Surgical Retractors Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

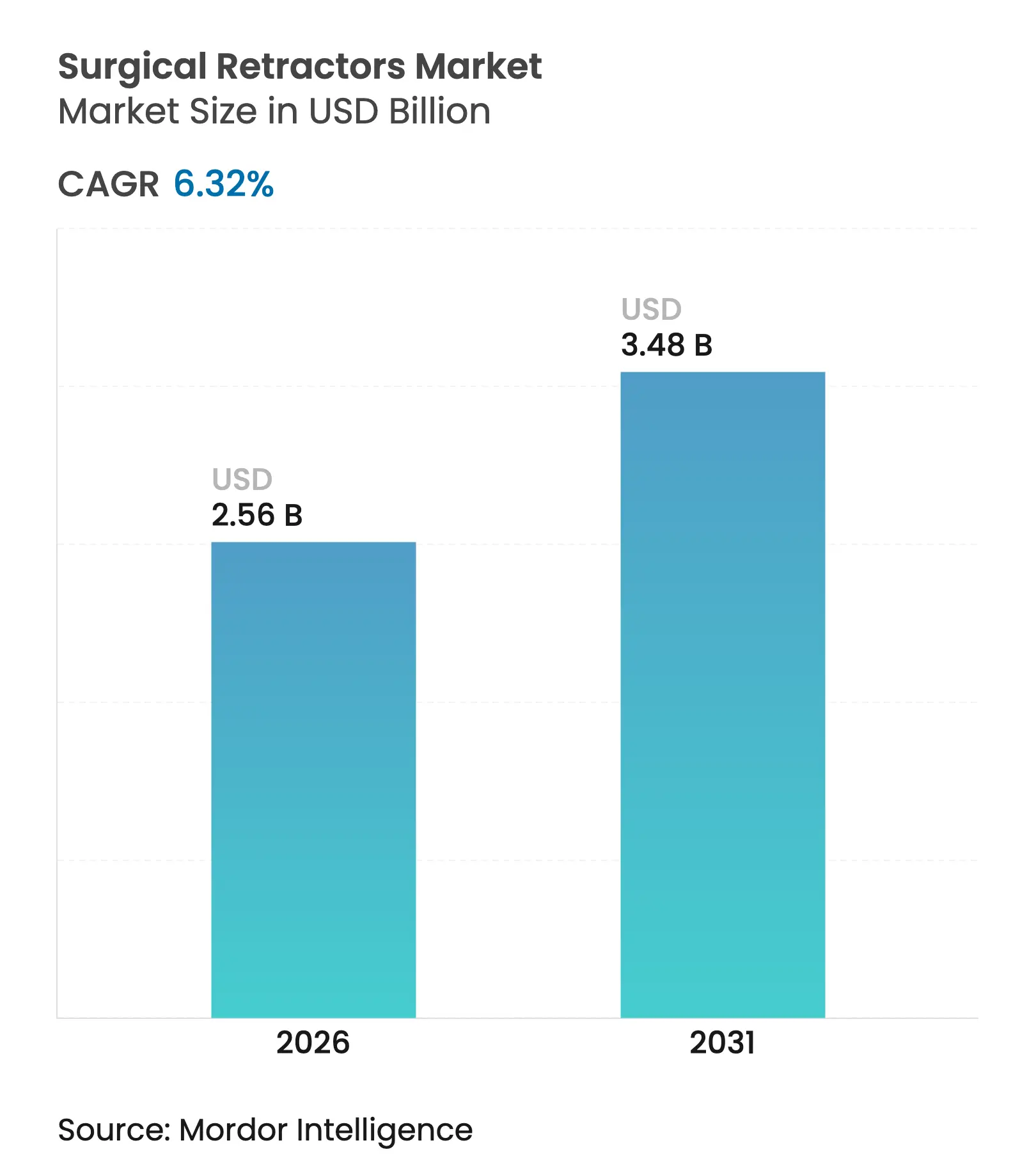

| Market Size (2026) | USD 2.56 Billion |

| Market Size (2031) | USD 3.48 Billion |

| Growth Rate (2026 - 2031) | 6.32 % CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Surgical Retractors Market Analysis by Mordor Intelligence

Strong caseload recovery, heightened adoption of minimally invasive surgery, and robust innovation from LED illumination to polymer frames anchor growth in high-income and emerging regions alike. Rapid demographic aging lifts orthopedic and cardiovascular workloads, while ambulatory surgical centers (ASCs) fuel sales of compact, procedure-agnostic instruments. Procurement teams also favor self-retaining and single-use variants that offset staff shortages and sterilization bottlenecks, giving technologically advanced suppliers a pricing edge. Simultaneously, surgeons increasingly align with polymer-based, weight-saving designs that reduce fatigue in long operations, cementing the strategic importance of material science advances for global vendors. The surgical retractors market, therefore, blends resilient base demand with clear upgrade cycles around ergonomics, illumination, and infection control.

Key Report Takeaways

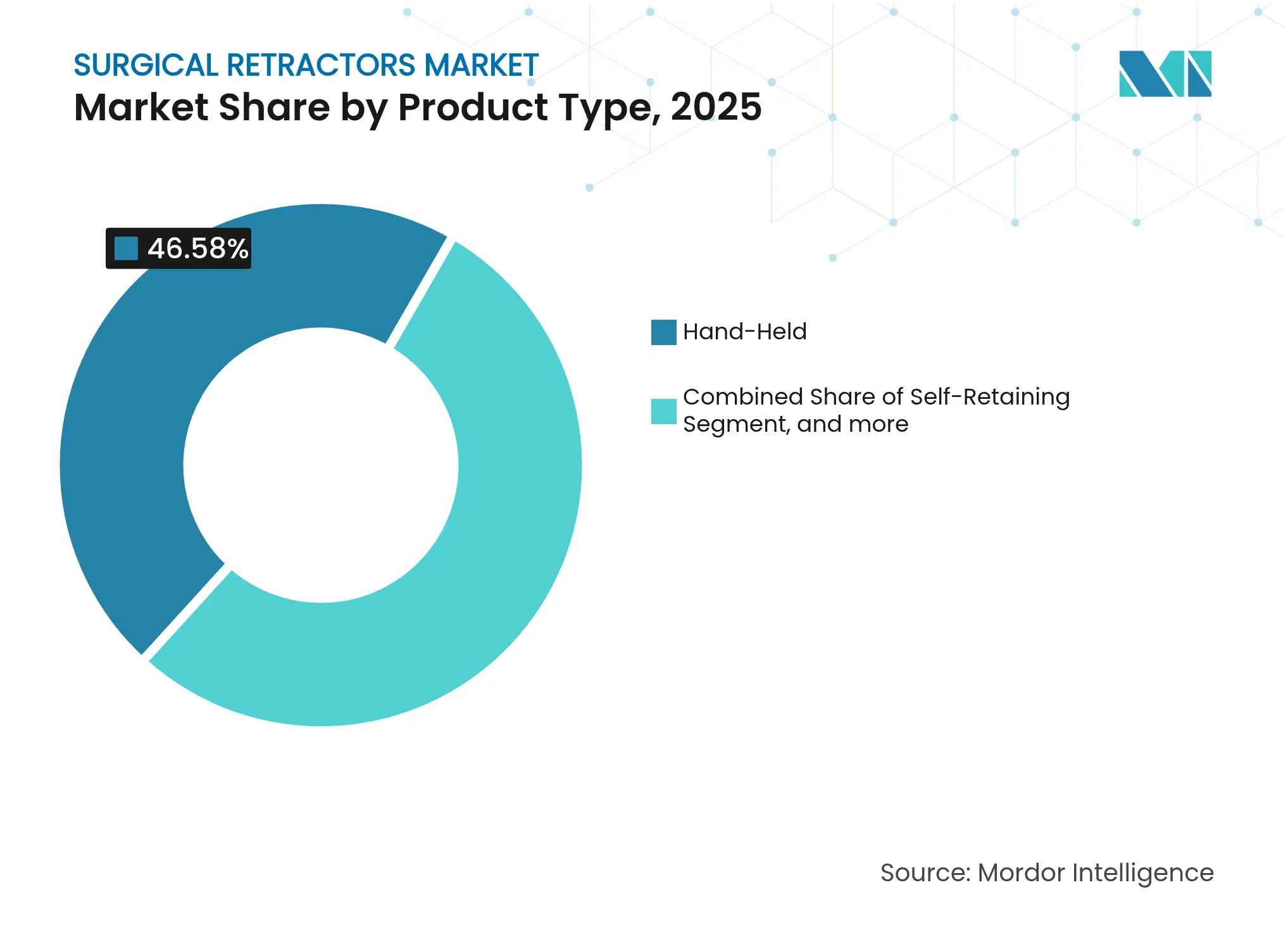

- By product type, self-retaining systems captured 53.42% of the surgical retractors market share in 2025, whereas illuminated/fiber-optic units are poised to grow at 7.68% CAGR through 2031.

- By material, stainless steel commanded a 56.21% share of the surgical retractors market in 2025, while high-performance polymers are projected to rise 9.55% CAGR between 2026 and 2031.

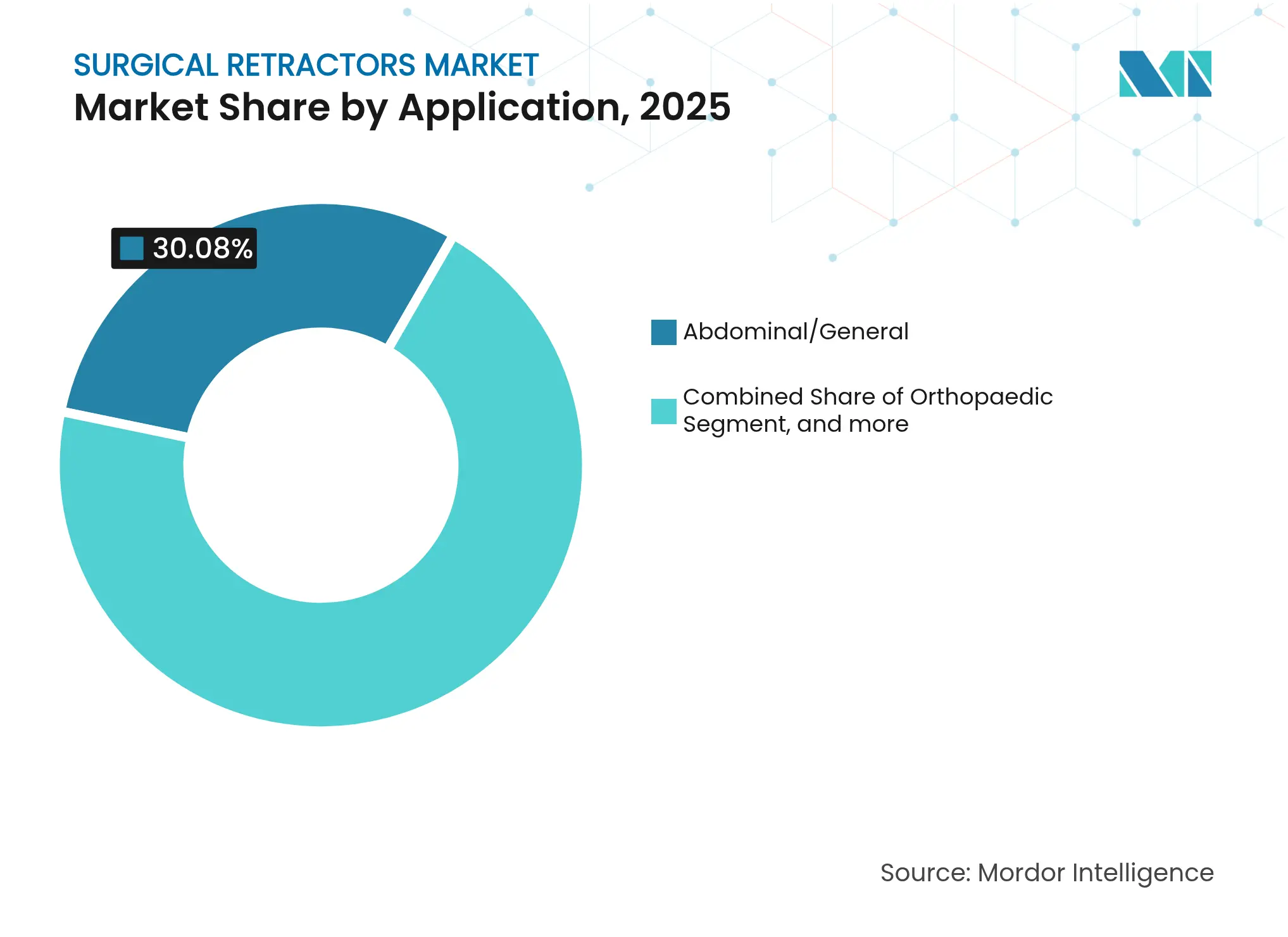

- By application, abdominal/general surgery accounted for a 30.08% share of the surgical retractors market size in 2025, and neurological procedures are advancing at a 9.92% CAGR through 2031.

- By end user, hospitals held 60.98% revenue share of the surgical retractors market in 2025; ASCs exhibit the fastest expansion at 8.12% CAGR to 2031.

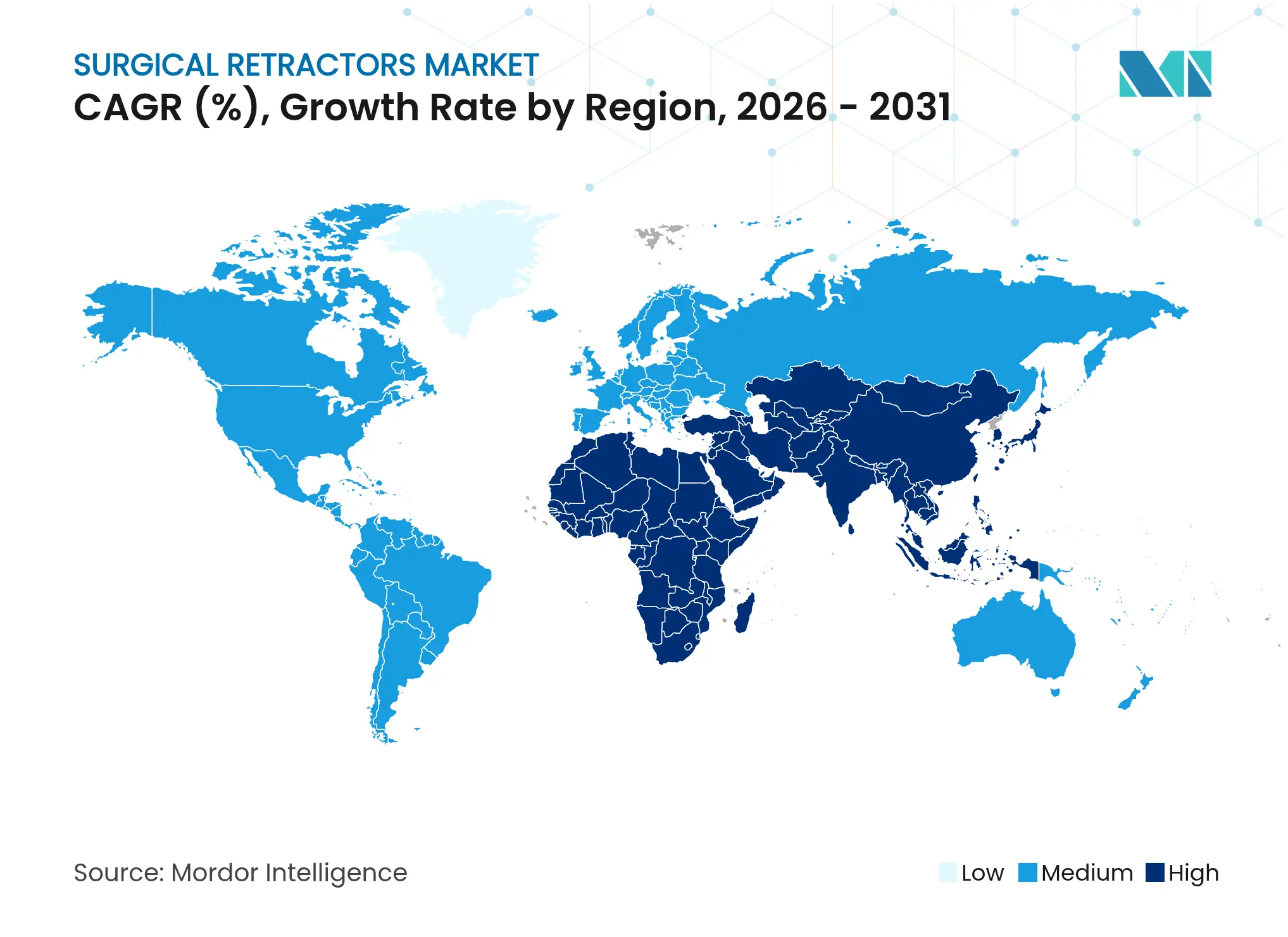

- By geography, North America led the surgical retractors market in 2025, with a 39.28% revenue share; Asia-Pacific was the fastest-growing region, with a 8.95% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Surgical Retractors Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rapid Rise in

Elective & Trauma Surgeries Post-COVID backlogs

Rapid Rise in

Elective & Trauma Surgeries Post-COVID backlogs

| +1.8% | Global, with acute impact in North America & Europe | Short term (≤ 2 years) |

(~) %

Impact on CAGR Forecast

:

+1.8%

|

Geographic

Relevance

:

Global, with

acute impact in North America & Europe

|

Impact

Timeline

:

Short term (≤

2 years)

|

Ageing

Population Fuelling Orthopaedic & Cardiovascular Procedures

Ageing

Population Fuelling Orthopaedic & Cardiovascular Procedures

| +1.5% | Global, concentrated in developed markets | Long term (≥ 4 years) | |||

Expansion of

Ambulatory Surgical Centers (ASCs) Growth in Emerging Countries

Expansion of

Ambulatory Surgical Centers (ASCs) Growth in Emerging Countries

| +1.2% | APAC core, spill-over to MEA | Medium term (2-4 years) | |||

Adoption of

Single-Use Illuminated Retractors

Adoption of

Single-Use Illuminated Retractors

| +0.9% | North America & EU, expanding to APAC | Medium term (2-4 years) | |||

Emergence of

AI-Guided Robotic Retractors

Emergence of

AI-Guided Robotic Retractors

| +0.7% | North America, selective EU markets | Long term (≥ 4 years) | |||

Increasing

Preference for Minimally Invasive Surgery (MIS)

Increasing

Preference for Minimally Invasive Surgery (MIS)

| +1.1% | Global | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Rapid Rise in Elective & Trauma Surgeries Post-COVID Backlogs

Sustained procedural deficits are pushing surgical departments to operate at elevated volumes well beyond historical peaks. Australia reported a cumulative gap of 42,307 joint replacements between 2020-2022, necessitating a 16% caseload jump by 2024 to restore equilibrium.[1]Medical Journal of Australia, “Operating backlog after COVID-19 and joint-replacement recovery,” mja.com.au Similar patterns in the United Kingdom prompted a new USD 64 million elective center designed for 6,500 extra annual operations. Extended backlogs translate into persistent demand for versatile self-retaining retractors capable of withstanding high throughput without compromising tissue protection. Hospitals prioritize modular sets that can shift quickly between orthopedics, cardiovascular, and general surgery, amplifying order books for premium brands. As a result, the surgical retractors market experiences a volume-led uplift in the short term, building a wider installed base that will require replacement in later cycles.

Ageing Population Fuelling Orthopedic & Cardiovascular Procedures

People aged 65+ now constitute more than 18% of populations in North America, Western Europe, and Japan, driving a disproportionate surge in joint arthroplasty and valve replacements. Older patients require longer exposure times and gentler tissue handling, stimulating surgeon preference for self-retaining frames that maintain consistent retraction while minimizing pressure hotspots. Polymer-based blades and silicone-coated edges reduce skin shear, directly addressing geriatric fragility concerns. This demographic tailwind is structurally embedded for the next two decades, ensuring continual upgrades across tertiary care centers. In parallel, robotic-assisted knee and cardiac procedures adopted in 2025 integrate digitally tracked retractor arms, reinforcing the long-term demand cycle in the surgical retractors market.

Expansion of Ambulatory Surgical Centers (ASCs) Growth in Emerging Countries

ASCs now perform 72% of US surgeries, offering 45-60% unit-cost savings relative to hospitals, with projected procedure growth of 25% over the coming decade.[2]Stryker, “PhotonGuide Adapt delivers brighter light with lower heat,” stryker.com Their lean staffing models favor single-surgeon workflows, elevating demand for hands-free retractors that free nurses for anesthesia tasks. Emerging economies emulate this high-throughput blueprint to widen elective surgery capacity while curbing public spending. Governments in India and Indonesia included ASCs in universal health schemes in 2024, unlocking fresh tenders for bulk-packaged illuminated retractors. Manufacturers that tailor lightweight, quick-sterilization sets for multiprocedure use are gaining early share, positioning the surgical retractors market for robust medium-term expansion in cost-sensitive geographies.

Adoption of Single-Use Illuminated Retractors

Infection control imperatives accelerated after several high-profile sterile-processing lapses revealed that 91% of errors originate at reprocessing stages. Single-use designs eliminate this variable, and when coupled with embedded LEDs they deliver consistent field lighting without towers or headlamps. Stryker’s PhotonGuide Adapt technology demonstrated 20% brighter illumination with zero heat build-up during trials in 2024.[3]Ambulatory Surgery Center Association, “ASC volume trends 2025,” ascasociation.org Early adopters report 30-minute turnover savings per case, a compelling metric for ASCs and high-volume trauma centers alike. The shift boosts average selling prices but reduces lifecycle service costs, generating a win-win scenario for providers and suppliers and cementing a differentiated growth pocket within the surgical retractors market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Price

Pressure from Low-Cost Imports

Price

Pressure from Low-Cost Imports

| -0.8% | Global, acute in price-sensitive markets | Short term (≤ 2 years) |

(~) %

Impact on CAGR Forecast

:

-0.8%

|

Geographic

Relevance

:

Global, acute

in price-sensitive markets

|

Impact

Timeline

:

Short term (≤

2 years)

|

Capital

Budget Constraints in Hospitals Investment

Capital

Budget Constraints in Hospitals Investment

| -0.7% | Global, severe in public healthcare systems | Short term (≤ 2 years) | |||

Steep

Learning Curve for Advanced Systems

Steep

Learning Curve for Advanced Systems

| -0.5% | Global, concentrated in emerging markets | Medium term (2-4 years) | |||

Sterilization

and Reusability Concerns

Sterilization

and Reusability Concerns

| -0.4% | Global, regulatory focus in developed markets | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Price Pressure from Low-Cost Imports

Chinese suppliers leveraging the Made in China 2025 policy now deliver entry-level retractor sets 40% below branded European equivalents, straining premium vendors’ margin structures. Tariffs on imported medical devices added 15% to US landed costs in 2024, prompting some buyers to trial low-cost alternatives. Nevertheless, surgeons remain wary of blade flexibility and locking-mechanism reliability, sustaining a two-tier market where commodity lines face deflation while specialty retractors retain pricing power. The pressure is most severe in Latin America and parts of Africa, where reimbursement reforms lag, marginally dampening the aggregate CAGR of the surgical retractors market.

Capital Budget Constraints in Hospitals

Inflation-driven wage hikes and post-pandemic debt left public hospitals with 12% lower capital budgets in 2025 versus 2023. Competing priorities, such as imaging suites and robotic platforms, delay new retractor fleet purchases. Procurement teams respond by negotiating extended payment terms and leaning on group purchasing organizations, which 93% of US hospitals plan to use by 2026. Vendors that bundle multi-specialty kits and offer service-inclusive leases secure wins, but overall, near-term volumes in slower macro regions may soften, tempering the otherwise upbeat outlook for the surgical retractors market.

Segment Analysis

By Product Type: Self-Retaining Systems Drive Market Leadership

Self-retaining frames controlled 53.42% of surgical retractors market share in 2025, propelled by the need to free surgical assistants’ hands during complex procedures. Their dominance comes from lock-in arms that maintain constant tension, reducing fatigue and standardizing exposure quality. Hospitals value the clear return on investment that stems from shorter operative times and better visualization. Illuminated and fiber-optic variants are climbing fastest at 7.68% CAGR through 2031 as LED costs drop and optics become slimmer. Disposable lighting strips integrated into polymer blades negate overhead towers, simplifying room setup in ASCs. Hand-held retractors remain indispensable in plastic and ENT specialties where tactile feedback guides tissue planes. Meanwhile, table-mounted rigs serve open spine and thoracic cases lasting several hours. Single-use instruments are expanding in trauma centers grappling with sterilization backlogs, and their growing uptake amplifies volume growth within the surgical retractors market.

Manufacturers are now releasing modular trays that combine clip-on blades with pivoting handles, allowing surgeons to switch between abdominal, orthopedic, and vascular modes within one system. Stryker’s 2025 Oculan platform, featuring Fly-Eye optics that disperse heat, exemplifies this convergence. Surgeons receive uniform lighting and consistent ergonomics, while sterile-processing teams handle a smaller instrument base. Over the forecast period, self-retaining and illuminated units will keep defining the competitive battleground, as their value proposition dovetails with hospital efficiency metrics and ASC turnover targets.

Note: Segment shares of all individual segments available upon report purchase

By Material: Stainless Steel Dominance Challenged by Polymer Innovation

Stainless steel retained 56.21% share of the surgical retractors market in 2025 thanks to durability, ease of sterilization, and surgeon familiarity. Yet high-performance polymers led by PEEK are charging ahead at 9.55% CAGR to 2031. Victrex’s medical-grade PEEK allows 70% weight reduction compared to steel while preserving torsional rigidity, lowering hand strain during prolonged spine exposures. Weight relief directly correlates with precision for fine dissection tasks, motivating neurosurgeons to switch. Polymers also permit integrated illumination channels and radiolucency for intra-operative imaging. Titanium keeps a niche in procedures needing absolute corrosion resistance, such as cardiovascular cases. Meanwhile, 3D-printed polymer retractors enable patient-specific curvature, particularly advantageous in pediatric orthopedics where anatomy varies widely.

Sterilization protocols are adapting to lower temperature cycles for polymer tools, further improving longevity and throughput. As providers calculate total cost of ownership, polymer’s extended life—despite higher upfront pricing—is winning tenders in Europe and Japan. With additive manufacturing centers coming online in India and Mexico, localized production will compress lead times and import duties, improving affordability. These shifts reinforce sustained double-digit expansion of polymer lines, though steel will remain the baseline in many public systems, ensuring a blended material mix across the surgical retractors market.

By Application: Neurological Procedures Lead Growth Momentum

Abdominal and general surgery continued to generate the highest absolute volume, holding 30.08% share of the surgical retractors market size in 2025. Laparoscopic cholecystectomies, hernia repairs, and bariatric cases remain routine, requiring diverse blade geometries. Nevertheless, neurological and spine procedures are the pace-setter, expanding at 9.92% CAGR through 2031 on the back of aging patients and robotic endoscope adoption. Endoscopic lumbar decompressions now rely on canoe-shaped polymer retractors that protect nerve roots while allowing irrigation. Intra-operative MRI compatibility drives demand for non-ferromagnetic frames, another factor favoring advanced polymers.

Orthopedic segments ride the wave of arthroplasty recovery, aided by backlog reduction initiatives. Cardiothoracic applications evolve alongside transcatheter valve innovations, where mini-thoracotomy access demands slim, illuminated arms. Obstetric and gynecologic surgery integrates low-profile self-retainers for laparoscopic hysterectomies, decreasing trocar counts and incision lengths. Plastic and reconstructive surgeons value fine ratcheting mechanisms for scar-minimizing incisions, supporting specialty-driven product lines. Overall, application-tailored engineering remains a core differentiation lever, cementing multi-segment penetration for the surgical retractors market amid shifting procedural mixes.

Note: Segment shares of all individual segments available upon report purchase

By End User: ASCs Challenge Hospital Dominance

Hospitals accounted for 60.98% revenue in 2025, reflecting their breadth of complex surgeries and extensive instrument inventories. However, ASCs post an 8.12% CAGR as payers mandate site-of-service shifts for cost containment. Facility managers in ASCs demand compact, multi-use retractor kits that support orthopedic, ophthalmic, and general cases in rapid succession. They lean toward single-use illuminated models to bypass reprocessing queues, a pattern that boosts order frequency. Specialty clinics maintain stable demand aligned with ENT and cosmetic procedures but lack the volume surge seen in ASC chains.

GPOs negotiate umbrella contracts covering both hospitals and affiliated ASCs, pushing manufacturers to standardize SKUs across care settings. Vendors that supply universal handles accepting steel and polymer blades gain favor because they lower per-case spend. Training modules now accompany shipments, shortening onboarding time for traveling surgeons. Collectively, these trends redistribute purchasing power without dislodging hospitals from the top position, yet they propel diverse growth paths within the surgical retractors market.

Geography Analysis

North America preserved leadership with 39.28% of 2025 revenue, leveraging high procedural counts, rapid backlog recovery, and enduring preference for premium systems. The opening of a new elective hub at Southmead Hospital anticipates 6,500 extra annual surgeries and mirrors similar capacities across US states. Reimbursement models reward minimally invasive approaches, prompting hospitals to invest in illuminated self-retaining frames that reduce operative time. Robust ASC pipelines in Texas, Florida, and Ontario further multiply unit demand. Surgeons embracing robotics also spur orders for retractor arms compatible with console workflows, enriching the region’s technology mix and reinforcing the primacy of the surgical retractors market in North America.

Asia-Pacific emerges as the fastest mover with a 8.95% CAGR to 2031. Japan’s Smart-Hospital initiative provides subsidies for polymer-based devices that integrate optical fibers, accelerating high-spec adoption. India’s expansion of insurance schemes under Ayushman Bharat drives elective procedure growth in tier-two cities, where ASCs dominate and favor cost-efficient yet durable retractors. Regional suppliers establish local molding sites, curbing import costs and enhancing responsiveness, thereby propelling the surgical retractors market forward.

Europe shows steady mid-single-digit growth anchored in aging demographics and stringent quality regulations. Germany’s DRG reform incentivizes outpatient hip replacements, which rely on self-retaining retractors to limit incision size. France’s funding for infection-free theatres boosts single-use instrument uptake. Meanwhile, Middle East & Africa and South America register rising adoption of versatile kits suited for mixed caseloads in resource-constrained hospitals. Gulf states allocate oil windfalls to surgical robotics, indirectly upping demand for premium retractor accessories. In Brazil, public-private surgery centers hybridize hospital and ASC models, creating fresh distribution channels. Collectively, diverse regional dynamics buttress the global expansion of the surgical retractors market.

Competitive Landscape

Market Concentration

The surgical retractors market sits in a moderately concentrated state where the top five suppliers hold major share of market. Johnson & Johnson’s Ethicon, Medtronic, Stryker, and B. Braun anchor the upper tier with deep R&D pipelines and global service networks. Stryker’s purchase of vascular specialist Inari Medical in 2024 underscores a strategy of solution bundling across entire episodes of care. Medtronic’s acquisition of Fortimedix feeds its robotic program, ensuring seamless retractor-arm linkages with laparoscopic towers.

Mid-sized contenders Integra LifeSciences, June Medical, and CooperSurgical differentiate through niche innovations such as graphene-coated blades and ring retractors for microsurgery. CooperSurgical’s 2024 acquisition of obp Surgical added battery-integrated LED handles, expanding its outpatient portfolio. Start-ups exploit 3D printing to deliver patient-specific retractors within 48 hours, gaining traction in pediatric spine centers. Cross-licensing agreements between polymer suppliers and device makers accelerate time-to-market for ergonomic designs. Competitive intensity revolves around securing GPO contracts and building training ecosystems that lock surgeons into proprietary platforms.

Pricing strategies bifurcate: premium players bundle service, data analytics, and sterile-processing audits, whereas value brands market stripped-down stainless sets to price-sensitive institutions. Sustainability pledges such as recycled PEEK content are emerging differentiators, resonating with ESG-minded health systems in Europe. Over the forecast horizon, AI-enabled tension feedback and robotic docking compatibility will likely dictate share gains. The continual introduction of upgradeable illumination modules ensures recurring revenue, sustaining the long-term vitality of the surgical retractors market.

Surgical Retractors Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: JUNE MEDICAL, a globally recognized innovator in surgical device design, is thrilled to announce a landmark collaboration with Aspen Surgical, a premier supplier of medical solutions. This strategic partnership will focus on expanding U.S. market access to JUNE MEDICAL’s award-winning Galaxy II retractor system a game-changing advancement in self-retaining surgical retraction.

- August 2024: CooperCompanies announced a strategic expansion of its surgical capabilities through the acquisition of obp Surgical, a U.S.-based innovator in advanced medical devices. The acquisition was completed for approximately USD 100 million and marks a significant step forward in CooperSurgical’s commitment to enhancing surgical efficiency and innovation.

Table of Contents for Surgical Retractors Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rapid Rise in Elective & Trauma Surgeries Post-COVID backlogs

- 4.2.2Ageing Population Fuelling Orthopaedic & Cardiovascular Procedures

- 4.2.3Expansion of Ambulatory Surgical Centers (ASCs) Growth in Emerging Countries

- 4.2.4Adoption of Single-Use Illuminated Retractors

- 4.2.5Emergence of AI-Guided Robotic Retractors

- 4.2.6Increasing Preference for Minimally Invasive Surgery (MIS)

- 4.3Market Restraints

- 4.3.1Price Pressure from Low-Cost Imports

- 4.3.2Steep Learning Curve for Advanced Systems

- 4.3.3Capital Budget Constraints in Hospitals Investment

- 4.3.4Sterilization and Reusability Concerns

- 4.4Technological Outlook

- 4.5Porter’s Five Forces

- 4.5.1Threat of New Entrants

- 4.5.2Bargaining Power of Buyers

- 4.5.3Bargaining Power of Suppliers

- 4.5.4Threat of Substitutes

- 4.5.5Competitive Rivalry

5. Market Size & Growth Forecasts (Value in USD)

- 5.1By Product Type

- 5.1.1Hand-Held

- 5.1.2Self-Retaining

- 5.1.3Table-Mounted

- 5.1.4Illuminated/Fiber-Optic

- 5.1.5Disposable/Single-Use

- 5.2By Material

- 5.2.1Stainless Steel

- 5.2.2Titanium

- 5.2.3High-Performance Polymers

- 5.3By Application

- 5.3.1Orthopaedic

- 5.3.2Abdominal/General

- 5.3.3Cardiothoracic

- 5.3.4Obstetric & Gynaecological

- 5.3.5Neurological & Spine

- 5.3.6Plastic & Reconstructive

- 5.4By End User

- 5.4.1Hospitals

- 5.4.2Ambulatory Surgical Centres

- 5.4.3Specialty Clinics

- 5.5By Geography

- 5.5.1North America

- 5.5.1.1United States

- 5.5.1.2Canada

- 5.5.1.3Mexico

- 5.5.2Europe

- 5.5.2.1Germany

- 5.5.2.2United Kingdom

- 5.5.2.3France

- 5.5.2.4Italy

- 5.5.2.5Spain

- 5.5.2.6Rest of Europe

- 5.5.3Asia-Pacific

- 5.5.3.1China

- 5.5.3.2Japan

- 5.5.3.3India

- 5.5.3.4Australia

- 5.5.3.5South Korea

- 5.5.3.6Rest of Asia-Pacific

- 5.5.4Middle East & Africa

- 5.5.4.1GCC

- 5.5.4.2South Africa

- 5.5.4.3Rest of Middle East & Africa

- 5.5.5South America

- 5.5.5.1Brazil

- 5.5.5.2Argentina

- 5.5.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1Johnson & Johnson (Ethicon)

- 6.3.2Medtronic

- 6.3.3B. Braun Melsungen AG

- 6.3.4Becton, Dickinson and Company

- 6.3.5Teleflex Incorporated

- 6.3.6Stryker Corporation

- 6.3.7Applied Medical Resources

- 6.3.8Cook Group Incorporated

- 6.3.9Medline Industries

- 6.3.10Invuity (Stryker)

- 6.3.11Novo Surgical

- 6.3.12Thompson Surgical

- 6.3.13OBP Medical

- 6.3.14Safe Orthopaedics

- 6.3.15BR Surgical

- 6.3.16Arthrex

- 6.3.17MicroSurgical Technology

- 6.3.18Möller Medical

- 6.3.19Henry Schein (Miltex)

- 6.3.20Jiangsu Tonghui Medical

- 6.3.21Purple Surgical

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-Need Assessment

Global Surgical Retractors Market Report Scope

As per the scope of the report, surgical retractors are the instruments used during surgical procedures to separate and hold the edges of a surgical incision or wound. These are also called surgical distractors. As per the scope of the report, surgical retractors are handheld or self-retained and used for many surgical procedures.

The surgical retractors market is segmented by type (handheld and self-retaining), application (orthopedic retractors, abdominal retractors, cardiothoracic retractors, obstetric or gynecological retractors, and others), end user (hospitals and ambulatory surgical centers), and geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report also covers the estimated market sizes and trends for 17 countries across major global regions. The report offers the value (USD million) for the above segments.