Hernia Repair Devices And Procedures Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 7.06 Billion |

| Market Size (2031) | USD 8.71 Billion |

| Growth Rate (2026 - 2031) | 4.29% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hernia Repair Devices And Procedures Market Analysis by Mordor Intelligence

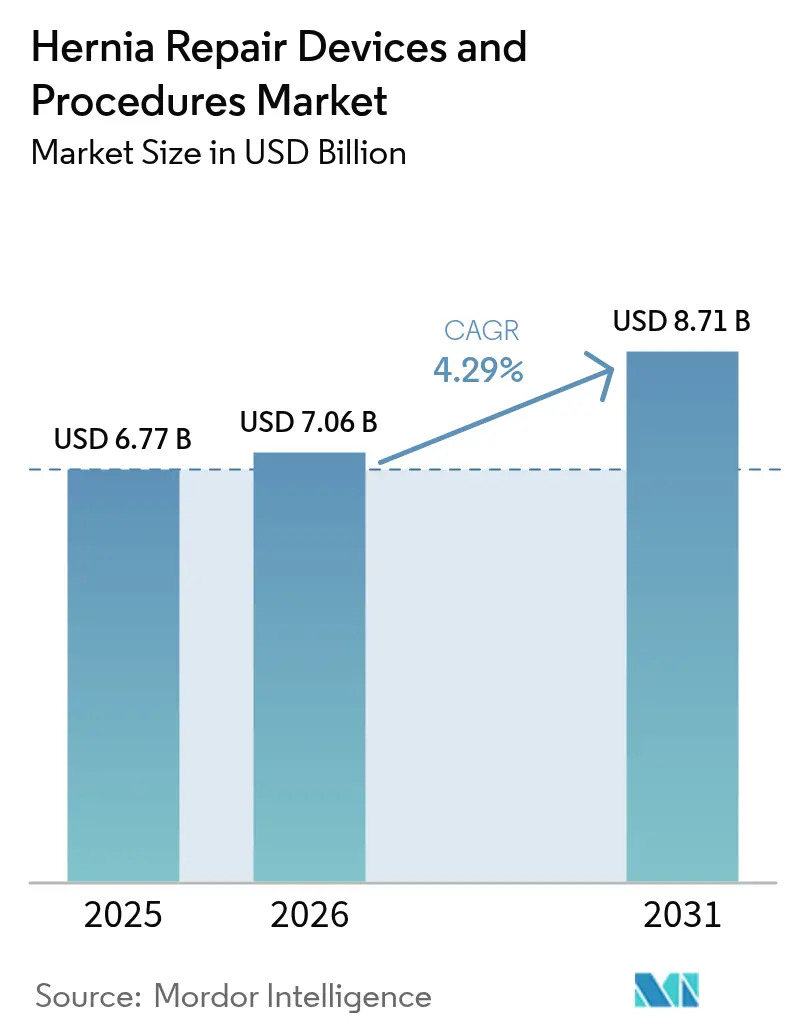

The hernia repair devices and procedures market size was valued at USD 6.77 billion in 2025 and estimated to grow from USD 7.06 billion in 2026 to reach USD 8.71 billion by 2031, at a CAGR of 4.29% during the forecast period (2026-2031). Stable growth is taking shape as the field matures, yet continuous device innovation, wider ambulatory surgery center (ASC) use and robotic adoption keep procedural volumes and average selling prices on an upward slope. Demand also remains anchored to a sizeable clinical need: more than 6.75 million patients lived with hernia in 2021, and incidence is trending higher in aging, increasingly obese populations. Robotic inguinal repair penetration jumped from 0.8% to 24.2% in just six years, while ventral repairs moved from 0.02% to 17.0%, underscoring a decisive technological shift. Synthetic polypropylene mesh keeps its cost-driven lead, but biologic and biosynthetic alternatives are scaling quickly as centres seek lower chronic-pain and infection rates. Litigation headwinds have started to clear—BD’s USD 1 billion settlement in October 2024 removed a major overhang—enabling manufacturers to reinvest in next-generation materials, fixation technologies and surgical robotics.

Key Report Takeaways

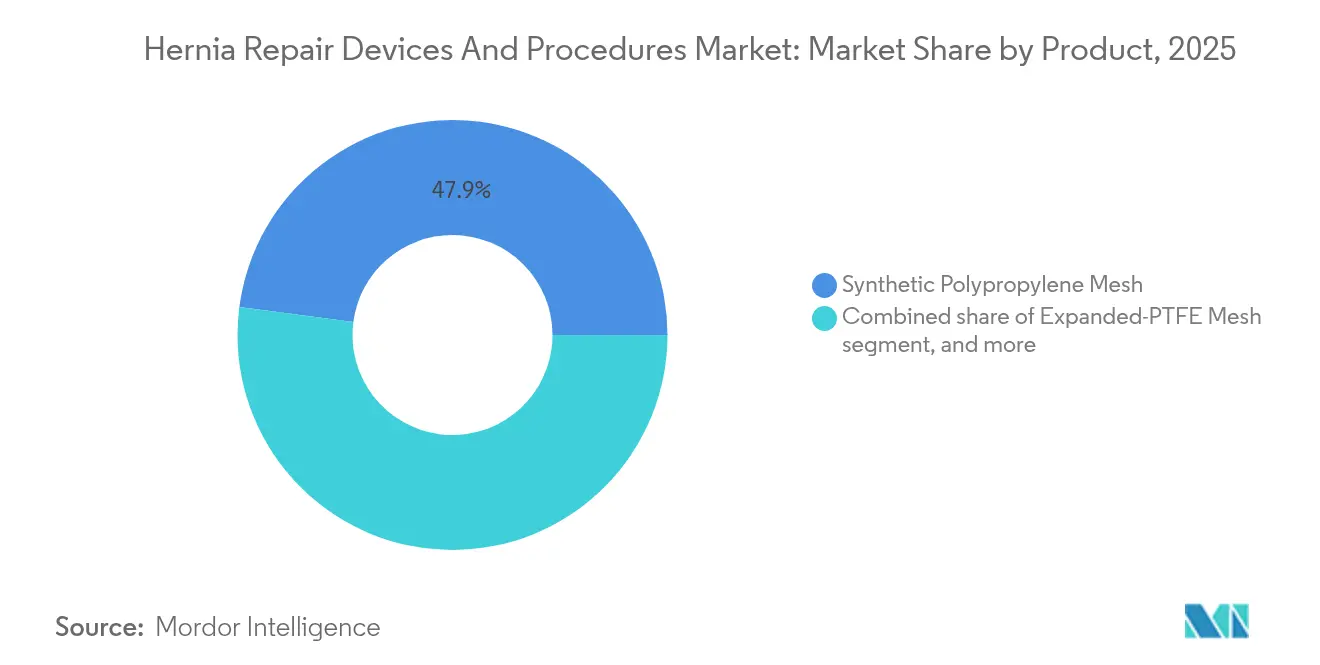

- By product, synthetic polypropylene mesh led with 47.92% revenue share in 2025; biologic and biosynthetic mesh is projected to expand at a 6.23% CAGR through 2031.

- By procedure, open tension-free repair held 42.10% of the hernia repair devices and procedures market share in 2025, while robotic-assisted laparoscopic repair is pacing the field at a 6.55% CAGR to 2031.

- By hernia type, inguinal repairs captured 65.75% share in 2025; incisional and ventral repairs are the fastest-growing at 6.57% CAGR.

- By material, synthetic options accounted for 70.55% share in 2025; biologic materials are rising at a 6.90% CAGR.

- By end user, hospitals commanded 60.70% share in 2025, whereas ASCs are expanding at a 7.72% CAGR on cost and convenience advantages.

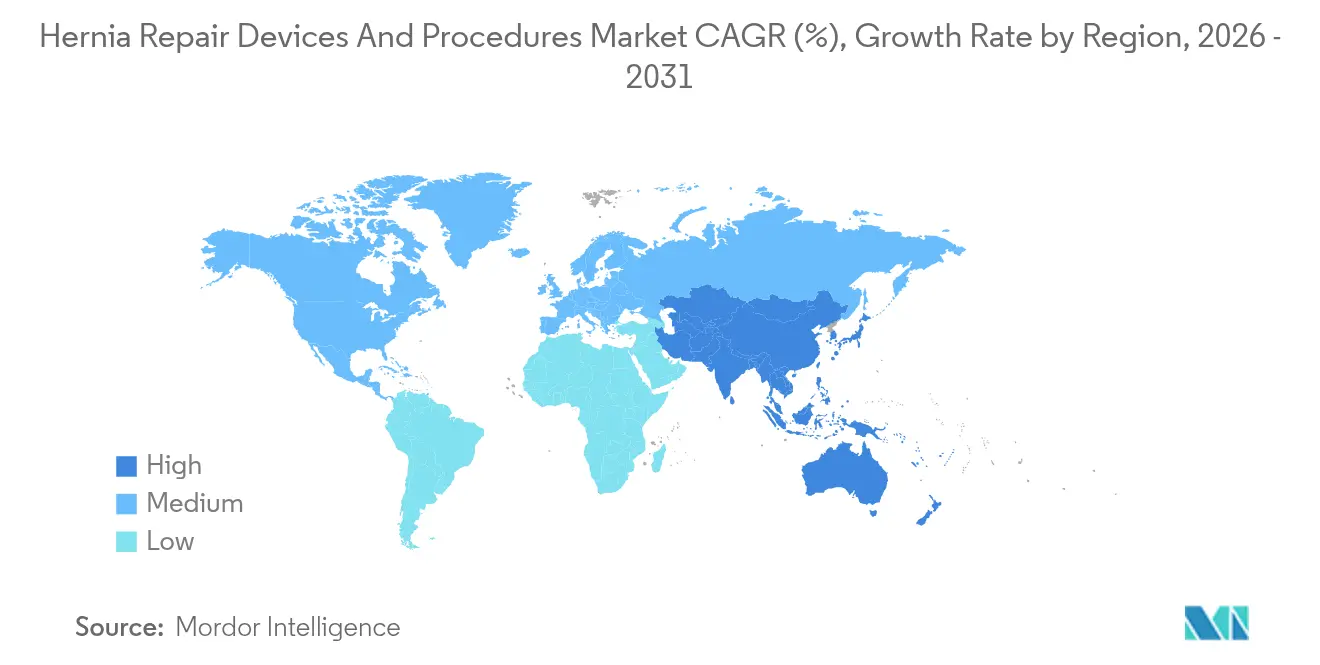

- By geography, North America maintained 39.98% share in 2025; Asia-Pacific is advancing at a 5.59% CAGR, lifted by infrastructure upgrades and rising surgical volumes.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Hernia Repair Devices And Procedures Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global surgical hernia burden | +1.2% | Worldwide; highest in aging markets | Long term (≥4years) |

| Advancements in minimally invasive repair technologies | +0.8% | North America & Europe leading; Asia-Pacific scaling | Medium term (2-4years) |

| Expanding insurance coverage for elective hernia surgeries | +0.6% | United States, Canada, Western Europe | Medium term (2-4years) |

| Growing adoption of composite and lightweight meshes | +0.4% | Global; first in premium healthcare systems | Short term (≤2years) |

| Surge in ambulatory surgery center procedures | +0.7% | United States; spreading to Europe | Medium term (2-4years) |

| Integration of robotics and AI for enhanced surgical outcomes | +0.5% | High-income economies | Long term (≥4years) |

| Source: Mordor Intelligence | |||

Rising Global Surgical Hernia Burden

Worldwide hernia incidence is climbing, with analysts projecting a 19.7% increase in new cases by 2050 as populations age and obesity rates rise. Adults older than 45 now account for most new diagnoses, and a male-to-female ratio of roughly 7:1 concentrates demand among men. In low- and middle-income nations such as India and China, procedural backlogs persist, positioning these regions as sizeable untapped volumes once surgical capacity expands. The sheer epidemiologic weight supplies the hernia repair devices and procedures market with steady baseline growth.

Advancements In Minimally Invasive Repair Technologies

Robotic systems and improved laparoscopic instrumentation deliver smaller incisions, less postoperative pain and faster return to work. Real-world data showed median console times of 37 minutes for unilateral robotic repairs and quick learning curves among early adopters. Although capital expense remains high, payer coverage is broadening and AI-guided planning is expected to shorten training cycles. Premium mesh designs compatible with robotic delivery also command higher average selling prices, supporting revenue gains even where case volumes plateau.

Expanding Insurance Coverage For Elective Hernia Surgeries

Medicare introduced a cost measure specific to hernia repair in its 2024 Merit-based Incentive Payment System, covering more than 1 million annual procedures at average costs of USD 2,000-2,500. At the same time, 2023 CPT code revisions improved billing accuracy, and private insurers have started reimbursing robotic techniques when evidence shows fewer readmissions[1]American College of Surgeons, “2023 CPT Code Revisions for Hernia,” facs.org. Reimbursement stability incentivises surgeons to adopt premium technologies, feeding sustained equipment and mesh turnover.

Growing Adoption Of Composite And Lightweight Meshes

Poly-4-hydroxybutyrate, ePTFE-polypropylene hybrids and fully resorbable biosynthetics promise lower chronic pain and infection rates. BD’s Phasix mesh posts tensile strength three times greater than native tissue yet absorbs in 12-18 months. Gore’s SYNECOR provides 2.5x stronger repair and under 1% recurrence, underpinning price premiums. Surgeons treating obese or contaminated fields increasingly reserve conventional heavyweight polypropylene for cost-sensitive cases.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of biologic and biosynthetic meshes | -0.9% | Global; acute in price-sensitive markets | Medium term (2-4 years) |

| Product recalls and litigation over mesh complications | -1.1% | North America & Europe | Short term (≤ 2 years) |

| Shortage of skilled laparoscopic and robotic surgeons | -0.7% | Emerging and low-volume markets | Long term (≥ 4 years) |

| Procurement delays due to capital budget constraints in hospitals | -0.4% | Public and rural hospitals worldwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cost Of Biologic And Biosynthetic Meshes

Biologic patches derived from porcine dermis or bovine pericardium can cost 5-10 times more than polypropylene, limiting uptake where payer budgets are tighter. Even biosynthetics such as Gore BIO-A run well above heavyweight mesh, and extended operating-room time adds further expense. Hospitals in emerging markets therefore default to suture-only or basic polypropylene techniques, tempering global adoption curves.

Product Recalls And Litigation Over Mesh Complications

More than 86,000 adverse-event reports filed since 2019 prompted the FDA to release draft labelling guidance in June 2025[2]U.S. FDA, “Draft Guidance for Hernia Surgical Mesh,” Federal Register, federalregister.gov. While BD’s USD 1 billion settlement resolved 38,000 lawsuits, pending cases against smaller suppliers create caution among surgeons and procurement teams, pushing some facilities back to established, lower-risk products. Compliance costs and longer trial timelines weigh on new-product ROI in the near term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Synthetic Mesh Dominance Faces Biologic Challenge

Synthetic polypropylene commanded 47.92% of revenue in 2025, underscoring its entrenched clinical track record and budget-friendly pricing. The hernia repair devices and procedures market size for synthetic mesh equated to nearly half of total industry sales last year. Lightweight, large-pore designs are helping retain share by reducing postoperative pain. Biologic and biosynthetic alternatives hold smaller volume now but are climbing at 6.23% CAGR as infection-prone ventral cases drive surgeons toward absorbable or hybrid constructs.

The fixation sub-segment is modernising as well. TELA Bio’s LIQUIFIX, the first FDA-cleared liquid adhesive for internal hernia use, is gaining traction for its uniform distribution and reduced tack trauma. Antimicrobial coatings, especially chlorhexidine films, are also differentiating suppliers by cutting infection risk versus gentamicin-impregnated competitors. Suppliers that marry mesh, fixation and adjunct tools into single-vendor kits strengthen their stickiness with purchasing committees.

By Procedure: Robotic Revolution Accelerates Despite Open Surgery Persistence

Open tension-free Lichtenstein still represented 42.10% of 2025 procedures, a testament to surgeon familiarity and low consumable cost. For many straightforward inguinal cases, hospitals retain this approach to maximise throughput and minimise capital spend. Yet robotic-assisted laparoscopic repair is advancing at 6.55% CAGR, winning converts for complex bilateral and ventral presentations where ergonomics and 3-D visualisation pay off.

The hernia repair devices and procedures market share for robotic systems continues to rise as ASC investment grows and vendors roll out lower-priced four-arm models. Early recurrence spikes reported in Nordic registries appear tied to learning curves rather than intrinsic technique flaws. AI-enhanced vision is expected to flatten that curve, broadening the surgeon pool and lifting disposable instrument volumes.

By Hernia Type: Inguinal Dominance Masks Ventral Growth Opportunity

Inguinal repairs generated 65.75% of 2025 volume, supported by a clear male disease bias and well-defined outpatient pathways. The hernia repair devices and procedures market size allocated to inguinal repairs will hold steady through 2031 even as other categories outpace growth. Incisional and ventral repairs, at a 6.57% CAGR, are rising on the back of higher abdominal surgery rates, obesity and better imaging that uncovers complex fascial defects earlier.

Advanced meshes that resist infection and reinforce large gaps are specifically designed for ventral cases, allowing suppliers to charge up to 3-times inguinal-mesh ASPs. Innovative approaches—such as posterior rectus sheath flaps for paraesophageal augmentation—show how technique evolution underpins demand for specialised materials.

By Material: Synthetic Leadership Challenged by Biologic Innovation

Synthetic fibres controlled 70.55% share in 2025 due to their favourable price-to-performance ratio and widespread surgeon familiarity. Yet biologic and hybrid biosynthetic meshes, advancing at 6.90% CAGR, are gaining ground in contaminated fields and high-risk patients. The hernia repair devices and procedures market share advantage of synthetics will narrow slightly as reimbursement accommodates proven infection-sparing benefits of premium alternatives.

Gore BIO-A, for example, demonstrated 83% intact repairs in complex ventral cases while costing under half of traditional porcine-based dermal patches. At the same time, platelet-rich fibrin barriers are moving toward clinical use, potentially improving synthetic-mesh compatibility and extending the practical life of cheaper implants.

By End User: Hospital Dominance Faces ASC Disruption

Hospitals remained the primary customer base with 60.70% share in 2025, largely because complex or redo repairs often need multidisciplinary support and overnight observation. Nonetheless, ASCs are growing at 7.72% CAGR as reimbursement parity improves and protocols enable same-day discharge even for bilateral laparoscopic cases.

More than 3,000 U.S. ASCs now list hernia repair as a core service, and firms such as Medtronic offer bundled “ASC-fit” robotic packages with lower capital outlays and pay-per-use instrument pricing. Specialty hernia centres—often physician-owned—are emerging as referral hubs, intensifying purchasing power and demanding integrated device ecosystems.

Geography Analysis

North America generated 39.98% of global revenue in 2025, supported by high procedure volumes, early technology uptake and broad insurance coverage. Medicare alone reimburses more than 1 million hernia repairs annually, translating to a USD 2.5 billion addressable spend for meshes, fixation and instruments. U.S. robotic penetration in inguinal repair hit 24.2% by 2019, and the FDA’s new labelling guidance is expected to standardise performance claims, smoothing future rollouts. Canada and Mexico add incremental growth through cross-border medical tourism and infrastructure upgrades.

Europe trails slightly but benefits from robust clinical registries that favour premium devices with long-term data. Germany, the United Kingdom and France are early adopters of lightweight and biosynthetic meshes, while Southern Europe is raising laparoscopic and robotic volumes to cut LOS and chronic pain. The 2025 European launch of TELA Bio’s OviTex Inguinal underpins distributor interest in solutions optimised for minimally invasive and robotic delivery. Nonetheless, reimbursement heterogeneity across 27 EU states requires suppliers to tailor value dossiers country by country.

Asia-Pacific is the fastest-growing geography, advancing at 5.59% CAGR through 2031. China and India each conduct more than 1 million repairs yearly, yet mesh usage remains uneven, creating white-space for economical synthetics and mid-tier biosynthetics. Japan’s mature payer system supports robotic adoption, while Australia and South Korea champion outpatient pathways. International OEMs increasingly partner with regional distributors to navigate varying regulatory timelines and local tender processes.

Regulatory Landscape

In the United States, hernia surgical mesh is regulated by the FDA primarily as a Class II device under 21 CFR 878.3300, which generally follows the 510(k) premarket notification pathway for new products and iterations. In June 2025, the FDA issued the draft guidance "Hernia Mesh, Package Labeling Recommendations" to standardize labeling content and support safer use, raising the weight of compliant claims, clearer instructions, and more uniform package information across suppliers.

In Europe, hernia meshes fall under the EU Medical Device Regulation (Regulation (EU) 2017/745), which is in force as of January 1, 2026. Long-term implantable surgical meshes are treated as high-risk devices (commonly Class III), which increases expectations for clinical and technical documentation. Harmonized standards coordinated through CEN and Cenelec shape conformity assessments, affecting how manufacturers plan evidence generation, update technical files, and manage multi-market submissions for mesh, fixation, and procedure-enabling device combinations.

Competitive Landscape

The hernia repair devices and procedures market features a core of diversified multinationals plus a cohort of focused innovators. BD, after settling the bulk of mesh lawsuits for USD 1 billion, is channelling capital toward fully absorbable platforms and antimicrobial designs. Medtronic is integrating its mesh portfolio with the Hugo RAS robot, targeting seamless instrument-mesh workflows that can lift procedure throughput. Johnson & Johnson’s Ethicon unit remains a volume leader, but the company is refreshing its lineup with energy devices compatible across open, laparoscopic and robotic modalities.

Specialists add competitive friction. TELA Bio grew revenue 26% in Q3 2024 by positioning biologic-reinforced OviTex as a cost-effective alternative to porcine dermis while securing CE-mark for robotic delivery. W. L. Gore leans on ePTFE and biosynthetic R&D to anchor premium ASPs. New entrants such as Absolutions are pursuing breakthrough status for novel closure systems that could slash operating time and seroma rates. Across the board, vendors that bundle mesh, fixation, robotics and analytics into end-to-end solutions are gaining favour with large hospital systems aiming to standardise supplies.

Hernia Repair Devices And Procedures Industry Leaders

Medtronic Plc

Johnson & Johnson (Ethicon)

Becton, Dickinson and Company

B. Braun SE

Cook Medical LLC

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Robotic-assisted hernia repair is moving beyond early-adopter centers and into broader general-surgery workflows. This creates openings for vendors that can bring robots, instruments, mesh designs, and fixation methods together into standardized procedure kits for hospitals and ASCs. A specific market signal came in June 2026, when Medtronic submitted additional 510(k) filings to expand its Hugo robotic-assisted surgery system into U.S. general surgery indications, including hernia, reinforcing a shift toward broader use in abdominal wall cases rather than niche complex procedures only.

On the implant side, demand is concentrating around differentiated synthetic and resorbable platforms aimed at lowering chronic pain, infection risk, and OR friction while staying within cost constraints. The FDA has continued clearing next-generation mesh configurations, including a May 2026 510(k) clearance for ProGrip Advanced self-gripping polypropylene mesh, which supports supplier strategies that reduce fixation steps and standardize outcomes. At the same time, FDA labeling scrutiny after the June 2025 draft guidance increases the value of high-quality clinical and post-market evidence packages, favoring manufacturers that can substantiate performance claims across open, laparoscopic, and robotic approaches.

Recent Industry Developments

- June 2026: Medtronic expanded its U.S. regulatory push in hernia by receiving FDA 510(k) clearance for ProGrip Advanced mesh and by submitting additional 510(k) filings to broaden Hugo robotic-assisted surgery system indications into general surgery, including hernia repair. Together, these actions strengthen the company's ability to pair procedure platforms with hernia-specific consumables, tightening integration between robotic workflows and mesh usage in routine cases.

- September 2025: Medtronic announced results from the Enable Hernia Repair clinical study supporting the safety and effectiveness of the Hugo robotic-assisted surgery system in inguinal and ventral hernia repair. The readout adds clinical backing that can support hospital committee approvals and training investments for robotic hernia programs, which in turn lifts demand for compatible instruments and premium meshes.

- April 2025: BD received FDA 510(k) clearance and commercially launched the Phasix ST Umbilical Hernia Patch, extending its absorbable P4HB-based platform into a specific defect-focused configuration. The launch reinforces competitive momentum in bioabsorbable and biosynthetic materials, where suppliers differentiate on handling, resorption profile, and complication-risk management rather than only price.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of devices used in hernia repair and the procedure-linked consumables that go with them, across open, laparoscopic, and robotic approaches, as recorded at the point of clinical use and purchasing.

Scope exclusions: We exclude general operating room capital equipment, non-hernia general surgery tools, and post-operative drugs used for pain control or infection management.

Segmentation Overview

- By Product

- Synthetic Polypropylene Mesh

- Expanded-PTFE Mesh

- Light-Weight Large-Pore Mesh

- Biologic/Biosynthetic Mesh

- Surgical & Endoscopic Instruments

- Fixation Devices (Tackers, Sutures, Glues)

- By Procedure

- Open Tension Repair

- Open Tension-Free (Lichtenstein) Repair

- Laparoscopic Intraperitoneal-Onlay Mesh (IPOM)

- Robotic-Assisted Laparoscopic Repair

- By Hernia Type

- Inguinal Hernia

- Incisional/Ventral Hernia

- Umbilical Hernia

- Femoral & Other Hernias

- By Material

- Synthetic

- Biologic

- Hybrid Biosynthetic

- By End User

- Hospitals

- Ambulatory Surgical Centres (ASCs)

- Specialty Hernia Clinics

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the initial market structure and to anchor the demand pool by country and care setting. We relied on public sources such as CDC and NIH publications, WHO health statistics, OECD health spending and procedure trend series, FDA device databases and safety communications, and clinical guideline groups that publish hernia management recommendations.

On the supply side, we reviewed company annual reports, investor presentations, and reputable press coverage to understand portfolio mix and route-to-market patterns. In addition, paid subscriptions for company financials and intelligence, patent databases, and an import-export shipment-level database were used selectively to cross-check product availability signals and directional pricing movement across regions. These examples are not exhaustive, and many other sources were also consulted for data collection, validation, and clarification during the study.

Primary Interviews and Surveys

Primary work was done through expert interviews and structured surveys with surgeons, procurement teams, distributors, and clinical staff who regularly handle hernia cases, so the inputs reflect procedure choices and purchase behavior at hospitals and ASCs. Since this is a global market, coverage was spread across major regions to confirm adoption of laparoscopic and robotic repair, mesh material preferences, and the practical impact of shifts toward ambulatory surgical centers.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 20% | APAC: 43% |

| Mid tier: 46% | Functional/Unit leaders: 23% | EMEA: 34% |

| Smaller Players: 22% | Managers: 57% | Americas: 23% |

Market-Sizing & Forecasting

Sizing starts from a top-down demand pool, where procedure incidence, hospital and ASC case mix, and access to minimally invasive surgery are used to reconstruct the annual count of hernia repairs by region. Once that base is in place, expected device and consumable use per case is applied, including mesh penetration, fixation choice, and the typical mix of synthetic versus biologic or biosynthetic materials. That unit usage is then converted to value using region-relevant pricing bands.

To corroborate totals, selective bottom-up approximations were used, such as sampled average selling price times estimated unit consumption for common mesh and fixation lines, along with channel checks on tender activity and distributor inventory movement. When bottom-up signals were incomplete for smaller countries, gap handling relied on peer-country analogs tied to procedure volumes, payer mix, and site-of-care share, followed by expert review.

Forecasts were built using scenario analysis supported by multivariate regression checks, so growth reflects the combined effect of minimally invasive adoption, robotic case share, procedure shifting toward ASCs, pricing normalization by material type, and litigation-related demand recovery patterns where relevant. Inputs were adjusted only after validation with primary respondents, especially when a country showed sharp year-to-year swings that did not match procedure or hospital activity signals.

Data Validation & Update Cycle

Outputs were validated through triangulation against independent signals, such as procedure volume direction, device approval and safety updates, and observed pricing bands across care settings. Variance checks were run at country and regional levels, and outliers were reviewed by an analyst before the model was finalized.

The draft is then reviewed in steps, with re-contact triggered when a key assumption moves beyond an expected range, like a sudden shift in laparoscopic share or fixation uptake. Reports are refreshed annually, with interim updates when material events occur, and a final fresh pass is completed before delivery so clients receive the latest updated view.

Mordor Intelligence's Hernia Repair Devices and Procedures Market Size Measured Against Other Published Estimates

Published market sizes for hernia repair often do not line up because the boundary of what is counted can change, and the year chosen for the starting point can be different. Differences also come from how procedure volumes are translated into device value, particularly when mesh type and fixation practice vary by region and care setting.

Procedure volumes by hernia type, the split of open versus laparoscopic versus robotic repairs, and observed mesh and fixation use per case are the main gap drivers in this market. Evidence from procedure mix checks and care-setting shifts is what ties Mordor Intelligence's estimate to a repeatable demand pool, rather than only scaling from a device category total.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 6.77 B (2025) | |

| Global Data Publisher A | USD 5.64 B (2025) | Uses a narrower device-only boundary in practice, and procedure-linked consumables and certain instrument categories can be treated inconsistently across regions, which pulls the total down. |

| Market Tracker B | USD 5.26 B (2024) | Starts from a different base year and leans more on reported device revenue bands, which can understate value when pricing is not normalized by mesh material mix and fixation choice by site of care. |

The spread in the table is mainly explained by scope cutoffs and how procedure activity is translated into device value at the point of use. By keeping the model tied to procedure mix, per-case utilization, and realistic price bands, the final number stays transparent and can be rechecked with the same inputs over time.

Key Questions Answered in the Report

What is the current size of the hernia repair devices and procedures market?

The market is valued at USD 7.06 billion in 2026 and is forecast to reach USD 8.71 billion by 2031.

Which product type leads the market?

Synthetic polypropylene mesh holds the top spot with a 47.92% revenue share as of 2025.

How fast are robotic hernia repairs growing?

Robotic-assisted laparoscopic repairs are expanding at a 6.55% CAGR through 2031, the quickest pace among procedure types.

Why are ambulatory surgery centers gaining share?

Medicare payment increases, same-day discharge protocols and lower facility fees are driving ASC volumes, supporting a 7.72% CAGR.

Which region is the fastest growing?

Asia-Pacific is advancing at a 5.59% CAGR thanks to infrastructure investment and rising surgical capacity in China, India and Japan.

What impact did BD’s litigation settlement have on the market?

The USD 1 billion settlement resolved most mesh lawsuits, reducing regulatory uncertainty and allowing BD and peers to refocus on product innovation.

Page last updated on: