Kitting And Assembly Packaging Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

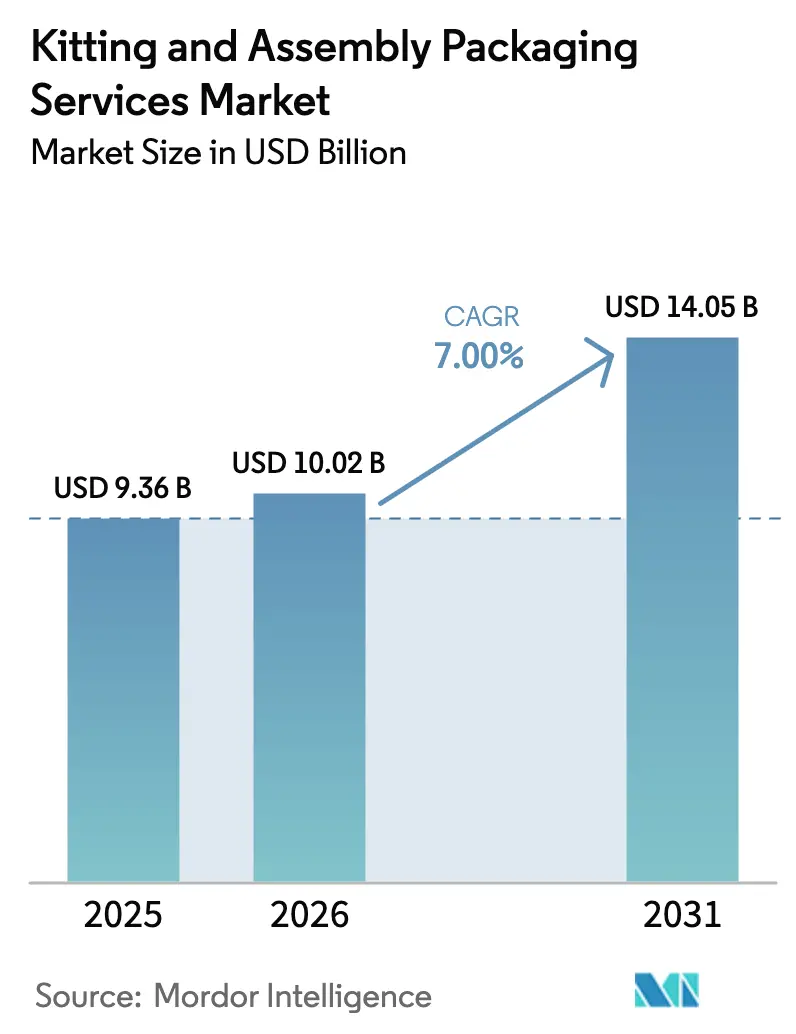

| Market Size (2026) | USD 10.02 Billion |

| Market Size (2031) | USD 14.05 Billion |

| Growth Rate (2026 - 2031) | 7.00% CAGR |

| Fastest Growing Market | Asia |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Kitting And Assembly Packaging Services Market Analysis by Mordor Intelligence

The Kitting and Assembly Packaging Services Market size was valued at USD 9.36 billion in 2025 and estimated to grow from USD 10.02 billion in 2026 to reach USD 14.05 billion by 2031, at a CAGR of 7.00% during the forecast period (2026-2031). Robust outsourcing demand from electronics, healthcare, and direct-to-consumer brands underpins steady expansion, while 3PL providers scale value-added operations that combine light manufacturing with advanced fulfillment. Automation investments, particularly in cobotics and vision-guided picking, are reducing unit costs, mitigating the impact of persistent labor shortages in core logistics hubs. Parallel momentum stems from returnable-kit programs that align with extended producer responsibility mandates, along with heightened traceability obligations in regulated sectors, which elevate barriers to entry. Market participants that integrate cloud-native inventory management and real-time serialization are capturing disproportionate share as omnichannel retailers tighten service-level agreements and push single-day delivery norms.

Key Report Takeaways

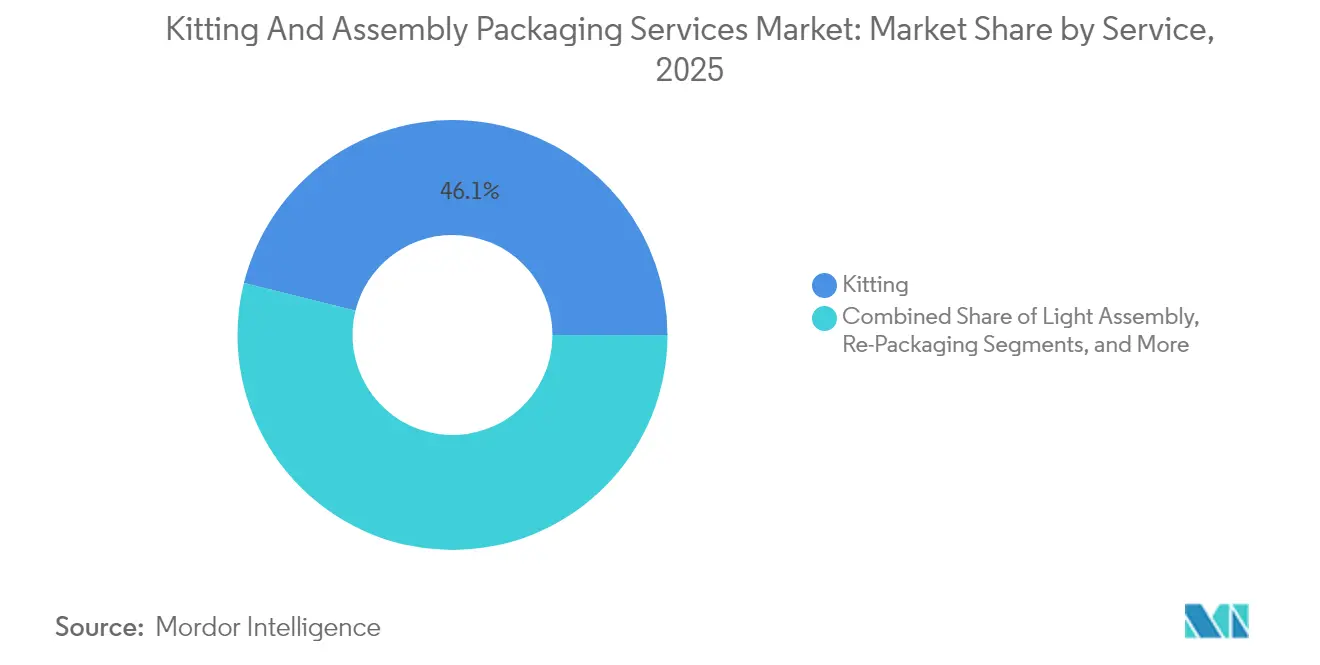

- By service type, kitting captured 46.12% of the Kitting and Assembly Packaging Services Market share in 2025.

- By material, Kitting and Assembly Packaging Services Market size for composites is projected to grow at a 9.55% CAGR between 2026–2031.

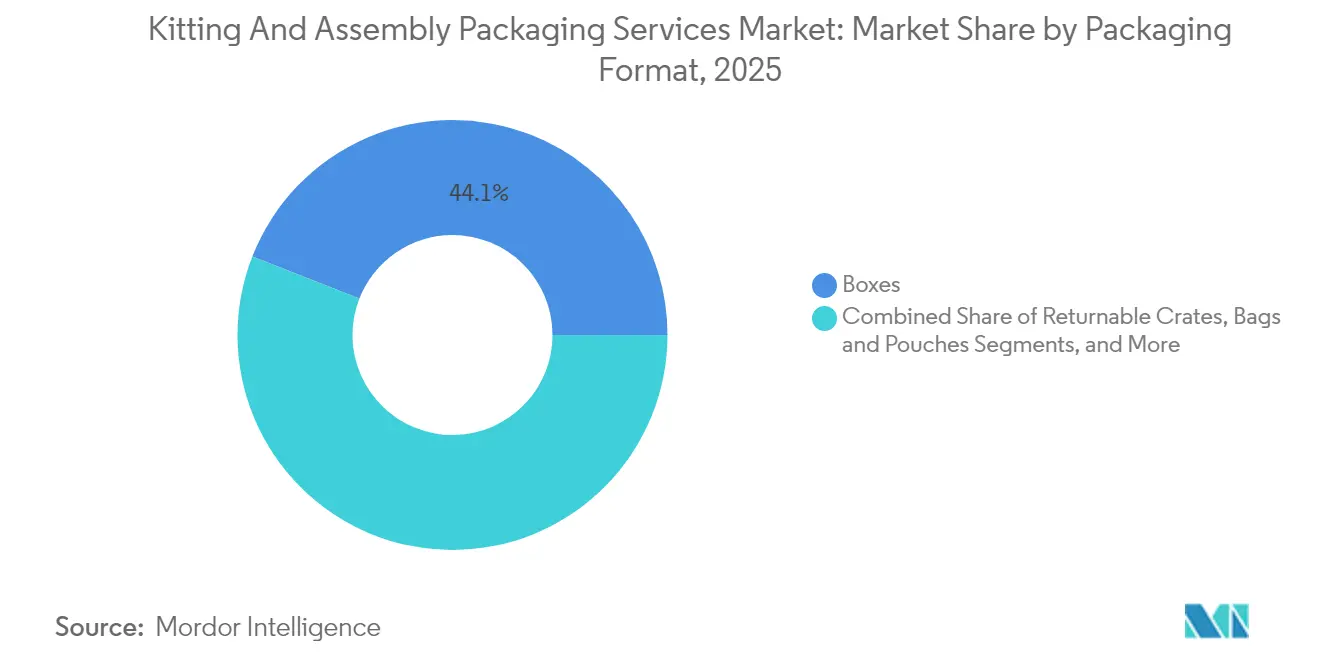

- By packaging format, boxes captured 44.05% of the Kitting and Assembly Packaging Services Market share in 2025.

- By end-user industry, the Kitting and Assembly Packaging Services Market size for electronics is projected to grow at a 8.91% CAGR between 2026–2031.

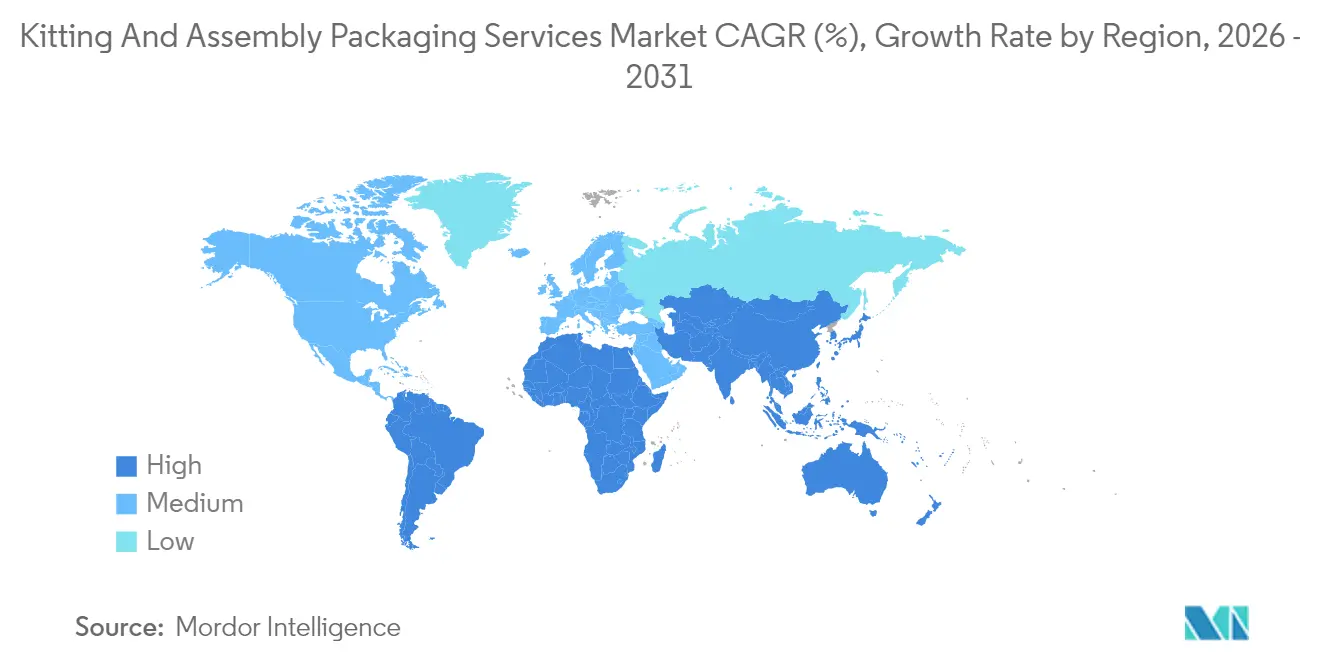

- By geography, North America captured 34.10% of the Kitting and Assembly Packaging Services Market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Kitting And Assembly Packaging Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Subscription-box and D2C fulfillment surge | +1.8% | North America, Europe, global spillover | Medium term (2-4 years) |

| Omni-channel retail and micro-fulfillment growth | +1.5% | APAC, North America | Short term (≤ 2 years) |

| SKU-level compliance in healthcare and aerospace | +1.2% | North America, Europe, expanding APAC | Long term (≥ 4 years) |

| Cost-down pressure shifting OEMs to outsourcing | +1.4% | Global, strongest in APAC hubs | Medium term (2-4 years) |

| Industry 4.0 smart packaging lines | +1.1% | Developed markets, emerging adoption | Long term (≥ 4 years) |

| Sustainability mandates favor returnable kits | +0.9% | Europe leading, global uptake | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rise of Subscription-Box and D2C Fulfillment Models

Rapid scaling of subscription commerce demands agile kitting networks that can support hundreds of product permutations within a single monthly cycle. Providers are responding with modular conveyors, automated carton-erection cells, and SKU-agnostic pick-to-light stations that enable single-piece flow at high velocity. Variable demand patterns encourage flexible labor scheduling, yet growing wage inflation accelerates the adoption of robotics that can operate continuously and reduce error rates. Brand owners are increasingly relying on the kitting and assembly packaging services market for personalized inserts printed on demand, which enhances unboxing experiences while minimizing inventory write-offs. Compliance with country-specific e-commerce packaging waste rules adds complexity that favors 3PLs with dedicated regulatory teams.

Growth of Omni-Channel Retail and Micro-Fulfillment Centers

Urban micro-fulfillment nodes compress storage footprints to under 10,000 square feet, necessitating vertical shuttle systems and compact sortation that merge consumer parcel flows with store-replenishment cartons. The kitting and assembly packaging services market addresses this density challenge with all-in-one workcells that can erect, pack, weigh, and label within a 1.5-square-meter space. Same-day delivery windows are tightening cut-off times, so 3PLs position technicians on-site to dynamically adjust box dimensions, thereby shaving shipping volume and emissions. Retailers reward partners who integrate order-management APIs for inventory accuracy, with a variance threshold of under 99.8%. High real-estate costs reinforce outsourcing, because micro-fulfillment leases exceed suburban rates by 30%, relegating non-core activities to specialized providers.

Stringent SKU-Level Compliance in Healthcare and Aerospace

Serialization under the Drug Supply Chain Security Act requires unique identifiers on every saleable unit, propelling investments in camera-based verification and blockchain event logging. Aerospace counterparts mirror these traceability standards for flight-safety components, driving demand for controlled-environment kitting spaces with Foreign Object Damage (FOD) protocols in place. Providers in the kitting and assembly packaging services market introduce zero-defect regimes, utilizing statistical process control and validated software, which enables them to pass routine audits by the FDA and the European Medicines Agency. Capital outlays for line-level aggregation modules can exceed USD 2 million per facility, dissuading smaller entrants. Consequently, market consolidation intensifies as compliance becomes a decisive competitive moat.[1]Aerospace Industries Association, “Aerospace Facts and Figures 2024,” aia-aerospace.org

Cost-Down Pressure Shifting OEMs to Outsourcing

Short product cycles in electronics compress breakeven horizons on dedicated packaging assets. Total cost-of-ownership analyses indicate 15–20% lifecycle savings when late-stage assembly is migrated to external partners located adjacent to final test sites. Providers manage interchangeable tooling and electrostatic-safe workcells, allowing OEMs to launch variants without capital spikes. Fixed costs translate into variable fees, synchronizing expense curves with revenue recognition. The kitting and assembly packaging services market thus evolves from a logistics adjunct to a profit-leverage lever, capable of absorbing demand volatility and de-risking balance sheets, particularly for semiconductor players that operate at 90% factory utilization.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Labor shortages and wage inflation in 3PL hubs | −1.3% | North America, Western Europe | Short term (≤ 2 years) |

| Volatility in corrugated and polymer prices | −0.8% | Global, variable by region | Medium term (2-4 years) |

| Rising trade-lane disruptions and freight costs | −0.7% | APAC export corridors | Short term (≤ 2 years) |

| Cyber-security risks in automated facilities | −0.4% | Highly automated markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Labor Shortages and High Wage Inflation in 3PL Hubs

Unemployment rates below 4% in major logistics regions constrain hiring pipelines, while required technical aptitude rises as machinery becomes data-driven. Average hourly wages for packaging line technicians in the United States increased to USD 27.40 in 2024, up 18% year-over-year, which is straining cost-plus contracts. Providers bridge gaps with tuition-reimbursement programs and augmented-reality training tools that reduce onboarding time by 40%. In the near term, margin compression persists until depreciation of new automation exceeds incremental wage increases. Regional disparities also emerge: Central European facilities tap into migrant labor pools, whereas U.S. coastal metros pivot faster toward robotics densities surpassing 250 units per 10,000 workers.

Volatility in Corrugated and Polymer Prices

Pulp supply shocks and energy-price swings have pushed kraftliner costs above USD 900 per metric ton twice since 2024, complicating six-month price locks common in retail contracts. Recycled high-density polyethylene quotes similarly fluctuated 25% within single quarters, influenced by resin import tariffs and refinery outages. To stabilize earnings, operators in the kitting and assembly packaging services market adopt index-linked pass-through clauses and diversify vendors across continents. Larger players forward-purchase commodities under multi-year framework agreements, leveraging scale to hedge risk. Smaller firms rely on lightweighting designs and digital print flexibility to curb raw material intensity, yet still face working capital strain during extended price peaks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Expanding Assembly Reshapes Value Propositions

Light-assembly revenue is rising at an 8.82% CAGR, narrowing the historical gap with kitting, which retained a 46.12% share in 2025. The kitting and assembly packaging services market size for light assembly reached an estimated USD 2.83 billion in 2025, reflecting OEM appetite for outsourcing printed-circuit board sub-assemblies, cable harness insertion, and firmware flashing close to end markets. Providers deploy electrostatic-discharge flooring and ISO-class clean zones, enabling them to meet IPC-610 standards required by premium electronics brands. Over the forecast horizon, multi-SKU lines shift toward algorithm-driven work sequencing, which balances takt times and reduces changeover delays by 35% on average.

Kitting continues to anchor vendor relationships because it integrates demand forecasting, component staging, and postponement strategies that minimize finished goods inventory. Retail seasonality drives peaks of 400% above base volumes, prompting the widespread adoption of shuttle robots that track slot utilization in real-time. While labor intensity remains higher than in automated assembly, ROI on low-capital kitting cells stays attractive for pilot runs and region-specific bundles. Sustainability imperatives encourage kitting providers to champion reusable dunnage and QR-code instruction sheets, cutting single-use inserts by half within two years. Continuous improvement programs that apply Six Sigma methodologies maintain defect rates below 150 parts per million, reinforcing customer loyalty in over-equipped marketplaces.

By Material: Sustainable Composites Move Center Stage

Composites, such as glass-fiber-reinforced polypropylene, are growing at a 9.55% CAGR, although corrugated paper still held a 41.12% market share in the kitting and assembly packaging services market in 2025. Automotive tier-one suppliers specify returnable composite totes that achieve 40+ trip rotations, delivering lifetime cost savings compared to single-trip corrugated boxes. The material’s dimensional stability under humidity swings makes it attractive for coastal distribution centers, and embedded RFID chips streamline asset tracking.

Conversely, corrugated packaging remains indispensable for parcel networks because it strikes a balance between cushioning, printability, and curbside recyclability. Operators invest in high-speed digital presses that print 600 dpi graphics directly on board-fed at 200 linear meters per minute, supporting brand mandates for personalized product launches. Sustainability targets accelerate the shift to recycled-content liners exceeding 80%, enabled by continuous pulping innovations. Bio-based barrier coatings are now replacing polyethylene laminates in food-grade boxes, aligning with EU packaging waste directives. Cost management remains essential as pulp prices fluctuate; predictive analytics tools forecast demand and allocate linerboard rolls efficiently, resulting in a 5–7% annual reduction in material waste.

By Packaging Format: Returnable Systems Accelerate Circularity

Returnable crates, advancing at an 8.41% CAGR, exemplify circular-economy economics that cut lifetime material consumption by up to 70%. Automotive OEMs extend crate leases over five-year vehicle programs, integrating serial-number scanning to log reverse-logistics mileage and preventive-maintenance intervals. Sensors embedded in crate walls transmit shock and tilt data, alerting operators to handling anomalies that could compromise precision components.

Boxes dominate with a 44.05% share of the kitting and assembly packaging services market size in 2025, supported by e-commerce parcel growth that exceeds 12 billion U.S. shipments annually. Dimensional-weight pricing drives adoption of right-sized cartons produced on demand by CNC slotters, trimming transport cube utilization. Blister packs, clam-shells, and thermoforms remain critical for theft-prone or tamper-evident SKUs in pharmaceuticals and consumer electronics, yet their flexible counterparts, notably stand-up pouches, are encroaching through barrier-film advances. Equipment vendors respond with modular tooling platforms that switch from blister to pouch within 15 minutes, amplifying line agility.

By End-user Industry: Electronics Sets Pace for Advanced Services

Electronics posted the fastest 8.91% CAGR, buoyed by semiconductor demand and the proliferation of smart devices. Trace-sensitive Surface-Mount Technology components necessitate vacuum-sealed moisture-barrier bags with desiccants calibrated to JEDEC J-STD-033 standards. The kitting and assembly packaging services market co-locates final pack-out lines within chip assembly campuses, thereby shrinking lead times and reducing in-process inventory. Quality control integrates X-ray counting to verify component levels in reels, limiting short ships that halt production. Consumer goods, although still the largest at 38.62%, mature as private-label programs internalize simple kitting. Providers differentiate themselves through value-added tasks, such as influencer co-packing and limited-edition bundling, which billionaire consumer-facing firms use to retain brand stickiness. Healthcare packaging demands ISO 13485 certification, pushing providers to validate cold-chain inserts and Class 7 cleanroom assembly under Good Manufacturing Practice guidelines. Aerospace volumes remain niche but yield premium margins, as precision-machined parts require anti-corrosion vapor-phase inhibitors and custom foam cavities water-jet cut to micron tolerances.

Geography Analysis

North America generated 34.10% of global revenue in 2025. Nearshoring intensifies in Mexico, where labor rates are 25–30% lower than U.S. averages, and new maquiladora sites reduce cross-border transit to under 48 hours. U.S. providers integrate USMCA-compliant content tracking, ensuring automotive clients can trace the regional value content of components. Canada’s Pacific ports facilitate the trans-loading of Asian imports into domestic parcel networks, spurring investments in Vancouver-area multi-client kitting hubs equipped with automated storage/retrieval systems.

The Asia-Pacific region registers the highest 10.95% CAGR, reflecting accelerated industrialization and the adoption of digital retail. China’s Guangdong province is piloting “smart-factory clusters,” where packaging cells synchronize with MES platforms to feed real-time production data into upstream SMT lines. India offers a 50% capital subsidy program for packaging automation under the Production Linked Incentive scheme, luring multinational medical device manufacturers. [2]Asian Development Bank, “Asia’s Evolution as Global Manufacturing Hub,” adb.org South Korea pioneers 5G-enabled cobots that improve overall equipment effectiveness beyond 85%, a technology that regional peers rapidly emulate. ASEAN regional integration under the Regional Comprehensive Economic Partnership simplifies material transfers, lowering tariff burdens on crate returns within cross-border loops.

Europe, a mature yet innovation-driven territory, enforces the EU Circular Economy Action Plan that caps land-filled packaging waste and pushes recovery targets beyond 70% by 2030. Germany’s Green Dot fees incentivize weight reductions, so providers adopt algorithmic design tools to optimize panel thickness. The United Kingdom recalibrates customs declarations post-Brexit, leading to dual stock allocations held in mainland Europe and on the island to avert shipment delays. Scandinavian countries lead bio-polymer adoption, experimenting with mycelium-based inserts that biodegrade within 45 days under industrial composting.

Competitive Landscape

Market fragmentation persists, yet the top five providers collectively control roughly 35% of global revenue, signaling moderate concentration. UPS Supply Chain Solutions, FedEx, Deutsche Post DHL, XPO, and CEVA Logistics integrate end-to-end digital platforms that centralize demand planning, inventory visibility, and KPI dashboards, providing a comprehensive view of operations. Mid-tier specialists carve defensible niches in pharmaceutical serialization, aerospace clean-room assembly, or sustainable crate pooling where domain expertise trumps scale.

Technology leadership drives differentiation: leading players deploy AI-guided robotic arms capable of mixed-SKU picking at 600 units per hour, outpacing manual rates by threefold. Vision systems paired with edge computing verify label accuracy instantaneously, achieving near-zero defects. Patents filed for adaptive grippers and carton rightsizing algorithms increased by 23% in 2024, underscoring the competitive intensity.

Strategic alliances are proliferating as capital-intensive automation fuels merger and acquisition activity. Large integrators acquire regional assets to secure cold-chain competencies or regulatory certifications, illustrated by FedEx’s purchase of BioTech Logistics.[3]FedEx Corporation, “Press Release—FedEx Acquires BioTech Logistics,” fedex.com Private-equity interest intensifies, focusing on providers with proprietary software that fosters enduring customer relationships through API integrations and predictive analytics modules.

Kitting And Assembly Packaging Services Industry Leaders

Ryder System, Inc.

Deutsche Post AG

XPO, Inc.

Geodis S.A.

FedEx Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Deutsche Post DHL Group committed EUR 200 million (USD 213 million) toward automated packaging facilities in Singapore and Malaysia, featuring collaborative robots and AI-driven inventory optimization.

- October 2025: FedEx Corporation acquired BioTech Logistics for USD 450 million, broadening temperature-controlled kitting and adding FDA-validated suites.

- September 2025: XPO Inc. rolled out its Smart Assembly platform across North American sites, leveraging machine-learning analytics to cut assembly cycle times by 25%.

- August 2025: Ryder System Inc. partnered with Berkshire Grey to install robotic workcells in 15 U.S. facilities, a USD 75 million automation investment.

Global Kitting And Assembly Packaging Services Market Report Scope

| Kitting |

| Light Assembly |

| Re-Packaging |

| Labelling |

| Other Services |

| Corrugated Paper |

| Plastics |

| Metals |

| Composites |

| Other Materials |

| Boxes |

| Blister and Clamshells |

| Bags and Pouches |

| Returnable Crates |

| Other Packaging Formats |

| Consumer Goods |

| Healthcare and Pharma |

| Industrial and Aerospace |

| Electronics |

| Others End-user Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Service | Kitting | ||

| Light Assembly | |||

| Re-Packaging | |||

| Labelling | |||

| Other Services | |||

| By Material | Corrugated Paper | ||

| Plastics | |||

| Metals | |||

| Composites | |||

| Other Materials | |||

| By Packaging Format | Boxes | ||

| Blister and Clamshells | |||

| Bags and Pouches | |||

| Returnable Crates | |||

| Other Packaging Formats | |||

| By End-user Industry | Consumer Goods | ||

| Healthcare and Pharma | |||

| Industrial and Aerospace | |||

| Electronics | |||

| Others End-user Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the kitting and assembly packaging services market by 2031?

The market is forecast to reach USD 14.05 billion by 2031, growing at a 7.00% CAGR.

Which region is expanding the fastest?

Asia-Pacific is set to post an 10.95% CAGR as its manufacturing base deepens and e-commerce accelerates.

Which service type is growing quickest?

Light assembly leads with an 8.82% CAGR as OEMs outsource late-stage production steps.

How do sustainability mandates influence material choice?

They spur the adoption of composites and high-recycled-content corrugated materials, while returnable packaging reduces single-use waste.

What technologies are reshaping operations?

AI-enabled robotics, real-time serialization, and cloud inventory platforms are elevating throughput and compliance.

Which end-user sector offers the strongest growth opportunity?

AI-enabled robotics, real-time serialization, and cloud inventory platforms are elevating throughput and compliance.

Page last updated on: