to reduce waste without compromising hygiene. Machinery dedicated to tubes must now handle wall thicknesses below 300 microns and adjust sealing parameters in milliseconds, tasks that are impossible for legacy thermal knives. The cosmetic packaging machinery market for tube fillers is therefore capturing incremental capex as brands localize production to avoid tariffs on empty containers.

Flexible films also support cost-effective sampling programs, enabling marketers to seed social media influencers without shipping heavy glass jars. Servo-driven tension control maintains print registration, even on contoured pouches, ensuring shelf impact. Rigid jars continue to dominate rich balms and scrubs, but their share erodes where airlines enforce 100-milliliter liquid limits. Brands consequently reformat hero SKUs into 30-gram pods, compelling OEMs to integrate scale weighers and nitrogen flushers on the same frame.

By Cosmetic Product: Hair-Care Accelerates on Salon Premiumization

Skin-care retained 38.94% share in 2025, buoyed by demand for airless pumps that shield retinol and vitamin C from oxidation. Yet hair care is the fastest-growing segment, with a 6.02% CAGR through 2031. Sulfate-free shampoos foam more readily, so gravity-fed fillers risk bubble formation that disrupts cap torque. Servo-controlled bottom-up nozzles solve this problem, reducing rework and elevating equipment prices. The cosmetic packaging machinery market share for hair-care lines will therefore widen as salons upsell bond-repair treatments and color-safe conditioners.

Make-up manufacturers chase sustainability targets with magnetic refill pans, requiring precision stamping and pick-and-place robots to avoid contaminating surface finishes. Fragrance bottlers continue to rely on crimping heads capable of ±0.05-millimeter positional accuracy to stop propellant leaks. Specialty segments such as men’s grooming integrate aluminum tubes that require lower crimp force and anodized surface coatings, encouraging equipment suppliers to diversify head materials.

Geography Analysis

North America leads the cosmetic packaging machinery market with 39.87 % of market share in 2025, supported by mature contract-manufacturing infrastructure and robust replacement demand. Domestic brands target two-day shipping windows, driving investment in digital changeover technologies that compress downtime to single-digit minutes. The United States benefits from equipment-financing options unavailable in many emerging markets, allowing mid-cap producers to automate earlier in their life cycles. Canada’s clean-energy incentives lower operating costs for servo-rich lines, improving net present value calculations.

Asia-Pacific trails in absolute revenue but posts the fastest 6.11 % CAGR through 2031. China adds capacity to sidestep tariffs on imported finished goods, and provincial grants subsidize vision-inspection retrofits. India’s cosmetics ecosystem, centered in Bengaluru and Mumbai, installs digital presses that print 2,500-unit label runs, ideal for regional formulations sold through e-commerce. Southeast Asian assemblers, however, face export controls on advanced servos, lengthening lead times and prompting multinational customer pivots to joint ventures with Japanese or South Korean integrators.

Europe ranks third in revenue yet sets global compliance benchmarks. The EU microplastics ban triggers a spike in mono-material tube demand, fostering machinery upgrades that measure moisture in real time to avoid laminate delamination. OEMs headquartered in Italy and Germany accelerate R and D spending on paper-based laminates even as regional order books flatten near term. South America grows more slowly due to currency volatility and high loan rates, though Brazil and Argentina still import flexible fillers to serve indie brands. The Middle East and Africa adopt duty-free-zone strategies to attract contract-manufacturing investments, while Mexico captures near-shoring flows under the USMCA agreement by offering dual-plant footprints that cut border dwell times.

Competitive Landscape

The cosmetic packaging machinery market is fragmented. Each leverages installed bases to sell multi-year service contracts that include 24-hour remote monitoring. Asian assemblers undercut list prices by up to 40 %, but premium brands often select European lines for their proven validation documents. Platform architectures that allow filling, capping, and labeling modules to slide onto a common backbone dominate recent launch announcements.

Technology differentiation centers on vision-inspection fidelity, changeover speed, and digital-twin accuracy. A 2024 camera platform cut false rejects by 40 % in high-refraction bottles, an advantage that justifies premium per-camera pricing. Leasing and usage-based contracts attract cash-focused indie brands, but they also shift residual-value risk back to suppliers, increasing emphasis on modular designs that can retrofit future compliance features. Patent filings surge in servo-tension control for paper-laminate tubes and in AI-based defect classification, signaling where next-generation margins will accrue.

Mergers and acquisitions continue. Duravant announced its Pattyn buyout to deepen horizontal form-fill-seal know-how, while Sidel commissioned an aseptic PET line in India to anchor future aftermarket sales. Partnerships proliferate: Aptar teamed with Pinard on an airless PET bottle with 40 % less plastic; Silgan prepared a recyclable tube-pump line that ships in November 2026. Disruptors such as Unmade use cloud dashboards and modular fillers to serve 50-unit pilot runs, forcing incumbent OEMs to reassess minimum-order thresholds.

Cosmetic Packaging Machinery Industry Leaders

Syntegon Technology GmbH

IMA Industria Macchine Automatiche SpA

Marchesini Group SpA

Coesia S.p.A (PackSys Global etc.)

ProMach Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Sidel Group commissioned an aseptic PET filling line in India, allowing a multinational client to localize shelf-stable cosmetic production and cut lead times by up to eight weeks.

- February 2026: Cosmogen unveiled a refillable powder compact at Paris Packaging Week featuring a magnetic closure and a replaceable inner pan that trims packaging mass by 65 %.

- January 2026: Nuon Medical showcased NFC-enabled cosmetic jars at CES 2026 that prompt automatic reorders through a mobile application.

- October 2025: Silgan Dispensing Systems announced the ERA recyclable tube pump, with commercial production slated for Nov 2026.

Global Cosmetic Packaging Machinery Market Report Scope

Cosmetics include products such as lipstick, eye shadow, and other makeup, as well as nail polish, facial creams, skin lotions, and shampoo. Even perfumes and toothpaste could be considered cosmetics. The products packaged in the cosmetic industry are wide and varied, and the packaging machines used to pack them are identified as cosmetic packaging machinery. The market defines revenue generated from the sale of cosmetic packaging machinery across various regions, packaged with multiple materials such as paper, glass, and plastic.

The Cosmetic Packaging Machinery Market Report is Segmented by Machine Type (Form/Fill/Seal, Labelling, Capping, Wrapping and Bundling, Cartoning and Case-Packing, Inspection and Vision Systems, and Other Machine Types), Automation Level (Fully-Automatic, and Semi-Automatic), Packaging Type (Rigid Containers and Jars, Tubes/Sachets/Pouches, Bottles/Pumps/Dispensers, and Flexible Films and Wraps), Cosmetic Product (Skin-Care, Hair-Care, Make-Up and Color Cosmetics, Fragrances and Deodorants, and Other Cosmetic Products), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

By Machine Type

| Form/Fill/Seal Machinery |

| Labelling Machinery |

| Capping Machinery |

| Wrapping and Bundling Machinery |

| Cartoning and Case-Packing Machinery |

| Inspection and Vision Systems |

| Other Machine Types |

By Automation Level

| Fully-Automatic Systems |

| Semi-Automatic Systems |

By Packaging Type

| Rigid Containers and Jars |

| Tubes, Sachets and Pouches |

| Bottles, Pumps and Dispensers |

| Flexible Films and Wraps |

By Cosmetic Product

| Skin-Care Products |

| Hair-Care Products |

| Make-Up and Color Cosmetics |

| Fragrances and Deodorants |

| Other Cosmetic Products |

By Geography

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Kenya | ||

| Rest of Africa | ||

| By Machine Type | Form/Fill/Seal Machinery | ||

| Labelling Machinery | |||

| Capping Machinery | |||

| Wrapping and Bundling Machinery | |||

| Cartoning and Case-Packing Machinery | |||

| Inspection and Vision Systems | |||

| Other Machine Types | |||

| By Automation Level | Fully-Automatic Systems | ||

| Semi-Automatic Systems | |||

| By Packaging Type | Rigid Containers and Jars | ||

| Tubes, Sachets and Pouches | |||

| Bottles, Pumps and Dispensers | |||

| Flexible Films and Wraps | |||

| By Cosmetic Product | Skin-Care Products | ||

| Hair-Care Products | |||

| Make-Up and Color Cosmetics | |||

| Fragrances and Deodorants | |||

| Other Cosmetic Products | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| France | |||

| United Kingdom | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Kenya | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the cosmetic packaging machinery market by 2031?

The market is forecast to reach USD 4.19 billion by 2031.

Which machine type is growing fastest in cosmetic packaging applications?

Labeling equipment, driven by serialization and digital-engagement mandates, is advancing at a 5.27% CAGR.

Why are brands investing in fully automatic packaging lines?

Fully automatic systems cut changeover time, embed predictive maintenance, and deliver uptime needed for multi-shift operations.

How do sustainability rules influence equipment design?

EU and U.S. regulations favor mono-material tubes and lightweight formats, prompting machines with precise heat-seal and moisture-control features.

What regions will add the most new packaging-machinery capacity?

Asia-Pacific, especially China and India, will post the highest 6.11% CAGR as local fill-finish plants bypass tariffs.

How are suppliers addressing the technician shortage?

OEMs integrate remote diagnostics and augmented-reality guides that allow fewer, less experienced staff to maintain complex lines.

Page last updated on: